Audit and Assurance Report Analysis: Coca-Cola Amatil Company Review

VerifiedAdded on 2021/06/15

|7

|725

|21

Report

AI Summary

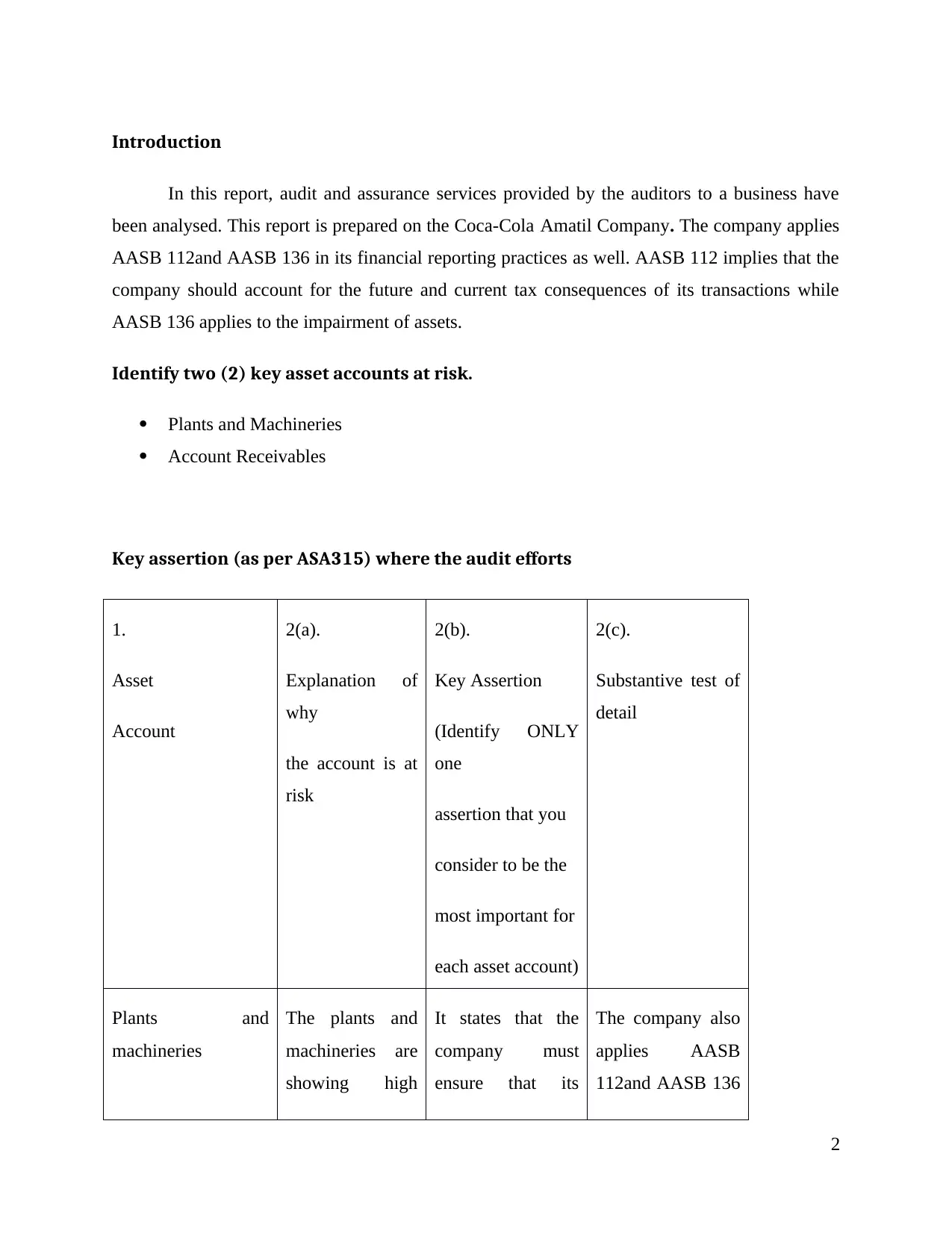

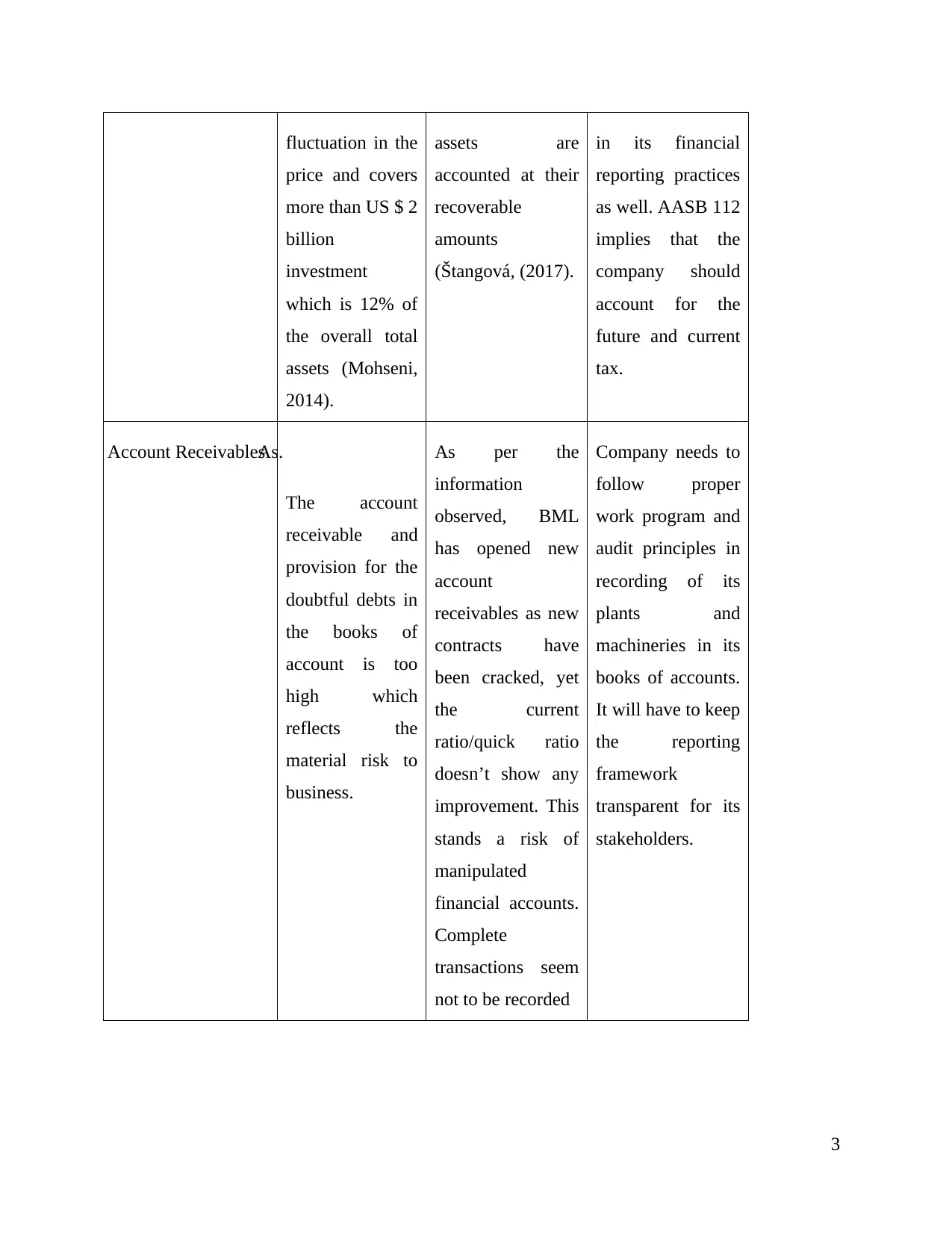

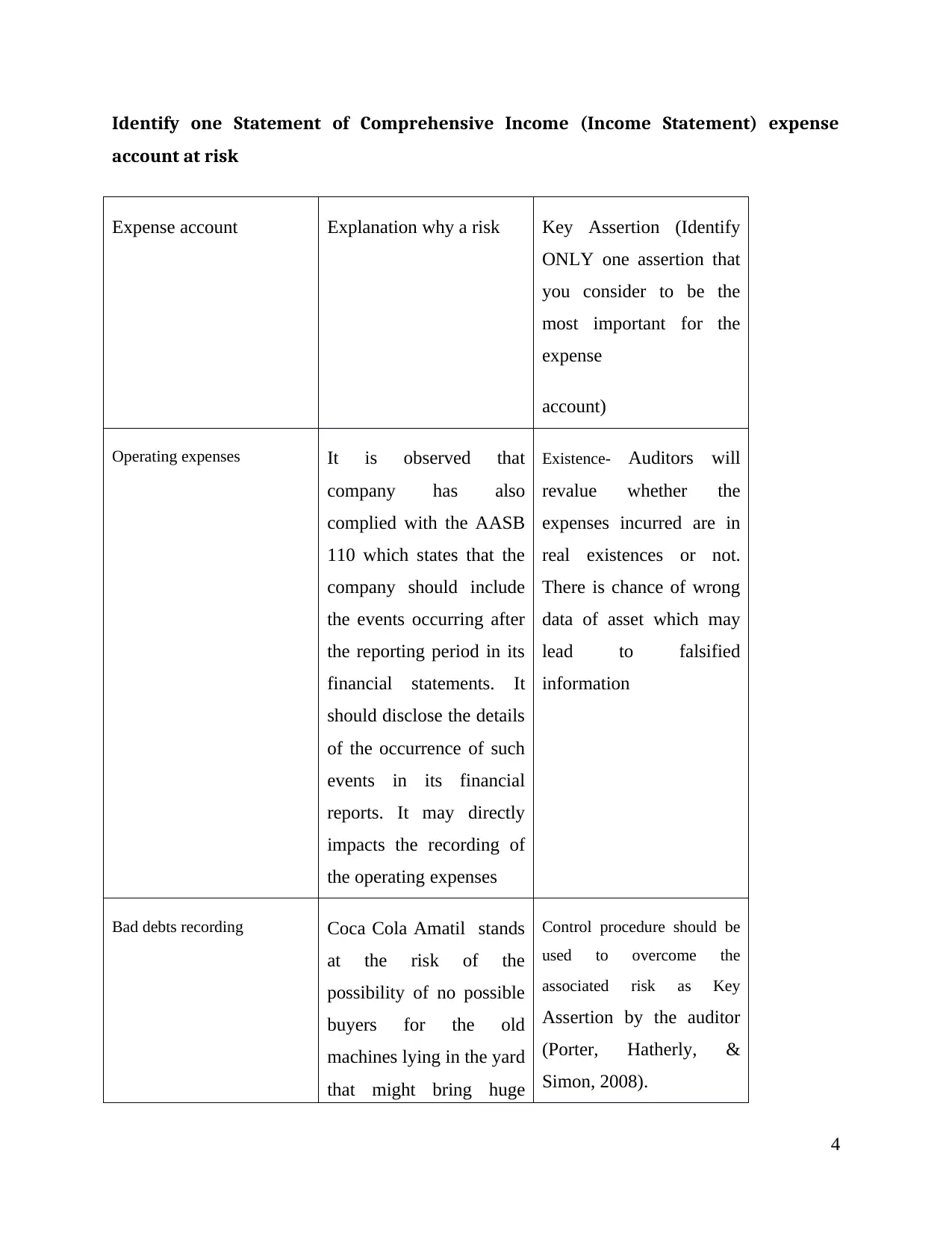

This report provides an audit and assurance analysis of Coca-Cola Amatil, examining the company's financial reporting practices, particularly concerning AASB 112 and AASB 136. It identifies key asset accounts at risk, including plants and machineries and accounts receivables, detailing the associated risks and relevant audit assertions as per ASA315. The report also highlights risks related to operating expenses and the potential for misstated financial information. It emphasizes the importance of proper audit control mechanisms to ensure accurate asset valuation, compliance with accounting standards, and reliable financial reporting. The analysis underscores the need for transparent financial reporting and robust internal controls to mitigate financial risks and ensure the integrity of the company's financial statements. The report concludes by recommending the implementation of effective audit control mechanisms to safeguard assets, ensure legal compliance, and achieve organizational goals efficiently and effectively.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.