Evaluating Contemporary Issues in Accounting: Cochlear Limited

VerifiedAdded on 2023/06/16

|14

|2361

|430

Report

AI Summary

This report evaluates the conceptual framework applied by Cochlear Limited, focusing on its adherence to recognition criteria for assets, liabilities, equities, expenses, and revenues. It examines the company's compliance with Australian Accounting Standards (AASBs) and the Corporations Act 2001, highlighting the use of net GST amounts for revenue, assets, and expenses. The report discusses the qualitative characteristics of Cochlear's financial reporting, including the reliability and faithfulness of descriptions, and the use of graphical representations. It further explores the fair measurement of derivative instruments and the annual consideration of asset impairment, concluding that Cochlear Limited demonstrates strong compliance with relevant accounting standards and effective financial reporting practices. Desklib provides this assignment as a solved example for students.

Running head: CONTEMPORARY ISSUES IN ACCOUNTING

Contemporary Issues in Accounting

Name of Student:

Name of University:

Author’s Note:

Contemporary Issues in Accounting

Name of Student:

Name of University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The study’s main objective has been discerned with the evaluation of conceptual framework

required for Cochlear Limited. The report has shown whether the concern has adhered to the

recognition for “assets, liabilities, equities, expenses and revenues”. The next section of the

learning has been able to discuss acquiescence of the company for “assets, liabilities, equities,

expenses and revenues”. It has been further able to discuss on the different aspect of the study

which is related to the qualitative characteristics depicted in the annual report. This is seen with

the several types of the depictions which are related to the reliability and faithfulness in

description of the financial events. The findings have revealed that the company has complied

with “Australian Accounting Standards (AASBs)” followed by “Australian Accounting

Standards Board and the Corporations Act 2001”. The revenue, assets and the expenses has been

based on recognition of the net GST amount. The impairment asset is further seen with annual

consideration. The fair measurement of the derivative instrument is considered with selling of the

investments. The characteristics of financial reporting is discerned with use of graphical

representation of data.

CONTEMPORARY ISSUES IN ACCOUNTING

Executive Summary

The study’s main objective has been discerned with the evaluation of conceptual framework

required for Cochlear Limited. The report has shown whether the concern has adhered to the

recognition for “assets, liabilities, equities, expenses and revenues”. The next section of the

learning has been able to discuss acquiescence of the company for “assets, liabilities, equities,

expenses and revenues”. It has been further able to discuss on the different aspect of the study

which is related to the qualitative characteristics depicted in the annual report. This is seen with

the several types of the depictions which are related to the reliability and faithfulness in

description of the financial events. The findings have revealed that the company has complied

with “Australian Accounting Standards (AASBs)” followed by “Australian Accounting

Standards Board and the Corporations Act 2001”. The revenue, assets and the expenses has been

based on recognition of the net GST amount. The impairment asset is further seen with annual

consideration. The fair measurement of the derivative instrument is considered with selling of the

investments. The characteristics of financial reporting is discerned with use of graphical

representation of data.

2

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Adherence to the objectives of the conceptual framework with its reporting.................................3

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue and

Expenses..........................................................................................................................................4

Adherence with the qualitative enhancing characteristics of financial reporting............................5

Adherence with enhancing characteristics of financial reporting....................................................6

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

List of Appendix............................................................................................................................10

CONTEMPORARY ISSUES IN ACCOUNTING

Table of Contents

Introduction......................................................................................................................................3

Adherence to the objectives of the conceptual framework with its reporting.................................3

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue and

Expenses..........................................................................................................................................4

Adherence with the qualitative enhancing characteristics of financial reporting............................5

Adherence with enhancing characteristics of financial reporting....................................................6

Conclusion.......................................................................................................................................7

References........................................................................................................................................8

List of Appendix............................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

“Cochlear Limited” was formed in 1981 with taking the finance from Australian

Government and to commercialise the implants based on pioneering done by Dr Graeme Clark.

At present the company is seen to hold more than two third of the worldwide hearing implant.

Company has been further seen to consider more than 250,000 people receiving one of

Cochlear's implants since 1982. The company has been further seen to be given as one of the

most advanced company in 2002 and 2003.The Cochlear is considered as a medical device

which is seen to design, manufacture and supply for the Cochlear implant of the Nucleas, Baha

bone conduction implant and Hybrid electro-acoustic implant.

The main objective of the study has been seen with the evaluation of conceptual

framework required for Cochlear Limited. The report has shown whether the concern has

adhered to the recognition for “assets, liabilities, equities, expenses and revenues”. The next

section of the study has been able to discuss compliance of the company for “assets, liabilities,

equities, expenses and revenues”. It has been further able to discuss on the different aspect of the

study which is related to the qualitative characteristics depicted in the annual report. This has

been seen with the various types of the depictions which are related to the reliability and

authenticity in explanation of the financial events (Karkhanis, Mack and Franklin 2013).

Adherence to the objectives of the conceptual framework with its reporting

The adherence to the Australian framework has been discerned with the compliance with

“Australian Accounting Standards Board (AASB)”. This has been conducive in the discussion of

developing of the financial report in both private and public concerns. The main concern for the

CONTEMPORARY ISSUES IN ACCOUNTING

Introduction

“Cochlear Limited” was formed in 1981 with taking the finance from Australian

Government and to commercialise the implants based on pioneering done by Dr Graeme Clark.

At present the company is seen to hold more than two third of the worldwide hearing implant.

Company has been further seen to consider more than 250,000 people receiving one of

Cochlear's implants since 1982. The company has been further seen to be given as one of the

most advanced company in 2002 and 2003.The Cochlear is considered as a medical device

which is seen to design, manufacture and supply for the Cochlear implant of the Nucleas, Baha

bone conduction implant and Hybrid electro-acoustic implant.

The main objective of the study has been seen with the evaluation of conceptual

framework required for Cochlear Limited. The report has shown whether the concern has

adhered to the recognition for “assets, liabilities, equities, expenses and revenues”. The next

section of the study has been able to discuss compliance of the company for “assets, liabilities,

equities, expenses and revenues”. It has been further able to discuss on the different aspect of the

study which is related to the qualitative characteristics depicted in the annual report. This has

been seen with the various types of the depictions which are related to the reliability and

authenticity in explanation of the financial events (Karkhanis, Mack and Franklin 2013).

Adherence to the objectives of the conceptual framework with its reporting

The adherence to the Australian framework has been discerned with the compliance with

“Australian Accounting Standards Board (AASB)”. This has been conducive in the discussion of

developing of the financial report in both private and public concerns. The main concern for the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

CONTEMPORARY ISSUES IN ACCOUNTING

contributing role of “AASB” is seen to be considered with “Australian securities and investment

commission at 2001”. As per the data issued in December 2013 by AASB the significant

amendment has been brought with “measurement, presentation, reporting entity and de-

recognition”. The important modifications are seen to be related to the facts which are

conducive in driving the main changes in associated to the Stewardship associated to the other

entities (Hammond 2014).

The information brought in by “Cochlear Limited” annual report, has been further able to

state on the varied type of the specific factors which has been considered with the “Australian

Accounting Standards (AASBs)” followed by “Australian Accounting Standards Board and the

Corporations Act 2001”. The financial statement consolidation is seen to be related to varied

types of the factors which is associated to the consolidation of the financial statement as per

“International Financial Reporting Standards (IFRS)” and interpolation done as per

“International Accounting Standards Board”. The implementation of the new measures has been

considered from 17 August 2017 (Australian Institute for Teaching and School Leadership,

2014).

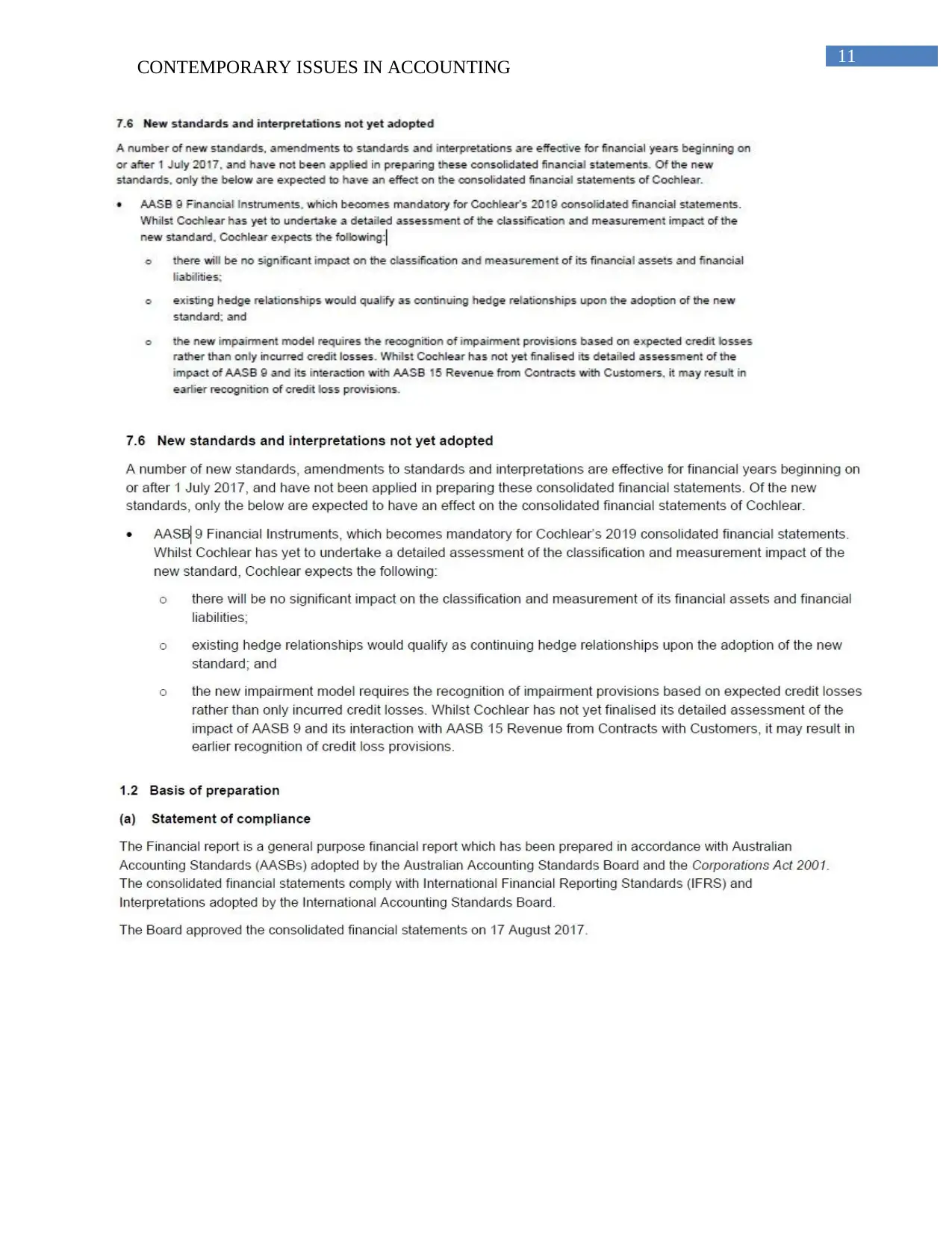

As per the annual report depiction the standards yet to be adopted has been seen with

“AASB 9 Financial Instruments”. The other standards which are yet to be seen with the

assessment has been seen to be considered with effect on “AASB 9 and its interaction with

AASB 15 Revenue from Contracts with Customers” (Robertson 2013).

CONTEMPORARY ISSUES IN ACCOUNTING

contributing role of “AASB” is seen to be considered with “Australian securities and investment

commission at 2001”. As per the data issued in December 2013 by AASB the significant

amendment has been brought with “measurement, presentation, reporting entity and de-

recognition”. The important modifications are seen to be related to the facts which are

conducive in driving the main changes in associated to the Stewardship associated to the other

entities (Hammond 2014).

The information brought in by “Cochlear Limited” annual report, has been further able to

state on the varied type of the specific factors which has been considered with the “Australian

Accounting Standards (AASBs)” followed by “Australian Accounting Standards Board and the

Corporations Act 2001”. The financial statement consolidation is seen to be related to varied

types of the factors which is associated to the consolidation of the financial statement as per

“International Financial Reporting Standards (IFRS)” and interpolation done as per

“International Accounting Standards Board”. The implementation of the new measures has been

considered from 17 August 2017 (Australian Institute for Teaching and School Leadership,

2014).

As per the annual report depiction the standards yet to be adopted has been seen with

“AASB 9 Financial Instruments”. The other standards which are yet to be seen with the

assessment has been seen to be considered with effect on “AASB 9 and its interaction with

AASB 15 Revenue from Contracts with Customers” (Robertson 2013).

5

CONTEMPORARY ISSUES IN ACCOUNTING

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue

and Expenses

The financial statement depicts of the company has been seen to be conducive in the

discussion of the several types of the facets which are seen to be associated to translation of the

company’s functional currency as per foreign exchange rates and it is considered with the date of

the transaction (Karkhanis, Mack and Franklin 2013). The financial statement adherence is done

as per IFRS necessities. This has been able to take into consideration the necessary judgement

for the assumptions and estimates for the accounting guidelines amounting for the assets,

liabilities, income and expenses. The continuing process for the ongoing process for the revisions

of the accounting estimates is seen to be recognised for the future years. The critical judgement

made for the application of the essential accounting policy has been considered with

consequence on “Employee benefit liabilities, Share based payments, Intangible assets, Business

combinations, contingent liabilities and financial risk management” (Middleton et al. 2014).

The revenue, assets and the expenses has been further seen with the acknowledgement of

the net GST amount. The impairment asset is further seen with annual consideration. The issues

for the monetary liabilities and assets has been further denominated as per foreign exchange rate

dominant on the date of reportage and functional currency at a foreign exchange rate ruling.

Adherence with the qualitative enhancing characteristics of financial reporting

In the financial note 5.6, the main provisions of the balance sheet have been seen to be

discerned with factors which are related to total number of the obligations. As per the board of

Cochlear the primary enhancing characterises of the financial report along with Board and

executive remuneration. This has been further seen to be assed as per reasonable and equitable

CONTEMPORARY ISSUES IN ACCOUNTING

Adherence with the recognition criteria for reporting Assets, Liabilities, Equity, Revenue

and Expenses

The financial statement depicts of the company has been seen to be conducive in the

discussion of the several types of the facets which are seen to be associated to translation of the

company’s functional currency as per foreign exchange rates and it is considered with the date of

the transaction (Karkhanis, Mack and Franklin 2013). The financial statement adherence is done

as per IFRS necessities. This has been able to take into consideration the necessary judgement

for the assumptions and estimates for the accounting guidelines amounting for the assets,

liabilities, income and expenses. The continuing process for the ongoing process for the revisions

of the accounting estimates is seen to be recognised for the future years. The critical judgement

made for the application of the essential accounting policy has been considered with

consequence on “Employee benefit liabilities, Share based payments, Intangible assets, Business

combinations, contingent liabilities and financial risk management” (Middleton et al. 2014).

The revenue, assets and the expenses has been further seen with the acknowledgement of

the net GST amount. The impairment asset is further seen with annual consideration. The issues

for the monetary liabilities and assets has been further denominated as per foreign exchange rate

dominant on the date of reportage and functional currency at a foreign exchange rate ruling.

Adherence with the qualitative enhancing characteristics of financial reporting

In the financial note 5.6, the main provisions of the balance sheet have been seen to be

discerned with factors which are related to total number of the obligations. As per the board of

Cochlear the primary enhancing characterises of the financial report along with Board and

executive remuneration. This has been further seen to be assed as per reasonable and equitable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

CONTEMPORARY ISSUES IN ACCOUNTING

rewards which is able to motivate successful and experienced and ongoing business to deliver the

growth meeting the expectation of the shareholders in long-term. The comprehensive statement

of income of the company has been further seen to be taken into consideration with the various

factors motivating successful team delivering the required business growth for long-term

(Karkhanis, Mack and Franklin 2015). As per the statement of comprehensive income it has been

determined that the actual portion of the changes in the fair value of net assets and cash flow

hedges. The fair measurement of the derivative instrument is considered with marketing of the

investments. It has further depicted the changes in the fair value available for selling in net profit.

This has been considered as the main form of the enhancing characteristics of the financial

report. The statement of variations of equity has been further seen to considered with the

qualitative characteristics and changes with the fair value of the cash flow hedges and net tax

(Edmonds, Cashin and Heartfield 2016).

Adherence with enhancing characteristics of financial reporting

The enhancing qualitative characteristics of Cohclear Limited has been taken into

account with the various kinds of the depiction of “KMP STI against the sales revenue and

EBIT”. The bar graph and histogram used for the comparison of “fixed, short term incentives,

deferred short term incentives and long-term incentives” has been seen as the chief form of

qualitative characteristics of learning (Food Standards Australia New Zealand 2016). As per the

income statement of the company it has been discerned that the company has been able to

present the various aspects of the data with the comparison of the earlier year. The statement of

comprehensive income released by the company has been further able to depict that the total

profit has amounted to $ 223,616 in 2017 and $ 188921 in 2016. The consideration for the

timeliness aspect has been considered with coloration and compliance as per “Australian

CONTEMPORARY ISSUES IN ACCOUNTING

rewards which is able to motivate successful and experienced and ongoing business to deliver the

growth meeting the expectation of the shareholders in long-term. The comprehensive statement

of income of the company has been further seen to be taken into consideration with the various

factors motivating successful team delivering the required business growth for long-term

(Karkhanis, Mack and Franklin 2015). As per the statement of comprehensive income it has been

determined that the actual portion of the changes in the fair value of net assets and cash flow

hedges. The fair measurement of the derivative instrument is considered with marketing of the

investments. It has further depicted the changes in the fair value available for selling in net profit.

This has been considered as the main form of the enhancing characteristics of the financial

report. The statement of variations of equity has been further seen to considered with the

qualitative characteristics and changes with the fair value of the cash flow hedges and net tax

(Edmonds, Cashin and Heartfield 2016).

Adherence with enhancing characteristics of financial reporting

The enhancing qualitative characteristics of Cohclear Limited has been taken into

account with the various kinds of the depiction of “KMP STI against the sales revenue and

EBIT”. The bar graph and histogram used for the comparison of “fixed, short term incentives,

deferred short term incentives and long-term incentives” has been seen as the chief form of

qualitative characteristics of learning (Food Standards Australia New Zealand 2016). As per the

income statement of the company it has been discerned that the company has been able to

present the various aspects of the data with the comparison of the earlier year. The statement of

comprehensive income released by the company has been further able to depict that the total

profit has amounted to $ 223,616 in 2017 and $ 188921 in 2016. The consideration for the

timeliness aspect has been considered with coloration and compliance as per “Australian

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

CONTEMPORARY ISSUES IN ACCOUNTING

Accounting Standards (AASBs)” on 17th August 2017 (Lagakos et al. 2014). The notes as per

financial statement has been able to consider “assets, liabilities in both present and previous

year”. For an enhanced comparison of results and employee benefit has been interpreted in 2016

and 2017. Performance and fair value has been considered with the depicted with “EPS

performance based conditions, TSR based conditions and deferred STI service based

conditions”. This comparison has been seen to be done on monthly (Groeller et al. 2015).

Conclusion

The study has inferred that the Cochlear has been able to comply with “Australian

Accounting Standards (AASBs)” followed by “Australian Accounting Standards Board and the

Corporations Act 2001”. The financial statement consolidation has been further seen to be

related to varied types of the factors which is associated to the consolidation of the financial

statement as per “International Financial Reporting Standards (IFRS)”. It has been further

discerned that “Assets, Liabilities, Equity, Revenue and Expenses” of the company has been

discerned with translation of the company’s functional currency as per foreign exchange rates

and it is considered with the date of the transaction. Qualitative enhancing characteristics of

financial reporting has been depicted in terms of fair measurement of the derivative instrument

for selling of the investments. Enhancing characteristics of financial reporting has been discerned

with bar graph and histogram used for the comparison of “fixed, short term incentives, deferred

short term incentives and long-term incentives”.

CONTEMPORARY ISSUES IN ACCOUNTING

Accounting Standards (AASBs)” on 17th August 2017 (Lagakos et al. 2014). The notes as per

financial statement has been able to consider “assets, liabilities in both present and previous

year”. For an enhanced comparison of results and employee benefit has been interpreted in 2016

and 2017. Performance and fair value has been considered with the depicted with “EPS

performance based conditions, TSR based conditions and deferred STI service based

conditions”. This comparison has been seen to be done on monthly (Groeller et al. 2015).

Conclusion

The study has inferred that the Cochlear has been able to comply with “Australian

Accounting Standards (AASBs)” followed by “Australian Accounting Standards Board and the

Corporations Act 2001”. The financial statement consolidation has been further seen to be

related to varied types of the factors which is associated to the consolidation of the financial

statement as per “International Financial Reporting Standards (IFRS)”. It has been further

discerned that “Assets, Liabilities, Equity, Revenue and Expenses” of the company has been

discerned with translation of the company’s functional currency as per foreign exchange rates

and it is considered with the date of the transaction. Qualitative enhancing characteristics of

financial reporting has been depicted in terms of fair measurement of the derivative instrument

for selling of the investments. Enhancing characteristics of financial reporting has been discerned

with bar graph and histogram used for the comparison of “fixed, short term incentives, deferred

short term incentives and long-term incentives”.

8

CONTEMPORARY ISSUES IN ACCOUNTING

References

Australian Institute for Teaching and School Leadership, Teaching, A. and Leadership, S. (2014)

‘Australian Professional Standards for Teachers’, Education Services Australia, pp. 1–28. doi:

10.1177/002248715901000125.

Edmonds, L., Cashin, A. and Heartfield, M. (2016) ‘Comparison of Australian specialty nurse

standards with registered nurse standards’, International Nursing Review, 63(2), pp. 162–179.

doi: 10.1111/inr.12235.

Food Standards Australia New Zealand (2016) Food standards code, Food Standards Australia

New Zealand. Available at: http://www.foodstandards.gov.au/code/Pages/default.aspx

%0Ahttp://www.foodstandards.gov.au/code/Pages/default.aspx

%5Cnwww.foodstandards.gov.au.

Groeller, H., Fullagar, H. H. K., Sampson, J. A., Mott, B. J. and Taylor, N. A. S. (2015)

‘Employment Standards for Australian Urban Firefighters’, Journal of Occupational and

Environmental Medicine, 57(10), pp. 1083–1091. doi: 10.1097/JOM.0000000000000527.

Hammond, J. (2014) ‘An Australian perspective on standards-based education, teacher

knowledge, and students of english as an additional language’, TESOL Quarterly, 48(3), pp.

507–532. doi: 10.1002/tesq.173.

CONTEMPORARY ISSUES IN ACCOUNTING

References

Australian Institute for Teaching and School Leadership, Teaching, A. and Leadership, S. (2014)

‘Australian Professional Standards for Teachers’, Education Services Australia, pp. 1–28. doi:

10.1177/002248715901000125.

Edmonds, L., Cashin, A. and Heartfield, M. (2016) ‘Comparison of Australian specialty nurse

standards with registered nurse standards’, International Nursing Review, 63(2), pp. 162–179.

doi: 10.1111/inr.12235.

Food Standards Australia New Zealand (2016) Food standards code, Food Standards Australia

New Zealand. Available at: http://www.foodstandards.gov.au/code/Pages/default.aspx

%0Ahttp://www.foodstandards.gov.au/code/Pages/default.aspx

%5Cnwww.foodstandards.gov.au.

Groeller, H., Fullagar, H. H. K., Sampson, J. A., Mott, B. J. and Taylor, N. A. S. (2015)

‘Employment Standards for Australian Urban Firefighters’, Journal of Occupational and

Environmental Medicine, 57(10), pp. 1083–1091. doi: 10.1097/JOM.0000000000000527.

Hammond, J. (2014) ‘An Australian perspective on standards-based education, teacher

knowledge, and students of english as an additional language’, TESOL Quarterly, 48(3), pp.

507–532. doi: 10.1002/tesq.173.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

CONTEMPORARY ISSUES IN ACCOUNTING

Karkhanis, S., Mack, P. and Franklin, D. (2013) ‘Age estimation standards for a Western

Australian population using the coronal pulp cavity index’, Forensic Science International,

231(1–3). doi: 10.1016/j.forsciint.2013.04.004.

Karkhanis, S., Mack, P. and Franklin, D. (2015) ‘Dental age estimation standards for a Western

Australian population’, Forensic Science International, 257, p. 509.e1-509.e9. doi:

10.1016/j.forsciint.2015.06.021.

Lagakos, B. D., Moll, B., Porzio, T. and Qian, N. (2014) ‘Experience Matters: Human Capital

and Development Accouting’, NBER Working Paper Series, Working Pa. doi: 10.3386/w18602.

Middleton, P. G., Wagenaar, M., Matson, A. G., Craig, M. E., Holmes-Walker, D. J., Katz, T.

and Hameed, S. (2014) ‘Australian standards of care for cystic fibrosis-related diabetes’,

Respirology, 19(2), pp. 185–192. doi: 10.1111/resp.12227.

Robertson, J. (2013) ‘Australian forensic science reaches new standards!’, Australian Journal of

Forensic Sciences, pp. 345–346. doi: 10.1080/00450618.2013.859730.

CONTEMPORARY ISSUES IN ACCOUNTING

Karkhanis, S., Mack, P. and Franklin, D. (2013) ‘Age estimation standards for a Western

Australian population using the coronal pulp cavity index’, Forensic Science International,

231(1–3). doi: 10.1016/j.forsciint.2013.04.004.

Karkhanis, S., Mack, P. and Franklin, D. (2015) ‘Dental age estimation standards for a Western

Australian population’, Forensic Science International, 257, p. 509.e1-509.e9. doi:

10.1016/j.forsciint.2015.06.021.

Lagakos, B. D., Moll, B., Porzio, T. and Qian, N. (2014) ‘Experience Matters: Human Capital

and Development Accouting’, NBER Working Paper Series, Working Pa. doi: 10.3386/w18602.

Middleton, P. G., Wagenaar, M., Matson, A. G., Craig, M. E., Holmes-Walker, D. J., Katz, T.

and Hameed, S. (2014) ‘Australian standards of care for cystic fibrosis-related diabetes’,

Respirology, 19(2), pp. 185–192. doi: 10.1111/resp.12227.

Robertson, J. (2013) ‘Australian forensic science reaches new standards!’, Australian Journal of

Forensic Sciences, pp. 345–346. doi: 10.1080/00450618.2013.859730.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

CONTEMPORARY ISSUES IN ACCOUNTING

List of Appendix

CONTEMPORARY ISSUES IN ACCOUNTING

List of Appendix

11

CONTEMPORARY ISSUES IN ACCOUNTING

CONTEMPORARY ISSUES IN ACCOUNTING

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.