Research Project: Analyzing Climate Change and Firm Performance

VerifiedAdded on 2020/05/28

|7

|1174

|67

Report

AI Summary

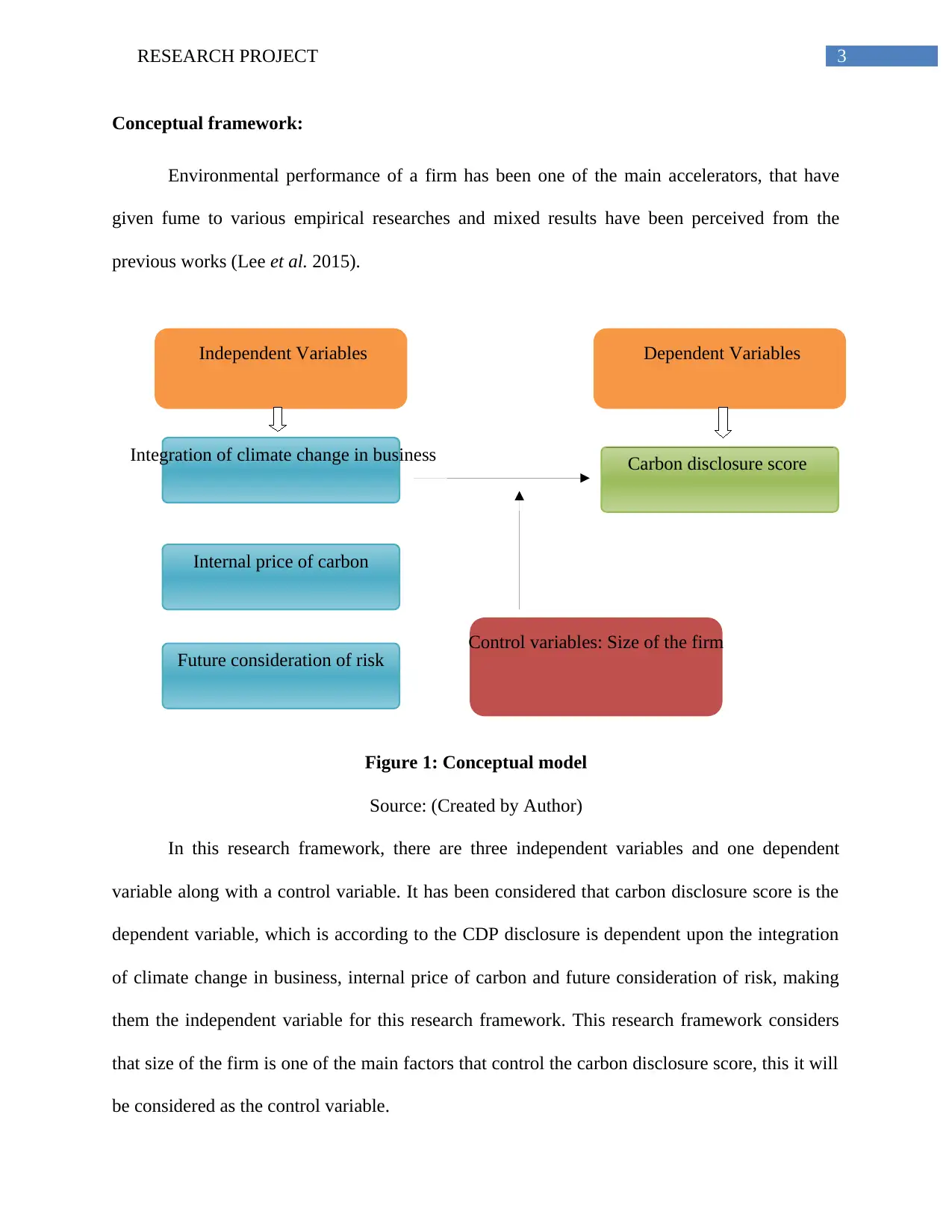

This research report presents a framework to analyze the impact of climate change on firm performance, incorporating the Climate Disclosure Project (CDP) and legitimacy theory. The report outlines a conceptual framework, detailing independent and dependent variables, including carbon disclosure scores, integration of climate change in business, internal carbon pricing, and future risk considerations. It establishes a hypothesis suggesting a positive relationship between these independent variables and carbon disclosure scores, with firm size as a control variable. Proxy measures, utilizing CDP data and firm age, are proposed to assess carbon disclosure and environmental responsibility. The study aims to analyze the firm’s economic and environmental performance in relation to corporate responses and climate change risks, using regression analysis on data from 1047 companies. The research underscores the importance of corporate responses in addressing climate change and its impact on firm performance.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.