BUACC5931: Research Report on ISO 9000 Certification Impact in China

VerifiedAdded on 2022/10/10

|50

|5886

|51

Report

AI Summary

This report presents an empirical analysis of the impact of ISO 9000 certification on service firms in China, utilizing chi-square tests, ANOVA, and regression analysis. The study, based on secondary data from the National Bureau of Statistics of China, investigates the relationship between ISO 9000 certification and factors such as foreign direct investment (FDI), financial attributes, and business performance. The findings suggest that ISO 9000 certification is not a prerequisite for attracting overseas investment in Chinese service firms, although it does have a positive impact on profit through better quality management. The report provides descriptive and inferential statistics, including t-tests and correlation analyses, to support its conclusions, and discusses the implications of the findings for businesses. The study also acknowledges limitations and suggests areas for further research, offering valuable insights into the role and impact of ISO 9000 certification in the Chinese business context.

Running head: IMPACT OF ISO 9000 CERTIFICATION IN CHINA

Impact of ISO 9000 Certification in China

Name of the Student:

Name of the University:

Author Note:

Impact of ISO 9000 Certification in China

Name of the Student:

Name of the University:

Author Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1IMPACT OF ISO 9000 CERTIFICATION IN CHINA

Table of Contents

Executive Summary...................................................................................................................2

Back ground of the Study...........................................................................................................2

Literature Review.......................................................................................................................3

Methodology..............................................................................................................................4

Analysis and Findings................................................................................................................5

Descriptive Statistics..............................................................................................................5

Inferential Statistics................................................................................................................8

Sample Independent t-test..................................................................................................8

ANOVA...........................................................................................................................11

Chi-square test..................................................................................................................13

Correlation........................................................................................................................13

Discussion and Managerial Advices........................................................................................15

Limitation and Further Research..............................................................................................15

Reference..................................................................................................................................17

Appendices...............................................................................................................................20

Appendix 1...............................................................................................................................20

Appendix 2...............................................................................................................................41

Appendix 3...............................................................................................................................44

Appendix 4...............................................................................................................................46

Table of Contents

Executive Summary...................................................................................................................2

Back ground of the Study...........................................................................................................2

Literature Review.......................................................................................................................3

Methodology..............................................................................................................................4

Analysis and Findings................................................................................................................5

Descriptive Statistics..............................................................................................................5

Inferential Statistics................................................................................................................8

Sample Independent t-test..................................................................................................8

ANOVA...........................................................................................................................11

Chi-square test..................................................................................................................13

Correlation........................................................................................................................13

Discussion and Managerial Advices........................................................................................15

Limitation and Further Research..............................................................................................15

Reference..................................................................................................................................17

Appendices...............................................................................................................................20

Appendix 1...............................................................................................................................20

Appendix 2...............................................................................................................................41

Appendix 3...............................................................................................................................44

Appendix 4...............................................................................................................................46

2IMPACT OF ISO 9000 CERTIFICATION IN CHINA

Executive Summary

The report presents the empirical analysis which includes the chi-square test and

regression analysis to check the potential impact of ISO 9000 Certification in China. The test

concludes that for overseas investment, it is not necessary to have an ISO 9000 certification

to the service firms of China. Here, it is recommended to the firms to attract the overseas

investment there is no need of ISO certification. They should focus on other factors that may

have impact on attracting the FDI. However, the regression result shows that the greater

impact on profit is found from the return on asset followed by the certification. Here, ISO

certificate raises the profit. This is because of better quality management which is approved

by the certificate of ISO 9000.

Back ground of the Study

ISO 9000 implies a number of international standards for quality assurance and

management and this provides the companies easy documentation system to maintain an

effective quality system. This quality management systems standard was introduced in 1987

an since then it is extensively used by the companies all over the world (Chatzoglou,

Chatzoudes & Kipraios, 2015). The purpose of the study is to check the relationship between

the certification and FDI. Moreover, the impact of this standard along with other factors on

the revenue of the company. The research objective is mentioned in the form of research

hypothesis:

Research Aim

The interest of the study is to find out the impacts of adoption of ISO 9000.

Hence, the research question,

1. What is the impact of ISO certification on the company’s financial attributes like,

source of capital, assets, equity and demographics of the employees?

Executive Summary

The report presents the empirical analysis which includes the chi-square test and

regression analysis to check the potential impact of ISO 9000 Certification in China. The test

concludes that for overseas investment, it is not necessary to have an ISO 9000 certification

to the service firms of China. Here, it is recommended to the firms to attract the overseas

investment there is no need of ISO certification. They should focus on other factors that may

have impact on attracting the FDI. However, the regression result shows that the greater

impact on profit is found from the return on asset followed by the certification. Here, ISO

certificate raises the profit. This is because of better quality management which is approved

by the certificate of ISO 9000.

Back ground of the Study

ISO 9000 implies a number of international standards for quality assurance and

management and this provides the companies easy documentation system to maintain an

effective quality system. This quality management systems standard was introduced in 1987

an since then it is extensively used by the companies all over the world (Chatzoglou,

Chatzoudes & Kipraios, 2015). The purpose of the study is to check the relationship between

the certification and FDI. Moreover, the impact of this standard along with other factors on

the revenue of the company. The research objective is mentioned in the form of research

hypothesis:

Research Aim

The interest of the study is to find out the impacts of adoption of ISO 9000.

Hence, the research question,

1. What is the impact of ISO certification on the company’s financial attributes like,

source of capital, assets, equity and demographics of the employees?

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3IMPACT OF ISO 9000 CERTIFICATION IN CHINA

2. Is there any relationship between above mentioned variables and the adoption of ISO

9000 certification?

In this report, the first section is about introduction and a brief literature review is

discussed in the very next section. Third section describes the methodology and fourth

section discusses the findings and results. Fifth and sixth section is about discussion and

managerial advices and limitation and further research respectively.

Literature Review

The ISO certification provides directly or indirectly some extent of non-monetary

benefits. There is a lack of research that has found the impact of ISO on monetary gains

(Fikru, 2014). There is a study in Nigeria, that reveals the positive impact of ISO certification

on raising the total amount of return from the asset. The firms with ISO certification have

larger amount of sales due to hike in exports and thus the productivity is higher (Goedhuys &

Sleuwaegen, 2013). The spread of ISO 9000 certification in under developed countries that

are trying to be developed turn out to create the rise in inward FDI and the rise of export in

the trade flow (Allur, Arana-Landin & Heras Saizarbitoria, 2014). There are few papers that

describes the objective, standard and implication of quality management and performance of

the certified organizations that are improved. Now, there studies that says rise in the

performance and quality can raise the profit of those organizations (Terziovski & Guerrero,

2014). The number of studies is very less where researchers have estimated the financial

impacts of ISO certification. A research has found a positive relation with stock prices on the

particular day of being certified with ISO 900 (Terziovski & Guerrero, 2014). Again there is

a study that have noticed a positive reaction in stock market for the introduction of ISO 9000

certification (Lakhal, 2014). However, this is found that the impact was only for small firms

not for the large firms (Djofack & Camacho, 2017). There is a relationship between ISO

certification and superior performance in financial part of the company (Cai, & Jun, 2018).

2. Is there any relationship between above mentioned variables and the adoption of ISO

9000 certification?

In this report, the first section is about introduction and a brief literature review is

discussed in the very next section. Third section describes the methodology and fourth

section discusses the findings and results. Fifth and sixth section is about discussion and

managerial advices and limitation and further research respectively.

Literature Review

The ISO certification provides directly or indirectly some extent of non-monetary

benefits. There is a lack of research that has found the impact of ISO on monetary gains

(Fikru, 2014). There is a study in Nigeria, that reveals the positive impact of ISO certification

on raising the total amount of return from the asset. The firms with ISO certification have

larger amount of sales due to hike in exports and thus the productivity is higher (Goedhuys &

Sleuwaegen, 2013). The spread of ISO 9000 certification in under developed countries that

are trying to be developed turn out to create the rise in inward FDI and the rise of export in

the trade flow (Allur, Arana-Landin & Heras Saizarbitoria, 2014). There are few papers that

describes the objective, standard and implication of quality management and performance of

the certified organizations that are improved. Now, there studies that says rise in the

performance and quality can raise the profit of those organizations (Terziovski & Guerrero,

2014). The number of studies is very less where researchers have estimated the financial

impacts of ISO certification. A research has found a positive relation with stock prices on the

particular day of being certified with ISO 900 (Terziovski & Guerrero, 2014). Again there is

a study that have noticed a positive reaction in stock market for the introduction of ISO 9000

certification (Lakhal, 2014). However, this is found that the impact was only for small firms

not for the large firms (Djofack & Camacho, 2017). There is a relationship between ISO

certification and superior performance in financial part of the company (Cai, & Jun, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4IMPACT OF ISO 9000 CERTIFICATION IN CHINA

This implies that the rise in stock price indicates a better position in financial sector which

has potential to raise the profit of the company. There is a study on 160 Australian

companies, it shows the positive impacts of ISO 9000 on relation with its customers, products

and services, the product quality awareness of the company, satisfaction of the customers,

management of the company and a relative growth of the company, with its competitors

(Ong, Kathawala & Sawalha, 2015). Similarly, another study conducted in UK has claimed

that the certification has contributed positively in raising the number of new contracts,

reducing the customer audits, improving the market relation and giving an international

exposure (Kunnaala, Lappalainen & Tapaninen, 2013). Moreover, there are studies that

claims that the ISO 9000 has a contribution in raising the operational and business

performance which is reflected by the attributes like collection of capital from different

sources, assets and equities which has direct linkage in raising business and the profit

(Georgiev & Georgiev, 2015). Again there are few studies which has claimed that the ISO

certification has no role in improvement of quality management, profitability and

productivity (Grela, 2015). In this case, it is necessary to check the profitability of a firm due

to ISO certification and the attributes that are linked with the financial performance of a firm.

Methodology

In order to find the significant evidence for the answers of research questions, a large

data is collected on service firms in China. The data is secondary and collected from the

National Bureau of Statistics of China from an economic census which was conducted in

2008. A chi-square test is conducted to find the association between FDI and ISO

certification. There is ANOVA test and independence test to check the mean difference in the

variables of certified and non-certified companies. The Pearson correlation is computed to

check the relationship between the variables sales, profit, asset, capital paid, capital from

others, return on sales and return on asset and ISO 9000 certification.

This implies that the rise in stock price indicates a better position in financial sector which

has potential to raise the profit of the company. There is a study on 160 Australian

companies, it shows the positive impacts of ISO 9000 on relation with its customers, products

and services, the product quality awareness of the company, satisfaction of the customers,

management of the company and a relative growth of the company, with its competitors

(Ong, Kathawala & Sawalha, 2015). Similarly, another study conducted in UK has claimed

that the certification has contributed positively in raising the number of new contracts,

reducing the customer audits, improving the market relation and giving an international

exposure (Kunnaala, Lappalainen & Tapaninen, 2013). Moreover, there are studies that

claims that the ISO 9000 has a contribution in raising the operational and business

performance which is reflected by the attributes like collection of capital from different

sources, assets and equities which has direct linkage in raising business and the profit

(Georgiev & Georgiev, 2015). Again there are few studies which has claimed that the ISO

certification has no role in improvement of quality management, profitability and

productivity (Grela, 2015). In this case, it is necessary to check the profitability of a firm due

to ISO certification and the attributes that are linked with the financial performance of a firm.

Methodology

In order to find the significant evidence for the answers of research questions, a large

data is collected on service firms in China. The data is secondary and collected from the

National Bureau of Statistics of China from an economic census which was conducted in

2008. A chi-square test is conducted to find the association between FDI and ISO

certification. There is ANOVA test and independence test to check the mean difference in the

variables of certified and non-certified companies. The Pearson correlation is computed to

check the relationship between the variables sales, profit, asset, capital paid, capital from

others, return on sales and return on asset and ISO 9000 certification.

5IMPACT OF ISO 9000 CERTIFICATION IN CHINA

Analysis and Findings

Descriptive Statistics

The descriptive statistics is presented for each variable in this section of the report.

Each variable is discussed one by one in the following section.

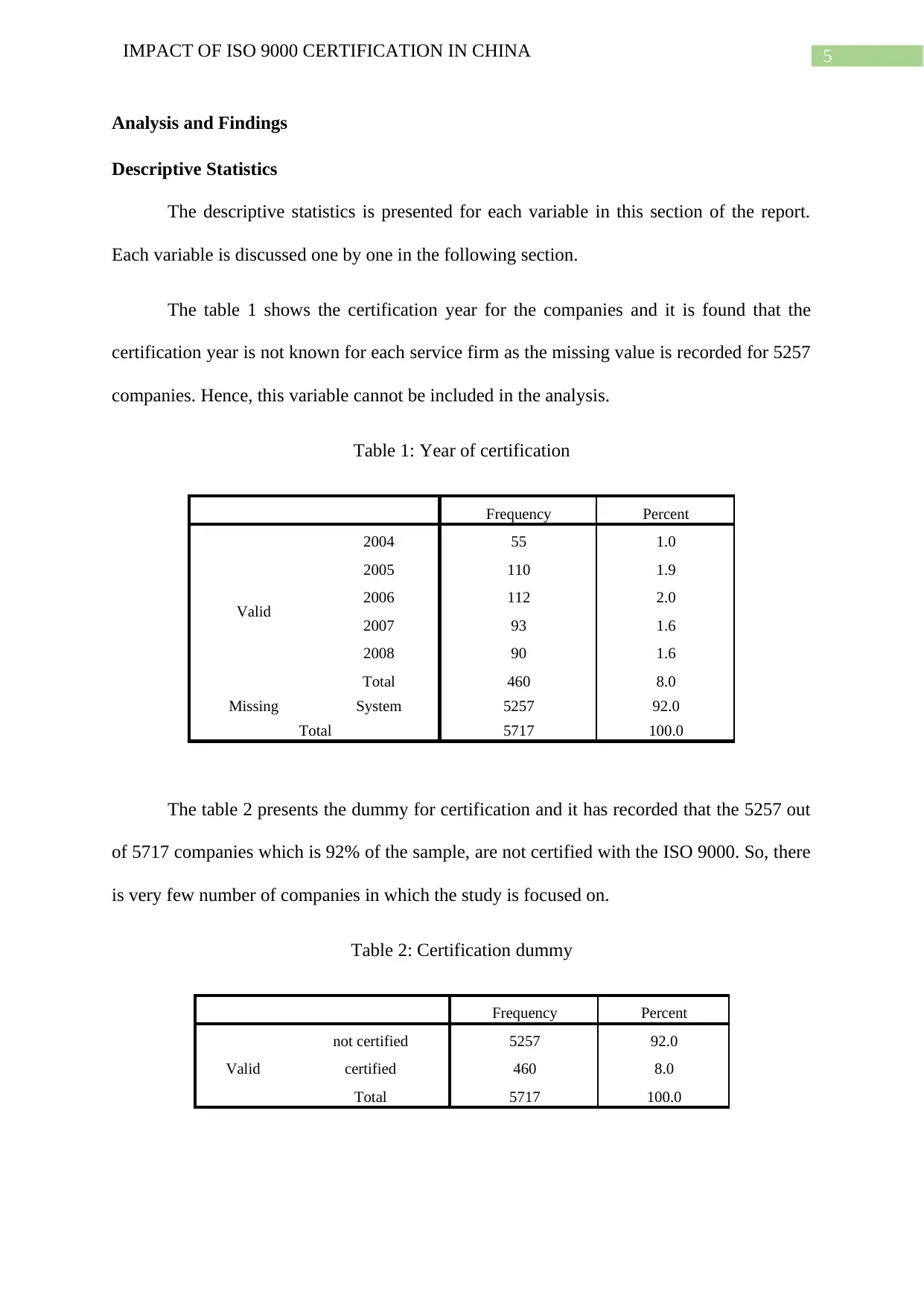

The table 1 shows the certification year for the companies and it is found that the

certification year is not known for each service firm as the missing value is recorded for 5257

companies. Hence, this variable cannot be included in the analysis.

Table 1: Year of certification

Frequency Percent

Valid

2004 55 1.0

2005 110 1.9

2006 112 2.0

2007 93 1.6

2008 90 1.6

Total 460 8.0

Missing System 5257 92.0

Total 5717 100.0

The table 2 presents the dummy for certification and it has recorded that the 5257 out

of 5717 companies which is 92% of the sample, are not certified with the ISO 9000. So, there

is very few number of companies in which the study is focused on.

Table 2: Certification dummy

Frequency Percent

Valid

not certified 5257 92.0

certified 460 8.0

Total 5717 100.0

Analysis and Findings

Descriptive Statistics

The descriptive statistics is presented for each variable in this section of the report.

Each variable is discussed one by one in the following section.

The table 1 shows the certification year for the companies and it is found that the

certification year is not known for each service firm as the missing value is recorded for 5257

companies. Hence, this variable cannot be included in the analysis.

Table 1: Year of certification

Frequency Percent

Valid

2004 55 1.0

2005 110 1.9

2006 112 2.0

2007 93 1.6

2008 90 1.6

Total 460 8.0

Missing System 5257 92.0

Total 5717 100.0

The table 2 presents the dummy for certification and it has recorded that the 5257 out

of 5717 companies which is 92% of the sample, are not certified with the ISO 9000. So, there

is very few number of companies in which the study is focused on.

Table 2: Certification dummy

Frequency Percent

Valid

not certified 5257 92.0

certified 460 8.0

Total 5717 100.0

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6IMPACT OF ISO 9000 CERTIFICATION IN CHINA

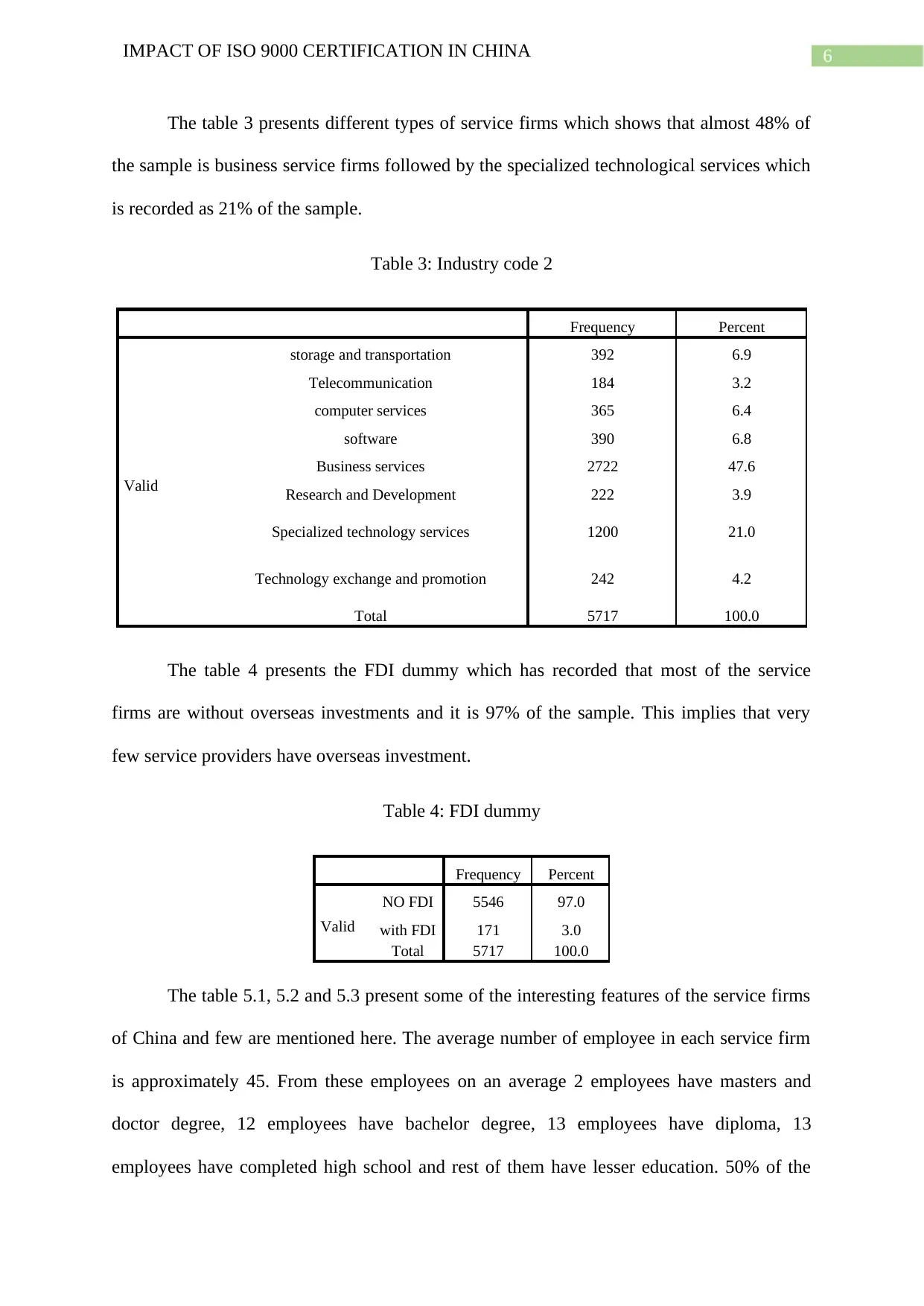

The table 3 presents different types of service firms which shows that almost 48% of

the sample is business service firms followed by the specialized technological services which

is recorded as 21% of the sample.

Table 3: Industry code 2

Frequency Percent

Valid

storage and transportation 392 6.9

Telecommunication 184 3.2

computer services 365 6.4

software 390 6.8

Business services 2722 47.6

Research and Development 222 3.9

Specialized technology services 1200 21.0

Technology exchange and promotion 242 4.2

Total 5717 100.0

The table 4 presents the FDI dummy which has recorded that most of the service

firms are without overseas investments and it is 97% of the sample. This implies that very

few service providers have overseas investment.

Table 4: FDI dummy

Frequency Percent

Valid

NO FDI 5546 97.0

with FDI 171 3.0

Total 5717 100.0

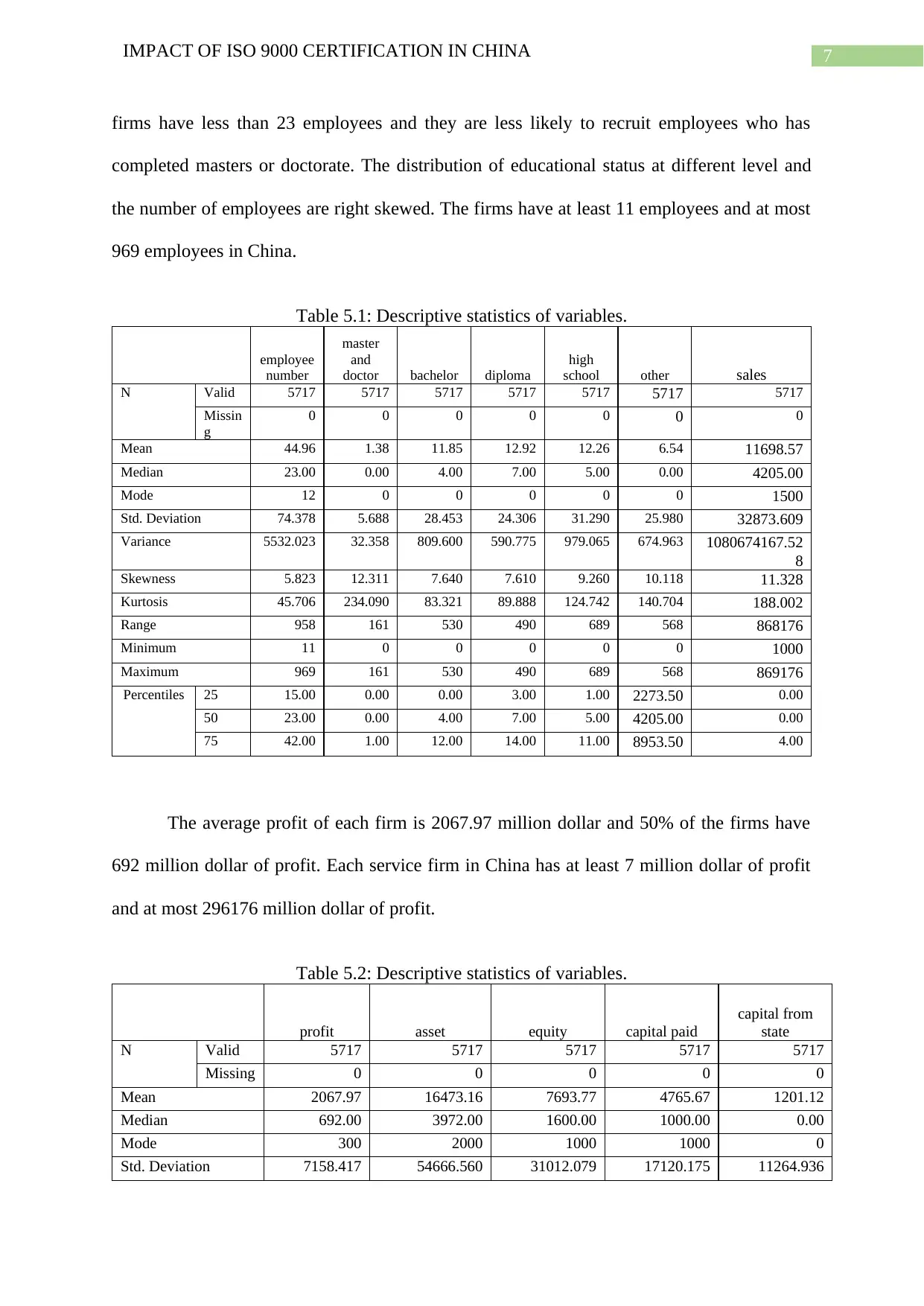

The table 5.1, 5.2 and 5.3 present some of the interesting features of the service firms

of China and few are mentioned here. The average number of employee in each service firm

is approximately 45. From these employees on an average 2 employees have masters and

doctor degree, 12 employees have bachelor degree, 13 employees have diploma, 13

employees have completed high school and rest of them have lesser education. 50% of the

The table 3 presents different types of service firms which shows that almost 48% of

the sample is business service firms followed by the specialized technological services which

is recorded as 21% of the sample.

Table 3: Industry code 2

Frequency Percent

Valid

storage and transportation 392 6.9

Telecommunication 184 3.2

computer services 365 6.4

software 390 6.8

Business services 2722 47.6

Research and Development 222 3.9

Specialized technology services 1200 21.0

Technology exchange and promotion 242 4.2

Total 5717 100.0

The table 4 presents the FDI dummy which has recorded that most of the service

firms are without overseas investments and it is 97% of the sample. This implies that very

few service providers have overseas investment.

Table 4: FDI dummy

Frequency Percent

Valid

NO FDI 5546 97.0

with FDI 171 3.0

Total 5717 100.0

The table 5.1, 5.2 and 5.3 present some of the interesting features of the service firms

of China and few are mentioned here. The average number of employee in each service firm

is approximately 45. From these employees on an average 2 employees have masters and

doctor degree, 12 employees have bachelor degree, 13 employees have diploma, 13

employees have completed high school and rest of them have lesser education. 50% of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7IMPACT OF ISO 9000 CERTIFICATION IN CHINA

firms have less than 23 employees and they are less likely to recruit employees who has

completed masters or doctorate. The distribution of educational status at different level and

the number of employees are right skewed. The firms have at least 11 employees and at most

969 employees in China.

Table 5.1: Descriptive statistics of variables.

employee

number

master

and

doctor bachelor diploma

high

school other sales

N Valid 5717 5717 5717 5717 5717 5717 5717

Missin

g

0 0 0 0 0 0 0

Mean 44.96 1.38 11.85 12.92 12.26 6.54 11698.57

Median 23.00 0.00 4.00 7.00 5.00 0.00 4205.00

Mode 12 0 0 0 0 0 1500

Std. Deviation 74.378 5.688 28.453 24.306 31.290 25.980 32873.609

Variance 5532.023 32.358 809.600 590.775 979.065 674.963 1080674167.52

8

Skewness 5.823 12.311 7.640 7.610 9.260 10.118 11.328

Kurtosis 45.706 234.090 83.321 89.888 124.742 140.704 188.002

Range 958 161 530 490 689 568 868176

Minimum 11 0 0 0 0 0 1000

Maximum 969 161 530 490 689 568 869176

Percentiles 25 15.00 0.00 0.00 3.00 1.00 2273.50 0.00

50 23.00 0.00 4.00 7.00 5.00 4205.00 0.00

75 42.00 1.00 12.00 14.00 11.00 8953.50 4.00

The average profit of each firm is 2067.97 million dollar and 50% of the firms have

692 million dollar of profit. Each service firm in China has at least 7 million dollar of profit

and at most 296176 million dollar of profit.

Table 5.2: Descriptive statistics of variables.

profit asset equity capital paid

capital from

state

N Valid 5717 5717 5717 5717 5717

Missing 0 0 0 0 0

Mean 2067.97 16473.16 7693.77 4765.67 1201.12

Median 692.00 3972.00 1600.00 1000.00 0.00

Mode 300 2000 1000 1000 0

Std. Deviation 7158.417 54666.560 31012.079 17120.175 11264.936

firms have less than 23 employees and they are less likely to recruit employees who has

completed masters or doctorate. The distribution of educational status at different level and

the number of employees are right skewed. The firms have at least 11 employees and at most

969 employees in China.

Table 5.1: Descriptive statistics of variables.

employee

number

master

and

doctor bachelor diploma

high

school other sales

N Valid 5717 5717 5717 5717 5717 5717 5717

Missin

g

0 0 0 0 0 0 0

Mean 44.96 1.38 11.85 12.92 12.26 6.54 11698.57

Median 23.00 0.00 4.00 7.00 5.00 0.00 4205.00

Mode 12 0 0 0 0 0 1500

Std. Deviation 74.378 5.688 28.453 24.306 31.290 25.980 32873.609

Variance 5532.023 32.358 809.600 590.775 979.065 674.963 1080674167.52

8

Skewness 5.823 12.311 7.640 7.610 9.260 10.118 11.328

Kurtosis 45.706 234.090 83.321 89.888 124.742 140.704 188.002

Range 958 161 530 490 689 568 868176

Minimum 11 0 0 0 0 0 1000

Maximum 969 161 530 490 689 568 869176

Percentiles 25 15.00 0.00 0.00 3.00 1.00 2273.50 0.00

50 23.00 0.00 4.00 7.00 5.00 4205.00 0.00

75 42.00 1.00 12.00 14.00 11.00 8953.50 4.00

The average profit of each firm is 2067.97 million dollar and 50% of the firms have

692 million dollar of profit. Each service firm in China has at least 7 million dollar of profit

and at most 296176 million dollar of profit.

Table 5.2: Descriptive statistics of variables.

profit asset equity capital paid

capital from

state

N Valid 5717 5717 5717 5717 5717

Missing 0 0 0 0 0

Mean 2067.97 16473.16 7693.77 4765.67 1201.12

Median 692.00 3972.00 1600.00 1000.00 0.00

Mode 300 2000 1000 1000 0

Std. Deviation 7158.417 54666.560 31012.079 17120.175 11264.936

8IMPACT OF ISO 9000 CERTIFICATION IN CHINA

Variance 51242940.369 2988432750.32

1

961749073.465 293100400.983 126898792.888

Skewness 19.254 9.296 12.702 11.566 20.017

Kurtosis 602.738 113.569 228.913 183.898 514.075

Range 296159 977548 879356 402100 402110

Minimum 17 1000 -1367 10 0

Maximum 296176 978548 877989 402110 402110

Percentile

s

25 313.00 2065.00 800.00 0.00 500.00

50 692.00 3972.00 1600.00 0.00 1000.00

75 1542.00 9671.00 4309.50 0.00 3000.00

In China, the service firms are doing business for an average of 7.62 years and 50% of

the companies have the age of less than 6 years. The newest firm in China is operating for

last 2 years and the oldest firm in China is operating for last 61 years.

Table 5.3: Descriptive statistics of variables.

capital from

overseas

capital from

other

return

on

sales

return

on

asset

percentage

of FDI

age of

company

in years

N Valid 5717 5717 5717 5717 5717 5717

Missing 0 0 0 0 0 0

Mean 348.87 3215.68 .1911 .2236 .0245 7.62

Median 0.00 1000.00 .1700 .1550 0.0000 6.00

Mode 0 1000 .24 .04a 0.00 2

Std. Deviation 4598.814 11765.554 .12397 .20858 .14937 7.074

Variance 21149093.297 138428249.797 .015 .044 .022 50.044

Skewness 21.317 15.536 .514 1.500 6.168 3.540

Kurtosis 535.442 368.302 -.701 2.021 36.651 17.849

Range 150000 400000 .49 1.01 1.00 59

Minimum 0 0 .01 .01 0.00 2

Maximum 150000 400000 .51 1.02 1.00 61

Percentiles 25 0.00 400.00 .0847 .0649 0.0000 3.00

50 0.00 1000.00 .1700 .1550 0.0000 6.00

75 0.00 2077.50 .2840 .3148 0.0000 9.00

Inferential Statistics

Sample Independent t-test

The below table is the inferential table for the independence t-test where the certification

dummy is used as a factor. This shows the comparison of the factors that are influenced by

Variance 51242940.369 2988432750.32

1

961749073.465 293100400.983 126898792.888

Skewness 19.254 9.296 12.702 11.566 20.017

Kurtosis 602.738 113.569 228.913 183.898 514.075

Range 296159 977548 879356 402100 402110

Minimum 17 1000 -1367 10 0

Maximum 296176 978548 877989 402110 402110

Percentile

s

25 313.00 2065.00 800.00 0.00 500.00

50 692.00 3972.00 1600.00 0.00 1000.00

75 1542.00 9671.00 4309.50 0.00 3000.00

In China, the service firms are doing business for an average of 7.62 years and 50% of

the companies have the age of less than 6 years. The newest firm in China is operating for

last 2 years and the oldest firm in China is operating for last 61 years.

Table 5.3: Descriptive statistics of variables.

capital from

overseas

capital from

other

return

on

sales

return

on

asset

percentage

of FDI

age of

company

in years

N Valid 5717 5717 5717 5717 5717 5717

Missing 0 0 0 0 0 0

Mean 348.87 3215.68 .1911 .2236 .0245 7.62

Median 0.00 1000.00 .1700 .1550 0.0000 6.00

Mode 0 1000 .24 .04a 0.00 2

Std. Deviation 4598.814 11765.554 .12397 .20858 .14937 7.074

Variance 21149093.297 138428249.797 .015 .044 .022 50.044

Skewness 21.317 15.536 .514 1.500 6.168 3.540

Kurtosis 535.442 368.302 -.701 2.021 36.651 17.849

Range 150000 400000 .49 1.01 1.00 59

Minimum 0 0 .01 .01 0.00 2

Maximum 150000 400000 .51 1.02 1.00 61

Percentiles 25 0.00 400.00 .0847 .0649 0.0000 3.00

50 0.00 1000.00 .1700 .1550 0.0000 6.00

75 0.00 2077.50 .2840 .3148 0.0000 9.00

Inferential Statistics

Sample Independent t-test

The below table is the inferential table for the independence t-test where the certification

dummy is used as a factor. This shows the comparison of the factors that are influenced by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9IMPACT OF ISO 9000 CERTIFICATION IN CHINA

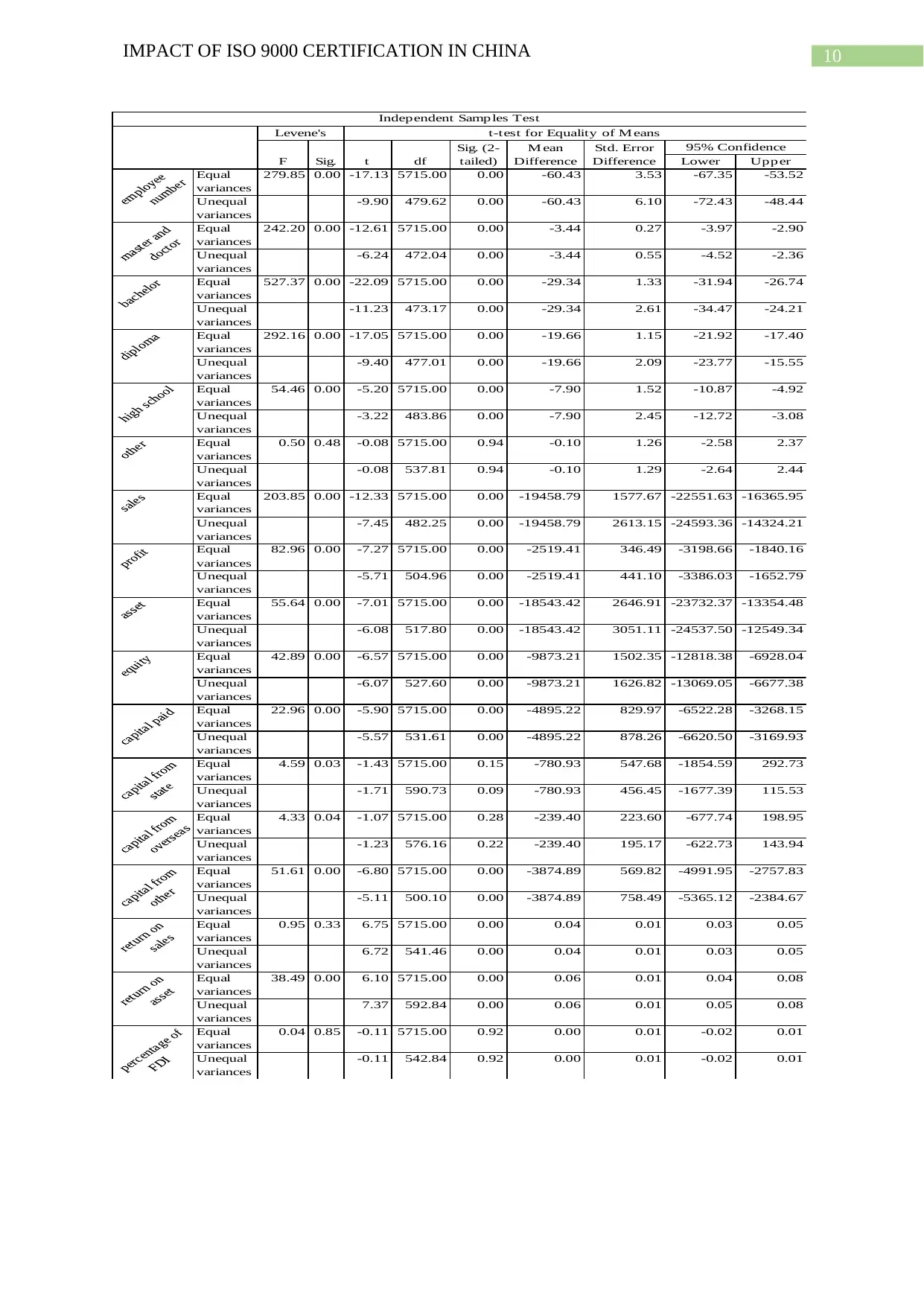

the ISO 9000 certification. Now, if the p-value for the equal variance is greater than 0.05 then

the assumption of equal variance is not violated otherwise there is unequal variance. Now

looking at the p-value of t-stat for all variables, it is found that the p-value is greater than 0.05

for other level of educational qualification, capital from state and capital from overseas and

percentage of FDI. This implies that these variables are not significantly different for the

certified and non-certified companies. This implies that the mean value of employee number,

master and doctor, bachelor, diploma, high school, sales, profit, asset, equity, capital paid,

capital from other, return on sales and return on asset off certified and uncertified companies

are significantly different.

Table 6: Result of sample independent t-test

the ISO 9000 certification. Now, if the p-value for the equal variance is greater than 0.05 then

the assumption of equal variance is not violated otherwise there is unequal variance. Now

looking at the p-value of t-stat for all variables, it is found that the p-value is greater than 0.05

for other level of educational qualification, capital from state and capital from overseas and

percentage of FDI. This implies that these variables are not significantly different for the

certified and non-certified companies. This implies that the mean value of employee number,

master and doctor, bachelor, diploma, high school, sales, profit, asset, equity, capital paid,

capital from other, return on sales and return on asset off certified and uncertified companies

are significantly different.

Table 6: Result of sample independent t-test

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10IMPACT OF ISO 9000 CERTIFICATION IN CHINA

Lower Upper

Std. Error

Difference

95% Confidence

Independent Samples Test

Levene's t-test for Equality of Means

F Sig. t df

Sig. (2-

tailed)

M ean

Difference

Equal

variances

279.85 0.00 -17.13 5715.00 0.00 -60.43 3.53 -67.35 -53.52

Unequal

variances

-9.90 479.62 0.00 -60.43 6.10 -72.43 -48.44

Equal

variances

242.20 0.00 -12.61 5715.00 0.00 -3.44 0.27 -3.97 -2.90

Unequal

variances

-6.24 472.04 0.00 -3.44 0.55 -4.52 -2.36

Equal

variances

527.37 0.00 -22.09 5715.00 0.00 -29.34 1.33 -31.94 -26.74

Unequal

variances

-11.23 473.17 0.00 -29.34 2.61 -34.47 -24.21

Equal

variances

292.16 0.00 -17.05 5715.00 0.00 -19.66 1.15 -21.92 -17.40

Unequal

variances

-9.40 477.01 0.00 -19.66 2.09 -23.77 -15.55

Equal

variances

54.46 0.00 -5.20 5715.00 0.00 -7.90 1.52 -10.87 -4.92

Unequal

variances

-3.22 483.86 0.00 -7.90 2.45 -12.72 -3.08

Equal

variances

0.50 0.48 -0.08 5715.00 0.94 -0.10 1.26 -2.58 2.37

Unequal

variances

-0.08 537.81 0.94 -0.10 1.29 -2.64 2.44

Equal

variances

203.85 0.00 -12.33 5715.00 0.00 -19458.79 1577.67 -22551.63 -16365.95

Unequal

variances

-7.45 482.25 0.00 -19458.79 2613.15 -24593.36 -14324.21

Equal

variances

82.96 0.00 -7.27 5715.00 0.00 -2519.41 346.49 -3198.66 -1840.16

Unequal

variances

-5.71 504.96 0.00 -2519.41 441.10 -3386.03 -1652.79

Equal

variances

55.64 0.00 -7.01 5715.00 0.00 -18543.42 2646.91 -23732.37 -13354.48

Unequal

variances

-6.08 517.80 0.00 -18543.42 3051.11 -24537.50 -12549.34

Equal

variances

42.89 0.00 -6.57 5715.00 0.00 -9873.21 1502.35 -12818.38 -6928.04

Unequal

variances

-6.07 527.60 0.00 -9873.21 1626.82 -13069.05 -6677.38

Equal

variances

22.96 0.00 -5.90 5715.00 0.00 -4895.22 829.97 -6522.28 -3268.15

Unequal

variances

-5.57 531.61 0.00 -4895.22 878.26 -6620.50 -3169.93

Equal

variances

4.59 0.03 -1.43 5715.00 0.15 -780.93 547.68 -1854.59 292.73

Unequal

variances

-1.71 590.73 0.09 -780.93 456.45 -1677.39 115.53

Equal

variances

4.33 0.04 -1.07 5715.00 0.28 -239.40 223.60 -677.74 198.95

Unequal

variances

-1.23 576.16 0.22 -239.40 195.17 -622.73 143.94

Equal

variances

51.61 0.00 -6.80 5715.00 0.00 -3874.89 569.82 -4991.95 -2757.83

Unequal

variances

-5.11 500.10 0.00 -3874.89 758.49 -5365.12 -2384.67

Equal

variances

0.95 0.33 6.75 5715.00 0.00 0.04 0.01 0.03 0.05

Unequal

variances

6.72 541.46 0.00 0.04 0.01 0.03 0.05

Equal

variances

38.49 0.00 6.10 5715.00 0.00 0.06 0.01 0.04 0.08

Unequal

variances

7.37 592.84 0.00 0.06 0.01 0.05 0.08

Equal

variances

0.04 0.85 -0.11 5715.00 0.92 0.00 0.01 -0.02 0.01

Unequal

variances

-0.11 542.84 0.92 0.00 0.01 -0.02 0.01

Lower Upper

Std. Error

Difference

95% Confidence

Independent Samples Test

Levene's t-test for Equality of Means

F Sig. t df

Sig. (2-

tailed)

M ean

Difference

Equal

variances

279.85 0.00 -17.13 5715.00 0.00 -60.43 3.53 -67.35 -53.52

Unequal

variances

-9.90 479.62 0.00 -60.43 6.10 -72.43 -48.44

Equal

variances

242.20 0.00 -12.61 5715.00 0.00 -3.44 0.27 -3.97 -2.90

Unequal

variances

-6.24 472.04 0.00 -3.44 0.55 -4.52 -2.36

Equal

variances

527.37 0.00 -22.09 5715.00 0.00 -29.34 1.33 -31.94 -26.74

Unequal

variances

-11.23 473.17 0.00 -29.34 2.61 -34.47 -24.21

Equal

variances

292.16 0.00 -17.05 5715.00 0.00 -19.66 1.15 -21.92 -17.40

Unequal

variances

-9.40 477.01 0.00 -19.66 2.09 -23.77 -15.55

Equal

variances

54.46 0.00 -5.20 5715.00 0.00 -7.90 1.52 -10.87 -4.92

Unequal

variances

-3.22 483.86 0.00 -7.90 2.45 -12.72 -3.08

Equal

variances

0.50 0.48 -0.08 5715.00 0.94 -0.10 1.26 -2.58 2.37

Unequal

variances

-0.08 537.81 0.94 -0.10 1.29 -2.64 2.44

Equal

variances

203.85 0.00 -12.33 5715.00 0.00 -19458.79 1577.67 -22551.63 -16365.95

Unequal

variances

-7.45 482.25 0.00 -19458.79 2613.15 -24593.36 -14324.21

Equal

variances

82.96 0.00 -7.27 5715.00 0.00 -2519.41 346.49 -3198.66 -1840.16

Unequal

variances

-5.71 504.96 0.00 -2519.41 441.10 -3386.03 -1652.79

Equal

variances

55.64 0.00 -7.01 5715.00 0.00 -18543.42 2646.91 -23732.37 -13354.48

Unequal

variances

-6.08 517.80 0.00 -18543.42 3051.11 -24537.50 -12549.34

Equal

variances

42.89 0.00 -6.57 5715.00 0.00 -9873.21 1502.35 -12818.38 -6928.04

Unequal

variances

-6.07 527.60 0.00 -9873.21 1626.82 -13069.05 -6677.38

Equal

variances

22.96 0.00 -5.90 5715.00 0.00 -4895.22 829.97 -6522.28 -3268.15

Unequal

variances

-5.57 531.61 0.00 -4895.22 878.26 -6620.50 -3169.93

Equal

variances

4.59 0.03 -1.43 5715.00 0.15 -780.93 547.68 -1854.59 292.73

Unequal

variances

-1.71 590.73 0.09 -780.93 456.45 -1677.39 115.53

Equal

variances

4.33 0.04 -1.07 5715.00 0.28 -239.40 223.60 -677.74 198.95

Unequal

variances

-1.23 576.16 0.22 -239.40 195.17 -622.73 143.94

Equal

variances

51.61 0.00 -6.80 5715.00 0.00 -3874.89 569.82 -4991.95 -2757.83

Unequal

variances

-5.11 500.10 0.00 -3874.89 758.49 -5365.12 -2384.67

Equal

variances

0.95 0.33 6.75 5715.00 0.00 0.04 0.01 0.03 0.05

Unequal

variances

6.72 541.46 0.00 0.04 0.01 0.03 0.05

Equal

variances

38.49 0.00 6.10 5715.00 0.00 0.06 0.01 0.04 0.08

Unequal

variances

7.37 592.84 0.00 0.06 0.01 0.05 0.08

Equal

variances

0.04 0.85 -0.11 5715.00 0.92 0.00 0.01 -0.02 0.01

Unequal

variances

-0.11 542.84 0.92 0.00 0.01 -0.02 0.01

11IMPACT OF ISO 9000 CERTIFICATION IN CHINA

ANOVA

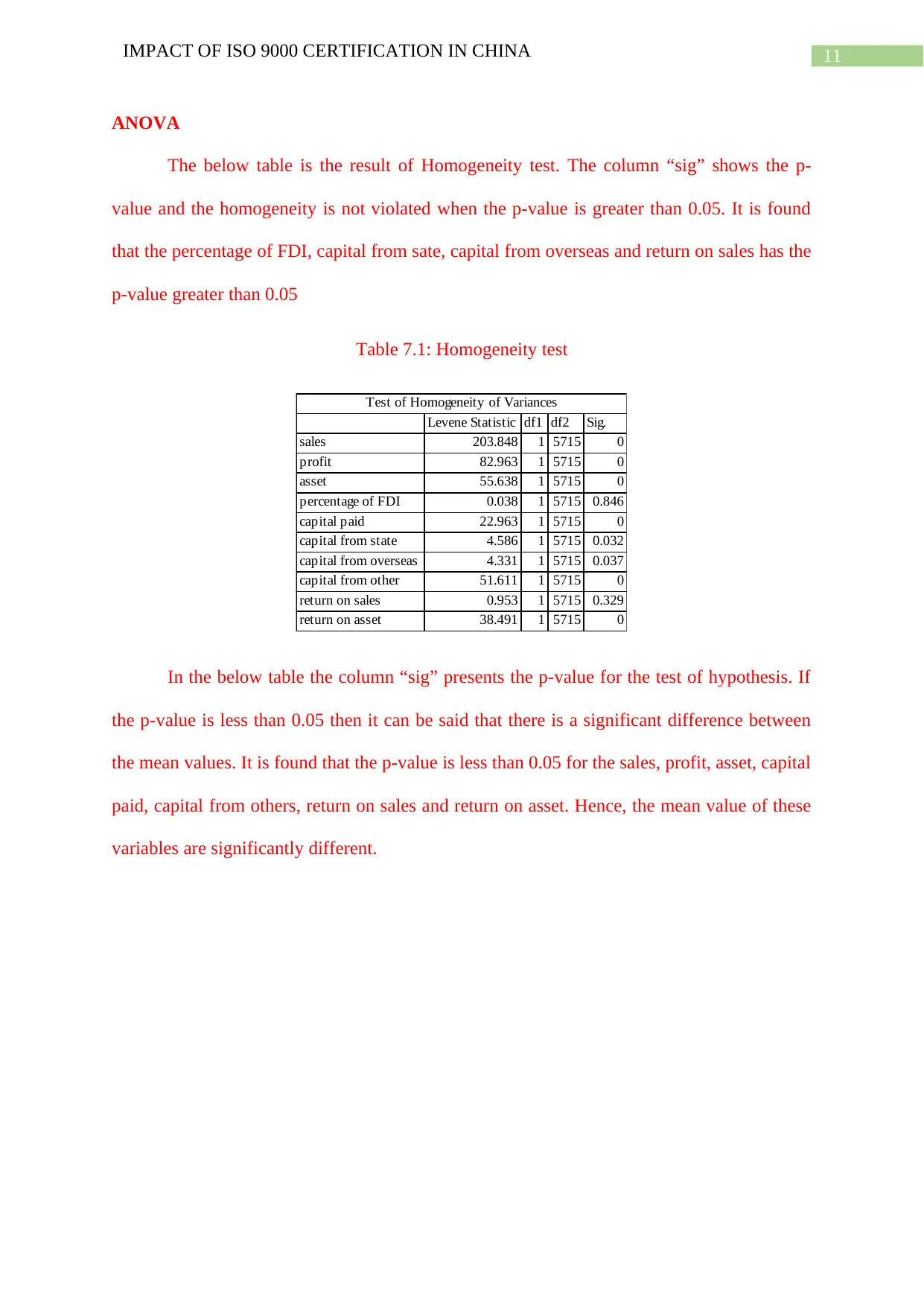

The below table is the result of Homogeneity test. The column “sig” shows the p-

value and the homogeneity is not violated when the p-value is greater than 0.05. It is found

that the percentage of FDI, capital from sate, capital from overseas and return on sales has the

p-value greater than 0.05

Table 7.1: Homogeneity test

Levene Statistic df1 df2 Sig.

sales 203.848 1 5715 0

profit 82.963 1 5715 0

asset 55.638 1 5715 0

percentage of FDI 0.038 1 5715 0.846

capital paid 22.963 1 5715 0

capital from state 4.586 1 5715 0.032

capital from overseas 4.331 1 5715 0.037

capital from other 51.611 1 5715 0

return on sales 0.953 1 5715 0.329

return on asset 38.491 1 5715 0

Test of Homogeneity of Variances

In the below table the column “sig” presents the p-value for the test of hypothesis. If

the p-value is less than 0.05 then it can be said that there is a significant difference between

the mean values. It is found that the p-value is less than 0.05 for the sales, profit, asset, capital

paid, capital from others, return on sales and return on asset. Hence, the mean value of these

variables are significantly different.

ANOVA

The below table is the result of Homogeneity test. The column “sig” shows the p-

value and the homogeneity is not violated when the p-value is greater than 0.05. It is found

that the percentage of FDI, capital from sate, capital from overseas and return on sales has the

p-value greater than 0.05

Table 7.1: Homogeneity test

Levene Statistic df1 df2 Sig.

sales 203.848 1 5715 0

profit 82.963 1 5715 0

asset 55.638 1 5715 0

percentage of FDI 0.038 1 5715 0.846

capital paid 22.963 1 5715 0

capital from state 4.586 1 5715 0.032

capital from overseas 4.331 1 5715 0.037

capital from other 51.611 1 5715 0

return on sales 0.953 1 5715 0.329

return on asset 38.491 1 5715 0

Test of Homogeneity of Variances

In the below table the column “sig” presents the p-value for the test of hypothesis. If

the p-value is less than 0.05 then it can be said that there is a significant difference between

the mean values. It is found that the p-value is less than 0.05 for the sales, profit, asset, capital

paid, capital from others, return on sales and return on asset. Hence, the mean value of these

variables are significantly different.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 50

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.