Selecting Crowdfunding Types Through Startup Life Cycle Stages

VerifiedAdded on 2023/01/18

|11

|8591

|25

Report

AI Summary

This report examines crowdfunding as a crucial funding source for startups, analyzing its various types—donation, lending, and equity crowdfunding—and the benefits each offers. It emphasizes how crowdfunding goes beyond just financial resources, providing non-monetary advantages like market validation, product refinement through customer feedback, and marketing opportunities. The report introduces a framework for startups to select the most suitable crowdfunding type based on their specific life cycle stages, addressing the unique resource needs at each stage. It provides practical advice on best practices for crowdfunding campaigns, aiming to help startups achieve their funding goals and build a loyal customer base. By understanding these aspects, startups can strategically leverage crowdfunding to overcome funding challenges and foster growth.

See discussions, stats, and author profiles for this publication at: https://www.researchgate.net/publication/311854157

Choose wisely: Crowdfunding through the stages of the startup life cycle

Article in Business Horizons · December 2016

DOI: 10.1016/j.bushor.2016.11.003

CITATIONS

18

READS

1,795

1 author:

Some of the authors of this publication are also working on these related projects:

The role of IT for value creation in service ecosystemsView project

Jeannette Paschen

KTH Royal Institute of Technology

15PUBLICATIONS30CITATIONS

SEE PROFILE

Choose wisely: Crowdfunding through the stages of the startup life cycle

Article in Business Horizons · December 2016

DOI: 10.1016/j.bushor.2016.11.003

CITATIONS

18

READS

1,795

1 author:

Some of the authors of this publication are also working on these related projects:

The role of IT for value creation in service ecosystemsView project

Jeannette Paschen

KTH Royal Institute of Technology

15PUBLICATIONS30CITATIONS

SEE PROFILE

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Choosewisely: Crowdfundingthroughthe

stagesof the startup life cycle

Jeannette Paschen

RoyalInstitute of Technology(KTH), Stockholm,Sweden

1. Startupsand crowdfunding

Startupsrequireresourcesto succeedandoneof the

most importantresourcesis money.Traditionally,

the optionsfor capitalformationavailableto start-

ups were few and comprisedprimarily of FFF

(friends, family, fools), angel investors, venture

capitalists, and seed funding (Startup Explore,

2014). More recently, there has been a surge in

alternative models. Among these, crowdfunding

has emergedas a popularsourceof capital forma-

tion in variousfields–—frompurelyfor-profitto social

causes,technology,performingarts, real estate,

and music.

Crowdfundingdrawsinspirationfromthe ideasof

microfinance(Morduch,1999)andcrowdsourcing.It

encompassesthe outsourcingof an organizational

function (capital formation) to a strategically

definednetworkof actors (crowd) in the form of

an opencall (Kietzmann,2017)via dedicatedweb-

sites(crowdfundingplatforms).And smallamounts

of moneyfrom a largenumberof peopleadd up. In

2010,crowdfundingwas a relativelysmallindustry

BusinessHorizons(2017)60, 179—188

Availableonlineat www.sciencedirect.com

ScienceDirect www.elsevier.com/locate/bushor

KEYWORDS

Crowdfunding;

Startupfunding;

Crowdsourcing;

Crowdcapital;

Information

asymmetry;

Crowdcommunication;

Startupstrategy

Abstract Crowdfundingis attractiveto startupsas an alternativefundingsource

and offers nonmonetaryresourcesthroughorganizationallearning.It encompasses

the outsourcingof an organizationalfunction,throughIT, to a strategicallydefined

networkof actors(i.e., thecrowd)in theformof anopencall–—specifically,requesting

monetarycontributionstowarda commercialor social businessgoal. Nonetheless,

manystartupsarehesitantto considercrowdfundingbecauselittle guidanceexistson

how the varioustypesof crowdfundingadd valuein differentlife cycle stagesand

which type is best suited for which stage. In responseto this gap, this article

introducesa typologyof crowdfunding,the benefitsit offers, and how specific

benefitsrelate to the identifiedcrowdfundingtypes. On this basis, we presenta

frameworkfor choosingthe rightcrowdfundingtypefor eachstagein the startuplife

cycle, in additionto providingpracticaladviceon crowdfundingbestpractices.The

best practicesoutlinedhave showndemonstrablecontributionstoward achieving

fundinggoalsand are likely to provevaluablefor startups.

# 2016KelleySchoolof Business,IndianaUniversity.Publishedby ElsevierInc. All

rightsreserved.

E-mail address:jeannette.paschen@indek.kth.se

0007-6813/$— see front matter# 2016KelleySchoolof Business,IndianaUniversity.Publishedby ElsevierInc. All rightsreserved.

http://dx.doi.org/10.1016/j.bushor.2016.11.003

stagesof the startup life cycle

Jeannette Paschen

RoyalInstitute of Technology(KTH), Stockholm,Sweden

1. Startupsand crowdfunding

Startupsrequireresourcesto succeedandoneof the

most importantresourcesis money.Traditionally,

the optionsfor capitalformationavailableto start-

ups were few and comprisedprimarily of FFF

(friends, family, fools), angel investors, venture

capitalists, and seed funding (Startup Explore,

2014). More recently, there has been a surge in

alternative models. Among these, crowdfunding

has emergedas a popularsourceof capital forma-

tion in variousfields–—frompurelyfor-profitto social

causes,technology,performingarts, real estate,

and music.

Crowdfundingdrawsinspirationfromthe ideasof

microfinance(Morduch,1999)andcrowdsourcing.It

encompassesthe outsourcingof an organizational

function (capital formation) to a strategically

definednetworkof actors (crowd) in the form of

an opencall (Kietzmann,2017)via dedicatedweb-

sites(crowdfundingplatforms).And smallamounts

of moneyfrom a largenumberof peopleadd up. In

2010,crowdfundingwas a relativelysmallindustry

BusinessHorizons(2017)60, 179—188

Availableonlineat www.sciencedirect.com

ScienceDirect www.elsevier.com/locate/bushor

KEYWORDS

Crowdfunding;

Startupfunding;

Crowdsourcing;

Crowdcapital;

Information

asymmetry;

Crowdcommunication;

Startupstrategy

Abstract Crowdfundingis attractiveto startupsas an alternativefundingsource

and offers nonmonetaryresourcesthroughorganizationallearning.It encompasses

the outsourcingof an organizationalfunction,throughIT, to a strategicallydefined

networkof actors(i.e., thecrowd)in theformof anopencall–—specifically,requesting

monetarycontributionstowarda commercialor social businessgoal. Nonetheless,

manystartupsarehesitantto considercrowdfundingbecauselittle guidanceexistson

how the varioustypesof crowdfundingadd valuein differentlife cycle stagesand

which type is best suited for which stage. In responseto this gap, this article

introducesa typologyof crowdfunding,the benefitsit offers, and how specific

benefitsrelate to the identifiedcrowdfundingtypes. On this basis, we presenta

frameworkfor choosingthe rightcrowdfundingtypefor eachstagein the startuplife

cycle, in additionto providingpracticaladviceon crowdfundingbestpractices.The

best practicesoutlinedhave showndemonstrablecontributionstoward achieving

fundinggoalsand are likely to provevaluablefor startups.

# 2016KelleySchoolof Business,IndianaUniversity.Publishedby ElsevierInc. All

rightsreserved.

E-mail address:jeannette.paschen@indek.kth.se

0007-6813/$— see front matter# 2016KelleySchoolof Business,IndianaUniversity.Publishedby ElsevierInc. All rightsreserved.

http://dx.doi.org/10.1016/j.bushor.2016.11.003

to the tune of $880 million worldwide. In 2015,

estimatesput the global crowdfundingindustryat

$34.4billion (Massolution,2015).

Crowdfundingis especiallysuited for startups

trying to turn an idea into a viable businessand

youngcompaniesaimingto maintainor grow their

venture(Stemler,2013).Bothface challengeswhen

tryingto securefunding.Dueto lack of credit and

operatinghistory,startupfoundersoften havediffi-

cultiesconveyingthevalueof theirproposedventure

to investors.Startups, therefore, have difficulty

accessingtraditionalfundingoptionssuch as bank

loans,venturecapital,or angelinvestments.These

challengesare exacerbatedfor social ventures,

which are drivenby the ambiguousand sometimes

dichotomousgoal to achievea doublebottomline:

to balancesocialandfor-profitgoals(Lehner,2013).

In addition,it is often prohibitivelyexpensivefor

youngbusinessesto accesswidertraditionalcapital

markets(Tunguz,2013).These and other factors,

such as the shortageof capital provokedby the

globalfinancialcrisisand the growthin otherforms

of crowdsourcing,have contributedto the rise of

the crowdfundingphenomenonin recent years

(Giudici,Guerini,& Lamastra,2013).

As crowdfundinghasbeengrowingin popularity,

so has its exposurein academicand practitioner-

orientedliterature. A numberof articles havede-

velopedindependentlyof oneanotherbut withouta

unifyingframeworkto understandcrowdfundingin

the contextof the startuplife cycle. As a result,

startupsconsideringcrowdfundinghavelittle guid-

anceon howto decideamongthe differenttypesof

crowdfundingavailableand the benefitseach type

can offer in different startup stages. This is an

importantconsiderationsince fundingneeds vary

significantlyacrossstages,asdo the typesof returns

and assurancesoffered to a crowd in different

crowdfundingvariants.

Thisarticleclosesthe researchgapbyelucidating

which crowdfundingtype is most appropriatefor

startupsin each life cycle stage.It first lays out a

typologyof crowdfunding,the benefitscrowdfund-

ing offers in terms of financialand nonmonetary

resourceprovision,and how thesetwo aspectsin-

tersect. This leads to a frameworkfor decision

making,enablingthe startupto choosethe crowd-

fundingtype best suited for its specificlife cycle

stage.Once crowdfundingalternativesare consid-

eredanda choicehasbeenmade,startupsface the

next problem:how to attract a crowdand its con-

tributions.This article addressesthis by outlining

bestpracticesfor crowdfundingalternativesat each

stage.

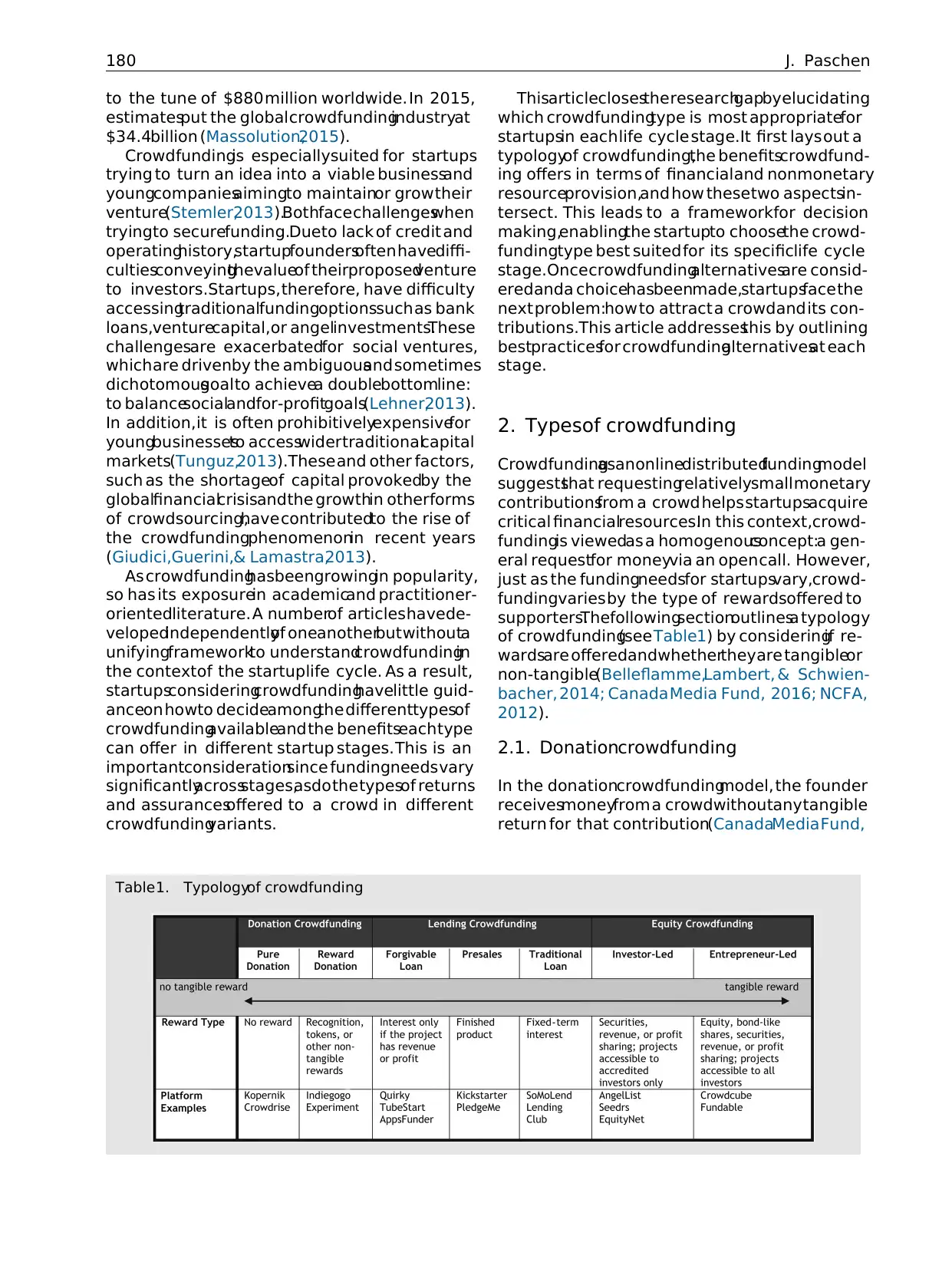

2. Typesof crowdfunding

Crowdfundingasanonlinedistributedfundingmodel

suggeststhat requestingrelativelysmall monetary

contributionsfrom a crowd helps startupsacquire

critical financialresources.In this context,crowd-

fundingis viewedas a homogenousconcept:a gen-

eral requestfor moneyvia an open call. However,

just as the fundingneedsfor startupsvary,crowd-

fundingvaries by the type of rewardsoffered to

supporters.Thefollowingsectionoutlinesa typology

of crowdfunding(see Table1) by consideringif re-

wardsare offeredandwhethertheyare tangibleor

non-tangible(Belleflamme,Lambert, & Schwien-

bacher, 2014; Canada Media Fund, 2016; NCFA,

2012).

2.1. Donationcrowdfunding

In the donationcrowdfundingmodel, the founder

receivesmoneyfrom a crowdwithoutany tangible

return for that contribution(CanadaMedia Fund,

Table 1. Typologyof crowdfunding

180 J. Paschen

estimatesput the global crowdfundingindustryat

$34.4billion (Massolution,2015).

Crowdfundingis especiallysuited for startups

trying to turn an idea into a viable businessand

youngcompaniesaimingto maintainor grow their

venture(Stemler,2013).Bothface challengeswhen

tryingto securefunding.Dueto lack of credit and

operatinghistory,startupfoundersoften havediffi-

cultiesconveyingthevalueof theirproposedventure

to investors.Startups, therefore, have difficulty

accessingtraditionalfundingoptionssuch as bank

loans,venturecapital,or angelinvestments.These

challengesare exacerbatedfor social ventures,

which are drivenby the ambiguousand sometimes

dichotomousgoal to achievea doublebottomline:

to balancesocialandfor-profitgoals(Lehner,2013).

In addition,it is often prohibitivelyexpensivefor

youngbusinessesto accesswidertraditionalcapital

markets(Tunguz,2013).These and other factors,

such as the shortageof capital provokedby the

globalfinancialcrisisand the growthin otherforms

of crowdsourcing,have contributedto the rise of

the crowdfundingphenomenonin recent years

(Giudici,Guerini,& Lamastra,2013).

As crowdfundinghasbeengrowingin popularity,

so has its exposurein academicand practitioner-

orientedliterature. A numberof articles havede-

velopedindependentlyof oneanotherbut withouta

unifyingframeworkto understandcrowdfundingin

the contextof the startuplife cycle. As a result,

startupsconsideringcrowdfundinghavelittle guid-

anceon howto decideamongthe differenttypesof

crowdfundingavailableand the benefitseach type

can offer in different startup stages. This is an

importantconsiderationsince fundingneeds vary

significantlyacrossstages,asdo the typesof returns

and assurancesoffered to a crowd in different

crowdfundingvariants.

Thisarticleclosesthe researchgapbyelucidating

which crowdfundingtype is most appropriatefor

startupsin each life cycle stage.It first lays out a

typologyof crowdfunding,the benefitscrowdfund-

ing offers in terms of financialand nonmonetary

resourceprovision,and how thesetwo aspectsin-

tersect. This leads to a frameworkfor decision

making,enablingthe startupto choosethe crowd-

fundingtype best suited for its specificlife cycle

stage.Once crowdfundingalternativesare consid-

eredanda choicehasbeenmade,startupsface the

next problem:how to attract a crowdand its con-

tributions.This article addressesthis by outlining

bestpracticesfor crowdfundingalternativesat each

stage.

2. Typesof crowdfunding

Crowdfundingasanonlinedistributedfundingmodel

suggeststhat requestingrelativelysmall monetary

contributionsfrom a crowd helps startupsacquire

critical financialresources.In this context,crowd-

fundingis viewedas a homogenousconcept:a gen-

eral requestfor moneyvia an open call. However,

just as the fundingneedsfor startupsvary,crowd-

fundingvaries by the type of rewardsoffered to

supporters.Thefollowingsectionoutlinesa typology

of crowdfunding(see Table1) by consideringif re-

wardsare offeredandwhethertheyare tangibleor

non-tangible(Belleflamme,Lambert, & Schwien-

bacher, 2014; Canada Media Fund, 2016; NCFA,

2012).

2.1. Donationcrowdfunding

In the donationcrowdfundingmodel, the founder

receivesmoneyfrom a crowdwithoutany tangible

return for that contribution(CanadaMedia Fund,

Table 1. Typologyof crowdfunding

180 J. Paschen

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2016;NCFA,2012).In the pure donationmodel,no

rewardsat all are offeredto contributors.Thefunds

receivedare essentiallya grantgivenfor a specific

purpose,but withoutthe expectationof a specific

return to the funder.Accordingto a 2015industry

reportby Massolutions,donationcrowdfundinggen-

erates the second-largestfundingvolumeglobally

(NCFA,2015)andthe ideaof donationcrowdfunding

hasbeensuccessfullyutilizedin socialmarketingfor

a numberof years(Lehner& Nicholls,2014).

The rewards-baseddonationmodel employsan

incentivesystemwherebybackersreceivenonmon-

etary rewardsthat includepersonalrecognitionor

experientialrewards, such as the opportunityto

meet the creators,attend specialevents,or even

to participatein the creationof the product.Dona-

tion crowdfundingis morepopularfor projectswith

smaller funding goals; globally, 90%of donation

crowdfundingcampaignsraised less than $10,000

(NCFA,2012).

2.2. Lendingcrowdfunding

Lendingcrowdfunding,oftenreferredto aspeer-to-

business(P2B)or peer-to-peer(P2P)crowdfunding,

raises moneywith the expectationthat founders

will repaysupporters.Lendingcrowdfundingis the

largestcrowdfundingtypebyfundingvolume(NCFA,

2015)andtakesoneof threeforms:(1) the presales

model,(2) thetraditionallendingmodel,and(3) the

forgivableloan (NCFA,2012).The presalesmodel

offersthe finishedproductin returnfor the contrib-

utor’s pledge; the contributionamountrequested

from each crowd memberis determinedby an as-

sessmentof the fair marketvalue of the product.

How many presale copies the founder offers de-

pendson the funder’stotal contributionamount–—

larger contributionstypically mean a supporter

receives more copies (NCFA, 2012). The first-

generationPebble smartwatchis amongthe most

well-known presale campaigns.It raised more

than $10 million from nearly 70,000 funders on

Kickstarter,more than 100 times its fundinggoal,

and Pebble delivered its first round of watches

10 months after the campaignended (Schroter,

2014).Thetraditionallendingagreementusesstan-

dard terms where loans are repaid with interest

determinedpre-campaignlaunch. The forgivable

loan repays contributionsonly if and when the

project beginsto generaterevenueor profit. With

boththe traditionalandforgivableloan,crowdfund-

ing projects are assessedaccordingto their risk

levels–—eitherby the platformitself or by a third-

party evaluator.Lenderschoosethe level of risk

they are preparedto accept and supportprojects

accordingly.

2.3. Equity crowdfunding

In the equitycrowdfundingmodel,also referredto

as investmentcrowdfunding,the venture raises

moneyfrom a crowdin exchangefor an ownership

stake in the firm. That is, investorsare offered

equity or bond-like shares (Ahlers, Cumming,

Guenther,& Schweizer,2015).Equitycrowdfunding

is the fastest growingcrowdfundingcategoryand

the averagecampaignvalue is high.1 Investor-led

equity crowdfundingtypically involvesaccredited

investors,suchas venturecapitalists,angelinves-

tors, or sector specialistswho negotiatewith the

founderon fundingterms.Theseprojectsare then

promotedto accreditedinvestorsvia platformsthat

are often subscription-only(Wagner, 2014). In

entrepreneur-ledequity crowdfunding,campaigns

are accessibleto all crowd investorsand the cam-

paignproponentsetsthe valuationsanddetermines

the termsof the offering.

3. Benefitsof crowdfundingfor

startups

The previous section introduced a typology of

crowdfundingthat considersthe type of return or

rewardto backers.While this is an importantfirst

aspectto understand,a startupalso needsto con-

sider the specific benefits it aims to achieve in

pursuingcrowdfundingefforts. First, crowdfunding

helps alleviate the capital crunch many startups

face. Manycampaignsaimto raisea relativelysmall

sumof moneyfor a one-timeprojector event(Mollick

& Kuppuswamy,2016).Otherprojectsintendto raise

a substantialamountof moneyfor more complex

andlong-termundertakings,providingfounderswith

the funds to turn an idea into a viable business

(Mollick,2014).Thismethodworks;9 in 10successful

projectsonKickstarterhaveturnedintoongoingfirms

and existed up to 3 years later (Painter,2014).

However,crowdfundingin a startupcontextis not

just aboutfunding;it alsooffersnonmonetarybene-

fits that encompassthe following (Belleflamme,

Lambert,& Schwienbacher,2010;Brown, Boon, &

Pitt, 2017;Gerber& Hui, 2013;Mollick,2014):

Validatingthe overall businessidea–—Doesthe

idea actually solve a consumerproblem(prob-

lem/solutionvalidation)?

Refiningthe product or service with potential

customersby receiving their feedback, likes,

1 About175,000in North America(CanadaMediaFund, 2015)

Choosewisely:Crowdfundingthroughthe stagesof the startuplife cycle 181

rewardsat all are offeredto contributors.Thefunds

receivedare essentiallya grantgivenfor a specific

purpose,but withoutthe expectationof a specific

return to the funder.Accordingto a 2015industry

reportby Massolutions,donationcrowdfundinggen-

erates the second-largestfundingvolumeglobally

(NCFA,2015)andthe ideaof donationcrowdfunding

hasbeensuccessfullyutilizedin socialmarketingfor

a numberof years(Lehner& Nicholls,2014).

The rewards-baseddonationmodel employsan

incentivesystemwherebybackersreceivenonmon-

etary rewardsthat includepersonalrecognitionor

experientialrewards, such as the opportunityto

meet the creators,attend specialevents,or even

to participatein the creationof the product.Dona-

tion crowdfundingis morepopularfor projectswith

smaller funding goals; globally, 90%of donation

crowdfundingcampaignsraised less than $10,000

(NCFA,2012).

2.2. Lendingcrowdfunding

Lendingcrowdfunding,oftenreferredto aspeer-to-

business(P2B)or peer-to-peer(P2P)crowdfunding,

raises moneywith the expectationthat founders

will repaysupporters.Lendingcrowdfundingis the

largestcrowdfundingtypebyfundingvolume(NCFA,

2015)andtakesoneof threeforms:(1) the presales

model,(2) thetraditionallendingmodel,and(3) the

forgivableloan (NCFA,2012).The presalesmodel

offersthe finishedproductin returnfor the contrib-

utor’s pledge; the contributionamountrequested

from each crowd memberis determinedby an as-

sessmentof the fair marketvalue of the product.

How many presale copies the founder offers de-

pendson the funder’stotal contributionamount–—

larger contributionstypically mean a supporter

receives more copies (NCFA, 2012). The first-

generationPebble smartwatchis amongthe most

well-known presale campaigns.It raised more

than $10 million from nearly 70,000 funders on

Kickstarter,more than 100 times its fundinggoal,

and Pebble delivered its first round of watches

10 months after the campaignended (Schroter,

2014).Thetraditionallendingagreementusesstan-

dard terms where loans are repaid with interest

determinedpre-campaignlaunch. The forgivable

loan repays contributionsonly if and when the

project beginsto generaterevenueor profit. With

boththe traditionalandforgivableloan,crowdfund-

ing projects are assessedaccordingto their risk

levels–—eitherby the platformitself or by a third-

party evaluator.Lenderschoosethe level of risk

they are preparedto accept and supportprojects

accordingly.

2.3. Equity crowdfunding

In the equitycrowdfundingmodel,also referredto

as investmentcrowdfunding,the venture raises

moneyfrom a crowdin exchangefor an ownership

stake in the firm. That is, investorsare offered

equity or bond-like shares (Ahlers, Cumming,

Guenther,& Schweizer,2015).Equitycrowdfunding

is the fastest growingcrowdfundingcategoryand

the averagecampaignvalue is high.1 Investor-led

equity crowdfundingtypically involvesaccredited

investors,suchas venturecapitalists,angelinves-

tors, or sector specialistswho negotiatewith the

founderon fundingterms.Theseprojectsare then

promotedto accreditedinvestorsvia platformsthat

are often subscription-only(Wagner, 2014). In

entrepreneur-ledequity crowdfunding,campaigns

are accessibleto all crowd investorsand the cam-

paignproponentsetsthe valuationsanddetermines

the termsof the offering.

3. Benefitsof crowdfundingfor

startups

The previous section introduced a typology of

crowdfundingthat considersthe type of return or

rewardto backers.While this is an importantfirst

aspectto understand,a startupalso needsto con-

sider the specific benefits it aims to achieve in

pursuingcrowdfundingefforts. First, crowdfunding

helps alleviate the capital crunch many startups

face. Manycampaignsaimto raisea relativelysmall

sumof moneyfor a one-timeprojector event(Mollick

& Kuppuswamy,2016).Otherprojectsintendto raise

a substantialamountof moneyfor more complex

andlong-termundertakings,providingfounderswith

the funds to turn an idea into a viable business

(Mollick,2014).Thismethodworks;9 in 10successful

projectsonKickstarterhaveturnedintoongoingfirms

and existed up to 3 years later (Painter,2014).

However,crowdfundingin a startupcontextis not

just aboutfunding;it alsooffersnonmonetarybene-

fits that encompassthe following (Belleflamme,

Lambert,& Schwienbacher,2010;Brown, Boon, &

Pitt, 2017;Gerber& Hui, 2013;Mollick,2014):

Validatingthe overall businessidea–—Doesthe

idea actually solve a consumerproblem(prob-

lem/solutionvalidation)?

Refiningthe product or service with potential

customersby receiving their feedback, likes,

1 About175,000in North America(CanadaMediaFund, 2015)

Choosewisely:Crowdfundingthroughthe stagesof the startuplife cycle 181

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

and dislikes(productvalidation).In this context,

crowdfunding is a means to support user-

generated innovation and a way to better

understandcustomerpreferences.

Paintinganaccuratepictureof howa newproduct

will perform before officially going to market

(marketvalidation),thusallowingstartupsto fail

early withoutinvestingadditionaltime or money

if they see little interestfrom a crowd.

Marketing,such as promotinga product or a

direct sales channelby providingbackerswith

the finishedproductandensuringa readilyavail-

ablesalespipeline(marketpenetration/growth).

Crowdfundingfurther helps establisha loyal com-

munity of engagedcustomers.The successesof

PebbleandOuya–—avideogameconsole–—ledother

developersto write applicationsfor theseproducts

even before they were released to the market,

helpingto build a competitiveadvantage.

In summary,crowdfundingprovidescritical orga-

nizationalresourcesin the formof moneybut it also

providesnon-financialresources,or crowd capital,

an organizational-levelresourceobtainedfrom a

crowd(Prpic´, Shukla,Kietzmann,& McCarthy,2015).

4. Selectingthe best crowdfunding

type for each stage

As previouslylaid out, crowdfundingprovidesmon-

etary and non-financialresources.However,in the

prevailingview,a startupis oftenviewedasa single

construct:an individualaimingto turnanideainto a

viable businessthat requiresresources.The chal-

lengewith this viewis that it ignoresthe life cyclea

startupundergoes,whereeachlife cycle stagehas

uniquemonetaryandnonmonetaryresourceneeds.

The followingsectionaddressesthis challengeand

suggeststhat a startupcan identify the mostsuit-

able crowdfundingmethodby consideringits life

cycle stagealongwith the resourceneedsat each

stage. Adoptingthe businesslife cycle framework

proposedbyChurchillandLewis(1983),threestages

are differentiated. For each stage, key resource

requirementsare outlined along with the crowd-

funding type best suited to meet these require-

ments.

4.1. Pre-startup stage:Donation

crowdfunding

In the pre-startupstage of the crowdfundinglife

cycle, the founder has an idea and exploresthe

feasibilityof buildinga businessbasedon this idea

(Majoran,2014;MaRS,2009a).Pre-startupefforts

focuson developinga viableofferingthat solvesa

significantcustomerproblemas well as identifying

the targetmarket,partners,distributors,andcom-

petitors. In this formativephase, achievingprob-

lem/solutionfit and creatinga viablebusinessplan

are of key importance.Fundingneedsare primarily

for pre-startupR&D,producttesting,generatingthe

businessplan, and preparingto launchthe venture

(MaRS,2009a).

Donationcrowdfundingis the mostsuitabletype

to meettheseneedsfor threereasons.First, it does

not offer a tangiblerewardto a crowd. At the pre-

startupstage,whenthe venturehasnot yet gener-

atedrevenuefromthe offering,it is still developing

the businessplanandgenerallyhasno financialplan

and no track record. The risk of project failure is

highestat thisstage;therefore,the founderis not in

a positionto promisetangibleor monetaryrewards.

Second,donationcrowdfundingtypicallyallowsfor

more operational flexibility compared to other

forms of crowdfundingthat have more conditions

attached to the financial contributionsmade by

a crowd. Third, the common characteristicsof

donation-basedcrowdfundingprojects help keep

the risk of disappointingcrowdmemberslow. Over-

all fundinggoals and individualcontributionsare

usuallysmall.For example,a successfulKickstarter

project raisesan averageof $6,000,while the aver-

age individualcontributionis just $25 (Heyman,

2015).Donationcrowdfundingcan feasiblyprovide

the necessarycapital to movethe ventureto the

next stagein the startuplife cycle, at whichpoint

foundersshouldreevaluatefundraisingapproaches.

4.2. Startup stage:Lendingcrowdfunding

As the ventureentersthe startupstage,it hasascer-

tainedthefeasibilityof theideaandthecredibilityof

the businessmodel to deliver the offering to an

attractive target market (Majoran, 2014; MaRS,

2009b).Effortsnowfocuson refiningthe solutionor

prototypeintoa minimumviableproductandadvanc-

ing the initial revenuemodelinto a viablebusiness

plan(Moogk,2012).Keyconcernsin thestartupstage

arevalidatingproduct/marketfit. Doestheproductor

servicedeliveron customers’needs(productvalida-

tion)? Are prospectivecustomersand distribution

partnerswilling to purchasethe productwhenit is

ready for commercialoffering and at what price

(marketvalidation)?Howcanthestartupexpandfrom

that one key customersegmentto a broaderand

sustainablesalesbase?(Churchill& Lewis,1983).

Resourcesin the startup phaseare requiredto

build productsfor prospectivecustomersto test,

182 J. Paschen

crowdfunding is a means to support user-

generated innovation and a way to better

understandcustomerpreferences.

Paintinganaccuratepictureof howa newproduct

will perform before officially going to market

(marketvalidation),thusallowingstartupsto fail

early withoutinvestingadditionaltime or money

if they see little interestfrom a crowd.

Marketing,such as promotinga product or a

direct sales channelby providingbackerswith

the finishedproductandensuringa readilyavail-

ablesalespipeline(marketpenetration/growth).

Crowdfundingfurther helps establisha loyal com-

munity of engagedcustomers.The successesof

PebbleandOuya–—avideogameconsole–—ledother

developersto write applicationsfor theseproducts

even before they were released to the market,

helpingto build a competitiveadvantage.

In summary,crowdfundingprovidescritical orga-

nizationalresourcesin the formof moneybut it also

providesnon-financialresources,or crowd capital,

an organizational-levelresourceobtainedfrom a

crowd(Prpic´, Shukla,Kietzmann,& McCarthy,2015).

4. Selectingthe best crowdfunding

type for each stage

As previouslylaid out, crowdfundingprovidesmon-

etary and non-financialresources.However,in the

prevailingview,a startupis oftenviewedasa single

construct:an individualaimingto turnanideainto a

viable businessthat requiresresources.The chal-

lengewith this viewis that it ignoresthe life cyclea

startupundergoes,whereeachlife cycle stagehas

uniquemonetaryandnonmonetaryresourceneeds.

The followingsectionaddressesthis challengeand

suggeststhat a startupcan identify the mostsuit-

able crowdfundingmethodby consideringits life

cycle stagealongwith the resourceneedsat each

stage. Adoptingthe businesslife cycle framework

proposedbyChurchillandLewis(1983),threestages

are differentiated. For each stage, key resource

requirementsare outlined along with the crowd-

funding type best suited to meet these require-

ments.

4.1. Pre-startup stage:Donation

crowdfunding

In the pre-startupstage of the crowdfundinglife

cycle, the founder has an idea and exploresthe

feasibilityof buildinga businessbasedon this idea

(Majoran,2014;MaRS,2009a).Pre-startupefforts

focuson developinga viableofferingthat solvesa

significantcustomerproblemas well as identifying

the targetmarket,partners,distributors,andcom-

petitors. In this formativephase, achievingprob-

lem/solutionfit and creatinga viablebusinessplan

are of key importance.Fundingneedsare primarily

for pre-startupR&D,producttesting,generatingthe

businessplan, and preparingto launchthe venture

(MaRS,2009a).

Donationcrowdfundingis the mostsuitabletype

to meettheseneedsfor threereasons.First, it does

not offer a tangiblerewardto a crowd. At the pre-

startupstage,whenthe venturehasnot yet gener-

atedrevenuefromthe offering,it is still developing

the businessplanandgenerallyhasno financialplan

and no track record. The risk of project failure is

highestat thisstage;therefore,the founderis not in

a positionto promisetangibleor monetaryrewards.

Second,donationcrowdfundingtypicallyallowsfor

more operational flexibility compared to other

forms of crowdfundingthat have more conditions

attached to the financial contributionsmade by

a crowd. Third, the common characteristicsof

donation-basedcrowdfundingprojects help keep

the risk of disappointingcrowdmemberslow. Over-

all fundinggoals and individualcontributionsare

usuallysmall.For example,a successfulKickstarter

project raisesan averageof $6,000,while the aver-

age individualcontributionis just $25 (Heyman,

2015).Donationcrowdfundingcan feasiblyprovide

the necessarycapital to movethe ventureto the

next stagein the startuplife cycle, at whichpoint

foundersshouldreevaluatefundraisingapproaches.

4.2. Startup stage:Lendingcrowdfunding

As the ventureentersthe startupstage,it hasascer-

tainedthefeasibilityof theideaandthecredibilityof

the businessmodel to deliver the offering to an

attractive target market (Majoran, 2014; MaRS,

2009b).Effortsnowfocuson refiningthe solutionor

prototypeintoa minimumviableproductandadvanc-

ing the initial revenuemodelinto a viablebusiness

plan(Moogk,2012).Keyconcernsin thestartupstage

arevalidatingproduct/marketfit. Doestheproductor

servicedeliveron customers’needs(productvalida-

tion)? Are prospectivecustomersand distribution

partnerswilling to purchasethe productwhenit is

ready for commercialoffering and at what price

(marketvalidation)?Howcanthestartupexpandfrom

that one key customersegmentto a broaderand

sustainablesalesbase?(Churchill& Lewis,1983).

Resourcesin the startup phaseare requiredto

build productsfor prospectivecustomersto test,

182 J. Paschen

hire employees,manageoperations,establishthe

productin the market,and executethe marketing

planfor commerciallaunch(Hofstrand,2013;MaRS,

2009b). Lending crowdfundingis best suited for

venturesin this stage.Havingbuilt a viableproduct

that has gone througha few iteration cycles and

having generated some initial revenue demon-

stratesearlytraction,puttingthe startupin a stron-

ger position to credibly offer tangible rewards

such as monetaryinterest or a presalesproduct.

In addition, a key goal in the startupstageis to

validateproduct/marketfit. Thelendingmodelhelps

to achievethis goalby providinga real-lifeestimate

of demandandcustomers’willingnessto pay,partic-

ularlyin the caseof the presalesmodel.It alsobuilds

an initial group of excited early adopters,which

createsa competitiveadvantagefor the business.

Finally,the startupstagerequiressubstantiallymore

fundingthanthepre-startupstage(Hofstrand,2013).

P2P or P2Blendingplatformsoften requirea higher

minimumloan amountfrom eachbacker.The mini-

mumloanamountonLendingClub,a P2Pplatform,is

$5,000and FundingCircle requiresan even higher

minimuminvestmentof $25,000(Herrick, 2016).

Lendingcrowdfundingalignswell with this needfor

highercapitalamounts.

4.3. Growth stage:Equity crowdfunding

The growthstagetypicallybeginswhenthe startup

hasbecomean efficient,profitableentity.The ven-

ture is financiallyhealthy,has sufficientsize and

marketpenetration,and hasachievedproductand

marketvalidation.Startupactivitiesfocuson scal-

ing operations,processes,and systemsto, at a

minimum,remainprofitablebut preferablyto grow

and earnan above-averageeconomicreturnon the

resourcesemployed(Churchill& Lewis, 1983;Ma-

joran, 2014).As the startuptransitionsinto expan-

sion, it has demonstratedstrong growth that is

expectedto continue. Funds raised at this stage

areusedto supportfurthergrowthandmayhelpthe

startup acquire another companyas a way to

achievescale or to provide liquidity and an exit

for the founder(MaRS,2013).

Equity crowdfunding,which offers a financial

return to backers,is the most appropriatecrowd-

funding type for the growth stage. The capital

necessaryto scaleandgrowthe businessis typically

high and often unattainableby the donation or

lendingcrowdfundingmodels.The averagefunding

amount for an equity crowdfundingcampaignis

higher,makingthis type more suitablethan other

models(Sandlund,2013).At this stage,the venture

is able to demonstratesuccess and can pitch

its funding requeststo prospectivebackerswith

objectivelyverifiableinformation,suchas financial

data or informationabout its customerbase. The

risk of failure for the ventureis lower than at its

beginningand the startupis, in turn, able to offer

monetaryrewardsmore credibly.This crowdfund-

ing model fits well at this stageas growth means

an opportunityfor organizationalchange and a

shift of power.The founderand the businesshave

becomereasonablyseparate;the startupis decen-

tralized and often organized by key functions

(Churchill & Lewis, 1983). Thus, the founder is

typicallymore open to the idea of givingup some

ownershipandcontrolof the business–—aninherent

requirementof equity crowdfunding–—duringthe

growthphase.

5. Best practiceson how to attract a

crowd and its contributions

Aslaid out in the previoussection,startupsare able

to identifythe mostsuitablecrowdfundingtype by

consideringtheir specificlife cycle stage and re-

source requirements.Once the choice of crowd-

fundingtype is made, campaignproponentsface

the next challenge,whichis how to attract people

and their contributions.Crowdfundingis a transac-

tionalrelationshipbetweenfounderandfunder.The

informationasymmetrybetweenthesetwo parties

makesthis relationshipimbalancedand inefficient,

likelyimpedingthe outcome(McCarthy,Silvestre,&

Kietzmann,2013).Usingcue utilizationas a theo-

reticallens,thissectionprovidespracticalguidance

on howstartupscancommunicatethe valueof their

proposedendeavorto crowdmembers.

Cue utilizationtheory(Olson,1972)positsthat,

whenfaced with ambiguityaboutthe qualityof an

entity(person,product,firm, institution),individu-

als use surrogateinformationto make inferences

about the entity’s quality (Bahadir,DeKinder,&

Kohli, 2014). Firms can influencethis assessment

processby sendingsignalsor cuesthat conveythe

quality desiredby the firm. Signalsare definedas

the informationunder the direct control of the

entity, such as its own publishedinformationor

certificationsto acceptedstandards.Cues, on the

other hand, consist of informationthat includes

signalsas well as additionalinformationavailable

throughthirdpartiesor the generalenvironment.As

such,cuesare not alwaysdirectlyunderthe control

of the entity.A youngfirmin aninitial publicoffering

(IPO) may staff its board with a diversegroup of

esteemeddirectorsto conveyits legitimacyto in-

vestors. This, along with audited and regulated

statementsthat are part of the IPO process,encom-

passesthe signals.If news outlets or social media

Choosewisely:Crowdfundingthroughthe stagesof the startuplife cycle 183

productin the market,and executethe marketing

planfor commerciallaunch(Hofstrand,2013;MaRS,

2009b). Lending crowdfundingis best suited for

venturesin this stage.Havingbuilt a viableproduct

that has gone througha few iteration cycles and

having generated some initial revenue demon-

stratesearlytraction,puttingthe startupin a stron-

ger position to credibly offer tangible rewards

such as monetaryinterest or a presalesproduct.

In addition, a key goal in the startupstageis to

validateproduct/marketfit. Thelendingmodelhelps

to achievethis goalby providinga real-lifeestimate

of demandandcustomers’willingnessto pay,partic-

ularlyin the caseof the presalesmodel.It alsobuilds

an initial group of excited early adopters,which

createsa competitiveadvantagefor the business.

Finally,the startupstagerequiressubstantiallymore

fundingthanthepre-startupstage(Hofstrand,2013).

P2P or P2Blendingplatformsoften requirea higher

minimumloan amountfrom eachbacker.The mini-

mumloanamountonLendingClub,a P2Pplatform,is

$5,000and FundingCircle requiresan even higher

minimuminvestmentof $25,000(Herrick, 2016).

Lendingcrowdfundingalignswell with this needfor

highercapitalamounts.

4.3. Growth stage:Equity crowdfunding

The growthstagetypicallybeginswhenthe startup

hasbecomean efficient,profitableentity.The ven-

ture is financiallyhealthy,has sufficientsize and

marketpenetration,and hasachievedproductand

marketvalidation.Startupactivitiesfocuson scal-

ing operations,processes,and systemsto, at a

minimum,remainprofitablebut preferablyto grow

and earnan above-averageeconomicreturnon the

resourcesemployed(Churchill& Lewis, 1983;Ma-

joran, 2014).As the startuptransitionsinto expan-

sion, it has demonstratedstrong growth that is

expectedto continue. Funds raised at this stage

areusedto supportfurthergrowthandmayhelpthe

startup acquire another companyas a way to

achievescale or to provide liquidity and an exit

for the founder(MaRS,2013).

Equity crowdfunding,which offers a financial

return to backers,is the most appropriatecrowd-

funding type for the growth stage. The capital

necessaryto scaleandgrowthe businessis typically

high and often unattainableby the donation or

lendingcrowdfundingmodels.The averagefunding

amount for an equity crowdfundingcampaignis

higher,makingthis type more suitablethan other

models(Sandlund,2013).At this stage,the venture

is able to demonstratesuccess and can pitch

its funding requeststo prospectivebackerswith

objectivelyverifiableinformation,suchas financial

data or informationabout its customerbase. The

risk of failure for the ventureis lower than at its

beginningand the startupis, in turn, able to offer

monetaryrewardsmore credibly.This crowdfund-

ing model fits well at this stageas growth means

an opportunityfor organizationalchange and a

shift of power.The founderand the businesshave

becomereasonablyseparate;the startupis decen-

tralized and often organized by key functions

(Churchill & Lewis, 1983). Thus, the founder is

typicallymore open to the idea of givingup some

ownershipandcontrolof the business–—aninherent

requirementof equity crowdfunding–—duringthe

growthphase.

5. Best practiceson how to attract a

crowd and its contributions

Aslaid out in the previoussection,startupsare able

to identifythe mostsuitablecrowdfundingtype by

consideringtheir specificlife cycle stage and re-

source requirements.Once the choice of crowd-

fundingtype is made, campaignproponentsface

the next challenge,whichis how to attract people

and their contributions.Crowdfundingis a transac-

tionalrelationshipbetweenfounderandfunder.The

informationasymmetrybetweenthesetwo parties

makesthis relationshipimbalancedand inefficient,

likelyimpedingthe outcome(McCarthy,Silvestre,&

Kietzmann,2013).Usingcue utilizationas a theo-

reticallens,thissectionprovidespracticalguidance

on howstartupscancommunicatethe valueof their

proposedendeavorto crowdmembers.

Cue utilizationtheory(Olson,1972)positsthat,

whenfaced with ambiguityaboutthe qualityof an

entity(person,product,firm, institution),individu-

als use surrogateinformationto make inferences

about the entity’s quality (Bahadir,DeKinder,&

Kohli, 2014). Firms can influencethis assessment

processby sendingsignalsor cuesthat conveythe

quality desiredby the firm. Signalsare definedas

the informationunder the direct control of the

entity, such as its own publishedinformationor

certificationsto acceptedstandards.Cues, on the

other hand, consist of informationthat includes

signalsas well as additionalinformationavailable

throughthirdpartiesor the generalenvironment.As

such,cuesare not alwaysdirectlyunderthe control

of the entity.A youngfirmin aninitial publicoffering

(IPO) may staff its board with a diversegroup of

esteemeddirectorsto conveyits legitimacyto in-

vestors. This, along with audited and regulated

statementsthat are part of the IPO process,encom-

passesthe signals.If news outlets or social media

Choosewisely:Crowdfundingthroughthe stagesof the startuplife cycle 183

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

pickedup on the compositionof the boardand the

past successesof its members,interestedparties

could receivecues.

5.1. Harnessingcues and signalsfor

donationcrowdfunding

5.1.1. Choosea specializedplatform and all-

or-nothingpayout model

The centraltenetof donationcrowdfundingis thatit

does not offer tangiblerewardsto backers.This

meansthe founderneedsto communicatethe value

of theprojectin nonmonetaryterms.Crowdmembers

mustbe convincedthatthecausetheyarecontribut-

ingto isworthyof theirsupport.Inthiscontext,dueto

the fact that the ventureis in the pre-startupphase,

there are few objectivelyverifiablesignalsat the

founder’sdisposal.The choiceof platformis one of

the strongest,signalinga specializationandaddress-

ing a particularcrowdthat is drawnto the chosen

platform.CrowdfundingonQuirkyindicatesa product

focus(e.g., a collapsibleyogamat)andan invitation

to participatein theactualdevelopmentof theprod-

uct. UsingStartsomegood,on the otherhand,signals

that the projectendeavorsto contributetowardthe

social goodof society(e.g., a campaignto fund a

WorldPeaceandPrayerDay).

In addition,employingthe all-or-nothingmodel

signalsto a crowdthatthestartupis committedto the

projectandwill onlyproceedif the requiredthresh-

old is met (Cumming,Leboeuf, & Schwienbacher,

2014).In the all-or-nothing(or fixedfunding)payout

model,the creatoronlyreceivesfundsif the funding

goalis met or surpassedduringthe campaignperiod

(Kickstarter,2016), while in the keep-what-you-

earned(orflexiblefunding)model,thefounderkeeps

all funds raised. Empiricalevidencesuggeststhat

campaignsemployingthe all-or-nothingmodel are

moresuccessfulin achievingtheir fundinggoaland

outperformprojectsusingtheflexiblefundingmodel

withrespectto thenumberof supportersattractedto

their campaigns(Kolenda,2016).

5.1.2. Be transparentand accountable

The secondsuggestedbest practiceincludesa de-

tailedbreakdownof whatthe investedfundswill be

used for. This reducesthe informationasymmetry

betweenfoundersand crowdmembersby signaling

that contributionsareindeedmakinga differencein

the project being supported.In the case of pure

donationcrowdfunding,the necessityof sendinga

strongsignalof accountabilityhasbeenrecognized

in scientificliteratureon charitablegiving(Murphy,

n.d.). There is a strongconsensusthat by keeping

donorsinformedabouttheir contribution’simpact,

organizationsimprovetheir fundraisingoutcomes

(Blackbaud,2012),especiallyif they demonstrate

that donationsgo to the core cause rather than

towardoverheadcosts(Prior,2014).The bandPro-

testthe HerocrowdfundedanalbumviaIndiegogoin

2013.Not onlydid the bandincludean itemizedlist

of expensesin its pitch, but alsomemberswerevery

explicit about their motivationto do so in their

campaigndescription (Protest the Hero, 2013).

Thecampaignendedwith a total of $341,146raised,

exceedingthe target by 173%.

5.1.3. Publicize backer information

Anotherbestpracticeis the publicationof supporter

details. This practice makes the project appear

more relatable (Kolenda, 2016), which has been

shownas a successfactor in charitablegivingand

donations(Karlan & List, 2007;Leonhardt,2008).

The charity:water crowdfundingcampaign pro-

motessupporterswith elaborateeditorial content

and illustrates the importanceof being able to

relate. In a prominentexample,RachelBeckwith,

a girl from Washingtonstate, set out to raise $300

for charity:waterby foregoinggifts for her ninth

birthday(Beckwith,2011).While her initial cam-

paignfell shortof her goal,her tragicdeathin a car

accidentled to a revivalof her campaignthat has

raisedmorethan $1.2 million to date.

This examplealso illustratesthe opportunityto

trigger herd behavior,which is the tendencyfor

individualsto mimic the actionsof a larger group

(Phung, 2007). Herd behaviormay be causedby

social pressureof conformityor by the common

rationale that it is unlikely such a large group

could be wrong.Herd behaviorrepresentsan indi-

rectly controllablecue for the startupthat is con-

tributingsignificantlyto a crowdfundingcampaign’s

success.It is estimatedthat four investorscontrib-

uting $1 each will trigger anotherthree investors

to do the same, for no other reasonthan having

seen others engagedwith the project (Estrin &

Khavul,2016).

5.2. Harnessingcues and signalsfor

lendingcrowdfunding

5.2.1. Offer tangiblerewards

Lendingcrowdfundingrequiresthestartupto signala

reliable ability to compensatean investingcrowd.

Oneof the potentialrewardformshereis monetary

interest.Thisis a slightvariationof traditionaldebt

fundingwhereestablishedmeasurescanbe brought

to bear.The DutchplatformTailWindCrowd,for ex-

ample,publishestheriskprofilescoreandthird-party

assessmentsunderlyingthe fair interest that the

founderoffers to a crowd (TailwindCrowd, 2016).

The startup founder can use this score and the

184 J. Paschen

past successesof its members,interestedparties

could receivecues.

5.1. Harnessingcues and signalsfor

donationcrowdfunding

5.1.1. Choosea specializedplatform and all-

or-nothingpayout model

The centraltenetof donationcrowdfundingis thatit

does not offer tangiblerewardsto backers.This

meansthe founderneedsto communicatethe value

of theprojectin nonmonetaryterms.Crowdmembers

mustbe convincedthatthecausetheyarecontribut-

ingto isworthyof theirsupport.Inthiscontext,dueto

the fact that the ventureis in the pre-startupphase,

there are few objectivelyverifiablesignalsat the

founder’sdisposal.The choiceof platformis one of

the strongest,signalinga specializationandaddress-

ing a particularcrowdthat is drawnto the chosen

platform.CrowdfundingonQuirkyindicatesa product

focus(e.g., a collapsibleyogamat)andan invitation

to participatein theactualdevelopmentof theprod-

uct. UsingStartsomegood,on the otherhand,signals

that the projectendeavorsto contributetowardthe

social goodof society(e.g., a campaignto fund a

WorldPeaceandPrayerDay).

In addition,employingthe all-or-nothingmodel

signalsto a crowdthatthestartupis committedto the

projectandwill onlyproceedif the requiredthresh-

old is met (Cumming,Leboeuf, & Schwienbacher,

2014).In the all-or-nothing(or fixedfunding)payout

model,the creatoronlyreceivesfundsif the funding

goalis met or surpassedduringthe campaignperiod

(Kickstarter,2016), while in the keep-what-you-

earned(orflexiblefunding)model,thefounderkeeps

all funds raised. Empiricalevidencesuggeststhat

campaignsemployingthe all-or-nothingmodel are

moresuccessfulin achievingtheir fundinggoaland

outperformprojectsusingtheflexiblefundingmodel

withrespectto thenumberof supportersattractedto

their campaigns(Kolenda,2016).

5.1.2. Be transparentand accountable

The secondsuggestedbest practiceincludesa de-

tailedbreakdownof whatthe investedfundswill be

used for. This reducesthe informationasymmetry

betweenfoundersand crowdmembersby signaling

that contributionsareindeedmakinga differencein

the project being supported.In the case of pure

donationcrowdfunding,the necessityof sendinga

strongsignalof accountabilityhasbeenrecognized

in scientificliteratureon charitablegiving(Murphy,

n.d.). There is a strongconsensusthat by keeping

donorsinformedabouttheir contribution’simpact,

organizationsimprovetheir fundraisingoutcomes

(Blackbaud,2012),especiallyif they demonstrate

that donationsgo to the core cause rather than

towardoverheadcosts(Prior,2014).The bandPro-

testthe HerocrowdfundedanalbumviaIndiegogoin

2013.Not onlydid the bandincludean itemizedlist

of expensesin its pitch, but alsomemberswerevery

explicit about their motivationto do so in their

campaigndescription (Protest the Hero, 2013).

Thecampaignendedwith a total of $341,146raised,

exceedingthe target by 173%.

5.1.3. Publicize backer information

Anotherbestpracticeis the publicationof supporter

details. This practice makes the project appear

more relatable (Kolenda, 2016), which has been

shownas a successfactor in charitablegivingand

donations(Karlan & List, 2007;Leonhardt,2008).

The charity:water crowdfundingcampaign pro-

motessupporterswith elaborateeditorial content

and illustrates the importanceof being able to

relate. In a prominentexample,RachelBeckwith,

a girl from Washingtonstate, set out to raise $300

for charity:waterby foregoinggifts for her ninth

birthday(Beckwith,2011).While her initial cam-

paignfell shortof her goal,her tragicdeathin a car

accidentled to a revivalof her campaignthat has

raisedmorethan $1.2 million to date.

This examplealso illustratesthe opportunityto

trigger herd behavior,which is the tendencyfor

individualsto mimic the actionsof a larger group

(Phung, 2007). Herd behaviormay be causedby

social pressureof conformityor by the common

rationale that it is unlikely such a large group

could be wrong.Herd behaviorrepresentsan indi-

rectly controllablecue for the startupthat is con-

tributingsignificantlyto a crowdfundingcampaign’s

success.It is estimatedthat four investorscontrib-

uting $1 each will trigger anotherthree investors

to do the same, for no other reasonthan having

seen others engagedwith the project (Estrin &

Khavul,2016).

5.2. Harnessingcues and signalsfor

lendingcrowdfunding

5.2.1. Offer tangiblerewards

Lendingcrowdfundingrequiresthestartupto signala

reliable ability to compensatean investingcrowd.

Oneof the potentialrewardformshereis monetary

interest.Thisis a slightvariationof traditionaldebt

fundingwhereestablishedmeasurescanbe brought

to bear.The DutchplatformTailWindCrowd,for ex-

ample,publishestheriskprofilescoreandthird-party

assessmentsunderlyingthe fair interest that the

founderoffers to a crowd (TailwindCrowd, 2016).

The startup founder can use this score and the

184 J. Paschen

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

associatedinterestset by the platformto signalthe

qualityof the proposedcampaign.

Inherentto the presalemodelof lendingcrowd-

fundingis rewardingcrowdmemberswith a tangible

productfrom the project. Pebblehasraisedrecord-

breakingamountsin both of its productreleasesby

offeringpresalesof smartwatchesthat were still in

the developmentstages(Dredge,2015).The reward

to the crowdwastwofold:(1) assuredandpreferred

access–—thefirst 100 funderscontributing$235or

morewere guaranteedworkingprototypes,and (2)

a discountedprice–—anyonecontributing$115was

assureda productionwatch,whichcomparedfavor-

ablywith the $150marketpricetag(Pape& Imbesi,

2014).The extra incentivefor early backerswas a

signalintendedto triggerthe herdeffect mentioned

earlier.

5.2.2. Detail the startupfounder’scredentials

The secondbestpracticefor lendingcrowdfundingis

the publicationof details regardingthe founder’s

background.A fundingcrowd is not only investing

in a productor an idea, but alsoin the personwhois

shepherdingthis idea fromthe pre-startupphaseto

success.With propereducationalcredentialsand a

successfultrackrecord,foundersprovetheircompe-

tency.This increasesthe probabilityof fundingsuc-

cessand is commonwith more-traditionalventure

capital funding(Hsu, 2007).This best practicehas

been widely employedby successfulcrowdfunding

campaignsin ways that are appropriatefor their

circumstances–—rangingfrom the board members

publicizedby Elio Motors(2016)as an ‘‘impressive

roster of industryicons’’in their questto build an

affordable,fuel efficientvehicleto the decadesof

beekeepingexperienceof the Flow Hive team(An-

derson,2015).

5.2.3. Frequently update a funding crowd

The third best practice involvesfrequentupdates

and communicationwith a fundingcrowd. One of

the key learningsthat the founderof the successful

Goldiebloxcampaignremarkson in her final update

on Kickstarteris that membersof a fundingcrowd

‘‘deserveto hear from us more’’ (Sterling,2013).

Goldiebloxhad developedThe EngineeringToy for

Girls and receivedfundingfrom manybackerswho

were promisedthe finishedproduct. Whendelays

occurred,communicationto supporterswas a key

tool usedto ensurethat the supportbaseremained

committedto the project. Commentsposted to

Goldieblox’supdatesindicatethat the transparency

and accountabilitywere viewed positively,or at

least as mitigatingfactorsin negativeexperiences,

thus helping keep the crucial cues of the online

communityengagedand supportingthe project.

5.3. Harnessingcues and signalsfor

equity crowdfunding

5.3.1. Provide third-party verifiable reports

Thefirstbestpracticefor equitycrowdfundingis the

useof third-partyverifiableinformation.Regulatory

requirementsfor equitycrowdfunding,suchas im-

plementationguidelinesfor the U.S. JOBS Act and

regulationsin Canada,mandatedifferent levelsof

financialdisclosurefor companiesof differentsizes

(Rose,2012;Thompson,2016).The releaseof finan-

cial and other information reduces information

asymmetrybetween the startup and investors.

Startupsshould be careful, though, not to limit

the signalsto the government-mandatedminimum

disclosurestandards.Verifiableanddigestibleinfor-

mationonthecompanyandits keyprojectshasbeen

identifiedas a contributingfactor to equitycrowd-

funding success(Millard, 2016). One exampleof

successis Mouth(https://angel.co/mouth),an on-

line storefor U.S.-madeindiefoodandspirits,which

raised$1.1million in equityfunding.It proactively

informedsupportersof its vision,strategies,team,

andevenproductto clarifyits valuepropositionand

mitigateperceivedrisksfor potentialinvestors.

5.3.2. Attract reputable early investors

Incidentally,Mouthhas also employedthe second

bestpracticethat sendsa strongsignalto potential

investors.By publishingdata on early, reputable

investors,startupsbenefitfromthe informationcas-

cadingto subsequentpotentialinvestors.Theequity

crowdfundingplatformCrowdfunderhas embraced

this idea so thoroughlythat it displaysa featured

investoron the homepagefor eachcampaign.Fur-

thermore, some campaignsprovide significantly

more informationin investorprofiles than in the

biographiesof the startupteam. Digitzs,for exam-

ple, is a facilitator of payment processingfor

e-commercecompaniesandits campaignwasunder-

way at the time of this writing.Investorsare listed

withvaryinglevelsof detail,butprominentinvestors,

like KevinHarringtonfromthe ABCshowSharkTank,

get visibleplacementwith shortbiographiesdetail-

ing their experience(Crowdfunder,n.d.).

5.3.3. Targeta crowd that can empathize

The third best practice for equity crowdfunding

is to target a crowd that can empathizewith the

founder’snetwork,geographicalproximity,or busi-

nessaim.A founder’sindividualsocialcapital–—their

personaland businessnetwork–—hasshownto cor-

relate positivelywith successin a crowdfunding

campaign(Giudici et al., 2013). This findingwas

supportedby a studyof approximately48,500proj-

ects, whichfoundthat geographicproximityto the

Choosewisely:Crowdfundingthroughthe stagesof the startuplife cycle 185

qualityof the proposedcampaign.

Inherentto the presalemodelof lendingcrowd-

fundingis rewardingcrowdmemberswith a tangible

productfrom the project. Pebblehasraisedrecord-

breakingamountsin both of its productreleasesby

offeringpresalesof smartwatchesthat were still in

the developmentstages(Dredge,2015).The reward

to the crowdwastwofold:(1) assuredandpreferred

access–—thefirst 100 funderscontributing$235or

morewere guaranteedworkingprototypes,and (2)

a discountedprice–—anyonecontributing$115was

assureda productionwatch,whichcomparedfavor-

ablywith the $150marketpricetag(Pape& Imbesi,

2014).The extra incentivefor early backerswas a

signalintendedto triggerthe herdeffect mentioned

earlier.

5.2.2. Detail the startupfounder’scredentials

The secondbestpracticefor lendingcrowdfundingis

the publicationof details regardingthe founder’s

background.A fundingcrowd is not only investing

in a productor an idea, but alsoin the personwhois

shepherdingthis idea fromthe pre-startupphaseto

success.With propereducationalcredentialsand a

successfultrackrecord,foundersprovetheircompe-

tency.This increasesthe probabilityof fundingsuc-

cessand is commonwith more-traditionalventure

capital funding(Hsu, 2007).This best practicehas

been widely employedby successfulcrowdfunding

campaignsin ways that are appropriatefor their

circumstances–—rangingfrom the board members

publicizedby Elio Motors(2016)as an ‘‘impressive

roster of industryicons’’in their questto build an

affordable,fuel efficientvehicleto the decadesof

beekeepingexperienceof the Flow Hive team(An-

derson,2015).

5.2.3. Frequently update a funding crowd

The third best practice involvesfrequentupdates

and communicationwith a fundingcrowd. One of

the key learningsthat the founderof the successful

Goldiebloxcampaignremarkson in her final update

on Kickstarteris that membersof a fundingcrowd

‘‘deserveto hear from us more’’ (Sterling,2013).

Goldiebloxhad developedThe EngineeringToy for

Girls and receivedfundingfrom manybackerswho

were promisedthe finishedproduct. Whendelays

occurred,communicationto supporterswas a key

tool usedto ensurethat the supportbaseremained

committedto the project. Commentsposted to

Goldieblox’supdatesindicatethat the transparency

and accountabilitywere viewed positively,or at

least as mitigatingfactorsin negativeexperiences,

thus helping keep the crucial cues of the online

communityengagedand supportingthe project.

5.3. Harnessingcues and signalsfor

equity crowdfunding

5.3.1. Provide third-party verifiable reports

Thefirstbestpracticefor equitycrowdfundingis the

useof third-partyverifiableinformation.Regulatory

requirementsfor equitycrowdfunding,suchas im-

plementationguidelinesfor the U.S. JOBS Act and

regulationsin Canada,mandatedifferent levelsof

financialdisclosurefor companiesof differentsizes

(Rose,2012;Thompson,2016).The releaseof finan-

cial and other information reduces information

asymmetrybetween the startup and investors.

Startupsshould be careful, though, not to limit

the signalsto the government-mandatedminimum

disclosurestandards.Verifiableanddigestibleinfor-

mationonthecompanyandits keyprojectshasbeen

identifiedas a contributingfactor to equitycrowd-

funding success(Millard, 2016). One exampleof

successis Mouth(https://angel.co/mouth),an on-

line storefor U.S.-madeindiefoodandspirits,which

raised$1.1million in equityfunding.It proactively

informedsupportersof its vision,strategies,team,

andevenproductto clarifyits valuepropositionand

mitigateperceivedrisksfor potentialinvestors.

5.3.2. Attract reputable early investors

Incidentally,Mouthhas also employedthe second

bestpracticethat sendsa strongsignalto potential

investors.By publishingdata on early, reputable

investors,startupsbenefitfromthe informationcas-

cadingto subsequentpotentialinvestors.Theequity

crowdfundingplatformCrowdfunderhas embraced

this idea so thoroughlythat it displaysa featured

investoron the homepagefor eachcampaign.Fur-

thermore, some campaignsprovide significantly

more informationin investorprofiles than in the

biographiesof the startupteam. Digitzs,for exam-

ple, is a facilitator of payment processingfor

e-commercecompaniesandits campaignwasunder-

way at the time of this writing.Investorsare listed

withvaryinglevelsof detail,butprominentinvestors,

like KevinHarringtonfromthe ABCshowSharkTank,

get visibleplacementwith shortbiographiesdetail-

ing their experience(Crowdfunder,n.d.).

5.3.3. Targeta crowd that can empathize

The third best practice for equity crowdfunding

is to target a crowd that can empathizewith the

founder’snetwork,geographicalproximity,or busi-

nessaim.A founder’sindividualsocialcapital–—their

personaland businessnetwork–—hasshownto cor-

relate positivelywith successin a crowdfunding

campaign(Giudici et al., 2013). This findingwas

supportedby a studyof approximately48,500proj-

ects, whichfoundthat geographicproximityto the

Choosewisely:Crowdfundingthroughthe stagesof the startuplife cycle 185

founderis positivelylinkedto venturecapitalfund-

ing (Mollick,2014).The closenessto the aim of the

project can be seen in a numberof venturesthat

targeta specificcrowd,suchasFarmHill, a delivery

service for healthy lunch food operatingin the

Silicon Valley area. It raised $1 million in equity

crowdfunding,with a numberof the investorsiden-

tified as ‘foodies’ or previousinvestorsin similar

ventures(FarmHill, n.d.). Anotherexampleis Plum

(2015),whichdevelopeda wi-fi-enabledsmartlight

switchanddrewfunderswhohadextensiveprevious

experiencein successfulsmart home networking

companies.Plum exceededits $5 million equity

crowdfundinggoal.

5.4. Best practicesmini-summary

In summary,a startup should develop, maintain,

and use its personal and professionalnetworks

extensivelyin the lead up to and duringan equity

crowdfundingcampaign.Thiscontributespositively

to oneof the keysuccessfactorsfor a crowdfunding

campaign: achieving and sustainingmomentum

behindthe campaign,especiallyin the early post-

launchdays.Evidenceshowsthat oncea campaign

hits30%of its fundinggoalthe successrateclimbsto

90%,comparedto only50%after a campaignreaches

the 5%mark.Andthefasterthemomentumis gained

the better; campaignsthat reach the 30%mark

within the first week are more likely to achieve

their fundinggoals(CanadaMediaFund, 2016).

6. Final thoughtson crowdfundingfor

startups

This article offers contributionsto both the practi-

tioner and researchcommunities.For startups,it

demonstratesthat crowdfundingcan generatea

valuable organizationalresource base, primarily

throughthe acquisitionof funds, but also through

nonmonetaryresourcesin the form of learning,the

formationof crowd capital, and marketing(Brown

et al., 2017; McCarthyet al., 2013;Prpic´ et al.,

2015).But not all crowdfundingtypes are equally

suitedto supportthe variousresourcerequirements

in different life cycle stages, and neither are

all crowdfundingtypes a feasible option. When

choosingamongthe different crowdfundingtypes,

a startup needs to considerits specific lifecycle

stage, alongwith intendedcrowdfundingbenefits

like resource provision and constraintsin terms

of the type of reward it is able to offer credibly.

This article providesa frameworkto guidestartup

decisionsin this context, which is illustrated in

Figure 1.

In the pre-startupphase,organizationalresources

focus on validatingthe idea and a crowd provides

Figure 1. Frameworkfor startup crowdfunding

Startup Stage

Resources needed to

achieve…

GrowthStartupPre-startup

Problem/Solution

Fit

Product

Validation

Market

Validation

Market

Penetration

Market

Expansion

Verifiability of

Information

Optimal Type of

Crowdfunding Donation Lending Equity

Reward Offered No (tangible) return Interest ($), Product Securities, Profit

Sharing

Best Practices 1. Choose a

specialized

platform and all-

or-nothingpayout

model

2. Be transparent

and accountable

3. Publicize backer

information

1. Offer tangible

rewards

2. Detail thestartup

founder’s

credentials

3. Frequently

updatea funding

crowd

1. Provide third-

party verifiable

reports

2. Attract reputable

early investors

3. Target a crowd

that can

empathize

Yes No Yes No Yes No

186 J. Paschen

ing (Mollick,2014).The closenessto the aim of the

project can be seen in a numberof venturesthat

targeta specificcrowd,suchasFarmHill, a delivery

service for healthy lunch food operatingin the

Silicon Valley area. It raised $1 million in equity

crowdfunding,with a numberof the investorsiden-

tified as ‘foodies’ or previousinvestorsin similar

ventures(FarmHill, n.d.). Anotherexampleis Plum

(2015),whichdevelopeda wi-fi-enabledsmartlight

switchanddrewfunderswhohadextensiveprevious

experiencein successfulsmart home networking

companies.Plum exceededits $5 million equity

crowdfundinggoal.

5.4. Best practicesmini-summary

In summary,a startup should develop, maintain,

and use its personal and professionalnetworks

extensivelyin the lead up to and duringan equity

crowdfundingcampaign.Thiscontributespositively

to oneof the keysuccessfactorsfor a crowdfunding

campaign: achieving and sustainingmomentum

behindthe campaign,especiallyin the early post-

launchdays.Evidenceshowsthat oncea campaign

hits30%of its fundinggoalthe successrateclimbsto

90%,comparedto only50%after a campaignreaches

the 5%mark.Andthefasterthemomentumis gained

the better; campaignsthat reach the 30%mark

within the first week are more likely to achieve

their fundinggoals(CanadaMediaFund, 2016).

6. Final thoughtson crowdfundingfor

startups

This article offers contributionsto both the practi-

tioner and researchcommunities.For startups,it

demonstratesthat crowdfundingcan generatea

valuable organizationalresource base, primarily

throughthe acquisitionof funds, but also through

nonmonetaryresourcesin the form of learning,the

formationof crowd capital, and marketing(Brown

et al., 2017; McCarthyet al., 2013;Prpic´ et al.,

2015).But not all crowdfundingtypes are equally

suitedto supportthe variousresourcerequirements

in different life cycle stages, and neither are

all crowdfundingtypes a feasible option. When

choosingamongthe different crowdfundingtypes,

a startup needs to considerits specific lifecycle

stage, alongwith intendedcrowdfundingbenefits

like resource provision and constraintsin terms

of the type of reward it is able to offer credibly.

This article providesa frameworkto guidestartup

decisionsin this context, which is illustrated in

Figure 1.

In the pre-startupphase,organizationalresources

focus on validatingthe idea and a crowd provides

Figure 1. Frameworkfor startup crowdfunding

Startup Stage

Resources needed to

achieve…

GrowthStartupPre-startup

Problem/Solution

Fit

Product

Validation

Market

Validation

Market

Penetration

Market

Expansion

Verifiability of

Information

Optimal Type of

Crowdfunding Donation Lending Equity

Reward Offered No (tangible) return Interest ($), Product Securities, Profit

Sharing

Best Practices 1. Choose a

specialized

platform and all-

or-nothingpayout

model

2. Be transparent

and accountable

3. Publicize backer

information

1. Offer tangible

rewards

2. Detail thestartup

founder’s

credentials

3. Frequently

updatea funding

crowd

1. Provide third-

party verifiable

reports

2. Attract reputable

early investors

3. Target a crowd

that can

empathize

Yes No Yes No Yes No

186 J. Paschen

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

valuableresourcesthroughfundingandfeedbackon

a proposedsolution.Venturesin this stageneither

havea developedproductto offer as a reward,nor

aretheyableto offer financialor equity-likereturns;

donation crowdfundingis optimal to meet their

resourceneedswithin these constraints.Similarly,

resourcesin the growthstagearerequiredto market

the offering and scale the venture’soperations.

Equitycrowdfundingis bestsuitedto meetthehigher

capitalneedsin this phase,in additionto providing

criticalnonmonetaryresourcesin theformof product

promotion,sales,andmarketing.

Oncea choiceonthetypeof crowdfundingis made,

startupsface the next problem:how to convince

potentialbackersto fundtheirventure.Asa solution,

this article offers a numberof best practicesas

guidelinesthat havebeenshownto havea measur-

able effect on the successrates of crowdfunding

initiativesandarelikelyto provevaluablefor startups

(seeFigure1). Thisleadsto anotherkeyfinding.The

circumstancesfor differentcrowdfundingendeavors

are so diversethat it canbe arguedthat eachcrowd