MacEwan University ACCT 324 Classic Pen Company ABC Model

VerifiedAdded on 2023/03/30

|6

|686

|233

Case Study

AI Summary

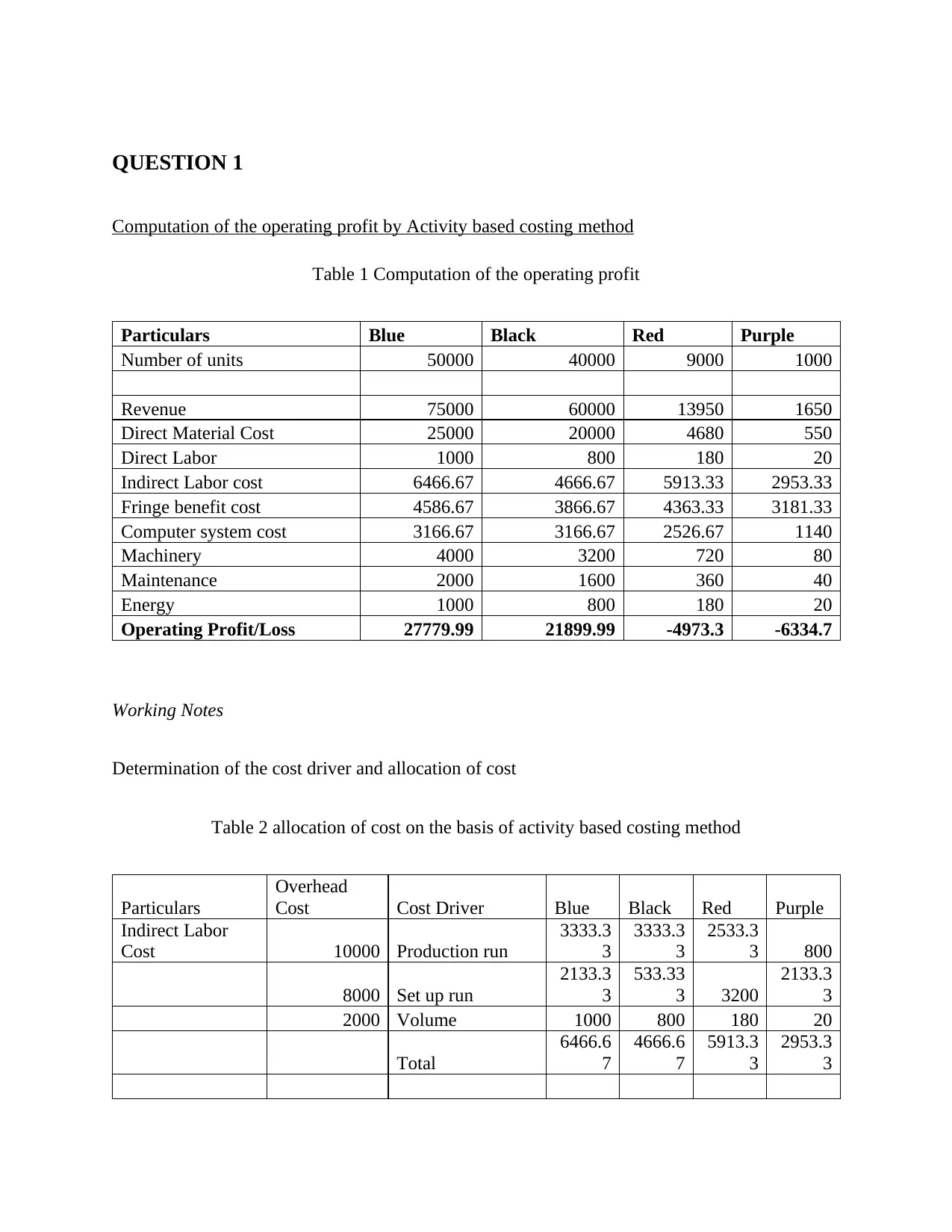

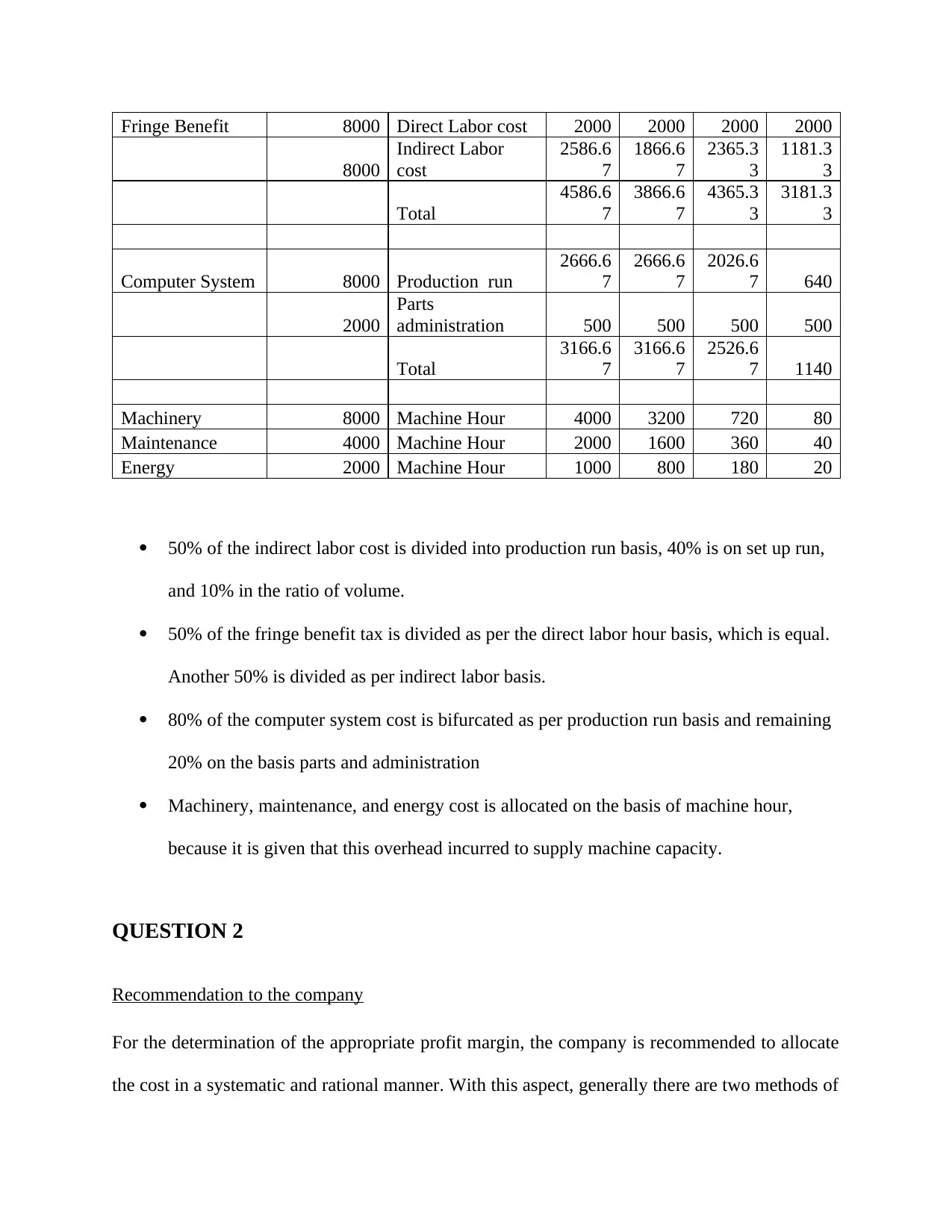

This case study solution analyzes the Classic Pen Company using the Activity Based Costing (ABC) model to determine the operating profit for different pen types (Blue, Black, Red, and Purple). It includes detailed calculations for cost allocation, considering factors like direct materials, direct labor, indirect labor, fringe benefits, computer system costs, machinery maintenance, and energy. The solution recommends that the company adopt a more systematic and rational approach to cost allocation, comparing traditional costing methods with activity-based costing. It suggests simplifying the cost allocation process and implementing performance-based compensation for employees. The document references relevant academic sources to support its analysis and recommendations. Desklib offers a platform with a variety of study tools and resources for students.

1 out of 6

Related Documents

![Management Accounting: Costing Analysis of Office Desks - [Company]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Fjv%2Fc197923795a34b81bdce50f667d18d4c.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.