Dog Pound Golf: COMM 210 Winter 2020 Term 2 Budget Project Analysis

VerifiedAdded on 2022/09/06

|23

|5031

|36

Project

AI Summary

This report analyzes the budget for Dog Pound Golf, comparing its current business model with a proposed retail expansion. The assignment involves preparing master budgets, including sales, production, materials, labor, overhead, and cash budgets, along with financial statements for both scenarios. The analysis reveals that the retail expansion negatively impacts profitability, increases short-term borrowings, and strains the company's cash position. The student recommends against the expansion in the current period, emphasizing the need for improved cash management and expense reduction. The report provides detailed financial comparisons and highlights the adverse effects of the proposed expansion on key financial metrics, offering recommendations based on the analysis.

1

COMM 210 Introduction to Managerial

Accounting

COMM 210 Introduction to Managerial

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Executive summary

The report has been prepared by using the budgeting and in that there has been

undertaking the master budget which is prepared for two scenarios of the business. There is

the use of all the elements in that and with the help of that, the overall evaluation has been

carried out. All the changes which will be taking place with the undertaking of retail

expansion have been incorporated and the impact which will be faced with that has also been

covered. The budgets have been revised with the new changes and then evaluation with the

change that is taking place has been made. It has been ascertained that there is a negative

influence and the profitability of the business has been affected in an adverse manner. The

undertaking of the proposal will bring various issues for the company such as the cash

shortage for which the short-term borrowings are required. This will raise another issue of

increasing interest thereby reducing the profits and that will also be inappropriate for the

business. By considering all the relevant aspects recommendation has been made to the

company to not undertake the proposal for now and skip the plan for expansion in the current

period.

Executive summary

The report has been prepared by using the budgeting and in that there has been

undertaking the master budget which is prepared for two scenarios of the business. There is

the use of all the elements in that and with the help of that, the overall evaluation has been

carried out. All the changes which will be taking place with the undertaking of retail

expansion have been incorporated and the impact which will be faced with that has also been

covered. The budgets have been revised with the new changes and then evaluation with the

change that is taking place has been made. It has been ascertained that there is a negative

influence and the profitability of the business has been affected in an adverse manner. The

undertaking of the proposal will bring various issues for the company such as the cash

shortage for which the short-term borrowings are required. This will raise another issue of

increasing interest thereby reducing the profits and that will also be inappropriate for the

business. By considering all the relevant aspects recommendation has been made to the

company to not undertake the proposal for now and skip the plan for expansion in the current

period.

3

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Importance of budgeting............................................................................................................4

Alternative..................................................................................................................................5

Decision criteria.........................................................................................................................6

Conclusion..................................................................................................................................8

Recommendations......................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................10

Table of Contents

Executive summary....................................................................................................................2

Introduction................................................................................................................................4

Importance of budgeting............................................................................................................4

Alternative..................................................................................................................................5

Decision criteria.........................................................................................................................6

Conclusion..................................................................................................................................8

Recommendations......................................................................................................................8

References..................................................................................................................................9

Appendix..................................................................................................................................10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

Introduction

In the business, there is a need for the proper budgeting by which all of the incomes

and expenditures will be planned. The budget is a plan in which all the activities of the

company are considered and for that predictions are made. In the given report the master

budget will be prepared in respect of two products which are made by the company. For that,

there will be consideration of two options that are available including the base case and the

retail outlets. The various budgets which are involved in the master budget will be prepared

and with the help of that, the company will be able to make the appropriate evaluation. This

will help in taking the most appropriate decision that will be beneficial for the company in the

long-run.

Importance of budgeting

The planning for the appropriate use of the funds is made under the process of

budgeting and that is highly important for any business. The budget is prepared to make the

proper use of funds that are available and they will be allocated in the required manner. There

will be the determination of the funds which will be required in the undertaking of the various

operations which are involved (PRIYA, 2020). This will help the company in planning the

manner in which appropriate management will be made possible. This will be ensuring that

business always has the required funds and there is no shortage which is faced. With the help

of a budget, the objectives and goals are set and they are worked upon. The budget acts as the

standard and that is required to be followed by all which gives directions and guidelines. This

ensures that all the members are making the use of funds in the manner it is specified in the

budget (Ezzamel et al., 2012). The best of the performance will be made with the use of this

and that will ensure that the most effective and efficient performance will be made which is

in the interest of the company.

Introduction

In the business, there is a need for the proper budgeting by which all of the incomes

and expenditures will be planned. The budget is a plan in which all the activities of the

company are considered and for that predictions are made. In the given report the master

budget will be prepared in respect of two products which are made by the company. For that,

there will be consideration of two options that are available including the base case and the

retail outlets. The various budgets which are involved in the master budget will be prepared

and with the help of that, the company will be able to make the appropriate evaluation. This

will help in taking the most appropriate decision that will be beneficial for the company in the

long-run.

Importance of budgeting

The planning for the appropriate use of the funds is made under the process of

budgeting and that is highly important for any business. The budget is prepared to make the

proper use of funds that are available and they will be allocated in the required manner. There

will be the determination of the funds which will be required in the undertaking of the various

operations which are involved (PRIYA, 2020). This will help the company in planning the

manner in which appropriate management will be made possible. This will be ensuring that

business always has the required funds and there is no shortage which is faced. With the help

of a budget, the objectives and goals are set and they are worked upon. The budget acts as the

standard and that is required to be followed by all which gives directions and guidelines. This

ensures that all the members are making the use of funds in the manner it is specified in the

budget (Ezzamel et al., 2012). The best of the performance will be made with the use of this

and that will ensure that the most effective and efficient performance will be made which is

in the interest of the company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

Alternative

In the given case of Dog pound golf, they are preparing two types of balls and are

currently providing them directly to the customers. In this process, the manufacturing is

undertaken and after that, the proper selling activities are performed. The company is

considering the new proposal of expansion in which there will be an incorporation of the sale

to retail outlets also. By this, there will be various changes that will be required to be made

and they will help in evaluating the proposal (Becker et al., 2016). It is necessary to identify

whether the expansion is for the benefit of the company or not. For this purpose, the master

budgets have been made for both the options and are presented in an appendix.

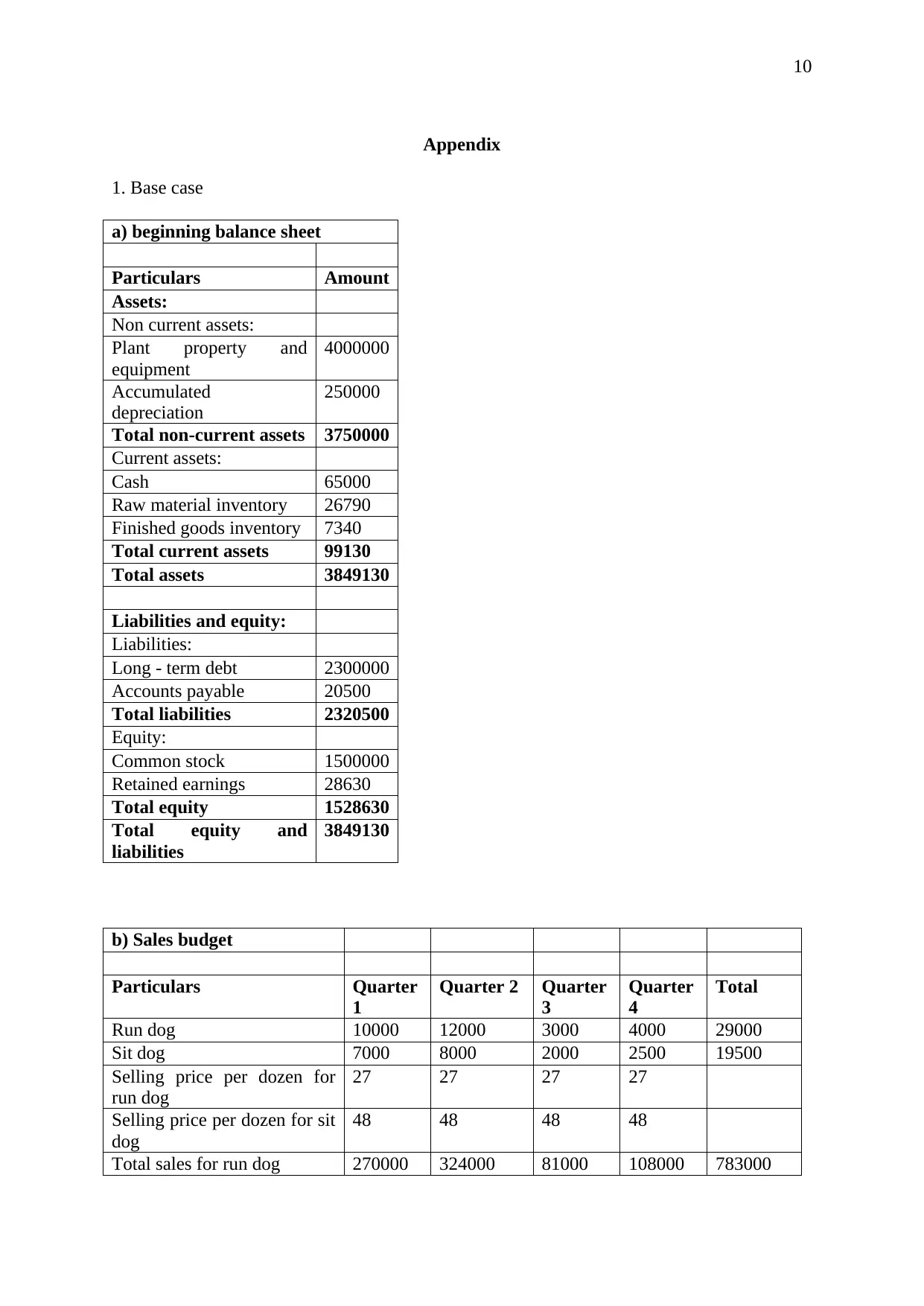

The budgets have been prepared and in that, all of the major aspects have been

covered. The sales are made and it can be noted form the appendix 1 sales budget and

appendix 2 sales budget that with the new proposal the sales of the company will be

increasing which good. The sale is increasing but then also the profitability of the business is

presenting the adverse impact. There are profits which are made in the base case and that can

be seen in the appendix 1 income statement but the situation changed with the expansion and

in that there are losses which are made. The profit of $129541turned to the loss of $197266

and this is because of an increase in the various expenses which are incurred.

The cash position of the business is very important and shall be maintained in the

business in proper manner and for the ascertainment of that cash budget has been prepared

and the one for the base case is presented in appendix 1 cash budget. The closing balance

which has been obtained from the same is $131406 which is a positive level and will be

efficient to manage the operations. There is no short-term borrowing which is made in this

case as there was no shortage and so the need did not arise. On the contrary to this with the

retail outlet's option, there was the balance of $51635 which was maintained and that is

Alternative

In the given case of Dog pound golf, they are preparing two types of balls and are

currently providing them directly to the customers. In this process, the manufacturing is

undertaken and after that, the proper selling activities are performed. The company is

considering the new proposal of expansion in which there will be an incorporation of the sale

to retail outlets also. By this, there will be various changes that will be required to be made

and they will help in evaluating the proposal (Becker et al., 2016). It is necessary to identify

whether the expansion is for the benefit of the company or not. For this purpose, the master

budgets have been made for both the options and are presented in an appendix.

The budgets have been prepared and in that, all of the major aspects have been

covered. The sales are made and it can be noted form the appendix 1 sales budget and

appendix 2 sales budget that with the new proposal the sales of the company will be

increasing which good. The sale is increasing but then also the profitability of the business is

presenting the adverse impact. There are profits which are made in the base case and that can

be seen in the appendix 1 income statement but the situation changed with the expansion and

in that there are losses which are made. The profit of $129541turned to the loss of $197266

and this is because of an increase in the various expenses which are incurred.

The cash position of the business is very important and shall be maintained in the

business in proper manner and for the ascertainment of that cash budget has been prepared

and the one for the base case is presented in appendix 1 cash budget. The closing balance

which has been obtained from the same is $131406 which is a positive level and will be

efficient to manage the operations. There is no short-term borrowing which is made in this

case as there was no shortage and so the need did not arise. On the contrary to this with the

retail outlet's option, there was the balance of $51635 which was maintained and that is

6

because of the account sales which is made in this option and also the expenses have

increased with the undertaking of additional equipment financing and that is adverse for

business.

The short term financing position of the business is also getting affected and it has

been identified that there was no shortage faced in the base care and due to that the borrowing

is not undertaken (Vaznonienė & Stončiuvienė, 2012). This can be noted from the appendix 1

cash budget whereas in the appendix 2 cash budget of retail outlets there is a high amount of

borrowings which are made. The cash shortage is faced and to deal with that there are

borrowings which have been made and on them, the interest is paid which increased the

expenses also. This shows the insufficiency of the cash to manage the business operations

which is not beneficial.

Decision criteria

The new proposal brought various changes to the values and by that, the decision will

be made. All the changes are represented below:

Particulars Base

case

retail case Change

Profit 129541 -197266 -326807

Cash 131406 51635 -79771

Short term borrowings 0 545000 545000

because of the account sales which is made in this option and also the expenses have

increased with the undertaking of additional equipment financing and that is adverse for

business.

The short term financing position of the business is also getting affected and it has

been identified that there was no shortage faced in the base care and due to that the borrowing

is not undertaken (Vaznonienė & Stončiuvienė, 2012). This can be noted from the appendix 1

cash budget whereas in the appendix 2 cash budget of retail outlets there is a high amount of

borrowings which are made. The cash shortage is faced and to deal with that there are

borrowings which have been made and on them, the interest is paid which increased the

expenses also. This shows the insufficiency of the cash to manage the business operations

which is not beneficial.

Decision criteria

The new proposal brought various changes to the values and by that, the decision will

be made. All the changes are represented below:

Particulars Base

case

retail case Change

Profit 129541 -197266 -326807

Cash 131406 51635 -79771

Short term borrowings 0 545000 545000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

All the major elements in which the changes are taking place are shown above in the

table. This shows that with the new retail proposal the business is not gaining any advantage

rather the situation is getting adverse. There are a high amount of losses that are being made

and that will affect the future operations and profitability of the company. The retained

income is made from the profits from adverse circumstances but due to the negative profits,

there will be no retained earning which will be left. This will be disadvantageous for the

business in the long run and the expansion will be made difficult (Kerler et al., 2012). With

the reducing cash balance, the situation will further get worse as that is the basic need to

manage the activities.

Without the appropriate level of cash, the short term obligations will not be met by the

company in an effective manner. The balance which is available in the retail case is also with

the help of the borrowings that have been made otherwise the cash shortage has been faced.

This has resulted in an increase in the borrowings and that is not beneficial. The situation will

have an additional negative impact on the business as the borrowing will lead to the payment

of the interest (Siyanbola, 2013). There will be an impact of the same on the profits also as

the interest will be rising the overall expenses and with that, the new equipment is also

purchased by which the other interests are also increasing. There is the installment that is paid

for the equipment and by that also the cash position is getting affected adversely. Overall

there are all the negative changes which are taking place and that is not good for the

company.

All the major elements in which the changes are taking place are shown above in the

table. This shows that with the new retail proposal the business is not gaining any advantage

rather the situation is getting adverse. There are a high amount of losses that are being made

and that will affect the future operations and profitability of the company. The retained

income is made from the profits from adverse circumstances but due to the negative profits,

there will be no retained earning which will be left. This will be disadvantageous for the

business in the long run and the expansion will be made difficult (Kerler et al., 2012). With

the reducing cash balance, the situation will further get worse as that is the basic need to

manage the activities.

Without the appropriate level of cash, the short term obligations will not be met by the

company in an effective manner. The balance which is available in the retail case is also with

the help of the borrowings that have been made otherwise the cash shortage has been faced.

This has resulted in an increase in the borrowings and that is not beneficial. The situation will

have an additional negative impact on the business as the borrowing will lead to the payment

of the interest (Siyanbola, 2013). There will be an impact of the same on the profits also as

the interest will be rising the overall expenses and with that, the new equipment is also

purchased by which the other interests are also increasing. There is the installment that is paid

for the equipment and by that also the cash position is getting affected adversely. Overall

there are all the negative changes which are taking place and that is not good for the

company.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

Conclusion

The evaluation in the business for the available proposal has been made and in that,

there has been the preparation of the master budgets for both the available scenarios. In that,

there is the preparation of production budget, material budget, labor budget, overheads

budget, cash budget and all the financial statements. With the help of them, the evaluation is

made and the various aspects have been considered for the same. In that, the changes which

are taking place and the impact which will be made by them has been considered in the

report. With that, the positive and negative impact on the business with the undertaking of

expansion proposal has been accounted for. In that, there is the involvement of the proper

comparison among the values of the base case and the retail outlets and there is the negative

impact of the new proposal which has been identified in terms of the profitability, short-term

borrowings and cash position.

Recommendations

The evaluation is done and from that, the financial position and performance of the

business with both the base case and retail outlets have been accounted for. It has been noted

that there is a negative impact that is made on the business with the new expansion proposal

and that will be harmful. Due to this, it is recommended that the expansion to the retail

market shall not be undertaken in the current position as that will be harming the overall

performance of the company in the long run. The improvements are required to be made and

in that the cash position will be improved in the first place. There is a need for the company

to manage the cash in such a manner that it can be used for expansion. The business will be

required to undertake the appropriate actions by which the expenses which are not necessary

can be identified and the elimination of them will be made to make the situation positive.

Conclusion

The evaluation in the business for the available proposal has been made and in that,

there has been the preparation of the master budgets for both the available scenarios. In that,

there is the preparation of production budget, material budget, labor budget, overheads

budget, cash budget and all the financial statements. With the help of them, the evaluation is

made and the various aspects have been considered for the same. In that, the changes which

are taking place and the impact which will be made by them has been considered in the

report. With that, the positive and negative impact on the business with the undertaking of

expansion proposal has been accounted for. In that, there is the involvement of the proper

comparison among the values of the base case and the retail outlets and there is the negative

impact of the new proposal which has been identified in terms of the profitability, short-term

borrowings and cash position.

Recommendations

The evaluation is done and from that, the financial position and performance of the

business with both the base case and retail outlets have been accounted for. It has been noted

that there is a negative impact that is made on the business with the new expansion proposal

and that will be harmful. Due to this, it is recommended that the expansion to the retail

market shall not be undertaken in the current position as that will be harming the overall

performance of the company in the long run. The improvements are required to be made and

in that the cash position will be improved in the first place. There is a need for the company

to manage the cash in such a manner that it can be used for expansion. The business will be

required to undertake the appropriate actions by which the expenses which are not necessary

can be identified and the elimination of them will be made to make the situation positive.

9

References

Becker, S. D., Mahlendorf, M. D., Schäffer, U., & Thaten, M. (2016). Budgeting in times of

economic crisis. Contemporary Accounting Research, 33(4), 1489-1517.

Ezzamel, M., Robson, K., & Stapleton, P. (2012). The logic of budgeting: Theorization and

practice variation in the educational field. Accounting, Organizations and

society, 37(5), 281-303.

Kerler, W. A., Allport, C. D., & Fleming, A. S. (2012). Impact of framed information and

project importance on capital budgeting decisions. Advances in Management

Accounting, 21, 1-24.

PRIYA, S. (2020). A STUDY ON THE IMPORTANCE OF BUDGETING IN AN

ORGANISATION. Studies in Indian Place Names, 40(46), 500-505.

Siyanbola, T. T. (2013). The impact of budgeting and budgetary control on the performance

of manufacturing company in Nigeria. Journal of Business Management & Social

Sciences Research, 2(12), 8-16.

Vaznonienė, M., & Stončiuvienė, N. (2012). The formation of company budgeting system:

importance, problems and solutions. Management theory and studies for rural

business and infrastructure development, 30(1).

References

Becker, S. D., Mahlendorf, M. D., Schäffer, U., & Thaten, M. (2016). Budgeting in times of

economic crisis. Contemporary Accounting Research, 33(4), 1489-1517.

Ezzamel, M., Robson, K., & Stapleton, P. (2012). The logic of budgeting: Theorization and

practice variation in the educational field. Accounting, Organizations and

society, 37(5), 281-303.

Kerler, W. A., Allport, C. D., & Fleming, A. S. (2012). Impact of framed information and

project importance on capital budgeting decisions. Advances in Management

Accounting, 21, 1-24.

PRIYA, S. (2020). A STUDY ON THE IMPORTANCE OF BUDGETING IN AN

ORGANISATION. Studies in Indian Place Names, 40(46), 500-505.

Siyanbola, T. T. (2013). The impact of budgeting and budgetary control on the performance

of manufacturing company in Nigeria. Journal of Business Management & Social

Sciences Research, 2(12), 8-16.

Vaznonienė, M., & Stončiuvienė, N. (2012). The formation of company budgeting system:

importance, problems and solutions. Management theory and studies for rural

business and infrastructure development, 30(1).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

10

Appendix

1. Base case

a) beginning balance sheet

Particulars Amount

Assets:

Non current assets:

Plant property and

equipment

4000000

Accumulated

depreciation

250000

Total non-current assets 3750000

Current assets:

Cash 65000

Raw material inventory 26790

Finished goods inventory 7340

Total current assets 99130

Total assets 3849130

Liabilities and equity:

Liabilities:

Long - term debt 2300000

Accounts payable 20500

Total liabilities 2320500

Equity:

Common stock 1500000

Retained earnings 28630

Total equity 1528630

Total equity and

liabilities

3849130

b) Sales budget

Particulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Run dog 10000 12000 3000 4000 29000

Sit dog 7000 8000 2000 2500 19500

Selling price per dozen for

run dog

27 27 27 27

Selling price per dozen for sit

dog

48 48 48 48

Total sales for run dog 270000 324000 81000 108000 783000

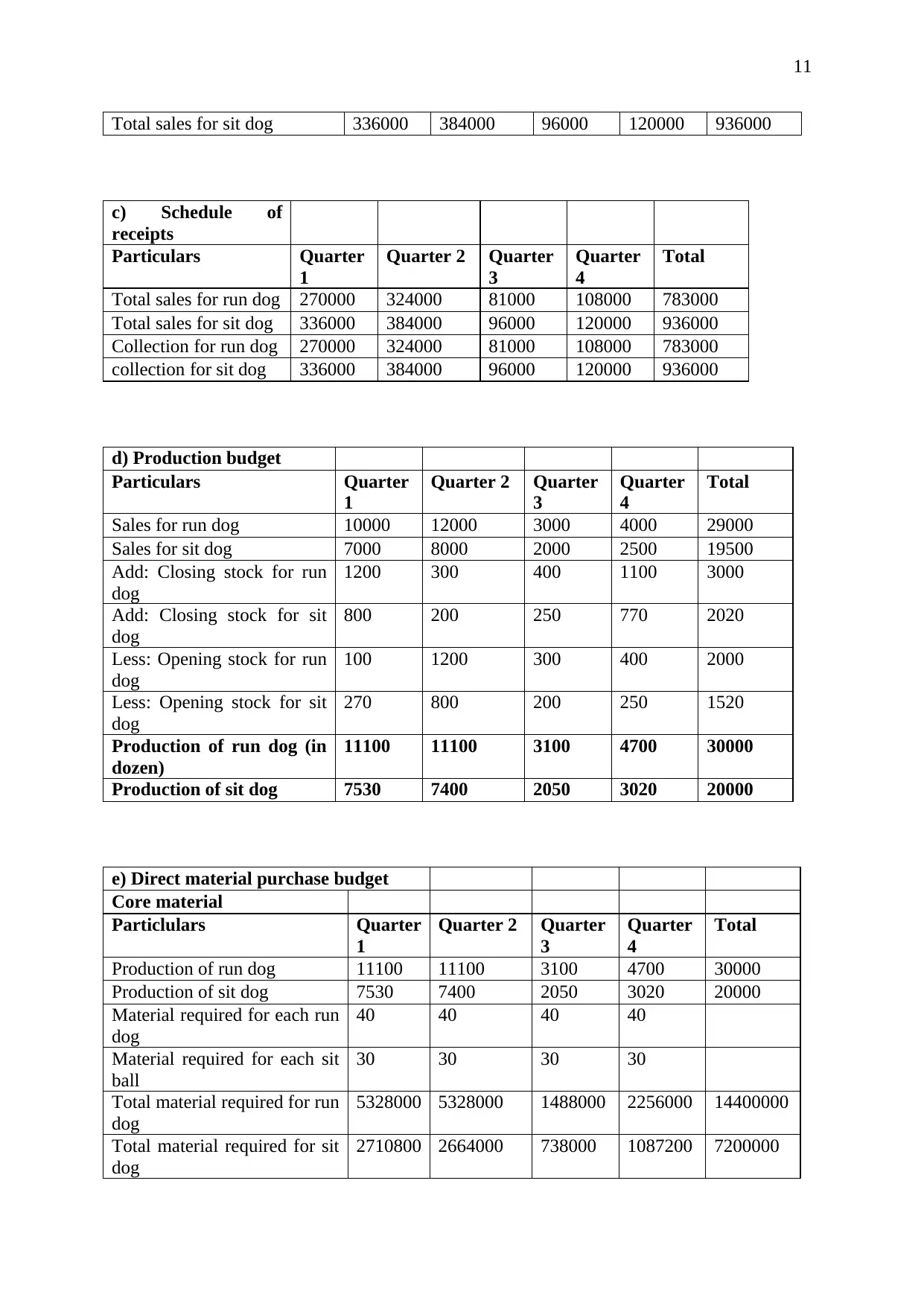

Appendix

1. Base case

a) beginning balance sheet

Particulars Amount

Assets:

Non current assets:

Plant property and

equipment

4000000

Accumulated

depreciation

250000

Total non-current assets 3750000

Current assets:

Cash 65000

Raw material inventory 26790

Finished goods inventory 7340

Total current assets 99130

Total assets 3849130

Liabilities and equity:

Liabilities:

Long - term debt 2300000

Accounts payable 20500

Total liabilities 2320500

Equity:

Common stock 1500000

Retained earnings 28630

Total equity 1528630

Total equity and

liabilities

3849130

b) Sales budget

Particulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Run dog 10000 12000 3000 4000 29000

Sit dog 7000 8000 2000 2500 19500

Selling price per dozen for

run dog

27 27 27 27

Selling price per dozen for sit

dog

48 48 48 48

Total sales for run dog 270000 324000 81000 108000 783000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

Total sales for sit dog 336000 384000 96000 120000 936000

c) Schedule of

receipts

Particulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Total sales for run dog 270000 324000 81000 108000 783000

Total sales for sit dog 336000 384000 96000 120000 936000

Collection for run dog 270000 324000 81000 108000 783000

collection for sit dog 336000 384000 96000 120000 936000

d) Production budget

Particulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Sales for run dog 10000 12000 3000 4000 29000

Sales for sit dog 7000 8000 2000 2500 19500

Add: Closing stock for run

dog

1200 300 400 1100 3000

Add: Closing stock for sit

dog

800 200 250 770 2020

Less: Opening stock for run

dog

100 1200 300 400 2000

Less: Opening stock for sit

dog

270 800 200 250 1520

Production of run dog (in

dozen)

11100 11100 3100 4700 30000

Production of sit dog 7530 7400 2050 3020 20000

e) Direct material purchase budget

Core material

Particlulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Production of run dog 11100 11100 3100 4700 30000

Production of sit dog 7530 7400 2050 3020 20000

Material required for each run

dog

40 40 40 40

Material required for each sit

ball

30 30 30 30

Total material required for run

dog

5328000 5328000 1488000 2256000 14400000

Total material required for sit

dog

2710800 2664000 738000 1087200 7200000

Total sales for sit dog 336000 384000 96000 120000 936000

c) Schedule of

receipts

Particulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Total sales for run dog 270000 324000 81000 108000 783000

Total sales for sit dog 336000 384000 96000 120000 936000

Collection for run dog 270000 324000 81000 108000 783000

collection for sit dog 336000 384000 96000 120000 936000

d) Production budget

Particulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Sales for run dog 10000 12000 3000 4000 29000

Sales for sit dog 7000 8000 2000 2500 19500

Add: Closing stock for run

dog

1200 300 400 1100 3000

Add: Closing stock for sit

dog

800 200 250 770 2020

Less: Opening stock for run

dog

100 1200 300 400 2000

Less: Opening stock for sit

dog

270 800 200 250 1520

Production of run dog (in

dozen)

11100 11100 3100 4700 30000

Production of sit dog 7530 7400 2050 3020 20000

e) Direct material purchase budget

Core material

Particlulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Production of run dog 11100 11100 3100 4700 30000

Production of sit dog 7530 7400 2050 3020 20000

Material required for each run

dog

40 40 40 40

Material required for each sit

ball

30 30 30 30

Total material required for run

dog

5328000 5328000 1488000 2256000 14400000

Total material required for sit

dog

2710800 2664000 738000 1087200 7200000

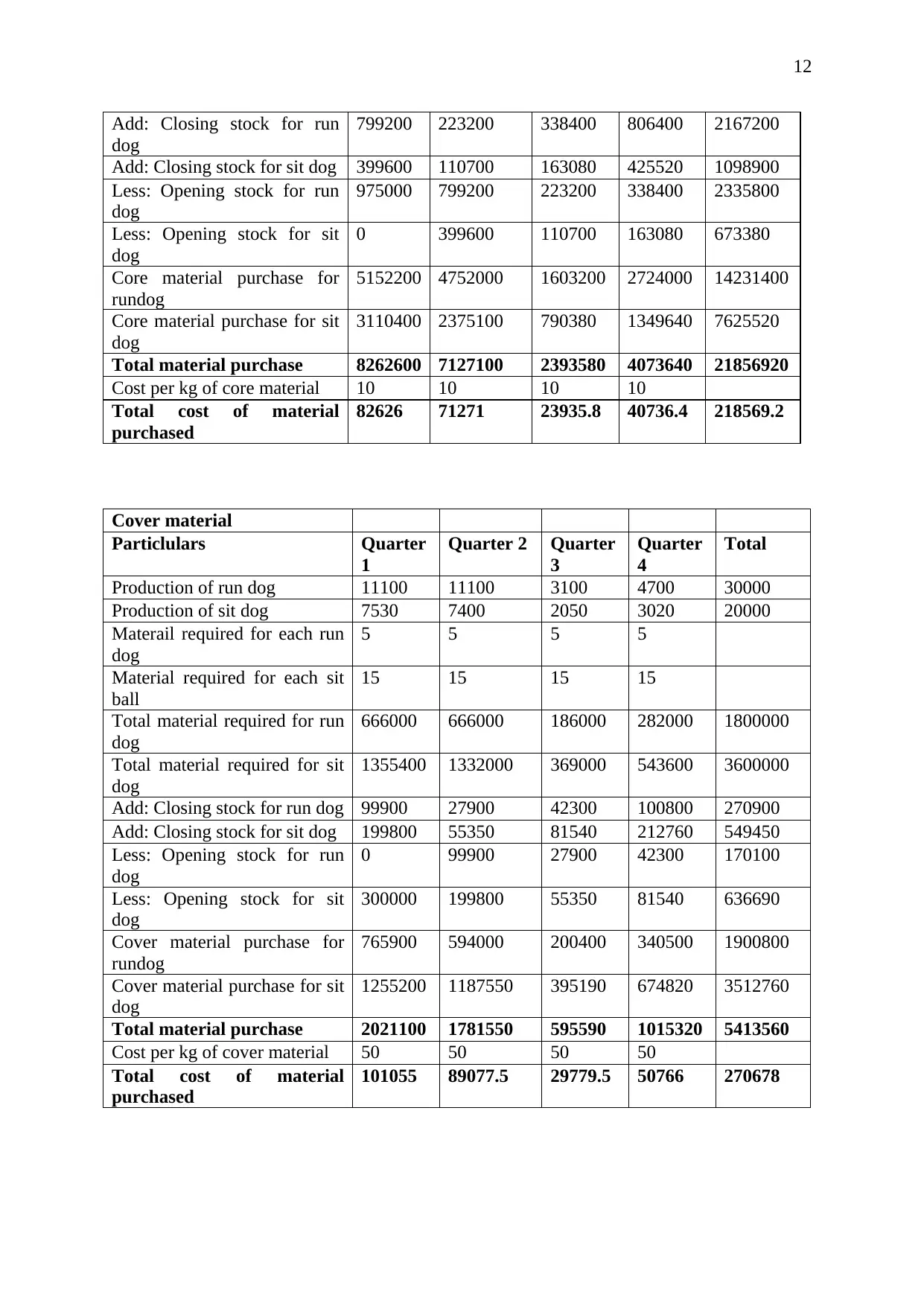

12

Add: Closing stock for run

dog

799200 223200 338400 806400 2167200

Add: Closing stock for sit dog 399600 110700 163080 425520 1098900

Less: Opening stock for run

dog

975000 799200 223200 338400 2335800

Less: Opening stock for sit

dog

0 399600 110700 163080 673380

Core material purchase for

rundog

5152200 4752000 1603200 2724000 14231400

Core material purchase for sit

dog

3110400 2375100 790380 1349640 7625520

Total material purchase 8262600 7127100 2393580 4073640 21856920

Cost per kg of core material 10 10 10 10

Total cost of material

purchased

82626 71271 23935.8 40736.4 218569.2

Cover material

Particlulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Production of run dog 11100 11100 3100 4700 30000

Production of sit dog 7530 7400 2050 3020 20000

Materail required for each run

dog

5 5 5 5

Material required for each sit

ball

15 15 15 15

Total material required for run

dog

666000 666000 186000 282000 1800000

Total material required for sit

dog

1355400 1332000 369000 543600 3600000

Add: Closing stock for run dog 99900 27900 42300 100800 270900

Add: Closing stock for sit dog 199800 55350 81540 212760 549450

Less: Opening stock for run

dog

0 99900 27900 42300 170100

Less: Opening stock for sit

dog

300000 199800 55350 81540 636690

Cover material purchase for

rundog

765900 594000 200400 340500 1900800

Cover material purchase for sit

dog

1255200 1187550 395190 674820 3512760

Total material purchase 2021100 1781550 595590 1015320 5413560

Cost per kg of cover material 50 50 50 50

Total cost of material

purchased

101055 89077.5 29779.5 50766 270678

Add: Closing stock for run

dog

799200 223200 338400 806400 2167200

Add: Closing stock for sit dog 399600 110700 163080 425520 1098900

Less: Opening stock for run

dog

975000 799200 223200 338400 2335800

Less: Opening stock for sit

dog

0 399600 110700 163080 673380

Core material purchase for

rundog

5152200 4752000 1603200 2724000 14231400

Core material purchase for sit

dog

3110400 2375100 790380 1349640 7625520

Total material purchase 8262600 7127100 2393580 4073640 21856920

Cost per kg of core material 10 10 10 10

Total cost of material

purchased

82626 71271 23935.8 40736.4 218569.2

Cover material

Particlulars Quarter

1

Quarter 2 Quarter

3

Quarter

4

Total

Production of run dog 11100 11100 3100 4700 30000

Production of sit dog 7530 7400 2050 3020 20000

Materail required for each run

dog

5 5 5 5

Material required for each sit

ball

15 15 15 15

Total material required for run

dog

666000 666000 186000 282000 1800000

Total material required for sit

dog

1355400 1332000 369000 543600 3600000

Add: Closing stock for run dog 99900 27900 42300 100800 270900

Add: Closing stock for sit dog 199800 55350 81540 212760 549450

Less: Opening stock for run

dog

0 99900 27900 42300 170100

Less: Opening stock for sit

dog

300000 199800 55350 81540 636690

Cover material purchase for

rundog

765900 594000 200400 340500 1900800

Cover material purchase for sit

dog

1255200 1187550 395190 674820 3512760

Total material purchase 2021100 1781550 595590 1015320 5413560

Cost per kg of cover material 50 50 50 50

Total cost of material

purchased

101055 89077.5 29779.5 50766 270678

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.