The Influence of Civil Servants on Online Loan Aggregator Platforms

VerifiedAdded on 2021/05/13

|20

|6916

|77

Project

AI Summary

This MBA research project investigates the factors influencing Malaysian civil servants' intention to use online loan aggregator platforms, specifically focusing on the MyAzZahra portal. The study examines the impact of Fintech on the cooperative credit landscape and explores the application of the Technology Acceptance Model (TAM), considering factors such as perceived ease of use, perceived usefulness, trust, and attitude towards technology. The research aims to identify the key drivers and barriers to adoption, providing insights into the low acceptance rate of these platforms among government servants. The project also assesses the performance of cooperatives in Malaysia, the role of microfinance, and the significance of digital transformation in the financial sector. The research employs a case study approach, analyzing the MyAzZahra platform's features and offerings to understand how they influence users' behavior and loan application decisions. The study's findings are expected to provide valuable information for the National Cooperative Movement and other stakeholders in the financial industry, offering insights into improving user engagement and platform adoption.

THE OTHMAN YEOP ABDULLAH GRADUATE SCHOOL OF

BUSINESS (OYAGSB)

INDIVIDUAL ASSIGNMENT

ODMR6013 - BUSINESS RESEARCH METHODS

RESEARCH TITLE:

THE INFLUENCES OF CIVIL SERVANTS ATTITUDE ON

INTENTION TO USE ONLINE LOAN AGGREGATOR PLATFORM:

A CASE STUDY OF MYAZZAHRA PORTAL

SEMESTER : FIRST SESSION 2020/2021 (201)

PROGRAMME : MASTER OF BUSINESS ADMINISTRATION (MBA)

GROUP NAME : ANGKASA (A)

PREPARED FOR : ASSOC. PROF. DR ZAEMAH ZAINUDDIN

PREPARED BY : NURHANA BINTI ZAHRULLAIL

STUDENT ID : 826736

DATELINE : 18th APRIL 2021

BUSINESS (OYAGSB)

INDIVIDUAL ASSIGNMENT

ODMR6013 - BUSINESS RESEARCH METHODS

RESEARCH TITLE:

THE INFLUENCES OF CIVIL SERVANTS ATTITUDE ON

INTENTION TO USE ONLINE LOAN AGGREGATOR PLATFORM:

A CASE STUDY OF MYAZZAHRA PORTAL

SEMESTER : FIRST SESSION 2020/2021 (201)

PROGRAMME : MASTER OF BUSINESS ADMINISTRATION (MBA)

GROUP NAME : ANGKASA (A)

PREPARED FOR : ASSOC. PROF. DR ZAEMAH ZAINUDDIN

PREPARED BY : NURHANA BINTI ZAHRULLAIL

STUDENT ID : 826736

DATELINE : 18th APRIL 2021

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DECLARATION OF OWN WORK

Name : NURHANA ZAHRULLAIL

Matric No : 826736

Title of Research: The Influence of Civil Servants Attitude on Intention to use Online

Loan Aggregator Platform

I confirm that the above work was solely undertaken by myself and that no help was

provided from other sources as those allowed. All sections of the paper that use quotes or

describe an argument or concept developed by another author have been referenced,

including all secondary literature used, to show that this material has been adopted to

support my work.

I understand that any false claim for this work will be penalized in accordance with the

University regulations.

Signature

Date : 4th March 2021

TABLE OF CONTENT

ABSTRACT 4

CHAPTER ONE: INTRODUCTION AND PROBLEMS IDENTIFICATION 5

1.0 BACKGROUND OF THE STUDY 5

1.2 PROBLEM STATEMENT 7

1.3 RESEARCH OBJECTIVES 8

1.4 SCOPE OF INVESTIGATION 8

1.5 SIGNIFICANCE OF THE STUDY 9

Name : NURHANA ZAHRULLAIL

Matric No : 826736

Title of Research: The Influence of Civil Servants Attitude on Intention to use Online

Loan Aggregator Platform

I confirm that the above work was solely undertaken by myself and that no help was

provided from other sources as those allowed. All sections of the paper that use quotes or

describe an argument or concept developed by another author have been referenced,

including all secondary literature used, to show that this material has been adopted to

support my work.

I understand that any false claim for this work will be penalized in accordance with the

University regulations.

Signature

Date : 4th March 2021

TABLE OF CONTENT

ABSTRACT 4

CHAPTER ONE: INTRODUCTION AND PROBLEMS IDENTIFICATION 5

1.0 BACKGROUND OF THE STUDY 5

1.2 PROBLEM STATEMENT 7

1.3 RESEARCH OBJECTIVES 8

1.4 SCOPE OF INVESTIGATION 8

1.5 SIGNIFICANCE OF THE STUDY 9

1.6 FRAMEWORK OF THE STUDY 10

1.7 THE TECHNOLOGY ACCEPTANCE MODEL (TAM) 10

Perceived Ease of Use 11

Perceived Usefulness 11

Trust 12

Attitude towards Using Technology 12

Behavioral Intention to Use 13

CHAPTER TWO: THE PAST AND PRESENT: AN OVERVIEW 14

2.1 ASSESSING THE PERFORMANCE OF CO-OPERATIVES IN MALAYSIA 14

2.2 COOPERATIVES AND MICROFINANCE: ANY REVOLUTION? 16

CHAPTER THREE: RESEARCH METHODOLOGY 18

3.1 hypothesis and research model 18

3.2 DATA AND SURVEY INSTRUMENT 20

3.3 DATA COLLECTION and analysis 21

REFERENCES 23

ABSTRACT

With competition from online lenders and web aggregators offering near microloans

especially for credit cooperatives are focusing on digital experiences with the development of

financial technology (Fintech) in Malaysia give significance impact that will make lending

easy and more accessible to The Malaysian Co-operative Movement. Most of financial

institutions has been move from a traditional transaction into online transaction. Now,

customer can apply a personal financing through online and it replace the conventional way of

application form walk in at the counter. As a result, the MyAzZahra site was created to serve

1.7 THE TECHNOLOGY ACCEPTANCE MODEL (TAM) 10

Perceived Ease of Use 11

Perceived Usefulness 11

Trust 12

Attitude towards Using Technology 12

Behavioral Intention to Use 13

CHAPTER TWO: THE PAST AND PRESENT: AN OVERVIEW 14

2.1 ASSESSING THE PERFORMANCE OF CO-OPERATIVES IN MALAYSIA 14

2.2 COOPERATIVES AND MICROFINANCE: ANY REVOLUTION? 16

CHAPTER THREE: RESEARCH METHODOLOGY 18

3.1 hypothesis and research model 18

3.2 DATA AND SURVEY INSTRUMENT 20

3.3 DATA COLLECTION and analysis 21

REFERENCES 23

ABSTRACT

With competition from online lenders and web aggregators offering near microloans

especially for credit cooperatives are focusing on digital experiences with the development of

financial technology (Fintech) in Malaysia give significance impact that will make lending

easy and more accessible to The Malaysian Co-operative Movement. Most of financial

institutions has been move from a traditional transaction into online transaction. Now,

customer can apply a personal financing through online and it replace the conventional way of

application form walk in at the counter. As a result, the MyAzZahra site was created to serve

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

as an online loan aggregator for cooperative credit society unions. To ensure that they meet

industry trends, all credit cooperative unions have been gathered into a single platform. The

aim of this thesis is to look at Malaysian government servants' attitudes toward using a loan

aggregator website. Customer retention and engagement are top priorities for a service

company. Rapid developments in the Fintech sector are disrupting the financial services

environments, posing both opportunities and challenges for customers and service providers.

From artificial intelligence to bitcoin, the Fintech industry is transforming the financial

services landscapes, creating both opportunities and challenges for consumers and service

providers and regulators alike

Keyword: Online Loan Aggregator, Fintech, Cooperative Credit, Microloans, Civil Servants

and Technology Acceptance Model (TAM)

CHAPTER ONE: INTRODUCTION AND PROBLEMS IDENTIFICATION

1.0 BACKGROUND OF THE STUDY

Nowadays, the financial technology (fintech) has emerged with the aim to improve and

automate the conventional process to smooth operations (Chishti & Barberis 2016; Nicoletti

et al 2017). Studies by Lee and Shin (2018) explained the use of fintech helps the

organizations in their daily operation by utilizing technology advancement and algorithm.

Other studies by Kajan (2020), believes that when fintech emerged it applied for back-end

operation and being used by financial institutions. Gomber et al (2018) elaborate that

previously people thought that the bank business will never die if they have a many branches

and government support.

industry trends, all credit cooperative unions have been gathered into a single platform. The

aim of this thesis is to look at Malaysian government servants' attitudes toward using a loan

aggregator website. Customer retention and engagement are top priorities for a service

company. Rapid developments in the Fintech sector are disrupting the financial services

environments, posing both opportunities and challenges for customers and service providers.

From artificial intelligence to bitcoin, the Fintech industry is transforming the financial

services landscapes, creating both opportunities and challenges for consumers and service

providers and regulators alike

Keyword: Online Loan Aggregator, Fintech, Cooperative Credit, Microloans, Civil Servants

and Technology Acceptance Model (TAM)

CHAPTER ONE: INTRODUCTION AND PROBLEMS IDENTIFICATION

1.0 BACKGROUND OF THE STUDY

Nowadays, the financial technology (fintech) has emerged with the aim to improve and

automate the conventional process to smooth operations (Chishti & Barberis 2016; Nicoletti

et al 2017). Studies by Lee and Shin (2018) explained the use of fintech helps the

organizations in their daily operation by utilizing technology advancement and algorithm.

Other studies by Kajan (2020), believes that when fintech emerged it applied for back-end

operation and being used by financial institutions. Gomber et al (2018) elaborate that

previously people thought that the bank business will never die if they have a many branches

and government support.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Meanwhile, Kaufan (2014) explained the myths of "too big to fail" (TBTF) theory asserts that

certain corporations, particularly financial institutions, are so large and so interconnected that

their failure would be disastrous to the greater economic system, and that they therefore must

be supported by governments when they face potential failure. According to Westerman et al

(2018), with an innovation in a financial sector lead the increasing number of investment

where most of financial institutions are heavily investing in technology and they are going to

transform their business. Let me begin with a question: How financial institutions can be

successful in their transformation? The answer is a big data. It is a customer analytic, real-

time and predictive analytics. Big data technologies being used to collect, organize, process

and analyse a large set of data. The aims are to find a pattern and create a value information of

these data. The analysed data is important because it gives a relevant information needed for

decision making process.

Herbert (2017) discussed the use of this technology has been shifted from a back end oriented

to a consumer-oriented to give a convenience to the customers. Habidin et al (2020) stated

that cooperatives are regarded as significant employers and investors were collectively

constitute a significant component of Malaysia's social and economic ecosystems.

Cooperatives contribute greatly to the national economy as an integral component of the

social and economic communities. Their social and economic activities are regarded as

important as those made by businesses and non-profit organizations. In Malaysia, the

cooperative model of micro-lending is proving to be extremely popular, as co-operative

institutions make use of local economic capital and play an important role in mobilizing

micro-savings and micro-lending (Joseph, Vazhacharickal & Salih 2020).

Cooperative loans in Malaysia (commonly known as Pinjaman Koperasi in Malay) are credit

services provided by 478 credit cooperatives registered with the Cooperative Commission of

Malaysia (SKM) to their members who earn daily salary income, especially in the public

sector, legislative and private bodies. coops have been received a code for salary deduction

from ANGKASA (Musa et al, 2020). Hassan, Samad, & Shafii (2018) stated that there are

many credit coops are offering a financing product to the government servant. The rate is

competitive in the market and the procedure is more linen. Moreover, the Congress of Unions

of Employees in the Public and Civil Services (CUEPACS) accepts these loans because they

help civil servants overcome financial difficulties and reduce loan shark borrowing (The Star,

dated 14th June 2019). As a result, ANGKASA denied any participation in the suspected

syndicated loan scheme, alleging that the syndicate used the ANGKASA name and logo to

deceive many civil servants.

certain corporations, particularly financial institutions, are so large and so interconnected that

their failure would be disastrous to the greater economic system, and that they therefore must

be supported by governments when they face potential failure. According to Westerman et al

(2018), with an innovation in a financial sector lead the increasing number of investment

where most of financial institutions are heavily investing in technology and they are going to

transform their business. Let me begin with a question: How financial institutions can be

successful in their transformation? The answer is a big data. It is a customer analytic, real-

time and predictive analytics. Big data technologies being used to collect, organize, process

and analyse a large set of data. The aims are to find a pattern and create a value information of

these data. The analysed data is important because it gives a relevant information needed for

decision making process.

Herbert (2017) discussed the use of this technology has been shifted from a back end oriented

to a consumer-oriented to give a convenience to the customers. Habidin et al (2020) stated

that cooperatives are regarded as significant employers and investors were collectively

constitute a significant component of Malaysia's social and economic ecosystems.

Cooperatives contribute greatly to the national economy as an integral component of the

social and economic communities. Their social and economic activities are regarded as

important as those made by businesses and non-profit organizations. In Malaysia, the

cooperative model of micro-lending is proving to be extremely popular, as co-operative

institutions make use of local economic capital and play an important role in mobilizing

micro-savings and micro-lending (Joseph, Vazhacharickal & Salih 2020).

Cooperative loans in Malaysia (commonly known as Pinjaman Koperasi in Malay) are credit

services provided by 478 credit cooperatives registered with the Cooperative Commission of

Malaysia (SKM) to their members who earn daily salary income, especially in the public

sector, legislative and private bodies. coops have been received a code for salary deduction

from ANGKASA (Musa et al, 2020). Hassan, Samad, & Shafii (2018) stated that there are

many credit coops are offering a financing product to the government servant. The rate is

competitive in the market and the procedure is more linen. Moreover, the Congress of Unions

of Employees in the Public and Civil Services (CUEPACS) accepts these loans because they

help civil servants overcome financial difficulties and reduce loan shark borrowing (The Star,

dated 14th June 2019). As a result, ANGKASA denied any participation in the suspected

syndicated loan scheme, alleging that the syndicate used the ANGKASA name and logo to

deceive many civil servants.

ANGKASA has taken the initiative to partner with Orion IXL Berhad through its subsidiaries

to explore a loan aggregator website, namely the MyAzZahra portal's,

https://www.myazzahra.com/ in order to ensure that the credit cooperative movement is on

par with financial institutions. MyAzZahra portals serve as an aggregator of cooperative

finance goods, allowing applicants to pick and select the products best meet their needs and

apply directly to the cooperatives through the portal. Its offerings include FinTech-based

Loan Management Systems, call centre services, financial consulting, and system integration,

among others. MyAzZahra portals were crucial in the development of cooperative enterprise

and, eventually, a larger community.

The MyAzZahra portal's financing application system gives applicants a considerable

advantage in terms of choosing, applying, and monitoring their applications in an easy, fast,

secure, and straightforward atmosphere, as well as reducing the involvement of middlemen or

brokers and avoiding potential fraud, violence, and wrongdoing by credit firms or loan sharks

(Othman et al 2018). According to research conducted by Malaysian civil servants, low

acceptance of online loan platforms is attributed to a lack of understanding after one year of

operation. As a result, the aim of this paper is to examine the characteristics of customers

(borrowers) among public servants who plan to use an online loan aggregator site. About the

increased use of technology for microfinance loans, little study has been done on the factors

that drive cooperative members to apply for loans electronically.

1.2 PROBLEM STATEMENT

"FinTech" or a compound term of Financial Technology refers as a newly emerged industry

that utilizes IT-centered technologies which aims to boost the efficiency of the financial

ecosystem. Since its inception, FinTech has successfully established its presence in the global

financial industry due to the benefits and advantages of the system. In October 2018, Orion

and Sukaniaga Sdn Bhd entered into an agreement with Angkasa, Malaysia’s national co-

operative movement, to provide a fintech end-to-end loan application and approval platform

called MyAngkasa Az-Zahra (MyAzZahra) for its credit co-operatives to offer microloans to

government staff and targeting the platform-MyAzZahra to handle the approvals for RM1

billion microloans. However, the research studies that highlight the importance of FinTech are

scarce. Specifically, the study pertaining to the consumers' attitude towards FinTech products

and services which is microloans application from credit cooperatives to the government

servants remains unexplored by most of the studies. There is also got situation where they

unable to change because of the requirement of the support system. For example, is where

to explore a loan aggregator website, namely the MyAzZahra portal's,

https://www.myazzahra.com/ in order to ensure that the credit cooperative movement is on

par with financial institutions. MyAzZahra portals serve as an aggregator of cooperative

finance goods, allowing applicants to pick and select the products best meet their needs and

apply directly to the cooperatives through the portal. Its offerings include FinTech-based

Loan Management Systems, call centre services, financial consulting, and system integration,

among others. MyAzZahra portals were crucial in the development of cooperative enterprise

and, eventually, a larger community.

The MyAzZahra portal's financing application system gives applicants a considerable

advantage in terms of choosing, applying, and monitoring their applications in an easy, fast,

secure, and straightforward atmosphere, as well as reducing the involvement of middlemen or

brokers and avoiding potential fraud, violence, and wrongdoing by credit firms or loan sharks

(Othman et al 2018). According to research conducted by Malaysian civil servants, low

acceptance of online loan platforms is attributed to a lack of understanding after one year of

operation. As a result, the aim of this paper is to examine the characteristics of customers

(borrowers) among public servants who plan to use an online loan aggregator site. About the

increased use of technology for microfinance loans, little study has been done on the factors

that drive cooperative members to apply for loans electronically.

1.2 PROBLEM STATEMENT

"FinTech" or a compound term of Financial Technology refers as a newly emerged industry

that utilizes IT-centered technologies which aims to boost the efficiency of the financial

ecosystem. Since its inception, FinTech has successfully established its presence in the global

financial industry due to the benefits and advantages of the system. In October 2018, Orion

and Sukaniaga Sdn Bhd entered into an agreement with Angkasa, Malaysia’s national co-

operative movement, to provide a fintech end-to-end loan application and approval platform

called MyAngkasa Az-Zahra (MyAzZahra) for its credit co-operatives to offer microloans to

government staff and targeting the platform-MyAzZahra to handle the approvals for RM1

billion microloans. However, the research studies that highlight the importance of FinTech are

scarce. Specifically, the study pertaining to the consumers' attitude towards FinTech products

and services which is microloans application from credit cooperatives to the government

servants remains unexplored by most of the studies. There is also got situation where they

unable to change because of the requirement of the support system. For example, is where

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

there are coops that want to change but their fund is come from financial institution and they

still required a physical form of loan applications. Not only that, but the resistance also come

from customer where they prefer to deal with offline transaction rather than go online. There

are many restrictions such as afraid with the security of online transaction, not a tech savvy,

facing difficulties, and many other factors. Sometimes, the process is failed to meet their ideal

expectations. This is a normal effect of innovation resistance when doing a change. The

adoption rate of new young generation is greater than their parents.

1.3 RESEARCH OBJECTIVES

From the preceding highlighted issues, the key goal of this analysis is to examine the

evolution of the major digital technology- MyAzZahra portals with enhancement of new

offerings such as marketplace, unified contact centre, business-to-business (B2B) framework

(cooperative borrowings from financial institutions), digital wallet or e-wallet facility, and

payment and collection gateway.

RO 1: To identify the potential factors that influence consumers' intention to adopt

online loan aggregator platform.

RO 2: To examine the positive impact of perceived ease of use, perceived usefulness,

trust, and user innovation for attitude towards using an online loan aggregator

platform and the positive impact of attitude towards use for behavioral intention

to use online loan aggregator platform

1.4 SCOPE OF INVESTIGATION

This paper employs MyAzZahra, an award-winning “Digital Financial Services” (DFS)

platform for public servants, as a research object to investigate the key factors that influence

lenders' loan confidence. It also investigates the effects of these influences on lending intent.

1.5 SIGNIFICANCE OF THE STUDY

The Malaysian National Cooperative Movement (MNCM) was active in developing

MyAzZahra Portal, which provides digitalization of the online loan application process for

cooperatives that provide an integrated cooperative credit scheme as well give convenience to

the cooperative members in Malaysia where they can have access to all those information’s

regarding loan financing provides by cooperative movements. The applicant can assess the

portal from anywhere and anytime. They can apply personal financing through online without

still required a physical form of loan applications. Not only that, but the resistance also come

from customer where they prefer to deal with offline transaction rather than go online. There

are many restrictions such as afraid with the security of online transaction, not a tech savvy,

facing difficulties, and many other factors. Sometimes, the process is failed to meet their ideal

expectations. This is a normal effect of innovation resistance when doing a change. The

adoption rate of new young generation is greater than their parents.

1.3 RESEARCH OBJECTIVES

From the preceding highlighted issues, the key goal of this analysis is to examine the

evolution of the major digital technology- MyAzZahra portals with enhancement of new

offerings such as marketplace, unified contact centre, business-to-business (B2B) framework

(cooperative borrowings from financial institutions), digital wallet or e-wallet facility, and

payment and collection gateway.

RO 1: To identify the potential factors that influence consumers' intention to adopt

online loan aggregator platform.

RO 2: To examine the positive impact of perceived ease of use, perceived usefulness,

trust, and user innovation for attitude towards using an online loan aggregator

platform and the positive impact of attitude towards use for behavioral intention

to use online loan aggregator platform

1.4 SCOPE OF INVESTIGATION

This paper employs MyAzZahra, an award-winning “Digital Financial Services” (DFS)

platform for public servants, as a research object to investigate the key factors that influence

lenders' loan confidence. It also investigates the effects of these influences on lending intent.

1.5 SIGNIFICANCE OF THE STUDY

The Malaysian National Cooperative Movement (MNCM) was active in developing

MyAzZahra Portal, which provides digitalization of the online loan application process for

cooperatives that provide an integrated cooperative credit scheme as well give convenience to

the cooperative members in Malaysia where they can have access to all those information’s

regarding loan financing provides by cooperative movements. The applicant can assess the

portal from anywhere and anytime. They can apply personal financing through online without

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

need to walk-in physically to coop office. The target market is 90% government e-services by

ANGKASA. The user of the loan aggregator platform can view the list of cooperatives that

provide loan, compare the rate, choose whichever suit with their criteria and make the

application through online.

The platform been developed to become the first coop’s loan aggregator platform. The main

functions of MyAzZahra Portal are an aggregator of coop’s financing products where the

Malaysian government servants can freely choose whichever products that suit their needs

and make the application directly to the respective cooperatives via the portal. The financing

application system provided by MyAzZahra Portal gives the applicant significant advantage

to choose, apply and monitor their applications in an easy, fast, safe and transparent

environment. However, the adoption rate among government servants is still low. Therefore,

this research will examine the factors that influence their decision either to use or not to use.

Currently, the process is still semi-manual. Some of the cooperative resist to change from

their manual transaction into online transactions. It is because, they feel comfortable with the

current systems. Finally, the study's importance is to include digitalization of the online loan

processing process for cooperatives that provide an interconnected cooperative credit scheme.

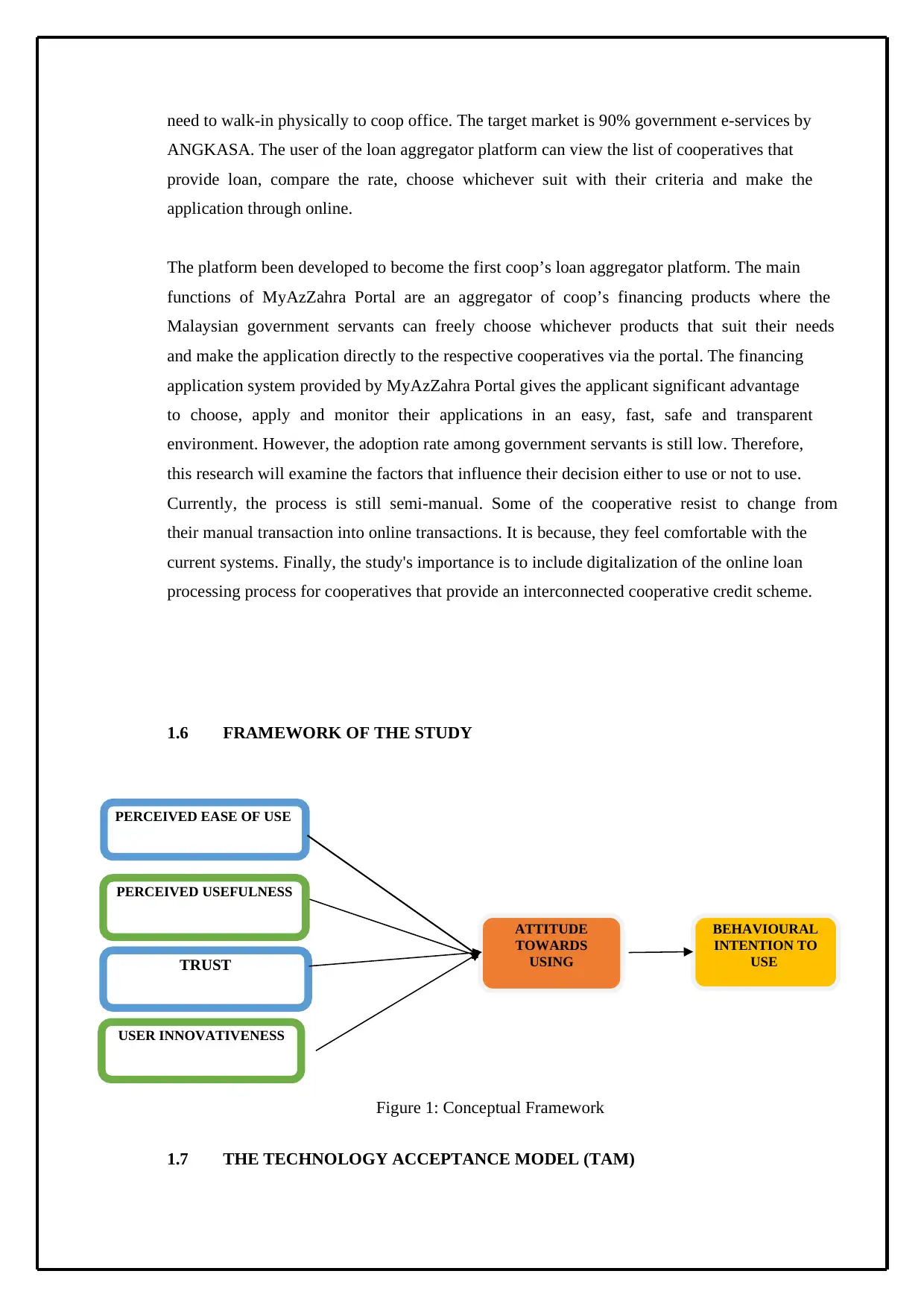

1.6 FRAMEWORK OF THE STUDY

Figure 1: Conceptual Framework

1.7 THE TECHNOLOGY ACCEPTANCE MODEL (TAM)

PERCEIVED EASE OF USE

PERCEIVED USEFULNESS

BEHAVIOURAL

INTENTION TO

USE

ATTITUDE

TOWARDS

USINGTRUST

USER INNOVATIVENESS

ANGKASA. The user of the loan aggregator platform can view the list of cooperatives that

provide loan, compare the rate, choose whichever suit with their criteria and make the

application through online.

The platform been developed to become the first coop’s loan aggregator platform. The main

functions of MyAzZahra Portal are an aggregator of coop’s financing products where the

Malaysian government servants can freely choose whichever products that suit their needs

and make the application directly to the respective cooperatives via the portal. The financing

application system provided by MyAzZahra Portal gives the applicant significant advantage

to choose, apply and monitor their applications in an easy, fast, safe and transparent

environment. However, the adoption rate among government servants is still low. Therefore,

this research will examine the factors that influence their decision either to use or not to use.

Currently, the process is still semi-manual. Some of the cooperative resist to change from

their manual transaction into online transactions. It is because, they feel comfortable with the

current systems. Finally, the study's importance is to include digitalization of the online loan

processing process for cooperatives that provide an interconnected cooperative credit scheme.

1.6 FRAMEWORK OF THE STUDY

Figure 1: Conceptual Framework

1.7 THE TECHNOLOGY ACCEPTANCE MODEL (TAM)

PERCEIVED EASE OF USE

PERCEIVED USEFULNESS

BEHAVIOURAL

INTENTION TO

USE

ATTITUDE

TOWARDS

USINGTRUST

USER INNOVATIVENESS

TAM is a theory that describes how people adopt and use a certain technology. Davis

developed the TAM model in 1989 to describe the behavior of computer technology adoption.

The TAM model considers two major constructs to affect behavioral purpose decision about a

technology

Perceived Usefulness and perceived ease of use are the two main structures. The two key

frameworks are used in the initial model to illustrate the impact of behaviors on the

application of a technology and can then be used to explain the actual use of the device. The

two primary structures will then be affected by outside factors.

According to the technology acceptance model (TAM) framework, perceived usefulness and

perceived ease of use have a significant impact on individual behavioral intentions

(Venkatesh & Davis, F.D 1996).

Since the TAM model will continuously explain differences in user intentions and attitudes

toward technology acceptance, it has been considered valid for use in assessing information

technology adoption. One of the TAM model's strengths is its simple model (Venkatesh &

Davis, 2000).This TAM model has been extensively used to study the introduction of

information technologies such as computers, Internet banking, mobile Internet, e-payment,

and e-wallets.

1.7.1 Perceived Ease of Use

The level of consumer trust that the technology easy to learn, easy to control, easy to

understand and clear, flexible, easy to master, and easy to use are some signs that a

technology is simple to use. In the field of fintech, perceived ease of use applies to how

relaxed customers are with using fintech services and putting forward effort in attempting to

learn them Davis, F. D. (1989).

Other metrics relating to the perceived ease of use of fintech applications, according to

another report, were the ease of the operation process and the ease of downloading the app.

The previous research, which was related to the fintech service acceptance study, found that

perceived ease of use has a positive impact on attitudes toward fintech use. Then, in a separate

analysis examining the viewpoints of users of online loan application platforms, it was

discovered that perceived ease of use has a favorable impact on views toward using online

loan aggregator platforms.

1.7.2 Perceived Usefulness

developed the TAM model in 1989 to describe the behavior of computer technology adoption.

The TAM model considers two major constructs to affect behavioral purpose decision about a

technology

Perceived Usefulness and perceived ease of use are the two main structures. The two key

frameworks are used in the initial model to illustrate the impact of behaviors on the

application of a technology and can then be used to explain the actual use of the device. The

two primary structures will then be affected by outside factors.

According to the technology acceptance model (TAM) framework, perceived usefulness and

perceived ease of use have a significant impact on individual behavioral intentions

(Venkatesh & Davis, F.D 1996).

Since the TAM model will continuously explain differences in user intentions and attitudes

toward technology acceptance, it has been considered valid for use in assessing information

technology adoption. One of the TAM model's strengths is its simple model (Venkatesh &

Davis, 2000).This TAM model has been extensively used to study the introduction of

information technologies such as computers, Internet banking, mobile Internet, e-payment,

and e-wallets.

1.7.1 Perceived Ease of Use

The level of consumer trust that the technology easy to learn, easy to control, easy to

understand and clear, flexible, easy to master, and easy to use are some signs that a

technology is simple to use. In the field of fintech, perceived ease of use applies to how

relaxed customers are with using fintech services and putting forward effort in attempting to

learn them Davis, F. D. (1989).

Other metrics relating to the perceived ease of use of fintech applications, according to

another report, were the ease of the operation process and the ease of downloading the app.

The previous research, which was related to the fintech service acceptance study, found that

perceived ease of use has a positive impact on attitudes toward fintech use. Then, in a separate

analysis examining the viewpoints of users of online loan application platforms, it was

discovered that perceived ease of use has a favorable impact on views toward using online

loan aggregator platforms.

1.7.2 Perceived Usefulness

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Perceived usefulness is another important factor in the TAM model. Users are likely willing

to adopt if they believe it has some benefits over new technologies, according to the diffusion

theory. In the sense of fintech, people will prefer to use fintech platforms if they believe

fintech solutions will benefit them. Furthermore, according to studies on the adoption of

online loan platforms, the perception of usefulness is described as a person's belief that

performing transactions over the internet can make their daily activities more productive and

successful. The purpose of use the fintech technology, according to the speaker, is the breadth

of user data information and the mapping of user awareness. Several previous studies have

shown that perceptions of usefulness have a favorable impact on attitudes toward the use of

fintech. Another research examining the viewpoints of consumers of online loan applications

found that perceived usefulness has a favorable impact on views toward using online loan

applications.

1.7.3 Trust

Trust can be interpreted that the trustee believes that the party given the trust has good

intentions. Trust in service providers is defined as customer confidence that the service

provider has integrity and is reliable. Trust can be seen in two aspects, namely customer trust

in service providers and trust in the technology used. In the context of the adoption of a

technology, the concept of trust is related to the intention or belief in using the technology. In

another study of fintech, the trust variable is an important factor because it is related to the

personal data needed for the service. Regarding the adoption of fintech lending with a peer-to-

peer form in Malaysia, a study revealed that the trust factor has a significant positive effect on

the adoption of the technology from the investor side. Highly innovative groups of individuals

tend to accept uncertainty about something and have more prejudice to innovate. The nature

of this innovation illustrates the level of willingness of an individual to try something new,

whether a new product or service. Another research stated that the nature of innovation in a

person is an innate trait related to the psychological need for uniqueness, and social

identification plays an important role in that trait. The innovative nature of the user is an

innate trait that can represent one’s personality. In some studies, related to mobile wallet, it is

stated that innovativeness has a significant positive effect on the intention to use the

technology. Related to fintech adoption studies, previous studies have shown that

innovativeness has a positive effect on attitudes towards the use of fintech services.

1.7.4 Attitude towards Using Technology

Attitude (attitude) is something that is felt by the user, both positive and negative feelings,

when they have to do something that has been set. In another definition, attitude is a

to adopt if they believe it has some benefits over new technologies, according to the diffusion

theory. In the sense of fintech, people will prefer to use fintech platforms if they believe

fintech solutions will benefit them. Furthermore, according to studies on the adoption of

online loan platforms, the perception of usefulness is described as a person's belief that

performing transactions over the internet can make their daily activities more productive and

successful. The purpose of use the fintech technology, according to the speaker, is the breadth

of user data information and the mapping of user awareness. Several previous studies have

shown that perceptions of usefulness have a favorable impact on attitudes toward the use of

fintech. Another research examining the viewpoints of consumers of online loan applications

found that perceived usefulness has a favorable impact on views toward using online loan

applications.

1.7.3 Trust

Trust can be interpreted that the trustee believes that the party given the trust has good

intentions. Trust in service providers is defined as customer confidence that the service

provider has integrity and is reliable. Trust can be seen in two aspects, namely customer trust

in service providers and trust in the technology used. In the context of the adoption of a

technology, the concept of trust is related to the intention or belief in using the technology. In

another study of fintech, the trust variable is an important factor because it is related to the

personal data needed for the service. Regarding the adoption of fintech lending with a peer-to-

peer form in Malaysia, a study revealed that the trust factor has a significant positive effect on

the adoption of the technology from the investor side. Highly innovative groups of individuals

tend to accept uncertainty about something and have more prejudice to innovate. The nature

of this innovation illustrates the level of willingness of an individual to try something new,

whether a new product or service. Another research stated that the nature of innovation in a

person is an innate trait related to the psychological need for uniqueness, and social

identification plays an important role in that trait. The innovative nature of the user is an

innate trait that can represent one’s personality. In some studies, related to mobile wallet, it is

stated that innovativeness has a significant positive effect on the intention to use the

technology. Related to fintech adoption studies, previous studies have shown that

innovativeness has a positive effect on attitudes towards the use of fintech services.

1.7.4 Attitude towards Using Technology

Attitude (attitude) is something that is felt by the user, both positive and negative feelings,

when they have to do something that has been set. In another definition, attitude is a

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

subjective assessment and individual tendency related to something. In studies related to

TAM, attitude variables have a relationship with someone's intention to use a technology. In

the study of technology adoption related to the banking world, there is a positive relationship

between user attitudes toward certain technologies with the intention of adopting the

technology. Then, related to the study of adoption of fintech services, attitudes toward use

also have a positive effect on the intention to use fintech services

1.7.5 Behavioral Intention to Use

In the other TAM model construct to analyze the level of adoption of a technology, the user

intention construct is commonly used as the dependent variable in the TAM model. A

person’s intention towards a behavior can represent the actual person's behavior. Behavior

intention to use is defined as the level of one’s intention to perform a particular behavior or

action. Behavioral intention in the previous study was mentioned as an important factor in the

successful adoption of a technology because psychologically a person would not use a

technology if one did not have the intention to use it before. In the context of technology

adoption, the intention to use can be interpreted as the level of someone having the intention

to use the new technology.

CHAPTER TWO: THE PAST AND PRESENT: AN OVERVIEW

2.1 ASSESSING THE PERFORMANCE OF CO-OPERATIVES IN MALAYSIA

The National Co-operative Organisation of Malaysia or Angkatan Koperasi Kebangsaan

Malaysia Berhad (ANGKASA) which is the apex co-operative was established on May 12th,

1971. ANGKASA is the representative of the co-operative movement in Malaysia. It was also

responsible for introducing the principles to the Malaysian co-operative movement (Ungku

Abdul Aziz Abdul Hamid, 1983; ANGKASA, 2006). It is affiliated to the International Co-

operative Alliance (ICA) and as an apex organization, served to guide and assists the

movement development. In 1966, the First Cooperative Congress was held with the goal to

establish a national cooperative union. The aim was to unite all the cooperatives in Malaysia

under one federation for cooperatives.

On 12 May 1971, Angkatan Kerjasama Kebangsaan Malaysia Berhad (ANGKASA) was

officially registered as the national union as a result from the Second Cooperative Congress.

With the inception of ANGKASA as a union of co-operative herald the beginning of a

TAM, attitude variables have a relationship with someone's intention to use a technology. In

the study of technology adoption related to the banking world, there is a positive relationship

between user attitudes toward certain technologies with the intention of adopting the

technology. Then, related to the study of adoption of fintech services, attitudes toward use

also have a positive effect on the intention to use fintech services

1.7.5 Behavioral Intention to Use

In the other TAM model construct to analyze the level of adoption of a technology, the user

intention construct is commonly used as the dependent variable in the TAM model. A

person’s intention towards a behavior can represent the actual person's behavior. Behavior

intention to use is defined as the level of one’s intention to perform a particular behavior or

action. Behavioral intention in the previous study was mentioned as an important factor in the

successful adoption of a technology because psychologically a person would not use a

technology if one did not have the intention to use it before. In the context of technology

adoption, the intention to use can be interpreted as the level of someone having the intention

to use the new technology.

CHAPTER TWO: THE PAST AND PRESENT: AN OVERVIEW

2.1 ASSESSING THE PERFORMANCE OF CO-OPERATIVES IN MALAYSIA

The National Co-operative Organisation of Malaysia or Angkatan Koperasi Kebangsaan

Malaysia Berhad (ANGKASA) which is the apex co-operative was established on May 12th,

1971. ANGKASA is the representative of the co-operative movement in Malaysia. It was also

responsible for introducing the principles to the Malaysian co-operative movement (Ungku

Abdul Aziz Abdul Hamid, 1983; ANGKASA, 2006). It is affiliated to the International Co-

operative Alliance (ICA) and as an apex organization, served to guide and assists the

movement development. In 1966, the First Cooperative Congress was held with the goal to

establish a national cooperative union. The aim was to unite all the cooperatives in Malaysia

under one federation for cooperatives.

On 12 May 1971, Angkatan Kerjasama Kebangsaan Malaysia Berhad (ANGKASA) was

officially registered as the national union as a result from the Second Cooperative Congress.

With the inception of ANGKASA as a union of co-operative herald the beginning of a

journey of a united and formidable co-operative movement in Malaysia. Since its

establishment, ANGKASA has played the role as the apex of cooperatives for the Malaysian

cooperative movement. With the approval of the new Cooperative Act in 1993, ANGKASA

was formally recognized by the government of Malaysia to represent the co-operative

movement nationally and internationally. ANGKASA implements co-operative

transformation programs through its participation in high value economy projects.

The government has identified the 7 key economic sectors; Financial Services, Wholesale &

Retail, Tourism & Healthcare, Agriculture & Agro-Base Industry, Plantation,

Telecommunication, and Property Development. ANGKASA continues to carry out its core

service which is providing salary deduction service to the government servants, co-operatives

statutory bodies, clubs, school co-operatives, unions and GLC companies. ANGKASA

maintains to play very active role in the formation and development of school cooperatives in

Malaysia. There are currently more than 12,000 co-operatives and over 7.5 million co-

operators under the stewardship of ANGKASA. The Government launched the 2011 - 2020

National Co-operative Policy and through a tri-partite agreement between Malaysia

Cooperative Societies Commission (MCSC), ANGKASA and Cooperative College of

Malaysia (CCM), ANGKASA has been given the following mandate:

To unite and represent co-operators in Malaysia at national and international level,

To stimulate and develop the co-operatives business by identifying new business

areas while developing and strengthening existing business to create a national and

international network,

To increase the understanding and practices of co-operative values and principles

aligned with ILO Recommendation 193 which recognize co-operatives as a tool for

economic and social development of the community.

As part of the Malaysian Economic Transformation Programme, ANGKASA plans to

spearhead the movement to achieve significant contribution to the Nation’s Gross Domestic

Product. The mechanisms and fundamentals to achieve this will ultimately rest on

ANGKASA - innovativeness and strategies in leveraging available resources and

networks. ANGKASA has positioned itself on the global co-operative platform and has been

entrusted to the Chairmanship as well as hosting the secretariat office of ASEAN Co-

operative Organisation (ACO) and the ICA Asia Pacific Malaysia Business Office (MBO).

With these responsibilities, ANGKASA is unswervingly developing new global economic

total linkages in new partnerships / alliances and networks.

establishment, ANGKASA has played the role as the apex of cooperatives for the Malaysian

cooperative movement. With the approval of the new Cooperative Act in 1993, ANGKASA

was formally recognized by the government of Malaysia to represent the co-operative

movement nationally and internationally. ANGKASA implements co-operative

transformation programs through its participation in high value economy projects.

The government has identified the 7 key economic sectors; Financial Services, Wholesale &

Retail, Tourism & Healthcare, Agriculture & Agro-Base Industry, Plantation,

Telecommunication, and Property Development. ANGKASA continues to carry out its core

service which is providing salary deduction service to the government servants, co-operatives

statutory bodies, clubs, school co-operatives, unions and GLC companies. ANGKASA

maintains to play very active role in the formation and development of school cooperatives in

Malaysia. There are currently more than 12,000 co-operatives and over 7.5 million co-

operators under the stewardship of ANGKASA. The Government launched the 2011 - 2020

National Co-operative Policy and through a tri-partite agreement between Malaysia

Cooperative Societies Commission (MCSC), ANGKASA and Cooperative College of

Malaysia (CCM), ANGKASA has been given the following mandate:

To unite and represent co-operators in Malaysia at national and international level,

To stimulate and develop the co-operatives business by identifying new business

areas while developing and strengthening existing business to create a national and

international network,

To increase the understanding and practices of co-operative values and principles

aligned with ILO Recommendation 193 which recognize co-operatives as a tool for

economic and social development of the community.

As part of the Malaysian Economic Transformation Programme, ANGKASA plans to

spearhead the movement to achieve significant contribution to the Nation’s Gross Domestic

Product. The mechanisms and fundamentals to achieve this will ultimately rest on

ANGKASA - innovativeness and strategies in leveraging available resources and

networks. ANGKASA has positioned itself on the global co-operative platform and has been

entrusted to the Chairmanship as well as hosting the secretariat office of ASEAN Co-

operative Organisation (ACO) and the ICA Asia Pacific Malaysia Business Office (MBO).

With these responsibilities, ANGKASA is unswervingly developing new global economic

total linkages in new partnerships / alliances and networks.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.