Analysis of Management Accounting Strategies: Coffeegreen and Galaxy

VerifiedAdded on 2021/11/19

|21

|4926

|36

Report

AI Summary

This report provides a detailed analysis of the management accounting practices of two companies, Coffeegreen and Galaxy, focusing on their financial data and decision-making processes. The report examines various planning tools like standard costs, budgets, and the balanced scorecard, evaluating their advantages and disadvantages. It includes calculations for contract costs, standard costs, and revenue maximization, along with a comprehensive monthly budget analysis for sales revenue, production volume, and resource costs. Furthermore, the report addresses cost variances and provides recommendations for improvement, including employee compensation and training. Finally, the report analyzes the PEST factors affecting the companies' operations.

TRAN DANG BAO TRAM _ 10190651 _ MA2.1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

A. INTRODUCTION

Management accounting (MA) is a method of giving financial data and information to

managers for use in making decisions inside a company. A corporation may make the

best option to handle any problem by using MA methodologies and tools. This

research examines the strategies of two companies, Coffeegreen and Galaxy, in order

to assess their expenses, financial aspects, and accounting management procedures.

Management accounting (MA) is a method of giving financial data and information to

managers for use in making decisions inside a company. A corporation may make the

best option to handle any problem by using MA methodologies and tools. This

research examines the strategies of two companies, Coffeegreen and Galaxy, in order

to assess their expenses, financial aspects, and accounting management procedures.

B. MAJOR FINDING

I. SCENARIO 1:

Question 1: Advantages and disadvantages of planning tools for Coffeegreen

a, Definition

Standard costs: is an essentrial subtopic of cost accounting. Standard costs have

historically been connected with the expenses of raw materials, direct labor, and

manufacturing overhead in a manufacturing organization (Accounting Coach,

n.d.).

Standard price: is the price per unit of input that has been precisely calculated

(Horngren, C.Datar.M. & Rajan.M., 2015).

Budget: is a forecast of revenue and spending for a certain future period of time

that is generally prepared and updated on a regular basis. Budgets may be created

for an individual, a group of individuals, a company, a government (Investopedia,

2021).

Balanced Scorecard: The BSC framework is built on a balance of leading and

lagging indicators, which may be thought of as the drivers and results of your

company's objectives, respectively. These important indicators, when utilized in

the Balanced Scorecard framework, tell you if you're on pace to meet your

objectives and if you're on track to meet future objectives (Jackson, n.d.)

b, The advantages and disadvantages of each planning tool

PLANNING TOOLS ADVANTAGES DISADVANTAGES

Standard cost Improved cost control:

establishing standards for

each type of expense

incurred, then highlighting

exceptions or variances—

cases where things did not go

as planned.

More useful data for

managerial planning and

Contentious materiality

limits for variances: Each

organization's management

must establish different

material limits, which may

result in process conflicts or

problems.

Non-reporting of some

variations: Employees may

I. SCENARIO 1:

Question 1: Advantages and disadvantages of planning tools for Coffeegreen

a, Definition

Standard costs: is an essentrial subtopic of cost accounting. Standard costs have

historically been connected with the expenses of raw materials, direct labor, and

manufacturing overhead in a manufacturing organization (Accounting Coach,

n.d.).

Standard price: is the price per unit of input that has been precisely calculated

(Horngren, C.Datar.M. & Rajan.M., 2015).

Budget: is a forecast of revenue and spending for a certain future period of time

that is generally prepared and updated on a regular basis. Budgets may be created

for an individual, a group of individuals, a company, a government (Investopedia,

2021).

Balanced Scorecard: The BSC framework is built on a balance of leading and

lagging indicators, which may be thought of as the drivers and results of your

company's objectives, respectively. These important indicators, when utilized in

the Balanced Scorecard framework, tell you if you're on pace to meet your

objectives and if you're on track to meet future objectives (Jackson, n.d.)

b, The advantages and disadvantages of each planning tool

PLANNING TOOLS ADVANTAGES DISADVANTAGES

Standard cost Improved cost control:

establishing standards for

each type of expense

incurred, then highlighting

exceptions or variances—

cases where things did not go

as planned.

More useful data for

managerial planning and

Contentious materiality

limits for variances: Each

organization's management

must establish different

material limits, which may

result in process conflicts or

problems.

Non-reporting of some

variations: Employees may

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decesion making: preparing

precise budgets and assessing

costs in order to bid on jobs.

Costs of production could

be reduced: Employees may

become more cost conscious

as a result of standard costs,

and seek out better ways to

complete their tasks.

not disclose or seek to

mitigate unfavorable

expenditure exceptions in

order to conceal inefficiency

and reduce budgeting

effectiveness.

Maybe low moral with some

employees: Low

performance often receives

more attention than high

performance because

management focuses on

unfavorable variances and

ignores favorable variances.

(course.lumenlearning.com, n.d.)

Standard price Selecting the best vendors:

Choosing the most

appropriate suppliers based

on price and material quality.

Adding more advantages:

Increasing last revenue by

lowering input costs is

possible.

To set aside funds for risk:

Provide background

information and data on how

to build an emergency fund

by fixing prices. • The

entry cost can be easily

controlled by the company.

It is a difficult situation to

deal with.

It was necessary for the

company to have extensive

knowledge of the market and

industry.

precise budgets and assessing

costs in order to bid on jobs.

Costs of production could

be reduced: Employees may

become more cost conscious

as a result of standard costs,

and seek out better ways to

complete their tasks.

not disclose or seek to

mitigate unfavorable

expenditure exceptions in

order to conceal inefficiency

and reduce budgeting

effectiveness.

Maybe low moral with some

employees: Low

performance often receives

more attention than high

performance because

management focuses on

unfavorable variances and

ignores favorable variances.

(course.lumenlearning.com, n.d.)

Standard price Selecting the best vendors:

Choosing the most

appropriate suppliers based

on price and material quality.

Adding more advantages:

Increasing last revenue by

lowering input costs is

possible.

To set aside funds for risk:

Provide background

information and data on how

to build an emergency fund

by fixing prices. • The

entry cost can be easily

controlled by the company.

It is a difficult situation to

deal with.

It was necessary for the

company to have extensive

knowledge of the market and

industry.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

(Blocher, Stout, Cokins, 2010)

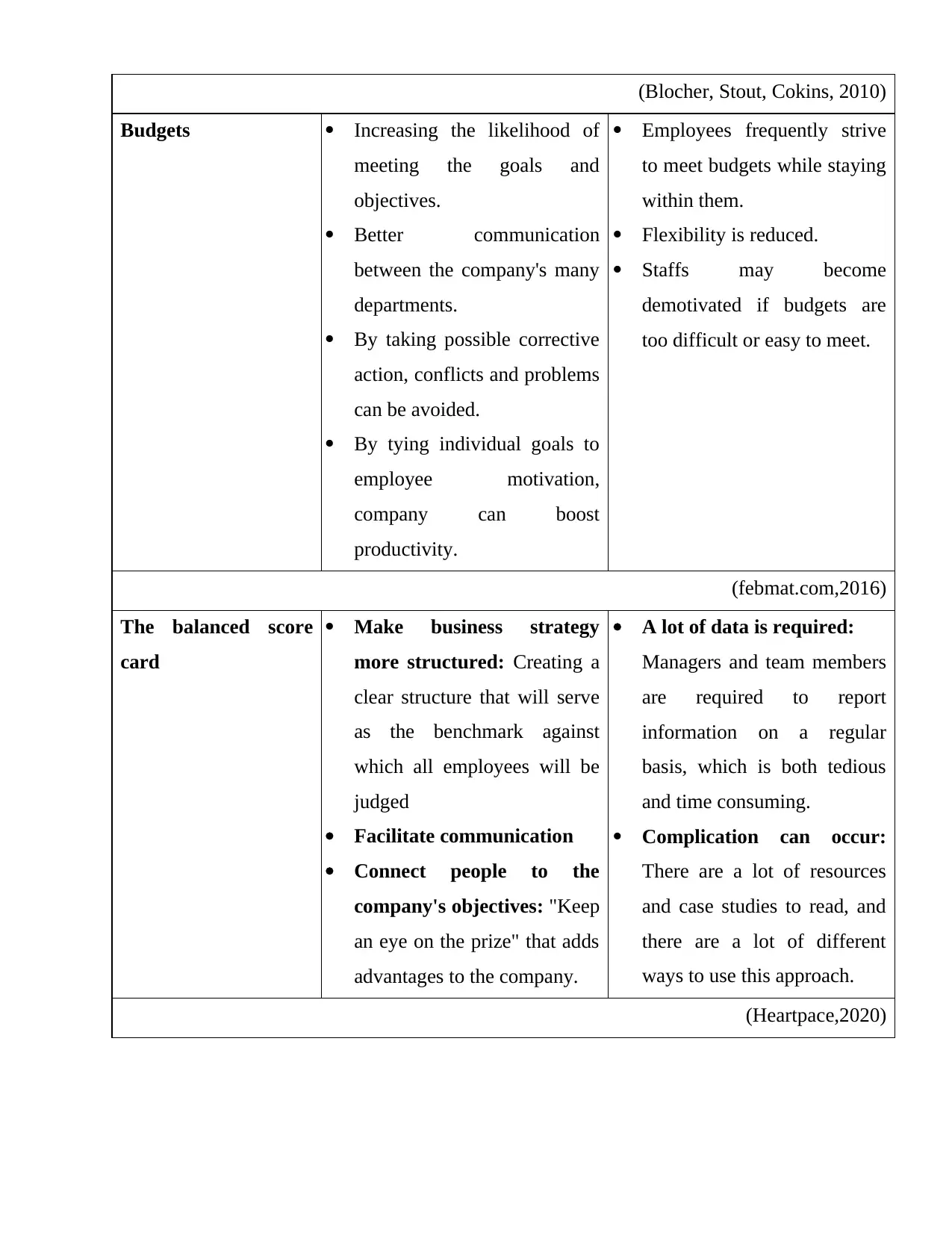

Budgets Increasing the likelihood of

meeting the goals and

objectives.

Better communication

between the company's many

departments.

By taking possible corrective

action, conflicts and problems

can be avoided.

By tying individual goals to

employee motivation,

company can boost

productivity.

Employees frequently strive

to meet budgets while staying

within them.

Flexibility is reduced.

Staffs may become

demotivated if budgets are

too difficult or easy to meet.

(febmat.com,2016)

The balanced score

card

Make business strategy

more structured: Creating a

clear structure that will serve

as the benchmark against

which all employees will be

judged

Facilitate communication

Connect people to the

company's objectives: "Keep

an eye on the prize" that adds

advantages to the company.

A lot of data is required:

Managers and team members

are required to report

information on a regular

basis, which is both tedious

and time consuming.

Complication can occur:

There are a lot of resources

and case studies to read, and

there are a lot of different

ways to use this approach.

(Heartpace,2020)

Budgets Increasing the likelihood of

meeting the goals and

objectives.

Better communication

between the company's many

departments.

By taking possible corrective

action, conflicts and problems

can be avoided.

By tying individual goals to

employee motivation,

company can boost

productivity.

Employees frequently strive

to meet budgets while staying

within them.

Flexibility is reduced.

Staffs may become

demotivated if budgets are

too difficult or easy to meet.

(febmat.com,2016)

The balanced score

card

Make business strategy

more structured: Creating a

clear structure that will serve

as the benchmark against

which all employees will be

judged

Facilitate communication

Connect people to the

company's objectives: "Keep

an eye on the prize" that adds

advantages to the company.

A lot of data is required:

Managers and team members

are required to report

information on a regular

basis, which is both tedious

and time consuming.

Complication can occur:

There are a lot of resources

and case studies to read, and

there are a lot of different

ways to use this approach.

(Heartpace,2020)

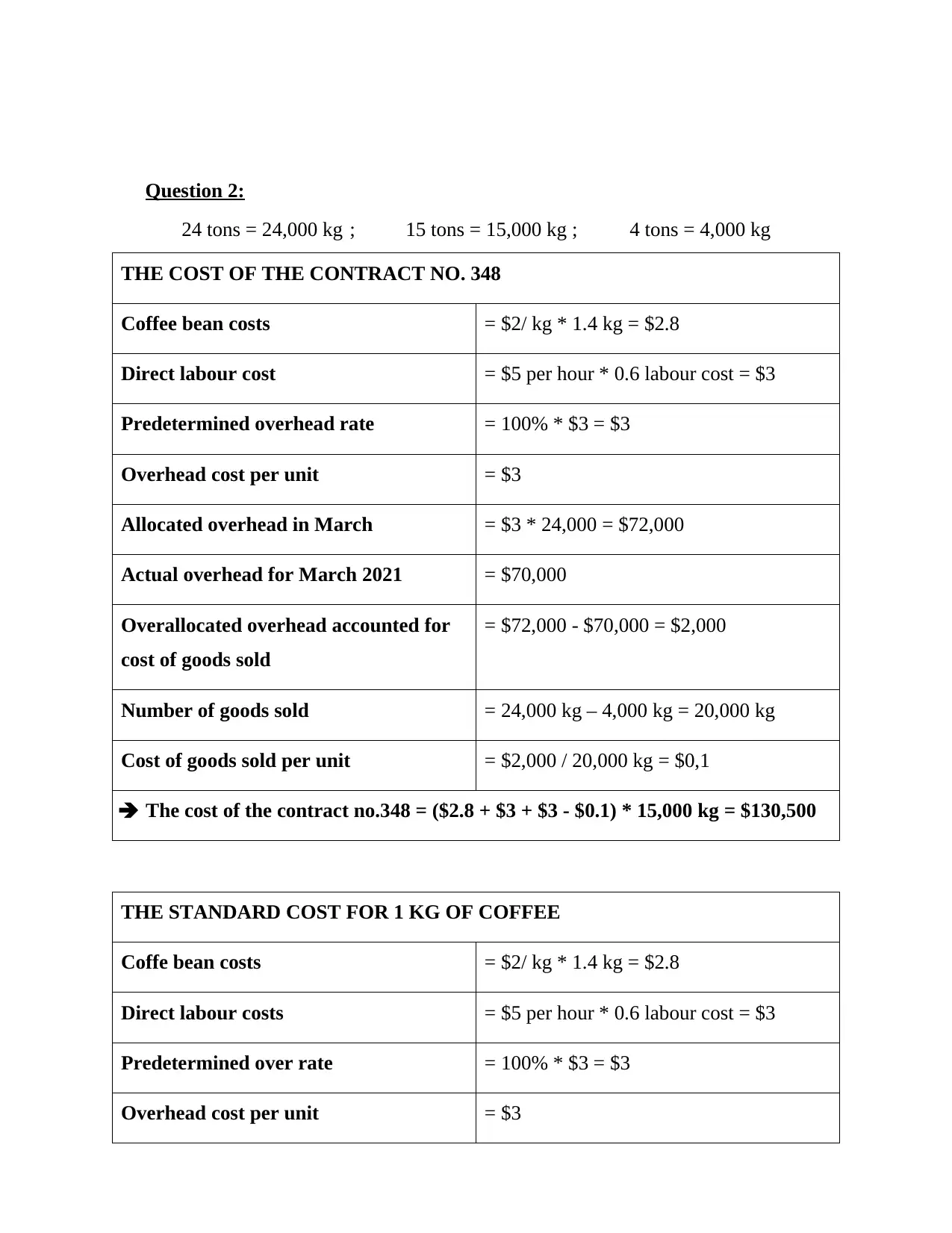

Question 2:

24 tons = 24,000 kg ; 15 tons = 15,000 kg ; 4 tons = 4,000 kg

THE COST OF THE CONTRACT NO. 348

Coffee bean costs = $2/ kg * 1.4 kg = $2.8

Direct labour cost = $5 per hour * 0.6 labour cost = $3

Predetermined overhead rate = 100% * $3 = $3

Overhead cost per unit = $3

Allocated overhead in March = $3 * 24,000 = $72,000

Actual overhead for March 2021 = $70,000

Overallocated overhead accounted for

cost of goods sold

= $72,000 - $70,000 = $2,000

Number of goods sold = 24,000 kg – 4,000 kg = 20,000 kg

Cost of goods sold per unit = $2,000 / 20,000 kg = $0,1

The cost of the contract no.348 = ($2.8 + $3 + $3 - $0.1) * 15,000 kg = $130,500

THE STANDARD COST FOR 1 KG OF COFFEE

Coffe bean costs = $2/ kg * 1.4 kg = $2.8

Direct labour costs = $5 per hour * 0.6 labour cost = $3

Predetermined over rate = 100% * $3 = $3

Overhead cost per unit = $3

24 tons = 24,000 kg ; 15 tons = 15,000 kg ; 4 tons = 4,000 kg

THE COST OF THE CONTRACT NO. 348

Coffee bean costs = $2/ kg * 1.4 kg = $2.8

Direct labour cost = $5 per hour * 0.6 labour cost = $3

Predetermined overhead rate = 100% * $3 = $3

Overhead cost per unit = $3

Allocated overhead in March = $3 * 24,000 = $72,000

Actual overhead for March 2021 = $70,000

Overallocated overhead accounted for

cost of goods sold

= $72,000 - $70,000 = $2,000

Number of goods sold = 24,000 kg – 4,000 kg = 20,000 kg

Cost of goods sold per unit = $2,000 / 20,000 kg = $0,1

The cost of the contract no.348 = ($2.8 + $3 + $3 - $0.1) * 15,000 kg = $130,500

THE STANDARD COST FOR 1 KG OF COFFEE

Coffe bean costs = $2/ kg * 1.4 kg = $2.8

Direct labour costs = $5 per hour * 0.6 labour cost = $3

Predetermined over rate = 100% * $3 = $3

Overhead cost per unit = $3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

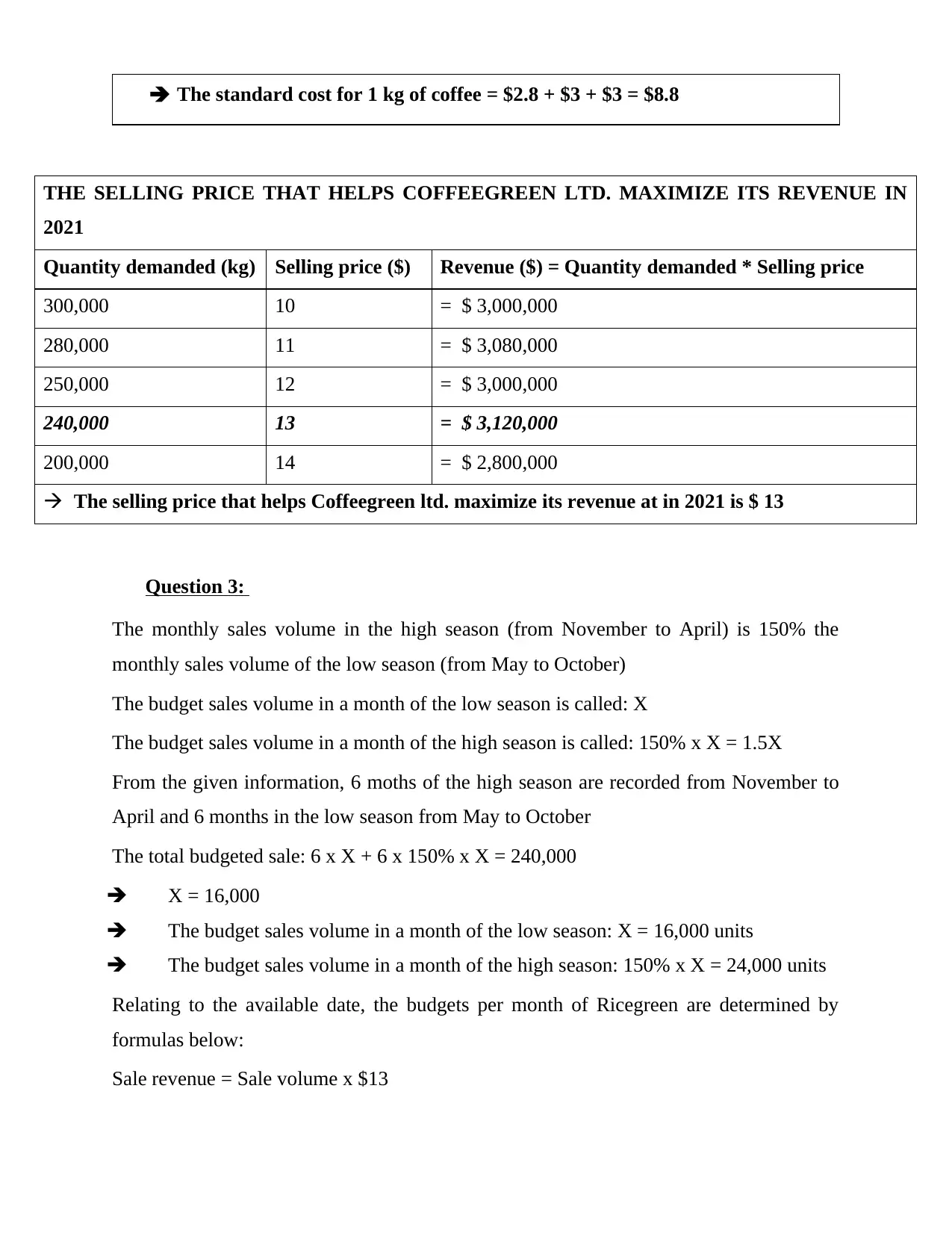

The standard cost for 1 kg of coffee = $2.8 + $3 + $3 = $8.8

THE SELLING PRICE THAT HELPS COFFEEGREEN LTD. MAXIMIZE ITS REVENUE IN

2021

Quantity demanded (kg) Selling price ($) Revenue ($) = Quantity demanded * Selling price

300,000 10 = $ 3,000,000

280,000 11 = $ 3,080,000

250,000 12 = $ 3,000,000

240,000 13 = $ 3,120,000

200,000 14 = $ 2,800,000

The selling price that helps Coffeegreen ltd. maximize its revenue at in 2021 is $ 13

Question 3:

The monthly sales volume in the high season (from November to April) is 150% the

monthly sales volume of the low season (from May to October)

The budget sales volume in a month of the low season is called: X

The budget sales volume in a month of the high season is called: 150% x X = 1.5X

From the given information, 6 moths of the high season are recorded from November to

April and 6 months in the low season from May to October

The total budgeted sale: 6 x X + 6 x 150% x X = 240,000

X = 16,000

The budget sales volume in a month of the low season: X = 16,000 units

The budget sales volume in a month of the high season: 150% x X = 24,000 units

Relating to the available date, the budgets per month of Ricegreen are determined by

formulas below:

Sale revenue = Sale volume x $13

THE SELLING PRICE THAT HELPS COFFEEGREEN LTD. MAXIMIZE ITS REVENUE IN

2021

Quantity demanded (kg) Selling price ($) Revenue ($) = Quantity demanded * Selling price

300,000 10 = $ 3,000,000

280,000 11 = $ 3,080,000

250,000 12 = $ 3,000,000

240,000 13 = $ 3,120,000

200,000 14 = $ 2,800,000

The selling price that helps Coffeegreen ltd. maximize its revenue at in 2021 is $ 13

Question 3:

The monthly sales volume in the high season (from November to April) is 150% the

monthly sales volume of the low season (from May to October)

The budget sales volume in a month of the low season is called: X

The budget sales volume in a month of the high season is called: 150% x X = 1.5X

From the given information, 6 moths of the high season are recorded from November to

April and 6 months in the low season from May to October

The total budgeted sale: 6 x X + 6 x 150% x X = 240,000

X = 16,000

The budget sales volume in a month of the low season: X = 16,000 units

The budget sales volume in a month of the high season: 150% x X = 24,000 units

Relating to the available date, the budgets per month of Ricegreen are determined by

formulas below:

Sale revenue = Sale volume x $13

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

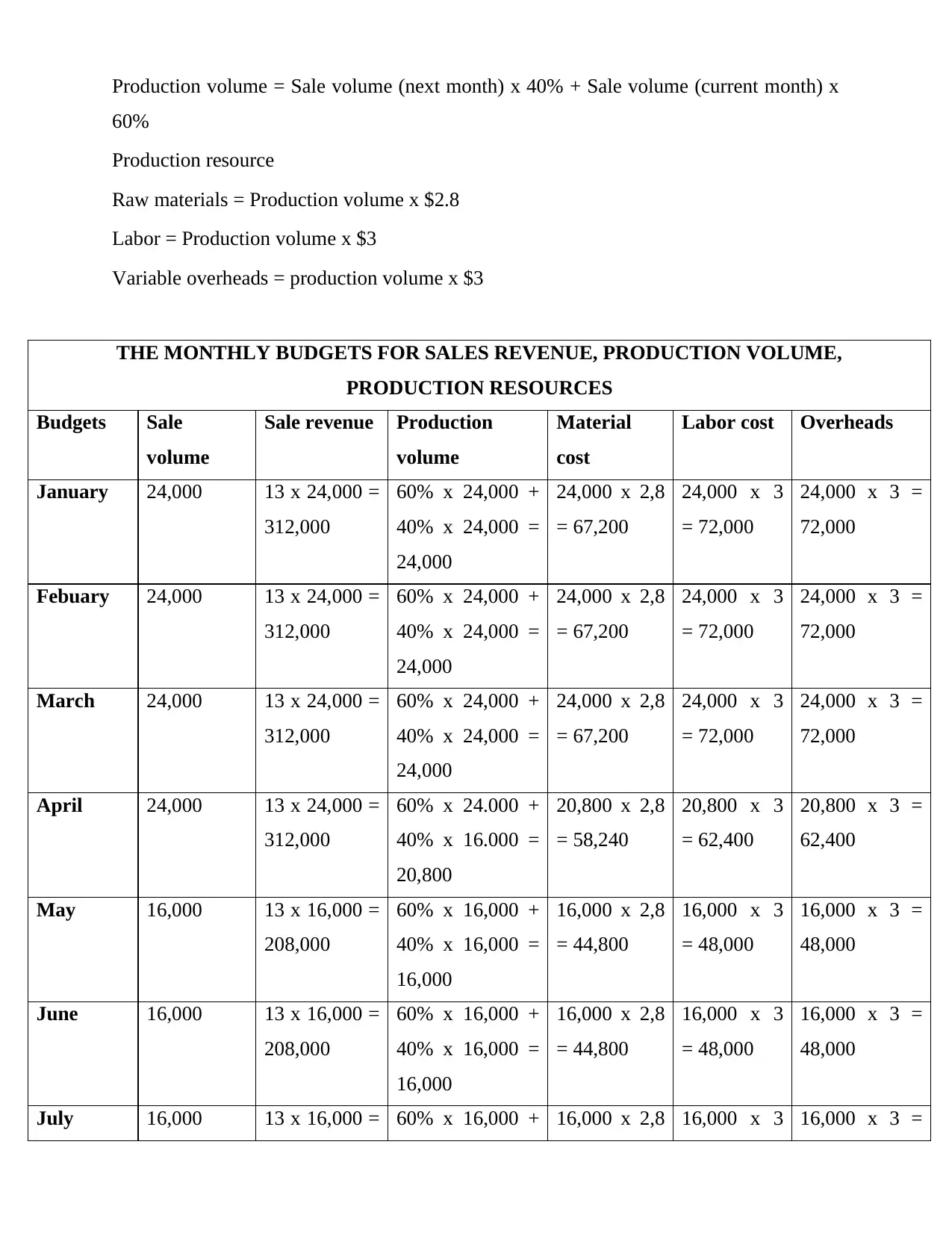

Production volume = Sale volume (next month) x 40% + Sale volume (current month) x

60%

Production resource

Raw materials = Production volume x $2.8

Labor = Production volume x $3

Variable overheads = production volume x $3

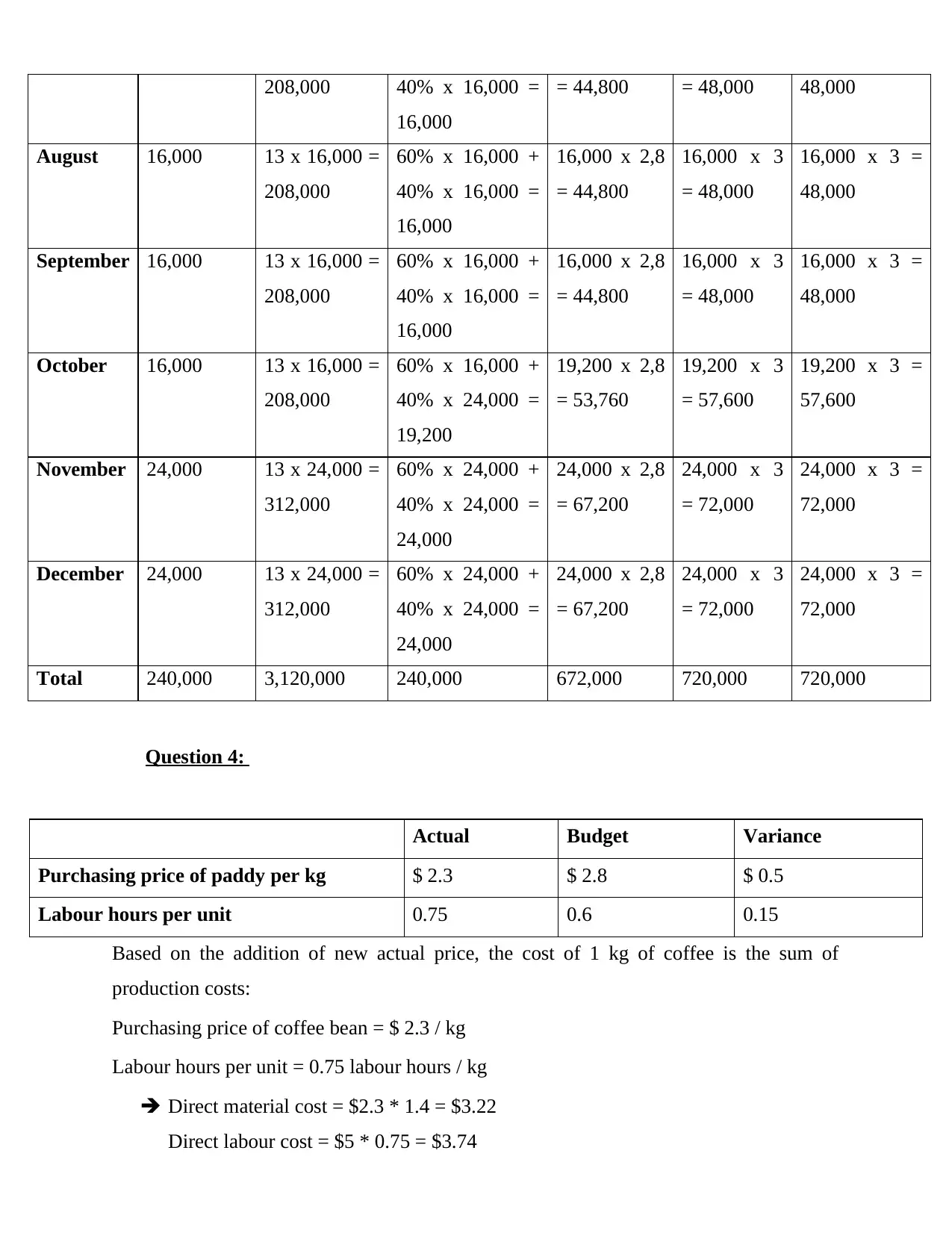

THE MONTHLY BUDGETS FOR SALES REVENUE, PRODUCTION VOLUME,

PRODUCTION RESOURCES

Budgets Sale

volume

Sale revenue Production

volume

Material

cost

Labor cost Overheads

January 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

Febuary 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

March 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

April 24,000 13 x 24,000 =

312,000

60% x 24.000 +

40% x 16.000 =

20,800

20,800 x 2,8

= 58,240

20,800 x 3

= 62,400

20,800 x 3 =

62,400

May 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

June 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

July 16,000 13 x 16,000 = 60% x 16,000 + 16,000 x 2,8 16,000 x 3 16,000 x 3 =

60%

Production resource

Raw materials = Production volume x $2.8

Labor = Production volume x $3

Variable overheads = production volume x $3

THE MONTHLY BUDGETS FOR SALES REVENUE, PRODUCTION VOLUME,

PRODUCTION RESOURCES

Budgets Sale

volume

Sale revenue Production

volume

Material

cost

Labor cost Overheads

January 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

Febuary 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

March 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

April 24,000 13 x 24,000 =

312,000

60% x 24.000 +

40% x 16.000 =

20,800

20,800 x 2,8

= 58,240

20,800 x 3

= 62,400

20,800 x 3 =

62,400

May 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

June 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

July 16,000 13 x 16,000 = 60% x 16,000 + 16,000 x 2,8 16,000 x 3 16,000 x 3 =

208,000 40% x 16,000 =

16,000

= 44,800 = 48,000 48,000

August 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

September 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

October 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 24,000 =

19,200

19,200 x 2,8

= 53,760

19,200 x 3

= 57,600

19,200 x 3 =

57,600

November 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

December 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

Total 240,000 3,120,000 240,000 672,000 720,000 720,000

Question 4:

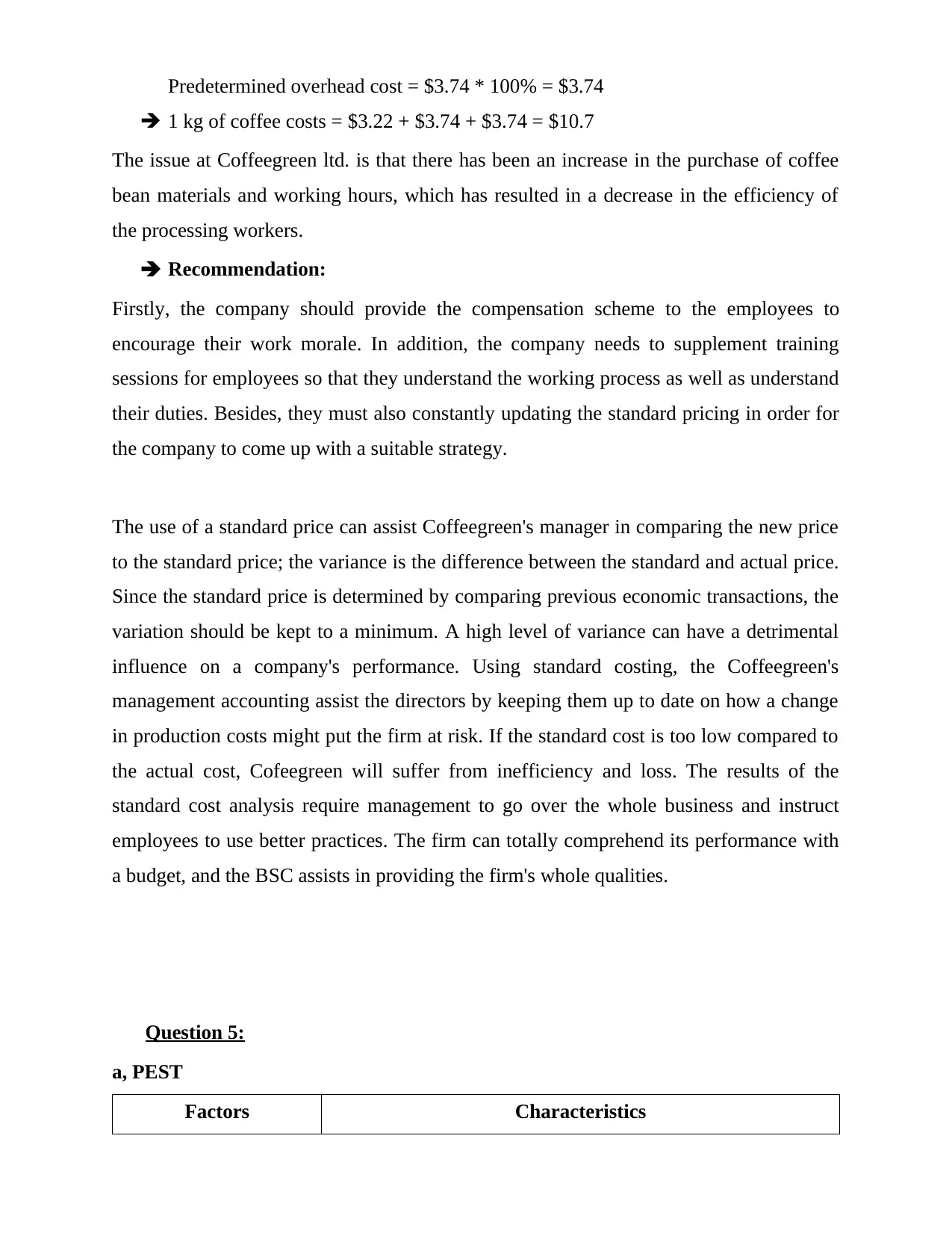

Actual Budget Variance

Purchasing price of paddy per kg $ 2.3 $ 2.8 $ 0.5

Labour hours per unit 0.75 0.6 0.15

Based on the addition of new actual price, the cost of 1 kg of coffee is the sum of

production costs:

Purchasing price of coffee bean = $ 2.3 / kg

Labour hours per unit = 0.75 labour hours / kg

Direct material cost = $2.3 * 1.4 = $3.22

Direct labour cost = $5 * 0.75 = $3.74

16,000

= 44,800 = 48,000 48,000

August 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

September 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 16,000 =

16,000

16,000 x 2,8

= 44,800

16,000 x 3

= 48,000

16,000 x 3 =

48,000

October 16,000 13 x 16,000 =

208,000

60% x 16,000 +

40% x 24,000 =

19,200

19,200 x 2,8

= 53,760

19,200 x 3

= 57,600

19,200 x 3 =

57,600

November 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

December 24,000 13 x 24,000 =

312,000

60% x 24,000 +

40% x 24,000 =

24,000

24,000 x 2,8

= 67,200

24,000 x 3

= 72,000

24,000 x 3 =

72,000

Total 240,000 3,120,000 240,000 672,000 720,000 720,000

Question 4:

Actual Budget Variance

Purchasing price of paddy per kg $ 2.3 $ 2.8 $ 0.5

Labour hours per unit 0.75 0.6 0.15

Based on the addition of new actual price, the cost of 1 kg of coffee is the sum of

production costs:

Purchasing price of coffee bean = $ 2.3 / kg

Labour hours per unit = 0.75 labour hours / kg

Direct material cost = $2.3 * 1.4 = $3.22

Direct labour cost = $5 * 0.75 = $3.74

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Predetermined overhead cost = $3.74 * 100% = $3.74

1 kg of coffee costs = $3.22 + $3.74 + $3.74 = $10.7

The issue at Coffeegreen ltd. is that there has been an increase in the purchase of coffee

bean materials and working hours, which has resulted in a decrease in the efficiency of

the processing workers.

Recommendation:

Firstly, the company should provide the compensation scheme to the employees to

encourage their work morale. In addition, the company needs to supplement training

sessions for employees so that they understand the working process as well as understand

their duties. Besides, they must also constantly updating the standard pricing in order for

the company to come up with a suitable strategy.

The use of a standard price can assist Coffeegreen's manager in comparing the new price

to the standard price; the variance is the difference between the standard and actual price.

Since the standard price is determined by comparing previous economic transactions, the

variation should be kept to a minimum. A high level of variance can have a detrimental

influence on a company's performance. Using standard costing, the Coffeegreen's

management accounting assist the directors by keeping them up to date on how a change

in production costs might put the firm at risk. If the standard cost is too low compared to

the actual cost, Cofeegreen will suffer from inefficiency and loss. The results of the

standard cost analysis require management to go over the whole business and instruct

employees to use better practices. The firm can totally comprehend its performance with

a budget, and the BSC assists in providing the firm's whole qualities.

Question 5:

a, PEST

Factors Characteristics

1 kg of coffee costs = $3.22 + $3.74 + $3.74 = $10.7

The issue at Coffeegreen ltd. is that there has been an increase in the purchase of coffee

bean materials and working hours, which has resulted in a decrease in the efficiency of

the processing workers.

Recommendation:

Firstly, the company should provide the compensation scheme to the employees to

encourage their work morale. In addition, the company needs to supplement training

sessions for employees so that they understand the working process as well as understand

their duties. Besides, they must also constantly updating the standard pricing in order for

the company to come up with a suitable strategy.

The use of a standard price can assist Coffeegreen's manager in comparing the new price

to the standard price; the variance is the difference between the standard and actual price.

Since the standard price is determined by comparing previous economic transactions, the

variation should be kept to a minimum. A high level of variance can have a detrimental

influence on a company's performance. Using standard costing, the Coffeegreen's

management accounting assist the directors by keeping them up to date on how a change

in production costs might put the firm at risk. If the standard cost is too low compared to

the actual cost, Cofeegreen will suffer from inefficiency and loss. The results of the

standard cost analysis require management to go over the whole business and instruct

employees to use better practices. The firm can totally comprehend its performance with

a budget, and the BSC assists in providing the firm's whole qualities.

Question 5:

a, PEST

Factors Characteristics

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

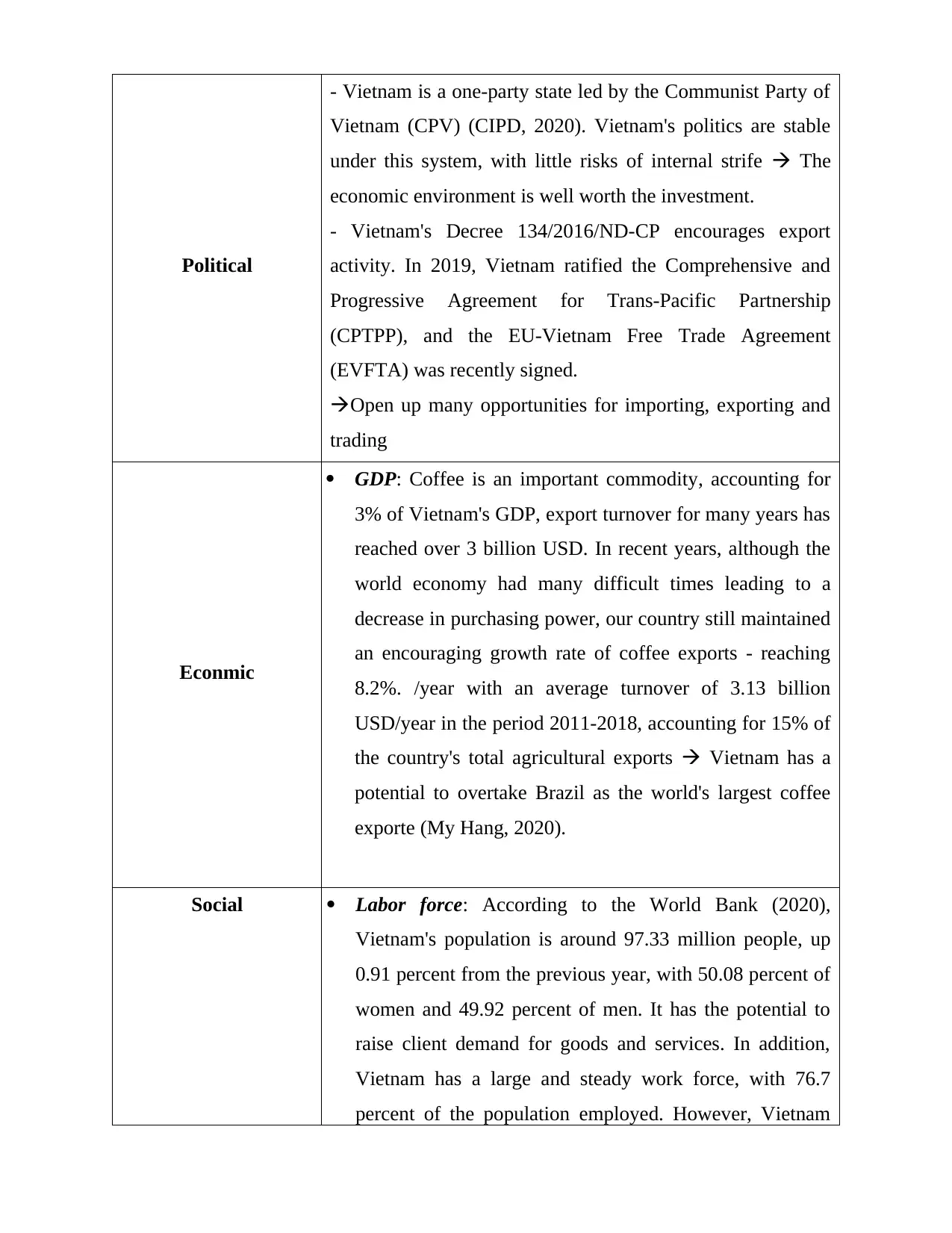

Political

- Vietnam is a one-party state led by the Communist Party of

Vietnam (CPV) (CIPD, 2020). Vietnam's politics are stable

under this system, with little risks of internal strife The

economic environment is well worth the investment.

- Vietnam's Decree 134/2016/ND-CP encourages export

activity. In 2019, Vietnam ratified the Comprehensive and

Progressive Agreement for Trans-Pacific Partnership

(CPTPP), and the EU-Vietnam Free Trade Agreement

(EVFTA) was recently signed.

Open up many opportunities for importing, exporting and

trading

Econmic

GDP: Coffee is an important commodity, accounting for

3% of Vietnam's GDP, export turnover for many years has

reached over 3 billion USD. In recent years, although the

world economy had many difficult times leading to a

decrease in purchasing power, our country still maintained

an encouraging growth rate of coffee exports - reaching

8.2%. /year with an average turnover of 3.13 billion

USD/year in the period 2011-2018, accounting for 15% of

the country's total agricultural exports Vietnam has a

potential to overtake Brazil as the world's largest coffee

exporte (My Hang, 2020).

Social Labor force: According to the World Bank (2020),

Vietnam's population is around 97.33 million people, up

0.91 percent from the previous year, with 50.08 percent of

women and 49.92 percent of men. It has the potential to

raise client demand for goods and services. In addition,

Vietnam has a large and steady work force, with 76.7

percent of the population employed. However, Vietnam

- Vietnam is a one-party state led by the Communist Party of

Vietnam (CPV) (CIPD, 2020). Vietnam's politics are stable

under this system, with little risks of internal strife The

economic environment is well worth the investment.

- Vietnam's Decree 134/2016/ND-CP encourages export

activity. In 2019, Vietnam ratified the Comprehensive and

Progressive Agreement for Trans-Pacific Partnership

(CPTPP), and the EU-Vietnam Free Trade Agreement

(EVFTA) was recently signed.

Open up many opportunities for importing, exporting and

trading

Econmic

GDP: Coffee is an important commodity, accounting for

3% of Vietnam's GDP, export turnover for many years has

reached over 3 billion USD. In recent years, although the

world economy had many difficult times leading to a

decrease in purchasing power, our country still maintained

an encouraging growth rate of coffee exports - reaching

8.2%. /year with an average turnover of 3.13 billion

USD/year in the period 2011-2018, accounting for 15% of

the country's total agricultural exports Vietnam has a

potential to overtake Brazil as the world's largest coffee

exporte (My Hang, 2020).

Social Labor force: According to the World Bank (2020),

Vietnam's population is around 97.33 million people, up

0.91 percent from the previous year, with 50.08 percent of

women and 49.92 percent of men. It has the potential to

raise client demand for goods and services. In addition,

Vietnam has a large and steady work force, with 76.7

percent of the population employed. However, Vietnam

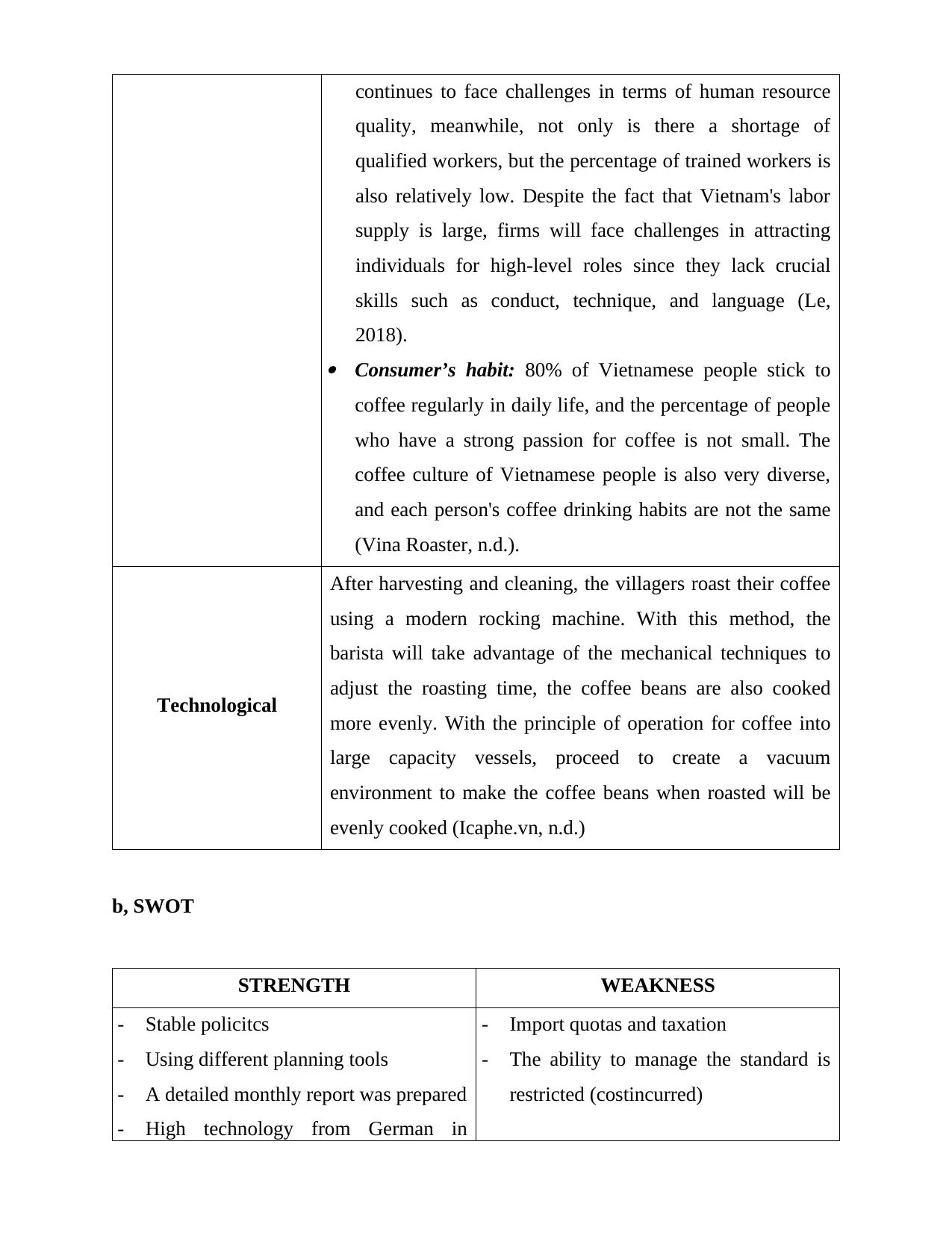

continues to face challenges in terms of human resource

quality, meanwhile, not only is there a shortage of

qualified workers, but the percentage of trained workers is

also relatively low. Despite the fact that Vietnam's labor

supply is large, firms will face challenges in attracting

individuals for high-level roles since they lack crucial

skills such as conduct, technique, and language (Le,

2018).

Consumer’s habit: 80% of Vietnamese people stick to

coffee regularly in daily life, and the percentage of people

who have a strong passion for coffee is not small. The

coffee culture of Vietnamese people is also very diverse,

and each person's coffee drinking habits are not the same

(Vina Roaster, n.d.).

Technological

After harvesting and cleaning, the villagers roast their coffee

using a modern rocking machine. With this method, the

barista will take advantage of the mechanical techniques to

adjust the roasting time, the coffee beans are also cooked

more evenly. With the principle of operation for coffee into

large capacity vessels, proceed to create a vacuum

environment to make the coffee beans when roasted will be

evenly cooked (Icaphe.vn, n.d.)

b, SWOT

STRENGTH WEAKNESS

- Stable policitcs

- Using different planning tools

- A detailed monthly report was prepared

- High technology from German in

- Import quotas and taxation

- The ability to manage the standard is

restricted (costincurred)

quality, meanwhile, not only is there a shortage of

qualified workers, but the percentage of trained workers is

also relatively low. Despite the fact that Vietnam's labor

supply is large, firms will face challenges in attracting

individuals for high-level roles since they lack crucial

skills such as conduct, technique, and language (Le,

2018).

Consumer’s habit: 80% of Vietnamese people stick to

coffee regularly in daily life, and the percentage of people

who have a strong passion for coffee is not small. The

coffee culture of Vietnamese people is also very diverse,

and each person's coffee drinking habits are not the same

(Vina Roaster, n.d.).

Technological

After harvesting and cleaning, the villagers roast their coffee

using a modern rocking machine. With this method, the

barista will take advantage of the mechanical techniques to

adjust the roasting time, the coffee beans are also cooked

more evenly. With the principle of operation for coffee into

large capacity vessels, proceed to create a vacuum

environment to make the coffee beans when roasted will be

evenly cooked (Icaphe.vn, n.d.)

b, SWOT

STRENGTH WEAKNESS

- Stable policitcs

- Using different planning tools

- A detailed monthly report was prepared

- High technology from German in

- Import quotas and taxation

- The ability to manage the standard is

restricted (costincurred)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.