CLWM4100 Taxation Law: Comprehensive Case Study on Australian Taxation

VerifiedAdded on 2023/06/07

|9

|1584

|260

Case Study

AI Summary

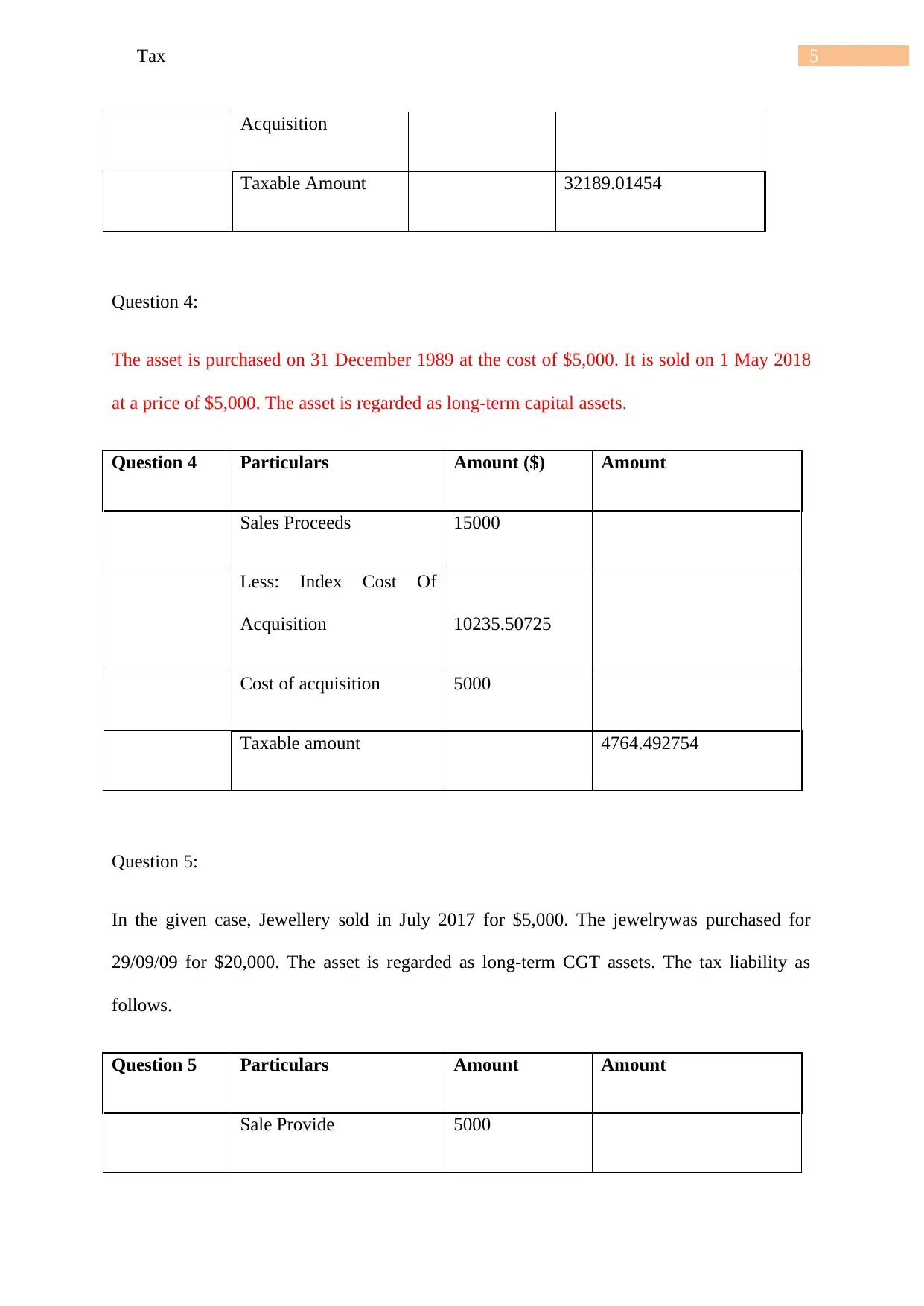

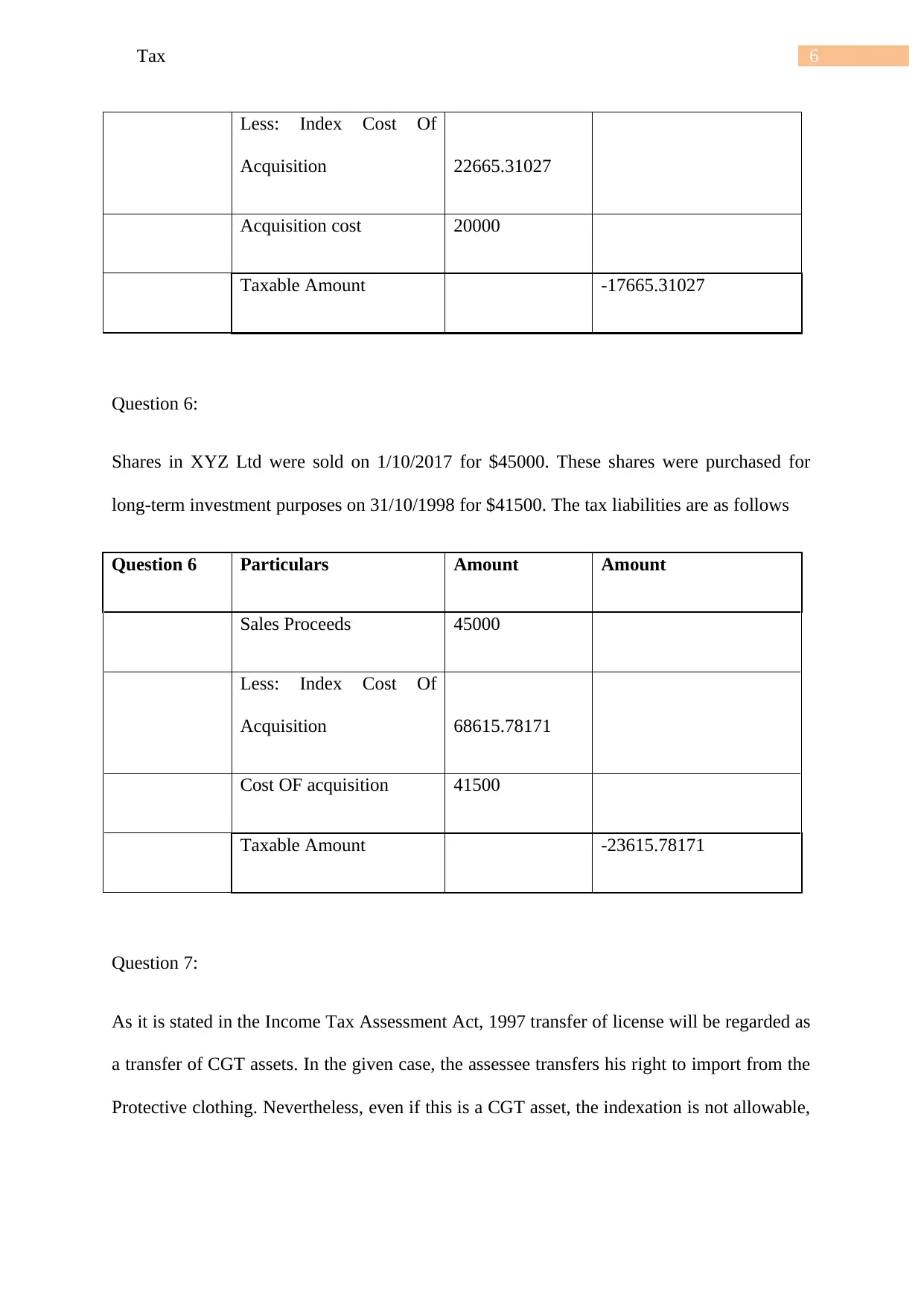

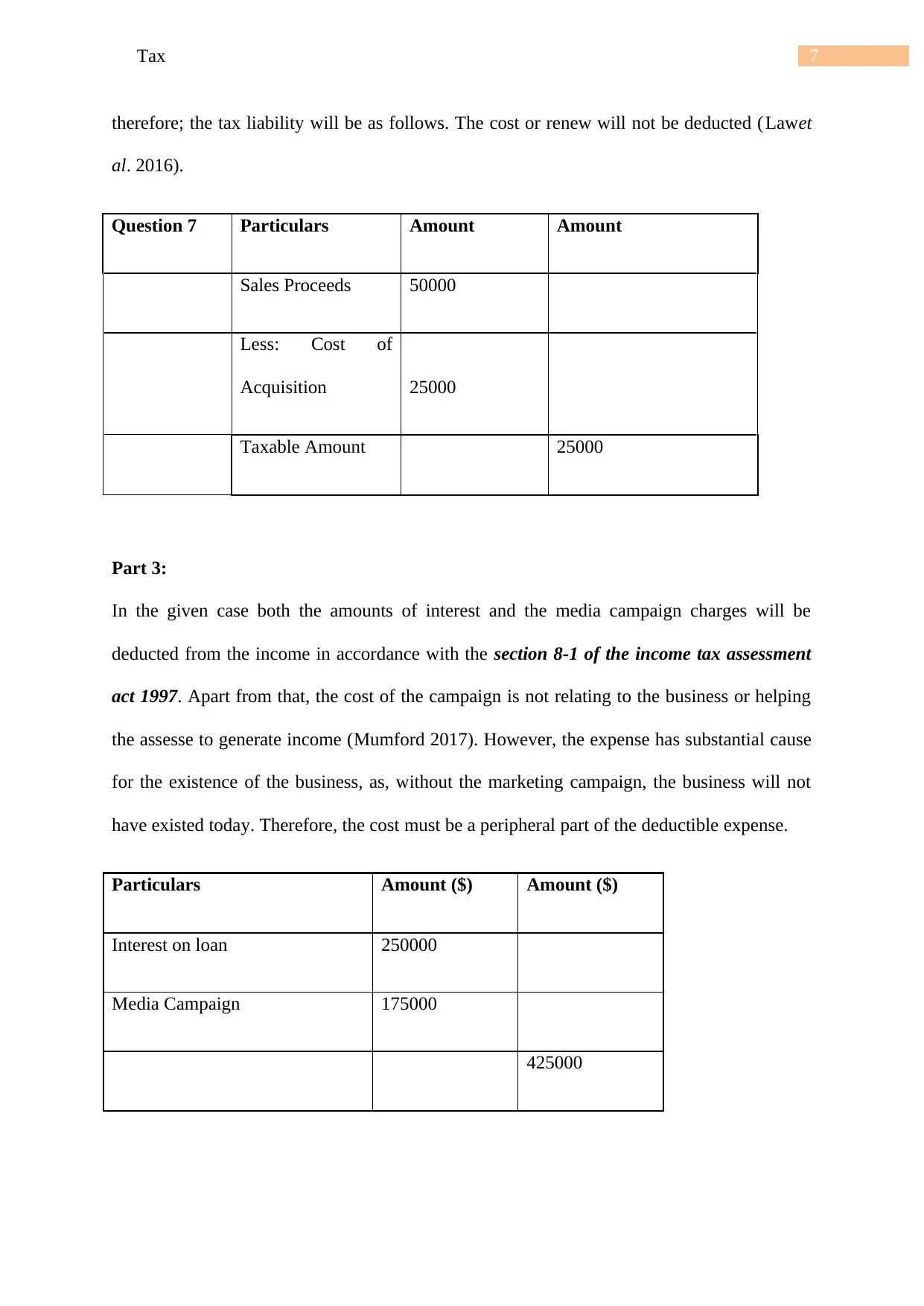

This case study delves into various aspects of Australian taxation law, focusing primarily on determining tax residency for a company operating both within Australia and internationally, and analyzing capital gains tax (CGT) implications for various asset sales. The analysis of tax residency involves applying section 6(1) of the Income Tax Assessment Act, considering factors such as the location of business operations, central management and control, and shareholder influence, referencing relevant case law like Bywater Investments Ltd & Ors V Commissioner of Taxation. The CGT component calculates taxable amounts from the sale of different assets, including land, shares, and jewelry, taking into account acquisition costs, indexation, and potential capital losses, referencing section 8-2 and 186-5 of the ITAA 97. Additionally, the case study addresses the deductibility of expenses such as loan interest and media campaign costs under section 8-1 of the Income Tax Assessment Act 1997, ultimately providing a comprehensive overview of key taxation principles and their practical application.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.