Financial Accounting Process Assignment: Journal Entries and Analysis

VerifiedAdded on 2021/10/27

|12

|1826

|92

Homework Assignment

AI Summary

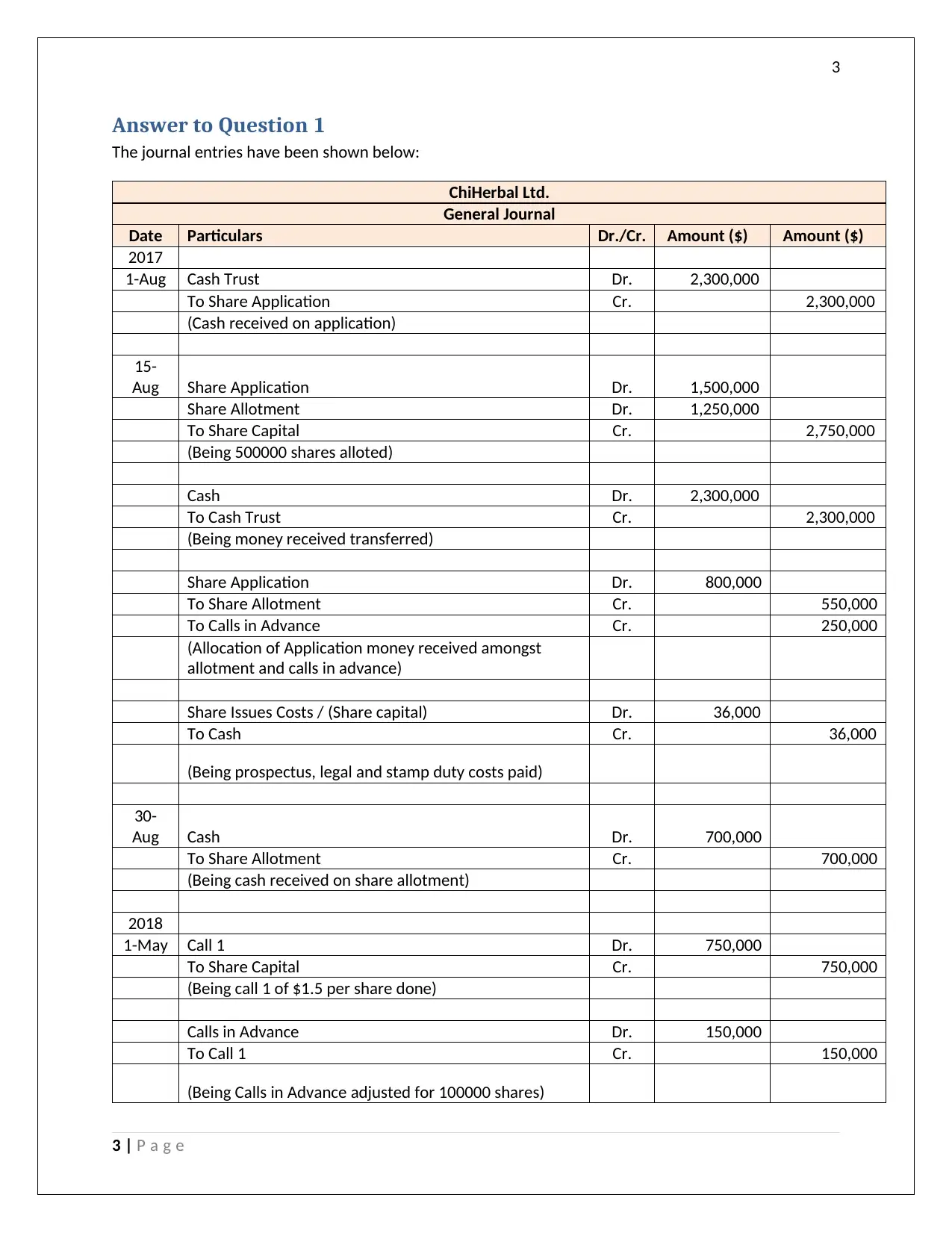

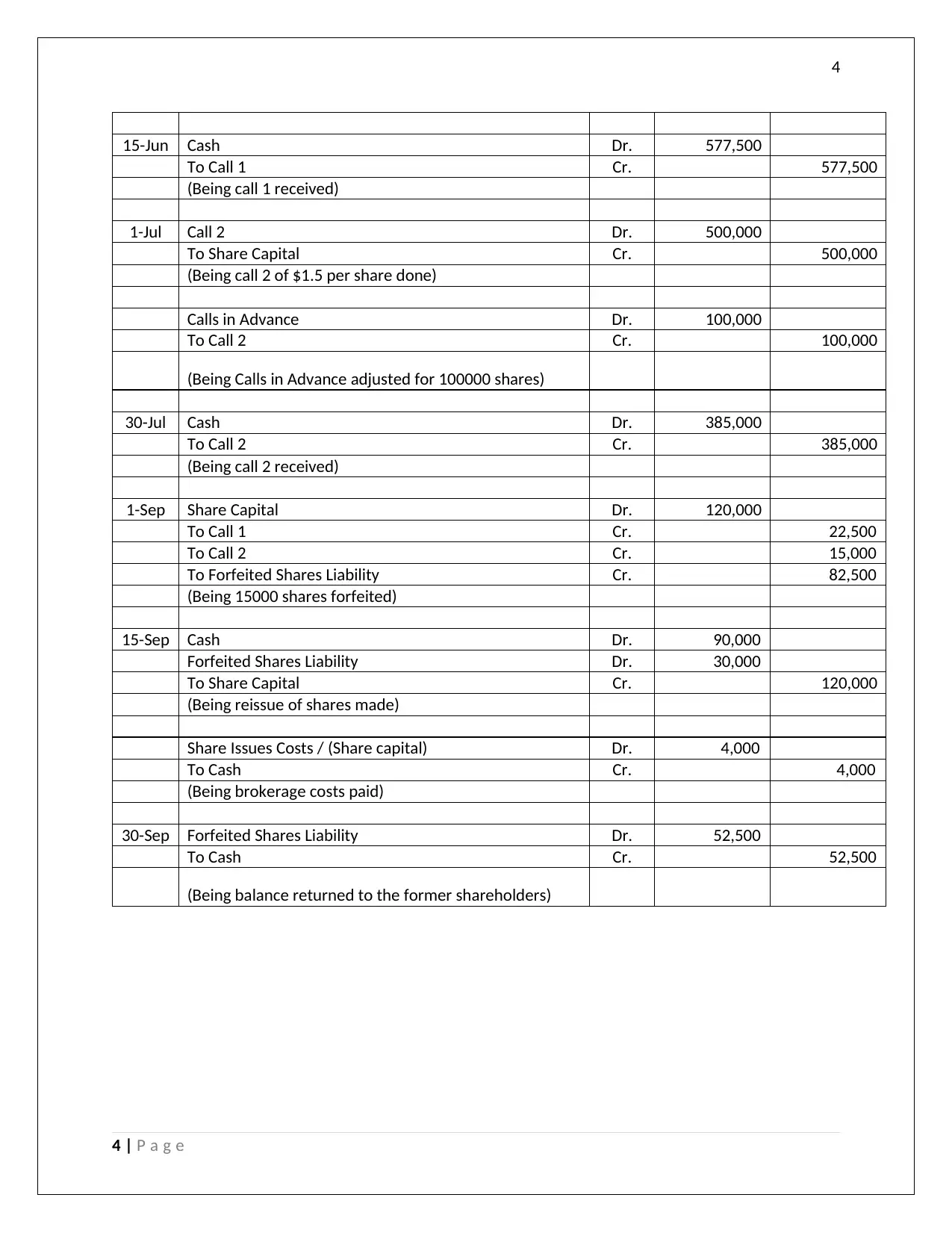

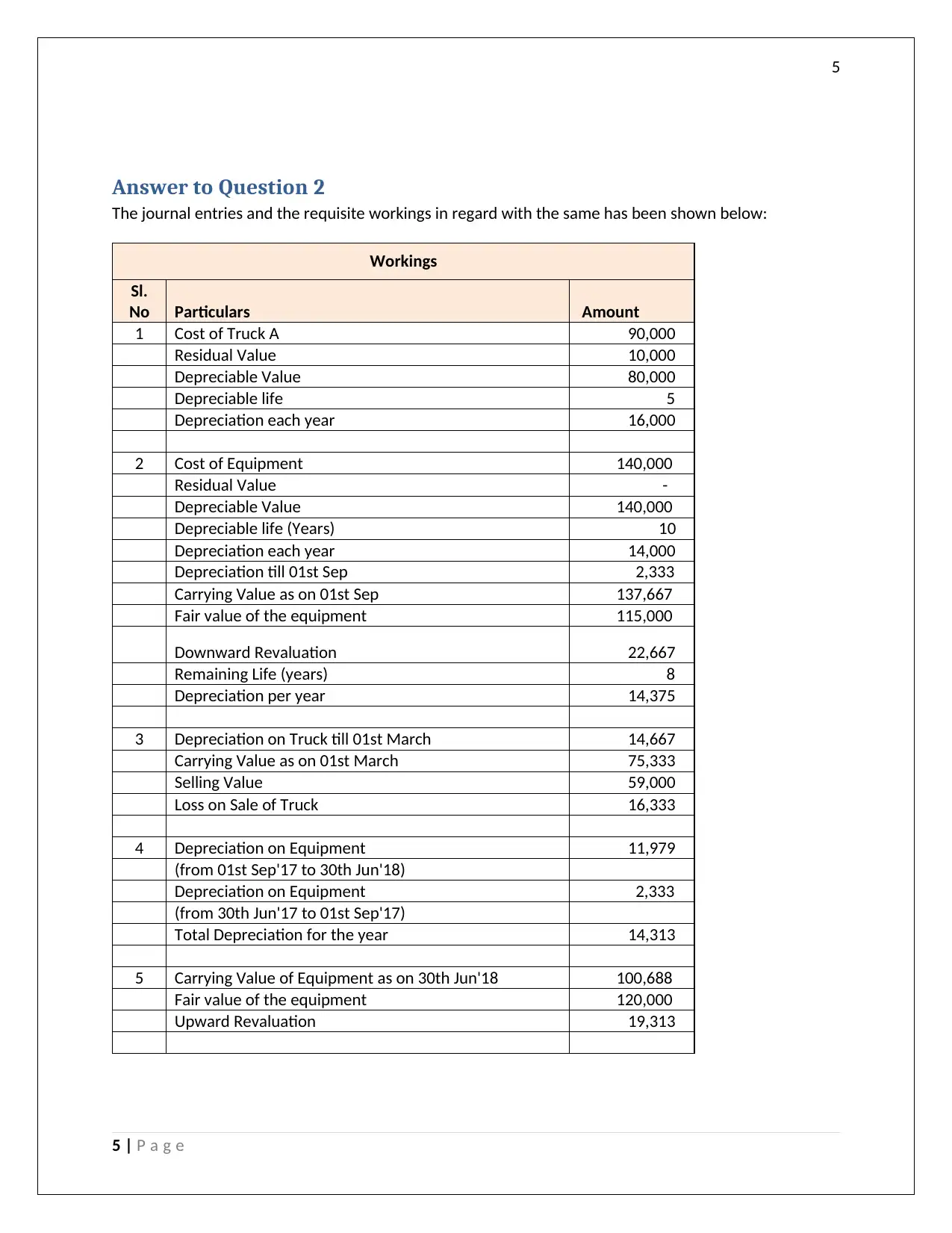

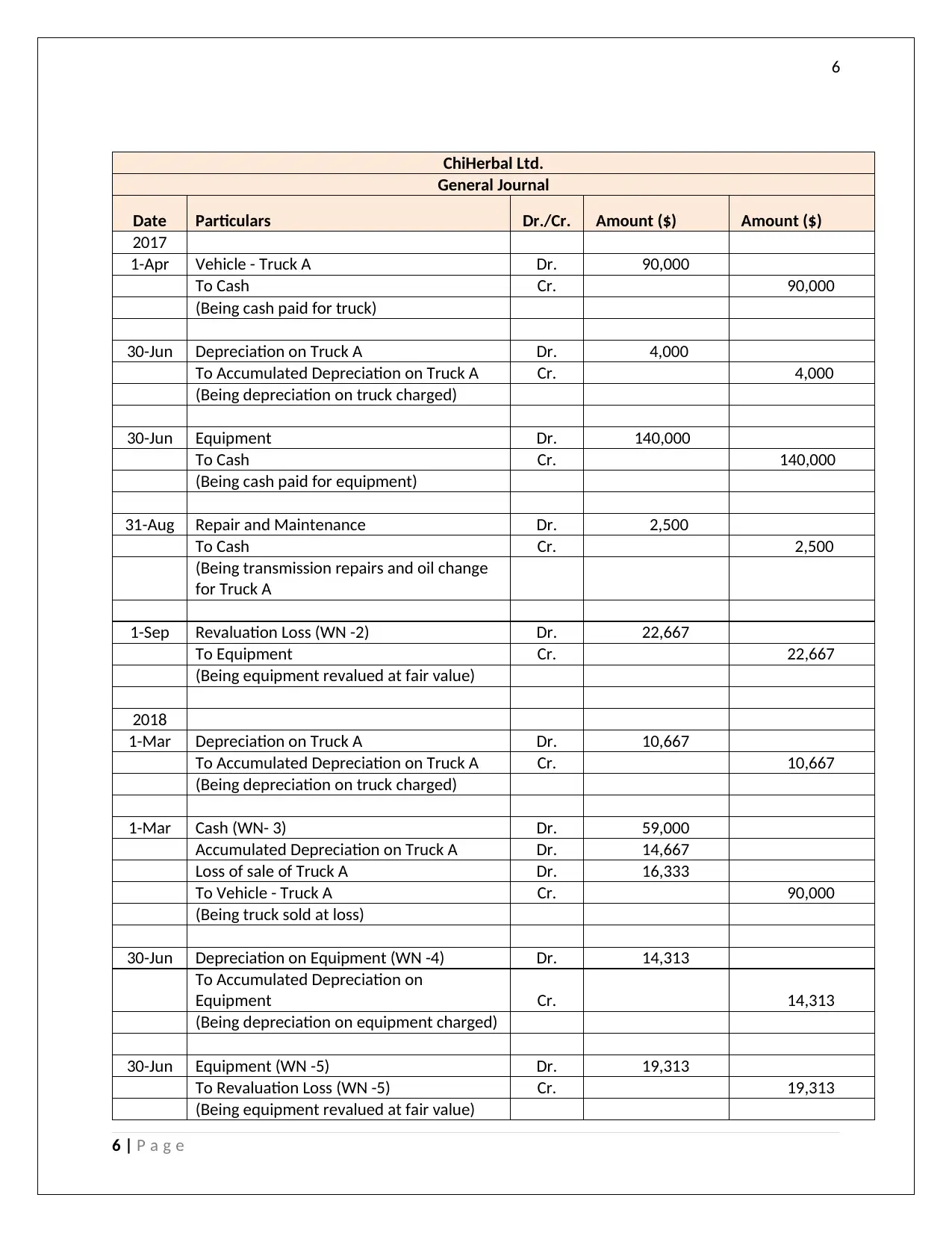

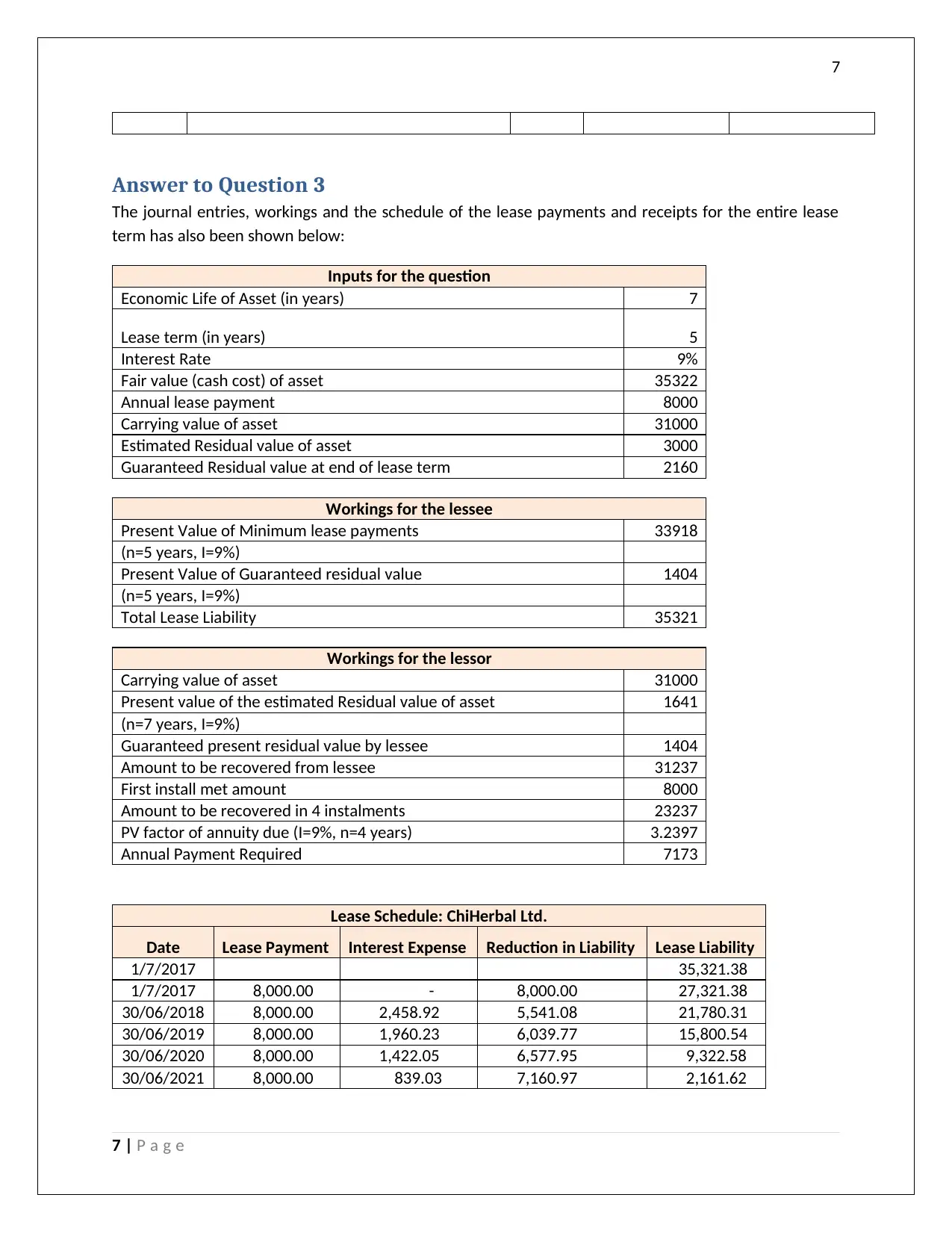

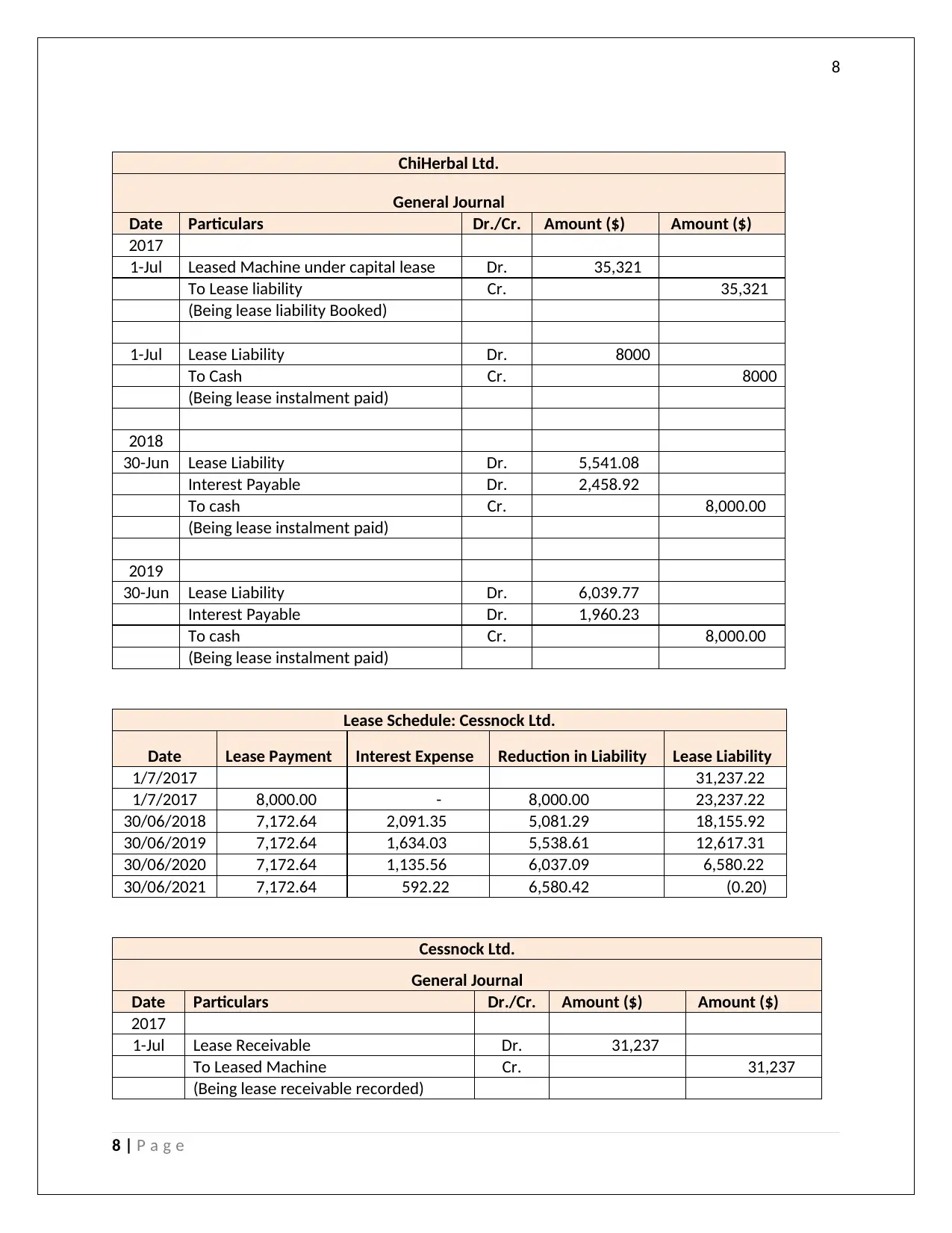

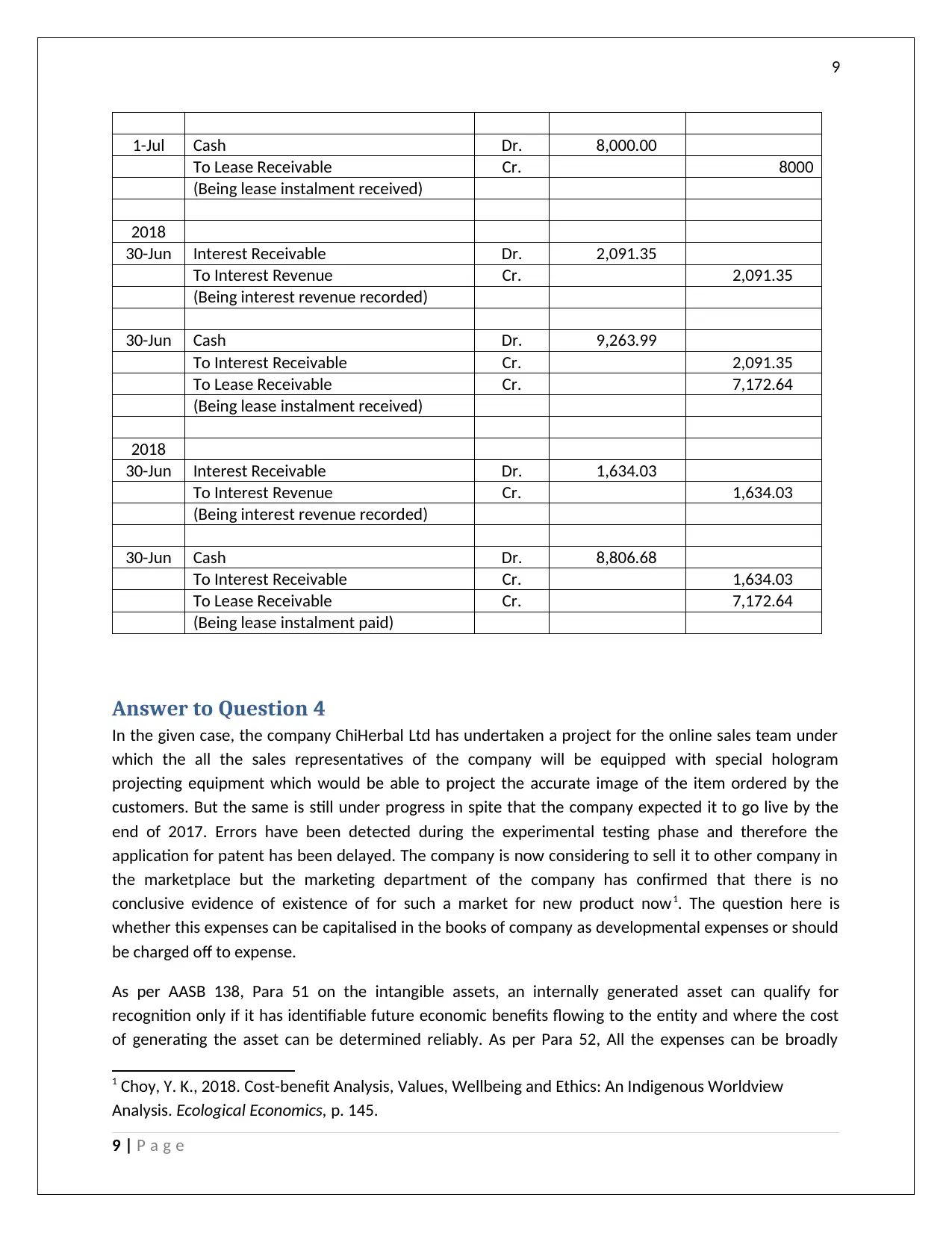

This financial accounting assignment provides a detailed analysis of various accounting processes for ChiHerbal Ltd. The assignment covers several key areas, including journal entries related to share capital, cash transactions, and share allotments. It then delves into the accounting treatment of property, plant, and equipment (PP&E), demonstrating the calculation and recording of depreciation for a truck and equipment, including revaluation adjustments and the sale of an asset. Furthermore, the assignment explores lease accounting, providing journal entries and schedules for both the lessee and lessor, including the calculation of present values, interest expense, and the reduction of lease liability. Finally, the assignment concludes with a discussion on the capitalization of development expenses, analyzing whether the expenses related to an online sales team project should be capitalized or expensed based on AASB 138 guidelines.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.