Corporate Accounting Report: Cleanaway Waste Management

VerifiedAdded on 2020/05/16

|9

|1297

|44

Report

AI Summary

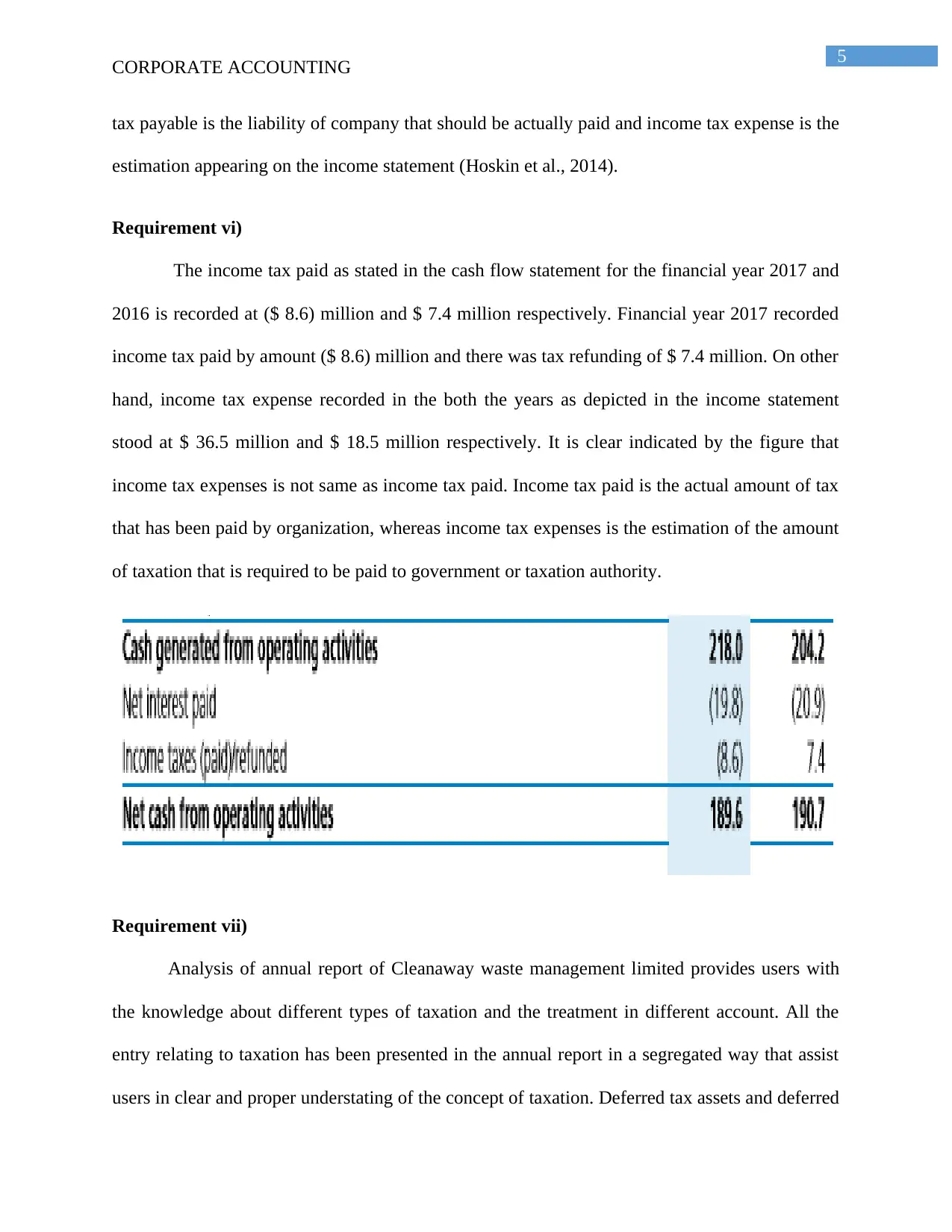

This report analyzes the annual report of Cleanaway Waste Management Limited, focusing on various aspects of corporate accounting. The analysis covers key items of equity, including issued capital, retained earnings, and reserves, and their respective values for the financial years 2017 and 2016. The report delves into tax expenses, comparing accounting income with income tax expenses and explaining the differences, including the impact of the 30% corporation tax rate. It highlights the presence of deferred tax assets and explains the difference between income tax payable and income tax expenses. Furthermore, it examines the income tax paid as stated in the cash flow statement and compares it to the income tax expense in the income statement. The report also discusses the treatment of taxation in the annual report, including the presentation of deferred tax assets and liabilities, the computation of basic earnings per share, and the treatment of franking credits and offsetting of deferred tax balances. The analysis aims to provide a clear understanding of Cleanaway's financial position and its accounting practices related to taxation.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.