Com Hem Case Study: Analyzing Financial Strategies & Investment Exit

VerifiedAdded on 2023/05/29

|8

|1754

|345

Case Study

AI Summary

This case study provides a financial analysis of Com Hem, a Swedish cable company, focusing on its buyout and exit strategies under the ownership of EQT, Carlyle Group, and Providence Equity Partners. It examines whether Com Hem was a successful buyout investment, the value added during the transactions, and the reasons behind Carlyle and Providence's decision to sell. The analysis also discusses the pros and cons of pursuing a dual-track procedure (IPO and auction) and identifies potential buyers, considering financial versus strategic investors. The study concludes by estimating the minimum bid required to prevent the termination of the sales process in favor of an IPO. The Com Hem key financials for the years 2007-2010 are also presented to support the analysis. Desklib provides students access to this and other solved assignments for academic support.

Financial Analysis

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Question 1.............................................................................................................................................2

Question 2.............................................................................................................................................2

Question 3.............................................................................................................................................3

Question 4.............................................................................................................................................4

References.............................................................................................................................................6

Appendix...............................................................................................................................................7

1

Question 1.............................................................................................................................................2

Question 2.............................................................................................................................................2

Question 3.............................................................................................................................................3

Question 4.............................................................................................................................................4

References.............................................................................................................................................6

Appendix...............................................................................................................................................7

1

Question 1

The performance of Com Hem is considered to be very good in the market as per the past

financial results. Com Hem AB is the leading cable company of Sweden. At the time of

acquisition by EQT, the organization generated an EBITDA of the amount of SEK 53 million

in 2002 on the net sales of amount SEK 1,071. Under the ownership of EQT, Com Hem

carried out extensive transformation programs and investment which increased the

profitability and growth.Com Hem by 2005 was leading triple play provided with 1430000

customers in Sweden. Com Hem under the ownership of EQT was able to make the required

transformation and investments which led to the increase in the profitability and growth. The

investments were done in broadening of offerings, improvement of the services and

technologies consisting of telephony services, broadband and cable TV. Thus, it can be

concluded that Com Hem was being a good buyout investment for Providence and Carlyle.

Providence Equity and Carlyle Group entered into an agreement to purchase Com Hem B for

an amount of SEK 10.5 billion from EQT partners on 5 December 2005. Com Hem AB at the

year ended 31 December 2004, reported a sales revenue of amount SEK 1579 million. The

Carlyle European Capital Partners II of amount USD 2.2 billion was being used by Carlyle

for the acquisition. A New Providence fund equity partners of amount USD 4.25 billion was

raised by Providence in 2004.

EQT Northern Europe on 23 April 2003, entered into a contract for acquiring Com Hem AB

from the company Telia Sonera which reported SEK 2.15 billion. EQT received bank loan

facility of amount SEK 1 billion for financing the acquisition and future investment. Com

Hem at the time acquisition generated an EBITDA of amount SEK 53 million in 2002 on the

net sales of amount SEK 1071 million. COM Hem was not being the core asset of the

company Telia and Com Hem's broadband services competed with the fibre network of Telia.

The customers of Com Hem had access to the quality and high-speed broadband internet

services, telephone services and television channels. EQT was able to see a large opportunity

for increasing efficiency improve its offerings and invest into the organization.

Question 2

Com Hem despite continued growth was experiencing issues with customer satisfaction. A

survey with the customers of the organization resulted that Com Hem was being ranked with

2

The performance of Com Hem is considered to be very good in the market as per the past

financial results. Com Hem AB is the leading cable company of Sweden. At the time of

acquisition by EQT, the organization generated an EBITDA of the amount of SEK 53 million

in 2002 on the net sales of amount SEK 1,071. Under the ownership of EQT, Com Hem

carried out extensive transformation programs and investment which increased the

profitability and growth.Com Hem by 2005 was leading triple play provided with 1430000

customers in Sweden. Com Hem under the ownership of EQT was able to make the required

transformation and investments which led to the increase in the profitability and growth. The

investments were done in broadening of offerings, improvement of the services and

technologies consisting of telephony services, broadband and cable TV. Thus, it can be

concluded that Com Hem was being a good buyout investment for Providence and Carlyle.

Providence Equity and Carlyle Group entered into an agreement to purchase Com Hem B for

an amount of SEK 10.5 billion from EQT partners on 5 December 2005. Com Hem AB at the

year ended 31 December 2004, reported a sales revenue of amount SEK 1579 million. The

Carlyle European Capital Partners II of amount USD 2.2 billion was being used by Carlyle

for the acquisition. A New Providence fund equity partners of amount USD 4.25 billion was

raised by Providence in 2004.

EQT Northern Europe on 23 April 2003, entered into a contract for acquiring Com Hem AB

from the company Telia Sonera which reported SEK 2.15 billion. EQT received bank loan

facility of amount SEK 1 billion for financing the acquisition and future investment. Com

Hem at the time acquisition generated an EBITDA of amount SEK 53 million in 2002 on the

net sales of amount SEK 1071 million. COM Hem was not being the core asset of the

company Telia and Com Hem's broadband services competed with the fibre network of Telia.

The customers of Com Hem had access to the quality and high-speed broadband internet

services, telephone services and television channels. EQT was able to see a large opportunity

for increasing efficiency improve its offerings and invest into the organization.

Question 2

Com Hem despite continued growth was experiencing issues with customer satisfaction. A

survey with the customers of the organization resulted that Com Hem was being ranked with

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

least satisfied customers as the TV brand in 2007, 2008 and 2009 in Sweden. Com Hem

between 2006 and 2011 invested around SEK 4 billion for upgrading the network and

improving the new services such as broadband up to 200 MB/s and TV On Demand.

Providence and Carlyle with the scope generating more profit and the successful sale of the

Kabel Baden Wuerttemberg GmbH & Co, a German cable organization in March 2011. A

dual track sales process was being carried out by Deutsche Bank on behalf of EQT for KBW

and ended up selling the organization for r €3.16 billion to Liberty Global. Carlyle and

Providence had managed Com Hem in an efficient manner which leads to the growth of the

organization. However, Carlye and Providence are selling the Com Hem with the scope

gaining more profit from the sale of Com Hem.

The private equity financed organization should exit an investment when they want to make

more money from the sale of the acquisition. The main reason for selling the acquired

organization is to generate a huge amount of profit which will be much higher than the

purchased amount. Apart from this, other consideration may also be taken into account such

as how long the organization was being operated and its financial performance. Also, the

private equity financed organization is looking to raise funds for other purposes can exit an

investment. The equity organization can also exit to generate returns for the potential

investors. The equity firms may also need capital funds for carrying out its business

operations1.

Question 3

The method to conduct an auction with for the IPO had increasingly become popular in

recent years which are especially among the private equity owners. However, the dual track

process was considered to be more expensive and complicated than simply run an IPO

procedure or stand-alone auction. It has many benefits consisting of increased flexibility and

higher valuations. The dual track process in comparison to IPO can decrease the exposures to

the market volatility. At the launch of the IPO, the favourable conditions can suddenly

change and adversely impact the pricing of IPO. Apart from this, the regulator and stock

exchange conducting the multi-month review process adds an additional unpredictability

element. The organizations carrying out the dual track process can mitigate some of the

uncertainties in the capital markets by providing the exiting option themselves through a sale.

1 Holton, Global Finance, 95.

3

between 2006 and 2011 invested around SEK 4 billion for upgrading the network and

improving the new services such as broadband up to 200 MB/s and TV On Demand.

Providence and Carlyle with the scope generating more profit and the successful sale of the

Kabel Baden Wuerttemberg GmbH & Co, a German cable organization in March 2011. A

dual track sales process was being carried out by Deutsche Bank on behalf of EQT for KBW

and ended up selling the organization for r €3.16 billion to Liberty Global. Carlyle and

Providence had managed Com Hem in an efficient manner which leads to the growth of the

organization. However, Carlye and Providence are selling the Com Hem with the scope

gaining more profit from the sale of Com Hem.

The private equity financed organization should exit an investment when they want to make

more money from the sale of the acquisition. The main reason for selling the acquired

organization is to generate a huge amount of profit which will be much higher than the

purchased amount. Apart from this, other consideration may also be taken into account such

as how long the organization was being operated and its financial performance. Also, the

private equity financed organization is looking to raise funds for other purposes can exit an

investment. The equity organization can also exit to generate returns for the potential

investors. The equity firms may also need capital funds for carrying out its business

operations1.

Question 3

The method to conduct an auction with for the IPO had increasingly become popular in

recent years which are especially among the private equity owners. However, the dual track

process was considered to be more expensive and complicated than simply run an IPO

procedure or stand-alone auction. It has many benefits consisting of increased flexibility and

higher valuations. The dual track process in comparison to IPO can decrease the exposures to

the market volatility. At the launch of the IPO, the favourable conditions can suddenly

change and adversely impact the pricing of IPO. Apart from this, the regulator and stock

exchange conducting the multi-month review process adds an additional unpredictability

element. The organizations carrying out the dual track process can mitigate some of the

uncertainties in the capital markets by providing the exiting option themselves through a sale.

1 Holton, Global Finance, 95.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The dual track process in the auction can create bargaining power for the potential acquirers.

The dual track IPO process at a minimum lends an urgency degree to the acquisition process.

The opportunity window was seen as closed by the strategic acquirers when the potential

targets commence the IPO process as the organization cannot be for the sale following the

IPO. During the IPO process, it is still possible for acquiring the organization but the terms

can likely to be less favourable. The organizations which are going public were likely to

consist of more stringent market examination on their pricing in comparison to the sales

process of the private organization. The buyers, as a result, can be inclined more to the act in

the credible possibility face of an IPO. Thus, the perceived leverage of the dual track process

leads to an increase in the sale price and targeting friendly deal conditions2.

The limitation of the dual track process is that it is more complicated which results in an

increase in the need for management efforts and time. The underwriter fees in the European

IPO were on average 4 per cent of the issue size. The investment bank in an auction operating

the process will charge usually 1-2 percent of the total price of the organization relying on the

expected size of the transaction. Additional fees in the dual track process can be incurred and

beyond the acquisition fees of IPO due to the fact that both the processes operate

simultaneously.

Leverage is all about control and pricing. The dual track process can lead to price tensions

through increasing competition because staring IPO process gives an organization a

maximum exposure in the market and prospective buyers are under-covered. The IPO process

is considered to be extremely burdensome and time-consuming process. The focus on

carrying out two processes can divert the attention of the management away from the

business. However, carrying out dual process allows the organization hedge against the

unstable market environment and provides an organization greater flexibility.

Question 4

The financial buyer would pay the most for Com Hem. The main aim of the financial buyer is

to acquire an organization with the interest of generating a higher return from the acquisition.

They examine how the acquisition fits with the strategic goals of the organization. The

financial buyer will purchase Com Hem because the organization have been one of the

established and growing cable firm consisting of a huge customer base and business

networks. The financial performance of Com Hem is also been increasing over the period

2 Viney, Financial Market Essentials, 155.

4

The dual track IPO process at a minimum lends an urgency degree to the acquisition process.

The opportunity window was seen as closed by the strategic acquirers when the potential

targets commence the IPO process as the organization cannot be for the sale following the

IPO. During the IPO process, it is still possible for acquiring the organization but the terms

can likely to be less favourable. The organizations which are going public were likely to

consist of more stringent market examination on their pricing in comparison to the sales

process of the private organization. The buyers, as a result, can be inclined more to the act in

the credible possibility face of an IPO. Thus, the perceived leverage of the dual track process

leads to an increase in the sale price and targeting friendly deal conditions2.

The limitation of the dual track process is that it is more complicated which results in an

increase in the need for management efforts and time. The underwriter fees in the European

IPO were on average 4 per cent of the issue size. The investment bank in an auction operating

the process will charge usually 1-2 percent of the total price of the organization relying on the

expected size of the transaction. Additional fees in the dual track process can be incurred and

beyond the acquisition fees of IPO due to the fact that both the processes operate

simultaneously.

Leverage is all about control and pricing. The dual track process can lead to price tensions

through increasing competition because staring IPO process gives an organization a

maximum exposure in the market and prospective buyers are under-covered. The IPO process

is considered to be extremely burdensome and time-consuming process. The focus on

carrying out two processes can divert the attention of the management away from the

business. However, carrying out dual process allows the organization hedge against the

unstable market environment and provides an organization greater flexibility.

Question 4

The financial buyer would pay the most for Com Hem. The main aim of the financial buyer is

to acquire an organization with the interest of generating a higher return from the acquisition.

They examine how the acquisition fits with the strategic goals of the organization. The

financial buyer will purchase Com Hem because the organization have been one of the

established and growing cable firm consisting of a huge customer base and business

networks. The financial performance of Com Hem is also been increasing over the period

2 Viney, Financial Market Essentials, 155.

4

which will also attract the interest of the financial buyer. They are considered to be the long-

term investors who look for well managed and solid organization. The financial buyers can

make changes in order to support the growth of the organization as well as making attractive

to the investors in future. The investors also expect that they would gain more return from the

acquired organization.

The minimum bid that can be expected in order to carry out the sales process and pursue the

IPO would be more than the actual value of Com Hem. Obviously, Providence and Carlyle

would not sale Com Hem at a loss to the investors. Providence and Carlyle have managed

Com Hem appropriate which led to the increase in the sales revenues and profitability. The

minimum bid should not be carried out at a loss which means Providence and Carlyle should

be in profit from the sale of the organization. The Providence and Carlyle should wait and

sale the Com Hem at right time in order to gain high profit from the sale of it.

5

term investors who look for well managed and solid organization. The financial buyers can

make changes in order to support the growth of the organization as well as making attractive

to the investors in future. The investors also expect that they would gain more return from the

acquired organization.

The minimum bid that can be expected in order to carry out the sales process and pursue the

IPO would be more than the actual value of Com Hem. Obviously, Providence and Carlyle

would not sale Com Hem at a loss to the investors. Providence and Carlyle have managed

Com Hem appropriate which led to the increase in the sales revenues and profitability. The

minimum bid should not be carried out at a loss which means Providence and Carlyle should

be in profit from the sale of the organization. The Providence and Carlyle should wait and

sale the Com Hem at right time in order to gain high profit from the sale of it.

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

References

Holton, Robert John. Global Finance. London: Routledge, 2012.

Viney, Christopher. Financial Market Essentials. North Ryde, N.S.W.: McGraw-Hill

Australia, 2011.

6

Holton, Robert John. Global Finance. London: Routledge, 2012.

Viney, Christopher. Financial Market Essentials. North Ryde, N.S.W.: McGraw-Hill

Australia, 2011.

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Appendix

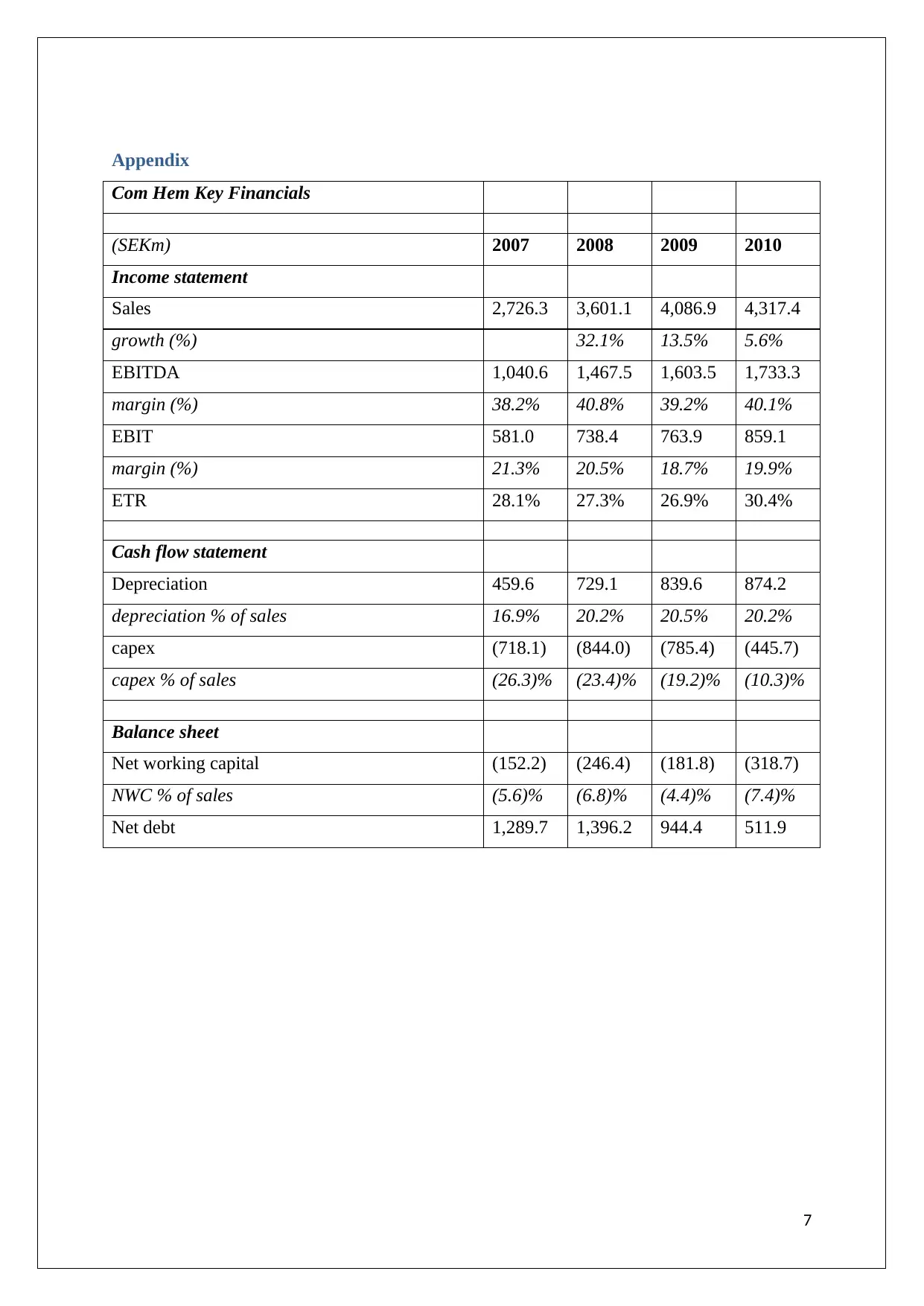

Com Hem Key Financials

(SEKm) 2007 2008 2009 2010

Income statement

Sales 2,726.3 3,601.1 4,086.9 4,317.4

growth (%) 32.1% 13.5% 5.6%

EBITDA 1,040.6 1,467.5 1,603.5 1,733.3

margin (%) 38.2% 40.8% 39.2% 40.1%

EBIT 581.0 738.4 763.9 859.1

margin (%) 21.3% 20.5% 18.7% 19.9%

ETR 28.1% 27.3% 26.9% 30.4%

Cash flow statement

Depreciation 459.6 729.1 839.6 874.2

depreciation % of sales 16.9% 20.2% 20.5% 20.2%

capex (718.1) (844.0) (785.4) (445.7)

capex % of sales (26.3)% (23.4)% (19.2)% (10.3)%

Balance sheet

Net working capital (152.2) (246.4) (181.8) (318.7)

NWC % of sales (5.6)% (6.8)% (4.4)% (7.4)%

Net debt 1,289.7 1,396.2 944.4 511.9

7

Com Hem Key Financials

(SEKm) 2007 2008 2009 2010

Income statement

Sales 2,726.3 3,601.1 4,086.9 4,317.4

growth (%) 32.1% 13.5% 5.6%

EBITDA 1,040.6 1,467.5 1,603.5 1,733.3

margin (%) 38.2% 40.8% 39.2% 40.1%

EBIT 581.0 738.4 763.9 859.1

margin (%) 21.3% 20.5% 18.7% 19.9%

ETR 28.1% 27.3% 26.9% 30.4%

Cash flow statement

Depreciation 459.6 729.1 839.6 874.2

depreciation % of sales 16.9% 20.2% 20.5% 20.2%

capex (718.1) (844.0) (785.4) (445.7)

capex % of sales (26.3)% (23.4)% (19.2)% (10.3)%

Balance sheet

Net working capital (152.2) (246.4) (181.8) (318.7)

NWC % of sales (5.6)% (6.8)% (4.4)% (7.4)%

Net debt 1,289.7 1,396.2 944.4 511.9

7

1 out of 8

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.