Finance Report: Analysis of City Brasserie Hotel Finances

VerifiedAdded on 2020/01/23

|19

|6609

|225

Report

AI Summary

This finance report provides a detailed analysis of the financial operations of City Brasserie Hotel. The report begins by exploring various sources of finance available to the hotel, including loans, retained earnings, private investors, trade credit, and loans from friends and relatives. It then delves into new methods of generating income, such as cookery classes, merchandising cookbooks and kitchen items, and event catering. The report also examines the elements of cost, including labor, consumables, and overheads, and discusses ways to increase the gross profit percentage through sales price adjustments and economies of scale. Furthermore, the report covers stock and cash control techniques, as well as security measures for cash on the premises. The analysis extends to the source and structure of a trial balance, the evaluation of business accounts, the purpose of financial budgeting, and variance analysis. Ratio analysis is conducted to determine business performance, followed by recommendations for improved financial management strategies. The report concludes with a discussion on different types of costs, the calculation of contribution per customer, cost-volume-profit relationships, and recommendations for short-term management decisions, including the breakeven point.

FINANCE IN THE

HOSPITALITY

HOSPITALITY

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance............................................................................................................1

1.2 New methods of generating incomes...............................................................................2

TASK 2............................................................................................................................................3

2.1 Elements of cost and ways in which gross profit percentage can be increased by changing

sales price...............................................................................................................................3

2.2 Stock and cash control as well as security of cash on the premises and business hours..4

TASK 3............................................................................................................................................4

3.1 Source and structure of trial balance................................................................................4

3.2 Evaluation of business accounts.......................................................................................5

3.3 Purpose of financial budget and process that can be used for budget control..................6

3.4 Variance analysis and justification of reason...................................................................7

TASK 4............................................................................................................................................8

AC 4.1 Calculation of ratios to determine business performance..........................................8

AC 4.2 Recommendation for improve financial management strategies...............................9

TASK 5..........................................................................................................................................10

AC 5.1 Type of costs............................................................................................................10

AC 5.2 Calculation of contribution per customer and cost volume profit relationship.......11

AC 5.3 Recommendation for short term management decisions.........................................12

(1) Breakeven point..............................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Sources of finance............................................................................................................1

1.2 New methods of generating incomes...............................................................................2

TASK 2............................................................................................................................................3

2.1 Elements of cost and ways in which gross profit percentage can be increased by changing

sales price...............................................................................................................................3

2.2 Stock and cash control as well as security of cash on the premises and business hours..4

TASK 3............................................................................................................................................4

3.1 Source and structure of trial balance................................................................................4

3.2 Evaluation of business accounts.......................................................................................5

3.3 Purpose of financial budget and process that can be used for budget control..................6

3.4 Variance analysis and justification of reason...................................................................7

TASK 4............................................................................................................................................8

AC 4.1 Calculation of ratios to determine business performance..........................................8

AC 4.2 Recommendation for improve financial management strategies...............................9

TASK 5..........................................................................................................................................10

AC 5.1 Type of costs............................................................................................................10

AC 5.2 Calculation of contribution per customer and cost volume profit relationship.......11

AC 5.3 Recommendation for short term management decisions.........................................12

(1) Breakeven point..............................................................................................................12

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION

Finance plays an important role in growth of an organization. In the report, sources of

finance are discussed in detail and along with this methods of generating income are also

described in detail. Apart from this, elements of cost and cash control as well as stock control

methods are also described. After that, importance of balance sheet and income statement is

described in detail and along with this; budget and purpose behind its preparation are discussed

briefly. At the end of the report, ratio analysis is done and it results are interpreted in the proper

manner. After that, cost volume relationship technique is applied and short term management

decision is taken in the report.

TASK 1

1.1 Sources of finance

Sources of finance that are available to City Brasserie hotel are as follows. Loan from bank- It is commonly used source of finance that are available to business.

Under this, firm takes a loan at specific interest rates from the financial institutions. In

return the company needs to mortgage its property as a security to the bank. Loan can be

taken at the fixed or floating interest rates. If loan is taken at the floating rate then it is

very risky for the firm. With the change in interest rate structure loan rate also changes

(Irwin and Scott, 2010). If this change happens in the negative direction then cost of the

firm may increase. Hence, City Brasserie must takes loan at the fixed interest rate. Retained earnings- City Brasserie can also use retained earnings in order to finance its

operations. It is a part of the profit that remains after deducting all expenses from the

revenue. By making use of retained earning firm can finance its business development

activities without paying any cost. Private investors- It is a different mode of finance and under this private investors makes

an investment in the firm and in return they get return from the firm on which they made

an investment (Brown, Bird and Schalatek, 2010). Private equity are covered under this

section in which there is a private equity firm which makes an investment in the any firm

and get shareholding in same. Till life time of investment private equity firm gets a share

in the invested amount. Hence, this source of finance is also suitable for the City

Brasserie hotel.

1

Finance plays an important role in growth of an organization. In the report, sources of

finance are discussed in detail and along with this methods of generating income are also

described in detail. Apart from this, elements of cost and cash control as well as stock control

methods are also described. After that, importance of balance sheet and income statement is

described in detail and along with this; budget and purpose behind its preparation are discussed

briefly. At the end of the report, ratio analysis is done and it results are interpreted in the proper

manner. After that, cost volume relationship technique is applied and short term management

decision is taken in the report.

TASK 1

1.1 Sources of finance

Sources of finance that are available to City Brasserie hotel are as follows. Loan from bank- It is commonly used source of finance that are available to business.

Under this, firm takes a loan at specific interest rates from the financial institutions. In

return the company needs to mortgage its property as a security to the bank. Loan can be

taken at the fixed or floating interest rates. If loan is taken at the floating rate then it is

very risky for the firm. With the change in interest rate structure loan rate also changes

(Irwin and Scott, 2010). If this change happens in the negative direction then cost of the

firm may increase. Hence, City Brasserie must takes loan at the fixed interest rate. Retained earnings- City Brasserie can also use retained earnings in order to finance its

operations. It is a part of the profit that remains after deducting all expenses from the

revenue. By making use of retained earning firm can finance its business development

activities without paying any cost. Private investors- It is a different mode of finance and under this private investors makes

an investment in the firm and in return they get return from the firm on which they made

an investment (Brown, Bird and Schalatek, 2010). Private equity are covered under this

section in which there is a private equity firm which makes an investment in the any firm

and get shareholding in same. Till life time of investment private equity firm gets a share

in the invested amount. Hence, this source of finance is also suitable for the City

Brasserie hotel.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Trade credit- In this, source of finance business firms takes a loan from the business

friends with whom they are working. This is common with suppliers in which business

firms purchase raw material at a credit. Thus, the firm can use this source of finance in

order to finance its purchase related operations.

Loan from friends and relatives- This is most preferred source of finance because in case

of this source of finance there is no cost of raising finance. This is easily available source

of finance but small amount can be raised from the friends and relatives which is also a

major limitation of this source of finance.

1.2 New methods of generating incomes

New methods through which City Brasserie hotel can generate revenue are as follows. Cookery classes- Currently, hospitality industry is growing at a rapid rate and more and

more people are going in hotel management course. This indicates that people are more

interested in developing their cooking skills. Hence, if I will commence cookery classes

and parsons that wants to learn cooking will join class. As a result, this will be a new

segment from which I will earn revenue. Jamie Oliver is running such kind of classes and

through these classes it is earning good amount of revenue. Hence, this business segment

requires due attention from the management side. Hence, if City Brasserie hotel is

providing a course and internship in food making then this makes help in increasing its

revenue at the rapid pace (Brown and Petersen, 2011). Moreover, this may become core

business segment for the City Brasserie hotel in future time period. Merchandising of cookbooks and kitchen items- Cookbook’s can be the method for

accelerating income level of the firm. In cookbook’s images of all food items is given

along with their price. Through cookbook’s consumer comes to know about the product

and its appearance. Appearance of the product attracts people to purchase the product. In

research it has been found that mostly people in restaurant when comes to eat new food

item are attracted by the color appearance of the product. Hence it can be said that

merchandising of cookbooks will help in increasing revenue of the firm (Sarasan and

et.al, 2011). In same way, if kitchen items are merchandise in systemic way then it will

put good impression on consumers and will help in increasing company’s profit. In order

to create customers for this product cook books will be sold to those who will visit the

2

friends with whom they are working. This is common with suppliers in which business

firms purchase raw material at a credit. Thus, the firm can use this source of finance in

order to finance its purchase related operations.

Loan from friends and relatives- This is most preferred source of finance because in case

of this source of finance there is no cost of raising finance. This is easily available source

of finance but small amount can be raised from the friends and relatives which is also a

major limitation of this source of finance.

1.2 New methods of generating incomes

New methods through which City Brasserie hotel can generate revenue are as follows. Cookery classes- Currently, hospitality industry is growing at a rapid rate and more and

more people are going in hotel management course. This indicates that people are more

interested in developing their cooking skills. Hence, if I will commence cookery classes

and parsons that wants to learn cooking will join class. As a result, this will be a new

segment from which I will earn revenue. Jamie Oliver is running such kind of classes and

through these classes it is earning good amount of revenue. Hence, this business segment

requires due attention from the management side. Hence, if City Brasserie hotel is

providing a course and internship in food making then this makes help in increasing its

revenue at the rapid pace (Brown and Petersen, 2011). Moreover, this may become core

business segment for the City Brasserie hotel in future time period. Merchandising of cookbooks and kitchen items- Cookbook’s can be the method for

accelerating income level of the firm. In cookbook’s images of all food items is given

along with their price. Through cookbook’s consumer comes to know about the product

and its appearance. Appearance of the product attracts people to purchase the product. In

research it has been found that mostly people in restaurant when comes to eat new food

item are attracted by the color appearance of the product. Hence it can be said that

merchandising of cookbooks will help in increasing revenue of the firm (Sarasan and

et.al, 2011). In same way, if kitchen items are merchandise in systemic way then it will

put good impression on consumers and will help in increasing company’s profit. In order

to create customers for this product cook books will be sold to those who will visit the

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

restaurant. Target customers by viewing images and recipes on the books will be

motivated to purchase the book. In this way, book will be sold to the people.

Events catering- This is the most successful business segment in the catering industry.

Under this, firm will provide food service to the guests on the specific events on behalf of

client. Hence, event catering can be certainly help firm in increasing its revenue.

TASK 2 NEED TO BE A FORMAT LETTER

To

The Board of directors of City Brasserie hotel

Date: 29th January 2016

2.1 Elements of cost and ways in which gross profit percentage can be increased by changing

sales price

There are three elements of cost and these are as follows. Labor cost- It is a cost that exists due to use of labors at the workplace for production

process. Labor cost is flexible in nature and can be changed with change in level of

output. Firms keep labors on contract basis. Hence, firm is in position to use labors

according to its situation. Labor cost can be divided in to two parts one is direct labor

and second is indirect labor cost (Davis, et.al. 2010). Direct labor cost refers to the cost

that is related to the production process and indirect labor refers to the cost that of labors

which is directly not linked to the production process. Consumables- It refers to the cost of material that is used for supporting delivery of the

service to the customers. Consumables for the product are washing liquid and tissues

etc. It is not a part of the firm’s prime cost and with change in production units’ use of

raw material also gets changed. This cost is related to the service delivery and due to

this reason it is assumed as an important part of the costing. This is because firm cannot

bear cost of purchasing consumables. Hence, in the final price of the product cost of

consumables is also included.

Overheads- It refers to the indirect expenses that are related to the business. These may

be transportation or other costs. These are the important part of the firm’s overall cost.

With change in production units overhead also get changed (Collier and et.al, 2012). So

the company must always try to reduce their cost by identifying cost reduction ideas.

3

motivated to purchase the book. In this way, book will be sold to the people.

Events catering- This is the most successful business segment in the catering industry.

Under this, firm will provide food service to the guests on the specific events on behalf of

client. Hence, event catering can be certainly help firm in increasing its revenue.

TASK 2 NEED TO BE A FORMAT LETTER

To

The Board of directors of City Brasserie hotel

Date: 29th January 2016

2.1 Elements of cost and ways in which gross profit percentage can be increased by changing

sales price

There are three elements of cost and these are as follows. Labor cost- It is a cost that exists due to use of labors at the workplace for production

process. Labor cost is flexible in nature and can be changed with change in level of

output. Firms keep labors on contract basis. Hence, firm is in position to use labors

according to its situation. Labor cost can be divided in to two parts one is direct labor

and second is indirect labor cost (Davis, et.al. 2010). Direct labor cost refers to the cost

that is related to the production process and indirect labor refers to the cost that of labors

which is directly not linked to the production process. Consumables- It refers to the cost of material that is used for supporting delivery of the

service to the customers. Consumables for the product are washing liquid and tissues

etc. It is not a part of the firm’s prime cost and with change in production units’ use of

raw material also gets changed. This cost is related to the service delivery and due to

this reason it is assumed as an important part of the costing. This is because firm cannot

bear cost of purchasing consumables. Hence, in the final price of the product cost of

consumables is also included.

Overheads- It refers to the indirect expenses that are related to the business. These may

be transportation or other costs. These are the important part of the firm’s overall cost.

With change in production units overhead also get changed (Collier and et.al, 2012). So

the company must always try to reduce their cost by identifying cost reduction ideas.

3

Gross profit percentage is directly linked to the sales price. There are two

options to increase gross profit percentage one is to increase sales price and second is to

generate economies of scale. In both cases, City Brasserie hotel gross profit percentage will

increase. In case of increase in sales price, cost will remain same and due to this reason gross

profit percentage will increase. Whereas in case of economies of scale cost will be reduced and

sales price will remain same. In this case also gross profit percentage will increase for the firm.

So, it can be said that City Brasserie hotel can select any of these available options.

2.2 Stock and cash control as well as security of cash on the premises and business hours

There are many techniques of cost control and City Brasserie hotel can select any of

these available techniques at its workplace. Economic order quantity- It refers to the quantity of raw material that a firm must

purchase in order to keep its holding cost low. By using this technique a target up to

which firm need to make purchase of raw material can be determined for a specific time

period. Thus, this technique helps in effective cost control by the firm. Re order lead time- It refers to the time between placing an order and receiving it.

Means that in this method minimum quantity is determined that must be kept for the

mentioned time period (Harvie and et.al, 2012). If stock level comes to that limit firm

immediately places an order for the raw material purchase. In this way it prevents the

problem of running out of raw material.

Batch control- Batch control is a stock control technique under which various types of

products are prepared in batches. As per this concept, if firm is producing fixed quantity

in the specific interval every time then it can order raw material in earlier stage. When

stock will comes to end firm will always have a raw material. Hence, by using this

technique stock is controlled in effective manner. In this method, goods are produced in

batches and at the end of the current batch of production; the Company is required to

identify needs for the next batch of production. In this, firm determines the number of

goods that it will be purchased in the next batch. Hence, firm is autocratically in position

to predict its raw material needs in proper manner. CLARIFY WHAT BATCH

CONTOL IS?EXAMPLE WHEN YOU FRY CHIPS IN THE SAME OVEN LIKE

FISH BEFORE YOU FINISH THE CHIPS YOU HAVE TO HAVE THE FISH RADY.

4

options to increase gross profit percentage one is to increase sales price and second is to

generate economies of scale. In both cases, City Brasserie hotel gross profit percentage will

increase. In case of increase in sales price, cost will remain same and due to this reason gross

profit percentage will increase. Whereas in case of economies of scale cost will be reduced and

sales price will remain same. In this case also gross profit percentage will increase for the firm.

So, it can be said that City Brasserie hotel can select any of these available options.

2.2 Stock and cash control as well as security of cash on the premises and business hours

There are many techniques of cost control and City Brasserie hotel can select any of

these available techniques at its workplace. Economic order quantity- It refers to the quantity of raw material that a firm must

purchase in order to keep its holding cost low. By using this technique a target up to

which firm need to make purchase of raw material can be determined for a specific time

period. Thus, this technique helps in effective cost control by the firm. Re order lead time- It refers to the time between placing an order and receiving it.

Means that in this method minimum quantity is determined that must be kept for the

mentioned time period (Harvie and et.al, 2012). If stock level comes to that limit firm

immediately places an order for the raw material purchase. In this way it prevents the

problem of running out of raw material.

Batch control- Batch control is a stock control technique under which various types of

products are prepared in batches. As per this concept, if firm is producing fixed quantity

in the specific interval every time then it can order raw material in earlier stage. When

stock will comes to end firm will always have a raw material. Hence, by using this

technique stock is controlled in effective manner. In this method, goods are produced in

batches and at the end of the current batch of production; the Company is required to

identify needs for the next batch of production. In this, firm determines the number of

goods that it will be purchased in the next batch. Hence, firm is autocratically in position

to predict its raw material needs in proper manner. CLARIFY WHAT BATCH

CONTOL IS?EXAMPLE WHEN YOU FRY CHIPS IN THE SAME OVEN LIKE

FISH BEFORE YOU FINISH THE CHIPS YOU HAVE TO HAVE THE FISH RADY.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

For controlling cash management, techniques are used by the companies. City Brasserie

hotel can also use this technique and under this it will decentralize its payment system and will

centralize its payment receipt system. By doing this, firm can delay its cash payment and can

boost cash receipt from debtors of its business. In order to secure cash after working hours

companies can took many steps (Brown and Petersen, 2011). It means that, it will use locker

facility which will be password protected. This will help in ensuring prevention of access of

unauthorized person from the company cash.

TASK 3 NEED TO BE A REPORT FORMAT

To

The Board of directors of City Brasserie hotel

Date: 29th January 2016

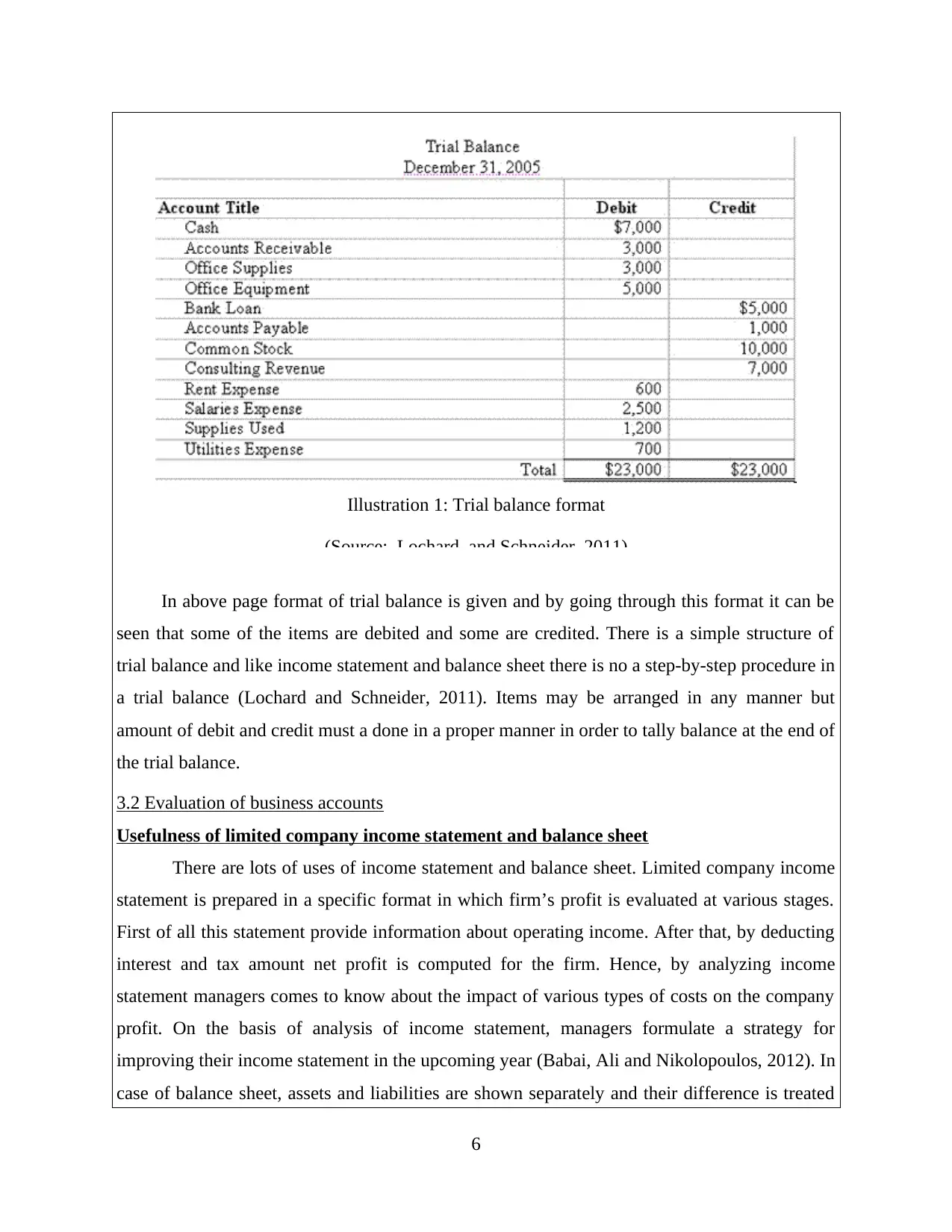

3.1 Source and structure of trial balance

Trial balance of the City Brasserie hotel indicates the balance of each and every account

individually. This means that all incoming and outgoing of money related to the specific person

will be taken into specific account which is also known as ledger account. In this account,

aggregate value will come in existence. This value is transferred to the trial balance (de Ridder

and et.al, 2012). Hence, it can be said that ledger account is a source of trial balance. Following

is the structure of trial balance.

5

hotel can also use this technique and under this it will decentralize its payment system and will

centralize its payment receipt system. By doing this, firm can delay its cash payment and can

boost cash receipt from debtors of its business. In order to secure cash after working hours

companies can took many steps (Brown and Petersen, 2011). It means that, it will use locker

facility which will be password protected. This will help in ensuring prevention of access of

unauthorized person from the company cash.

TASK 3 NEED TO BE A REPORT FORMAT

To

The Board of directors of City Brasserie hotel

Date: 29th January 2016

3.1 Source and structure of trial balance

Trial balance of the City Brasserie hotel indicates the balance of each and every account

individually. This means that all incoming and outgoing of money related to the specific person

will be taken into specific account which is also known as ledger account. In this account,

aggregate value will come in existence. This value is transferred to the trial balance (de Ridder

and et.al, 2012). Hence, it can be said that ledger account is a source of trial balance. Following

is the structure of trial balance.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

In above page format of trial balance is given and by going through this format it can be

seen that some of the items are debited and some are credited. There is a simple structure of

trial balance and like income statement and balance sheet there is no a step-by-step procedure in

a trial balance (Lochard and Schneider, 2011). Items may be arranged in any manner but

amount of debit and credit must a done in a proper manner in order to tally balance at the end of

the trial balance.

3.2 Evaluation of business accounts

Usefulness of limited company income statement and balance sheet

There are lots of uses of income statement and balance sheet. Limited company income

statement is prepared in a specific format in which firm’s profit is evaluated at various stages.

First of all this statement provide information about operating income. After that, by deducting

interest and tax amount net profit is computed for the firm. Hence, by analyzing income

statement managers comes to know about the impact of various types of costs on the company

profit. On the basis of analysis of income statement, managers formulate a strategy for

improving their income statement in the upcoming year (Babai, Ali and Nikolopoulos, 2012). In

case of balance sheet, assets and liabilities are shown separately and their difference is treated

6

Illustration 1: Trial balance format

(Source: Lochard, and Schneider, 2011)

seen that some of the items are debited and some are credited. There is a simple structure of

trial balance and like income statement and balance sheet there is no a step-by-step procedure in

a trial balance (Lochard and Schneider, 2011). Items may be arranged in any manner but

amount of debit and credit must a done in a proper manner in order to tally balance at the end of

the trial balance.

3.2 Evaluation of business accounts

Usefulness of limited company income statement and balance sheet

There are lots of uses of income statement and balance sheet. Limited company income

statement is prepared in a specific format in which firm’s profit is evaluated at various stages.

First of all this statement provide information about operating income. After that, by deducting

interest and tax amount net profit is computed for the firm. Hence, by analyzing income

statement managers comes to know about the impact of various types of costs on the company

profit. On the basis of analysis of income statement, managers formulate a strategy for

improving their income statement in the upcoming year (Babai, Ali and Nikolopoulos, 2012). In

case of balance sheet, assets and liabilities are shown separately and their difference is treated

6

Illustration 1: Trial balance format

(Source: Lochard, and Schneider, 2011)

as shareholder equity in the balance sheet. By using this statement, ratio analyses are

conducted and company financial condition is measured by the managers and analysts. Thus, it

can be said that both statements helps the managers in evaluating business from different sides.

Use of straight line of depreciation for adjustment

By using straight line of depreciation method firm per year aggregate depreciation is

computed by the accountant. The depreciation amount is deducted from the assets side of the

balance sheet and same amount is deducted from the income statement (Curdia and Woodford,

2011). This is the way adjustment is made in the company accounts.

Importance of account notes

Account notes have a great importance for the firm and stakeholders that have very deep

interest in the firm. These notes are shown in the company’s annual report (Ormiston and

Fraser, 2013). Under these notes, the firm discloses detail of the aggregate values that are

shown in the income statement and balance sheet. In the balance sheet of City Brasserie hotel

there is a long-term loan amount. Notes will show the way in which accountant arrive at the

final value of the long-term loan that is shown at the balance sheet of the mentioned firm.

3.3 Purpose of financial budget and process that can be used for budget control

Budgets are the set of the projections of the cost and revenue that firm think to be

happening in the future. It also acts as a target for the mangers that they want to achieve at the

end of the specific time period. The purpose of preparing budget is to give a specific direction

to the City Brasserie hotel performance. The second main purpose of preparing a budget is to

make sure that expenses of the firm will remain in control and necessary steps will be taken in

order to control expenses on time. By controlling costs, firm tries to increase its profitability in

the business. Along with this, employee’s motivation is another main purpose behind preparing

a budget. Budget set a target for the employees and forms commitment amount employees for

the achievement of the goal (Manthorpe and Samsi, 2013). Hence, due to commitment, an

employee tries achieve their goals by making their best efforts at the workplace. For

controlling budget, the City Brasserie hotel can use following process. Determination of standards – in this stage of budget preparation, the managers

determine standards. Those who are working at the ground level are responsible for

achieving these standards. Hence, in this regard employees make their best efforts. Measurement of performance- This is the second stage in which performance of the

7

conducted and company financial condition is measured by the managers and analysts. Thus, it

can be said that both statements helps the managers in evaluating business from different sides.

Use of straight line of depreciation for adjustment

By using straight line of depreciation method firm per year aggregate depreciation is

computed by the accountant. The depreciation amount is deducted from the assets side of the

balance sheet and same amount is deducted from the income statement (Curdia and Woodford,

2011). This is the way adjustment is made in the company accounts.

Importance of account notes

Account notes have a great importance for the firm and stakeholders that have very deep

interest in the firm. These notes are shown in the company’s annual report (Ormiston and

Fraser, 2013). Under these notes, the firm discloses detail of the aggregate values that are

shown in the income statement and balance sheet. In the balance sheet of City Brasserie hotel

there is a long-term loan amount. Notes will show the way in which accountant arrive at the

final value of the long-term loan that is shown at the balance sheet of the mentioned firm.

3.3 Purpose of financial budget and process that can be used for budget control

Budgets are the set of the projections of the cost and revenue that firm think to be

happening in the future. It also acts as a target for the mangers that they want to achieve at the

end of the specific time period. The purpose of preparing budget is to give a specific direction

to the City Brasserie hotel performance. The second main purpose of preparing a budget is to

make sure that expenses of the firm will remain in control and necessary steps will be taken in

order to control expenses on time. By controlling costs, firm tries to increase its profitability in

the business. Along with this, employee’s motivation is another main purpose behind preparing

a budget. Budget set a target for the employees and forms commitment amount employees for

the achievement of the goal (Manthorpe and Samsi, 2013). Hence, due to commitment, an

employee tries achieve their goals by making their best efforts at the workplace. For

controlling budget, the City Brasserie hotel can use following process. Determination of standards – in this stage of budget preparation, the managers

determine standards. Those who are working at the ground level are responsible for

achieving these standards. Hence, in this regard employees make their best efforts. Measurement of performance- This is the second stage in which performance of the

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

firm is measured by doing specific calculation. For this, figures can be taken from the

income statement and balance sheet of the firm. Performance measurement can be taken

in currency or units depending on the requirements of the measurement. Comparison of actual performance with the standards- In this, actual performance is

compared with the standards in order to identify the variance in the performance.

Variance may be positive or negative (Dunk, 2011). It is positive then there is no

problem but if variance is negative then it is a matter of concern for the firm. Hence,

managers must immediately take steps to ensure that such kind of error will not be

repeated again.

Comments by the top managers- This is the last stage in which manager comments on

the variance and proposes the ways that can be used to prevent errors that occurs in the

current evaluation stage.

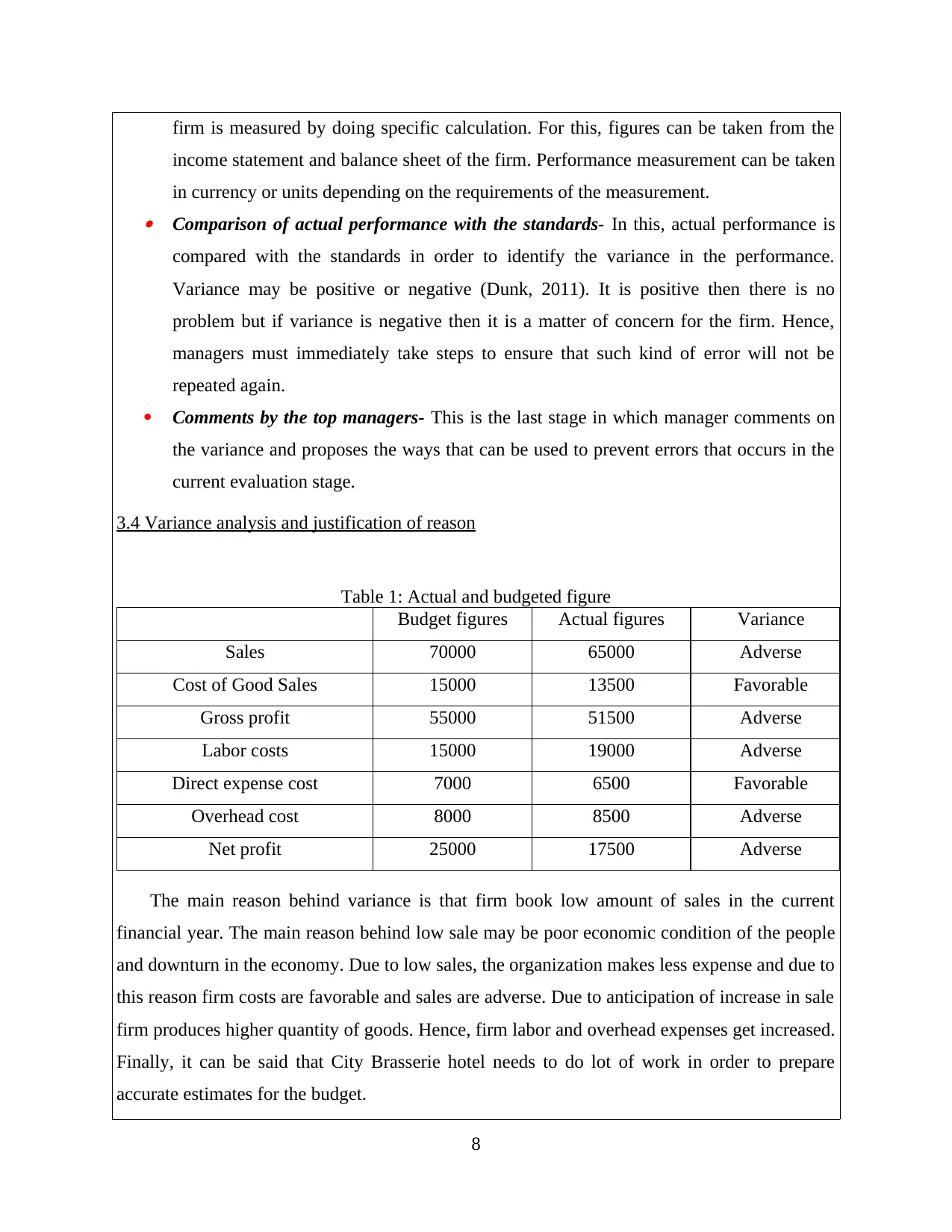

3.4 Variance analysis and justification of reason

Table 1: Actual and budgeted figure

Budget figures Actual figures Variance

Sales 70000 65000 Adverse

Cost of Good Sales 15000 13500 Favorable

Gross profit 55000 51500 Adverse

Labor costs 15000 19000 Adverse

Direct expense cost 7000 6500 Favorable

Overhead cost 8000 8500 Adverse

Net profit 25000 17500 Adverse

The main reason behind variance is that firm book low amount of sales in the current

financial year. The main reason behind low sale may be poor economic condition of the people

and downturn in the economy. Due to low sales, the organization makes less expense and due to

this reason firm costs are favorable and sales are adverse. Due to anticipation of increase in sale

firm produces higher quantity of goods. Hence, firm labor and overhead expenses get increased.

Finally, it can be said that City Brasserie hotel needs to do lot of work in order to prepare

accurate estimates for the budget.

8

income statement and balance sheet of the firm. Performance measurement can be taken

in currency or units depending on the requirements of the measurement. Comparison of actual performance with the standards- In this, actual performance is

compared with the standards in order to identify the variance in the performance.

Variance may be positive or negative (Dunk, 2011). It is positive then there is no

problem but if variance is negative then it is a matter of concern for the firm. Hence,

managers must immediately take steps to ensure that such kind of error will not be

repeated again.

Comments by the top managers- This is the last stage in which manager comments on

the variance and proposes the ways that can be used to prevent errors that occurs in the

current evaluation stage.

3.4 Variance analysis and justification of reason

Table 1: Actual and budgeted figure

Budget figures Actual figures Variance

Sales 70000 65000 Adverse

Cost of Good Sales 15000 13500 Favorable

Gross profit 55000 51500 Adverse

Labor costs 15000 19000 Adverse

Direct expense cost 7000 6500 Favorable

Overhead cost 8000 8500 Adverse

Net profit 25000 17500 Adverse

The main reason behind variance is that firm book low amount of sales in the current

financial year. The main reason behind low sale may be poor economic condition of the people

and downturn in the economy. Due to low sales, the organization makes less expense and due to

this reason firm costs are favorable and sales are adverse. Due to anticipation of increase in sale

firm produces higher quantity of goods. Hence, firm labor and overhead expenses get increased.

Finally, it can be said that City Brasserie hotel needs to do lot of work in order to prepare

accurate estimates for the budget.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TASK 4

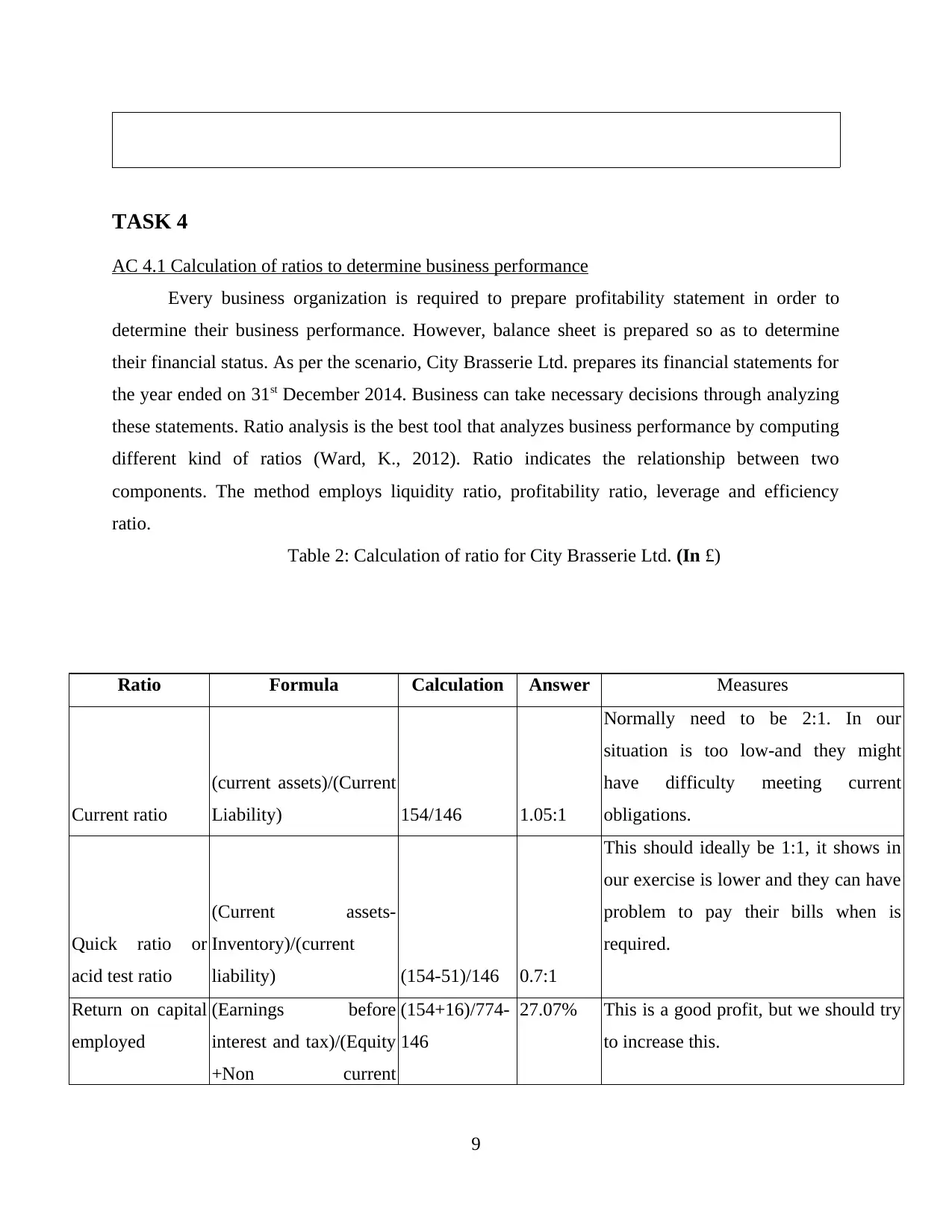

AC 4.1 Calculation of ratios to determine business performance

Every business organization is required to prepare profitability statement in order to

determine their business performance. However, balance sheet is prepared so as to determine

their financial status. As per the scenario, City Brasserie Ltd. prepares its financial statements for

the year ended on 31st December 2014. Business can take necessary decisions through analyzing

these statements. Ratio analysis is the best tool that analyzes business performance by computing

different kind of ratios (Ward, K., 2012). Ratio indicates the relationship between two

components. The method employs liquidity ratio, profitability ratio, leverage and efficiency

ratio.

Table 2: Calculation of ratio for City Brasserie Ltd. (In £)

Ratio Formula Calculation Answer Measures

Current ratio

(current assets)/(Current

Liability) 154/146 1.05:1

Normally need to be 2:1. In our

situation is too low-and they might

have difficulty meeting current

obligations.

Quick ratio or

acid test ratio

(Current assets-

Inventory)/(current

liability) (154-51)/146 0.7:1

This should ideally be 1:1, it shows in

our exercise is lower and they can have

problem to pay their bills when is

required.

Return on capital

employed

(Earnings before

interest and tax)/(Equity

+Non current

(154+16)/774-

146

27.07% This is a good profit, but we should try

to increase this.

9

AC 4.1 Calculation of ratios to determine business performance

Every business organization is required to prepare profitability statement in order to

determine their business performance. However, balance sheet is prepared so as to determine

their financial status. As per the scenario, City Brasserie Ltd. prepares its financial statements for

the year ended on 31st December 2014. Business can take necessary decisions through analyzing

these statements. Ratio analysis is the best tool that analyzes business performance by computing

different kind of ratios (Ward, K., 2012). Ratio indicates the relationship between two

components. The method employs liquidity ratio, profitability ratio, leverage and efficiency

ratio.

Table 2: Calculation of ratio for City Brasserie Ltd. (In £)

Ratio Formula Calculation Answer Measures

Current ratio

(current assets)/(Current

Liability) 154/146 1.05:1

Normally need to be 2:1. In our

situation is too low-and they might

have difficulty meeting current

obligations.

Quick ratio or

acid test ratio

(Current assets-

Inventory)/(current

liability) (154-51)/146 0.7:1

This should ideally be 1:1, it shows in

our exercise is lower and they can have

problem to pay their bills when is

required.

Return on capital

employed

(Earnings before

interest and tax)/(Equity

+Non current

(154+16)/774-

146

27.07% This is a good profit, but we should try

to increase this.

9

liability)*100

Gross profit

percentage

(Gross

profit)/(Sales)*100 500/920 54.3%

This is as high as possible; we need to

try to keep on track.

Net profit

percentage (net profit/(Sales)*100 103/920 11%

This is too low; we need to find some

solution to bring it a higher level.

Debtors

collection period

(Receivable)/

(revenue)*365 92*365/920 36.5 days

Try to collect your debts more quickly.

Should be in 30 days.

Creditors

payment period

(Creditors)/

(Purchase)*365 45*365/420

39.10

days

This is a good period to pay our debt.

Inventory

turnover ratio

(Cost of goods

sold)/(Inventory) 920/51

18.03

times per

year

This is a reasonable times per year.

Debt to equity

ratio (Debt)/(Equity) 571/203 2.81

We need to try to keep our debts lower.

Interpretations:

Profitability ratio: Profitability can be analyzed by computing gross profit ratio, net

profit ratio and return on capital employed. City Brasserie Ltd. gross margin and net margin are

54.3478% and 11.19565% respectively. However, return on capital employed is 27.07% in the

year 2014. It indicates that business is performing better in the market, as its profitability ratios

are good.

Liquidity ratio: It measures the business ability to pay its current liabilities. City Brasserie

Ltd. current ratio and quick ratio are 1.05 and 0.705 respectively. Business current assets and

liabilities are 154£ and 146£ respectively. It indicates that business have availability of working

capital which implies that company is able to discharge its current obligations. On contrary,

debtor’s collection period helps in measuring the business ability to receive cash from its

debtors. However, creditor’s payment period indicates the time taken to discharge business

creditors. In context to City Brasserie Ltd., creditor’s payment period and debtor’s collection

period are 39.107 days and 36.5 days. Higher the creditor’s collection period indicate that

business is taking higher time period to receive cash from debtors while debtors are paid earlier.

Thus, the ratios indicate that company will be having lower working capital for operational

10

Gross profit

percentage

(Gross

profit)/(Sales)*100 500/920 54.3%

This is as high as possible; we need to

try to keep on track.

Net profit

percentage (net profit/(Sales)*100 103/920 11%

This is too low; we need to find some

solution to bring it a higher level.

Debtors

collection period

(Receivable)/

(revenue)*365 92*365/920 36.5 days

Try to collect your debts more quickly.

Should be in 30 days.

Creditors

payment period

(Creditors)/

(Purchase)*365 45*365/420

39.10

days

This is a good period to pay our debt.

Inventory

turnover ratio

(Cost of goods

sold)/(Inventory) 920/51

18.03

times per

year

This is a reasonable times per year.

Debt to equity

ratio (Debt)/(Equity) 571/203 2.81

We need to try to keep our debts lower.

Interpretations:

Profitability ratio: Profitability can be analyzed by computing gross profit ratio, net

profit ratio and return on capital employed. City Brasserie Ltd. gross margin and net margin are

54.3478% and 11.19565% respectively. However, return on capital employed is 27.07% in the

year 2014. It indicates that business is performing better in the market, as its profitability ratios

are good.

Liquidity ratio: It measures the business ability to pay its current liabilities. City Brasserie

Ltd. current ratio and quick ratio are 1.05 and 0.705 respectively. Business current assets and

liabilities are 154£ and 146£ respectively. It indicates that business have availability of working

capital which implies that company is able to discharge its current obligations. On contrary,

debtor’s collection period helps in measuring the business ability to receive cash from its

debtors. However, creditor’s payment period indicates the time taken to discharge business

creditors. In context to City Brasserie Ltd., creditor’s payment period and debtor’s collection

period are 39.107 days and 36.5 days. Higher the creditor’s collection period indicate that

business is taking higher time period to receive cash from debtors while debtors are paid earlier.

Thus, the ratios indicate that company will be having lower working capital for operational

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.