City Technology Ltd. Management Accounting Report: Unit 5 Analysis

VerifiedAdded on 2023/01/10

|19

|5453

|78

Report

AI Summary

This report analyzes the management accounting practices of City Technology Ltd., a manufacturing firm. It begins by explaining management accounting, its essential systems (cost accounting, inventory management, job costing, and price optimization), and reporting methods (budget reports, performance reports, accounts receivables aging reports, and cost accounting reports). The report then calculates costs using marginal costing, highlighting its advantages. It explores the benefits of management accounting systems and their integration into organizational processes. The report further examines planning tools for budgetary control, including advantages and disadvantages. Finally, it compares organizations' responses to financial problems and evaluates planning tools. The report aims to provide a comprehensive understanding of management accounting principles and their practical application within a business context.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1: Explanation of management accounting and the essential requirements of its systems..................3

P2: Methods used for Management Accounting Reporting.....................................................................5

M1: Benefits of Management Accounting Systems.................................................................................6

D1: Integration of Management Accounting Systems and Management Accounting Reporting in

organizational processes.........................................................................................................................6

TASK 2..........................................................................................................................................................7

P3: Calculation of costs............................................................................................................................7

M2: Accurate application of management accounting techniques and producing of appropriate

financial documents...............................................................................................................................10

D2: Producing of financial reports.........................................................................................................12

TASK 3........................................................................................................................................................12

P4: Advantages and Disadvantages for different types of planning tools used for budgetary control. .12

M3: Analysis of use of planning tools and their application..................................................................14

TASK 4........................................................................................................................................................15

P5: Comparison of organizations...........................................................................................................15

M4: Analysis of organization’s response to financial problems.............................................................16

D3: Evaluation of planning tools for accounting....................................................................................17

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

INTRODUCTION...........................................................................................................................................3

TASK 1..........................................................................................................................................................3

P1: Explanation of management accounting and the essential requirements of its systems..................3

P2: Methods used for Management Accounting Reporting.....................................................................5

M1: Benefits of Management Accounting Systems.................................................................................6

D1: Integration of Management Accounting Systems and Management Accounting Reporting in

organizational processes.........................................................................................................................6

TASK 2..........................................................................................................................................................7

P3: Calculation of costs............................................................................................................................7

M2: Accurate application of management accounting techniques and producing of appropriate

financial documents...............................................................................................................................10

D2: Producing of financial reports.........................................................................................................12

TASK 3........................................................................................................................................................12

P4: Advantages and Disadvantages for different types of planning tools used for budgetary control. .12

M3: Analysis of use of planning tools and their application..................................................................14

TASK 4........................................................................................................................................................15

P5: Comparison of organizations...........................................................................................................15

M4: Analysis of organization’s response to financial problems.............................................................16

D3: Evaluation of planning tools for accounting....................................................................................17

CONCLUSION.............................................................................................................................................17

REFERENCES..............................................................................................................................................18

INTRODUCTION

Management Accounting refers to the use of financial data and provisions in such a

manner so that the right conclusions can be drawn and recommendations can be made effectively

and efficiently (Armitage, Webb and Glynn, 2016). This helps the managers a lot to take the

right decisions in the context of the situation and therefore helps in taking the right action.

Therefore, the management accountants are required to focus a lot on analysis and interpretation.

Thus using it they can compare the results of current year with the previous year and the industry

standards to find out the deviations and variances if any so that rectifying action can be taken

quickly to resolve these deviations and variances. For this report, City Technology Ltd. has been

chosen. It is a manufacturing firm is. In this assignment, specific analysis will be made on

understanding of management accounting systems, application of techniques, and explanation of

the use of planning tools. Additionally, comparison of ways in which organizations can make use

of management accounting to solve their financial problems will be discussed as a part of this

project.

TASK 1

P1: Explanation of management accounting and the essential requirements of its

systems

Management Accounting- Management Accounting refers to the use of right techniques

for analysis and interpretation of data in such a manner so that the decisions can be taken

effectively and efficiently by the company without any problems and issues. It can be used by

the managers of City Technology so that the right decisions can be taken which can help in

achievement of goals and objectives as well as maximization of the profits in the future time

period.

Management Accounting Systems-

Cost Accounting System- Cost Accounting System is a system in which the

management accountants analyze the overall costs incurring in an organization (Azudin and

Mansor, 2018). This helps them in making sure that they are able to use different types of

techniques for reducing the costs and therefore maximizing the available level of profits without

any problems and issues. Thus this will lead towards maximization of profits and achievement of

goals and objectives. Therefore the managers of City Technology can make use of it so that they

are able to reduce the costs and maximize the profits.

Essential requirements-

Cost Accounting System should be able to help the management accountants in

identification as well as segregation of the costs.

Management Accounting refers to the use of financial data and provisions in such a

manner so that the right conclusions can be drawn and recommendations can be made effectively

and efficiently (Armitage, Webb and Glynn, 2016). This helps the managers a lot to take the

right decisions in the context of the situation and therefore helps in taking the right action.

Therefore, the management accountants are required to focus a lot on analysis and interpretation.

Thus using it they can compare the results of current year with the previous year and the industry

standards to find out the deviations and variances if any so that rectifying action can be taken

quickly to resolve these deviations and variances. For this report, City Technology Ltd. has been

chosen. It is a manufacturing firm is. In this assignment, specific analysis will be made on

understanding of management accounting systems, application of techniques, and explanation of

the use of planning tools. Additionally, comparison of ways in which organizations can make use

of management accounting to solve their financial problems will be discussed as a part of this

project.

TASK 1

P1: Explanation of management accounting and the essential requirements of its

systems

Management Accounting- Management Accounting refers to the use of right techniques

for analysis and interpretation of data in such a manner so that the decisions can be taken

effectively and efficiently by the company without any problems and issues. It can be used by

the managers of City Technology so that the right decisions can be taken which can help in

achievement of goals and objectives as well as maximization of the profits in the future time

period.

Management Accounting Systems-

Cost Accounting System- Cost Accounting System is a system in which the

management accountants analyze the overall costs incurring in an organization (Azudin and

Mansor, 2018). This helps them in making sure that they are able to use different types of

techniques for reducing the costs and therefore maximizing the available level of profits without

any problems and issues. Thus this will lead towards maximization of profits and achievement of

goals and objectives. Therefore the managers of City Technology can make use of it so that they

are able to reduce the costs and maximize the profits.

Essential requirements-

Cost Accounting System should be able to help the management accountants in

identification as well as segregation of the costs.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Accounting System should be able to make sure that the right techniques are used in

order to reduce the costs and maximize the level of profits.

Inventory Management System- Inventory Management System should be able to help

the management accountants in making sure that the stock is valued in the right manner

and the right techniques are used effectively and efficiently (Bromwich and Scapens,

2016). Thus this helps in making sure that the inventory is valued and managed correctly.

Therefore the managers of City Technology can make use of it so that they are able to

manage the inventory properly.

Essential requirements-

Inventory Management System should be able to manage the stock levels using the right

techniques effectively and efficiently.

Inventory Management System should be able to identify the deviations and variances if

any in the stock valuation so that the right action can be taken to reduce them as soon as

possible.

Job Costing System- Job Costing System can be used by the organizations so that they

are able to make sure that they are able to manage their orders properly without facing

issues and problems. Thus efficiency and effectiveness can be brought in the order

management by the right use of this system (Bui and De Villiers, 2017). As City

Technology is a manufacturing company it can make the right use of this system

effectively and efficiently so it is able to bring the required efficiency and effectiveness in

its order management.

Essential requirements-

Job Costing System should be able to make sure that the job orders are managed

effectively and efficiently. This makes sure that the organization is able to manage them

without facing any kind of issues and problems.

Job Costing System should be able to make sure that the cost of completing job orders is

reduced so that the level of profits can be maximized. Thus in this way the company can

achieve higher level of efficiency as well as effectiveness in its operations.

order to reduce the costs and maximize the level of profits.

Inventory Management System- Inventory Management System should be able to help

the management accountants in making sure that the stock is valued in the right manner

and the right techniques are used effectively and efficiently (Bromwich and Scapens,

2016). Thus this helps in making sure that the inventory is valued and managed correctly.

Therefore the managers of City Technology can make use of it so that they are able to

manage the inventory properly.

Essential requirements-

Inventory Management System should be able to manage the stock levels using the right

techniques effectively and efficiently.

Inventory Management System should be able to identify the deviations and variances if

any in the stock valuation so that the right action can be taken to reduce them as soon as

possible.

Job Costing System- Job Costing System can be used by the organizations so that they

are able to make sure that they are able to manage their orders properly without facing

issues and problems. Thus efficiency and effectiveness can be brought in the order

management by the right use of this system (Bui and De Villiers, 2017). As City

Technology is a manufacturing company it can make the right use of this system

effectively and efficiently so it is able to bring the required efficiency and effectiveness in

its order management.

Essential requirements-

Job Costing System should be able to make sure that the job orders are managed

effectively and efficiently. This makes sure that the organization is able to manage them

without facing any kind of issues and problems.

Job Costing System should be able to make sure that the cost of completing job orders is

reduced so that the level of profits can be maximized. Thus in this way the company can

achieve higher level of efficiency as well as effectiveness in its operations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Price Optimization System- Price Optimization System can be used by the companies

so that the right price can be set by the companies which will make sure that the firms are

able to earn higher level of profits in the future time period without facing issues and

problems.

Essential requirements-

Price Optimization System should be able to manage the prices according to the demand

levels.

Price Optimization System should be able to make sure that the right prices are set to earn

higher level of profits.

P2: Methods used for Management Accounting Reporting

Different types of methods are used for the purpose of Management Accounting

Reporting. These are explained as follows-

Budget Reports- Budget Reports are prepared so that the right forecasts can be made

about the revenues and the expenses can be regulated effectively and efficiently (Christ

and Burritt, 2017). The managers of City Technology can use these reports so that they

are able to make a right estimate about the revenues and the level of expenditures. Thus it

is required from the managers that they should prepare a report using them and must use

them in the right manner. If they are able to frame a right budget report then this will

naturally lead the company towards achievement of sustainable success in the future time

period. These reports are prepared on the basis of various types of budgets such as cash

budget, sales budget, master budget etc. Thus the right conclusions and recommendations

can be made through these reports using the correct techniques of analysis and

interpretation.

Performance Reports- Performance Reports can be prepared so that the performance

can be gauged (Cooper, Ezzamel and Qu, 2017). In City Technology, there are different

departments which are operating such as Finance, HR, Production, Sales, and Marketing.

Therefore it is required from the managers that they must assess the performance of these

departments. This will make sure that the deviations and variations are addressed quickly

so that the required rectifying actions can be taken. The techniques through which the

performance can be increased in the different departments can be used so that higher

level of efficiency as well as effectiveness can be brought in the operations.

Accounts Receivables aging reports- Accounts Receivables Aging Reports can be

prepared in a company to make a list of the debtors who have to do the payment to the

so that the right price can be set by the companies which will make sure that the firms are

able to earn higher level of profits in the future time period without facing issues and

problems.

Essential requirements-

Price Optimization System should be able to manage the prices according to the demand

levels.

Price Optimization System should be able to make sure that the right prices are set to earn

higher level of profits.

P2: Methods used for Management Accounting Reporting

Different types of methods are used for the purpose of Management Accounting

Reporting. These are explained as follows-

Budget Reports- Budget Reports are prepared so that the right forecasts can be made

about the revenues and the expenses can be regulated effectively and efficiently (Christ

and Burritt, 2017). The managers of City Technology can use these reports so that they

are able to make a right estimate about the revenues and the level of expenditures. Thus it

is required from the managers that they should prepare a report using them and must use

them in the right manner. If they are able to frame a right budget report then this will

naturally lead the company towards achievement of sustainable success in the future time

period. These reports are prepared on the basis of various types of budgets such as cash

budget, sales budget, master budget etc. Thus the right conclusions and recommendations

can be made through these reports using the correct techniques of analysis and

interpretation.

Performance Reports- Performance Reports can be prepared so that the performance

can be gauged (Cooper, Ezzamel and Qu, 2017). In City Technology, there are different

departments which are operating such as Finance, HR, Production, Sales, and Marketing.

Therefore it is required from the managers that they must assess the performance of these

departments. This will make sure that the deviations and variations are addressed quickly

so that the required rectifying actions can be taken. The techniques through which the

performance can be increased in the different departments can be used so that higher

level of efficiency as well as effectiveness can be brought in the operations.

Accounts Receivables aging reports- Accounts Receivables Aging Reports can be

prepared in a company to make a list of the debtors who have to do the payment to the

firm (Fiondella and et.al., 2016). In the context of City Technology, it is highly essential

that the organizations are able to make sure that they make a list of the debtors and also

identify those have not paid their dues since a long period of time and thus this will help

in identifying the potential bad debts. Therefore through these reports a high-level of

efficiency as well as effectiveness is required to be brought into the system which h will

make sure that the goals and objectives are achieved without facing any kind of issues

and problems in the future time period. Identification of those debtors who have not paid

dues since a long-period of time can be made easily by using these reports. Further, the

receivables can be segregated as well so that the companies can take the correct action.

Cost Accounting Reports- Cost Accounting Reports can be used to analyze the costs in

an organization (Honggowati and et.al., 2017). The managers of City Technology can use

them to make sure that the excessive costs and unnecessary overheads are identified

quickly so that an action can be taken at the right time which will lead towards

achievement of higher level of efficiency as well as effectiveness. This will lead to

reduction in the overall costs and thus the firm can target the maximization of profits in

the future time period in order to achieve a strategic edge over its rivals. If the overheads

in a particular department are increasing then the reasons can be quickly identified and

immediate steps can also be taken so as to make sure that the firm is reduce them.

Therefore in this manner the required level of productivity can be achieved and thus

short-term and long-term goals and objectives can be attained in the future time period.

M1: Benefits of Management Accounting Systems

There are various types of benefits which the management accounting systems offer to an

organization. Cost Accounting System helps in reducing costs. Also it makes sure that the

required efficiency and effectiveness is achieved. Inventory Management System helps in proper

valuation of inventory. Also, it makes sure that the right management of stock is done. Job

Costing System helps a lot in management of job orders. Also, it can make sure that it is able to

track the job orders without issues and problems. Price Optimization System helps in optimizing

the price and making sure that the right price is charged so that profits can be maximized. Also, it

can help in making sure that prices are changed according to demand levels.

D1: Integration of Management Accounting Systems and Management Accounting

Reporting in organizational processes

Management Accounting Systems can help a lot in making sure that the productivity

level can be increased. They can be integrated in the organizational processes by making use of

right system whenever required. Also, Management Accounting Reporting helps in preparing

reports for the purpose of high-level analysis and interpretation. These reports can be integrated

in the organizational processes by doing proper analysis and interpretation whenever required.

Thus in this manner both the systems as well as reporting methods can be integrated according to

that the organizations are able to make sure that they make a list of the debtors and also

identify those have not paid their dues since a long period of time and thus this will help

in identifying the potential bad debts. Therefore through these reports a high-level of

efficiency as well as effectiveness is required to be brought into the system which h will

make sure that the goals and objectives are achieved without facing any kind of issues

and problems in the future time period. Identification of those debtors who have not paid

dues since a long-period of time can be made easily by using these reports. Further, the

receivables can be segregated as well so that the companies can take the correct action.

Cost Accounting Reports- Cost Accounting Reports can be used to analyze the costs in

an organization (Honggowati and et.al., 2017). The managers of City Technology can use

them to make sure that the excessive costs and unnecessary overheads are identified

quickly so that an action can be taken at the right time which will lead towards

achievement of higher level of efficiency as well as effectiveness. This will lead to

reduction in the overall costs and thus the firm can target the maximization of profits in

the future time period in order to achieve a strategic edge over its rivals. If the overheads

in a particular department are increasing then the reasons can be quickly identified and

immediate steps can also be taken so as to make sure that the firm is reduce them.

Therefore in this manner the required level of productivity can be achieved and thus

short-term and long-term goals and objectives can be attained in the future time period.

M1: Benefits of Management Accounting Systems

There are various types of benefits which the management accounting systems offer to an

organization. Cost Accounting System helps in reducing costs. Also it makes sure that the

required efficiency and effectiveness is achieved. Inventory Management System helps in proper

valuation of inventory. Also, it makes sure that the right management of stock is done. Job

Costing System helps a lot in management of job orders. Also, it can make sure that it is able to

track the job orders without issues and problems. Price Optimization System helps in optimizing

the price and making sure that the right price is charged so that profits can be maximized. Also, it

can help in making sure that prices are changed according to demand levels.

D1: Integration of Management Accounting Systems and Management Accounting

Reporting in organizational processes

Management Accounting Systems can help a lot in making sure that the productivity

level can be increased. They can be integrated in the organizational processes by making use of

right system whenever required. Also, Management Accounting Reporting helps in preparing

reports for the purpose of high-level analysis and interpretation. These reports can be integrated

in the organizational processes by doing proper analysis and interpretation whenever required.

Thus in this manner both the systems as well as reporting methods can be integrated according to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the needs and requirements of the organization. Therefore it is required from the firms that they

analyze whenever required to do so.

TASK 2

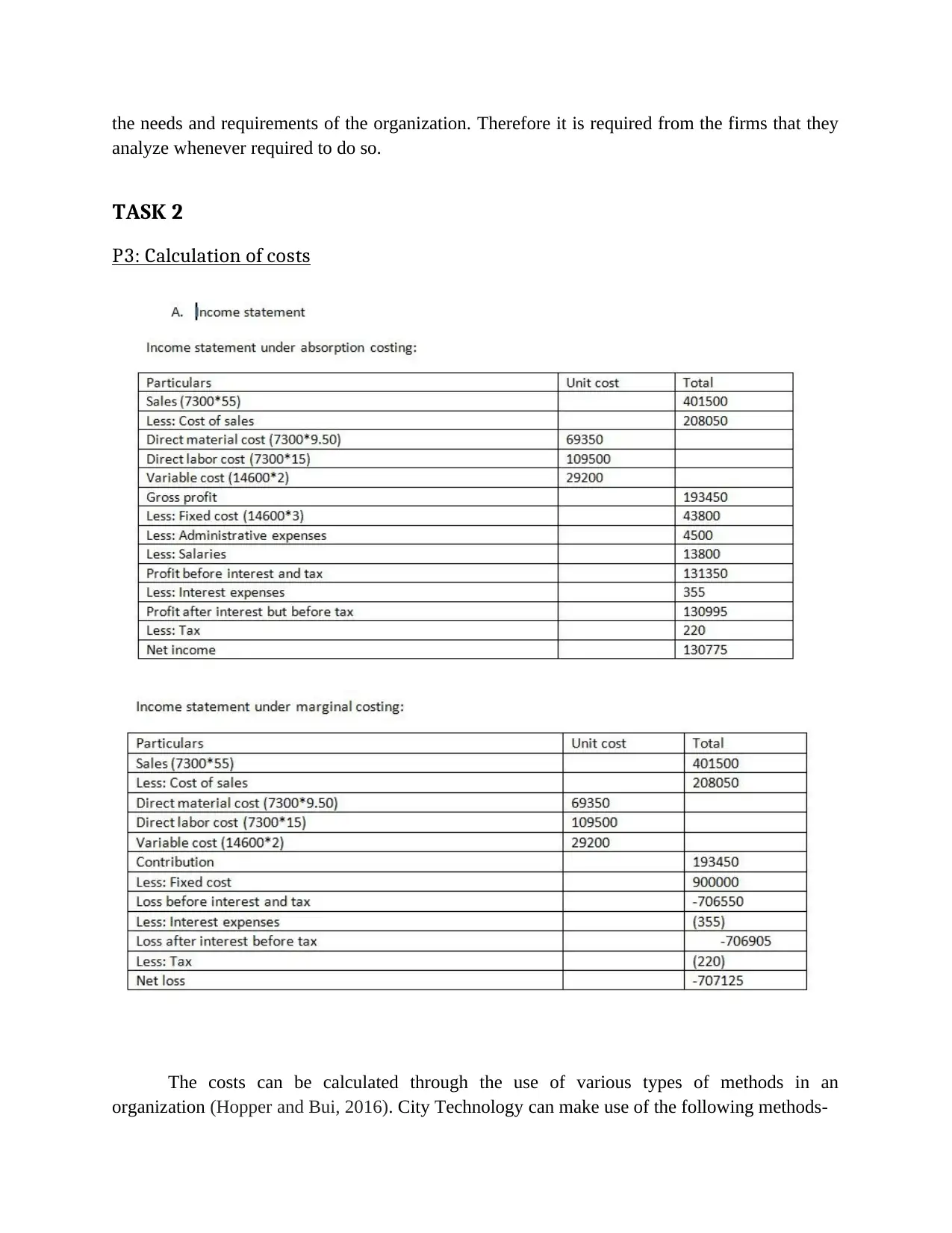

P3: Calculation of costs

The costs can be calculated through the use of various types of methods in an

organization (Hopper and Bui, 2016). City Technology can make use of the following methods-

analyze whenever required to do so.

TASK 2

P3: Calculation of costs

The costs can be calculated through the use of various types of methods in an

organization (Hopper and Bui, 2016). City Technology can make use of the following methods-

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Marginal Costing-

Marginal Costing is a technique which is used so that the variable cost is charged to the

units of production and the fixed cost is written off against the contribution level. This technique

is highly effective for the organization so that it can compute its costs. City Technology’s

managers make use of this technique so that they are able to get the work done without

encountering any kind of issues and problems in the future time period.

Advantages-

Marginal Costing system helps a lot in order to take the right decisions on the basis of

consideration made for various types of factors (Järvenpää and Länsiluoto, 2016). Thus

the managers of City Technology can make use of this system so that they are able to

take the right decisions.

In Marginal Costing system, the cost of sales can be calculated easily and therefore this

makes it quite easier to understand. Thus it is beneficial for the management of City

Technology so that they are able to make sure that they can calculate the right cost of

sales.

Disadvantages-

Marginal Costing System makes an assumption that all the expenses are either fixed or

variable in nature. This does not hold true for some of the expenses. Therefore this

creates a disadvantage for the managers of City Technology.

Marginal Costing System makes it quite difficult to segregate the costs and sometimes

the results which are obtained can be inaccurate. Thus this is a disadvantage which is

created for the managers of City Technology.

Absorption Costing-

Absorption costing technique can be used effectively for the purpose of calculation of the

total cost which is involved in the manufacturing of a product or providing a service by

an organization (Järvinen, 2016). By using it, a company can make sure that it is able to

calculate the right costs without problems and issues. Therefore the managers of City

Technology can make use of this technique so that they are able to get the accurate

estimate of costs which are likely to be incurred in the organization.

Marginal Costing is a technique which is used so that the variable cost is charged to the

units of production and the fixed cost is written off against the contribution level. This technique

is highly effective for the organization so that it can compute its costs. City Technology’s

managers make use of this technique so that they are able to get the work done without

encountering any kind of issues and problems in the future time period.

Advantages-

Marginal Costing system helps a lot in order to take the right decisions on the basis of

consideration made for various types of factors (Järvenpää and Länsiluoto, 2016). Thus

the managers of City Technology can make use of this system so that they are able to

take the right decisions.

In Marginal Costing system, the cost of sales can be calculated easily and therefore this

makes it quite easier to understand. Thus it is beneficial for the management of City

Technology so that they are able to make sure that they can calculate the right cost of

sales.

Disadvantages-

Marginal Costing System makes an assumption that all the expenses are either fixed or

variable in nature. This does not hold true for some of the expenses. Therefore this

creates a disadvantage for the managers of City Technology.

Marginal Costing System makes it quite difficult to segregate the costs and sometimes

the results which are obtained can be inaccurate. Thus this is a disadvantage which is

created for the managers of City Technology.

Absorption Costing-

Absorption costing technique can be used effectively for the purpose of calculation of the

total cost which is involved in the manufacturing of a product or providing a service by

an organization (Järvinen, 2016). By using it, a company can make sure that it is able to

calculate the right costs without problems and issues. Therefore the managers of City

Technology can make use of this technique so that they are able to get the accurate

estimate of costs which are likely to be incurred in the organization.

Advantages-

Fair pricing- Absorption Costing Technique helps a lot to the organizations in making

sure that they set a right price for their products and services (Kumarasiri and Jubb,

2016). Thus it is advantageous for the managers of City Technology. This is so because

they can set the right price and can earn higher level of profits.

Importance of fixed cost- Absorption Costing Technique is quite helpful for the

companies so that they understand the importance of fixed cost. Therefore it is

advantageous for the managers of City Technology.

Disadvantages-

Not suitable for decision-making- Absorption Costing Technique is not suitable for the

purpose of decision-making. The managers are not able to take the right decisions by

using this technique. Thus for the managers of City Technology this creates a

disadvantage.

Not suitable for flexible budget- Absorption Costing Technique is not suitable for

flexible budget. The managers are not able to prepare a flexible budget for different

departments by using this technique. Therefore for the managers of City Technology this

can create a disadvantage as this can lead towards problems.

Fair pricing- Absorption Costing Technique helps a lot to the organizations in making

sure that they set a right price for their products and services (Kumarasiri and Jubb,

2016). Thus it is advantageous for the managers of City Technology. This is so because

they can set the right price and can earn higher level of profits.

Importance of fixed cost- Absorption Costing Technique is quite helpful for the

companies so that they understand the importance of fixed cost. Therefore it is

advantageous for the managers of City Technology.

Disadvantages-

Not suitable for decision-making- Absorption Costing Technique is not suitable for the

purpose of decision-making. The managers are not able to take the right decisions by

using this technique. Thus for the managers of City Technology this creates a

disadvantage.

Not suitable for flexible budget- Absorption Costing Technique is not suitable for

flexible budget. The managers are not able to prepare a flexible budget for different

departments by using this technique. Therefore for the managers of City Technology this

can create a disadvantage as this can lead towards problems.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2: Accurate application of management accounting techniques and producing of

appropriate financial documents

appropriate financial documents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management Accounting Techniques of Marginal and Absorption Costing can be used in

the right manner in the organization. This is so because both of them have to be used correctly so

that the accurate picture of financial position of the company can be obtained. Thus the managers

of City Technology should make sure that they use them correctly so that they can accurately

determine the costs and can also make sure to draw the right conclusions and recommendations

from the results obtained by using these techniques.

the right manner in the organization. This is so because both of them have to be used correctly so

that the accurate picture of financial position of the company can be obtained. Thus the managers

of City Technology should make sure that they use them correctly so that they can accurately

determine the costs and can also make sure to draw the right conclusions and recommendations

from the results obtained by using these techniques.

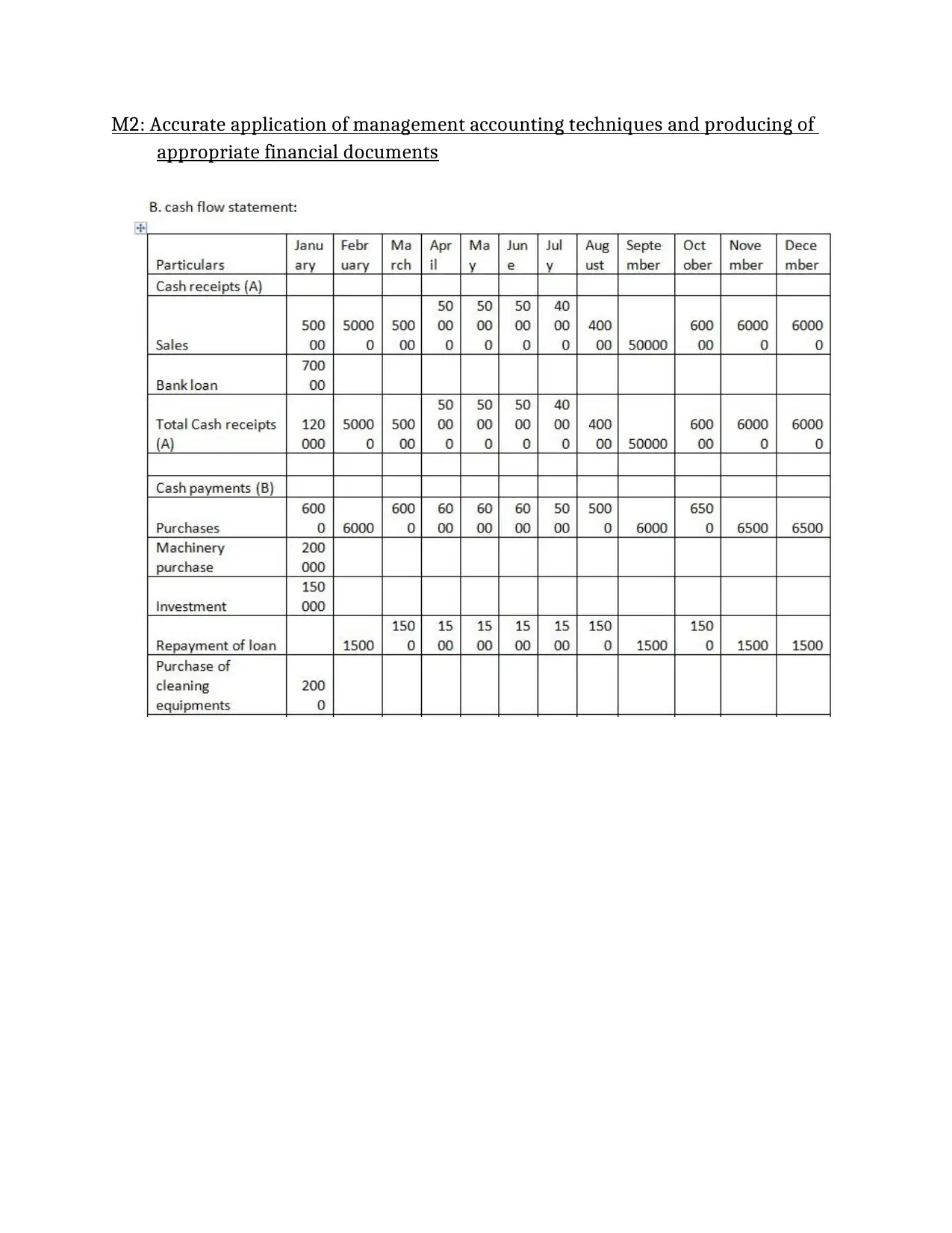

D2: Producing of financial reports

Interpretation- By analyzing the Cash Flow Statement of City Technology, it can be

interpreted that surplus cash is available for the firm all throughout the year. Thus it can be said

that firm manages its cash resources effectively and efficiently and makes sure that it is able to

have surplus cash available with it for day-to-day activities at any time whenever the need

occurs. From the Balance Sheet, it can be interpreted that the financial position of the company is

quite strong. Thus it can be said that the firm is making the right use of techniques of

management accounting in its operations.

Financial reports can be used by the managers of a particular organization so that they are

able to make the right judgments from the financial position obtained from them. In the context

of City Technology, it becomes highly essential that they are able to get the right work done

without the creation of problems and issues. Thus this helps the managers to take the right

decisions after analyzing the various types of aspects and thus by doing so they can make sure

that the level of efficiency and effectiveness in the company rises and thus it will be able to

maximize the level of profits by taking correct judgments.

TASK 3

P4: Advantages and Disadvantages for different types of planning tools used for

budgetary control

There are different types of planning tools which can be used for the purpose of

budgetary control by the organizations. These are explained as follows-

Cash Budget-

Cash Budget can be used by the organizations to forecast cash receipts and set a limit for

cash expenditures for a particular period of time mostly a year (Lachmann, Trapp and Trapp,

2017). This can be used by management of City Technology so that they are able to effectively

forecast and make assumptions using the right techniques.

Advantages-

Cash Budget can be used by the organizations so that they are able to take the right route

for planning for cash operations. Thus in this way it is advantageous for City

Technology’s managers.

Cash Budget can be used by the firms so that they are able to make sure that they can

manage the cash and liquid assets well. Therefore in this way it creates advantage for the

managers of City Technology.

Interpretation- By analyzing the Cash Flow Statement of City Technology, it can be

interpreted that surplus cash is available for the firm all throughout the year. Thus it can be said

that firm manages its cash resources effectively and efficiently and makes sure that it is able to

have surplus cash available with it for day-to-day activities at any time whenever the need

occurs. From the Balance Sheet, it can be interpreted that the financial position of the company is

quite strong. Thus it can be said that the firm is making the right use of techniques of

management accounting in its operations.

Financial reports can be used by the managers of a particular organization so that they are

able to make the right judgments from the financial position obtained from them. In the context

of City Technology, it becomes highly essential that they are able to get the right work done

without the creation of problems and issues. Thus this helps the managers to take the right

decisions after analyzing the various types of aspects and thus by doing so they can make sure

that the level of efficiency and effectiveness in the company rises and thus it will be able to

maximize the level of profits by taking correct judgments.

TASK 3

P4: Advantages and Disadvantages for different types of planning tools used for

budgetary control

There are different types of planning tools which can be used for the purpose of

budgetary control by the organizations. These are explained as follows-

Cash Budget-

Cash Budget can be used by the organizations to forecast cash receipts and set a limit for

cash expenditures for a particular period of time mostly a year (Lachmann, Trapp and Trapp,

2017). This can be used by management of City Technology so that they are able to effectively

forecast and make assumptions using the right techniques.

Advantages-

Cash Budget can be used by the organizations so that they are able to take the right route

for planning for cash operations. Thus in this way it is advantageous for City

Technology’s managers.

Cash Budget can be used by the firms so that they are able to make sure that they can

manage the cash and liquid assets well. Therefore in this way it creates advantage for the

managers of City Technology.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.