MA514 Business Finance: Client-Focused Financial Planning Report

VerifiedAdded on 2023/06/11

|14

|3050

|142

Report

AI Summary

This report provides a comprehensive analysis of property investment in Melbourne, focusing on financial planning for a client. It includes calculations of property price changes using a five-year average method, income growth projections, and expense analysis to determine savings capacity. The report evaluates different loan scenarios, including those with and without insurance premiums, to assess the client's ability to purchase property. It also compares financial plans with 20% and 5% upfront payments to determine the optimal strategy for property acquisition. Furthermore, the report includes an analysis of the client's income, expenses, and tax obligations to project net income and savings over time, ultimately providing a detailed financial roadmap for achieving the client's property investment goals. This assignment solution is available on Desklib, a platform offering a wide range of study resources for students.

Running head: BUSINESS FINANCE

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Business Finance

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

1

Table of Contents

Answer for the Question 1:........................................................................................................2

Answer for the Question 2:........................................................................................................4

Answer for the Question 3:........................................................................................................6

Answer for the Question 4:........................................................................................................7

Answer for the Question 5:........................................................................................................8

Answer for the Question 6:......................................................................................................10

Answer for the Question 7:......................................................................................................11

Reference and Bibliography:....................................................................................................12

1

Table of Contents

Answer for the Question 1:........................................................................................................2

Answer for the Question 2:........................................................................................................4

Answer for the Question 3:........................................................................................................6

Answer for the Question 4:........................................................................................................7

Answer for the Question 5:........................................................................................................8

Answer for the Question 6:......................................................................................................10

Answer for the Question 7:......................................................................................................11

Reference and Bibliography:....................................................................................................12

BUSINESS FINANCE

2

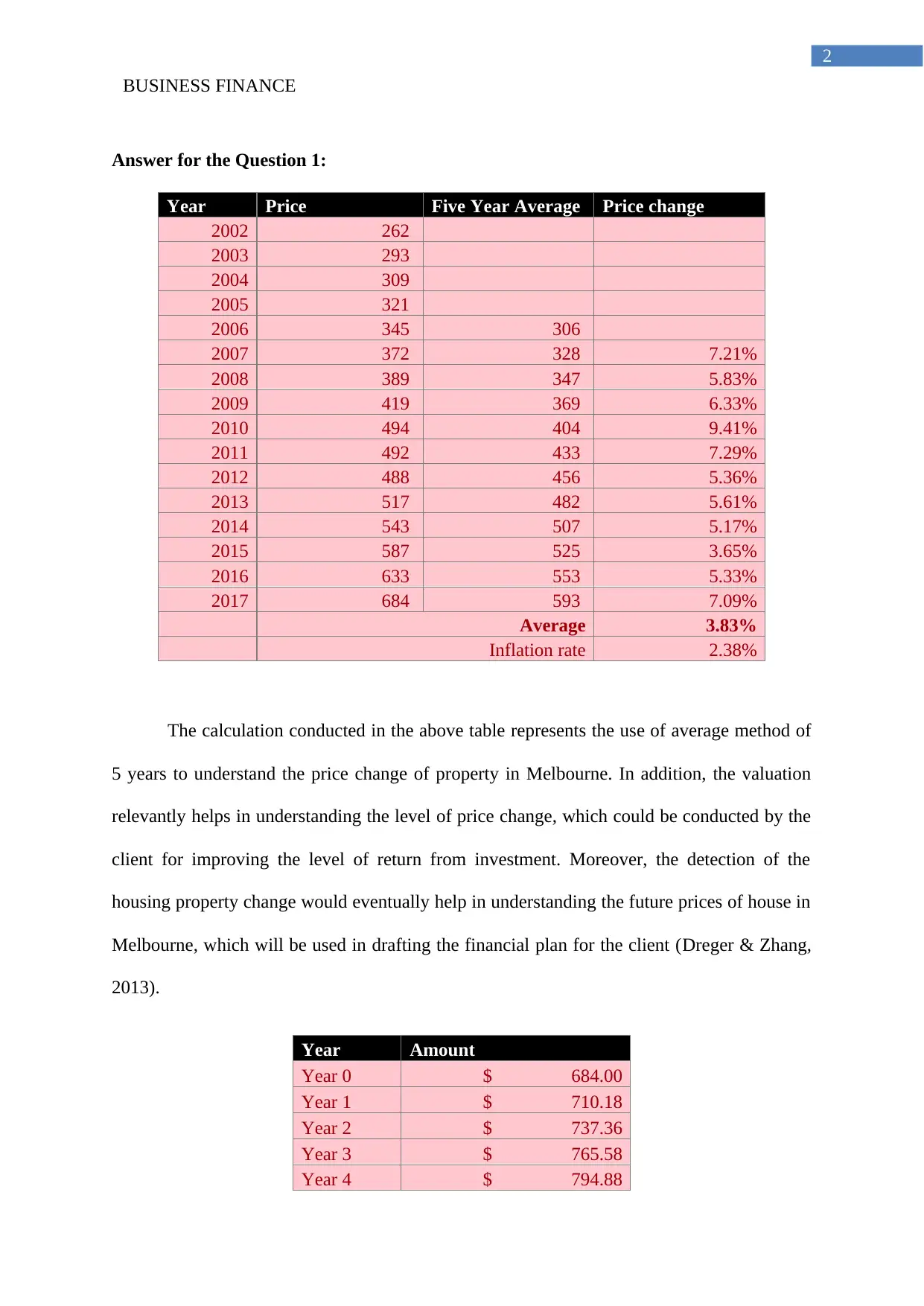

Answer for the Question 1:

Year Price Five Year Average Price change

2002 262

2003 293

2004 309

2005 321

2006 345 306

2007 372 328 7.21%

2008 389 347 5.83%

2009 419 369 6.33%

2010 494 404 9.41%

2011 492 433 7.29%

2012 488 456 5.36%

2013 517 482 5.61%

2014 543 507 5.17%

2015 587 525 3.65%

2016 633 553 5.33%

2017 684 593 7.09%

Average 3.83%

Inflation rate 2.38%

The calculation conducted in the above table represents the use of average method of

5 years to understand the price change of property in Melbourne. In addition, the valuation

relevantly helps in understanding the level of price change, which could be conducted by the

client for improving the level of return from investment. Moreover, the detection of the

housing property change would eventually help in understanding the future prices of house in

Melbourne, which will be used in drafting the financial plan for the client (Dreger & Zhang,

2013).

Year Amount

Year 0 $ 684.00

Year 1 $ 710.18

Year 2 $ 737.36

Year 3 $ 765.58

Year 4 $ 794.88

2

Answer for the Question 1:

Year Price Five Year Average Price change

2002 262

2003 293

2004 309

2005 321

2006 345 306

2007 372 328 7.21%

2008 389 347 5.83%

2009 419 369 6.33%

2010 494 404 9.41%

2011 492 433 7.29%

2012 488 456 5.36%

2013 517 482 5.61%

2014 543 507 5.17%

2015 587 525 3.65%

2016 633 553 5.33%

2017 684 593 7.09%

Average 3.83%

Inflation rate 2.38%

The calculation conducted in the above table represents the use of average method of

5 years to understand the price change of property in Melbourne. In addition, the valuation

relevantly helps in understanding the level of price change, which could be conducted by the

client for improving the level of return from investment. Moreover, the detection of the

housing property change would eventually help in understanding the future prices of house in

Melbourne, which will be used in drafting the financial plan for the client (Dreger & Zhang,

2013).

Year Amount

Year 0 $ 684.00

Year 1 $ 710.18

Year 2 $ 737.36

Year 3 $ 765.58

Year 4 $ 794.88

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

3

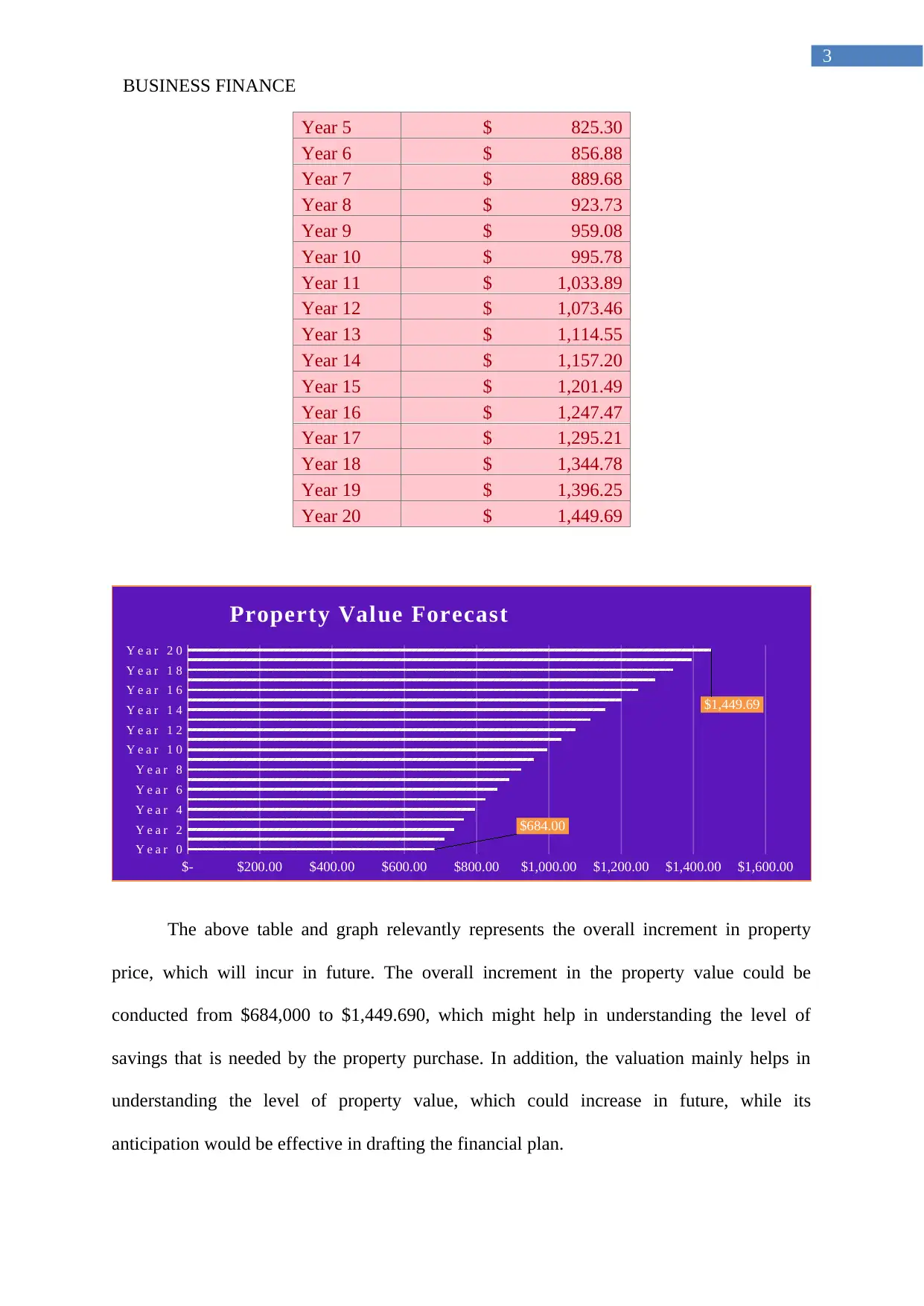

Year 5 $ 825.30

Year 6 $ 856.88

Year 7 $ 889.68

Year 8 $ 923.73

Year 9 $ 959.08

Year 10 $ 995.78

Year 11 $ 1,033.89

Year 12 $ 1,073.46

Year 13 $ 1,114.55

Year 14 $ 1,157.20

Year 15 $ 1,201.49

Year 16 $ 1,247.47

Year 17 $ 1,295.21

Year 18 $ 1,344.78

Year 19 $ 1,396.25

Year 20 $ 1,449.69

Y e a r 0

Y e a r 2

Y e a r 4

Y e a r 6

Y e a r 8

Y e a r 1 0

Y e a r 1 2

Y e a r 1 4

Y e a r 1 6

Y e a r 1 8

Y e a r 2 0

$- $200.00 $400.00 $600.00 $800.00 $1,000.00 $1,200.00 $1,400.00 $1,600.00

$684.00

$1,449.69

Property Value Forecast

The above table and graph relevantly represents the overall increment in property

price, which will incur in future. The overall increment in the property value could be

conducted from $684,000 to $1,449.690, which might help in understanding the level of

savings that is needed by the property purchase. In addition, the valuation mainly helps in

understanding the level of property value, which could increase in future, while its

anticipation would be effective in drafting the financial plan.

3

Year 5 $ 825.30

Year 6 $ 856.88

Year 7 $ 889.68

Year 8 $ 923.73

Year 9 $ 959.08

Year 10 $ 995.78

Year 11 $ 1,033.89

Year 12 $ 1,073.46

Year 13 $ 1,114.55

Year 14 $ 1,157.20

Year 15 $ 1,201.49

Year 16 $ 1,247.47

Year 17 $ 1,295.21

Year 18 $ 1,344.78

Year 19 $ 1,396.25

Year 20 $ 1,449.69

Y e a r 0

Y e a r 2

Y e a r 4

Y e a r 6

Y e a r 8

Y e a r 1 0

Y e a r 1 2

Y e a r 1 4

Y e a r 1 6

Y e a r 1 8

Y e a r 2 0

$- $200.00 $400.00 $600.00 $800.00 $1,000.00 $1,200.00 $1,400.00 $1,600.00

$684.00

$1,449.69

Property Value Forecast

The above table and graph relevantly represents the overall increment in property

price, which will incur in future. The overall increment in the property value could be

conducted from $684,000 to $1,449.690, which might help in understanding the level of

savings that is needed by the property purchase. In addition, the valuation mainly helps in

understanding the level of property value, which could increase in future, while its

anticipation would be effective in drafting the financial plan.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

4

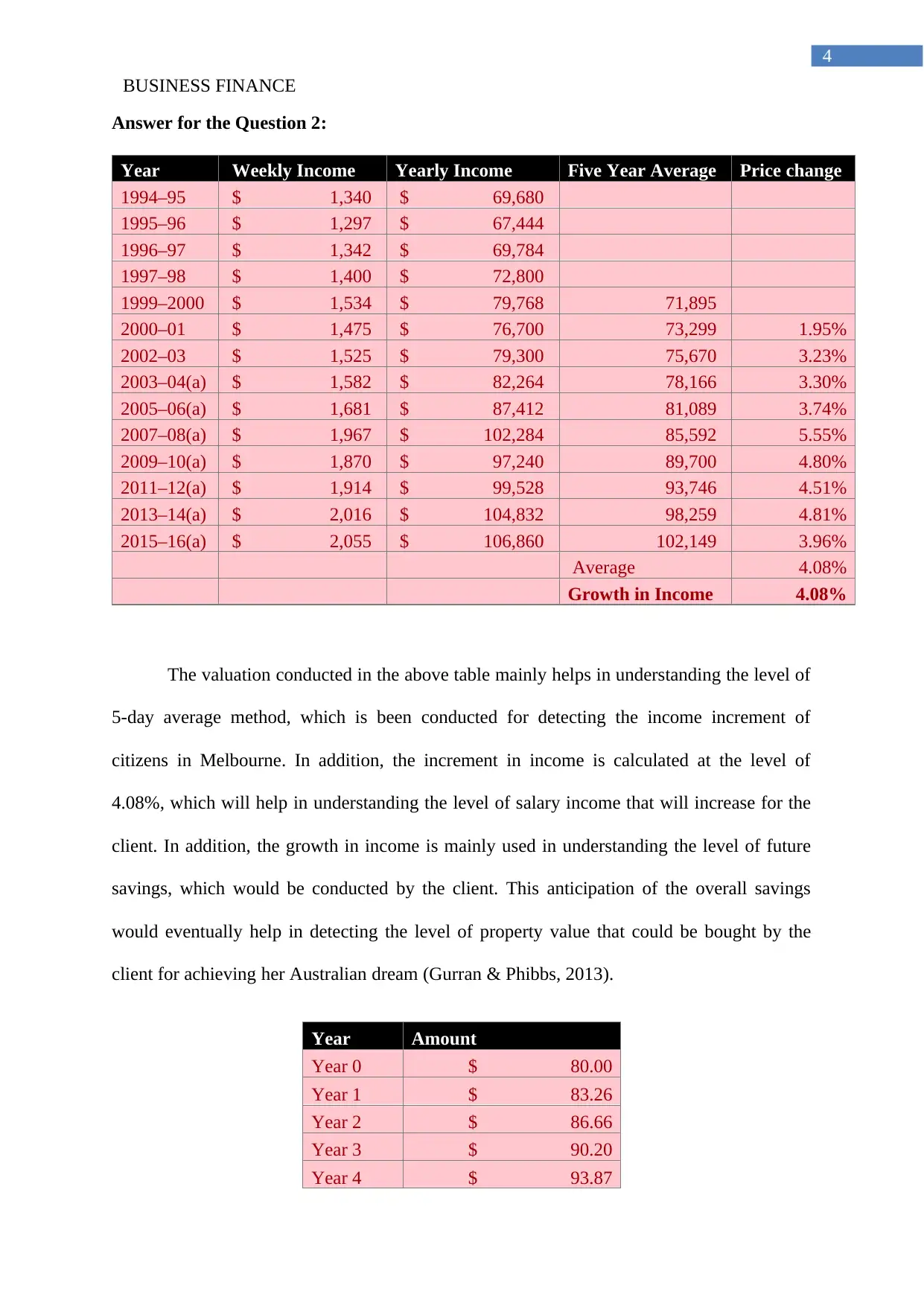

Answer for the Question 2:

Year Weekly Income Yearly Income Five Year Average Price change

1994–95 $ 1,340 $ 69,680

1995–96 $ 1,297 $ 67,444

1996–97 $ 1,342 $ 69,784

1997–98 $ 1,400 $ 72,800

1999–2000 $ 1,534 $ 79,768 71,895

2000–01 $ 1,475 $ 76,700 73,299 1.95%

2002–03 $ 1,525 $ 79,300 75,670 3.23%

2003–04(a) $ 1,582 $ 82,264 78,166 3.30%

2005–06(a) $ 1,681 $ 87,412 81,089 3.74%

2007–08(a) $ 1,967 $ 102,284 85,592 5.55%

2009–10(a) $ 1,870 $ 97,240 89,700 4.80%

2011–12(a) $ 1,914 $ 99,528 93,746 4.51%

2013–14(a) $ 2,016 $ 104,832 98,259 4.81%

2015–16(a) $ 2,055 $ 106,860 102,149 3.96%

Average 4.08%

Growth in Income 4.08%

The valuation conducted in the above table mainly helps in understanding the level of

5-day average method, which is been conducted for detecting the income increment of

citizens in Melbourne. In addition, the increment in income is calculated at the level of

4.08%, which will help in understanding the level of salary income that will increase for the

client. In addition, the growth in income is mainly used in understanding the level of future

savings, which would be conducted by the client. This anticipation of the overall savings

would eventually help in detecting the level of property value that could be bought by the

client for achieving her Australian dream (Gurran & Phibbs, 2013).

Year Amount

Year 0 $ 80.00

Year 1 $ 83.26

Year 2 $ 86.66

Year 3 $ 90.20

Year 4 $ 93.87

4

Answer for the Question 2:

Year Weekly Income Yearly Income Five Year Average Price change

1994–95 $ 1,340 $ 69,680

1995–96 $ 1,297 $ 67,444

1996–97 $ 1,342 $ 69,784

1997–98 $ 1,400 $ 72,800

1999–2000 $ 1,534 $ 79,768 71,895

2000–01 $ 1,475 $ 76,700 73,299 1.95%

2002–03 $ 1,525 $ 79,300 75,670 3.23%

2003–04(a) $ 1,582 $ 82,264 78,166 3.30%

2005–06(a) $ 1,681 $ 87,412 81,089 3.74%

2007–08(a) $ 1,967 $ 102,284 85,592 5.55%

2009–10(a) $ 1,870 $ 97,240 89,700 4.80%

2011–12(a) $ 1,914 $ 99,528 93,746 4.51%

2013–14(a) $ 2,016 $ 104,832 98,259 4.81%

2015–16(a) $ 2,055 $ 106,860 102,149 3.96%

Average 4.08%

Growth in Income 4.08%

The valuation conducted in the above table mainly helps in understanding the level of

5-day average method, which is been conducted for detecting the income increment of

citizens in Melbourne. In addition, the increment in income is calculated at the level of

4.08%, which will help in understanding the level of salary income that will increase for the

client. In addition, the growth in income is mainly used in understanding the level of future

savings, which would be conducted by the client. This anticipation of the overall savings

would eventually help in detecting the level of property value that could be bought by the

client for achieving her Australian dream (Gurran & Phibbs, 2013).

Year Amount

Year 0 $ 80.00

Year 1 $ 83.26

Year 2 $ 86.66

Year 3 $ 90.20

Year 4 $ 93.87

BUSINESS FINANCE

5

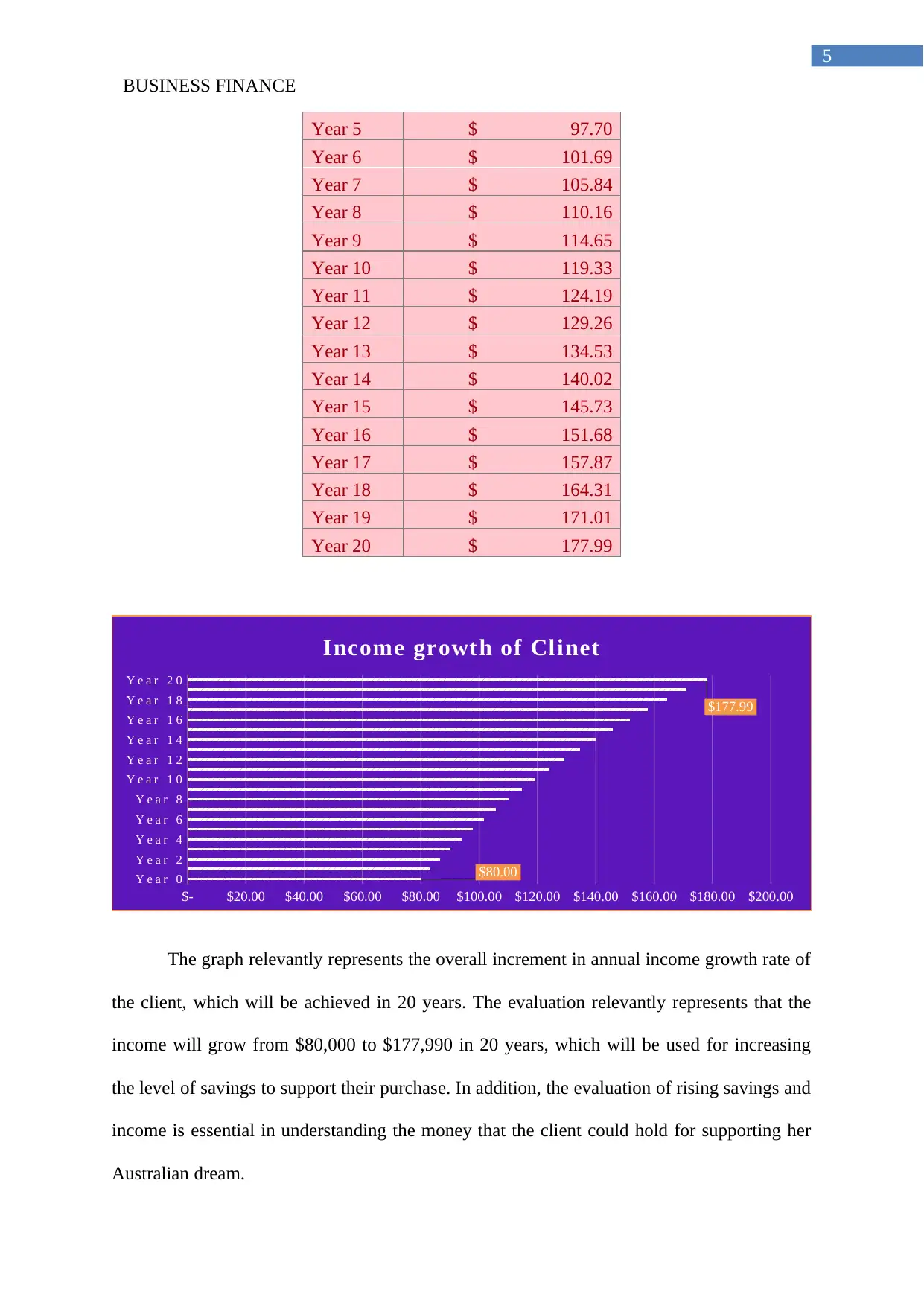

Year 5 $ 97.70

Year 6 $ 101.69

Year 7 $ 105.84

Year 8 $ 110.16

Year 9 $ 114.65

Year 10 $ 119.33

Year 11 $ 124.19

Year 12 $ 129.26

Year 13 $ 134.53

Year 14 $ 140.02

Year 15 $ 145.73

Year 16 $ 151.68

Year 17 $ 157.87

Year 18 $ 164.31

Year 19 $ 171.01

Year 20 $ 177.99

Y e a r 0

Y e a r 2

Y e a r 4

Y e a r 6

Y e a r 8

Y e a r 1 0

Y e a r 1 2

Y e a r 1 4

Y e a r 1 6

Y e a r 1 8

Y e a r 2 0

$- $20.00 $40.00 $60.00 $80.00 $100.00 $120.00 $140.00 $160.00 $180.00 $200.00

$80.00

$177.99

Income growth of Clinet

The graph relevantly represents the overall increment in annual income growth rate of

the client, which will be achieved in 20 years. The evaluation relevantly represents that the

income will grow from $80,000 to $177,990 in 20 years, which will be used for increasing

the level of savings to support their purchase. In addition, the evaluation of rising savings and

income is essential in understanding the money that the client could hold for supporting her

Australian dream.

5

Year 5 $ 97.70

Year 6 $ 101.69

Year 7 $ 105.84

Year 8 $ 110.16

Year 9 $ 114.65

Year 10 $ 119.33

Year 11 $ 124.19

Year 12 $ 129.26

Year 13 $ 134.53

Year 14 $ 140.02

Year 15 $ 145.73

Year 16 $ 151.68

Year 17 $ 157.87

Year 18 $ 164.31

Year 19 $ 171.01

Year 20 $ 177.99

Y e a r 0

Y e a r 2

Y e a r 4

Y e a r 6

Y e a r 8

Y e a r 1 0

Y e a r 1 2

Y e a r 1 4

Y e a r 1 6

Y e a r 1 8

Y e a r 2 0

$- $20.00 $40.00 $60.00 $80.00 $100.00 $120.00 $140.00 $160.00 $180.00 $200.00

$80.00

$177.99

Income growth of Clinet

The graph relevantly represents the overall increment in annual income growth rate of

the client, which will be achieved in 20 years. The evaluation relevantly represents that the

income will grow from $80,000 to $177,990 in 20 years, which will be used for increasing

the level of savings to support their purchase. In addition, the evaluation of rising savings and

income is essential in understanding the money that the client could hold for supporting her

Australian dream.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

6

Answer for the Question 3:

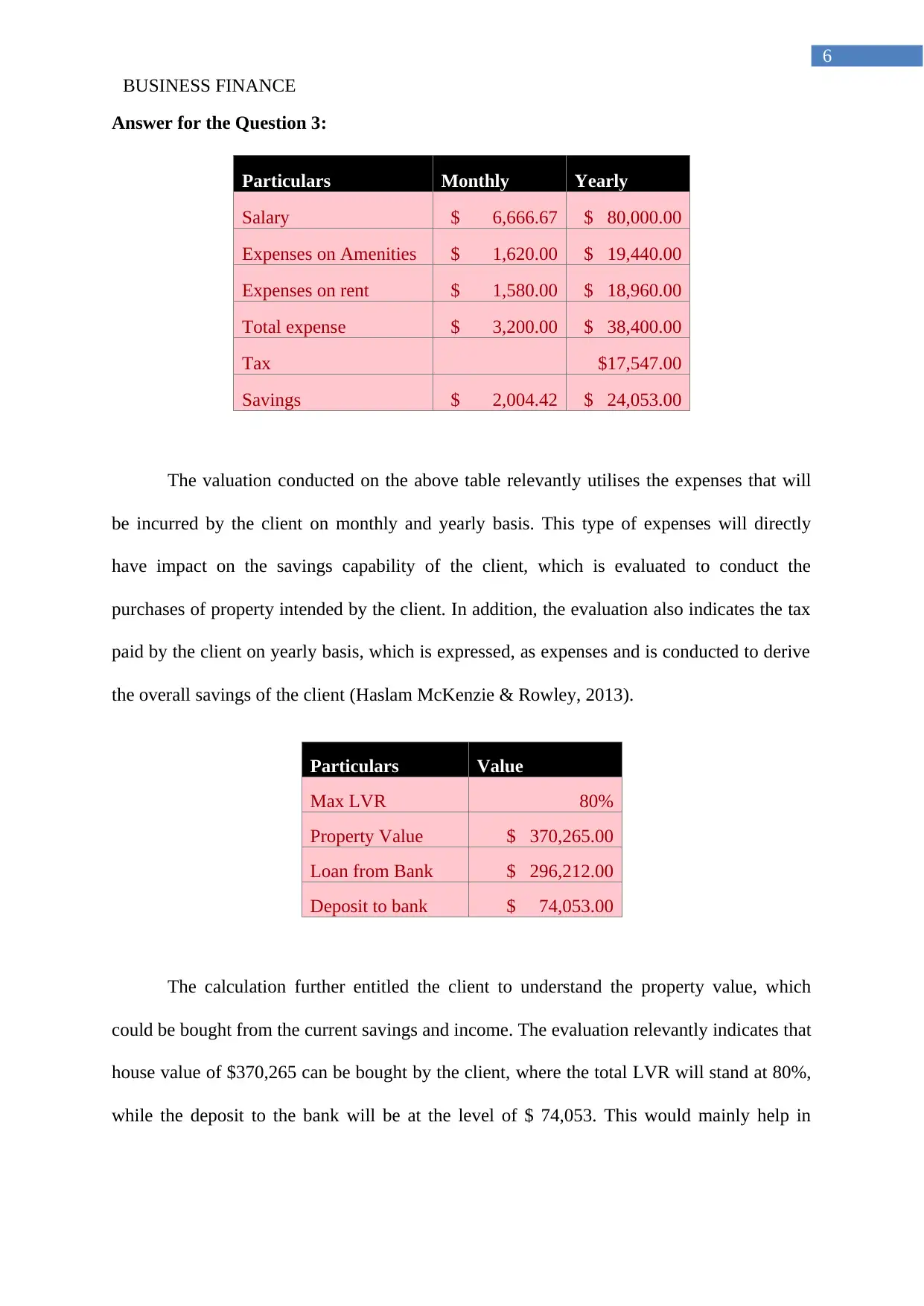

Particulars Monthly Yearly

Salary $ 6,666.67 $ 80,000.00

Expenses on Amenities $ 1,620.00 $ 19,440.00

Expenses on rent $ 1,580.00 $ 18,960.00

Total expense $ 3,200.00 $ 38,400.00

Tax $17,547.00

Savings $ 2,004.42 $ 24,053.00

The valuation conducted on the above table relevantly utilises the expenses that will

be incurred by the client on monthly and yearly basis. This type of expenses will directly

have impact on the savings capability of the client, which is evaluated to conduct the

purchases of property intended by the client. In addition, the evaluation also indicates the tax

paid by the client on yearly basis, which is expressed, as expenses and is conducted to derive

the overall savings of the client (Haslam McKenzie & Rowley, 2013).

Particulars Value

Max LVR 80%

Property Value $ 370,265.00

Loan from Bank $ 296,212.00

Deposit to bank $ 74,053.00

The calculation further entitled the client to understand the property value, which

could be bought from the current savings and income. The evaluation relevantly indicates that

house value of $370,265 can be bought by the client, where the total LVR will stand at 80%,

while the deposit to the bank will be at the level of $ 74,053. This would mainly help in

6

Answer for the Question 3:

Particulars Monthly Yearly

Salary $ 6,666.67 $ 80,000.00

Expenses on Amenities $ 1,620.00 $ 19,440.00

Expenses on rent $ 1,580.00 $ 18,960.00

Total expense $ 3,200.00 $ 38,400.00

Tax $17,547.00

Savings $ 2,004.42 $ 24,053.00

The valuation conducted on the above table relevantly utilises the expenses that will

be incurred by the client on monthly and yearly basis. This type of expenses will directly

have impact on the savings capability of the client, which is evaluated to conduct the

purchases of property intended by the client. In addition, the evaluation also indicates the tax

paid by the client on yearly basis, which is expressed, as expenses and is conducted to derive

the overall savings of the client (Haslam McKenzie & Rowley, 2013).

Particulars Value

Max LVR 80%

Property Value $ 370,265.00

Loan from Bank $ 296,212.00

Deposit to bank $ 74,053.00

The calculation further entitled the client to understand the property value, which

could be bought from the current savings and income. The evaluation relevantly indicates that

house value of $370,265 can be bought by the client, where the total LVR will stand at 80%,

while the deposit to the bank will be at the level of $ 74,053. This would mainly help in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

7

understanding the level of property value and loan from bank, which will be provided by the

lender to the client (Jacobs, 2015).

Answer for the Question 4:

Particulars (Without Insurance premium) Value

Max LVR 80%

Property Value $ 364,945.00

Loan from Bank $ 291,956.00

Deposit to bank $ 72,989.00

Stamp Duty $ 1,064.00

From the evaluation it could be identified that loan without the insurance premium

will only allow the cline to acquire the loan with LVR 80%. In addition, this will only allow

the client to acquire a loan amount of $291,956 from the bank, while the deposit to bank will

be at the level of $72,989. This would directly have an impact on property price where

restriction of savings will result in capability of the lender to acquire the loan.

Particulars (With Insurance premium) Value

Max LVR 98%

Property Value $ 715,000.00

Loan from Bank $ 698,404.00

Deposit to bank $ 16,596.00

Stamp Duty $ 29,110.00

Insurance Premium $ 28,347.00

The valuation mainly helps in understanding the level of property price with the

insurance premium, as it allows the borrower to increase the LVR as high as 98%. From the

overall valuation it could be detected that the client could afford a total house property value

of $715,000, where the total deposit to bank is at the level of $16,596 with the stamp duty at

7

understanding the level of property value and loan from bank, which will be provided by the

lender to the client (Jacobs, 2015).

Answer for the Question 4:

Particulars (Without Insurance premium) Value

Max LVR 80%

Property Value $ 364,945.00

Loan from Bank $ 291,956.00

Deposit to bank $ 72,989.00

Stamp Duty $ 1,064.00

From the evaluation it could be identified that loan without the insurance premium

will only allow the cline to acquire the loan with LVR 80%. In addition, this will only allow

the client to acquire a loan amount of $291,956 from the bank, while the deposit to bank will

be at the level of $72,989. This would directly have an impact on property price where

restriction of savings will result in capability of the lender to acquire the loan.

Particulars (With Insurance premium) Value

Max LVR 98%

Property Value $ 715,000.00

Loan from Bank $ 698,404.00

Deposit to bank $ 16,596.00

Stamp Duty $ 29,110.00

Insurance Premium $ 28,347.00

The valuation mainly helps in understanding the level of property price with the

insurance premium, as it allows the borrower to increase the LVR as high as 98%. From the

overall valuation it could be detected that the client could afford a total house property value

of $715,000, where the total deposit to bank is at the level of $16,596 with the stamp duty at

BUSINESS FINANCE

8

$29,110 and insurance premium at the level of $28,347. This relevantly indicates that the

client could effectively purchase high value property with the help of insurance premium and

fulfil her Australian dream (Lee, & Reed, 2013).

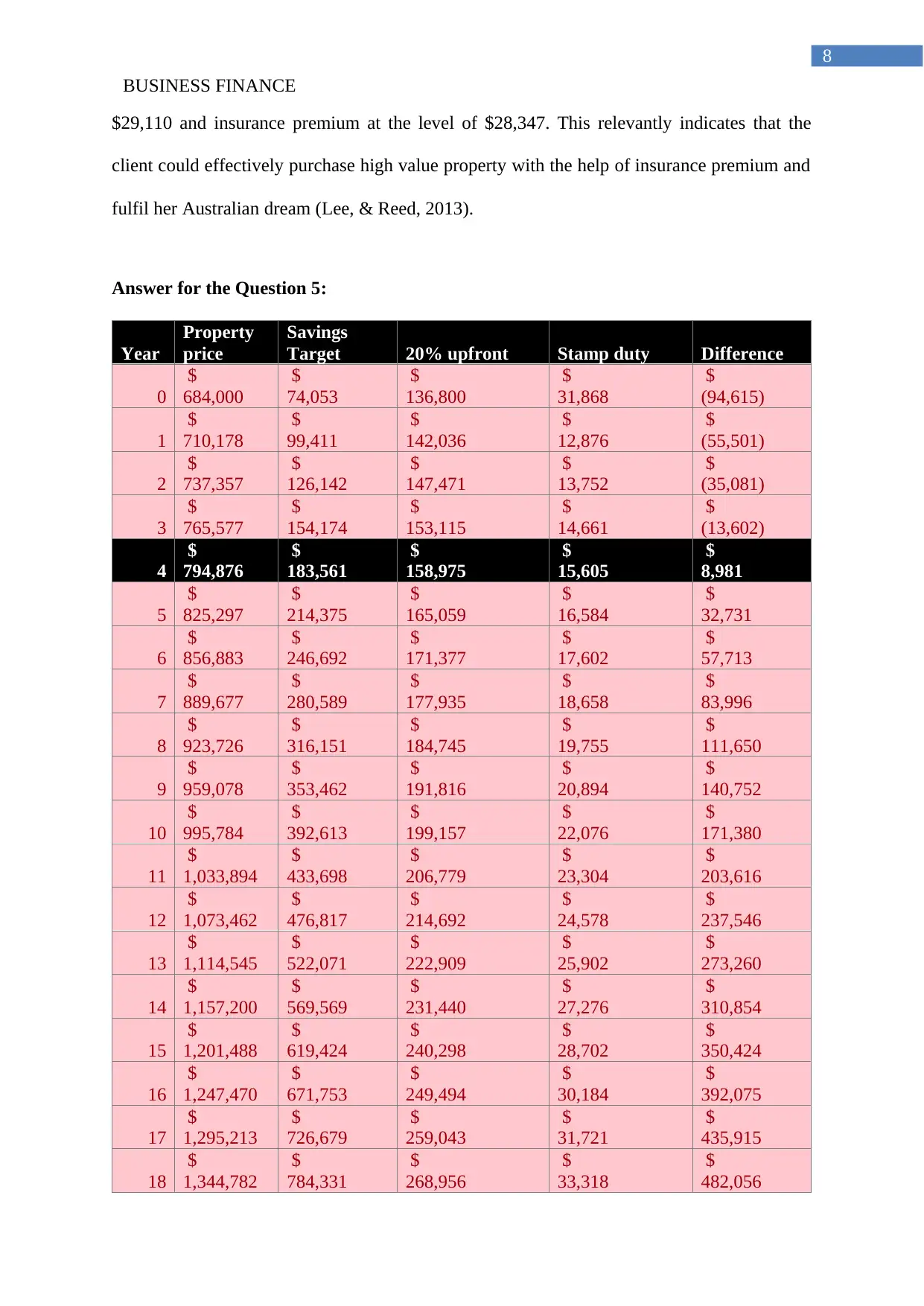

Answer for the Question 5:

Year

Property

price

Savings

Target 20% upfront Stamp duty Difference

0

$

684,000

$

74,053

$

136,800

$

31,868

$

(94,615)

1

$

710,178

$

99,411

$

142,036

$

12,876

$

(55,501)

2

$

737,357

$

126,142

$

147,471

$

13,752

$

(35,081)

3

$

765,577

$

154,174

$

153,115

$

14,661

$

(13,602)

4

$

794,876

$

183,561

$

158,975

$

15,605

$

8,981

5

$

825,297

$

214,375

$

165,059

$

16,584

$

32,731

6

$

856,883

$

246,692

$

171,377

$

17,602

$

57,713

7

$

889,677

$

280,589

$

177,935

$

18,658

$

83,996

8

$

923,726

$

316,151

$

184,745

$

19,755

$

111,650

9

$

959,078

$

353,462

$

191,816

$

20,894

$

140,752

10

$

995,784

$

392,613

$

199,157

$

22,076

$

171,380

11

$

1,033,894

$

433,698

$

206,779

$

23,304

$

203,616

12

$

1,073,462

$

476,817

$

214,692

$

24,578

$

237,546

13

$

1,114,545

$

522,071

$

222,909

$

25,902

$

273,260

14

$

1,157,200

$

569,569

$

231,440

$

27,276

$

310,854

15

$

1,201,488

$

619,424

$

240,298

$

28,702

$

350,424

16

$

1,247,470

$

671,753

$

249,494

$

30,184

$

392,075

17

$

1,295,213

$

726,679

$

259,043

$

31,721

$

435,915

18

$

1,344,782

$

784,331

$

268,956

$

33,318

$

482,056

8

$29,110 and insurance premium at the level of $28,347. This relevantly indicates that the

client could effectively purchase high value property with the help of insurance premium and

fulfil her Australian dream (Lee, & Reed, 2013).

Answer for the Question 5:

Year

Property

price

Savings

Target 20% upfront Stamp duty Difference

0

$

684,000

$

74,053

$

136,800

$

31,868

$

(94,615)

1

$

710,178

$

99,411

$

142,036

$

12,876

$

(55,501)

2

$

737,357

$

126,142

$

147,471

$

13,752

$

(35,081)

3

$

765,577

$

154,174

$

153,115

$

14,661

$

(13,602)

4

$

794,876

$

183,561

$

158,975

$

15,605

$

8,981

5

$

825,297

$

214,375

$

165,059

$

16,584

$

32,731

6

$

856,883

$

246,692

$

171,377

$

17,602

$

57,713

7

$

889,677

$

280,589

$

177,935

$

18,658

$

83,996

8

$

923,726

$

316,151

$

184,745

$

19,755

$

111,650

9

$

959,078

$

353,462

$

191,816

$

20,894

$

140,752

10

$

995,784

$

392,613

$

199,157

$

22,076

$

171,380

11

$

1,033,894

$

433,698

$

206,779

$

23,304

$

203,616

12

$

1,073,462

$

476,817

$

214,692

$

24,578

$

237,546

13

$

1,114,545

$

522,071

$

222,909

$

25,902

$

273,260

14

$

1,157,200

$

569,569

$

231,440

$

27,276

$

310,854

15

$

1,201,488

$

619,424

$

240,298

$

28,702

$

350,424

16

$

1,247,470

$

671,753

$

249,494

$

30,184

$

392,075

17

$

1,295,213

$

726,679

$

259,043

$

31,721

$

435,915

18

$

1,344,782

$

784,331

$

268,956

$

33,318

$

482,056

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

BUSINESS FINANCE

9

19

$

1,396,249

$

844,843

$

279,250

$

34,976

$

530,617

20

$

1,449,686

$

908,356

$

289,937

$

36,697

$

581,722

Year

Property

price

Savings

Target

5%

upfront

Insurance

premium Stamp duty Amount

0

$

684,000

$

74,053

$

34,200

$

20,222

$

31,868

$

(12,237)

1

$

710,178

$

99,411

$

35,509

$

20,996

$

12,876

$

30,030

2

$

737,357

$

126,142

$

36,868

$

21,799

$

13,752

$

53,723

3

$

765,577

$

154,174

$

38,279

$

22,634

$

14,661

$

78,601

4

$

794,876

$

183,561

$

39,744

$

23,500

$

15,605

$

104,713

5

$

825,297

$

214,375

$

41,265

$

24,399

$

16,584

$

132,127

6

$

856,883

$

246,692

$

42,844

$

25,333

$

17,602

$

160,913

7

$

889,677

$

280,589

$

44,484

$

26,303

$

18,658

$

191,145

8

$

923,726

$

316,151

$

46,186

$

27,309

$

19,755

$

222,900

9

$

959,078

$

353,462

$

47,954

$

28,355

$

20,894

$

256,259

10

$

995,784

$

392,613

$

49,789

$

29,440

$

22,076

$

291,308

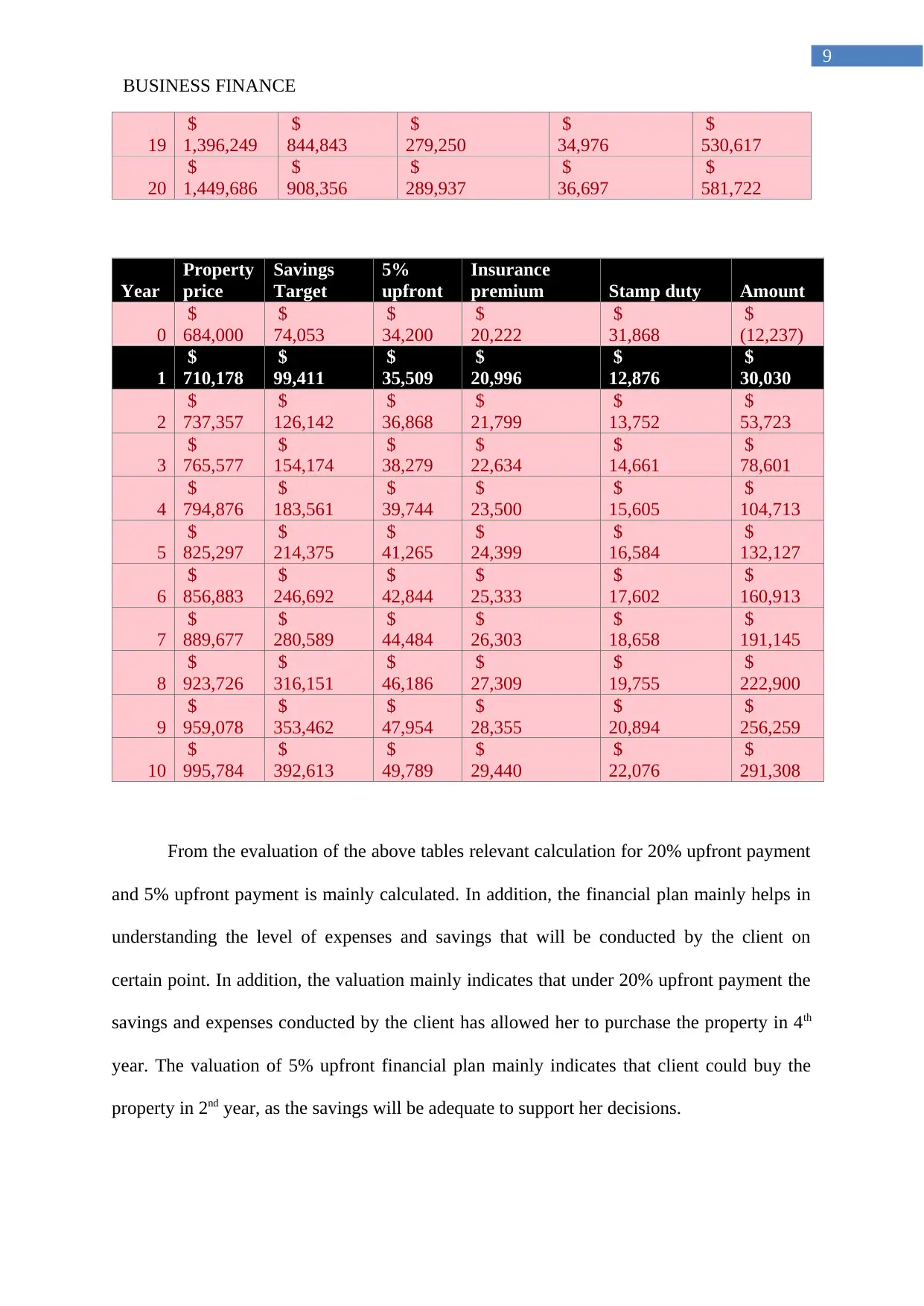

From the evaluation of the above tables relevant calculation for 20% upfront payment

and 5% upfront payment is mainly calculated. In addition, the financial plan mainly helps in

understanding the level of expenses and savings that will be conducted by the client on

certain point. In addition, the valuation mainly indicates that under 20% upfront payment the

savings and expenses conducted by the client has allowed her to purchase the property in 4th

year. The valuation of 5% upfront financial plan mainly indicates that client could buy the

property in 2nd year, as the savings will be adequate to support her decisions.

9

19

$

1,396,249

$

844,843

$

279,250

$

34,976

$

530,617

20

$

1,449,686

$

908,356

$

289,937

$

36,697

$

581,722

Year

Property

price

Savings

Target

5%

upfront

Insurance

premium Stamp duty Amount

0

$

684,000

$

74,053

$

34,200

$

20,222

$

31,868

$

(12,237)

1

$

710,178

$

99,411

$

35,509

$

20,996

$

12,876

$

30,030

2

$

737,357

$

126,142

$

36,868

$

21,799

$

13,752

$

53,723

3

$

765,577

$

154,174

$

38,279

$

22,634

$

14,661

$

78,601

4

$

794,876

$

183,561

$

39,744

$

23,500

$

15,605

$

104,713

5

$

825,297

$

214,375

$

41,265

$

24,399

$

16,584

$

132,127

6

$

856,883

$

246,692

$

42,844

$

25,333

$

17,602

$

160,913

7

$

889,677

$

280,589

$

44,484

$

26,303

$

18,658

$

191,145

8

$

923,726

$

316,151

$

46,186

$

27,309

$

19,755

$

222,900

9

$

959,078

$

353,462

$

47,954

$

28,355

$

20,894

$

256,259

10

$

995,784

$

392,613

$

49,789

$

29,440

$

22,076

$

291,308

From the evaluation of the above tables relevant calculation for 20% upfront payment

and 5% upfront payment is mainly calculated. In addition, the financial plan mainly helps in

understanding the level of expenses and savings that will be conducted by the client on

certain point. In addition, the valuation mainly indicates that under 20% upfront payment the

savings and expenses conducted by the client has allowed her to purchase the property in 4th

year. The valuation of 5% upfront financial plan mainly indicates that client could buy the

property in 2nd year, as the savings will be adequate to support her decisions.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

BUSINESS FINANCE

10

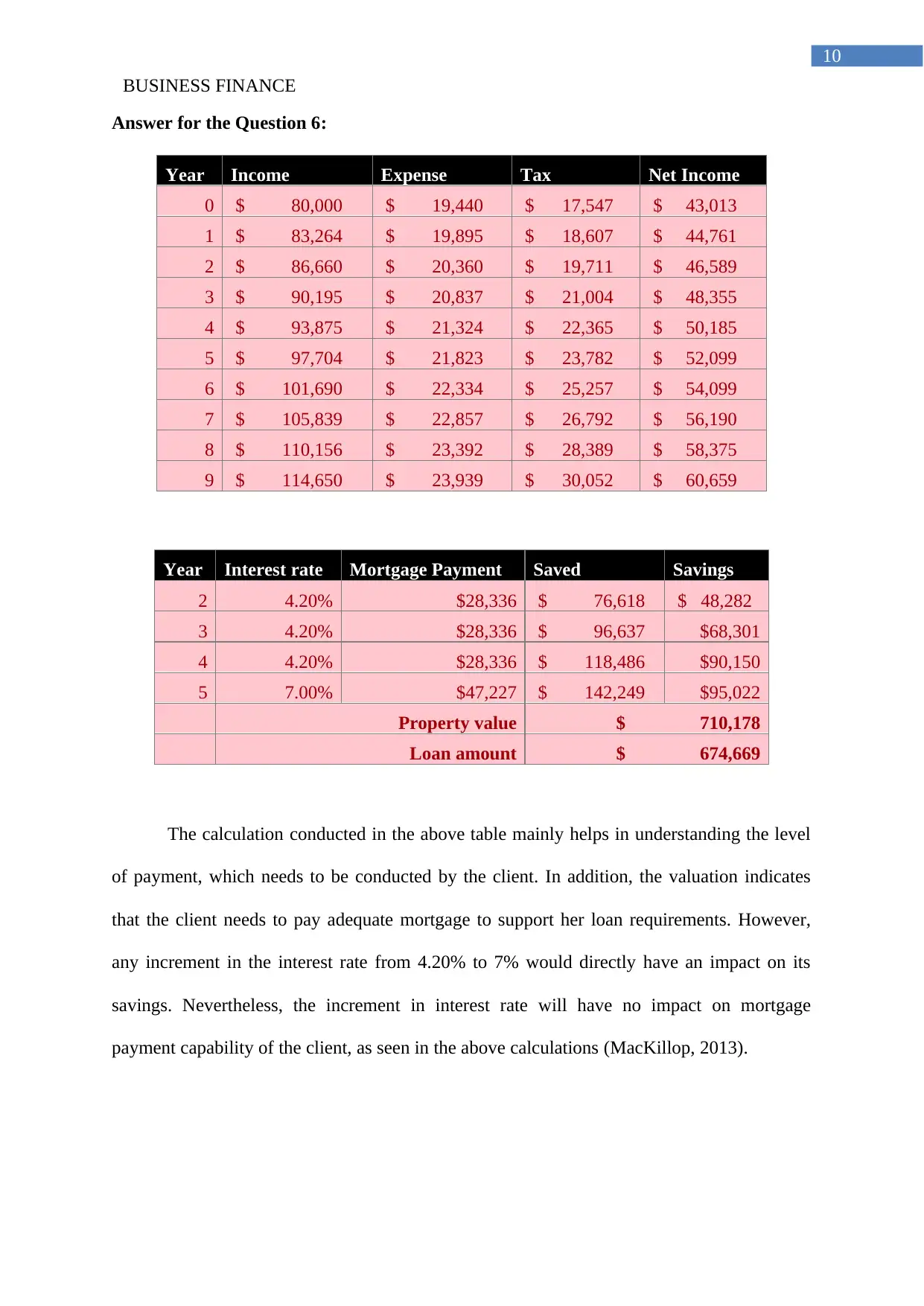

Answer for the Question 6:

Year Income Expense Tax Net Income

0 $ 80,000 $ 19,440 $ 17,547 $ 43,013

1 $ 83,264 $ 19,895 $ 18,607 $ 44,761

2 $ 86,660 $ 20,360 $ 19,711 $ 46,589

3 $ 90,195 $ 20,837 $ 21,004 $ 48,355

4 $ 93,875 $ 21,324 $ 22,365 $ 50,185

5 $ 97,704 $ 21,823 $ 23,782 $ 52,099

6 $ 101,690 $ 22,334 $ 25,257 $ 54,099

7 $ 105,839 $ 22,857 $ 26,792 $ 56,190

8 $ 110,156 $ 23,392 $ 28,389 $ 58,375

9 $ 114,650 $ 23,939 $ 30,052 $ 60,659

Year Interest rate Mortgage Payment Saved Savings

2 4.20% $28,336 $ 76,618 $ 48,282

3 4.20% $28,336 $ 96,637 $68,301

4 4.20% $28,336 $ 118,486 $90,150

5 7.00% $47,227 $ 142,249 $95,022

Property value $ 710,178

Loan amount $ 674,669

The calculation conducted in the above table mainly helps in understanding the level

of payment, which needs to be conducted by the client. In addition, the valuation indicates

that the client needs to pay adequate mortgage to support her loan requirements. However,

any increment in the interest rate from 4.20% to 7% would directly have an impact on its

savings. Nevertheless, the increment in interest rate will have no impact on mortgage

payment capability of the client, as seen in the above calculations (MacKillop, 2013).

10

Answer for the Question 6:

Year Income Expense Tax Net Income

0 $ 80,000 $ 19,440 $ 17,547 $ 43,013

1 $ 83,264 $ 19,895 $ 18,607 $ 44,761

2 $ 86,660 $ 20,360 $ 19,711 $ 46,589

3 $ 90,195 $ 20,837 $ 21,004 $ 48,355

4 $ 93,875 $ 21,324 $ 22,365 $ 50,185

5 $ 97,704 $ 21,823 $ 23,782 $ 52,099

6 $ 101,690 $ 22,334 $ 25,257 $ 54,099

7 $ 105,839 $ 22,857 $ 26,792 $ 56,190

8 $ 110,156 $ 23,392 $ 28,389 $ 58,375

9 $ 114,650 $ 23,939 $ 30,052 $ 60,659

Year Interest rate Mortgage Payment Saved Savings

2 4.20% $28,336 $ 76,618 $ 48,282

3 4.20% $28,336 $ 96,637 $68,301

4 4.20% $28,336 $ 118,486 $90,150

5 7.00% $47,227 $ 142,249 $95,022

Property value $ 710,178

Loan amount $ 674,669

The calculation conducted in the above table mainly helps in understanding the level

of payment, which needs to be conducted by the client. In addition, the valuation indicates

that the client needs to pay adequate mortgage to support her loan requirements. However,

any increment in the interest rate from 4.20% to 7% would directly have an impact on its

savings. Nevertheless, the increment in interest rate will have no impact on mortgage

payment capability of the client, as seen in the above calculations (MacKillop, 2013).

BUSINESS FINANCE

11

Answer for the Question 7:

The calculation conducted in the above financial plan mainly helps in understanding

the level of expenses and income that will be generated by the client. The evaluation is

mainly conducted on the basis income flow of the client, while any kind of extra increment in

expenses will result in fulfilment of the financial plan. The changes in inflation rate and

property price will have an impact on the financial position of the client, which will directly

have negative effect on savings of the client. The overall decline in income of the client will

have a drastic impact on the functionality of the financial plan, as the client will not be able to

support her living expense and mortgage payment, Hence, the main requirements of the

financial plan is to maintain adequate income thought out the life of mortgage.

11

Answer for the Question 7:

The calculation conducted in the above financial plan mainly helps in understanding

the level of expenses and income that will be generated by the client. The evaluation is

mainly conducted on the basis income flow of the client, while any kind of extra increment in

expenses will result in fulfilment of the financial plan. The changes in inflation rate and

property price will have an impact on the financial position of the client, which will directly

have negative effect on savings of the client. The overall decline in income of the client will

have a drastic impact on the functionality of the financial plan, as the client will not be able to

support her living expense and mortgage payment, Hence, the main requirements of the

financial plan is to maintain adequate income thought out the life of mortgage.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.