ACCT6003 - Financial Accounting Processes: Chi Herbal Ltd Analysis

VerifiedAdded on 2023/06/13

|15

|2165

|103

Report

AI Summary

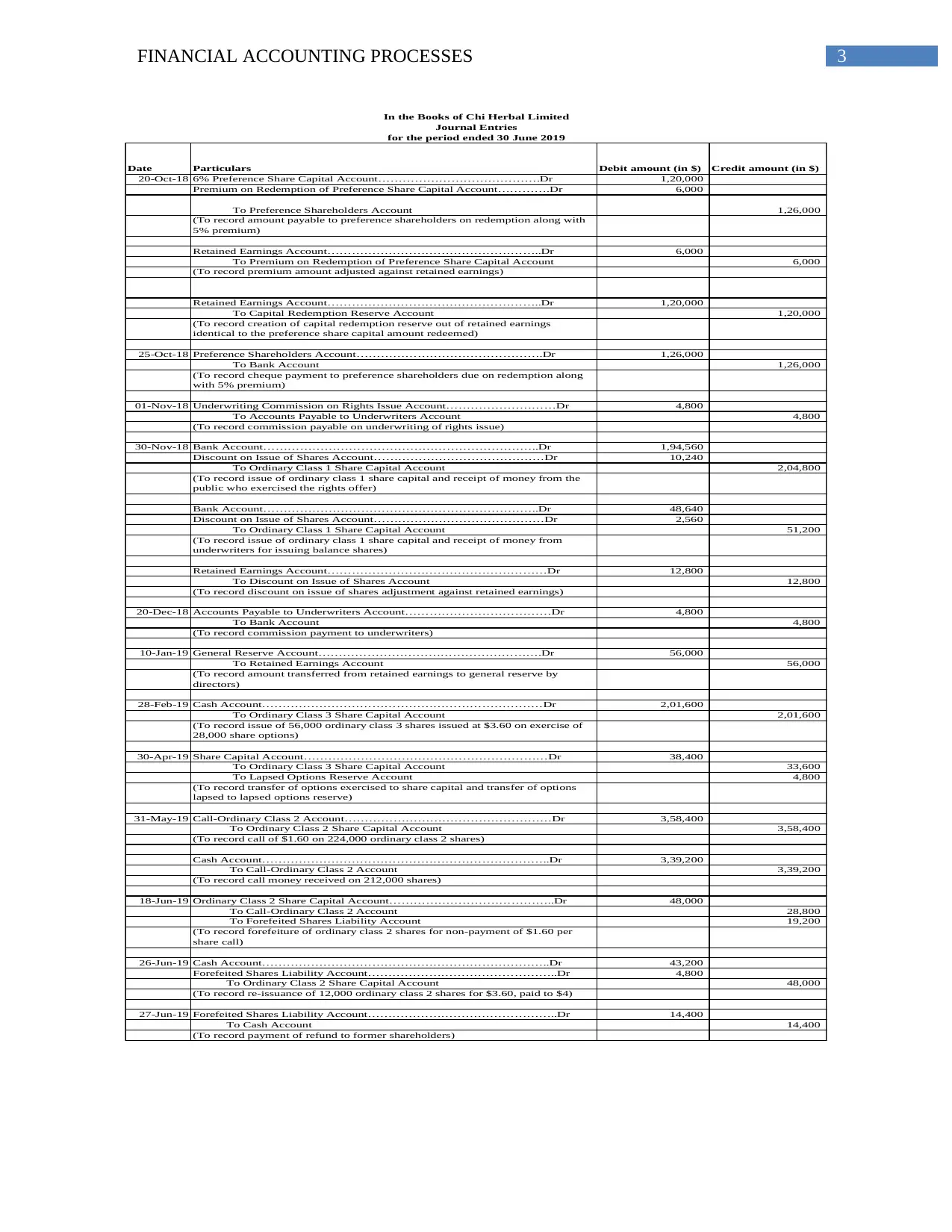

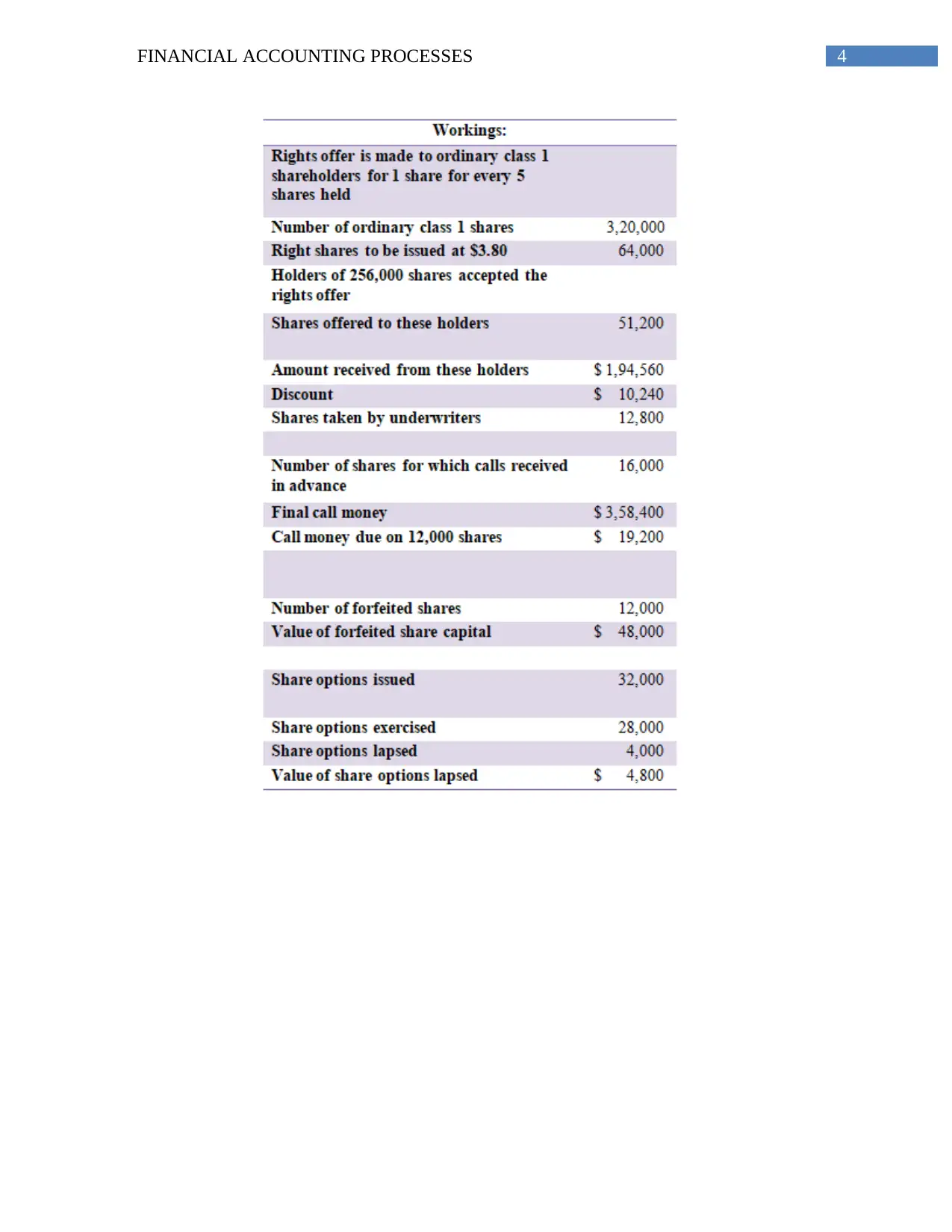

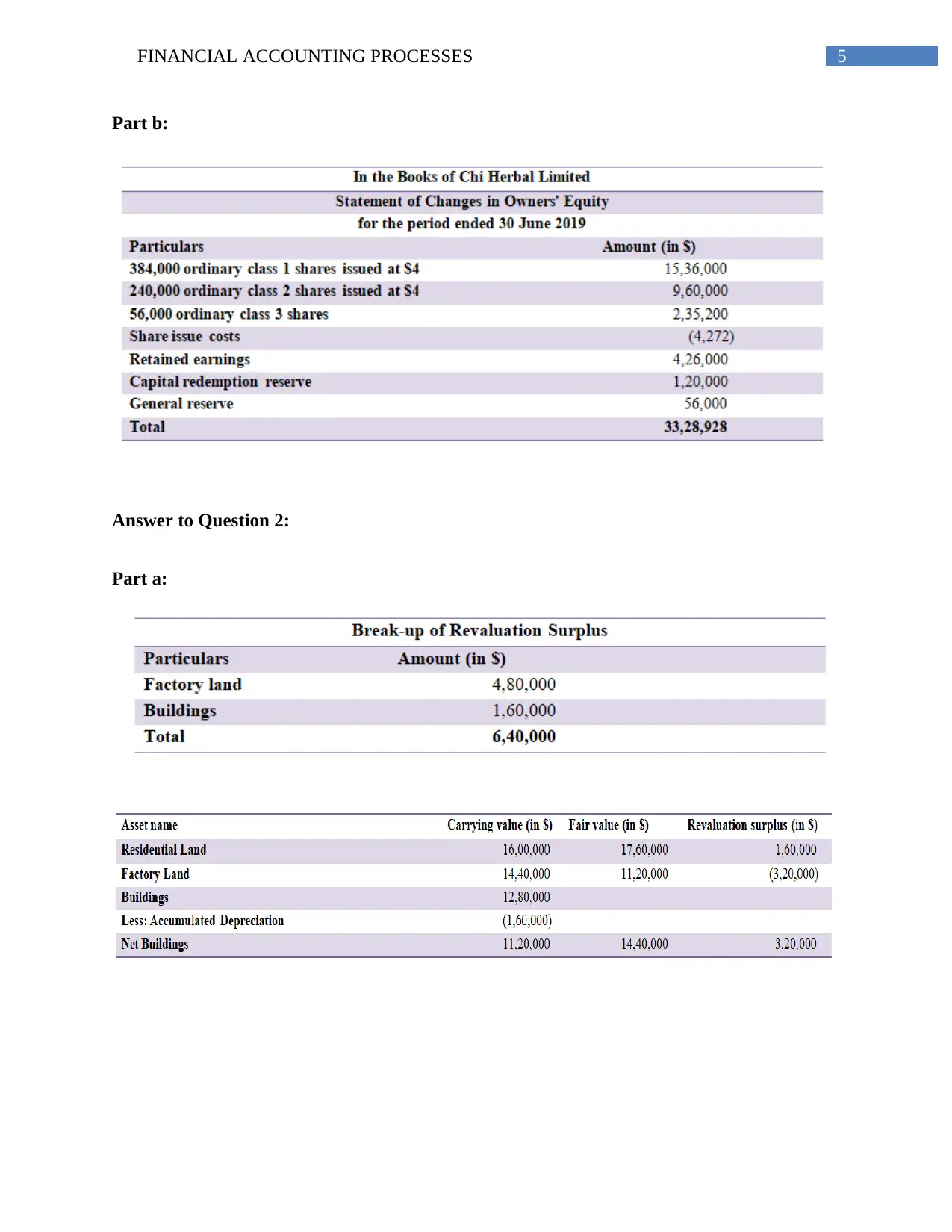

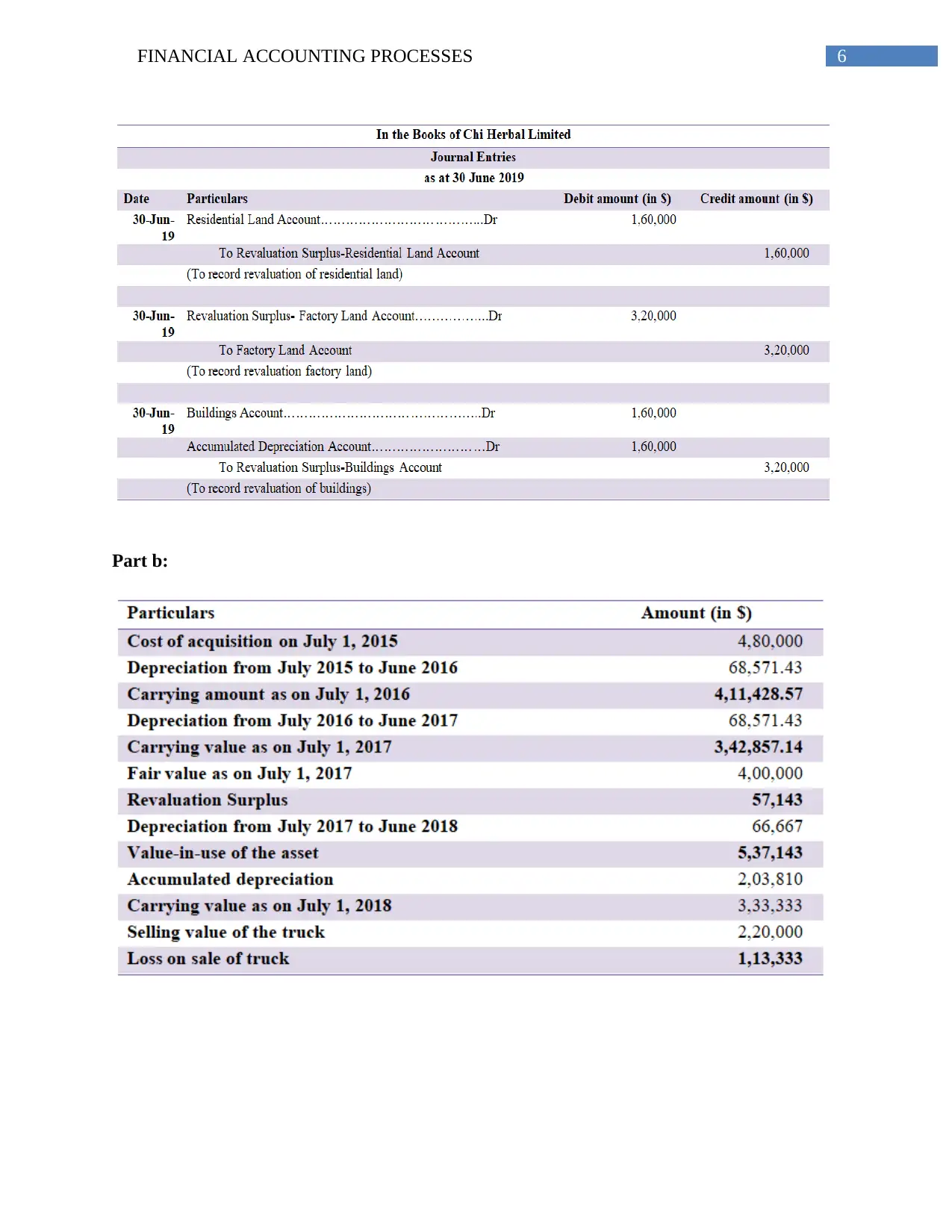

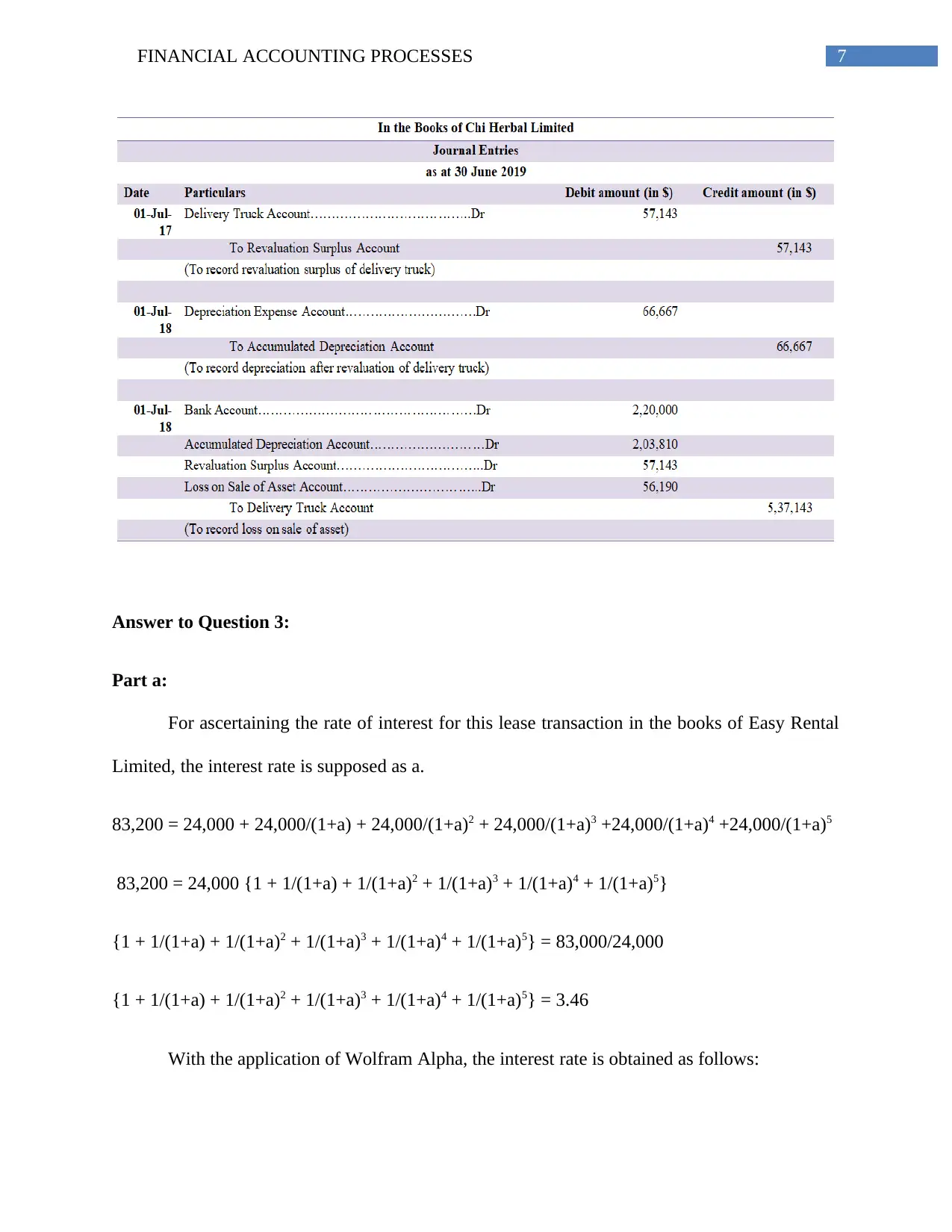

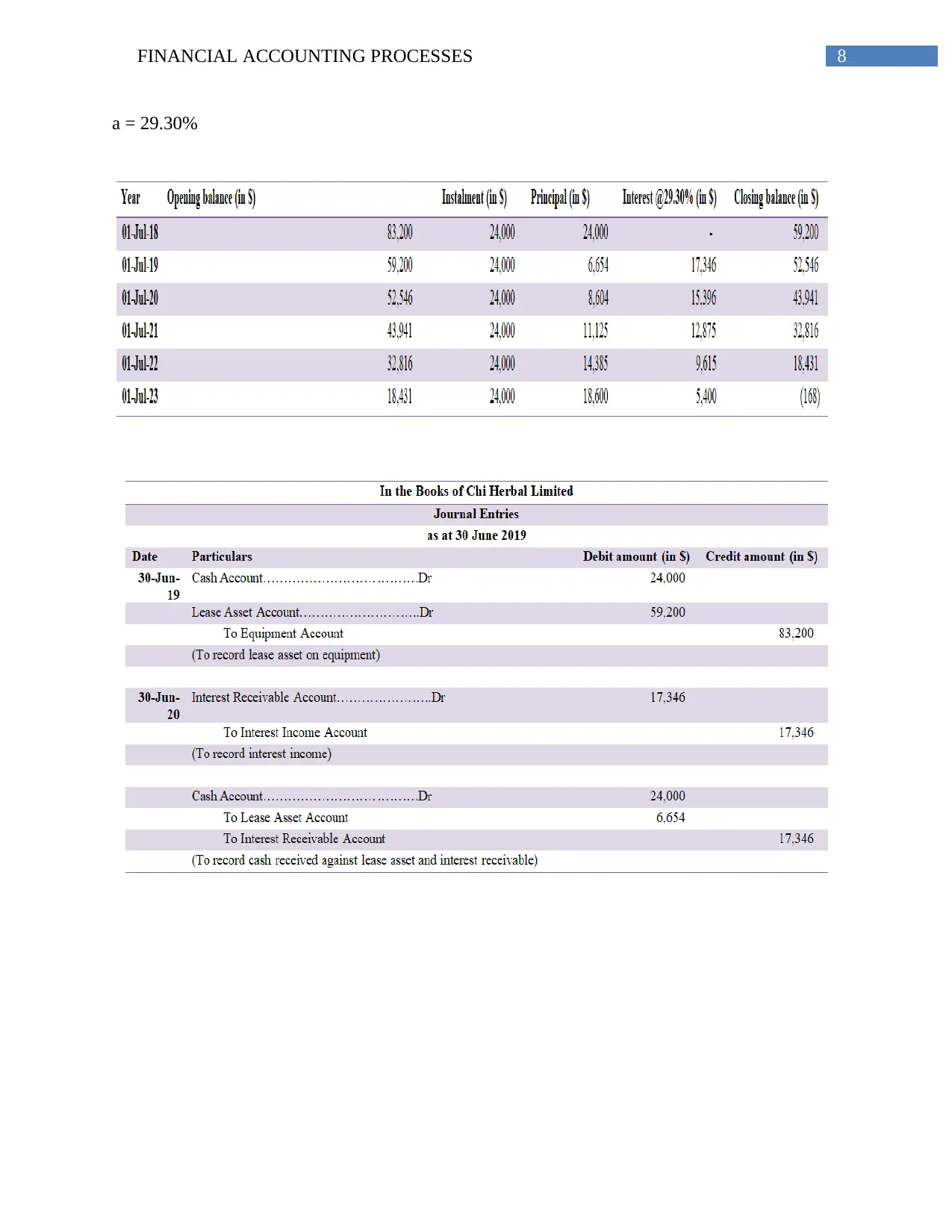

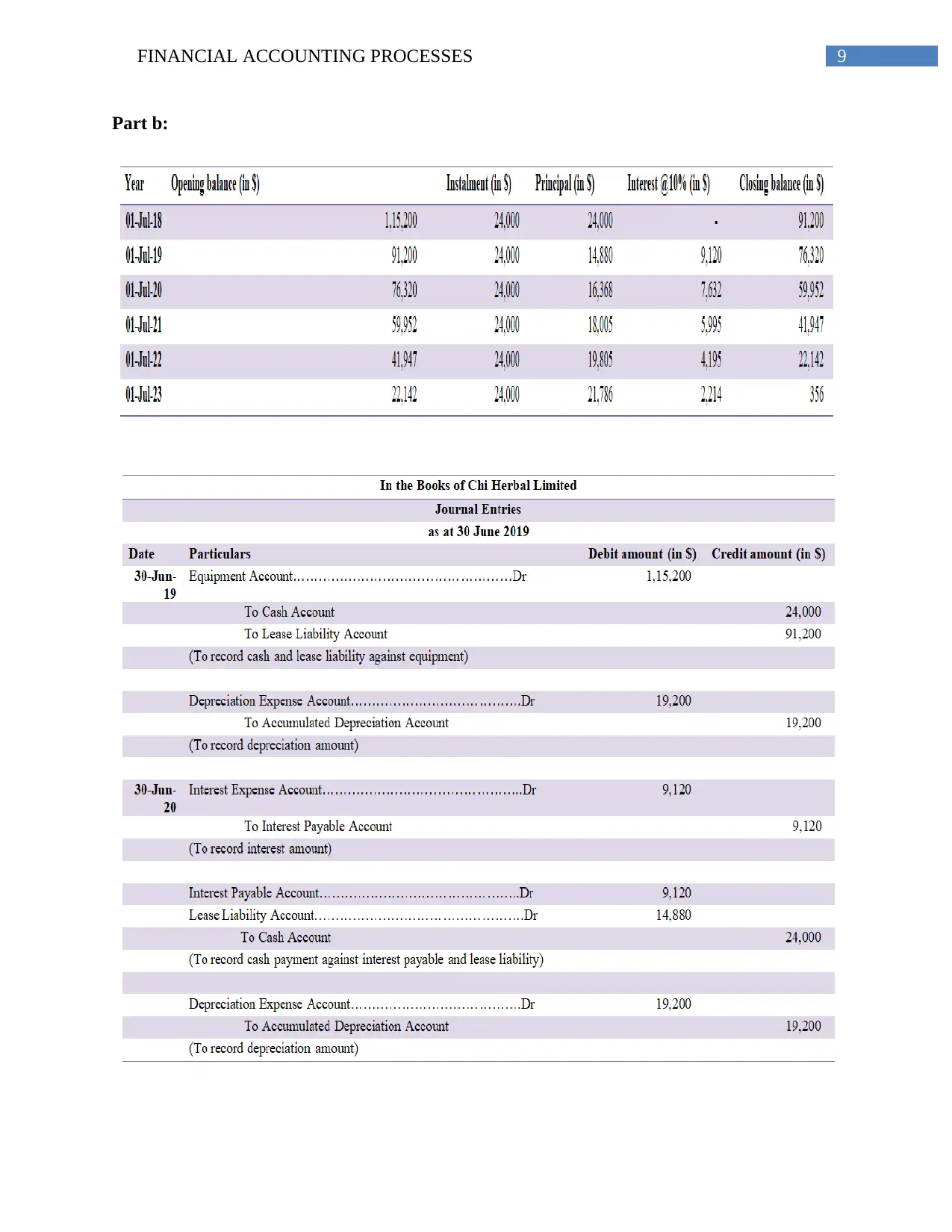

This report provides a detailed analysis of financial accounting processes, focusing on Chi Herbal Ltd. It includes journal entries for various transactions, such as preference share redemption, rights issue, and share options. The report also addresses lease accounting, determining the interest rate for a lease transaction and calculating the present value of lease payments. Furthermore, it examines the accounting treatment of intangible assets, specifically research and development costs, registration costs, and marketing expenses, in accordance with AASB 138. The report concludes with a recommendation for Chi Herbal Ltd regarding a competitor's offer, advising against acceptance due to potential financial losses. This comprehensive analysis offers valuable insights into the practical application of financial accounting principles.

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.