Financial Analysis and Management Accounting Report: Unit 5, City Tech

VerifiedAdded on 2023/01/10

|19

|5477

|64

Report

AI Summary

This report analyzes management accounting practices at City Technology Limited. It explores essential management accounting systems like inventory management, cost accounting, and price optimization, detailing their benefits and applications. The report evaluates various reporting methods, including cost accounting and inventory management reports, and assesses the link between accounting systems and reporting. It then delves into cost calculations using absorption and marginal costing, providing income statements for each method. Furthermore, the report examines the advantages and disadvantages of planning tools for budgetary control, and it analyzes how management accounting resolves financial issues and contributes to organizational success. The report also provides a cash flow statement. The analysis includes a critical evaluation of the relationship between accounting systems and reporting, demonstrating how these elements are interconnected to achieve business goals. The report provides a comprehensive overview of management accounting principles and their practical application within a business context.

Unit 5: Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

TASK 1............................................................................................................................................1

P1. Explain the essential requirement of management accounting systems................................1

P2. Evaluate different methods which are used in management accounting reporting...............2

M1. Evaluate the benefits of management accounting systems along with its applications.......3

D1. Critically evaluate that how accounting systems are linked with the accounting reporting.3

TASK 2............................................................................................................................................4

P3. Calculate the cost by using suitable techniques and prepare income statement....................4

M2. Implement the range of accounting techniques to produce financial reporting document. .5

D2. Produce financial reports that accurately apply and interpret data for complex business

activities.......................................................................................................................................7

TASK 3............................................................................................................................................8

P4. Evaluate the advantages and disadvantages of different planning tool which are used for

budgetary control.........................................................................................................................8

MAIN BODY..................................................................................................................................1

TASK 1............................................................................................................................................1

P1. Explain the essential requirement of management accounting systems................................1

P2. Evaluate different methods which are used in management accounting reporting...............2

M1. Evaluate the benefits of management accounting systems along with its applications.......3

D1. Critically evaluate that how accounting systems are linked with the accounting reporting.3

TASK 2............................................................................................................................................4

P3. Calculate the cost by using suitable techniques and prepare income statement....................4

M2. Implement the range of accounting techniques to produce financial reporting document. .5

D2. Produce financial reports that accurately apply and interpret data for complex business

activities.......................................................................................................................................7

TASK 3............................................................................................................................................8

P4. Evaluate the advantages and disadvantages of different planning tool which are used for

budgetary control.........................................................................................................................8

M3. Analyses the use of different planning tool and its applications in preparing budget and

forecast.......................................................................................................................................11

TASK 4..........................................................................................................................................11

P5. Compare how organizations follow management accounting systems to resolve their

financial issues...........................................................................................................................11

M4. Analyse that how management accounting leads to organization for sustainable success 13

D3. Evaluate that how planning tool used to resolve financial issues and leads towards

organizational success...............................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

forecast.......................................................................................................................................11

TASK 4..........................................................................................................................................11

P5. Compare how organizations follow management accounting systems to resolve their

financial issues...........................................................................................................................11

M4. Analyse that how management accounting leads to organization for sustainable success 13

D3. Evaluate that how planning tool used to resolve financial issues and leads towards

organizational success...............................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a specialized branch of accounting which includes reviewing

financial knowledge to generate and execute a corporate strategy (Brustbauer, 2016).

Management accountants also can assist with risk management, performance measurement and

strategic management for their companies. Skilled financial managers can operate for both

individuals and organizations throughout every area of industry. This report is based on City

Technology Limited which is UK based medium size company and deals in gas sensing units

which are their specialization. This assessment based on the several topics such as understanding

of management accounting systems, different types of reporting and planning tool which are

used for budgetary control. In addition, it also includes the demonstration regarding how

management accounting systems help in resolving financial issues of the company. Management

accounting is essential for the organization and it also helps the managers to evaluate the

operational performance and build strategies accordingly to improve the overall efficiency as

well as effectiveness.

MAIN BODY

TASK 1

P1. Explain the essential requirement of management accounting systems

There are several management accounting systems which are followed by the manager’s of

City Technology Limited to evaluate their operational efficiency as well effectiveness. All are

discussed below:

Inventory management system: With an efficient supply chain, it is the technology that

lets businesses monitor their inventory level. It optimizes the full range from buying stuff with

the service provider to order fulfilment for their client, evaluating a production company's

corporate pathway (Cooper, 2017). City Technology Limited management implement this

program into their business to monitor regularly the level of inventories in warehouses. It helps

in producing goods as per customer demands. This method is essential for managing the quality

of the product or being responsible in the organization. Manager is capable of creating a

successful plan for the organization to conduct its business well.

Cost accounting system: Costing tools are implemented by manufacturing businesses that

constantly track the flow of goods through the different phases of production and assess each

1

Management accounting is a specialized branch of accounting which includes reviewing

financial knowledge to generate and execute a corporate strategy (Brustbauer, 2016).

Management accountants also can assist with risk management, performance measurement and

strategic management for their companies. Skilled financial managers can operate for both

individuals and organizations throughout every area of industry. This report is based on City

Technology Limited which is UK based medium size company and deals in gas sensing units

which are their specialization. This assessment based on the several topics such as understanding

of management accounting systems, different types of reporting and planning tool which are

used for budgetary control. In addition, it also includes the demonstration regarding how

management accounting systems help in resolving financial issues of the company. Management

accounting is essential for the organization and it also helps the managers to evaluate the

operational performance and build strategies accordingly to improve the overall efficiency as

well as effectiveness.

MAIN BODY

TASK 1

P1. Explain the essential requirement of management accounting systems

There are several management accounting systems which are followed by the manager’s of

City Technology Limited to evaluate their operational efficiency as well effectiveness. All are

discussed below:

Inventory management system: With an efficient supply chain, it is the technology that

lets businesses monitor their inventory level. It optimizes the full range from buying stuff with

the service provider to order fulfilment for their client, evaluating a production company's

corporate pathway (Cooper, 2017). City Technology Limited management implement this

program into their business to monitor regularly the level of inventories in warehouses. It helps

in producing goods as per customer demands. This method is essential for managing the quality

of the product or being responsible in the organization. Manager is capable of creating a

successful plan for the organization to conduct its business well.

Cost accounting system: Costing tools are implemented by manufacturing businesses that

constantly track the flow of goods through the different phases of production and assess each

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

product's expense at particular points. Evaluation of the ultimate cost of the goods in the work-in

- progress and finish level is crucial. In addition, City Technology Limited executives are able to

create plans to reduce or manage costs throughout the development phase.

Price optimization system: It is the most critical accounting system because it helps the

enterprise to adjust the price of a product according to the wilfulness of the consumer which also

fulfils the goals of the organization. They want to link their net profits to earnings for City

Technology Limited, optimum retail rates are necessary and most specifically if the company's

goal is to increase profitability by retaining the same degree of consumer retention (Brewer,

Garrison and Noreen, 2015). This has become essentially crucial as price levels for individual

business units become strongly profitable. A range of organizations are already hoping to open

innovative brands including those in the consumer niche markets. Having the correct price

becomes much more crucially important in that sense or a business can end up wasting

substantial customer base itself on rivals.

Above discussed accounting systems followed by the managers of City technology

Limited in order to improve their overall operational efficiency as well as effectiveness.

Company manage their stock level, control their cost or set the suitable price for products which

meet customers and organizational objectives.

P2. Evaluate different methods which are used in management accounting reporting

Cost accounting report: In this report, managers include the several aspects such as each

unit cost, expenses of each activity which related to the production or help the organization to

maximise it demand among the customers (Fleischman and Parker, 2017). In context of City

Technology Limited, for the production of gas sensing unit management done several activities

and all are required cost to produce those items. All these information recorded in the cosy

accounting reports which help the managers or accountants to build strategic decision in respect

of the operations.

Inventory management report: Inventory control reports would also show how often

stock levels company have on their hand. Effectively trying to control stock level and makes sure

their valuable wealth has been used in the effective manner. This report helps the City

Technology Limited to customise their information related to stock such as how much inventory

are available on hand, how much used in the production and remained inventory for further use.

2

- progress and finish level is crucial. In addition, City Technology Limited executives are able to

create plans to reduce or manage costs throughout the development phase.

Price optimization system: It is the most critical accounting system because it helps the

enterprise to adjust the price of a product according to the wilfulness of the consumer which also

fulfils the goals of the organization. They want to link their net profits to earnings for City

Technology Limited, optimum retail rates are necessary and most specifically if the company's

goal is to increase profitability by retaining the same degree of consumer retention (Brewer,

Garrison and Noreen, 2015). This has become essentially crucial as price levels for individual

business units become strongly profitable. A range of organizations are already hoping to open

innovative brands including those in the consumer niche markets. Having the correct price

becomes much more crucially important in that sense or a business can end up wasting

substantial customer base itself on rivals.

Above discussed accounting systems followed by the managers of City technology

Limited in order to improve their overall operational efficiency as well as effectiveness.

Company manage their stock level, control their cost or set the suitable price for products which

meet customers and organizational objectives.

P2. Evaluate different methods which are used in management accounting reporting

Cost accounting report: In this report, managers include the several aspects such as each

unit cost, expenses of each activity which related to the production or help the organization to

maximise it demand among the customers (Fleischman and Parker, 2017). In context of City

Technology Limited, for the production of gas sensing unit management done several activities

and all are required cost to produce those items. All these information recorded in the cosy

accounting reports which help the managers or accountants to build strategic decision in respect

of the operations.

Inventory management report: Inventory control reports would also show how often

stock levels company have on their hand. Effectively trying to control stock level and makes sure

their valuable wealth has been used in the effective manner. This report helps the City

Technology Limited to customise their information related to stock such as how much inventory

are available on hand, how much used in the production and remained inventory for further use.

2

Basically, this report helps the managers to make raw material orders accordingly and make sure

that company does not face the issues regarding shortage as well as wastage of goods.

Account receivable aging report: It is a management tool which may indicate that some

customers become credit risks and it reveal that organization should continue to do business with

chronically late payers customers. Accounts receivable aging has different columns

which typically divided into 30 day, 60 days and 60 date ranges. This report shows total current

balance receivables as well as previous due receivables. In context of City Technology Limited,

company follow this report to include all the defaulters and the remaining balance which they

have to recover.

M1. Evaluate the benefits of management accounting systems along with its applications

In context of City Technology Limited, manager of the company adopted several

accounting systems such as inventory management, price optimization and cost management

which provide several benefits. With the help of inventory management system, managers of the

City Technology are able to track the level of stock in the production unit and analyse the

required for the future production as well (Gray, 2015). Cost management system beneficial to

calculate the cost of each produced unit. It help the managers to reduce the overall cosy by

implementing strategic approaches and try to control the cost overall the period. In addition,

price optimization system used to set the price level for the goods & Services Company offer and

make sure that it will meet the both parties objectives such as maximise the profit for

organization and match the price level for the consumers. Applications of such accounting

systems help the City Technology Limited to maximise its efficiency as well as effectiveness.

D1. Critically evaluate that how accounting systems are linked with the accounting reporting

It has been critically evaluated that accounting systems and accounting reporting both are

linked with each others. It was critically examined that the cost management system allows the

manager to evaluate the expenditure of the good or service further mentioned in the cost

management report. This report allows managers to be using the relevant data when constructing

techniques that improve operational performance and operating cycle. In addition, for further

study, the inventory control system was used to monitor raw material supply and then further this

data reported for conscious choice taking by City Technology Limited managers in the inventory

control report. It is evaluated that documents and procedures of the accounts are interlinked. This

further beneficial for the organizations to achieve its business goals & objectives.

3

that company does not face the issues regarding shortage as well as wastage of goods.

Account receivable aging report: It is a management tool which may indicate that some

customers become credit risks and it reveal that organization should continue to do business with

chronically late payers customers. Accounts receivable aging has different columns

which typically divided into 30 day, 60 days and 60 date ranges. This report shows total current

balance receivables as well as previous due receivables. In context of City Technology Limited,

company follow this report to include all the defaulters and the remaining balance which they

have to recover.

M1. Evaluate the benefits of management accounting systems along with its applications

In context of City Technology Limited, manager of the company adopted several

accounting systems such as inventory management, price optimization and cost management

which provide several benefits. With the help of inventory management system, managers of the

City Technology are able to track the level of stock in the production unit and analyse the

required for the future production as well (Gray, 2015). Cost management system beneficial to

calculate the cost of each produced unit. It help the managers to reduce the overall cosy by

implementing strategic approaches and try to control the cost overall the period. In addition,

price optimization system used to set the price level for the goods & Services Company offer and

make sure that it will meet the both parties objectives such as maximise the profit for

organization and match the price level for the consumers. Applications of such accounting

systems help the City Technology Limited to maximise its efficiency as well as effectiveness.

D1. Critically evaluate that how accounting systems are linked with the accounting reporting

It has been critically evaluated that accounting systems and accounting reporting both are

linked with each others. It was critically examined that the cost management system allows the

manager to evaluate the expenditure of the good or service further mentioned in the cost

management report. This report allows managers to be using the relevant data when constructing

techniques that improve operational performance and operating cycle. In addition, for further

study, the inventory control system was used to monitor raw material supply and then further this

data reported for conscious choice taking by City Technology Limited managers in the inventory

control report. It is evaluated that documents and procedures of the accounts are interlinked. This

further beneficial for the organizations to achieve its business goals & objectives.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3. Calculate the cost by using suitable techniques and prepare income statement

Absorption costing: This costing method is used to evaluate inventories for the production

purpose. It includes not only the costs of materials and labour, but also the operational costs of

both reliant and fixed production (Gullberg, 2016). Current value is also named the utilization

rate. It defines the value of the output concerning the fixed costs. Inland Revenue supports the

absorption costing process, as inventory is not underappreciated. The costing process of

absorption is often used to plan the financial statements.

Income statement by using absorption costing:

Income statement

Using Absorption Costing Approach

ITEM Number of

units

£

P.U

.

AMOUN

T £

AMOUN

T £

SALES 7,300 55 401500

Direct Material 7,300 9.5 69,350

Direct Labour 7,300 15 109500

Variable Expenses

7300

(7300*2 =

14600

machinery

hours)

2 29,200

Fixed indirect production cost 7,300 6 900,000

Total Production Cost 1,108,050

Total Production Cost 1,108,050

Gross Profit: sales – COGS -706,550

Admin Salaries 13,800

Admin Overheads 4,500

Profit Before Interest & Tax (PBIT) -724,850

Interest Expenses 355

4

P3. Calculate the cost by using suitable techniques and prepare income statement

Absorption costing: This costing method is used to evaluate inventories for the production

purpose. It includes not only the costs of materials and labour, but also the operational costs of

both reliant and fixed production (Gullberg, 2016). Current value is also named the utilization

rate. It defines the value of the output concerning the fixed costs. Inland Revenue supports the

absorption costing process, as inventory is not underappreciated. The costing process of

absorption is often used to plan the financial statements.

Income statement by using absorption costing:

Income statement

Using Absorption Costing Approach

ITEM Number of

units

£

P.U

.

AMOUN

T £

AMOUN

T £

SALES 7,300 55 401500

Direct Material 7,300 9.5 69,350

Direct Labour 7,300 15 109500

Variable Expenses

7300

(7300*2 =

14600

machinery

hours)

2 29,200

Fixed indirect production cost 7,300 6 900,000

Total Production Cost 1,108,050

Total Production Cost 1,108,050

Gross Profit: sales – COGS -706,550

Admin Salaries 13,800

Admin Overheads 4,500

Profit Before Interest & Tax (PBIT) -724,850

Interest Expenses 355

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Profit Before Tax [PBIT-interest] -725,205

Tax @19% 220

Net Profit: profit before tax - tax -725,425

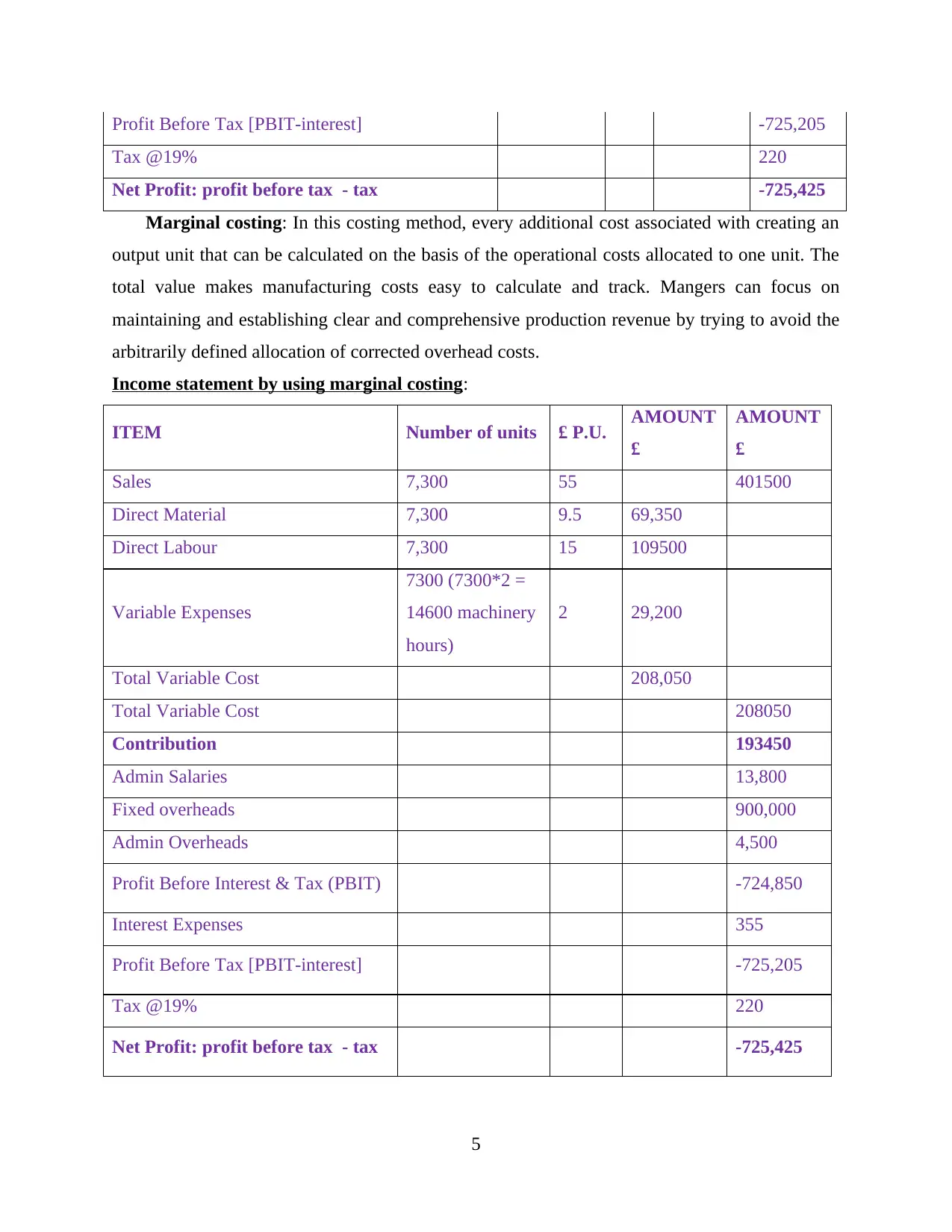

Marginal costing: In this costing method, every additional cost associated with creating an

output unit that can be calculated on the basis of the operational costs allocated to one unit. The

total value makes manufacturing costs easy to calculate and track. Mangers can focus on

maintaining and establishing clear and comprehensive production revenue by trying to avoid the

arbitrarily defined allocation of corrected overhead costs.

Income statement by using marginal costing:

ITEM Number of units £ P.U. AMOUNT

£

AMOUNT

£

Sales 7,300 55 401500

Direct Material 7,300 9.5 69,350

Direct Labour 7,300 15 109500

Variable Expenses

7300 (7300*2 =

14600 machinery

hours)

2 29,200

Total Variable Cost 208,050

Total Variable Cost 208050

Contribution 193450

Admin Salaries 13,800

Fixed overheads 900,000

Admin Overheads 4,500

Profit Before Interest & Tax (PBIT) -724,850

Interest Expenses 355

Profit Before Tax [PBIT-interest] -725,205

Tax @19% 220

Net Profit: profit before tax - tax -725,425

5

Tax @19% 220

Net Profit: profit before tax - tax -725,425

Marginal costing: In this costing method, every additional cost associated with creating an

output unit that can be calculated on the basis of the operational costs allocated to one unit. The

total value makes manufacturing costs easy to calculate and track. Mangers can focus on

maintaining and establishing clear and comprehensive production revenue by trying to avoid the

arbitrarily defined allocation of corrected overhead costs.

Income statement by using marginal costing:

ITEM Number of units £ P.U. AMOUNT

£

AMOUNT

£

Sales 7,300 55 401500

Direct Material 7,300 9.5 69,350

Direct Labour 7,300 15 109500

Variable Expenses

7300 (7300*2 =

14600 machinery

hours)

2 29,200

Total Variable Cost 208,050

Total Variable Cost 208050

Contribution 193450

Admin Salaries 13,800

Fixed overheads 900,000

Admin Overheads 4,500

Profit Before Interest & Tax (PBIT) -724,850

Interest Expenses 355

Profit Before Tax [PBIT-interest] -725,205

Tax @19% 220

Net Profit: profit before tax - tax -725,425

5

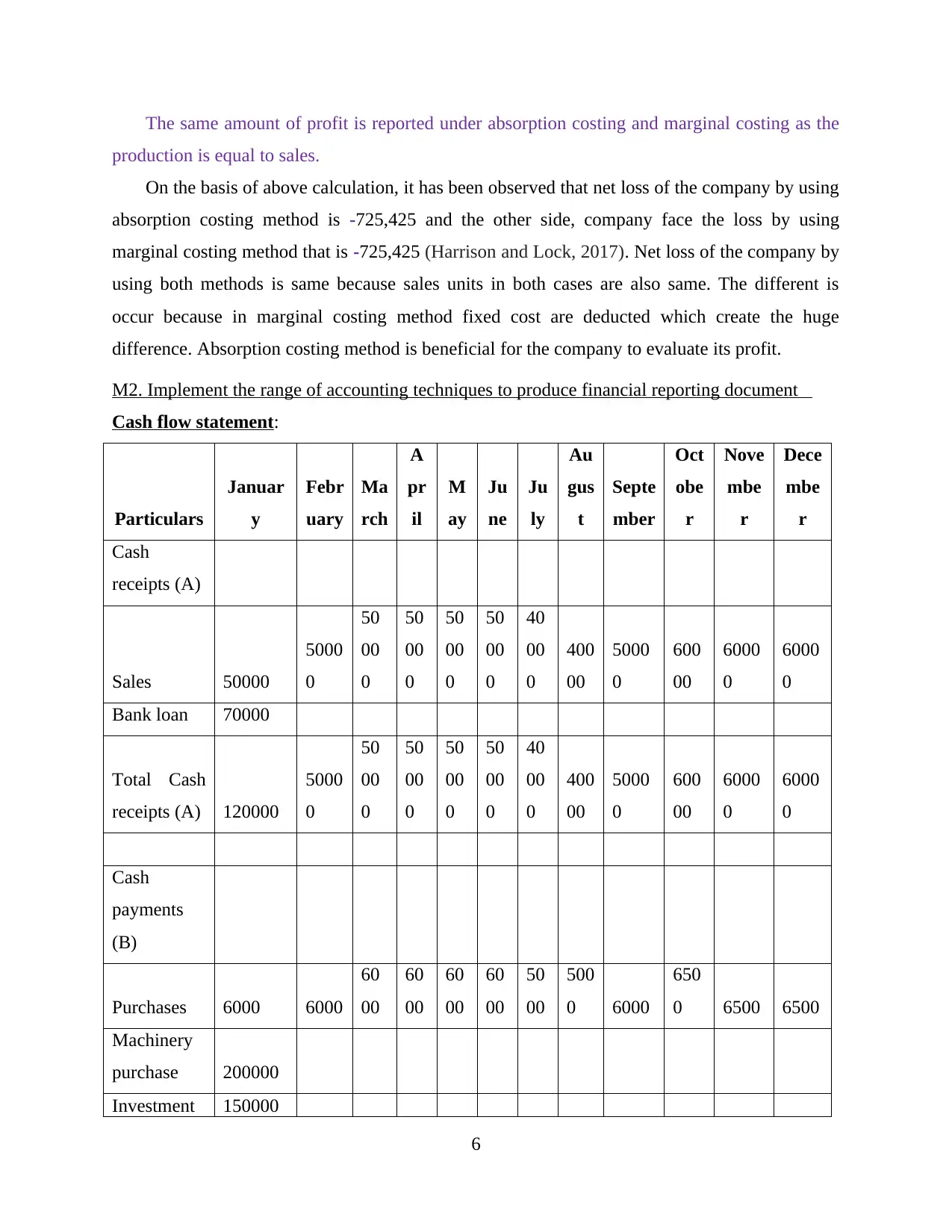

The same amount of profit is reported under absorption costing and marginal costing as the

production is equal to sales.

On the basis of above calculation, it has been observed that net loss of the company by using

absorption costing method is -725,425 and the other side, company face the loss by using

marginal costing method that is -725,425 (Harrison and Lock, 2017). Net loss of the company by

using both methods is same because sales units in both cases are also same. The different is

occur because in marginal costing method fixed cost are deducted which create the huge

difference. Absorption costing method is beneficial for the company to evaluate its profit.

M2. Implement the range of accounting techniques to produce financial reporting document

Cash flow statement:

Particulars

Januar

y

Febr

uary

Ma

rch

A

pr

il

M

ay

Ju

ne

Ju

ly

Au

gus

t

Septe

mber

Oct

obe

r

Nove

mbe

r

Dece

mbe

r

Cash

receipts (A)

Sales 50000

5000

0

50

00

0

50

00

0

50

00

0

50

00

0

40

00

0

400

00

5000

0

600

00

6000

0

6000

0

Bank loan 70000

Total Cash

receipts (A) 120000

5000

0

50

00

0

50

00

0

50

00

0

50

00

0

40

00

0

400

00

5000

0

600

00

6000

0

6000

0

Cash

payments

(B)

Purchases 6000 6000

60

00

60

00

60

00

60

00

50

00

500

0 6000

650

0 6500 6500

Machinery

purchase 200000

Investment 150000

6

production is equal to sales.

On the basis of above calculation, it has been observed that net loss of the company by using

absorption costing method is -725,425 and the other side, company face the loss by using

marginal costing method that is -725,425 (Harrison and Lock, 2017). Net loss of the company by

using both methods is same because sales units in both cases are also same. The different is

occur because in marginal costing method fixed cost are deducted which create the huge

difference. Absorption costing method is beneficial for the company to evaluate its profit.

M2. Implement the range of accounting techniques to produce financial reporting document

Cash flow statement:

Particulars

Januar

y

Febr

uary

Ma

rch

A

pr

il

M

ay

Ju

ne

Ju

ly

Au

gus

t

Septe

mber

Oct

obe

r

Nove

mbe

r

Dece

mbe

r

Cash

receipts (A)

Sales 50000

5000

0

50

00

0

50

00

0

50

00

0

50

00

0

40

00

0

400

00

5000

0

600

00

6000

0

6000

0

Bank loan 70000

Total Cash

receipts (A) 120000

5000

0

50

00

0

50

00

0

50

00

0

50

00

0

40

00

0

400

00

5000

0

600

00

6000

0

6000

0

Cash

payments

(B)

Purchases 6000 6000

60

00

60

00

60

00

60

00

50

00

500

0 6000

650

0 6500 6500

Machinery

purchase 200000

Investment 150000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Repayment

of loan 1500

15

00

15

00

15

00

15

00

15

00

150

0 1500

150

0 1500 1500

Purchase of

cleaning

equipments 2000

Long lasting

products 1500

15

00

15

00

15

00 1500 1500

Rent 6000 6000

60

00

60

00

60

00

60

00

60

00

600

0 6000

600

0 6000 6000

Cleaner

salary 800 800

80

0

80

0

80

0

80

0

80

0 800 800 800 800 800

Supervisor

salary 1500 1500

15

00

15

00

15

00

15

00

15

00

150

0 1500

150

0 1500 1500

Withdraw 3000

420

0 4200

420

0 4200 4200

Total Cash

payments

(B) 370800

1580

0

17

30

0

15

80

0

17

30

0

15

80

0

16

30

0

190

00

2150

0

205

00

2200

0

2050

0

Net cash

(A-B) -250800

3420

0

32

70

0

34

20

0

32

70

0

34

20

0

23

70

0

210

00

2850

0

395

00

3800

0

3950

0

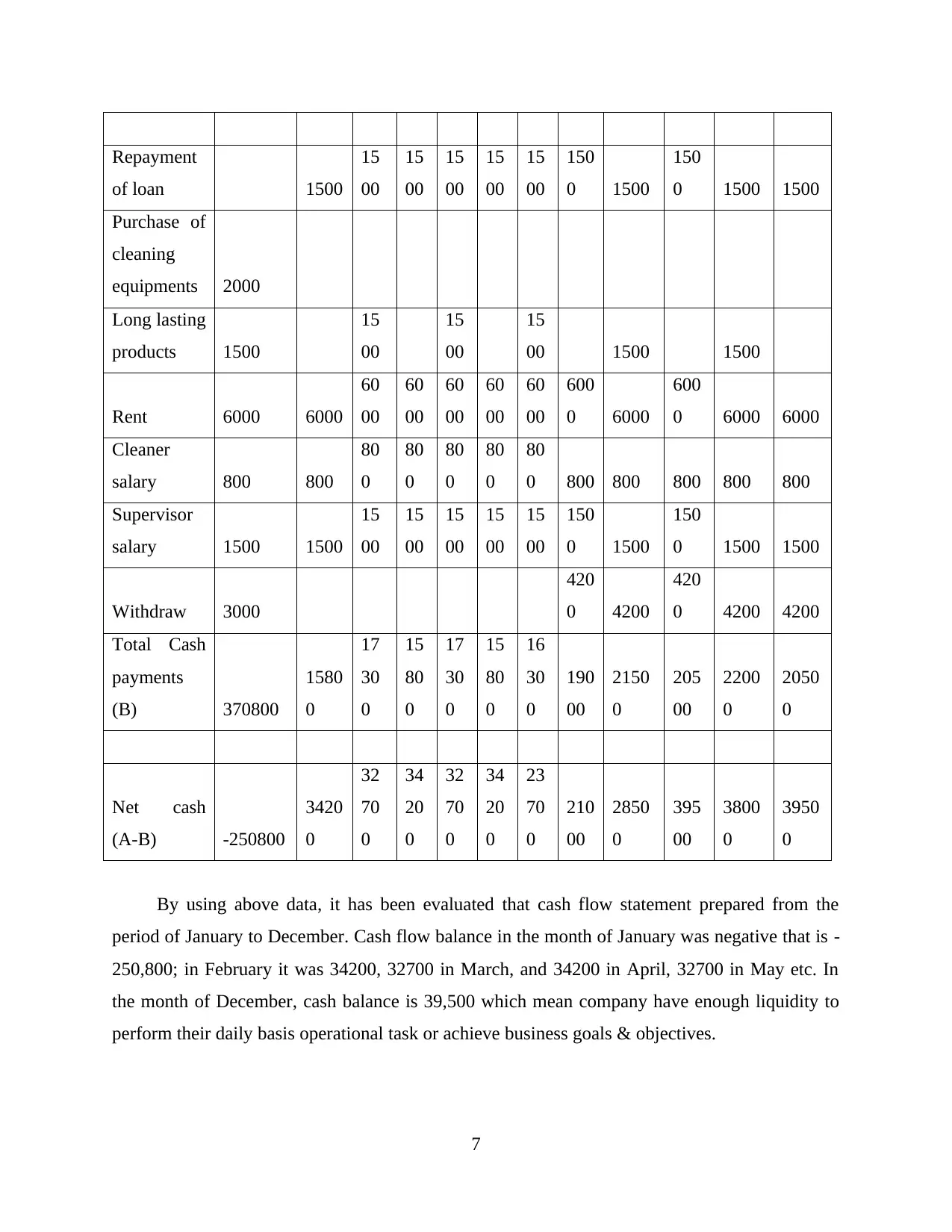

By using above data, it has been evaluated that cash flow statement prepared from the

period of January to December. Cash flow balance in the month of January was negative that is -

250,800; in February it was 34200, 32700 in March, and 34200 in April, 32700 in May etc. In

the month of December, cash balance is 39,500 which mean company have enough liquidity to

perform their daily basis operational task or achieve business goals & objectives.

7

of loan 1500

15

00

15

00

15

00

15

00

15

00

150

0 1500

150

0 1500 1500

Purchase of

cleaning

equipments 2000

Long lasting

products 1500

15

00

15

00

15

00 1500 1500

Rent 6000 6000

60

00

60

00

60

00

60

00

60

00

600

0 6000

600

0 6000 6000

Cleaner

salary 800 800

80

0

80

0

80

0

80

0

80

0 800 800 800 800 800

Supervisor

salary 1500 1500

15

00

15

00

15

00

15

00

15

00

150

0 1500

150

0 1500 1500

Withdraw 3000

420

0 4200

420

0 4200 4200

Total Cash

payments

(B) 370800

1580

0

17

30

0

15

80

0

17

30

0

15

80

0

16

30

0

190

00

2150

0

205

00

2200

0

2050

0

Net cash

(A-B) -250800

3420

0

32

70

0

34

20

0

32

70

0

34

20

0

23

70

0

210

00

2850

0

395

00

3800

0

3950

0

By using above data, it has been evaluated that cash flow statement prepared from the

period of January to December. Cash flow balance in the month of January was negative that is -

250,800; in February it was 34200, 32700 in March, and 34200 in April, 32700 in May etc. In

the month of December, cash balance is 39,500 which mean company have enough liquidity to

perform their daily basis operational task or achieve business goals & objectives.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

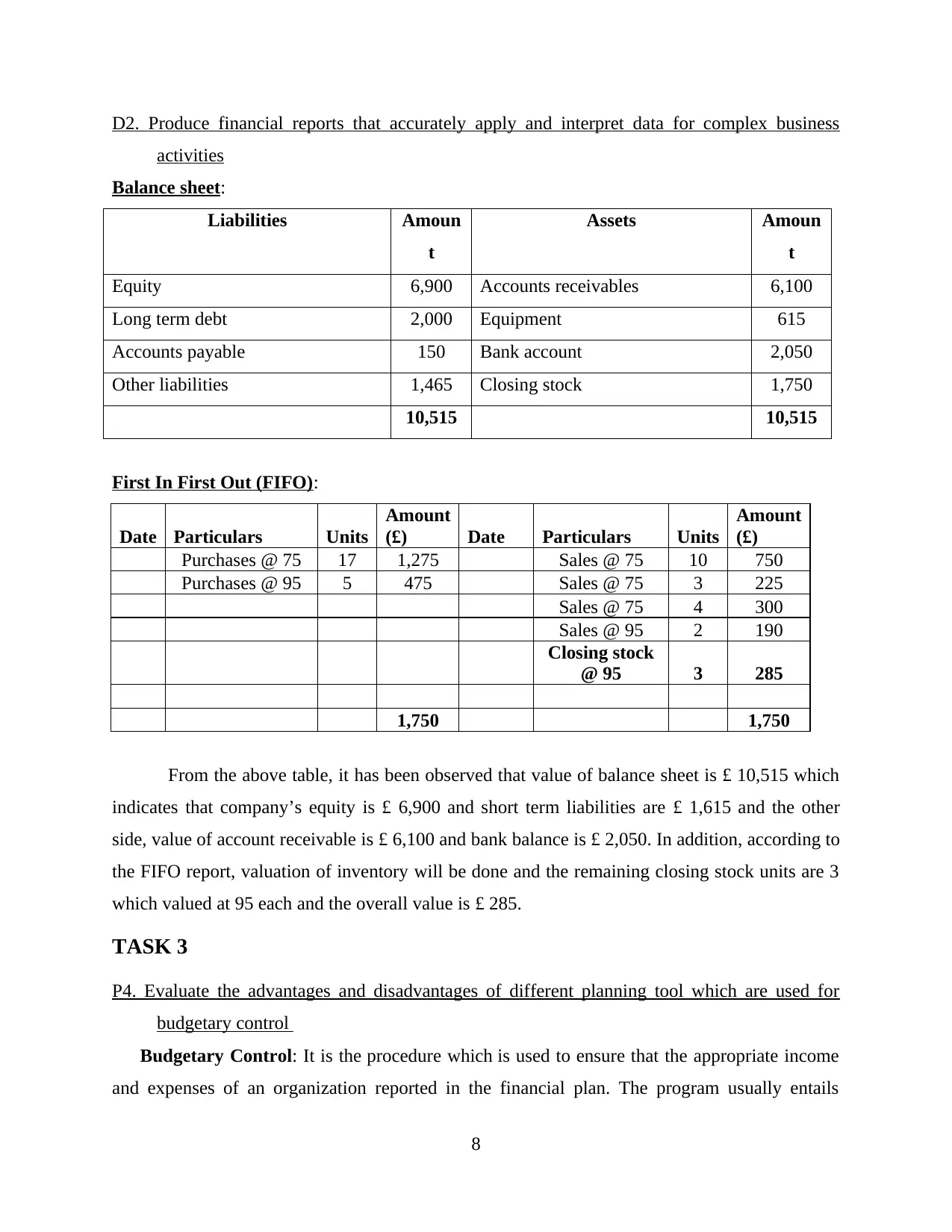

D2. Produce financial reports that accurately apply and interpret data for complex business

activities

Balance sheet:

Liabilities Amoun

t

Assets Amoun

t

Equity 6,900 Accounts receivables 6,100

Long term debt 2,000 Equipment 615

Accounts payable 150 Bank account 2,050

Other liabilities 1,465 Closing stock 1,750

10,515 10,515

First In First Out (FIFO):

Date Particulars Units

Amount

(£) Date Particulars Units

Amount

(£)

Purchases @ 75 17 1,275 Sales @ 75 10 750

Purchases @ 95 5 475 Sales @ 75 3 225

Sales @ 75 4 300

Sales @ 95 2 190

Closing stock

@ 95 3 285

1,750 1,750

From the above table, it has been observed that value of balance sheet is £ 10,515 which

indicates that company’s equity is £ 6,900 and short term liabilities are £ 1,615 and the other

side, value of account receivable is £ 6,100 and bank balance is £ 2,050. In addition, according to

the FIFO report, valuation of inventory will be done and the remaining closing stock units are 3

which valued at 95 each and the overall value is £ 285.

TASK 3

P4. Evaluate the advantages and disadvantages of different planning tool which are used for

budgetary control

Budgetary Control: It is the procedure which is used to ensure that the appropriate income

and expenses of an organization reported in the financial plan. The program usually entails

8

activities

Balance sheet:

Liabilities Amoun

t

Assets Amoun

t

Equity 6,900 Accounts receivables 6,100

Long term debt 2,000 Equipment 615

Accounts payable 150 Bank account 2,050

Other liabilities 1,465 Closing stock 1,750

10,515 10,515

First In First Out (FIFO):

Date Particulars Units

Amount

(£) Date Particulars Units

Amount

(£)

Purchases @ 75 17 1,275 Sales @ 75 10 750

Purchases @ 95 5 475 Sales @ 75 3 225

Sales @ 75 4 300

Sales @ 95 2 190

Closing stock

@ 95 3 285

1,750 1,750

From the above table, it has been observed that value of balance sheet is £ 10,515 which

indicates that company’s equity is £ 6,900 and short term liabilities are £ 1,615 and the other

side, value of account receivable is £ 6,100 and bank balance is £ 2,050. In addition, according to

the FIFO report, valuation of inventory will be done and the remaining closing stock units are 3

which valued at 95 each and the overall value is £ 285.

TASK 3

P4. Evaluate the advantages and disadvantages of different planning tool which are used for

budgetary control

Budgetary Control: It is the procedure which is used to ensure that the appropriate income

and expenses of an organization reported in the financial plan. The program usually entails

8

setting specific targets for budget based administrators, along with a series of incentives that will

be activated until the goals are met. Additionally, estimate and real assessments are regularly

given to those in possession of a line item of property; action is then required to be taken to

remedy any unfavourable variances. By using several planning tools, manager of City

technology limited able to control their budget and predict the operational expenses and income

for better outcomes.

Planning Tools: These tools that direct the measurements of corporate action relevant to an

plan, program, or activity. They will give comprehensive explanations of the action strategy for

the district, and how it has been created. Planning is essential towards meeting goals, if it’s a

corporate entity, an instructional body or perhaps an individual, setting goals and trying to reach

them is an important aspect (Hoque, Parker, Covaleski and Haynes, 2017). It may be various

goal types with differing degrees of significance and time periods. But one thing that stays

popular is to formulate a program that is sufficiently effective to help accomplish such goals.

City Technology Limited can accomplish goals by using an appropriate planning tool. There are

several planning tools which help the organizations as well as managers to take strategic

decisions to maximise company’s earning. Some of them are as follow:

Capital budgeting: It should be viewed as a budget related to evaluating the viability of

long-term investments in businesses such as on vehicles, plants, equipment etc. Department of

Finance provide valuable suggestions which concerns on the premise of this expenditure plan to

allow long-term investments. In relation to City Technology Limited, this planning tool used by

the experts to evaluate the effectiveness as well as profitability of the spending into any project.

Before considering this budget for decision making purpose, managers should evaluate

its benefits and drawbacks those are discussed below:

Benefits: In this budgetary control method, investment appraisal will be carried out

using various investment calculation methods such as Net Present Value (NPV), rate of

return (IRR), payback time etc. Organization makes their investment related decisions on

the basis of low recovery period and positive NPV (Kenyon and Kenyon, 2016). Higher

NPV or IRR are the ways of selecting any project to invest and managers of City

Technology Limited followed it in well manner to maximise overall operational

efficiency and earnings.

9

be activated until the goals are met. Additionally, estimate and real assessments are regularly

given to those in possession of a line item of property; action is then required to be taken to

remedy any unfavourable variances. By using several planning tools, manager of City

technology limited able to control their budget and predict the operational expenses and income

for better outcomes.

Planning Tools: These tools that direct the measurements of corporate action relevant to an

plan, program, or activity. They will give comprehensive explanations of the action strategy for

the district, and how it has been created. Planning is essential towards meeting goals, if it’s a

corporate entity, an instructional body or perhaps an individual, setting goals and trying to reach

them is an important aspect (Hoque, Parker, Covaleski and Haynes, 2017). It may be various

goal types with differing degrees of significance and time periods. But one thing that stays

popular is to formulate a program that is sufficiently effective to help accomplish such goals.

City Technology Limited can accomplish goals by using an appropriate planning tool. There are

several planning tools which help the organizations as well as managers to take strategic

decisions to maximise company’s earning. Some of them are as follow:

Capital budgeting: It should be viewed as a budget related to evaluating the viability of

long-term investments in businesses such as on vehicles, plants, equipment etc. Department of

Finance provide valuable suggestions which concerns on the premise of this expenditure plan to

allow long-term investments. In relation to City Technology Limited, this planning tool used by

the experts to evaluate the effectiveness as well as profitability of the spending into any project.

Before considering this budget for decision making purpose, managers should evaluate

its benefits and drawbacks those are discussed below:

Benefits: In this budgetary control method, investment appraisal will be carried out

using various investment calculation methods such as Net Present Value (NPV), rate of

return (IRR), payback time etc. Organization makes their investment related decisions on

the basis of low recovery period and positive NPV (Kenyon and Kenyon, 2016). Higher

NPV or IRR are the ways of selecting any project to invest and managers of City

Technology Limited followed it in well manner to maximise overall operational

efficiency and earnings.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.