Comprehensive Client Portfolio: Financial Accounting Principles

VerifiedAdded on 2024/06/04

|39

|4580

|181

Portfolio

AI Summary

This assignment is a portfolio of financial accounting clients, demonstrating the application of accounting principles and regulations. It includes journal entries, ledger accounts, sales and purchase day books, cash books, and control accounts. The portfolio covers various tasks such as preparing financial statements (profit and loss, balance sheet), bank reconciliation statements, and suspense account management. It also explains key accounting concepts like consistency and prudence, and discusses depreciation methods. The document uses real-world scenarios to showcase the practical implementation of financial accounting principles in different business contexts. Desklib is a platform where you can find this and many other solved assignments to help you with your studies.

Financial Accounting Principles

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

A. Report..........................................................................................................................................4

1. Define financial accounting.........................................................................................................4

2. Explain the regulations relating to financial accounting.............................................................4

3. Describe accounting rules and principles....................................................................................4

4. Explain the conventions and concepts relating to consistency and material disclosure..............5

B. Portfolio of clients.......................................................................................................................6

Client 1.............................................................................................................................................6

Client 2...........................................................................................................................................24

(a) The statement of profit or loss for Peter Piper for the period ended 31st December 2017.......24

(b) The statement of financial position for Peter Piper as at 31st December 2017........................24

Client 3...........................................................................................................................................27

(a) Prepare the statement of profit and loss of Raintree Ltd., for the year ended 30 September

2017...............................................................................................................................................27

(b) The statement of financial position of Raintree Ltd. as at 30 September 2017.......................27

(c) Explain the accounting concept of “consistency” and “prudence”..........................................28

(d) Briefly discuss the purpose of depreciation in formulating accounting statements and

illustrate two widely used methods of calculating it.....................................................................28

Client 4...........................................................................................................................................30

A. Explain the purpose of preparing bank reconciliation statement..............................................30

B. List and explain some of the areas, which may cause your record to vary from the bank

records............................................................................................................................................30

C. (i) Bank reconciliation statement at December 1, 2017............................................................30

(ii) Updated cash book...................................................................................................................30

(iii) Bank reconciliation statement as on December 2017.............................................................31

Client 5...........................................................................................................................................33

A. (i) Sales ledger control account................................................................................................33

(ii) Purchase ledger control account..............................................................................................33

B. Explain the term “control account”...........................................................................................34

Client 6...........................................................................................................................................35

A. Suspense account and its features.............................................................................................35

2

A. Report..........................................................................................................................................4

1. Define financial accounting.........................................................................................................4

2. Explain the regulations relating to financial accounting.............................................................4

3. Describe accounting rules and principles....................................................................................4

4. Explain the conventions and concepts relating to consistency and material disclosure..............5

B. Portfolio of clients.......................................................................................................................6

Client 1.............................................................................................................................................6

Client 2...........................................................................................................................................24

(a) The statement of profit or loss for Peter Piper for the period ended 31st December 2017.......24

(b) The statement of financial position for Peter Piper as at 31st December 2017........................24

Client 3...........................................................................................................................................27

(a) Prepare the statement of profit and loss of Raintree Ltd., for the year ended 30 September

2017...............................................................................................................................................27

(b) The statement of financial position of Raintree Ltd. as at 30 September 2017.......................27

(c) Explain the accounting concept of “consistency” and “prudence”..........................................28

(d) Briefly discuss the purpose of depreciation in formulating accounting statements and

illustrate two widely used methods of calculating it.....................................................................28

Client 4...........................................................................................................................................30

A. Explain the purpose of preparing bank reconciliation statement..............................................30

B. List and explain some of the areas, which may cause your record to vary from the bank

records............................................................................................................................................30

C. (i) Bank reconciliation statement at December 1, 2017............................................................30

(ii) Updated cash book...................................................................................................................30

(iii) Bank reconciliation statement as on December 2017.............................................................31

Client 5...........................................................................................................................................33

A. (i) Sales ledger control account................................................................................................33

(ii) Purchase ledger control account..............................................................................................33

B. Explain the term “control account”...........................................................................................34

Client 6...........................................................................................................................................35

A. Suspense account and its features.............................................................................................35

2

B. Trial balance..............................................................................................................................35

C. Journal entries to clear suspense account..................................................................................36

D. Differentiate between suspense and clearing account..............................................................37

Reference list.................................................................................................................................38

3

C. Journal entries to clear suspense account..................................................................................36

D. Differentiate between suspense and clearing account..............................................................37

Reference list.................................................................................................................................38

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

A. Report

1. Define financial accounting

According to Deegan (2013), financial accounting is one of the specialized branches in

accountancy that is concerned with the tracking of the financial transactions of companies and

converting them into financial statements and accounts by applying standardized guidelines.

2. Explain the regulations relating to financial accounting

Williams (2014) stated that the regulations related to financial accounting is different in different

countries. For instance, the companies in Australia follow the financial accounting regulations

stated under the Australian Accounting Standard Board. On the contrary, the companies working

in UK have to follow the regulations of financial accounting mentioned under the IFRS

(International Financial Regulatory Standards) and GAAP (Generally Accepted Accounting

Principles).

However, the regulations of financial accounting in UK vary from sector to sector. For instance,

the firms in the financial and banking sector of UK need to adapt to the regulations mentioned in

“Financial Services and Markets Act, 2000”, which states that all firms are required the

maintenance of high transparency of their financial statements and accounts (Warren, 2016). The

overall regulations and frameworks in UK related to financial accounting are governed through

UK’s Financial Reporting Council (Council, 2013). According to Council (2014), the new

regulations related to financial accounting in UK had been published in the FRS 100 in

November 2012. These are major regulations related to financial accounting in the UK, which

have to be followed in every company in the country for preparing financial statements.

3. Describe accounting rules and principles

Financial accounting consists of different rules and principles. As stated by Marshall (2016), the

golden rules of accounting are the basic financial accounting rules, which are as follows -

“Debit the receiver, credit the giver” (personal account)

“Debit what comes in, credit what goes out” (real account)

4

1. Define financial accounting

According to Deegan (2013), financial accounting is one of the specialized branches in

accountancy that is concerned with the tracking of the financial transactions of companies and

converting them into financial statements and accounts by applying standardized guidelines.

2. Explain the regulations relating to financial accounting

Williams (2014) stated that the regulations related to financial accounting is different in different

countries. For instance, the companies in Australia follow the financial accounting regulations

stated under the Australian Accounting Standard Board. On the contrary, the companies working

in UK have to follow the regulations of financial accounting mentioned under the IFRS

(International Financial Regulatory Standards) and GAAP (Generally Accepted Accounting

Principles).

However, the regulations of financial accounting in UK vary from sector to sector. For instance,

the firms in the financial and banking sector of UK need to adapt to the regulations mentioned in

“Financial Services and Markets Act, 2000”, which states that all firms are required the

maintenance of high transparency of their financial statements and accounts (Warren, 2016). The

overall regulations and frameworks in UK related to financial accounting are governed through

UK’s Financial Reporting Council (Council, 2013). According to Council (2014), the new

regulations related to financial accounting in UK had been published in the FRS 100 in

November 2012. These are major regulations related to financial accounting in the UK, which

have to be followed in every company in the country for preparing financial statements.

3. Describe accounting rules and principles

Financial accounting consists of different rules and principles. As stated by Marshall (2016), the

golden rules of accounting are the basic financial accounting rules, which are as follows -

“Debit the receiver, credit the giver” (personal account)

“Debit what comes in, credit what goes out” (real account)

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

“Debit losses and expenses, credit incomes and gains (nominal account)

The following are the basic principles of financial accounting -

Materiality principle - Edgley (2016) stated the materiality principle of financial

accounting states that only material transactions of a company should be recorded in its

financial accounts.

Conservatism principle - According to the conservatism principle, expenses and

liabilities are to be realized as and when recognized even when there are uncertainties

related to the outcomes (Penman, 2016). However, revenue and assets are to be realized

only when there it is assured to be received.

Accrual principle - This principle of financial accounting states that financial

transactions of a company are to be recorded when they occur, not when cash is realized

from the transactions (Kausar et al., 2017).

4. Explain the conventions and concepts relating to consistency and material disclosure

Material disclosure consistency - This convention of accountancy states that a business needs to

provided all necessary information relating to the company in its financial statements (Picker et

al., 2016).

Convention of consistency - Warren (2015) stated that the convention of consistency in financial

accounting says that accounting techniques, which have been adopted once, should be

consistently applied during the future as well. In all similar situations, the accounting techniques

must be consistent.

5

The following are the basic principles of financial accounting -

Materiality principle - Edgley (2016) stated the materiality principle of financial

accounting states that only material transactions of a company should be recorded in its

financial accounts.

Conservatism principle - According to the conservatism principle, expenses and

liabilities are to be realized as and when recognized even when there are uncertainties

related to the outcomes (Penman, 2016). However, revenue and assets are to be realized

only when there it is assured to be received.

Accrual principle - This principle of financial accounting states that financial

transactions of a company are to be recorded when they occur, not when cash is realized

from the transactions (Kausar et al., 2017).

4. Explain the conventions and concepts relating to consistency and material disclosure

Material disclosure consistency - This convention of accountancy states that a business needs to

provided all necessary information relating to the company in its financial statements (Picker et

al., 2016).

Convention of consistency - Warren (2015) stated that the convention of consistency in financial

accounting says that accounting techniques, which have been adopted once, should be

consistently applied during the future as well. In all similar situations, the accounting techniques

must be consistent.

5

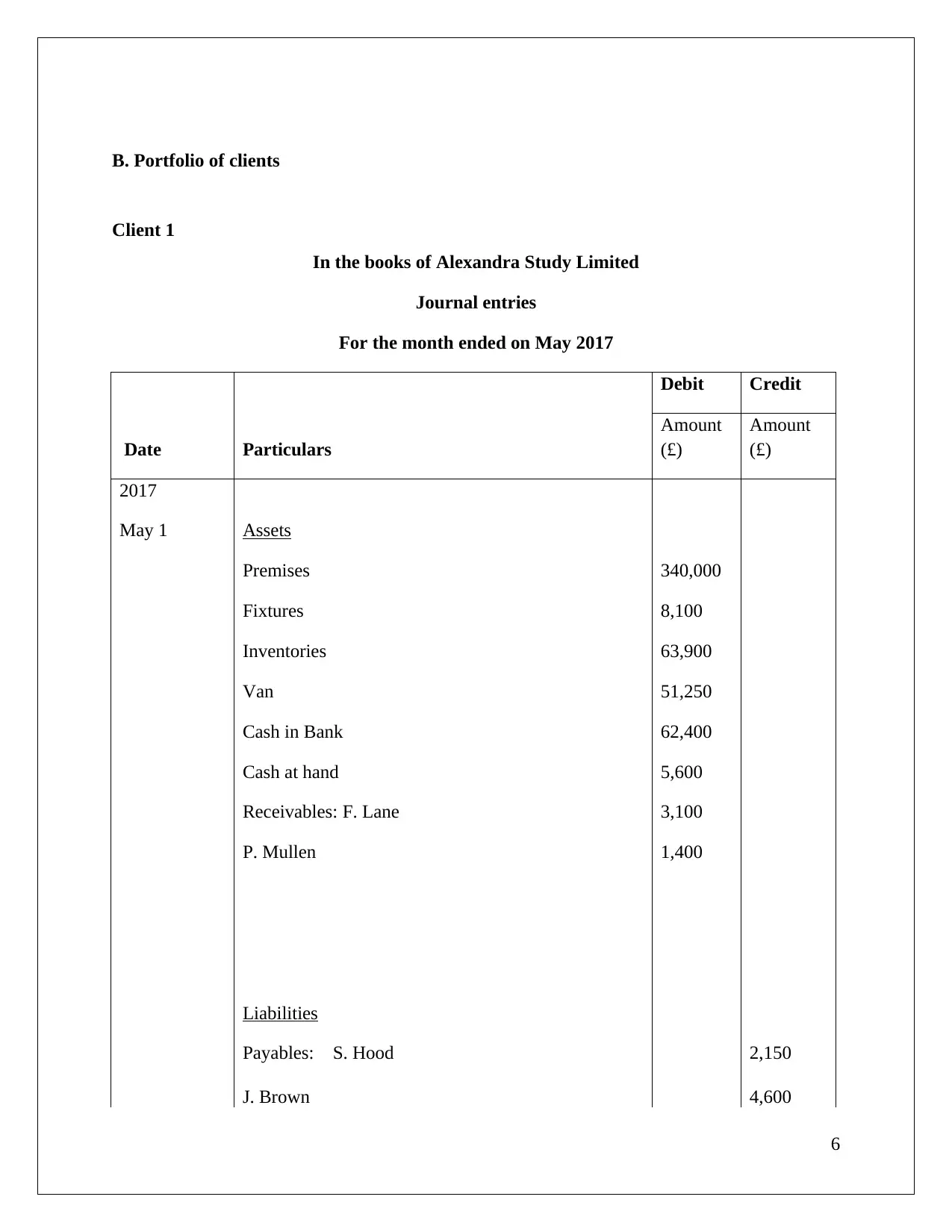

B. Portfolio of clients

Client 1

In the books of Alexandra Study Limited

Journal entries

For the month ended on May 2017

Date Particulars

Debit Credit

Amount

(£)

Amount

(£)

2017

May 1 Assets

Premises 340,000

Fixtures 8,100

Inventories 63,900

Van 51,250

Cash in Bank 62,400

Cash at hand 5,600

Receivables: F. Lane 3,100

P. Mullen 1,400

Liabilities

Payables: S. Hood 2,150

J. Brown 4,600

6

Client 1

In the books of Alexandra Study Limited

Journal entries

For the month ended on May 2017

Date Particulars

Debit Credit

Amount

(£)

Amount

(£)

2017

May 1 Assets

Premises 340,000

Fixtures 8,100

Inventories 63,900

Van 51,250

Cash in Bank 62,400

Cash at hand 5,600

Receivables: F. Lane 3,100

P. Mullen 1,400

Liabilities

Payables: S. Hood 2,150

J. Brown 4,600

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

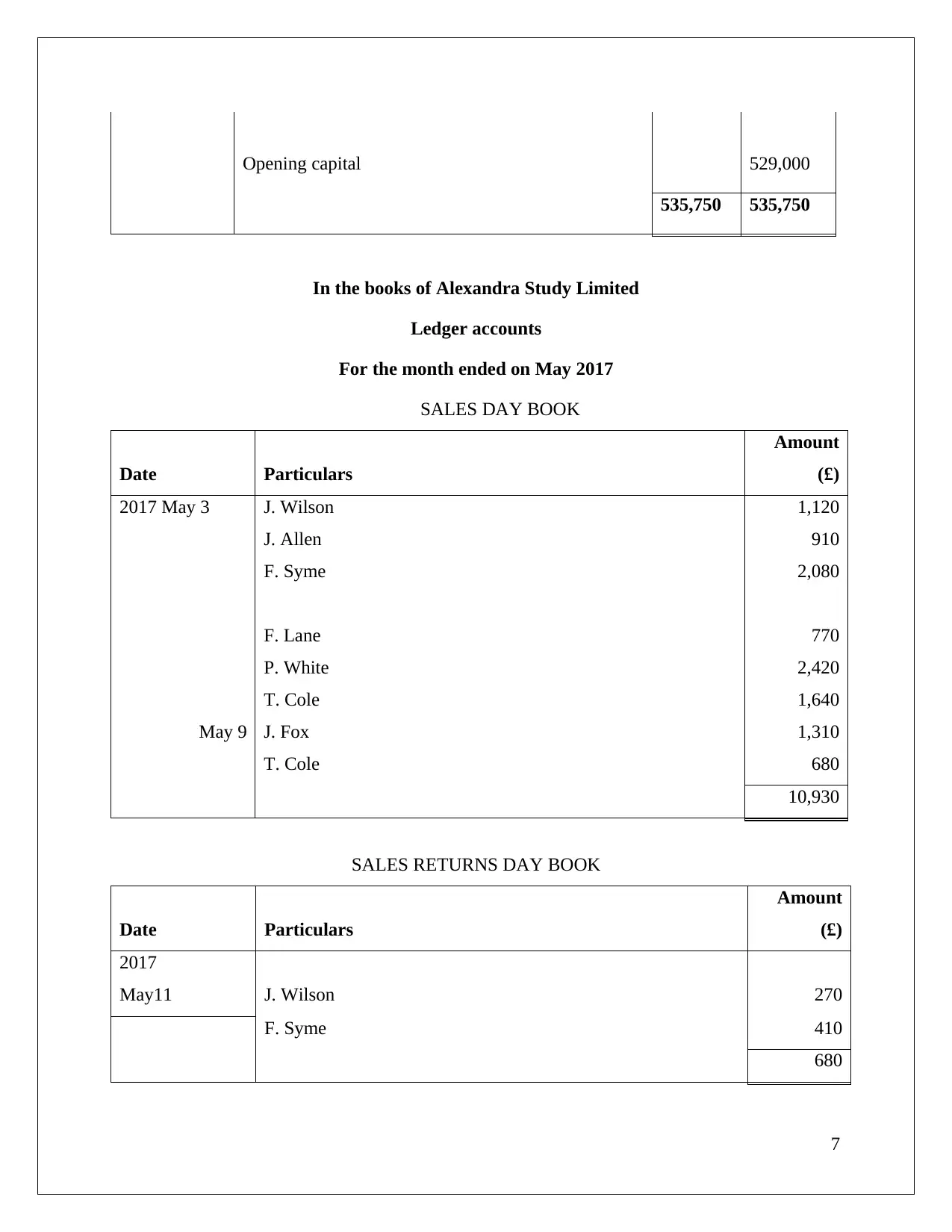

Opening capital 529,000

535,750 535,750

In the books of Alexandra Study Limited

Ledger accounts

For the month ended on May 2017

SALES DAY BOOK

Date Particulars

Amount

(£)

2017 May 3 J. Wilson 1,120

J. Allen 910

F. Syme 2,080

F. Lane 770

P. White 2,420

T. Cole 1,640

May 9 J. Fox 1,310

T. Cole 680

10,930

SALES RETURNS DAY BOOK

Date Particulars

Amount

(£)

2017

May11 J. Wilson 270

F. Syme 410

680

7

535,750 535,750

In the books of Alexandra Study Limited

Ledger accounts

For the month ended on May 2017

SALES DAY BOOK

Date Particulars

Amount

(£)

2017 May 3 J. Wilson 1,120

J. Allen 910

F. Syme 2,080

F. Lane 770

P. White 2,420

T. Cole 1,640

May 9 J. Fox 1,310

T. Cole 680

10,930

SALES RETURNS DAY BOOK

Date Particulars

Amount

(£)

2017

May11 J. Wilson 270

F. Syme 410

680

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

PURCHASES DAY BOOK

Date Particulars Amount (£)

2017

May 2 W. Tone 960

R. Foot 1,610

S. Hood 1,450

D. Main 2,060

May 22 L. Mole 1,830

W. Wright 1,910

9,820

PURCHASES RETURN DAY BOOK

Date Particulars

Amount

(£)

2017

May 11 R. Foot 50

50

CASHBOOK

Date Recei

pts

Discount

Allowed

Cash Bank Date Payment

s

Discount

Received

Cash Bank

Amount

(£)

Amou

nt (£)

Amou

nt (£)

Amount

(£)

Amou

nt (£)

Amou

nt (£)

2017

May 1

Balanc

e b/d

5,600 62,400 2017

May 1

Storage

cost

400

May

16

P.

Mulle

n

70 1,330 May 4 Motor

expenses

470

8

Date Particulars Amount (£)

2017

May 2 W. Tone 960

R. Foot 1,610

S. Hood 1,450

D. Main 2,060

May 22 L. Mole 1,830

W. Wright 1,910

9,820

PURCHASES RETURN DAY BOOK

Date Particulars

Amount

(£)

2017

May 11 R. Foot 50

50

CASHBOOK

Date Recei

pts

Discount

Allowed

Cash Bank Date Payment

s

Discount

Received

Cash Bank

Amount

(£)

Amou

nt (£)

Amou

nt (£)

Amount

(£)

Amou

nt (£)

Amou

nt (£)

2017

May 1

Balanc

e b/d

5,600 62,400 2017

May 1

Storage

cost

400

May

16

P.

Mulle

n

70 1,330 May 4 Motor

expenses

470

8

F.

Lane

155 2,945 May 7

Drawings

1500

J.

Wilso

n

43 807 May

24

S. Hood 360 3,240

F.

Syme

84 1,586 J. Brown 460 4,140

R. Foot 140 1,260

May

27

Salary 4,800

May

30

Business

rates

1,320

May

31

Abel

Motors

Ltd

20,500

May

31

Balance

c/d

3630 33,408

352 5,600 69,068 960 5,600 69,068

31

May

Balanc

e b/d

3630 33,408

DR P. Mullen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017 2017

May 1

To balance brought

down 1400 May 16 By Discount allowed 70

May 16 By Cash 1330

1,400 1,400

F. Lane Account

9

Lane

155 2,945 May 7

Drawings

1500

J.

Wilso

n

43 807 May

24

S. Hood 360 3,240

F.

Syme

84 1,586 J. Brown 460 4,140

R. Foot 140 1,260

May

27

Salary 4,800

May

30

Business

rates

1,320

May

31

Abel

Motors

Ltd

20,500

May

31

Balance

c/d

3630 33,408

352 5,600 69,068 960 5,600 69,068

31

May

Balanc

e b/d

3630 33,408

DR P. Mullen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017 2017

May 1

To balance brought

down 1400 May 16 By Discount allowed 70

May 16 By Cash 1330

1,400 1,400

F. Lane Account

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DR CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1 Balance brought down 3100 16 By Discount 155

3 Sales 770 16 By Cash 2945

31

By Balance carried

forward 770

3,870 3,870

31

To Balance brought

down 770

DR J. Wilson Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,120 11 By Sales return 270

16 By Cash 807

16 By Discount 43

1,120 1,120

DR T. Cole Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,640 31

By Balance carried

forward 2,320

9 To Sales 680

10

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

1 Balance brought down 3100 16 By Discount 155

3 Sales 770 16 By Cash 2945

31

By Balance carried

forward 770

3,870 3,870

31

To Balance brought

down 770

DR J. Wilson Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,120 11 By Sales return 270

16 By Cash 807

16 By Discount 43

1,120 1,120

DR T. Cole Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 1,640 31

By Balance carried

forward 2,320

9 To Sales 680

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2,320 2,320

31

To Balance brought

down 2,320

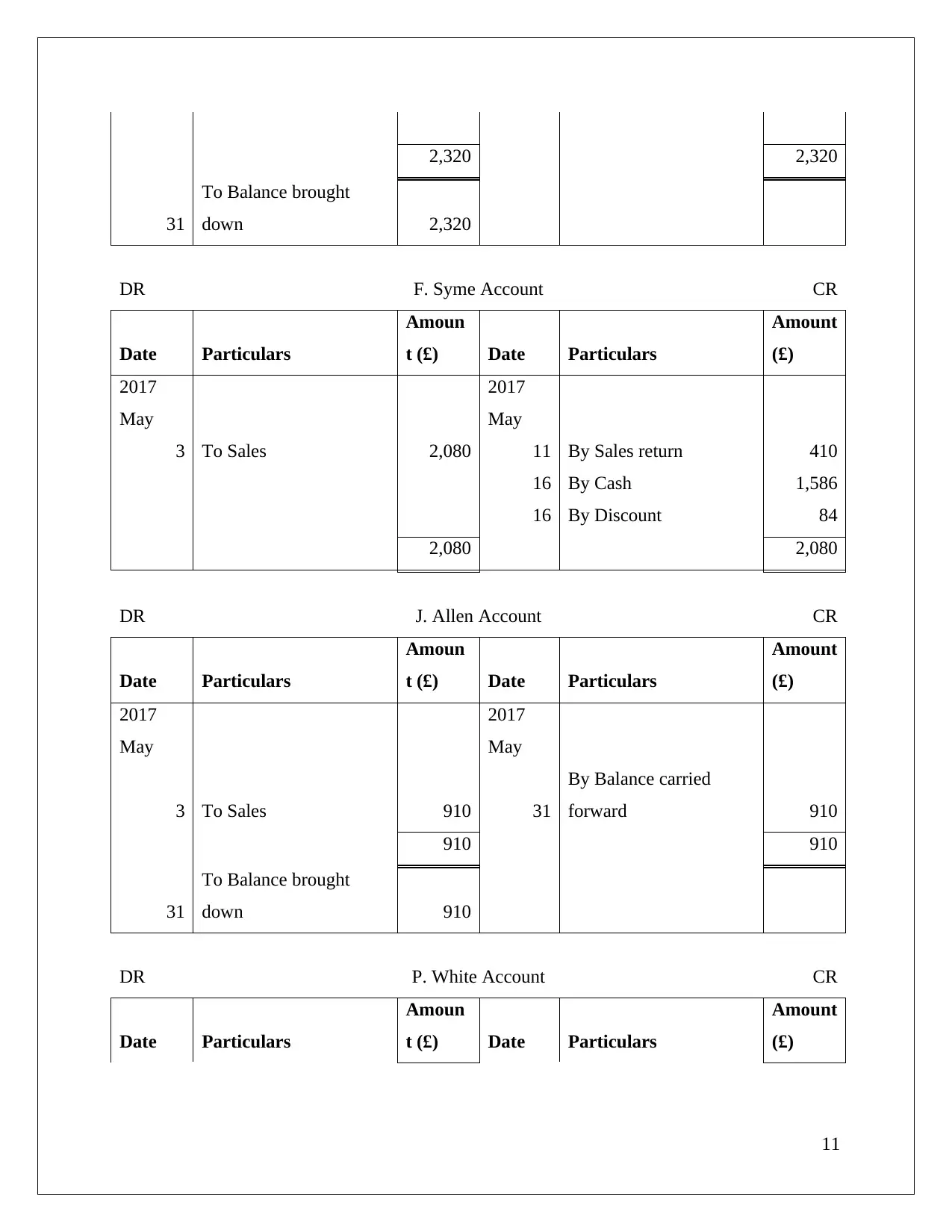

DR F. Syme Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 2,080 11 By Sales return 410

16 By Cash 1,586

16 By Discount 84

2,080 2,080

DR J. Allen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 910 31

By Balance carried

forward 910

910 910

31

To Balance brought

down 910

DR P. White Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

11

31

To Balance brought

down 2,320

DR F. Syme Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 2,080 11 By Sales return 410

16 By Cash 1,586

16 By Discount 84

2,080 2,080

DR J. Allen Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

3 To Sales 910 31

By Balance carried

forward 910

910 910

31

To Balance brought

down 910

DR P. White Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

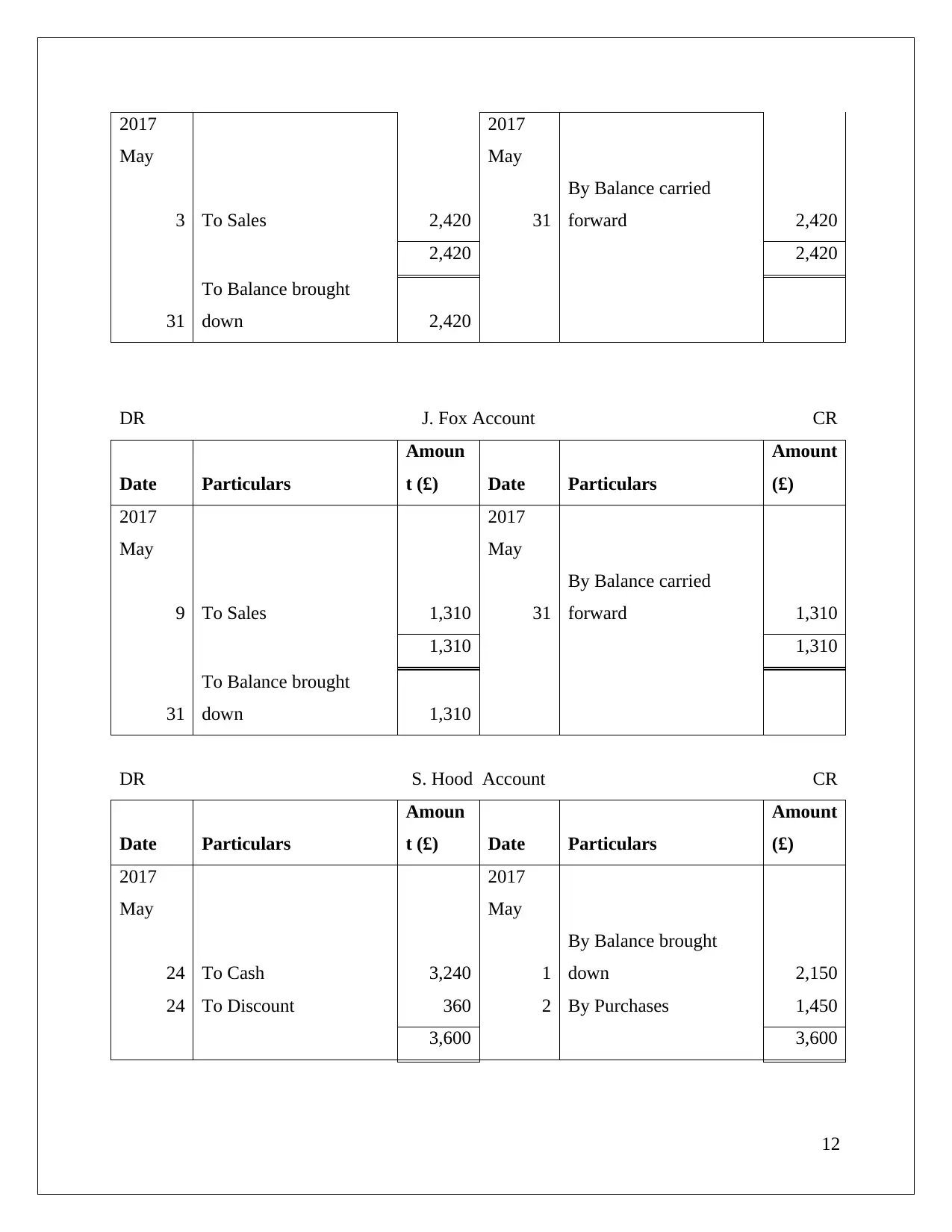

11

2017

May

2017

May

3 To Sales 2,420 31

By Balance carried

forward 2,420

2,420 2,420

31

To Balance brought

down 2,420

DR J. Fox Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

9 To Sales 1,310 31

By Balance carried

forward 1,310

1,310 1,310

31

To Balance brought

down 1,310

DR S. Hood Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

24 To Cash 3,240 1

By Balance brought

down 2,150

24 To Discount 360 2 By Purchases 1,450

3,600 3,600

12

May

2017

May

3 To Sales 2,420 31

By Balance carried

forward 2,420

2,420 2,420

31

To Balance brought

down 2,420

DR J. Fox Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

9 To Sales 1,310 31

By Balance carried

forward 1,310

1,310 1,310

31

To Balance brought

down 1,310

DR S. Hood Account CR

Date Particulars

Amoun

t (£) Date Particulars

Amount

(£)

2017

May

2017

May

24 To Cash 3,240 1

By Balance brought

down 2,150

24 To Discount 360 2 By Purchases 1,450

3,600 3,600

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 39

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.