Coca-Cola Amatil: Analysis of Financial Statements and Tax Expenditure

VerifiedAdded on 2021/06/14

|12

|2668

|76

Report

AI Summary

This report offers a comprehensive analysis of Coca-Cola Amatil's financial statements, focusing on key aspects such as cash flow, income tax expenditure, and other comprehensive income. It examines changes in the cash flow statement over several years, providing reasons for these shifts, and conducts a comparative analysis across operating, investing, and financing activities. The report delves into other comprehensive income statement items, explaining why certain items are not reported in the income statement, and explores the company's income tax expenditure, deferred tax, and current tax assets/liabilities. It also compares income tax expense with income tax paid, identifies unique features in the financial statements, and offers insights and recommendations based on the analysis. The report uses the annual reports of Coca-Cola Amatil to provide a detailed overview of the company's financial performance and accounting practices.

Running head: CORPORATE ACCOUNTING

Corporate Accounting

Name of the Student

Name of the University

Author Note

Corporate Accounting

Name of the Student

Name of the University

Author Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1CORPORATE ACCOUNTING

Table of Contents

Brief Overview of the Company................................................................................................3

Changes in item of cash flow statement over the past few years and reasons for the change...3

Comparative analysis of the company’s three broad categories of cash flows that is operating

activities, investing activities and financing activities:..............................................................4

Other Comprehensive Income Statement items and analysis of each items..............................5

Causes for the above items not reported in the income statement.............................................5

Explanation of the about the chosen company’s income tax expenditure.................................6

Whether tax figure that is same as company tax rate times the company’s accounting income6

Deferred tax reported in balance sheet and reasons for the record............................................7

Income tax payable or current tax assets recorded by the firm..................................................7

Whether Income tax expenditure that is shown in income statement same as income tax paid

shown in cash flow statement....................................................................................................8

Unique Features in the financial statements and the new insights along with recommendations

....................................................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................11

Table of Contents

Brief Overview of the Company................................................................................................3

Changes in item of cash flow statement over the past few years and reasons for the change...3

Comparative analysis of the company’s three broad categories of cash flows that is operating

activities, investing activities and financing activities:..............................................................4

Other Comprehensive Income Statement items and analysis of each items..............................5

Causes for the above items not reported in the income statement.............................................5

Explanation of the about the chosen company’s income tax expenditure.................................6

Whether tax figure that is same as company tax rate times the company’s accounting income6

Deferred tax reported in balance sheet and reasons for the record............................................7

Income tax payable or current tax assets recorded by the firm..................................................7

Whether Income tax expenditure that is shown in income statement same as income tax paid

shown in cash flow statement....................................................................................................8

Unique Features in the financial statements and the new insights along with recommendations

....................................................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................11

2CORPORATE ACCOUNTING

Brief Overview of the Company

The chosen company is Coca Cola Amatil that is listed under the ASX is that deals

with the soft drinks and non-alcoholic beverages in Australia. In order to analyze the annual

report the chosen organization listed on the Australian Stock exchange (ASX) The Company

offers a stable cash flows and comparatively low risks and it facilitates payment to the

investors along with the potential long-term growth. It seeks to establish the diversified

portfolio with regard to regulated utility infrastructure assets and continuing to be in the lead

position under the Australian infrastructure investment fund. Further, the values upon which

the company is maintaining its growth are fairness, honesty, maximizing the value of the

security holder and maintenance of the high standards for corporate governance.

Changes in item of cash flow statement over the past few years and reasons for the

change

By the evaluation and analysis of the cash flow statements of the business

organizations, it becomes easier to gain an understanding of their inflows as well as outflows.

For this paper, Coca Cola Amatil has been chosen and each item of its cash flow statement is

analyzed. The cash flow statement mainly consist of three sections that involves cash flow

from investing activities, operating activities, financing activities and net cash as well as cash

equivalents (Brooks, 2015). The items that are included in the operating activities involves

depreciation, adjustments to net income, liabilities changes, inventory changes, changes in

accounts receivable and changes in other operating activities. The items that are included in

the investment activities are capital expenses, investments and other cash flow from

investment activities. In this cash flow statement of Coca cola Amatil, financing activities

mainly consists of the paid dividends, net borrowings, purchase as well as sale of stocks and

other cash flows from the financing activities (Grant, 2016).

Brief Overview of the Company

The chosen company is Coca Cola Amatil that is listed under the ASX is that deals

with the soft drinks and non-alcoholic beverages in Australia. In order to analyze the annual

report the chosen organization listed on the Australian Stock exchange (ASX) The Company

offers a stable cash flows and comparatively low risks and it facilitates payment to the

investors along with the potential long-term growth. It seeks to establish the diversified

portfolio with regard to regulated utility infrastructure assets and continuing to be in the lead

position under the Australian infrastructure investment fund. Further, the values upon which

the company is maintaining its growth are fairness, honesty, maximizing the value of the

security holder and maintenance of the high standards for corporate governance.

Changes in item of cash flow statement over the past few years and reasons for the

change

By the evaluation and analysis of the cash flow statements of the business

organizations, it becomes easier to gain an understanding of their inflows as well as outflows.

For this paper, Coca Cola Amatil has been chosen and each item of its cash flow statement is

analyzed. The cash flow statement mainly consist of three sections that involves cash flow

from investing activities, operating activities, financing activities and net cash as well as cash

equivalents (Brooks, 2015). The items that are included in the operating activities involves

depreciation, adjustments to net income, liabilities changes, inventory changes, changes in

accounts receivable and changes in other operating activities. The items that are included in

the investment activities are capital expenses, investments and other cash flow from

investment activities. In this cash flow statement of Coca cola Amatil, financing activities

mainly consists of the paid dividends, net borrowings, purchase as well as sale of stocks and

other cash flows from the financing activities (Grant, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3CORPORATE ACCOUNTING

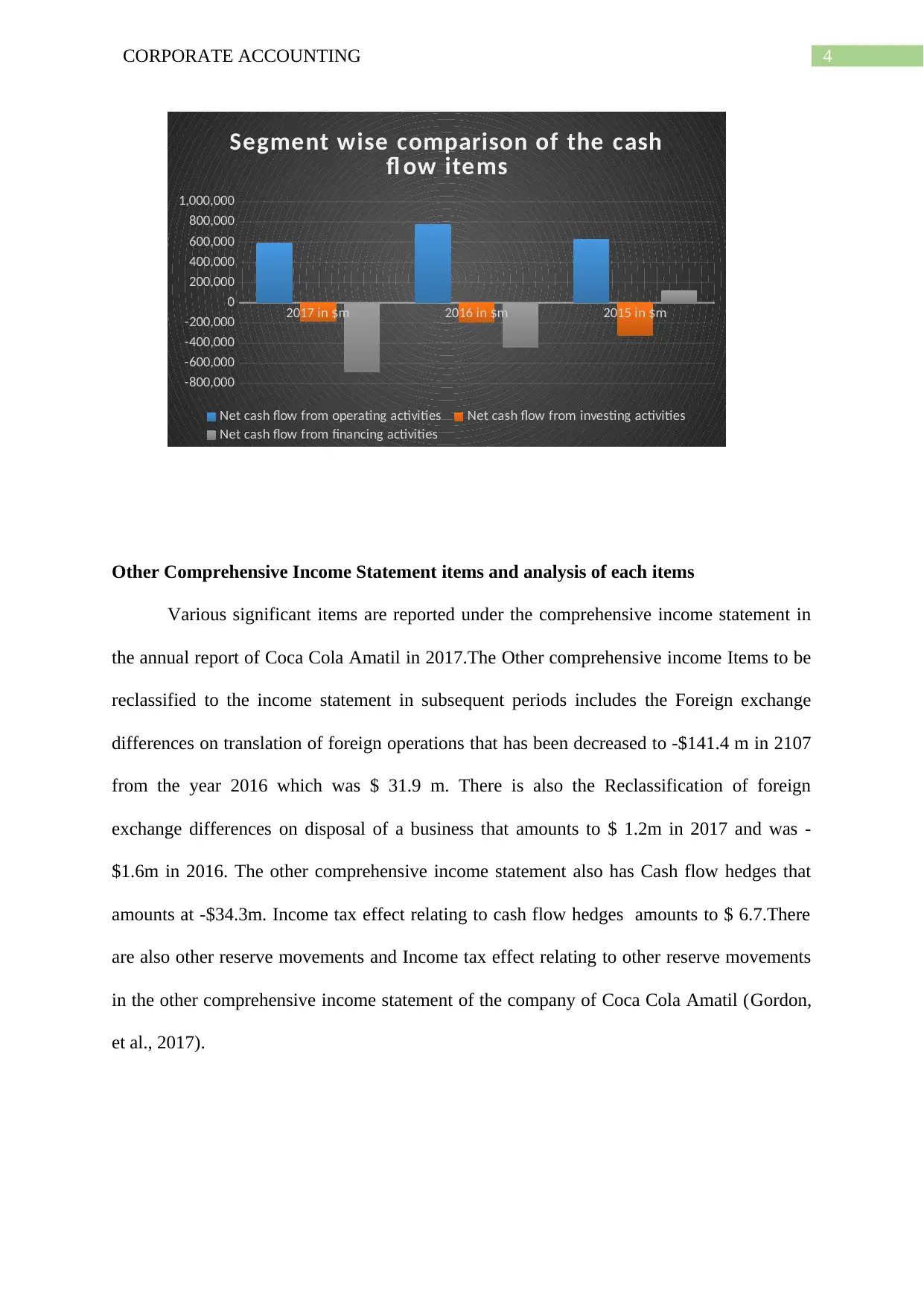

Comparative analysis of the company’s three broad categories of cash flows that is

operating activities, investing activities and financing activities:

Cash flows from operations:

It has been seen that the total cash flow of operating activities has increased in the

year 2017 to $5, 89,200 from the year 2016 and 2015.

Cash flows from investing activities:

It is evident that the total cash used for the investment activities increased in the year

2016 to -1, 89,800 from $ -3, 21,400 in the year 2015 and then again increased to $ -1, 82,600

in the year 2017.

Cash flows from financing activities:

There has been rise in total cash used in the financing activities in the year 2017 to -6,

84,500 from the year 2015 but in comparison to 2106 the cash out flow has been enhanced

from $-4, 38,500.

Moreover, the change in cash and cash equivalents amounts to $-3, 40,700 in the year

2017, $1, 39,600 in the year 2016 and $4, 34,400 in the year 2015.

Particular

2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating

activities 5,89,200 7,74,800 6,26,800

Net cash flow from investing activities -1,82,600 -1,89,800 -3,21,400

Net cash flow from financing

activities -6,84,500 -4,38,500 1,22,400

Comparative analysis of the company’s three broad categories of cash flows that is

operating activities, investing activities and financing activities:

Cash flows from operations:

It has been seen that the total cash flow of operating activities has increased in the

year 2017 to $5, 89,200 from the year 2016 and 2015.

Cash flows from investing activities:

It is evident that the total cash used for the investment activities increased in the year

2016 to -1, 89,800 from $ -3, 21,400 in the year 2015 and then again increased to $ -1, 82,600

in the year 2017.

Cash flows from financing activities:

There has been rise in total cash used in the financing activities in the year 2017 to -6,

84,500 from the year 2015 but in comparison to 2106 the cash out flow has been enhanced

from $-4, 38,500.

Moreover, the change in cash and cash equivalents amounts to $-3, 40,700 in the year

2017, $1, 39,600 in the year 2016 and $4, 34,400 in the year 2015.

Particular

2017 in

$m

2016 in

$m

2015 in

$m

Net cash flow from operating

activities 5,89,200 7,74,800 6,26,800

Net cash flow from investing activities -1,82,600 -1,89,800 -3,21,400

Net cash flow from financing

activities -6,84,500 -4,38,500 1,22,400

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4CORPORATE ACCOUNTING

2017 in $m 2016 in $m 2015 in $m

-800,000

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

Segment wise comparison of the cash

fl ow items

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Other Comprehensive Income Statement items and analysis of each items

Various significant items are reported under the comprehensive income statement in

the annual report of Coca Cola Amatil in 2017.The Other comprehensive income Items to be

reclassified to the income statement in subsequent periods includes the Foreign exchange

differences on translation of foreign operations that has been decreased to -$141.4 m in 2107

from the year 2016 which was $ 31.9 m. There is also the Reclassification of foreign

exchange differences on disposal of a business that amounts to $ 1.2m in 2017 and was -

$1.6m in 2016. The other comprehensive income statement also has Cash flow hedges that

amounts at -$34.3m. Income tax effect relating to cash flow hedges amounts to $ 6.7.There

are also other reserve movements and Income tax effect relating to other reserve movements

in the other comprehensive income statement of the company of Coca Cola Amatil (Gordon,

et al., 2017).

2017 in $m 2016 in $m 2015 in $m

-800,000

-600,000

-400,000

-200,000

0

200,000

400,000

600,000

800,000

1,000,000

Segment wise comparison of the cash

fl ow items

Net cash flow from operating activities Net cash flow from investing activities

Net cash flow from financing activities

Other Comprehensive Income Statement items and analysis of each items

Various significant items are reported under the comprehensive income statement in

the annual report of Coca Cola Amatil in 2017.The Other comprehensive income Items to be

reclassified to the income statement in subsequent periods includes the Foreign exchange

differences on translation of foreign operations that has been decreased to -$141.4 m in 2107

from the year 2016 which was $ 31.9 m. There is also the Reclassification of foreign

exchange differences on disposal of a business that amounts to $ 1.2m in 2017 and was -

$1.6m in 2016. The other comprehensive income statement also has Cash flow hedges that

amounts at -$34.3m. Income tax effect relating to cash flow hedges amounts to $ 6.7.There

are also other reserve movements and Income tax effect relating to other reserve movements

in the other comprehensive income statement of the company of Coca Cola Amatil (Gordon,

et al., 2017).

5CORPORATE ACCOUNTING

Causes for the above items not reported in the income statement

The comprehensive income statement is mainly used for measurement of change in

owner’s interest in the business. It generally incorporates income as well as expenditure

which have not yet realized and is utilized for bypassing income statement. In addition to

this, other comprehensive income mainly considers items that involve debt security on the

unrealized profits and losses, changes in transactions of foreign currency, profit or loss

obtained from the derivative instruments and any other pension profits or losses (Damodaran,

2016). The main purpose of Coca cola Amatil in forming the other comprehensive income

statement delivers the users with the essential information in relation to the above-mentioned

aspects. Thus, this statement provides an overview of transparent and holistic approach of

such items. Such causes are not engaged directly in order to derive income (Kroes &

Manikas, 2014).

Explanation of the about the chosen company’s income tax expenditure

The Coca Cola Amatil is obliged to conduct its tax accounting in accordance with the

norms of the Australian taxation. In the years 2016 and 2017, the tax rate that could be

applied to the organization is 30%. Based on the statement of financial performance in 2017,

the income tax expense reported has been -$148.6million in 2017 and- $135.8million in 2016.

The tax was calculated as expense of income tax divided by profit before income tax expense

from discontinued and continuing operations (Hackbarth & Sun, 2015).

Whether tax figure that is same as company tax rate times the company’s accounting

income

The amount of income tax has been computed by using tax rates, which have been

mainly ratified significantly from the statement of companies financial. Based on the

statement of financial performance in 2017, the income tax expense reported has been -

Causes for the above items not reported in the income statement

The comprehensive income statement is mainly used for measurement of change in

owner’s interest in the business. It generally incorporates income as well as expenditure

which have not yet realized and is utilized for bypassing income statement. In addition to

this, other comprehensive income mainly considers items that involve debt security on the

unrealized profits and losses, changes in transactions of foreign currency, profit or loss

obtained from the derivative instruments and any other pension profits or losses (Damodaran,

2016). The main purpose of Coca cola Amatil in forming the other comprehensive income

statement delivers the users with the essential information in relation to the above-mentioned

aspects. Thus, this statement provides an overview of transparent and holistic approach of

such items. Such causes are not engaged directly in order to derive income (Kroes &

Manikas, 2014).

Explanation of the about the chosen company’s income tax expenditure

The Coca Cola Amatil is obliged to conduct its tax accounting in accordance with the

norms of the Australian taxation. In the years 2016 and 2017, the tax rate that could be

applied to the organization is 30%. Based on the statement of financial performance in 2017,

the income tax expense reported has been -$148.6million in 2017 and- $135.8million in 2016.

The tax was calculated as expense of income tax divided by profit before income tax expense

from discontinued and continuing operations (Hackbarth & Sun, 2015).

Whether tax figure that is same as company tax rate times the company’s accounting

income

The amount of income tax has been computed by using tax rates, which have been

mainly ratified significantly from the statement of companies financial. Based on the

statement of financial performance in 2017, the income tax expense reported has been -

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6CORPORATE ACCOUNTING

$148.6million in 2017 and $-135.8million in 2016. The tax was calculated as expense of

income tax divided by profit before income tax expense from discontinued and continuing

operations. This shows that the income tax amount had decreased considerably in the year

2017. However, it cannot be estimated that whether the income tax expenditures figures are

same as that of tax rate times this company’s accounting income (Najmi, Sarraf & Darabi,

2015).

Deferred tax reported in balance sheet and reasons for the record

The Deferred tax is accounted using the method of balance sheet liability resulting

from temporary differences between the tax bases of liabilities and assets and their carrying

amount in the financial statements. The initial recognition of liabilities and assets does not

lead to recognition of deferred income tax and this does not have any impact on accounting or

taxable loss or profit (Delkhosh et al., 2017). Recognition of deferred tax assets are done to

the extent that the availability of future taxable profits is probable against the temporary

differences that are deductible. In current year, there has been deferred tax liabilities of Coca

Cola Amatil is $ 283.8 m in 2017 and $ 303.2 in 2016.

Income tax payable or current tax assets recorded by the firm

In the chosen company of Coca Cola Amatil the current tax assets amounts to $5.1 m

in 2017 and $ 1.5 m in 2016. There has also been current tax payable identified in the balance

sheet that amounts to $27.6 m in 2017 from $42.0 m in the year of 2016.

The Income tax assets is the amount that is calculated based on the standard

accounting rules and on the amount of tax that is owed by company to tax authorities (Chen,

Feldmann & Tang, 2015). Income tax payable is the amount that the entity owes in terms of

$148.6million in 2017 and $-135.8million in 2016. The tax was calculated as expense of

income tax divided by profit before income tax expense from discontinued and continuing

operations. This shows that the income tax amount had decreased considerably in the year

2017. However, it cannot be estimated that whether the income tax expenditures figures are

same as that of tax rate times this company’s accounting income (Najmi, Sarraf & Darabi,

2015).

Deferred tax reported in balance sheet and reasons for the record

The Deferred tax is accounted using the method of balance sheet liability resulting

from temporary differences between the tax bases of liabilities and assets and their carrying

amount in the financial statements. The initial recognition of liabilities and assets does not

lead to recognition of deferred income tax and this does not have any impact on accounting or

taxable loss or profit (Delkhosh et al., 2017). Recognition of deferred tax assets are done to

the extent that the availability of future taxable profits is probable against the temporary

differences that are deductible. In current year, there has been deferred tax liabilities of Coca

Cola Amatil is $ 283.8 m in 2017 and $ 303.2 in 2016.

Income tax payable or current tax assets recorded by the firm

In the chosen company of Coca Cola Amatil the current tax assets amounts to $5.1 m

in 2017 and $ 1.5 m in 2016. There has also been current tax payable identified in the balance

sheet that amounts to $27.6 m in 2017 from $42.0 m in the year of 2016.

The Income tax assets is the amount that is calculated based on the standard

accounting rules and on the amount of tax that is owed by company to tax authorities (Chen,

Feldmann & Tang, 2015). Income tax payable is the amount that the entity owes in terms of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7CORPORATE ACCOUNTING

tax based on rules of tax code.Until the company makes the payment of tax, the amount of

income tax payable appears on the balance sheet liability section.

Whether Income tax expenditure that is shown in income statement same as income tax

paid shown in cash flow statement

According to the latest annual report of Coca Cola Amatil, the income tax expense

shown in the income statement is not same as the income tax paid shown in the cash flow

statement which is -$173.4 m in 2017 that have been reduced from -$145.0 m. The Income

tax payments includes the impact of income tax of certain loss or gain relating to financing or

investing activities so that after tax cash flow is reflected in the subtotals of net cash flow. On

other hand Income tax expense is the amount that represents the recording of income tax

costs. Income tax payable is the liability account that helps in recording of the income tax

amount that is owed by organization but is yet to be paid (Almamy, Aston & Ngwa 2016).

Income tax expenses on other hand represent the amount that is incurred rather than being

paid. In this case, it is worth mentioning that the income tax expense recorded in the income

statement is the amount incurred in the current taxation year of the organization and the

payment is required to be made in the upcoming year (Scholes, 2015).

Unique Features in the financial statements and the new insights along with

recommendations

On the basis of the analysis of all the disclosed financial information, no surprising or

confusing elements could be observed in the tax-related treatment of Coca Cola Amatil. This

is because the organization has supplied the needed justifications and clarifications of the

taxation treatment as footnotes in the financial report. From the annual report, it can be

recognized that the total amount for income tax has been basically made based on the

adjusted profits which are generally attributable for non- assessable or disallowed items (Reid

tax based on rules of tax code.Until the company makes the payment of tax, the amount of

income tax payable appears on the balance sheet liability section.

Whether Income tax expenditure that is shown in income statement same as income tax

paid shown in cash flow statement

According to the latest annual report of Coca Cola Amatil, the income tax expense

shown in the income statement is not same as the income tax paid shown in the cash flow

statement which is -$173.4 m in 2017 that have been reduced from -$145.0 m. The Income

tax payments includes the impact of income tax of certain loss or gain relating to financing or

investing activities so that after tax cash flow is reflected in the subtotals of net cash flow. On

other hand Income tax expense is the amount that represents the recording of income tax

costs. Income tax payable is the liability account that helps in recording of the income tax

amount that is owed by organization but is yet to be paid (Almamy, Aston & Ngwa 2016).

Income tax expenses on other hand represent the amount that is incurred rather than being

paid. In this case, it is worth mentioning that the income tax expense recorded in the income

statement is the amount incurred in the current taxation year of the organization and the

payment is required to be made in the upcoming year (Scholes, 2015).

Unique Features in the financial statements and the new insights along with

recommendations

On the basis of the analysis of all the disclosed financial information, no surprising or

confusing elements could be observed in the tax-related treatment of Coca Cola Amatil. This

is because the organization has supplied the needed justifications and clarifications of the

taxation treatment as footnotes in the financial report. From the annual report, it can be

recognized that the total amount for income tax has been basically made based on the

adjusted profits which are generally attributable for non- assessable or disallowed items (Reid

8CORPORATE ACCOUNTING

& Myddelton, 2017). It can be seen from the above discussion that this enterprise has

followed all the basic requirements of the Australian Tax Office (ATO) while estimating

different taxes that has been included in the financial statement of the company (Robinson &

Sensoy, 2016).

& Myddelton, 2017). It can be seen from the above discussion that this enterprise has

followed all the basic requirements of the Australian Tax Office (ATO) while estimating

different taxes that has been included in the financial statement of the company (Robinson &

Sensoy, 2016).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9CORPORATE ACCOUNTING

References

Almamy, J., Aston, J., & Ngwa, L. N. (2016). An evaluation of Altman's Z-score using cash

flow ratio to predict corporate failure amid the recent financial crisis: Evidence from

the UK. Journal of Corporate Finance, 36, 278-285.

Brooks, R. (2015). Financial management: core concepts. Pearson.

Chen, L., Feldmann, A., & Tang, O. (2015). The relationship between disclosures of

corporate social performance and financial performance: Evidences from GRI reports

in manufacturing industry. International Journal of Production Economics, 170, 445-

456.

Damodaran, A. (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Delkhosh, M., Malek, Z., Rahimi, M., & Farokhi, Z. (2017). A comparative study of

information content of cash flow, cash value added, accounting earnings, and market

value added to book value of total assets in evaluating the firm

performance. International Journal of Accounting and Economics Studies, 5(2), 112-

117.

Gordon, E. A., Henry, E., Jorgensen, B. N., & Linthicum, C. L. (2017). Flexibility in cash-

flow classification under IFRS: determinants and consequences. Review of

Accounting Studies, 22(2), 839-872.

Grant, R. M. (2016). Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Hackbarth, D., & Sun, D. (2015). Corporate investment and financing dynamics.

References

Almamy, J., Aston, J., & Ngwa, L. N. (2016). An evaluation of Altman's Z-score using cash

flow ratio to predict corporate failure amid the recent financial crisis: Evidence from

the UK. Journal of Corporate Finance, 36, 278-285.

Brooks, R. (2015). Financial management: core concepts. Pearson.

Chen, L., Feldmann, A., & Tang, O. (2015). The relationship between disclosures of

corporate social performance and financial performance: Evidences from GRI reports

in manufacturing industry. International Journal of Production Economics, 170, 445-

456.

Damodaran, A. (2016). Damodaran on valuation: security analysis for investment and

corporate finance (Vol. 324). John Wiley & Sons.

Delkhosh, M., Malek, Z., Rahimi, M., & Farokhi, Z. (2017). A comparative study of

information content of cash flow, cash value added, accounting earnings, and market

value added to book value of total assets in evaluating the firm

performance. International Journal of Accounting and Economics Studies, 5(2), 112-

117.

Gordon, E. A., Henry, E., Jorgensen, B. N., & Linthicum, C. L. (2017). Flexibility in cash-

flow classification under IFRS: determinants and consequences. Review of

Accounting Studies, 22(2), 839-872.

Grant, R. M. (2016). Contemporary strategy analysis: Text and cases edition. John Wiley &

Sons.

Hackbarth, D., & Sun, D. (2015). Corporate investment and financing dynamics.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10CORPORATE ACCOUNTING

Kroes, J. R., & Manikas, A. S. (2014). Cash flow management and manufacturing firm

financial performance: A longitudinal perspective. International Journal of

Production Economics, 148, 37-50.

Najmi, M., Sarraf, F., & Darabi, R. (2015). Relationship between Capital Structure, Free

Cash Flow and Performance in Companies Listed on Tehran Stock

Exchange. European Online Journal of Natural and Social Sciences:

Proceedings, 4(1 (s)), pp-1229.

Reid, W., & Myddelton, D. R. (2017). The meaning of company accounts. Routledge.

Robinson, D. T., & Sensoy, B. A. (2016). Cyclicality, performance measurement, and cash

flow liquidity in private equity. Journal of Financial Economics, 122(3), 521-543.

Scholes, M. S. (2015). Taxes and business strategy. Prentice Hall.

Kroes, J. R., & Manikas, A. S. (2014). Cash flow management and manufacturing firm

financial performance: A longitudinal perspective. International Journal of

Production Economics, 148, 37-50.

Najmi, M., Sarraf, F., & Darabi, R. (2015). Relationship between Capital Structure, Free

Cash Flow and Performance in Companies Listed on Tehran Stock

Exchange. European Online Journal of Natural and Social Sciences:

Proceedings, 4(1 (s)), pp-1229.

Reid, W., & Myddelton, D. R. (2017). The meaning of company accounts. Routledge.

Robinson, D. T., & Sensoy, B. A. (2016). Cyclicality, performance measurement, and cash

flow liquidity in private equity. Journal of Financial Economics, 122(3), 521-543.

Scholes, M. S. (2015). Taxes and business strategy. Prentice Hall.

11CORPORATE ACCOUNTING

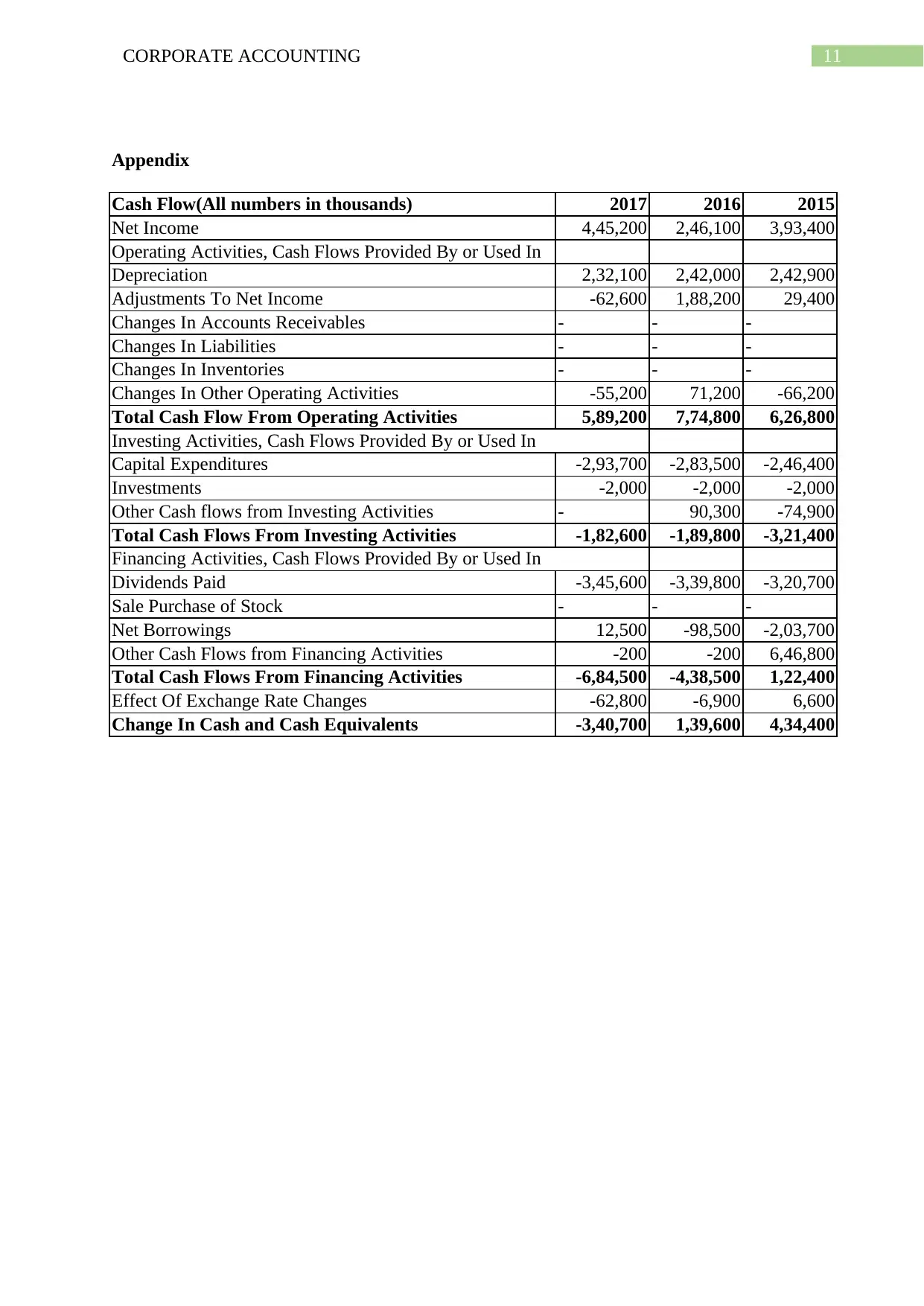

Appendix

Cash Flow(All numbers in thousands) 2017 2016 2015

Net Income 4,45,200 2,46,100 3,93,400

Operating Activities, Cash Flows Provided By or Used In

Depreciation 2,32,100 2,42,000 2,42,900

Adjustments To Net Income -62,600 1,88,200 29,400

Changes In Accounts Receivables - - -

Changes In Liabilities - - -

Changes In Inventories - - -

Changes In Other Operating Activities -55,200 71,200 -66,200

Total Cash Flow From Operating Activities 5,89,200 7,74,800 6,26,800

Investing Activities, Cash Flows Provided By or Used In

Capital Expenditures -2,93,700 -2,83,500 -2,46,400

Investments -2,000 -2,000 -2,000

Other Cash flows from Investing Activities - 90,300 -74,900

Total Cash Flows From Investing Activities -1,82,600 -1,89,800 -3,21,400

Financing Activities, Cash Flows Provided By or Used In

Dividends Paid -3,45,600 -3,39,800 -3,20,700

Sale Purchase of Stock - - -

Net Borrowings 12,500 -98,500 -2,03,700

Other Cash Flows from Financing Activities -200 -200 6,46,800

Total Cash Flows From Financing Activities -6,84,500 -4,38,500 1,22,400

Effect Of Exchange Rate Changes -62,800 -6,900 6,600

Change In Cash and Cash Equivalents -3,40,700 1,39,600 4,34,400

Appendix

Cash Flow(All numbers in thousands) 2017 2016 2015

Net Income 4,45,200 2,46,100 3,93,400

Operating Activities, Cash Flows Provided By or Used In

Depreciation 2,32,100 2,42,000 2,42,900

Adjustments To Net Income -62,600 1,88,200 29,400

Changes In Accounts Receivables - - -

Changes In Liabilities - - -

Changes In Inventories - - -

Changes In Other Operating Activities -55,200 71,200 -66,200

Total Cash Flow From Operating Activities 5,89,200 7,74,800 6,26,800

Investing Activities, Cash Flows Provided By or Used In

Capital Expenditures -2,93,700 -2,83,500 -2,46,400

Investments -2,000 -2,000 -2,000

Other Cash flows from Investing Activities - 90,300 -74,900

Total Cash Flows From Investing Activities -1,82,600 -1,89,800 -3,21,400

Financing Activities, Cash Flows Provided By or Used In

Dividends Paid -3,45,600 -3,39,800 -3,20,700

Sale Purchase of Stock - - -

Net Borrowings 12,500 -98,500 -2,03,700

Other Cash Flows from Financing Activities -200 -200 6,46,800

Total Cash Flows From Financing Activities -6,84,500 -4,38,500 1,22,400

Effect Of Exchange Rate Changes -62,800 -6,900 6,600

Change In Cash and Cash Equivalents -3,40,700 1,39,600 4,34,400

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.