Financial Feasibility Case Study: Launching a New Machine at CMC

VerifiedAdded on 2023/06/11

|7

|1553

|324

Case Study

AI Summary

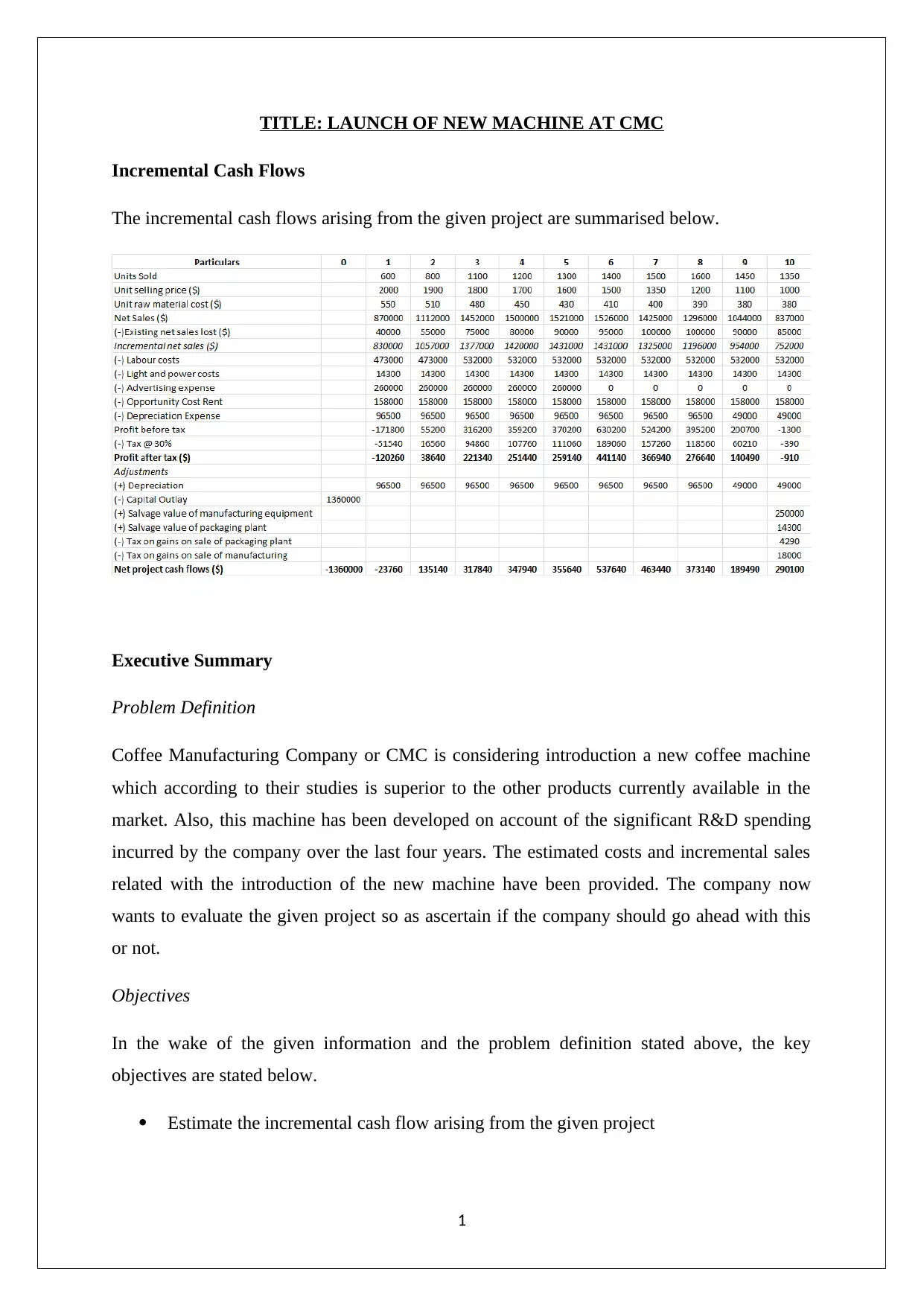

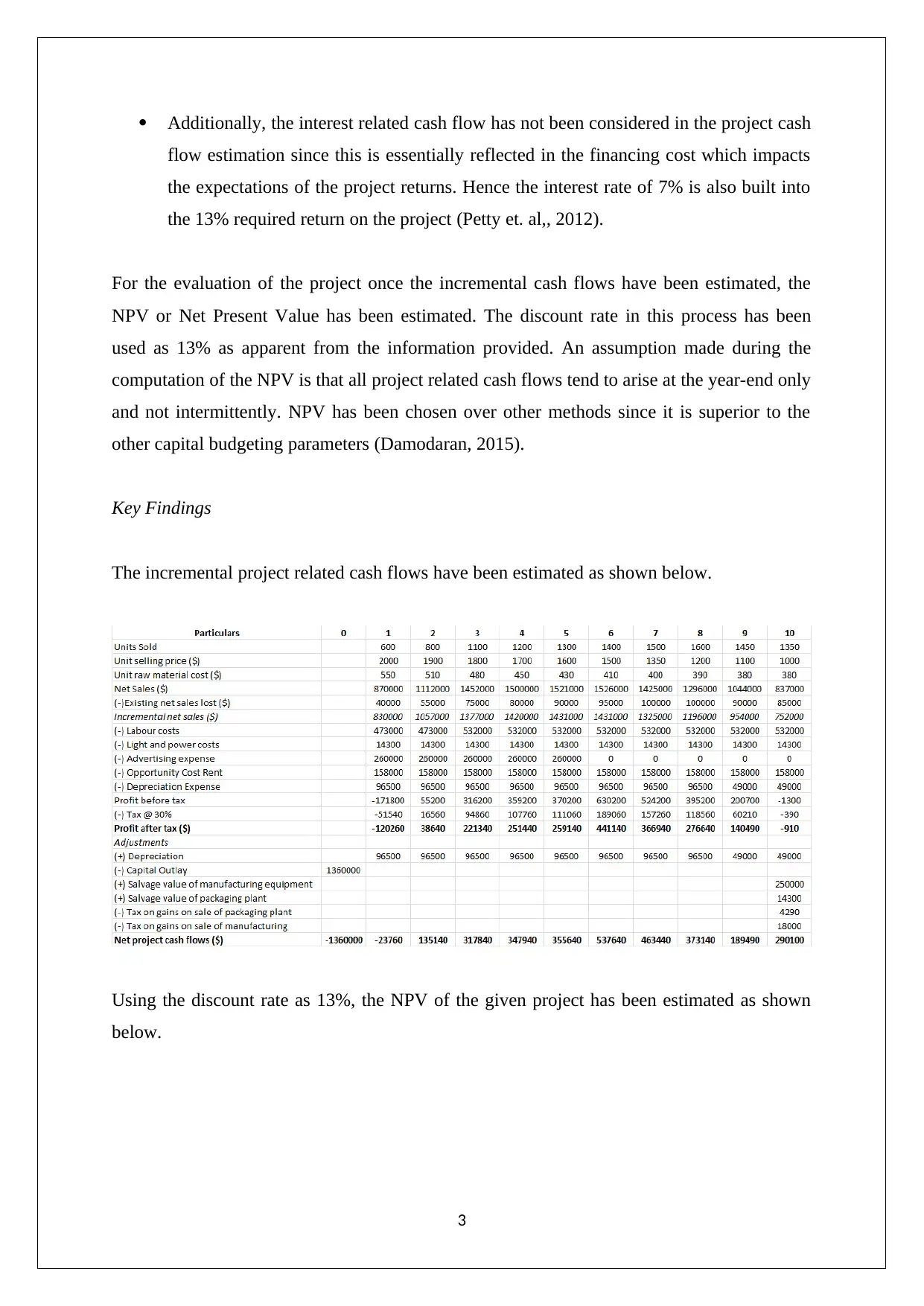

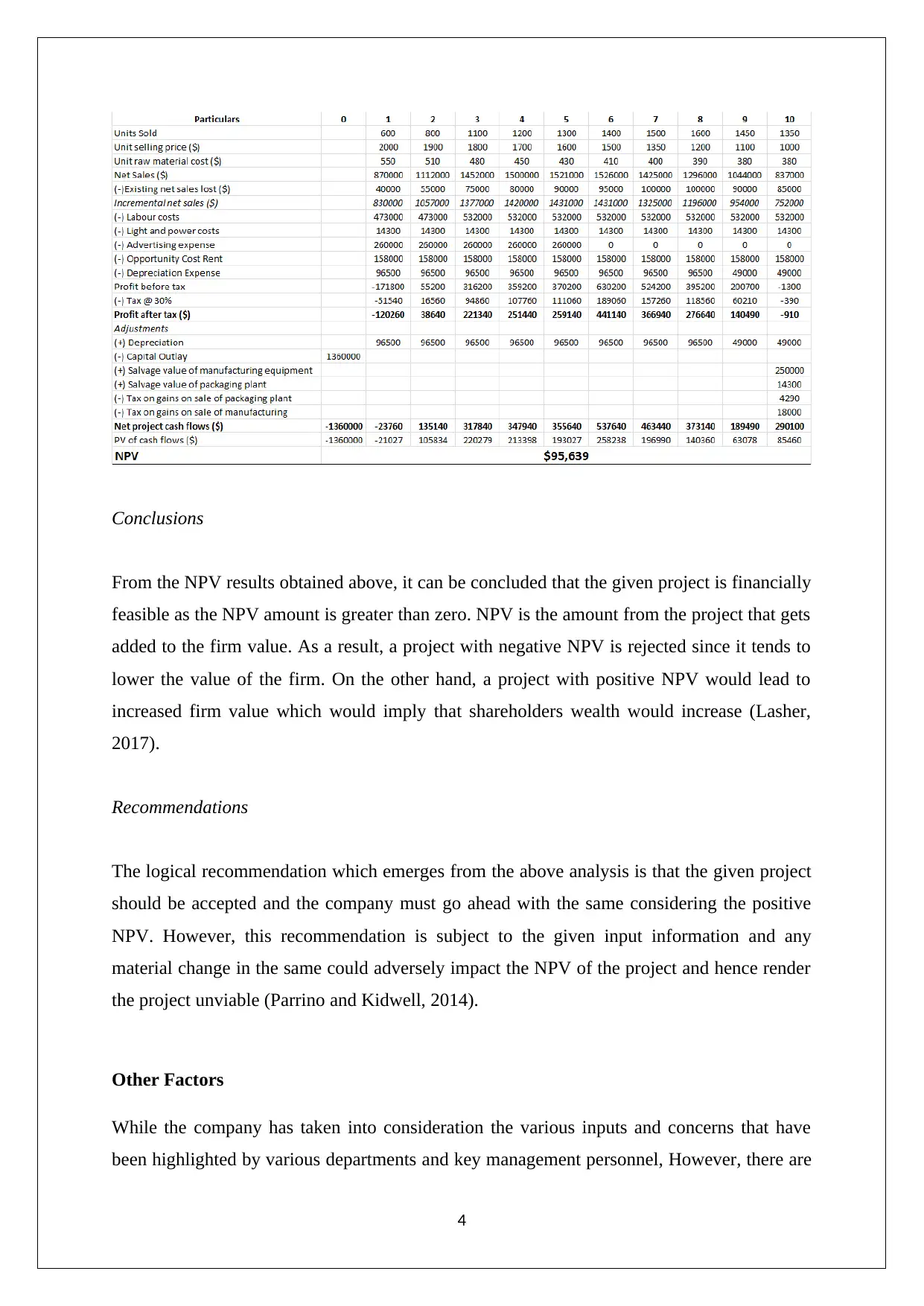

This case study examines the financial feasibility of Coffee Manufacturing Company's (CMC) plan to launch a new coffee machine. It details the estimation of incremental cash flows, considering factors like opportunity costs, depreciation, and potential competitive responses. The analysis uses Net Present Value (NPV) to determine project viability, concluding that the project is financially feasible due to a positive NPV. The study also highlights the importance of considering competitor reactions, uncertainty analysis, and broader market impacts for a comprehensive evaluation. Desklib provides a platform for students to access this and other solved assignments.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.