Financial Accounting Report: Client Financial Analysis and Statements

VerifiedAdded on 2020/07/23

|38

|4538

|35

Report

AI Summary

This report provides a comprehensive analysis of financial accounting principles and their practical application through various client case studies. It begins with an introduction to financial accounting, covering reporting regulations, the description and analysis of financial accounting, and the determination of accounting principles and concepts. The report then delves into six client scenarios, each presenting different aspects of financial accounting. Client 1 focuses on journal entries, ledger accounts, and trial balances. Client 2 presents profit and loss statements and balance sheets. Client 3 includes income statements and financial position analysis. Client 4 examines bank statements and reconciliation. Client 5 analyzes sales and purchase ledgers, while Client 6 covers suspense accounts and trial balances. The report also explores depreciation methods, the importance of financial statement analysis, and the application of accounting tools and techniques, concluding with a discussion of the importance of accurate calculations in constructing final accounts and the production of adequate accounting methods.

Financial Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

A. Reporting the accounting regulations for firm to the Line manager.................................1

1 Describing the financial accounting....................................................................................1

2 Analysing the financial accounting regulations..................................................................2

3 Determining the principles and necessary rules for accounting..........................................3

4 Explaining the concepts relevant to the material disclosure as well as consistency...........4

CLIENT 1........................................................................................................................................4

1. Preparing the Journal account for Client 1 for the date 1st May 2017...............................5

2. Ledger accounts of all the Journal entries..........................................................................7

3 Trail balance for client 1....................................................................................................16

M1 Analysing purchase and sale transactions to compile a trial balance............................16

D1 Presenting the accurate trail balance in consideration of accounting principles............17

CLIENT 2......................................................................................................................................17

A Profit and loss statement for Peter Piper for the year 31st December 2017.....................17

b Presenting the balance sheet for Peter Piper for the period 31st December 2017.............18

CLIENT 3......................................................................................................................................19

A Income statement for Raintree Ltd for the period 30th September 2017.........................19

b. Financial position of Raintree Ltd....................................................................................20

c Determining principles and concepts of accounting..........................................................25

C Analysing the importance of measuring and presenting depreciation in the financials of

business as well as describing the two methods for business...............................................26

M2 Analysing the P&L, balance sheet and cash flow statements........................................26

D2 Application of the accurate calculations in construction of the final accounts..............26

CLIENT 4......................................................................................................................................27

A Purpose behind preparing the bank statement..................................................................27

B Determining the causes of recording such bank statements or records............................27

C Cash books for the client..................................................................................................27

M3 Application of the reconciliation process and demonstrating various terms.................28

D3 Preparation of BRS in consideration of accounting tools and techniques......................28

INTRODUCTION...........................................................................................................................1

A. Reporting the accounting regulations for firm to the Line manager.................................1

1 Describing the financial accounting....................................................................................1

2 Analysing the financial accounting regulations..................................................................2

3 Determining the principles and necessary rules for accounting..........................................3

4 Explaining the concepts relevant to the material disclosure as well as consistency...........4

CLIENT 1........................................................................................................................................4

1. Preparing the Journal account for Client 1 for the date 1st May 2017...............................5

2. Ledger accounts of all the Journal entries..........................................................................7

3 Trail balance for client 1....................................................................................................16

M1 Analysing purchase and sale transactions to compile a trial balance............................16

D1 Presenting the accurate trail balance in consideration of accounting principles............17

CLIENT 2......................................................................................................................................17

A Profit and loss statement for Peter Piper for the year 31st December 2017.....................17

b Presenting the balance sheet for Peter Piper for the period 31st December 2017.............18

CLIENT 3......................................................................................................................................19

A Income statement for Raintree Ltd for the period 30th September 2017.........................19

b. Financial position of Raintree Ltd....................................................................................20

c Determining principles and concepts of accounting..........................................................25

C Analysing the importance of measuring and presenting depreciation in the financials of

business as well as describing the two methods for business...............................................26

M2 Analysing the P&L, balance sheet and cash flow statements........................................26

D2 Application of the accurate calculations in construction of the final accounts..............26

CLIENT 4......................................................................................................................................27

A Purpose behind preparing the bank statement..................................................................27

B Determining the causes of recording such bank statements or records............................27

C Cash books for the client..................................................................................................27

M3 Application of the reconciliation process and demonstrating various terms.................28

D3 Preparation of BRS in consideration of accounting tools and techniques......................28

CLIENT 5......................................................................................................................................29

A Preparing the sales and purchase ledger account for Henderson for the period May 201729

b Evaluating the term Control account.................................................................................29

CLIENT 6......................................................................................................................................30

A Suspense account and its main features............................................................................30

b. Presenting the trail balance...............................................................................................30

c Journal entries....................................................................................................................30

d Determining the difference between Clearing and suspense account...............................31

M4 Types of accounts and construction of reconciliation....................................................31

D4 Producing the adequate accounting methods..................................................................31

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

BIBLIOGRAPHY..........................................................................................................................35

A Preparing the sales and purchase ledger account for Henderson for the period May 201729

b Evaluating the term Control account.................................................................................29

CLIENT 6......................................................................................................................................30

A Suspense account and its main features............................................................................30

b. Presenting the trail balance...............................................................................................30

c Journal entries....................................................................................................................30

d Determining the difference between Clearing and suspense account...............................31

M4 Types of accounts and construction of reconciliation....................................................31

D4 Producing the adequate accounting methods..................................................................31

CONCLUSION..............................................................................................................................32

REFERENCES..............................................................................................................................33

BIBLIOGRAPHY..........................................................................................................................35

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

In the current scenario there has been use of various accounting principles rules and

regulation which in turn are beneficial for industry or organisation in analysing the adequate

requirement of funds to perform the business activities. Thus, in the present assessments there

will be study based on various principles concepts of financial accounting as well as presentation

of various accounts which are helping various clients to fetch the essential informations and

validate them to make favourable decisions. However, such analysis will be beneficial for

analysing the profitability of the firm through various financial statements such as income

statements, balance sheets, cash flow statements as well as adequate analysis of the operational

tasks.

A. Reporting the accounting regulations for firm to the Line manager

To: Line Manager

From: Junior accountant

Subject: Implication of the accounting terms as well as awareness which are relevant with such

accounting regulations.

Sir,

In order to improve the transactional activities of the business there is need to analyse

the usage, rules, regulations and methods of various accounting principles. Thus, such

accounting techniques will help the organisation in making appropriate improvements in the

business operations as well as make the adequate transactional activities (Robson, Young and

Power, 2017). However, there has been use of various accounting techniques which in turn

helps the business in making the fruitful plans for budgeting, forecasting and costs allocations

over various operational tasks of the business.

1 Describing the financial accounting

In consideration with financial analysing the company's accounts which in turn helps in

improving the investments, capital structure or the business operations of the firm in the long

run. However, with the help of such techniques organisations will help in building the

appropriate reputation in the current environment. Thus, there will be preparation for financial

statements such as income statements, balance sheet as well as stakeholder analysis for firm.

Hence, the motive behind such operational activity is that they help in enhancing the

1

In the current scenario there has been use of various accounting principles rules and

regulation which in turn are beneficial for industry or organisation in analysing the adequate

requirement of funds to perform the business activities. Thus, in the present assessments there

will be study based on various principles concepts of financial accounting as well as presentation

of various accounts which are helping various clients to fetch the essential informations and

validate them to make favourable decisions. However, such analysis will be beneficial for

analysing the profitability of the firm through various financial statements such as income

statements, balance sheets, cash flow statements as well as adequate analysis of the operational

tasks.

A. Reporting the accounting regulations for firm to the Line manager

To: Line Manager

From: Junior accountant

Subject: Implication of the accounting terms as well as awareness which are relevant with such

accounting regulations.

Sir,

In order to improve the transactional activities of the business there is need to analyse

the usage, rules, regulations and methods of various accounting principles. Thus, such

accounting techniques will help the organisation in making appropriate improvements in the

business operations as well as make the adequate transactional activities (Robson, Young and

Power, 2017). However, there has been use of various accounting techniques which in turn

helps the business in making the fruitful plans for budgeting, forecasting and costs allocations

over various operational tasks of the business.

1 Describing the financial accounting

In consideration with financial analysing the company's accounts which in turn helps in

improving the investments, capital structure or the business operations of the firm in the long

run. However, with the help of such techniques organisations will help in building the

appropriate reputation in the current environment. Thus, there will be preparation for financial

statements such as income statements, balance sheet as well as stakeholder analysis for firm.

Hence, the motive behind such operational activity is that they help in enhancing the

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

profitability, productivity as well as presenting the appropriate disclosure of such financials in

the market thereby it helps in gathering the large numbers of stakeholders.

Illustration 1: Kinds of financial statements

Source :(Zeff, 2016)

However, there has been various kinds of financial accounting which in turn helps in

presenting the financials of the business. Hence, such informations are to be used by External

stakeholders of the firm such as Shareholders, governmental departments as well as various

financial institutions like banks thereby analyse the annual turnover, taxation paid by the

government as well as the improvements in organisational growth.

2 Analysing the financial accounting regulations

There has been various operational activities in the business so the record of each and

every transaction is the prime requirements of the organisation. Thus, financial accounting is

consists of various rules and regulations which in turn helps in providing the legal framework of

the accounting. Hence, UK's corporate reporting and governance regulator has facilitated FRC1

which in turn regulates the financial reporting disclosure of the government departments, units

and various corporates (Regulation in Financial accounting, 2017). It helps in facilitating the

auditing of such accounts as well as improve the trade and business in the national economy.

However, there has been various regulations which are executing the universally accepted legal

framework of presenting the dataset such as:

FRC: In consideration with such accounting standard which are constituted for

monitoring and executing the financial disclosures made by various corporations of UK to

1 Financial Reporting Council

2

the market thereby it helps in gathering the large numbers of stakeholders.

Illustration 1: Kinds of financial statements

Source :(Zeff, 2016)

However, there has been various kinds of financial accounting which in turn helps in

presenting the financials of the business. Hence, such informations are to be used by External

stakeholders of the firm such as Shareholders, governmental departments as well as various

financial institutions like banks thereby analyse the annual turnover, taxation paid by the

government as well as the improvements in organisational growth.

2 Analysing the financial accounting regulations

There has been various operational activities in the business so the record of each and

every transaction is the prime requirements of the organisation. Thus, financial accounting is

consists of various rules and regulations which in turn helps in providing the legal framework of

the accounting. Hence, UK's corporate reporting and governance regulator has facilitated FRC1

which in turn regulates the financial reporting disclosure of the government departments, units

and various corporates (Regulation in Financial accounting, 2017). It helps in facilitating the

auditing of such accounts as well as improve the trade and business in the national economy.

However, there has been various regulations which are executing the universally accepted legal

framework of presenting the dataset such as:

FRC: In consideration with such accounting standard which are constituted for

monitoring and executing the financial disclosures made by various corporations of UK to

1 Financial Reporting Council

2

promote the high quality governance (Financial Reporting Council, 2017).

IASB2: The main motive of such board is to facilitate the adequate information and

guidelines to accounting professionals in context with preparing financial data base as well as

facilitate appropriate disclosure of such accounts. Thus, such legal framework has set the

criteria of financial disclosure which is worldwide accepted format and helps the organisation in

attracting the international investors (Loughran and McDonald, 2016).

IFRS: There has been informations and framework which are relevant with making the

disclosure of such financial statements that are helpful for the business in attracting the large

numbers of investors and it helps in making the beneficial estimation of the costs and the

relevant expense incurred in the operational activities.

3 Determining the principles and necessary rules for accounting

There has been various principles and concepts which are being facilitated by GAAP in

order to bring the logically accepted guidelines to the framework of accounting techniques used

by various organisation (Accounting Principles, 2017). However, there has been various

accounting principles which helps in providing the fruitful guidance to accounting

professionals, some of them are described below:

Monetary unit assumption: In consideration with making the business transactions

which are need to be in the US dollar cause this currency is universally accepted and have the

stable rate with fewer fluctuations (Dung, 2016).

Economic assumptions: There has been golden rule that consists of the rule that tall the

entity or firms which are operating in the market and having the revenue through trade practices

can be denoted as the septate legal entity and they have their own legal identity as well as

denoted as a person itself.

Cost principle: this are the techniques which is beneficial of the organisational

professionals in analysing the requirements of the costs that are known as the amount spent over

the operational activities. Hence, such costs or expense are to be budgeted and to be appropriate

to meet the trade requirements.

Full disclosure principles: This concept lies on the rule that during the financial year

2 International Accounting Standard Board

3

IASB2: The main motive of such board is to facilitate the adequate information and

guidelines to accounting professionals in context with preparing financial data base as well as

facilitate appropriate disclosure of such accounts. Thus, such legal framework has set the

criteria of financial disclosure which is worldwide accepted format and helps the organisation in

attracting the international investors (Loughran and McDonald, 2016).

IFRS: There has been informations and framework which are relevant with making the

disclosure of such financial statements that are helpful for the business in attracting the large

numbers of investors and it helps in making the beneficial estimation of the costs and the

relevant expense incurred in the operational activities.

3 Determining the principles and necessary rules for accounting

There has been various principles and concepts which are being facilitated by GAAP in

order to bring the logically accepted guidelines to the framework of accounting techniques used

by various organisation (Accounting Principles, 2017). However, there has been various

accounting principles which helps in providing the fruitful guidance to accounting

professionals, some of them are described below:

Monetary unit assumption: In consideration with making the business transactions

which are need to be in the US dollar cause this currency is universally accepted and have the

stable rate with fewer fluctuations (Dung, 2016).

Economic assumptions: There has been golden rule that consists of the rule that tall the

entity or firms which are operating in the market and having the revenue through trade practices

can be denoted as the septate legal entity and they have their own legal identity as well as

denoted as a person itself.

Cost principle: this are the techniques which is beneficial of the organisational

professionals in analysing the requirements of the costs that are known as the amount spent over

the operational activities. Hence, such costs or expense are to be budgeted and to be appropriate

to meet the trade requirements.

Full disclosure principles: This concept lies on the rule that during the financial year

2 International Accounting Standard Board

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the business keeps all the records of various transactions of different departments or units of the

organisation must be audited, complied as well as present the single statement of balances.

Hence, it can be said that all the accounts of the business must be disclosed at the end of such

financial period. There must be disclosure of the income statements, financial position and cash

flow statements of very operating firm.

Going concern Principles: This principle lies over the concept that all the company

which are performing in business will have the adequate growth as well as make the fruitful

disclosure of the accounts. Hence, which are need to be on the going or regular process

(Damodaran, 2016).

Materiality: There has been use of various financial data which are need to have the

authenticated sources as well as make the efforts in facilitating the relevant material.

4 Explaining the concepts relevant to the material disclosure as well as consistency

In terms with the conventions or concepts of the financial accounting there has been

various terms such as full disclosure, consistency, conservatism convention and materiality

(Grant, 2016). In order to understand the concepts being such principles there is need to make

the adequate disclosure of such accounts as well as understating these two concepts such as:

Consistency: This principle follows the nature that the organisation which has started

making trade practices in the market. It can be said that such business operations will have the

adequate consistency and have the fruitful profitability. Thus, it will be helpful for the firm in

gathering the profitable returns for the long period and facilitating the managers with adequate

operational outcomes.

Material disclosure: The disclosure of the financial accounts which are consists of

various material such as items are need to be monitored by the business professionals in context

with analysing the profitability and efficiency of the organisation in meeting such targets (Dutta

and Patatoukas, 2016).

4

organisation must be audited, complied as well as present the single statement of balances.

Hence, it can be said that all the accounts of the business must be disclosed at the end of such

financial period. There must be disclosure of the income statements, financial position and cash

flow statements of very operating firm.

Going concern Principles: This principle lies over the concept that all the company

which are performing in business will have the adequate growth as well as make the fruitful

disclosure of the accounts. Hence, which are need to be on the going or regular process

(Damodaran, 2016).

Materiality: There has been use of various financial data which are need to have the

authenticated sources as well as make the efforts in facilitating the relevant material.

4 Explaining the concepts relevant to the material disclosure as well as consistency

In terms with the conventions or concepts of the financial accounting there has been

various terms such as full disclosure, consistency, conservatism convention and materiality

(Grant, 2016). In order to understand the concepts being such principles there is need to make

the adequate disclosure of such accounts as well as understating these two concepts such as:

Consistency: This principle follows the nature that the organisation which has started

making trade practices in the market. It can be said that such business operations will have the

adequate consistency and have the fruitful profitability. Thus, it will be helpful for the firm in

gathering the profitable returns for the long period and facilitating the managers with adequate

operational outcomes.

Material disclosure: The disclosure of the financial accounts which are consists of

various material such as items are need to be monitored by the business professionals in context

with analysing the profitability and efficiency of the organisation in meeting such targets (Dutta

and Patatoukas, 2016).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

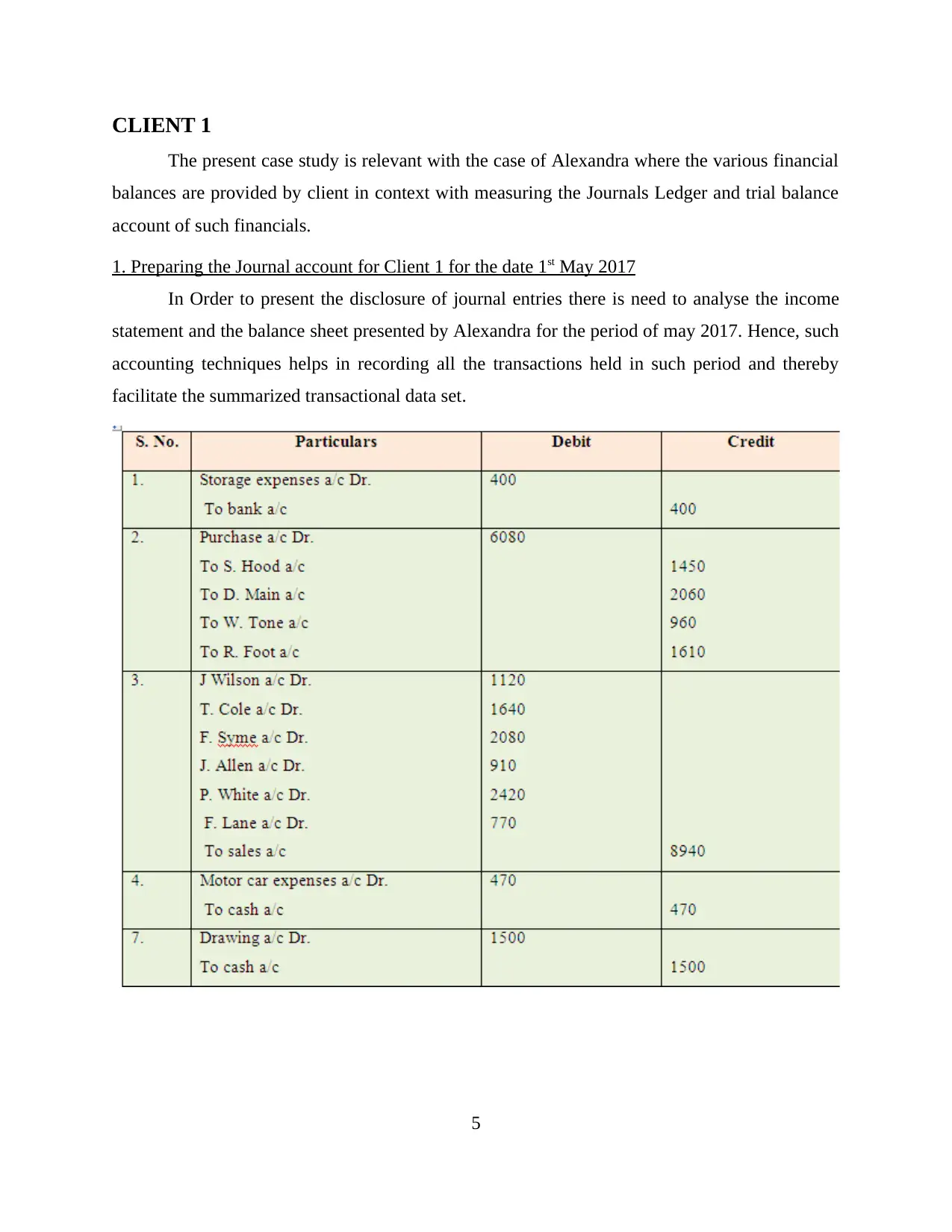

CLIENT 1

The present case study is relevant with the case of Alexandra where the various financial

balances are provided by client in context with measuring the Journals Ledger and trial balance

account of such financials.

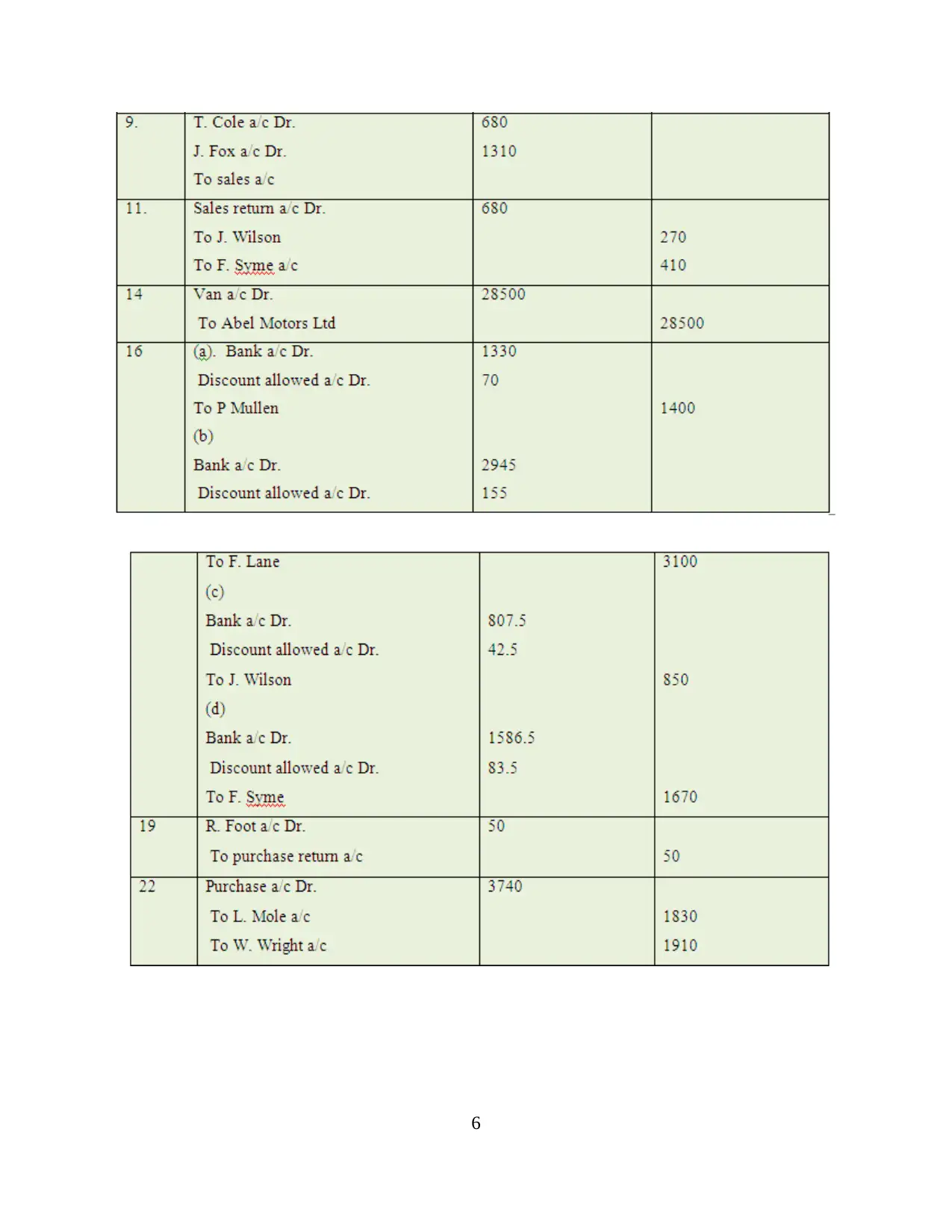

1. Preparing the Journal account for Client 1 for the date 1st May 2017

In Order to present the disclosure of journal entries there is need to analyse the income

statement and the balance sheet presented by Alexandra for the period of may 2017. Hence, such

accounting techniques helps in recording all the transactions held in such period and thereby

facilitate the summarized transactional data set.

5

The present case study is relevant with the case of Alexandra where the various financial

balances are provided by client in context with measuring the Journals Ledger and trial balance

account of such financials.

1. Preparing the Journal account for Client 1 for the date 1st May 2017

In Order to present the disclosure of journal entries there is need to analyse the income

statement and the balance sheet presented by Alexandra for the period of may 2017. Hence, such

accounting techniques helps in recording all the transactions held in such period and thereby

facilitate the summarized transactional data set.

5

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

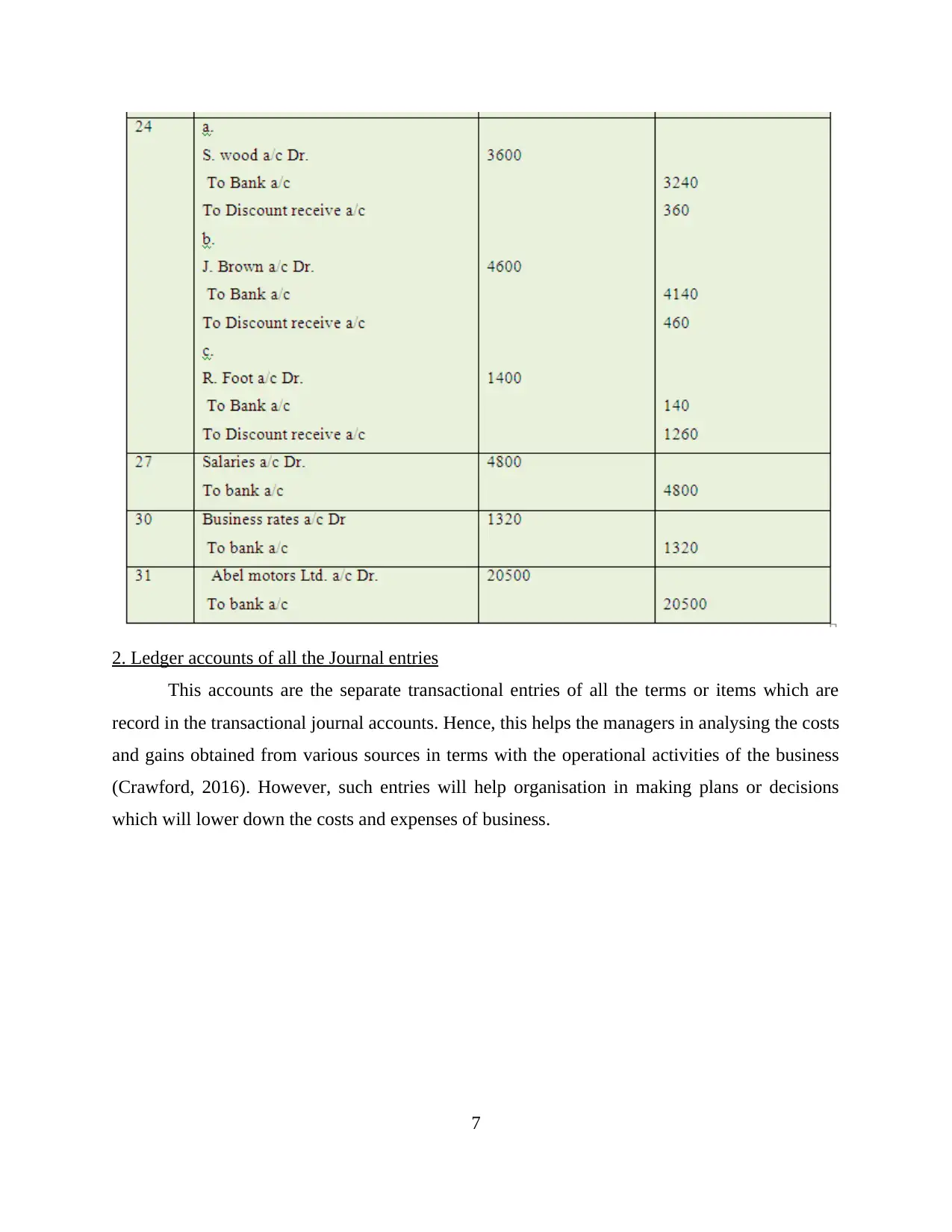

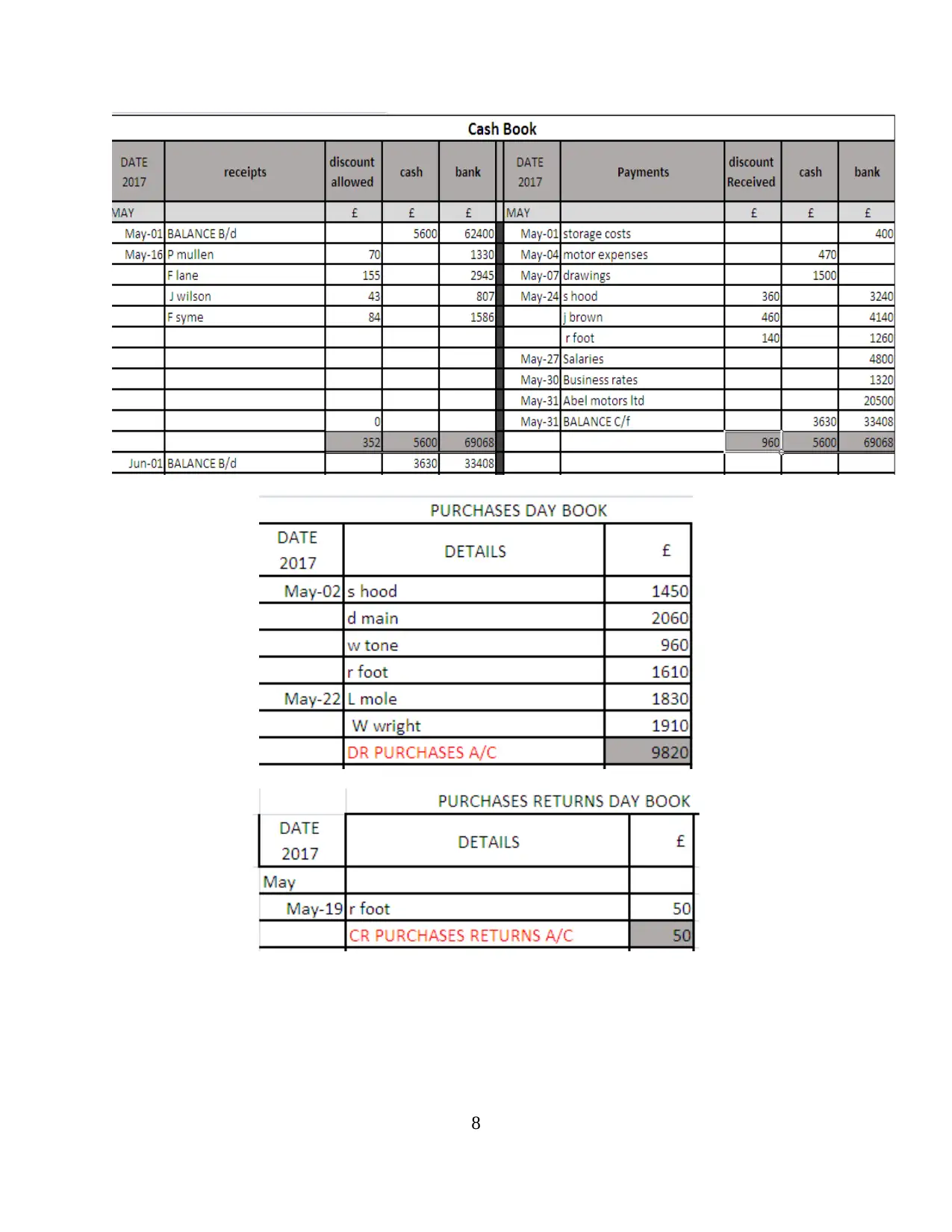

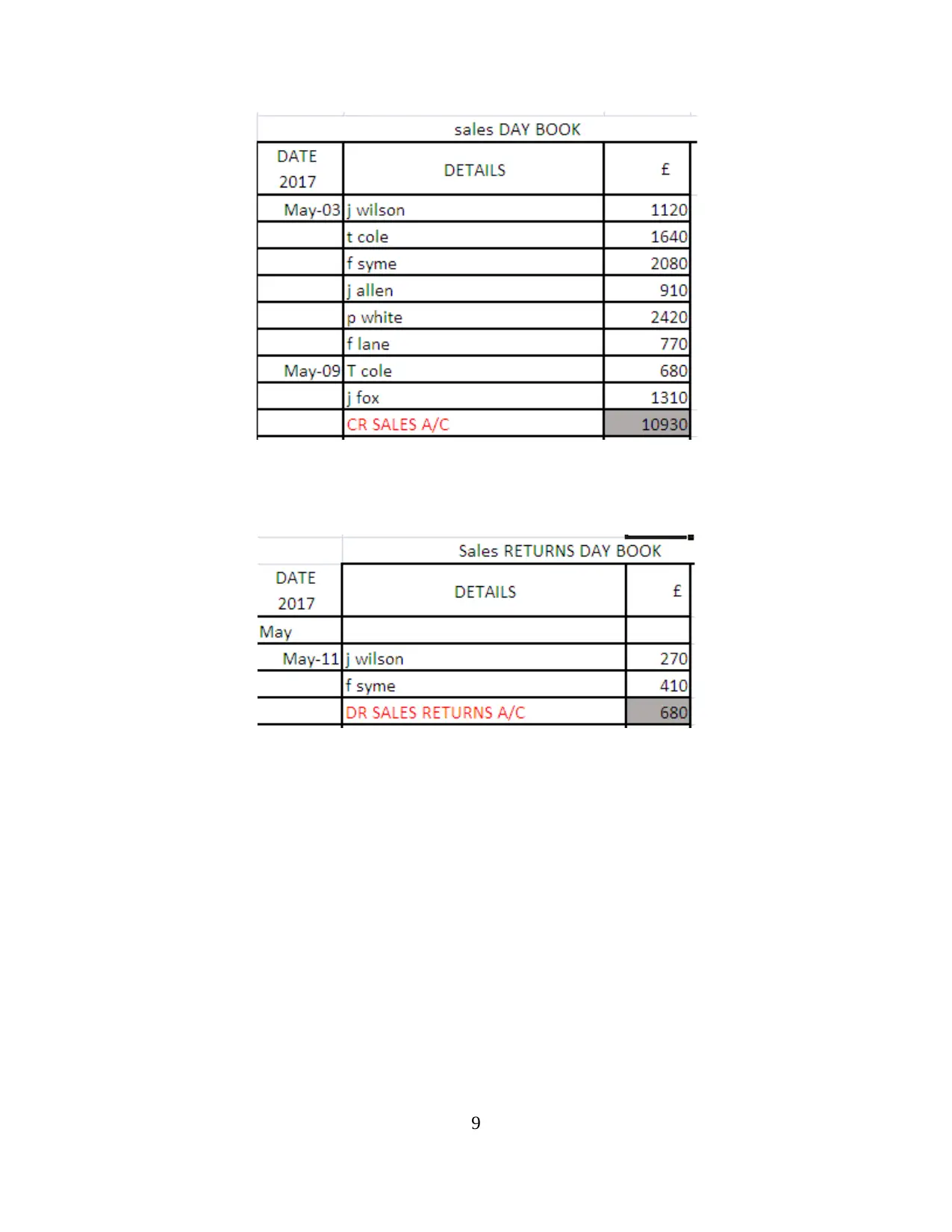

2. Ledger accounts of all the Journal entries

This accounts are the separate transactional entries of all the terms or items which are

record in the transactional journal accounts. Hence, this helps the managers in analysing the costs

and gains obtained from various sources in terms with the operational activities of the business

(Crawford, 2016). However, such entries will help organisation in making plans or decisions

which will lower down the costs and expenses of business.

7

This accounts are the separate transactional entries of all the terms or items which are

record in the transactional journal accounts. Hence, this helps the managers in analysing the costs

and gains obtained from various sources in terms with the operational activities of the business

(Crawford, 2016). However, such entries will help organisation in making plans or decisions

which will lower down the costs and expenses of business.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 38

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.