Accounting Standards: Coca-Cola Amatil's Financial Reporting Analysis

VerifiedAdded on 2023/06/12

|11

|2238

|447

Report

AI Summary

This report analyzes Coca-Cola Amatil's financial reporting practices to determine the extent of its compliance with the conceptual accounting framework set by the IASB. It examines whether the company's financial statements meet the general objectives of financial reporting and effectively cater to the needs of its target audience, including investors and creditors. The report further investigates the criteria used by Coca-Cola Amatil for recognizing financial statement elements, as well as how the company adheres to the fundamental and enhancing qualitative characteristics of the conceptual accounting framework, such as relevance, faithful presentation, comparability, verifiability, timeliness, and understandability. The analysis is based on Coca-Cola Amatil's 2016 annual report, concluding that the company effectively complies with the IASB's framework in its financial reporting.

Contemporary Issues in Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Executive Summary

The report is undertaken to analyze whether the business corporations listed on ASX are

implementing the conceptual accounting framework for developing their financial reports. Fir the

purpose, the financial reporting process of Coca-Cola Amatil, listed on ASX, is analyzed for

examining the compliance of its different sections with the accounting framework of IASB. It

has been depicted that the company has applied the standard principles of accounting framework

during its overall financial reporting process.

The report is undertaken to analyze whether the business corporations listed on ASX are

implementing the conceptual accounting framework for developing their financial reports. Fir the

purpose, the financial reporting process of Coca-Cola Amatil, listed on ASX, is analyzed for

examining the compliance of its different sections with the accounting framework of IASB. It

has been depicted that the company has applied the standard principles of accounting framework

during its overall financial reporting process.

Contents

Introduction......................................................................................................................................4

General Objective of Financial Reporting Met by Coca-Cola Amatil............................................4

Analysis of the Effectiveness of Financial Reports of Coca-Cola Amatil by Target Audience......5

Criteria of recognizing the Financial Statement Elements Used by Coca-Cola Amatil..................5

Fundamental Qualitative Characteristic of Conceptual Accounting Framework Met in Financial

Report of Coca-Cola Amatil............................................................................................................6

Enhancing Qualitative Characteristic of Conceptual Accounting Framework Met in Financial

Report of Coca-Cola Amatil............................................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

Introduction......................................................................................................................................4

General Objective of Financial Reporting Met by Coca-Cola Amatil............................................4

Analysis of the Effectiveness of Financial Reports of Coca-Cola Amatil by Target Audience......5

Criteria of recognizing the Financial Statement Elements Used by Coca-Cola Amatil..................5

Fundamental Qualitative Characteristic of Conceptual Accounting Framework Met in Financial

Report of Coca-Cola Amatil............................................................................................................6

Enhancing Qualitative Characteristic of Conceptual Accounting Framework Met in Financial

Report of Coca-Cola Amatil............................................................................................................7

Conclusion.......................................................................................................................................9

References......................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Introduction

Australian Accounting Standards Board (AASB) is currently placing large emphasis on

implementation of the conceptual accounting framework in the financial reporting process of

business corporations operating within Australia. This is done to ensure that financial reports are

developed as per the needs and requirements of the end-users by providing them all the

necessary information for decision-making. IASB (International Accounting Standards Board)

has developed the standard framework of accounting for providing a clear direction to the

business corporations worldwide regarding the nature of developing financial reports. The

adoption of this conceptual accounting framework will also benefit the business corporations of

Australia by increasing their global competitiveness through achieving the trust and confidence

of investors worldwide (Van der Meulen, Gaeremynck and Willekens, 2007). In this context, the

report provides an analysis of the extent of adoption of conceptual accounting framework by

selected business corporations listed on ASX, that is, one of the largest bottlers of non-alcoholic

ready to drink beverages in the Asia-Pacific region.

General Objective of Financial Reporting Met by Coca-Cola Amatil

The conceptual framework of accounting has described the major objective

behind the development of financial reports by business entities to support the decision-making

process of end-users. The end-users of financial information are present and future investors that

need to gain an analysis of the overall performance of a business entity through examining its

present financial growth and success. The general purpose financial statements developed by a

business corporation provide all the required information to the end-users about its financial

condition that can prove to be useful in decision-making (Conceptual Framework, 2017). Coca-

Cola Amatil has met the objective of developing financial reports through development and

presentation of its financial statements. The financial report of the company has disclosed the

consolidated financial statements that are, income sheet, balance sheet, statement of profit and

loss, statement of change sin equity and cash flow statement. All these general purpose financial

statements are developed in accordance with the AASB standards and Corporations Act 2001 to

comply with the standard principle of conceptual accounting framework (Coca-Cola Amatil:

Annual Report, 2016). The investors can review the general purpose financial statements for

Australian Accounting Standards Board (AASB) is currently placing large emphasis on

implementation of the conceptual accounting framework in the financial reporting process of

business corporations operating within Australia. This is done to ensure that financial reports are

developed as per the needs and requirements of the end-users by providing them all the

necessary information for decision-making. IASB (International Accounting Standards Board)

has developed the standard framework of accounting for providing a clear direction to the

business corporations worldwide regarding the nature of developing financial reports. The

adoption of this conceptual accounting framework will also benefit the business corporations of

Australia by increasing their global competitiveness through achieving the trust and confidence

of investors worldwide (Van der Meulen, Gaeremynck and Willekens, 2007). In this context, the

report provides an analysis of the extent of adoption of conceptual accounting framework by

selected business corporations listed on ASX, that is, one of the largest bottlers of non-alcoholic

ready to drink beverages in the Asia-Pacific region.

General Objective of Financial Reporting Met by Coca-Cola Amatil

The conceptual framework of accounting has described the major objective

behind the development of financial reports by business entities to support the decision-making

process of end-users. The end-users of financial information are present and future investors that

need to gain an analysis of the overall performance of a business entity through examining its

present financial growth and success. The general purpose financial statements developed by a

business corporation provide all the required information to the end-users about its financial

condition that can prove to be useful in decision-making (Conceptual Framework, 2017). Coca-

Cola Amatil has met the objective of developing financial reports through development and

presentation of its financial statements. The financial report of the company has disclosed the

consolidated financial statements that are, income sheet, balance sheet, statement of profit and

loss, statement of change sin equity and cash flow statement. All these general purpose financial

statements are developed in accordance with the AASB standards and Corporations Act 2001 to

comply with the standard principle of conceptual accounting framework (Coca-Cola Amatil:

Annual Report, 2016). The investors can review the general purpose financial statements for

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

analyzing the profitability, liquidity, efficiency and other financial metrics of the company before

making the investment decisions (Rezaee, 2003).

Analysis of the Effectiveness of Financial Reports of Coca-Cola Amatil by

Target Audience

Coca-Cola Amatil financial reports is developed and presented on yearly basis in its

annul report. The company integrates the financial performance of all its subsidiaries during the

development of its consolidated financial statements as per the principle of consolidation (Tarca,

2004). This facilitates the target audience, that are, present and future investors, analysts,

creditors and lenders to gain an overview of the performance of the company as a Group and

analyze its potential worth (Soderstrom and Sun, 2007). There is a separate section of the

financial report in the annual review provided by the company to the target audience. All the

consolidated financial statements are presented clearly and separately in the financial report so

that target audience can develop an overview of the integrated performance of the company and

its various subsidiaries as a single economic entity. The target audiences can easily and quickly

develop an analysis of the key financial performance indicters that helps them to take decisions

within a shirt-period of time. The financial reports are developed as per the standard accounting

principles and rules to ensure that it is reliable and capable of supporting the decisions of the

target audience (Coca-Cola Amatil: Annual Report, 2016). There is synchronized flow of

information through the overall financial report so that target audience can easily extract the

information they need and therefore fulfilling their varying requirements (Psaros and Trotman,

2004).

Criteria of recognizing the Financial Statement Elements Used by Coca-

Cola Amatil

The conceptual framework of accounting has directed all the business entities to

recognize and measure the value of elements of financial statements only when there is

expectation that they will provide economic benefit to them in future context. The recognition

and measurement criteria used by business entities during development of financial reports need

to be described adequately (McDaniel, Martin and Maines, 2002). The notes to financial

statements section of Coca-Cola Amatil has adequately disclosed all the key information about

making the investment decisions (Rezaee, 2003).

Analysis of the Effectiveness of Financial Reports of Coca-Cola Amatil by

Target Audience

Coca-Cola Amatil financial reports is developed and presented on yearly basis in its

annul report. The company integrates the financial performance of all its subsidiaries during the

development of its consolidated financial statements as per the principle of consolidation (Tarca,

2004). This facilitates the target audience, that are, present and future investors, analysts,

creditors and lenders to gain an overview of the performance of the company as a Group and

analyze its potential worth (Soderstrom and Sun, 2007). There is a separate section of the

financial report in the annual review provided by the company to the target audience. All the

consolidated financial statements are presented clearly and separately in the financial report so

that target audience can develop an overview of the integrated performance of the company and

its various subsidiaries as a single economic entity. The target audiences can easily and quickly

develop an analysis of the key financial performance indicters that helps them to take decisions

within a shirt-period of time. The financial reports are developed as per the standard accounting

principles and rules to ensure that it is reliable and capable of supporting the decisions of the

target audience (Coca-Cola Amatil: Annual Report, 2016). There is synchronized flow of

information through the overall financial report so that target audience can easily extract the

information they need and therefore fulfilling their varying requirements (Psaros and Trotman,

2004).

Criteria of recognizing the Financial Statement Elements Used by Coca-

Cola Amatil

The conceptual framework of accounting has directed all the business entities to

recognize and measure the value of elements of financial statements only when there is

expectation that they will provide economic benefit to them in future context. The recognition

and measurement criteria used by business entities during development of financial reports need

to be described adequately (McDaniel, Martin and Maines, 2002). The notes to financial

statements section of Coca-Cola Amatil has adequately disclosed all the key information about

the criteria used for recognizing and measuring the value of financial elements. The revenue is

recognized and measured by the company at the fair value on meeting the following criteria, sale

of products, rental income, and services provided and interest income received. There are

different recognition and measurement criteria used for assessing the value of expenses that are,

employee-related costs, finance costs and operating leases. The value of trade and receivables are

recognized by taking the due amount in consideration and also making an allowance for doubtful

amounts and recognize it in the income statements. Property, plant and equipment are recognized

at cost through deduction of the depreciation and impairment occurred. Similarly, the recognition

criteria used for identifying and ensuring the value of income tax, tangible assets and intangible

assets, inventory, impairment testing and others are clearly disclosed by the company in the note

section of the financial report (Coca-Cola Amatil: Annual Report, 2016).

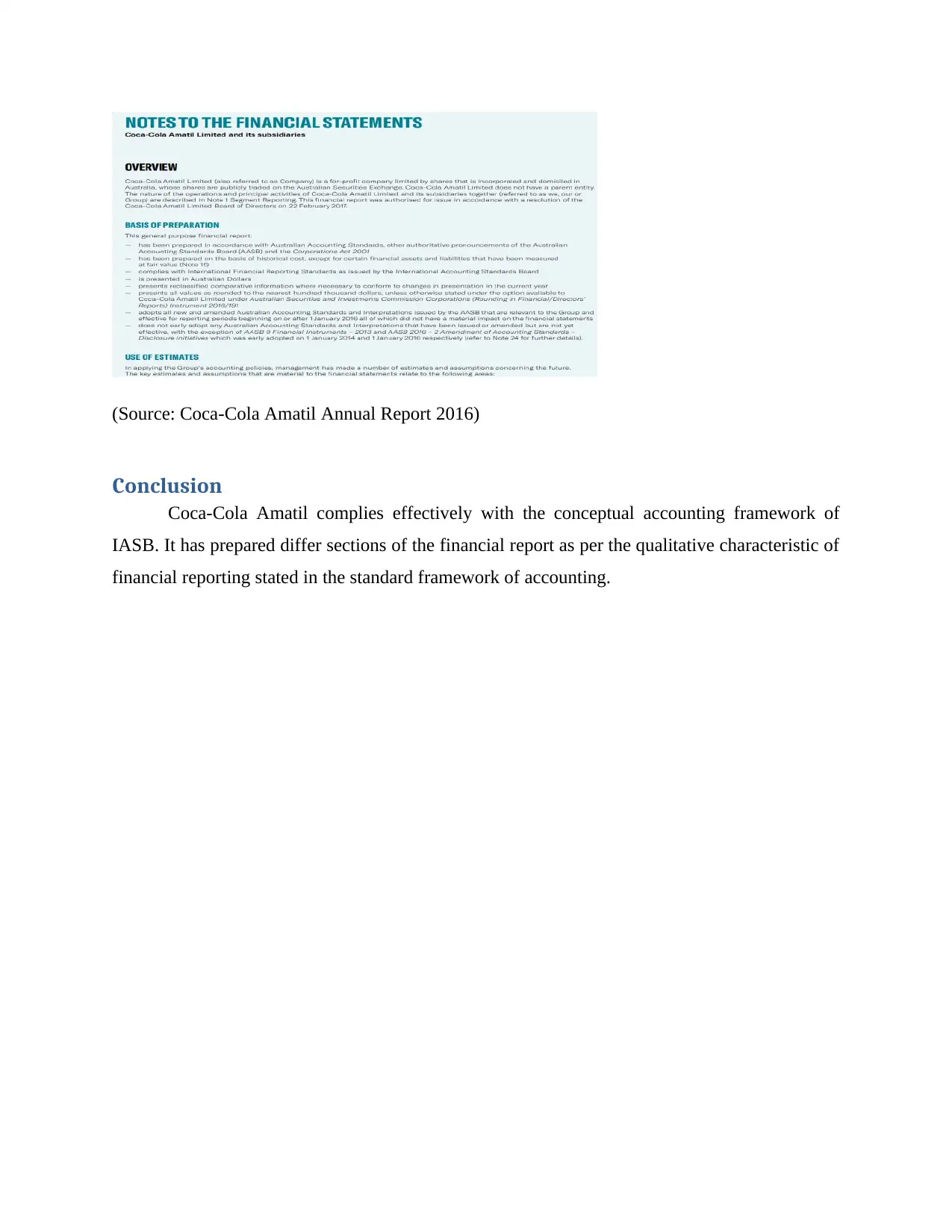

Fundamental Qualitative Characteristic of Conceptual Accounting

Framework Met in Financial Report of Coca-Cola Amatil

The major fundamental qualitative characteristic of financial report as provided in the

conceptual accounting framework is relevancy and faithful presentation. The financial

information can be regarded to be relevant if it has both predictive and confirmatory values.

Therefore, the financial information should provide a confirmed value and also estimated value

so that it is reliable in the mind of the target users (Gore and Zimmerman, 2007). The financial

report of Coca-Cola Amatil has provided both the confirmed and predictive value of different

elements of financial statements. The different general purpose financial statements has provided

the confirmed value of financial elements and also provided the predictive value based on the

accounting estimates and assumptions. The key assumptions used in estimating the future value

of certain financial elements is also disclosed in the financial report. The company has stated in

its financial report that management has used some key estimates and assumptions for predicting

the future value of some financial elements (Maines and Wahlen, 2006).

The key assumptions used are estimation in the useful lives of property, plant and

equipment and intangible assets. The assumptions are also applied in protecting the value of

impairment testing, income tax and promotional allowances. The other fundamental qualitative

characteristic of conceptual accounting framework is faithful presentation of financial

information. This means that financial information should be neutral, error-free and also

recognized and measured by the company at the fair value on meeting the following criteria, sale

of products, rental income, and services provided and interest income received. There are

different recognition and measurement criteria used for assessing the value of expenses that are,

employee-related costs, finance costs and operating leases. The value of trade and receivables are

recognized by taking the due amount in consideration and also making an allowance for doubtful

amounts and recognize it in the income statements. Property, plant and equipment are recognized

at cost through deduction of the depreciation and impairment occurred. Similarly, the recognition

criteria used for identifying and ensuring the value of income tax, tangible assets and intangible

assets, inventory, impairment testing and others are clearly disclosed by the company in the note

section of the financial report (Coca-Cola Amatil: Annual Report, 2016).

Fundamental Qualitative Characteristic of Conceptual Accounting

Framework Met in Financial Report of Coca-Cola Amatil

The major fundamental qualitative characteristic of financial report as provided in the

conceptual accounting framework is relevancy and faithful presentation. The financial

information can be regarded to be relevant if it has both predictive and confirmatory values.

Therefore, the financial information should provide a confirmed value and also estimated value

so that it is reliable in the mind of the target users (Gore and Zimmerman, 2007). The financial

report of Coca-Cola Amatil has provided both the confirmed and predictive value of different

elements of financial statements. The different general purpose financial statements has provided

the confirmed value of financial elements and also provided the predictive value based on the

accounting estimates and assumptions. The key assumptions used in estimating the future value

of certain financial elements is also disclosed in the financial report. The company has stated in

its financial report that management has used some key estimates and assumptions for predicting

the future value of some financial elements (Maines and Wahlen, 2006).

The key assumptions used are estimation in the useful lives of property, plant and

equipment and intangible assets. The assumptions are also applied in protecting the value of

impairment testing, income tax and promotional allowances. The other fundamental qualitative

characteristic of conceptual accounting framework is faithful presentation of financial

information. This means that financial information should be neutral, error-free and also

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

complete in all respects (Mazhambe, 2014). The financial report of Coca-Cola Amatil in order to

ensure that all the key financial performance indicators are faithfully presented has carried out

auditing of its general purpose financial statements. The auditing of financial reporting process is

carried out with the aim of reviewing the financial statements so that it can be assured that they

are free from any materialistic error. The independence declaration statement of auditor in the

financial report ensures that the financial elements values are free from any material error and as

such faithfully presented to the end-users (Coca-Cola Amatil: Annual Report, 2016).

(Source: Coca-Cola Amatil Annual Report 2016)

Enhancing Qualitative Characteristic of Conceptual Accounting

Framework Met in Financial Report of Coca-Cola Amatil

The conceptual framework of accounting has also stated some enhancing qualitative

characteristics for assisting the accountants in development of financial reports. These

characteristics are comparability, verifiability, timelines and understandability (Conceptual

Framework, 2017). The financial information disclosed should be comparable with that of the

previous year so that investors can asses whether there has been improvement in the financial

ensure that all the key financial performance indicators are faithfully presented has carried out

auditing of its general purpose financial statements. The auditing of financial reporting process is

carried out with the aim of reviewing the financial statements so that it can be assured that they

are free from any materialistic error. The independence declaration statement of auditor in the

financial report ensures that the financial elements values are free from any material error and as

such faithfully presented to the end-users (Coca-Cola Amatil: Annual Report, 2016).

(Source: Coca-Cola Amatil Annual Report 2016)

Enhancing Qualitative Characteristic of Conceptual Accounting

Framework Met in Financial Report of Coca-Cola Amatil

The conceptual framework of accounting has also stated some enhancing qualitative

characteristics for assisting the accountants in development of financial reports. These

characteristics are comparability, verifiability, timelines and understandability (Conceptual

Framework, 2017). The financial information disclosed should be comparable with that of the

previous year so that investors can asses whether there has been improvement in the financial

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

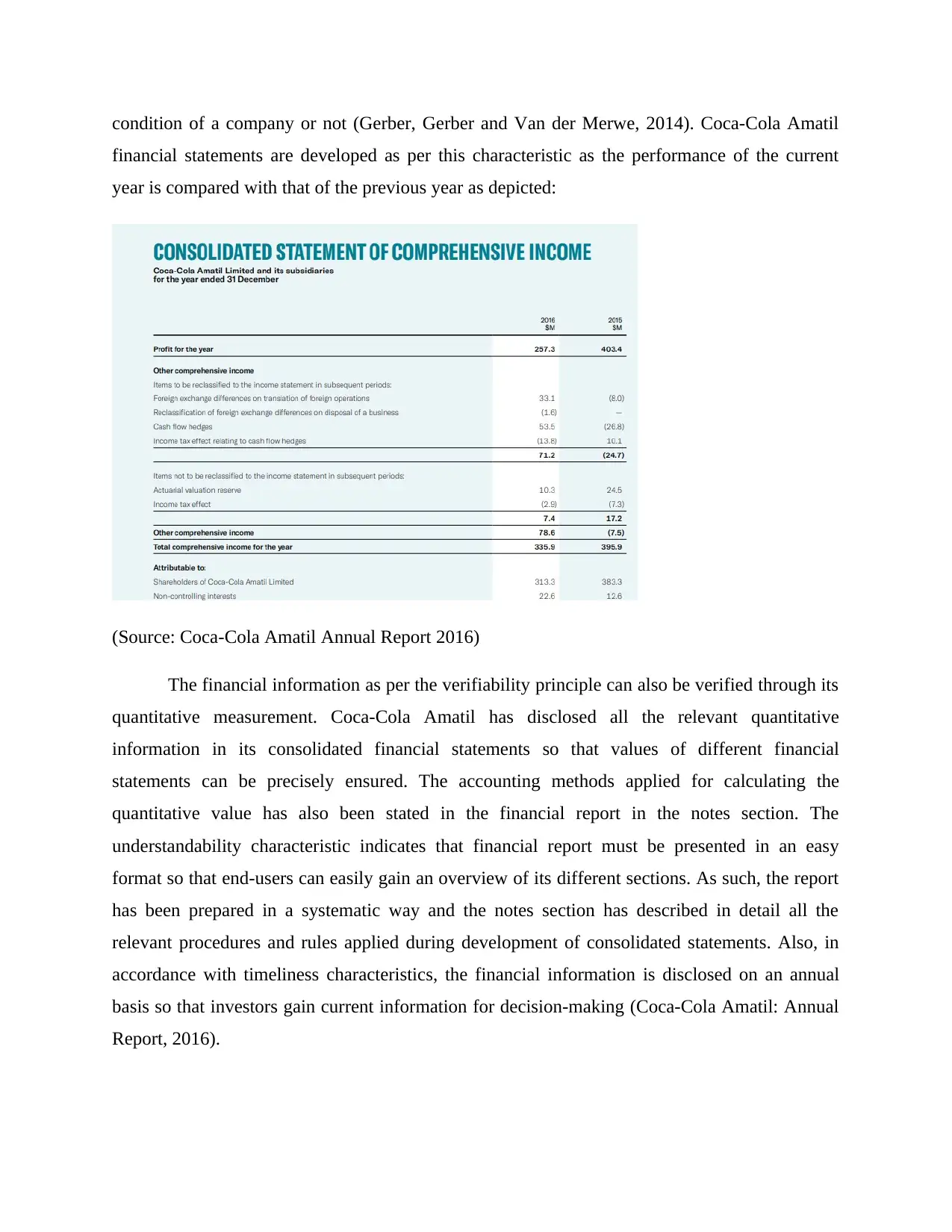

condition of a company or not (Gerber, Gerber and Van der Merwe, 2014). Coca-Cola Amatil

financial statements are developed as per this characteristic as the performance of the current

year is compared with that of the previous year as depicted:

(Source: Coca-Cola Amatil Annual Report 2016)

The financial information as per the verifiability principle can also be verified through its

quantitative measurement. Coca-Cola Amatil has disclosed all the relevant quantitative

information in its consolidated financial statements so that values of different financial

statements can be precisely ensured. The accounting methods applied for calculating the

quantitative value has also been stated in the financial report in the notes section. The

understandability characteristic indicates that financial report must be presented in an easy

format so that end-users can easily gain an overview of its different sections. As such, the report

has been prepared in a systematic way and the notes section has described in detail all the

relevant procedures and rules applied during development of consolidated statements. Also, in

accordance with timeliness characteristics, the financial information is disclosed on an annual

basis so that investors gain current information for decision-making (Coca-Cola Amatil: Annual

Report, 2016).

financial statements are developed as per this characteristic as the performance of the current

year is compared with that of the previous year as depicted:

(Source: Coca-Cola Amatil Annual Report 2016)

The financial information as per the verifiability principle can also be verified through its

quantitative measurement. Coca-Cola Amatil has disclosed all the relevant quantitative

information in its consolidated financial statements so that values of different financial

statements can be precisely ensured. The accounting methods applied for calculating the

quantitative value has also been stated in the financial report in the notes section. The

understandability characteristic indicates that financial report must be presented in an easy

format so that end-users can easily gain an overview of its different sections. As such, the report

has been prepared in a systematic way and the notes section has described in detail all the

relevant procedures and rules applied during development of consolidated statements. Also, in

accordance with timeliness characteristics, the financial information is disclosed on an annual

basis so that investors gain current information for decision-making (Coca-Cola Amatil: Annual

Report, 2016).

(Source: Coca-Cola Amatil Annual Report 2016)

Conclusion

Coca-Cola Amatil complies effectively with the conceptual accounting framework of

IASB. It has prepared differ sections of the financial report as per the qualitative characteristic of

financial reporting stated in the standard framework of accounting.

Conclusion

Coca-Cola Amatil complies effectively with the conceptual accounting framework of

IASB. It has prepared differ sections of the financial report as per the qualitative characteristic of

financial reporting stated in the standard framework of accounting.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Coca-Cola Amatil. 2016. Annual Report. [Online]. Available at:

https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2017/CCA181-Annual-

Report-2016-low-resolution.ashx [Accessed on: 17 April 2018].

Conceptual Framework. 2017. IFRS Foundation. [Online]. Available at:

http://www.frascanada.ca/international-financial-reporting-standards/resources/unaccompanied-

ifrss/item71833.pdf [Accessed on: 17 April 2018].

Gerber, M. C., Gerber, A. J., and Van der Merwe, A. J. 2014. An Analysis of Fundamental

Concepts in the Conceptual Framework Using Ontology Technologies. South African Journal of

Economic & Management Sciences 17 (4), pp. 396–411.

Gore, R., and Zimmerman, D. 2007. Building the Foundations of Financial Reporting: The

Conceptual Framework. The CPA Journal 77(8), pp. 30–34.

Maines, L. and Wahlen, J. 2006. The Nature of Accounting Information Reliability: Inferences

from Archival and Experimental Research. Accounting Horizons 20(4), pp. 399- 425.

Mazhambe, Z. 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework. Journal of Modern Accounting and Auditing 10 (8), pp. 835-845.

McDaniel, L., Martin, R. and Maines, L. 2002. Evaluating Financial Reporting Quality: the

Effects of Financial Expertise vs. Financial Literacy. The Accounting Review 77, pp.139-167.

Psaros, J. and Trotman, K. 2004. The Impact of the Type of Accounting Standards on Preparers’

Judgments. Abacus 40(1), pp. 76-93.

Rezaee, Z. 2003. High-quality financial reporting: The six-legged stool. Strategic Finance 84(8),

pp.26-30.

Soderstrom, N. and Sun, K. 2007. IFRS Adoption and Accounting Quality: A Review. European

Accounting Review 16(4), pp. 675-702.

Tarca, A. 2004. International Convergence of Accounting Practices: Choosing between IAS and

US GAAP. Journal of International Financial Management and Accounting 15(1), pp. 60-91.

Van der Meulen, S., Gaeremynck, A. and Willekens, M. 2007. Attribute differences between

U.S. GAAP and IFRS earnings: An exploratory study. The international Journal of Accounting

42, pp.123-142.

Coca-Cola Amatil. 2016. Annual Report. [Online]. Available at:

https://www.ccamatil.com/-/media/Cca/Corporate/Files/Annual-Reports/2017/CCA181-Annual-

Report-2016-low-resolution.ashx [Accessed on: 17 April 2018].

Conceptual Framework. 2017. IFRS Foundation. [Online]. Available at:

http://www.frascanada.ca/international-financial-reporting-standards/resources/unaccompanied-

ifrss/item71833.pdf [Accessed on: 17 April 2018].

Gerber, M. C., Gerber, A. J., and Van der Merwe, A. J. 2014. An Analysis of Fundamental

Concepts in the Conceptual Framework Using Ontology Technologies. South African Journal of

Economic & Management Sciences 17 (4), pp. 396–411.

Gore, R., and Zimmerman, D. 2007. Building the Foundations of Financial Reporting: The

Conceptual Framework. The CPA Journal 77(8), pp. 30–34.

Maines, L. and Wahlen, J. 2006. The Nature of Accounting Information Reliability: Inferences

from Archival and Experimental Research. Accounting Horizons 20(4), pp. 399- 425.

Mazhambe, Z. 2014. Review of International Accounting Standards Board (IASB) Proposed

New Conceptual Framework. Journal of Modern Accounting and Auditing 10 (8), pp. 835-845.

McDaniel, L., Martin, R. and Maines, L. 2002. Evaluating Financial Reporting Quality: the

Effects of Financial Expertise vs. Financial Literacy. The Accounting Review 77, pp.139-167.

Psaros, J. and Trotman, K. 2004. The Impact of the Type of Accounting Standards on Preparers’

Judgments. Abacus 40(1), pp. 76-93.

Rezaee, Z. 2003. High-quality financial reporting: The six-legged stool. Strategic Finance 84(8),

pp.26-30.

Soderstrom, N. and Sun, K. 2007. IFRS Adoption and Accounting Quality: A Review. European

Accounting Review 16(4), pp. 675-702.

Tarca, A. 2004. International Convergence of Accounting Practices: Choosing between IAS and

US GAAP. Journal of International Financial Management and Accounting 15(1), pp. 60-91.

Van der Meulen, S., Gaeremynck, A. and Willekens, M. 2007. Attribute differences between

U.S. GAAP and IFRS earnings: An exploratory study. The international Journal of Accounting

42, pp.123-142.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.