Finance for Business: Coca-Cola Performance Analysis Report - HI5002

VerifiedAdded on 2022/11/09

|9

|1001

|226

Report

AI Summary

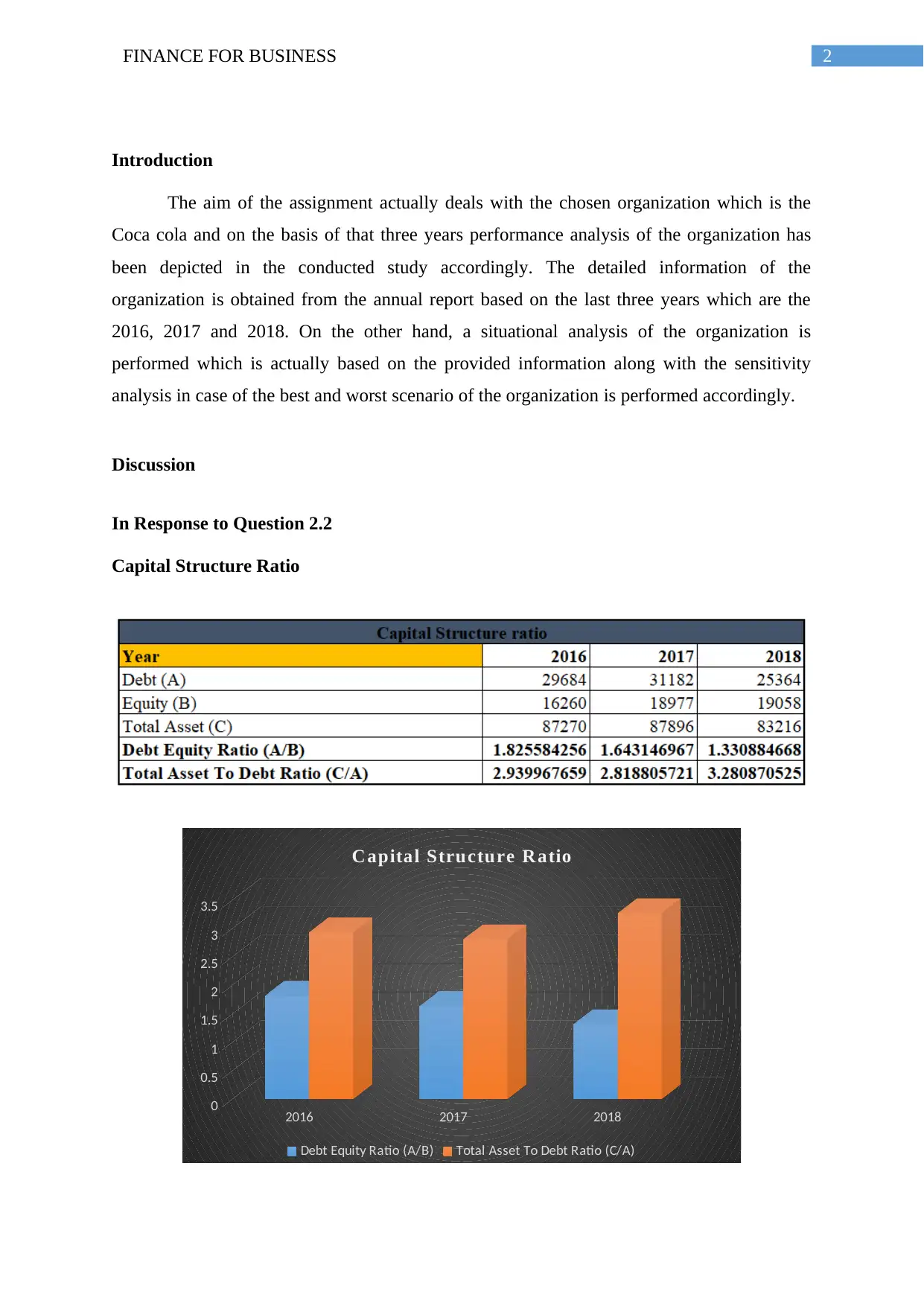

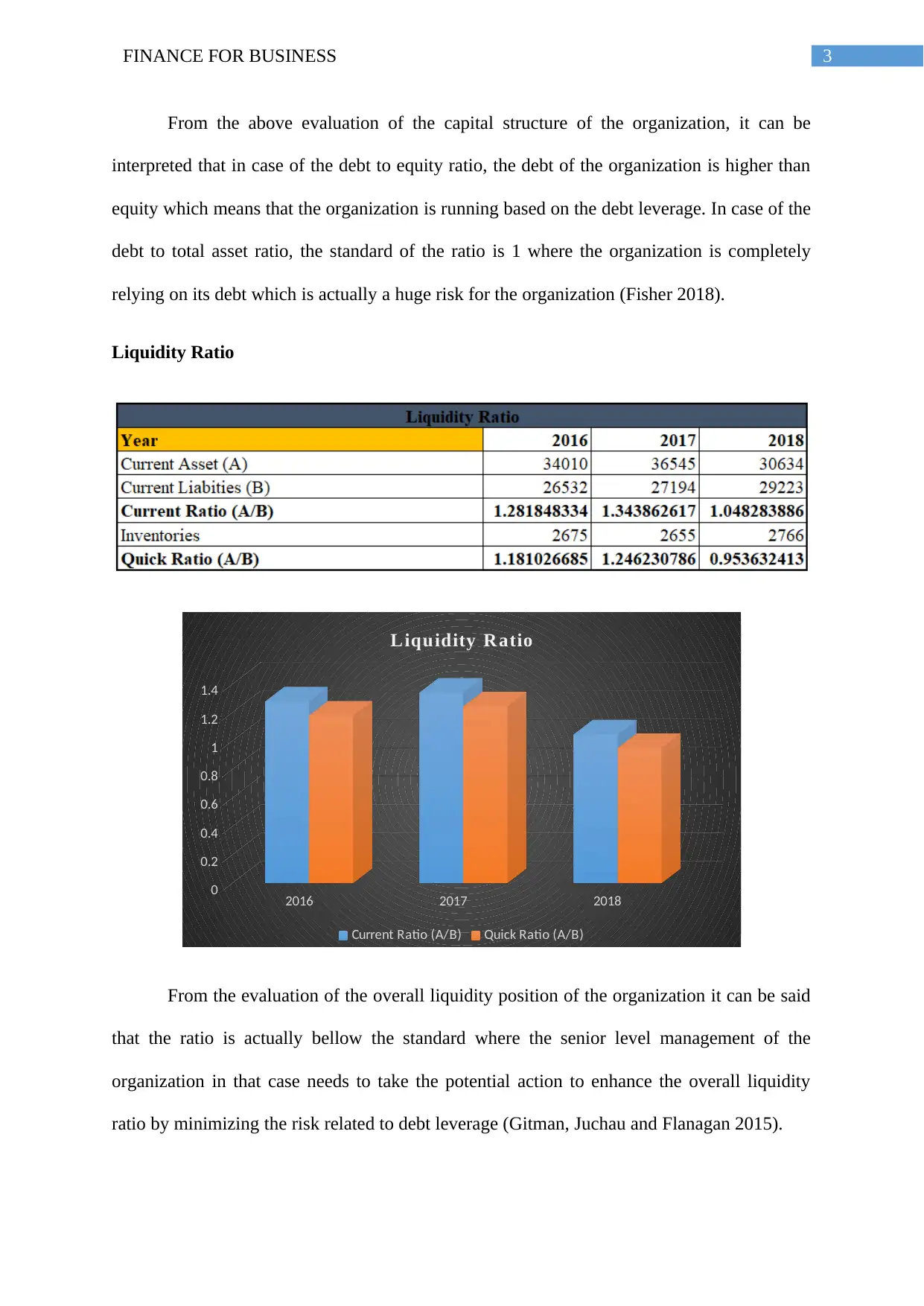

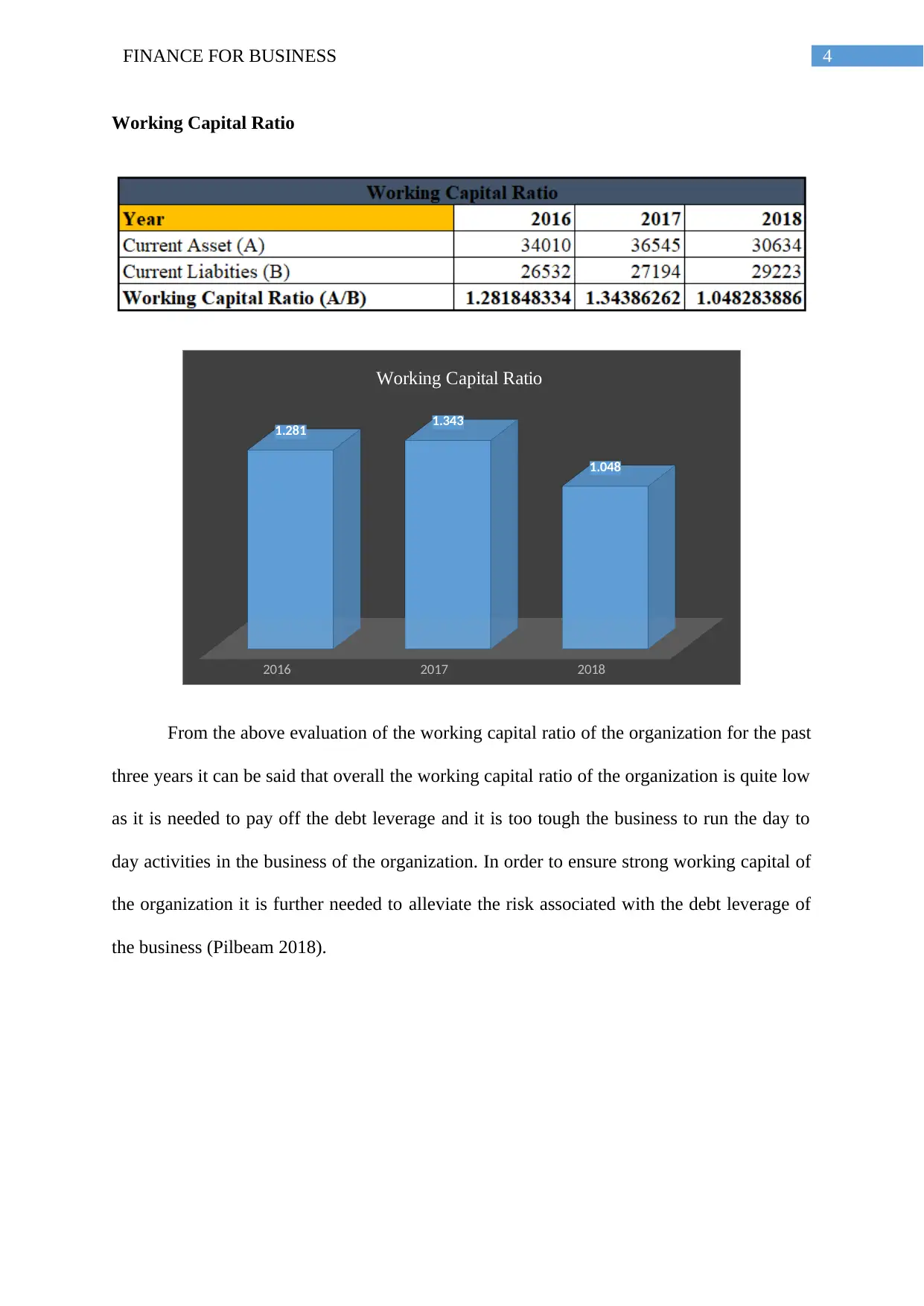

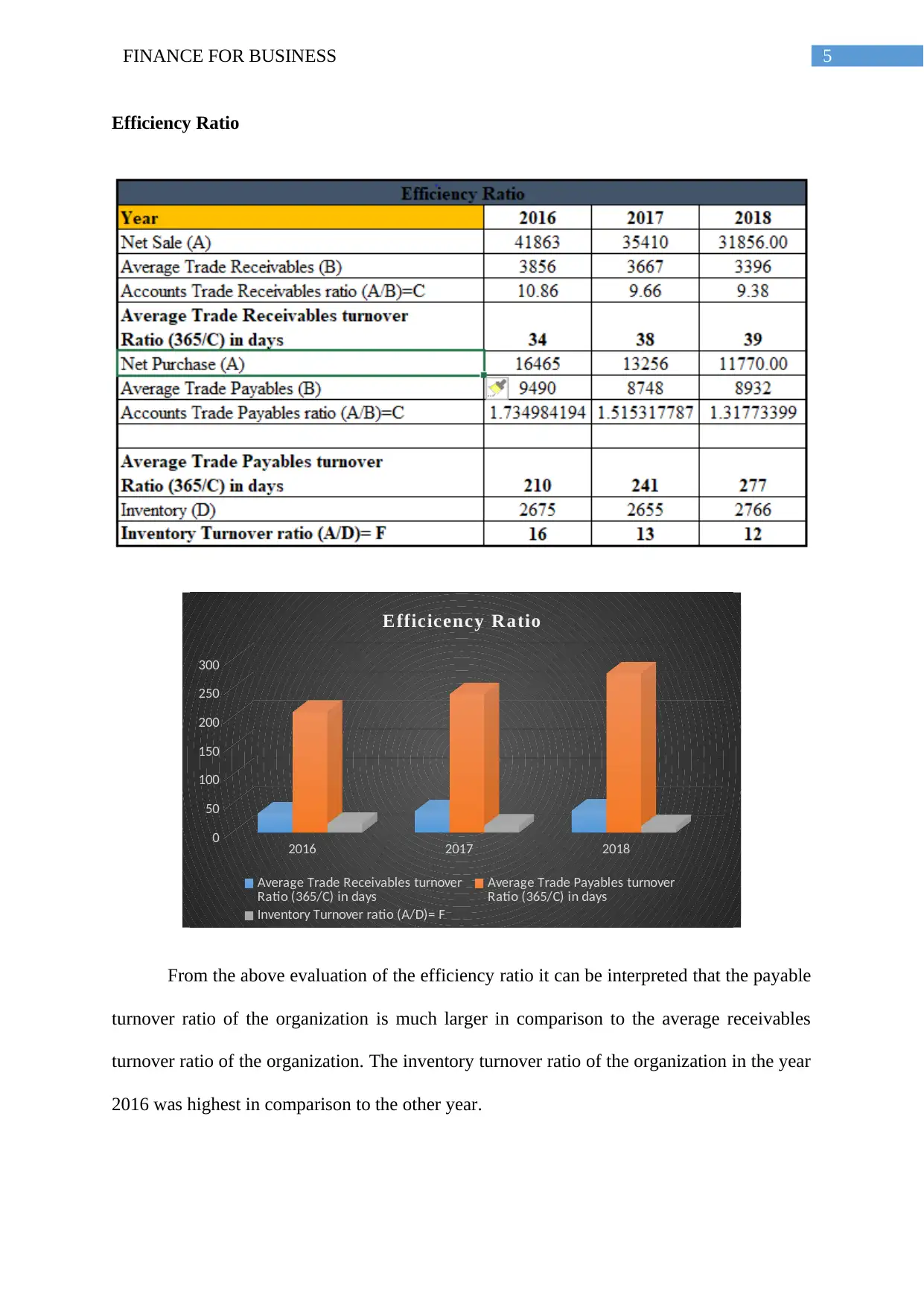

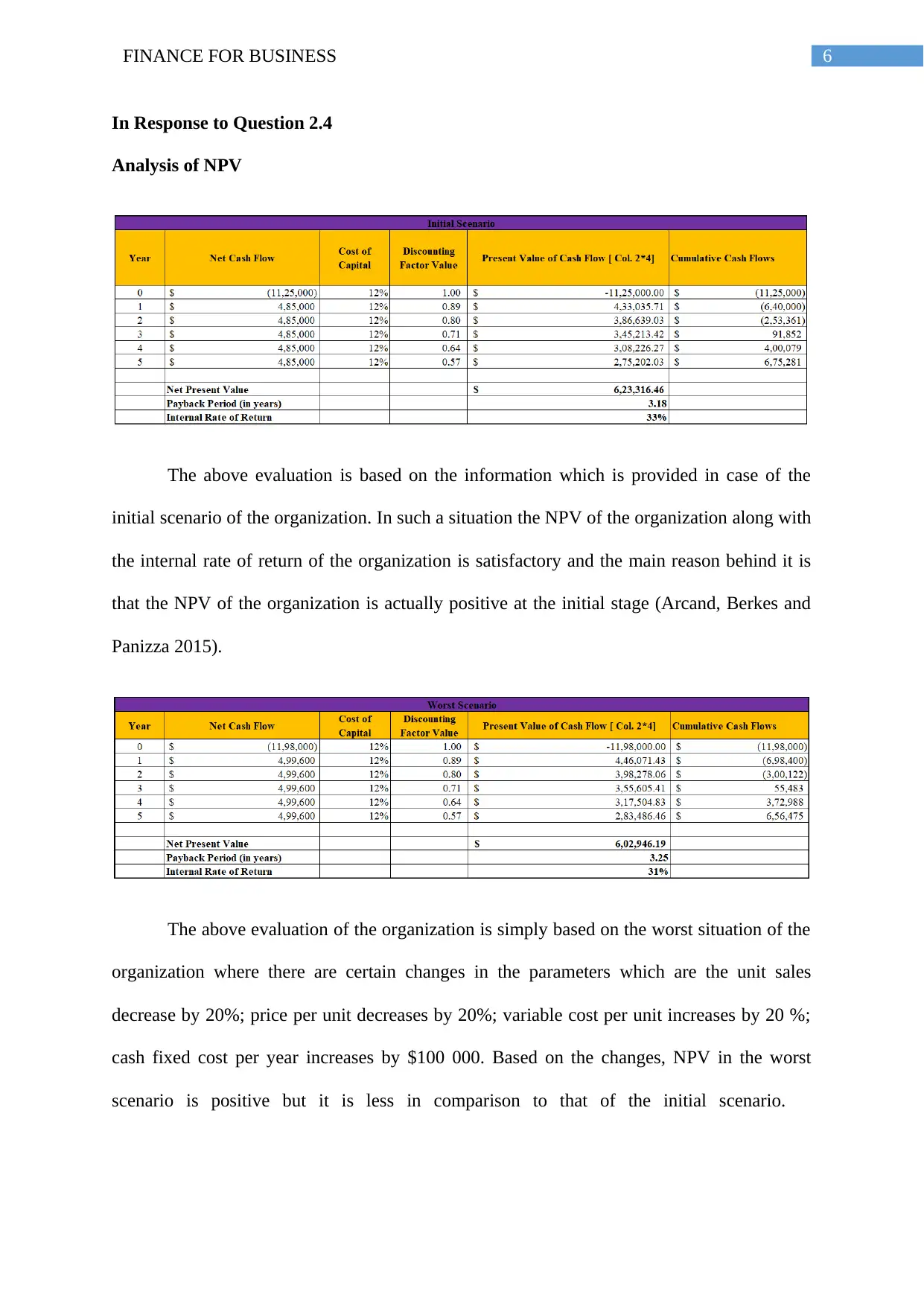

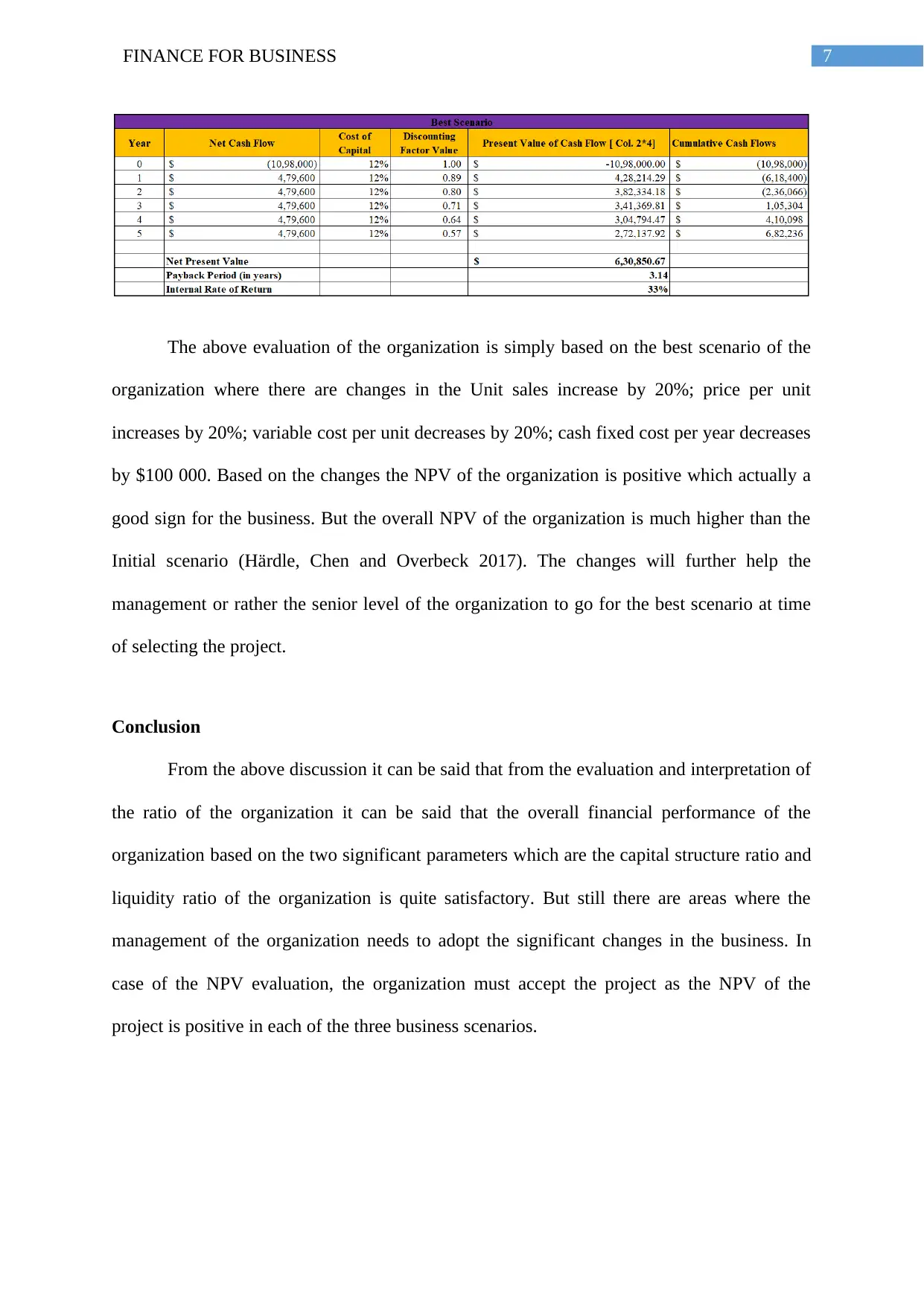

This report provides a comprehensive financial analysis of Coca-Cola's performance over three years (2016-2018), examining capital structure, liquidity, working capital, and efficiency ratios. The analysis includes a detailed assessment of the company's debt-to-equity ratio, debt-to-total-asset ratio, and liquidity position, highlighting areas for potential improvement. Furthermore, the report evaluates Coca-Cola's efficiency ratios, including payable turnover and inventory turnover. The study also presents a Net Present Value (NPV) analysis under initial, best-case, and worst-case scenarios, offering insights into the project's viability. The conclusion summarizes the financial performance, suggesting that while the financial performance based on capital structure and liquidity is satisfactory, the management should consider changes in certain areas. The report recommends accepting the project based on positive NPV across all scenarios.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.