Coca-Cola Amatil Auditing: Australian Standards, Compliance & Opinion

VerifiedAdded on 2023/06/05

|14

|3947

|53

Report

AI Summary

This report provides a detailed analysis of the auditing activities of Coca-Cola Amatil, an ASX-listed company, focusing on compliance with Australian Auditing Standards such as ASA 701, ASA 315, ASA 200, and ASA 570. The report examines the auditor's independence, remuneration, and key audit matters, including the valuation of intangible assets and accounting for rebates and promotional expenses. It also discusses the structure and responsibilities of the audit committee, the auditor's unqualified opinion, and the differences in responsibilities between directors, management, and auditors. The report concludes with recommendations to enhance the effectiveness of material information developed by the company's auditors. Desklib offers a wealth of similar solved assignments and past papers for students.

RUNNING HEAD: Auditing of Coca-Cola Amatil in Australia

Auditing and Assurance in Australia

Coca-Cola Amatil

Auditing and Assurance in Australia

Coca-Cola Amatil

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing of Coca-Cola Amatil in Australia 1

Executive Summary

The below mentioned paper evaluates the details about the auditing activities of the company

Coca-Cola Amatil that is listed in ASX. The ASA 701 talks about the communication with

auditors for the key audit matters in the independent auditor’s report. The report deals with the

responsibility of the auditors to circulate the key audit matters in the report made by the auditors

for the stakeholders of the company. The report should be formed with transparency and should

be true and fair as well. Apart from this, the ASA 315 is also implemented in the report that

helps in identifying and evaluating the risk of material misstatement by knowing the company

and its environment. The latter part of the report also identifies the misstatement of materials

occurred due to fraud or error in the books of accounts of the company. Other auditing standards

that are also applied in the report are ASA 200 and ASA 570. Lastly, recommendations are also

given to increase the effectiveness of the material information developed by the auditors of the

company.

Executive Summary

The below mentioned paper evaluates the details about the auditing activities of the company

Coca-Cola Amatil that is listed in ASX. The ASA 701 talks about the communication with

auditors for the key audit matters in the independent auditor’s report. The report deals with the

responsibility of the auditors to circulate the key audit matters in the report made by the auditors

for the stakeholders of the company. The report should be formed with transparency and should

be true and fair as well. Apart from this, the ASA 315 is also implemented in the report that

helps in identifying and evaluating the risk of material misstatement by knowing the company

and its environment. The latter part of the report also identifies the misstatement of materials

occurred due to fraud or error in the books of accounts of the company. Other auditing standards

that are also applied in the report are ASA 200 and ASA 570. Lastly, recommendations are also

given to increase the effectiveness of the material information developed by the auditors of the

company.

Auditing of Coca-Cola Amatil in Australia 2

Content

s

Introduction......................................................................................................................................4

Introduction of Company.................................................................................................................4

Compliance of Independence Requirements by Auditor.................................................................5

Nature of non-audit services provided.............................................................................................5

Analysis of the Auditor's remuneration as compared to the previous year.....................................6

Audit Procedures for Key Audit Matters.........................................................................................7

Structure, Responsibilities and Functions of Audit Committee......................................................8

Audit Opinion expressed.................................................................................................................8

The difference in Director’s and Management’s responsibilities with Auditor’s responsibilities. .9

Treatment of Material Subsequent Events.......................................................................................9

Presence of Other Material information........................................................................................10

Follow-ups taken from Auditor.....................................................................................................11

Recommendations and Conclusion................................................................................................11

References......................................................................................................................................12

Content

s

Introduction......................................................................................................................................4

Introduction of Company.................................................................................................................4

Compliance of Independence Requirements by Auditor.................................................................5

Nature of non-audit services provided.............................................................................................5

Analysis of the Auditor's remuneration as compared to the previous year.....................................6

Audit Procedures for Key Audit Matters.........................................................................................7

Structure, Responsibilities and Functions of Audit Committee......................................................8

Audit Opinion expressed.................................................................................................................8

The difference in Director’s and Management’s responsibilities with Auditor’s responsibilities. .9

Treatment of Material Subsequent Events.......................................................................................9

Presence of Other Material information........................................................................................10

Follow-ups taken from Auditor.....................................................................................................11

Recommendations and Conclusion................................................................................................11

References......................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing of Coca-Cola Amatil in Australia 3

Introduction

Interacting with the key audit matters helps in attaining additional information for the

stakeholders of the company. With the communication of such information the user can easily

understand diverse information about the activities of the organization. The ASA 701 refers to

the responsibility of the auditors to express key audit matters in the auditor's report. Further,

ASA 315 states that identification and assessment of the misstatement of information with

considerate of the entity and the environment. This aspect deals with the accountability of the

auditor to analyse the risks related to the information and applying internal controls of the entity.

This accounting standard also talks about the identification of the material misstatement by

understanding the company and its environment. This deals with the understanding and

accountability of the material misstatement (Kulkarni 2017).

Further ASA 570 talks about the going concern concept of the company. It is considered the duty

of the auditors to understand various legalities related to the going concern of the company and

state its implications on the report of auditors. Lastly, ASA 200 deals with the independence of

the auditors to conduct the financial audit without facing any pressure. This standard evaluates

the scope, objective and responsibilities of the auditor along with the nature of audit executed by

them. Below mentioned report evaluates the financial reports of the company Coca-Cola

Amatil(Auditing and Assurance Standards Board 2015). It analyses the various aspects of

auditing of the company and recommendations given to them for improving effectiveness. More

details about the report are discussed below:

Introduction of Company

Coca-Cola Amatil (CCA) is one of the biggest producers of non-alcoholic drinks present in the

Asia Pacific region. The company of five major Coca-Cola bottlers present in some of the

biggest nations worldwide like, Samoa, New Zealand, Fiji, Australia, Papua New Guinea and

Indonesia. The company Coca-Cola is listed on ASX and its headquartered in New South Wales,

Australia. Some of the products served by Coca-Cola Amatil are iced tea, spring water, fruit

juices, energy drinks, flavoured milk, coffee etc. The company earned revenue of AS$5.12

Introduction

Interacting with the key audit matters helps in attaining additional information for the

stakeholders of the company. With the communication of such information the user can easily

understand diverse information about the activities of the organization. The ASA 701 refers to

the responsibility of the auditors to express key audit matters in the auditor's report. Further,

ASA 315 states that identification and assessment of the misstatement of information with

considerate of the entity and the environment. This aspect deals with the accountability of the

auditor to analyse the risks related to the information and applying internal controls of the entity.

This accounting standard also talks about the identification of the material misstatement by

understanding the company and its environment. This deals with the understanding and

accountability of the material misstatement (Kulkarni 2017).

Further ASA 570 talks about the going concern concept of the company. It is considered the duty

of the auditors to understand various legalities related to the going concern of the company and

state its implications on the report of auditors. Lastly, ASA 200 deals with the independence of

the auditors to conduct the financial audit without facing any pressure. This standard evaluates

the scope, objective and responsibilities of the auditor along with the nature of audit executed by

them. Below mentioned report evaluates the financial reports of the company Coca-Cola

Amatil(Auditing and Assurance Standards Board 2015). It analyses the various aspects of

auditing of the company and recommendations given to them for improving effectiveness. More

details about the report are discussed below:

Introduction of Company

Coca-Cola Amatil (CCA) is one of the biggest producers of non-alcoholic drinks present in the

Asia Pacific region. The company of five major Coca-Cola bottlers present in some of the

biggest nations worldwide like, Samoa, New Zealand, Fiji, Australia, Papua New Guinea and

Indonesia. The company Coca-Cola is listed on ASX and its headquartered in New South Wales,

Australia. Some of the products served by Coca-Cola Amatil are iced tea, spring water, fruit

juices, energy drinks, flavoured milk, coffee etc. The company earned revenue of AS$5.12

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing of Coca-Cola Amatil in Australia 4

billion in the previous year and has more than 15,000 employees in total (Coca-Cola Amatil

2015).

Compliance of Independence Requirements by Auditor

According to the Auditing and Assurance Standards Board (2015) ASA 200 is applied to all the

financial reports as per the Corporations Act 2001. This aspect deals with the accountability of

the auditor to develop true and fair reports according to the Australia Accounting Standards.

Audits help in increasing the confidence of the stakeholders in the financial documents and the

activities of the organization. It gives an understanding that according to the opinion of the

auditor, the financial reports have been formed using financial reporting frameworks. The

auditors of Coca-Cola Amatil (2017) have circulated the information with the directors about the

future goals and objectives of the company along with audit procedures, findings evaluating

deficiencies present in the internal control system.

The auditors of the company have followed the Divisions 3,4 and 5 of part 2M.4 that talks about

the independence of the auditors and Section 307C of the Corporations Act 2001 along with,

APES 110 Code of Ethics of Professional Accountants, Auditing Standard ASQC 1 that talks

about the quality control of the company that execute the audit and review report and analyse

other financial information. The auditors of the company have also followed Standard ASA 220

that talks about the management of quality while conducting an audit of company’s financial

reports and evaluation of other historical financial information as well. It should also be noted

that the auditors of the company have also expressed their view on remuneration report created

by the directors of the company according to the Section 300A of Corporations Act 2001. The

auditor has circulated his opinion in the audit reports of Coca-Cola Amatil. The information that

is independent of any personal opinion and is resourceful for the stakeholders of the company

(Coca-Cola Amatil 2017).

Nature of non-audit services

Ernst & Young (Australia) takes tax compliance related services for the company Coca-Cola

Amatil for which they received $0.045 Million for assurance services or is about to receive

$0.587 for tax-related services.

billion in the previous year and has more than 15,000 employees in total (Coca-Cola Amatil

2015).

Compliance of Independence Requirements by Auditor

According to the Auditing and Assurance Standards Board (2015) ASA 200 is applied to all the

financial reports as per the Corporations Act 2001. This aspect deals with the accountability of

the auditor to develop true and fair reports according to the Australia Accounting Standards.

Audits help in increasing the confidence of the stakeholders in the financial documents and the

activities of the organization. It gives an understanding that according to the opinion of the

auditor, the financial reports have been formed using financial reporting frameworks. The

auditors of Coca-Cola Amatil (2017) have circulated the information with the directors about the

future goals and objectives of the company along with audit procedures, findings evaluating

deficiencies present in the internal control system.

The auditors of the company have followed the Divisions 3,4 and 5 of part 2M.4 that talks about

the independence of the auditors and Section 307C of the Corporations Act 2001 along with,

APES 110 Code of Ethics of Professional Accountants, Auditing Standard ASQC 1 that talks

about the quality control of the company that execute the audit and review report and analyse

other financial information. The auditors of the company have also followed Standard ASA 220

that talks about the management of quality while conducting an audit of company’s financial

reports and evaluation of other historical financial information as well. It should also be noted

that the auditors of the company have also expressed their view on remuneration report created

by the directors of the company according to the Section 300A of Corporations Act 2001. The

auditor has circulated his opinion in the audit reports of Coca-Cola Amatil. The information that

is independent of any personal opinion and is resourceful for the stakeholders of the company

(Coca-Cola Amatil 2017).

Nature of non-audit services

Ernst & Young (Australia) takes tax compliance related services for the company Coca-Cola

Amatil for which they received $0.045 Million for assurance services or is about to receive

$0.587 for tax-related services.

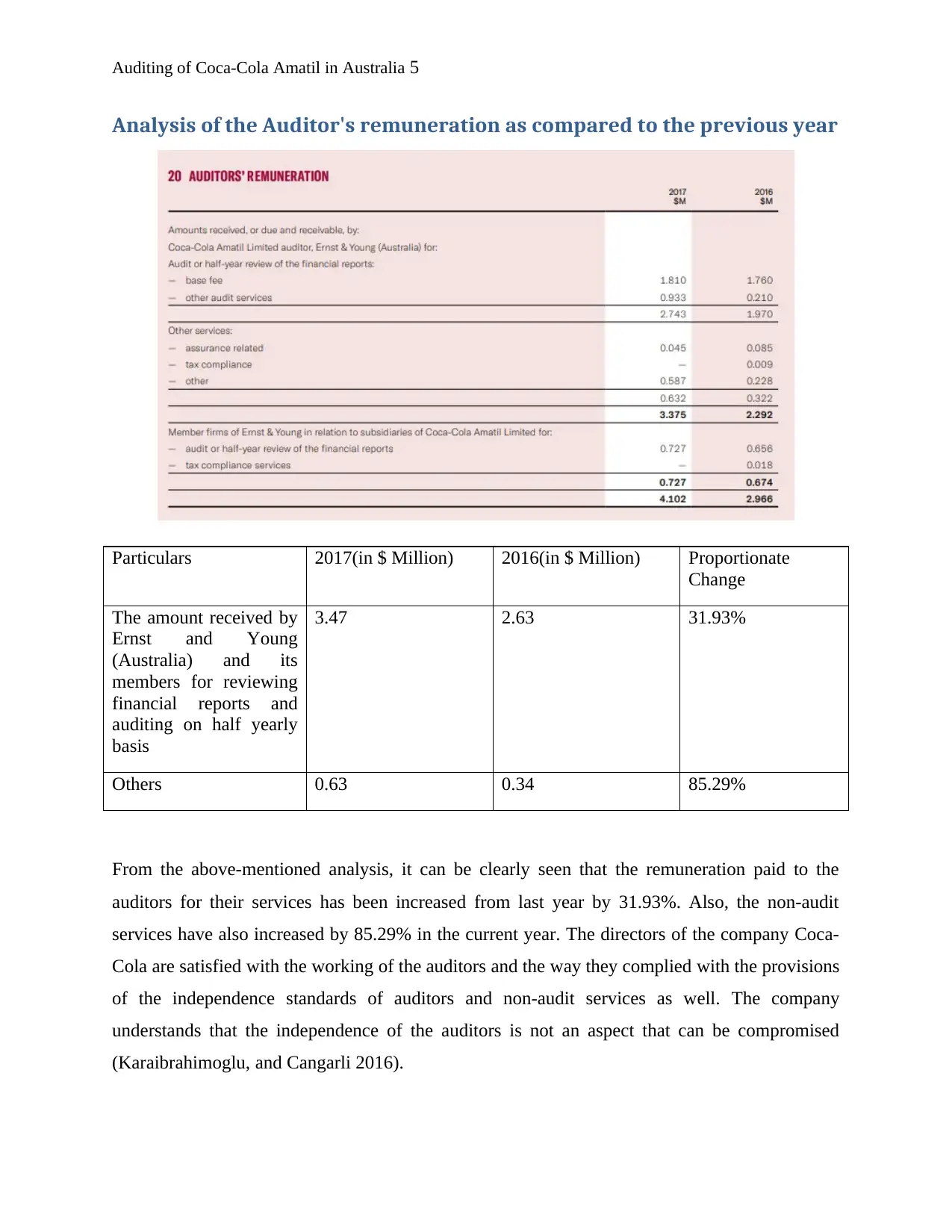

Auditing of Coca-Cola Amatil in Australia 5

Analysis of the Auditor's remuneration as compared to the previous year

Particulars 2017(in $ Million) 2016(in $ Million) Proportionate

Change

The amount received by

Ernst and Young

(Australia) and its

members for reviewing

financial reports and

auditing on half yearly

basis

3.47 2.63 31.93%

Others 0.63 0.34 85.29%

From the above-mentioned analysis, it can be clearly seen that the remuneration paid to the

auditors for their services has been increased from last year by 31.93%. Also, the non-audit

services have also increased by 85.29% in the current year. The directors of the company Coca-

Cola are satisfied with the working of the auditors and the way they complied with the provisions

of the independence standards of auditors and non-audit services as well. The company

understands that the independence of the auditors is not an aspect that can be compromised

(Karaibrahimoglu, and Cangarli 2016).

Analysis of the Auditor's remuneration as compared to the previous year

Particulars 2017(in $ Million) 2016(in $ Million) Proportionate

Change

The amount received by

Ernst and Young

(Australia) and its

members for reviewing

financial reports and

auditing on half yearly

basis

3.47 2.63 31.93%

Others 0.63 0.34 85.29%

From the above-mentioned analysis, it can be clearly seen that the remuneration paid to the

auditors for their services has been increased from last year by 31.93%. Also, the non-audit

services have also increased by 85.29% in the current year. The directors of the company Coca-

Cola are satisfied with the working of the auditors and the way they complied with the provisions

of the independence standards of auditors and non-audit services as well. The company

understands that the independence of the auditors is not an aspect that can be compromised

(Karaibrahimoglu, and Cangarli 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing of Coca-Cola Amatil in Australia 6

Audit Procedures for Key Audit Matters

Key audit matters are developed by the Auditing and Assurance Standards Board that is the most

significant part of the audit and is professional judgement of the auditors as well. ASA 701

determines that it is important for the auditor to include the key audit matter in the report of the

company so as to enhance the transparency in the company and the effectiveness of the audit as

well. The Key Audit Matters of the company Coca-Cola Amatil in the year 2017 was the

unlimited life of the intangible assets that was comprised with the investment agreement with the

bottlers amounting $929.3 million and goodwill to $147.5 million (Coca-Cola Amatil 2018).

Other assets of the company for that matter amounted $1093.1 Million, this amount also denoted

18% of the total resources of the group. According to the note 9 of financial statements, the

assessment of deficiency of the intangible assets and revenue generating units include the

estimation and supposition of future prospects along with cash flow of the company. The audit

procedures of the company include test of controls that relates to the execution of the procedures

and these procedures are directed towards evaluating the efficiency of design and implementing

internal controls as well. The auditors also determined the cash generating units that were used in

the impairment model. The auditors of the company also looked at the appropriateness of assets

and liabilities that were also involved in carrying value of CGU. They also tested the accuracy of

cash flow model (Stikeleather 2016).

The second key audit matter involves the accounting for the rebate and promotional expenses. In

such instances, the revenue for the sales is analysed with the rewards and risks of the ownership

that is being passed on to the consumers and the cash is measured. The understanding and

acceptance of the rebate and allowances include accrual at the end of the year that involves

prudent judgement and estimations as well. The applied audit procedures include the comparison

of data from different sources so as to determine the correctness of the information that is

reported. For the purpose of applying the analytical procedures, the auditors have selected a

performance of rebate and promotional allowances that includes the level of expected claims by

evaluating the past records, trends of claims and evaluating the adequateness of accruals

(Deloitte 2017).

Audit Procedures for Key Audit Matters

Key audit matters are developed by the Auditing and Assurance Standards Board that is the most

significant part of the audit and is professional judgement of the auditors as well. ASA 701

determines that it is important for the auditor to include the key audit matter in the report of the

company so as to enhance the transparency in the company and the effectiveness of the audit as

well. The Key Audit Matters of the company Coca-Cola Amatil in the year 2017 was the

unlimited life of the intangible assets that was comprised with the investment agreement with the

bottlers amounting $929.3 million and goodwill to $147.5 million (Coca-Cola Amatil 2018).

Other assets of the company for that matter amounted $1093.1 Million, this amount also denoted

18% of the total resources of the group. According to the note 9 of financial statements, the

assessment of deficiency of the intangible assets and revenue generating units include the

estimation and supposition of future prospects along with cash flow of the company. The audit

procedures of the company include test of controls that relates to the execution of the procedures

and these procedures are directed towards evaluating the efficiency of design and implementing

internal controls as well. The auditors also determined the cash generating units that were used in

the impairment model. The auditors of the company also looked at the appropriateness of assets

and liabilities that were also involved in carrying value of CGU. They also tested the accuracy of

cash flow model (Stikeleather 2016).

The second key audit matter involves the accounting for the rebate and promotional expenses. In

such instances, the revenue for the sales is analysed with the rewards and risks of the ownership

that is being passed on to the consumers and the cash is measured. The understanding and

acceptance of the rebate and allowances include accrual at the end of the year that involves

prudent judgement and estimations as well. The applied audit procedures include the comparison

of data from different sources so as to determine the correctness of the information that is

reported. For the purpose of applying the analytical procedures, the auditors have selected a

performance of rebate and promotional allowances that includes the level of expected claims by

evaluating the past records, trends of claims and evaluating the adequateness of accruals

(Deloitte 2017).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing of Coca-Cola Amatil in Australia 7

Structure, Responsibilities and Functions of Audit Committee

According to the Coca-Cola Amatil (2015), the company has an audit and risk committee that

supervises the risk management and internal control with thoroughly overseeing the financial

risks. It is important for the financial reporting to maintain balance, transparency along with

integrity with the organization and its policies. The financial reporting includes two aspects that

are the internal and external audit. The role of internal audit is to evaluate the efficiency of the

internal control and risk assessment process. Further external audit aims to make sure that the

process of the independent audit is followed along with recommendations to perform

independent audit. The function of the audit is to supervise the compliance of laws, policies and

procedures of the company(Auditing and Assurance Standards Board 2013).

It is considered as the responsibility of the auditor to exercise proper diligence in evaluating and

analysing the financial statements of Coca-Cola Amatil and to provide recommendations for the

favourableness of the accounting policies and adequately maintaining procedures as well. It is

the duty of the auditor to look after the risk management internal control system of the company.

The auditor of company oversee the risk management with internal control system of the

company and oversee various laws, standards and policies of the company. The association of

the ARC consists of three Non-executive Directors, who are independent directors. These

include independent Chairman that is not chairman of the Board and the Chairman of the

Sustainability Committee as well. The Board appoints all the members including the Chairman

(Auditing and Assurance Standards Board 2015).

Audit Opinion expressed

The evaluators communicated their view as an unqualified opinion. It is an expression as

communicated by the auditor reviewers with respect to the reasonableness and fitting portrayal

of budgetary proclamations. They have likewise expressed that the organization has agreed to the

accounting standards. They have evaluated the budgetary reports of the organization and its

backups including its consolidated balance sheet as at 31st December 2017 alongside an

announcement of changes in value and money streams for the year finishing. In this way, as they

would like to think, the organization has arranged its money related proclamations as per the

Companies Act 2001 (Eccles, and Serafeim 2015). The books of records uncover a genuine and

Structure, Responsibilities and Functions of Audit Committee

According to the Coca-Cola Amatil (2015), the company has an audit and risk committee that

supervises the risk management and internal control with thoroughly overseeing the financial

risks. It is important for the financial reporting to maintain balance, transparency along with

integrity with the organization and its policies. The financial reporting includes two aspects that

are the internal and external audit. The role of internal audit is to evaluate the efficiency of the

internal control and risk assessment process. Further external audit aims to make sure that the

process of the independent audit is followed along with recommendations to perform

independent audit. The function of the audit is to supervise the compliance of laws, policies and

procedures of the company(Auditing and Assurance Standards Board 2013).

It is considered as the responsibility of the auditor to exercise proper diligence in evaluating and

analysing the financial statements of Coca-Cola Amatil and to provide recommendations for the

favourableness of the accounting policies and adequately maintaining procedures as well. It is

the duty of the auditor to look after the risk management internal control system of the company.

The auditor of company oversee the risk management with internal control system of the

company and oversee various laws, standards and policies of the company. The association of

the ARC consists of three Non-executive Directors, who are independent directors. These

include independent Chairman that is not chairman of the Board and the Chairman of the

Sustainability Committee as well. The Board appoints all the members including the Chairman

(Auditing and Assurance Standards Board 2015).

Audit Opinion expressed

The evaluators communicated their view as an unqualified opinion. It is an expression as

communicated by the auditor reviewers with respect to the reasonableness and fitting portrayal

of budgetary proclamations. They have likewise expressed that the organization has agreed to the

accounting standards. They have evaluated the budgetary reports of the organization and its

backups including its consolidated balance sheet as at 31st December 2017 alongside an

announcement of changes in value and money streams for the year finishing. In this way, as they

would like to think, the organization has arranged its money related proclamations as per the

Companies Act 2001 (Eccles, and Serafeim 2015). The books of records uncover a genuine and

Auditing of Coca-Cola Amatil in Australia 8

reasonable viewpoint of the fiscal position and effective activities of the organization as of 31st

December 2017. It has additionally confirmed to the Australian Accounting Standards and

Corporate Regulations 2001. Adequate review confirms has been gotten which has given a

premise to the conclusion (Antao, et. al., 2016).

The difference in Director’s and Management’s responsibilities with

Auditor’s responsibilities

According to APES 110 Code of Ethics for Proficient Professional Accountants, it has been

expressed that the inspectors ought to embrace the rule of honesty that forces the commitment, to

be completely forthright, and clear in all the expert connections. It additionally suggests that they

ought to be reasonable and honest alongside embracing objectivity in the entirety of their

dealings. They likewise have the duty to embrace the standards of the expert witness and due

care, secrecy and expert conduct while managing the expert commitments (Albu, Albu, and

Alexander 2014).

The obligations of directors and administrators relate to responsibility and announcing. The

administration has the duty to stick to the Corporate Administration Standards and Proposals of

ASX. Its fundamental reason for existing is to speak to and serve the premiums of speculators by

guaranteeing that suitable human and monetary assets are set to help the organization in

achieving its goals (Florou, Kosi, and Pope 2017).

Treatment of Material Subsequent Events

According to ASA 570, the inspectors are responsible for expressing the different parts of a

going concern and ought to uncover its suggestions in the evaluator's report. ASA 315 states that

the evaluators ought to recognize and survey the danger of material misquotes by fathoming the

earth of an element (Backof, Bamber, and Carpenter 2013).

The financial risk management of the organization is executed by the treasury arrangement

which is endorsed by the board. The organization is stood up to by different kinds of risks like

commodity prices, foreign currency and interest rate. The other money-related dangers identified

with remote cash exchange, credit and liquidity (Libby 2017).

reasonable viewpoint of the fiscal position and effective activities of the organization as of 31st

December 2017. It has additionally confirmed to the Australian Accounting Standards and

Corporate Regulations 2001. Adequate review confirms has been gotten which has given a

premise to the conclusion (Antao, et. al., 2016).

The difference in Director’s and Management’s responsibilities with

Auditor’s responsibilities

According to APES 110 Code of Ethics for Proficient Professional Accountants, it has been

expressed that the inspectors ought to embrace the rule of honesty that forces the commitment, to

be completely forthright, and clear in all the expert connections. It additionally suggests that they

ought to be reasonable and honest alongside embracing objectivity in the entirety of their

dealings. They likewise have the duty to embrace the standards of the expert witness and due

care, secrecy and expert conduct while managing the expert commitments (Albu, Albu, and

Alexander 2014).

The obligations of directors and administrators relate to responsibility and announcing. The

administration has the duty to stick to the Corporate Administration Standards and Proposals of

ASX. Its fundamental reason for existing is to speak to and serve the premiums of speculators by

guaranteeing that suitable human and monetary assets are set to help the organization in

achieving its goals (Florou, Kosi, and Pope 2017).

Treatment of Material Subsequent Events

According to ASA 570, the inspectors are responsible for expressing the different parts of a

going concern and ought to uncover its suggestions in the evaluator's report. ASA 315 states that

the evaluators ought to recognize and survey the danger of material misquotes by fathoming the

earth of an element (Backof, Bamber, and Carpenter 2013).

The financial risk management of the organization is executed by the treasury arrangement

which is endorsed by the board. The organization is stood up to by different kinds of risks like

commodity prices, foreign currency and interest rate. The other money-related dangers identified

with remote cash exchange, credit and liquidity (Libby 2017).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Auditing of Coca-Cola Amatil in Australia 9

Foreign currency risks relate to the changes in the money streams because of advances in the

rates of remote currency. The risk management strategy enables the organization to support the

exchanges identified with the gauge cost of merchandise sold later on the capital consumptions

are supported upon the acknowledgement of the company's responsibility. The interest rate risks

related to presenting the organization to loan fee chance related with enthusiasm bearing

monetary resources, for example, money, credits, term stores and bank overdrafts (Sharma, and

Iselin 2012). The strategy received for its alleviation is reasonable administration of these

exposures. The normal development of the supporting portfolio is somewhere in the range of one

and five years. It goes into financing cost swap and choice and cross-money swap assertions for

dealing with these dangers. Product costs risks are the risk that emerges from instability in the

costs of items identifying with crude materials used in the business. The organization has gone

into choices, swaps and prospects contracts keeping in mind the end goal to fence the commodity

price risk at acquiring lower costs and greater solidness in the results of commodity costs

(Louwers, et. al., 2015).

With a specific end goal to relieve the liquidity chance, the organization has embraced the

liquidity arrangement which goes for the base level of offices in connection to net obligation. To

deal with the translation risks it relates to changing over the financial statements of the foreign

exchanges of the organization. The instability in the foreign trade rates can affect the net

resources, benefit and salary of the gathering. The organization does not fence the interpretation

hazard and when considered vital, it is supported intermittently. The credit risks of the

organization are relieved through receiving an arrangement for building up credit limits for the

substances it is managing and may require insurance securities for the same (Schmidt 2012).

Presence of Other Material information

The organization can't uncover the material data in regards to its intent to merge one of its units

or get some other organization. In the event that it does as such, it would result in spillage of the

price-sensitive data and insider trading. Moreover, it doesn't uncover the purpose of giving a

specific sum as compensation to the key administrative faculty. It likewise does not uncover the

inalienable hazard gone up against by the organization.

Foreign currency risks relate to the changes in the money streams because of advances in the

rates of remote currency. The risk management strategy enables the organization to support the

exchanges identified with the gauge cost of merchandise sold later on the capital consumptions

are supported upon the acknowledgement of the company's responsibility. The interest rate risks

related to presenting the organization to loan fee chance related with enthusiasm bearing

monetary resources, for example, money, credits, term stores and bank overdrafts (Sharma, and

Iselin 2012). The strategy received for its alleviation is reasonable administration of these

exposures. The normal development of the supporting portfolio is somewhere in the range of one

and five years. It goes into financing cost swap and choice and cross-money swap assertions for

dealing with these dangers. Product costs risks are the risk that emerges from instability in the

costs of items identifying with crude materials used in the business. The organization has gone

into choices, swaps and prospects contracts keeping in mind the end goal to fence the commodity

price risk at acquiring lower costs and greater solidness in the results of commodity costs

(Louwers, et. al., 2015).

With a specific end goal to relieve the liquidity chance, the organization has embraced the

liquidity arrangement which goes for the base level of offices in connection to net obligation. To

deal with the translation risks it relates to changing over the financial statements of the foreign

exchanges of the organization. The instability in the foreign trade rates can affect the net

resources, benefit and salary of the gathering. The organization does not fence the interpretation

hazard and when considered vital, it is supported intermittently. The credit risks of the

organization are relieved through receiving an arrangement for building up credit limits for the

substances it is managing and may require insurance securities for the same (Schmidt 2012).

Presence of Other Material information

The organization can't uncover the material data in regards to its intent to merge one of its units

or get some other organization. In the event that it does as such, it would result in spillage of the

price-sensitive data and insider trading. Moreover, it doesn't uncover the purpose of giving a

specific sum as compensation to the key administrative faculty. It likewise does not uncover the

inalienable hazard gone up against by the organization.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Auditing of Coca-Cola Amatil in Australia 10

It is the hazard presented by a blunder or exclusion in the money related proclamations as a

result of the components other than the disappointments to control them. It speaks to the situation

of the most pessimistic scenario as every one of the controls has been flopped in such manner

(Goh, Krishnan, and Li 2013).

Follow-ups taken from Auditor

The subsequent inquiries to be asked by the inspectors at the Annual General Meeting of the

organization would be what is the premise behind shaping an opinion in regards to the genuine

and reasonable perspective of the records of the organization? Another inquiry can be what level

of attestations they have expected while looking at the books of records of the organization?

For this, the inspectors ought to get the Management Representative letter which is to be marked

by the senior administration and signifies the precision of the monetary proclamations which the

organization has submitted to the evaluators for breaking down.

Recommendations and Conclusion

Thus, in the limelight of above mentioned events, the fact should be noted that with an aim to

find out the adequacy of material data by the auditors, the stakeholders ought to look after the

effectiveness of ASA 101 Presentation of Financial Statements of the organization. The money

related reports ought to give the data about the benefits, risk, value, salary and costs, changes in

value and money streams of the organization. The examiners should survey the money related

proclamations of the organization and its consistency with the Inspecting and Bookkeeping

Models and Partnerships Act 2001.

It is the hazard presented by a blunder or exclusion in the money related proclamations as a

result of the components other than the disappointments to control them. It speaks to the situation

of the most pessimistic scenario as every one of the controls has been flopped in such manner

(Goh, Krishnan, and Li 2013).

Follow-ups taken from Auditor

The subsequent inquiries to be asked by the inspectors at the Annual General Meeting of the

organization would be what is the premise behind shaping an opinion in regards to the genuine

and reasonable perspective of the records of the organization? Another inquiry can be what level

of attestations they have expected while looking at the books of records of the organization?

For this, the inspectors ought to get the Management Representative letter which is to be marked

by the senior administration and signifies the precision of the monetary proclamations which the

organization has submitted to the evaluators for breaking down.

Recommendations and Conclusion

Thus, in the limelight of above mentioned events, the fact should be noted that with an aim to

find out the adequacy of material data by the auditors, the stakeholders ought to look after the

effectiveness of ASA 101 Presentation of Financial Statements of the organization. The money

related reports ought to give the data about the benefits, risk, value, salary and costs, changes in

value and money streams of the organization. The examiners should survey the money related

proclamations of the organization and its consistency with the Inspecting and Bookkeeping

Models and Partnerships Act 2001.

Auditing of Coca-Cola Amatil in Australia 11

References

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards meet the local

context—Insights from an emerging economy. Critical Perspectives on Accounting, 25(6),

pp.489-510.

Antao, L., Insolia, G.E. and Kolls, H.B., Coca-Cola Co, 2016. Systems and methods for

providing electronic transaction auditing and accountability. U.S. Patent 9,460,440.

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 200 Overall

Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with

Australian Auditing Standards [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_200_Compiled_2015.pdf [Accessed

16th September , 2018].

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 701 Communicating

Key Audit Matters in the Independent Auditor’s Report [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 16th

September , 2018].

Auditing and Assurance Standards Board (2013) Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment[online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA

_315.pdf [Accessed 16th September , 2018].

Backof, A.G., Bamber, E.M. and Carpenter, T.D., 2013. More precise versus less precise

accounting standards: The effect of auditor judgment frameworks in constraining aggressive

reporting. University of Georgia.

Coca Cola Amatil (2015) Audit and Risk Committee Charter[online] Available from:

https://www.ccamatil.com/-/media/cca/corporate/files/our-company/corporate-governance/cg-

01-audit--risk-committee-charter8-december-2015.ashx?la=en [Accessed 16th September , 2018].

References

Albu, C.N., Albu, N. and Alexander, D., 2014. When global accounting standards meet the local

context—Insights from an emerging economy. Critical Perspectives on Accounting, 25(6),

pp.489-510.

Antao, L., Insolia, G.E. and Kolls, H.B., Coca-Cola Co, 2016. Systems and methods for

providing electronic transaction auditing and accountability. U.S. Patent 9,460,440.

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 200 Overall

Objectives of the Independent Auditor and the Conduct of an Audit in Accordance with

Australian Auditing Standards [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_200_Compiled_2015.pdf [Accessed

16th September , 2018].

Auditing and Assurance Standards Board (2015) Auditing Standard ASA 701 Communicating

Key Audit Matters in the Independent Auditor’s Report [online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/ASA_701_2015.pdf [Accessed 16th

September , 2018].

Auditing and Assurance Standards Board (2013) Auditing Standard ASA 315 Identifying and

Assessing the Risks of Material Misstatement through Understanding the Entity and Its

Environment[online] Available from:

https://www.auasb.gov.au/admin/file/content102/c3/Nov13_Compiled_Auditing_Standard_ASA

_315.pdf [Accessed 16th September , 2018].

Backof, A.G., Bamber, E.M. and Carpenter, T.D., 2013. More precise versus less precise

accounting standards: The effect of auditor judgment frameworks in constraining aggressive

reporting. University of Georgia.

Coca Cola Amatil (2015) Audit and Risk Committee Charter[online] Available from:

https://www.ccamatil.com/-/media/cca/corporate/files/our-company/corporate-governance/cg-

01-audit--risk-committee-charter8-december-2015.ashx?la=en [Accessed 16th September , 2018].

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.