CMBS Analysis: Structure, Benefits, and Investment Strategies Report

VerifiedAdded on 2022/09/14

|9

|1777

|11

Report

AI Summary

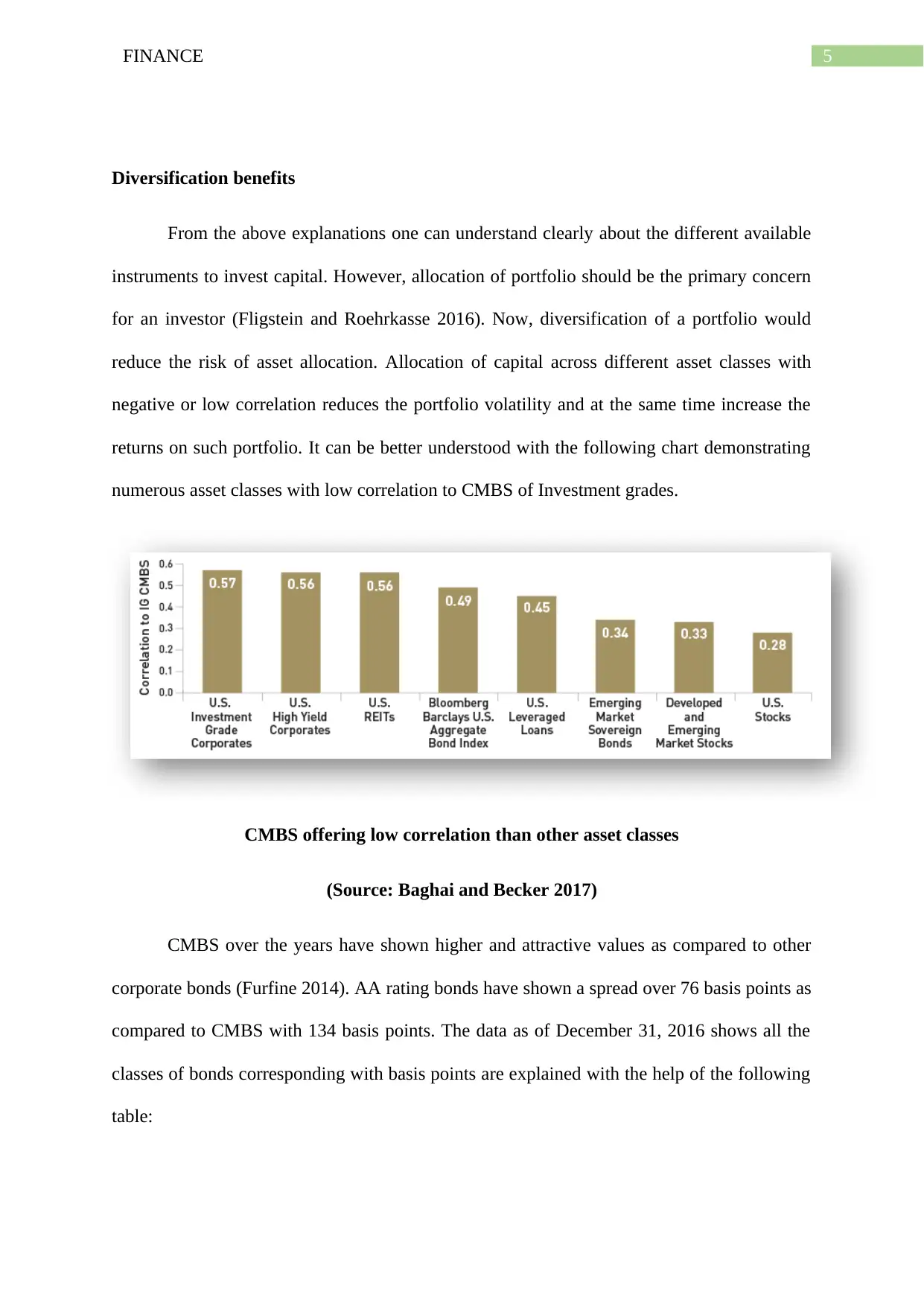

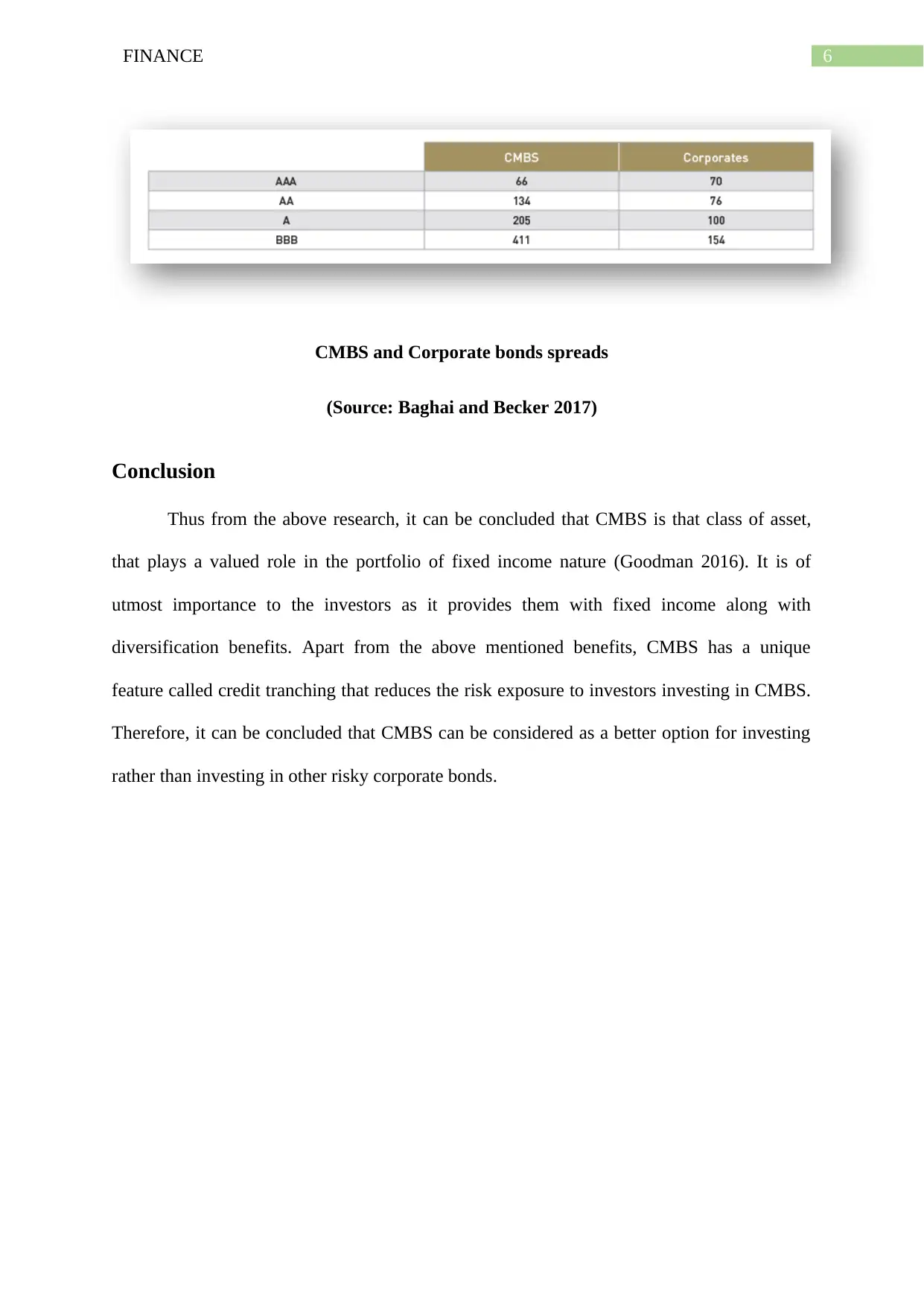

This report provides a detailed analysis of Commercial Mortgage-Backed Securities (CMBS). It begins with an introduction to CMBS, highlighting their unique features and role in providing liquidity to commercial lenders and real estate investors. The report explains the structure of CMBS, including how they are backed by commercial property mortgages, and the process of loan securitization. It then delves into credit tranching, explaining how CMBS are divided into tranches with varying risk levels to protect investors, and the diversification benefits of CMBS compared to other asset classes. The report also compares CMBS with corporate bonds and provides data on their spreads. Finally, it concludes that CMBS play a valuable role in fixed-income portfolios and can be a better investment option than other risky corporate bonds. The report includes tables and charts to illustrate key concepts, and references several academic sources.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.