Analysis of COGS and Primary Cost in Cost Accounting Principles

VerifiedAdded on 2023/01/04

|3

|491

|30

Homework Assignment

AI Summary

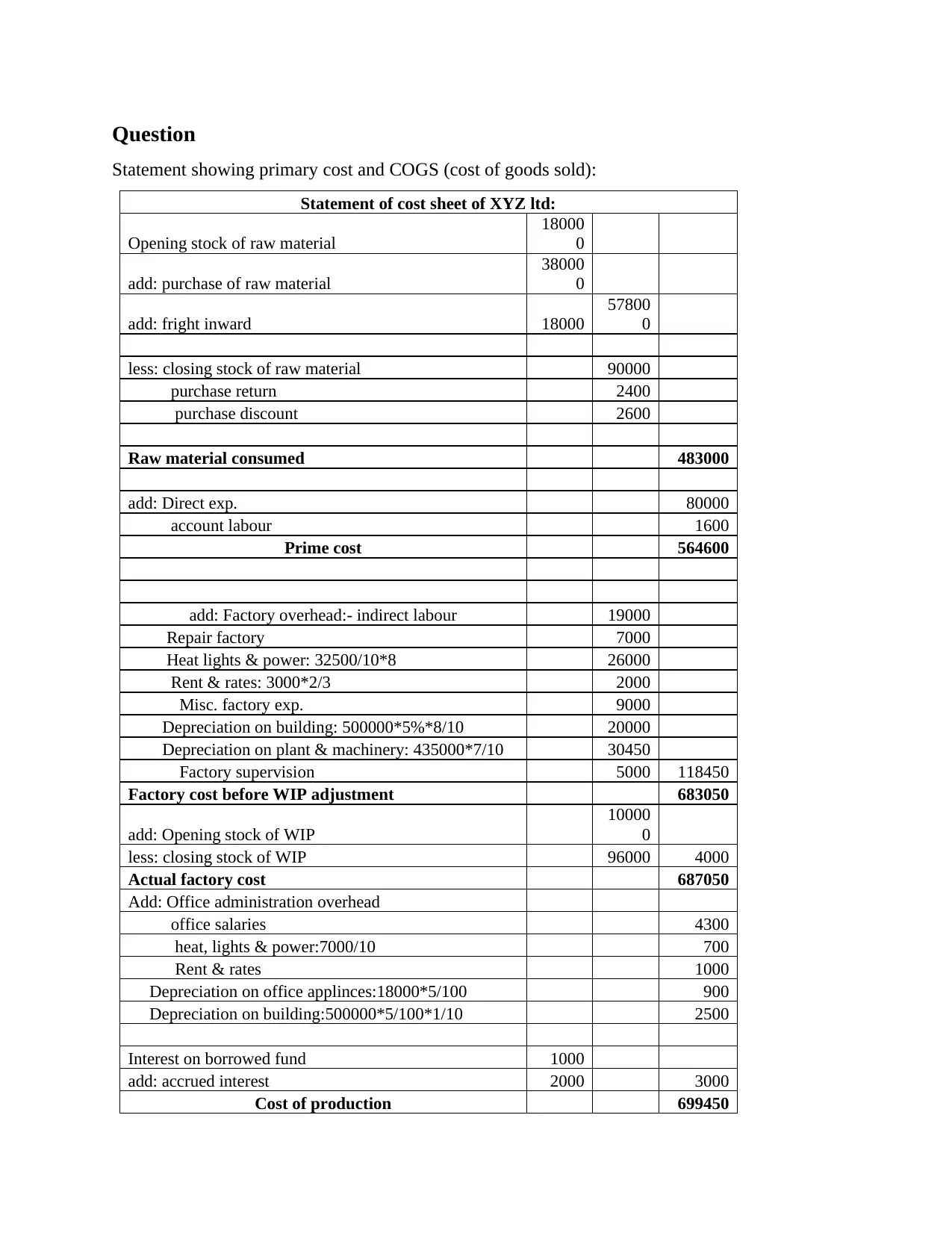

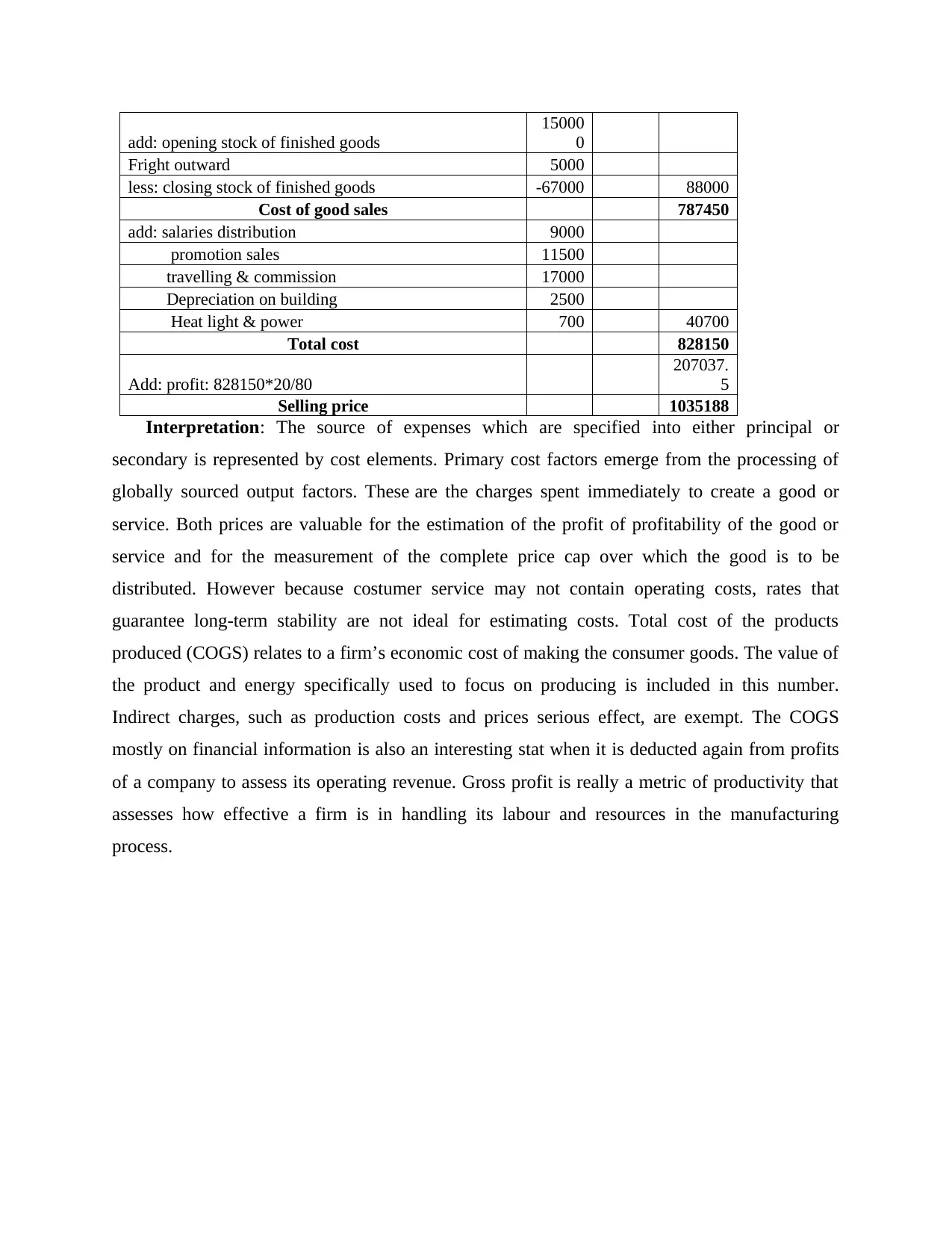

This assignment presents a detailed cost sheet analysis for XYZ Ltd., demonstrating the calculation of primary costs and the cost of goods sold (COGS). The solution meticulously breaks down various cost elements, including raw material consumption, direct expenses, factory overheads, and office administration overheads, to arrive at the actual factory cost and cost of production. It also includes the calculation of the cost of goods sold, considering opening and closing stock of finished goods, and the addition of selling and distribution expenses. The assignment provides an interpretation of the results, emphasizing the distinction between primary and secondary costs and their importance in determining profitability. It also defines COGS and its significance in assessing a company's operating revenue and gross profit, offering insights into how efficiently a firm manages its resources in the manufacturing process. The final calculation of the selling price, based on a 20% profit margin, completes the comprehensive cost analysis.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.