Commercial Property Management: GFC Impact and Future in Australia

VerifiedAdded on 2023/04/21

|28

|7311

|282

Report

AI Summary

This report examines the current and future implications for commercial property managers in Australia, particularly in light of structural changes in the Australian economy. It begins with an executive summary that emphasizes the importance of understanding property cycles and the impact of economic downturns, using the Global Financial Crisis (GFC) of 2007-2009 as a key case study. The report delves into the causes of the GFC, including the role of sub-prime loans in the United States and their ripple effects globally. It analyzes the impact of the GFC on the Australian property sector, including declining market rents, rising vacancy rates, and increased outgoings, using the case study of '18 Smith Street, Parramatta NSW' as a small insight into office property. The report provides a historical overview of the GFC, detailing the deregulation of the financial system, the rise of affordable credit, and the subsequent issues that led to the crisis. It also assesses the impacts on Australian banks and the government's response to the crisis. Furthermore, the report includes a literature review and a discussion section that focuses on Sydney office property, discussing vacancy rates, market rents, outgoings, and future forecasts, as well as preventative strategies for commercial property managers. The analysis also touches on key economic indicators prior to the GFC, the impact on housing prices, and the role of banks and borrowers in the crisis. The report concludes with a summary of findings and a list of references.

Title 1

Current and future implications for commercial property managers due to structural change in

the Australian economy.

Name

Date

Course

Institution

Tutor

Current and future implications for commercial property managers due to structural change in

the Australian economy.

Name

Date

Course

Institution

Tutor

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Title 2

Executive Summary:

As a Property professional, developer, investor or manager it is essential to hold adequate

knowledge of the ever-changing property cycles, across all markets. By examining and

gaining knowledge based upon previous errors made by past Governments, financial

companies and banks property enthusiasts are able to view the potential of property

worldwide. It is clear that the decline in the economic domain can directly affect property

markets, while growth within the economy can achieve benefits to property.

During the period of the second quarter of 2007 until early 2009, the Global Financial Crisis

(GFC) occurred shaping various markets around the world resulting in iconic events of

economic history. While a financial crisis primarily results in negative issues, society has

arguably learnt drastically with regard to ideas relating to investment, risk, finance, banks and

greed. A major factor that led to the GFC stemmed from sub-prime loans in America that

caused significant economic decline and were seen to have a significant effect on most major

countries worldwide. The Australian property sector was significantly affected during the

period of the GFC with direct regard to declining market rents, increasing outgoings and

rising vacancy rates. This is identified through the case study ‘18 Smith Street, Parramatta

NSW’ found within appendices to be a small insight into what is the larger scale of office

property. Australia’s office property sector can be broken down into three levels of scale;

Premium, A Grade and B grade.

Executive Summary:

As a Property professional, developer, investor or manager it is essential to hold adequate

knowledge of the ever-changing property cycles, across all markets. By examining and

gaining knowledge based upon previous errors made by past Governments, financial

companies and banks property enthusiasts are able to view the potential of property

worldwide. It is clear that the decline in the economic domain can directly affect property

markets, while growth within the economy can achieve benefits to property.

During the period of the second quarter of 2007 until early 2009, the Global Financial Crisis

(GFC) occurred shaping various markets around the world resulting in iconic events of

economic history. While a financial crisis primarily results in negative issues, society has

arguably learnt drastically with regard to ideas relating to investment, risk, finance, banks and

greed. A major factor that led to the GFC stemmed from sub-prime loans in America that

caused significant economic decline and were seen to have a significant effect on most major

countries worldwide. The Australian property sector was significantly affected during the

period of the GFC with direct regard to declining market rents, increasing outgoings and

rising vacancy rates. This is identified through the case study ‘18 Smith Street, Parramatta

NSW’ found within appendices to be a small insight into what is the larger scale of office

property. Australia’s office property sector can be broken down into three levels of scale;

Premium, A Grade and B grade.

Title 3

Table of Contents

Executive Summary:..................................................................................................................2

Introduction................................................................................................................................4

1.1History of the Global Financial Crisis:.............................................................................4

1.2 The causes of the GFC.....................................................................................................6

1.3 How the GFC unfolded....................................................................................................8

Literature review........................................................................................................................8

2.1The GFC’s impact on Australia:...........................................................................................8

2.2 The GFC and impact on Australian Bank Risk................................................................8

Discussion................................................................................................................................11

3.1 Sydney Office Property, Vacancy Rates:.......................................................................11

3.2 Sydney Office Properties, Market Rents:......................................................................14

3.3 Sydney Office Property outgoings levels.......................................................................16

3.4 Future forecast for Sydney Office Property...................................................................17

3.5 Preventative Strategies for commercial Property Managers:.........................................18

Conclusion...............................................................................................................................20

List of references......................................................................................................................22

Appendices:..............................................................................................................................25

Table of Contents

Executive Summary:..................................................................................................................2

Introduction................................................................................................................................4

1.1History of the Global Financial Crisis:.............................................................................4

1.2 The causes of the GFC.....................................................................................................6

1.3 How the GFC unfolded....................................................................................................8

Literature review........................................................................................................................8

2.1The GFC’s impact on Australia:...........................................................................................8

2.2 The GFC and impact on Australian Bank Risk................................................................8

Discussion................................................................................................................................11

3.1 Sydney Office Property, Vacancy Rates:.......................................................................11

3.2 Sydney Office Properties, Market Rents:......................................................................14

3.3 Sydney Office Property outgoings levels.......................................................................16

3.4 Future forecast for Sydney Office Property...................................................................17

3.5 Preventative Strategies for commercial Property Managers:.........................................18

Conclusion...............................................................................................................................20

List of references......................................................................................................................22

Appendices:..............................................................................................................................25

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Title 4

Introduction

It is important for commercial property investors, managers to hold sufficient knowledge on

the changing property cycles. They can only achieve this by assessing the errors made by

banks and past government to view the potential of property in the entire world. From

assessing these errors, it is clearly shown that any drop in the economic domain directly

affect property markets. The GFC that happened between 2007 and 2009 shaped many

markets in the world resulting in a major event in the economic history (Kindleberger and

Aliber 2011, p.35). The GFC results had the sharpest and largest drawback in different

economic activity throughout the world. Due to the negative effect of the GFC, various

governments particularly Australia learned many things with regard to ideas such as finance,

banks, greed and investment (Higgins 2010, p.48). Some of the areas that were immensely

affected in Australia include the drop in market rents, the rising vacancy rates and increased

outgoings. Misperception and mismanagement of the risks, higher interest levels and

stringent financial regulation were the major causes of the Global financial crisis. The drivers

of the GFC were all about human psychology on risk perceptions. As much as countries such

as the US, UK suffered, the government of Australia was not largely affected by the impacts

of the GFC. The Reserve Bank of Australia regulated this by increasing the interest rates.

Most of the banks in Australia suffered accordingly when the global share markets

experienced a fall in 2008.This paper seeks to analyze the ramifications of the past Global

Financial Crisis climate currently. The paper further provides the future forecast of the

economy as well as the relative vibrancy of commercial real estate with reference to

economic market and property cycles. Lastly, the paper will discuss how Australia has

managed to deal with the GFC solidly.

Introduction

It is important for commercial property investors, managers to hold sufficient knowledge on

the changing property cycles. They can only achieve this by assessing the errors made by

banks and past government to view the potential of property in the entire world. From

assessing these errors, it is clearly shown that any drop in the economic domain directly

affect property markets. The GFC that happened between 2007 and 2009 shaped many

markets in the world resulting in a major event in the economic history (Kindleberger and

Aliber 2011, p.35). The GFC results had the sharpest and largest drawback in different

economic activity throughout the world. Due to the negative effect of the GFC, various

governments particularly Australia learned many things with regard to ideas such as finance,

banks, greed and investment (Higgins 2010, p.48). Some of the areas that were immensely

affected in Australia include the drop in market rents, the rising vacancy rates and increased

outgoings. Misperception and mismanagement of the risks, higher interest levels and

stringent financial regulation were the major causes of the Global financial crisis. The drivers

of the GFC were all about human psychology on risk perceptions. As much as countries such

as the US, UK suffered, the government of Australia was not largely affected by the impacts

of the GFC. The Reserve Bank of Australia regulated this by increasing the interest rates.

Most of the banks in Australia suffered accordingly when the global share markets

experienced a fall in 2008.This paper seeks to analyze the ramifications of the past Global

Financial Crisis climate currently. The paper further provides the future forecast of the

economy as well as the relative vibrancy of commercial real estate with reference to

economic market and property cycles. Lastly, the paper will discuss how Australia has

managed to deal with the GFC solidly.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Title 5

1.1History of the Global Financial Crisis:

The current Global Financial Crisis (GFC) started in 1980s when economic

deregulation took place. It started when the governments decided to eradicate financial

system controls to provide a wide scope for competition to encourage efficiency and

innovation (Raymond and Fischer 2013, p.42). This led to affordable credit which eased

lending standards and the tighter lending margins prompting a rise in the rate of innovation.

The rising pace of innovation made it hard for lenders and regulators to gauge the asset

position as well as banking institution solvency.

Between 2008 and 2009, several mortgage lenders in the U.S failed and the Bank of

America took over to contain the crisis. This problem was not only experienced in America

but also surfaced in several superior European economies that had heavily invested in the US

financial sector. The GFC ended the stable growth and inflation that was being enjoyed by

several countries (Reinhart and Rogoff 2009, p.471). During this GFC period, the nominal

GDP rose dramatically in US, UK and Australia with 120, 150 and 156 per cent respectively.

Most of this growth happened as a result of heavy property investment that pushed prices up

and developing an asset bubble in the property market.

The GFC results have been the sharpest and largest drawback in different economic

activity throughout the world. Dramatic drop has been experienced in the patterns and

volumes of trade. Despite the complex assumptions underpinning the econometric modelling,

the acute extent of the crisis was not properly predicted. The Global Financial Crisis, also

known and referred to as the great depression 2.0 was the key influence in diminishing what

was a stable economic domain within the United States of America (Obstfeld and Rogoff

2009, p.23). However, Australia has also not been spared of these impacts of GFC that

affected property market sectors, investment as well as equity that lead various developments

and companies to succumb to economic stocks.

1.1History of the Global Financial Crisis:

The current Global Financial Crisis (GFC) started in 1980s when economic

deregulation took place. It started when the governments decided to eradicate financial

system controls to provide a wide scope for competition to encourage efficiency and

innovation (Raymond and Fischer 2013, p.42). This led to affordable credit which eased

lending standards and the tighter lending margins prompting a rise in the rate of innovation.

The rising pace of innovation made it hard for lenders and regulators to gauge the asset

position as well as banking institution solvency.

Between 2008 and 2009, several mortgage lenders in the U.S failed and the Bank of

America took over to contain the crisis. This problem was not only experienced in America

but also surfaced in several superior European economies that had heavily invested in the US

financial sector. The GFC ended the stable growth and inflation that was being enjoyed by

several countries (Reinhart and Rogoff 2009, p.471). During this GFC period, the nominal

GDP rose dramatically in US, UK and Australia with 120, 150 and 156 per cent respectively.

Most of this growth happened as a result of heavy property investment that pushed prices up

and developing an asset bubble in the property market.

The GFC results have been the sharpest and largest drawback in different economic

activity throughout the world. Dramatic drop has been experienced in the patterns and

volumes of trade. Despite the complex assumptions underpinning the econometric modelling,

the acute extent of the crisis was not properly predicted. The Global Financial Crisis, also

known and referred to as the great depression 2.0 was the key influence in diminishing what

was a stable economic domain within the United States of America (Obstfeld and Rogoff

2009, p.23). However, Australia has also not been spared of these impacts of GFC that

affected property market sectors, investment as well as equity that lead various developments

and companies to succumb to economic stocks.

Title 6

Prior to the GFC, key economic indicators provided a sense of confidence and

strength in the American economy including a limited and controlled inflation rate, a steadily

growing GDP percentage, while at the same time being contrasted against low rates of

interest and unemployment. The world’s view on the economy as a whole was positive as it

was producing strong development to all markets including the property sector, resulting in a

stable rise for housing prices (Kindleberger and Aliber 2011, p.39). Due to the sense of

security and confidence felt by general households and property developers, borrowing sky

rocketed with individuals and businesses diving at the opportunity to borrow from lenders in

a growing environment to acquire new homes and development sites.

The surge in the amount applications for loans and mortgages was positively

answered by the banks during the period of economic stability without reasonable knowledge

or investigation into the ability for borrowers to repay these loans. Primarily due to the

unforeseen repercussions of the GFC and the poorly advice and loans provided by bank

workers who were seeking commission on their ability to secure borrowers. Cost of

regulation has since become an issue to the consumer because of government auditing and

investigation on poorly advised loans, and in turn increased the cost of securing a loan for

consumers as these costs were passed on by the banks through consumer fees for loan

application. This limited consumers’ ability to purchase property, resulting in the value of

property assets not growing as rapidly (Karas, Pyle and Schoors 2013, p.187).

With the value of housing and property falling after a significant increase in long term

loans to consumers who were unable to repay their debts, the economy began to suffer as a

result of these major issues. As a result, banks were involuntary required to reclaim

ownership of borrower’s homes in order to cover the cost of unpaid loans by selling

properties below market value in order to cut the total amount of loss.

Prior to the GFC, key economic indicators provided a sense of confidence and

strength in the American economy including a limited and controlled inflation rate, a steadily

growing GDP percentage, while at the same time being contrasted against low rates of

interest and unemployment. The world’s view on the economy as a whole was positive as it

was producing strong development to all markets including the property sector, resulting in a

stable rise for housing prices (Kindleberger and Aliber 2011, p.39). Due to the sense of

security and confidence felt by general households and property developers, borrowing sky

rocketed with individuals and businesses diving at the opportunity to borrow from lenders in

a growing environment to acquire new homes and development sites.

The surge in the amount applications for loans and mortgages was positively

answered by the banks during the period of economic stability without reasonable knowledge

or investigation into the ability for borrowers to repay these loans. Primarily due to the

unforeseen repercussions of the GFC and the poorly advice and loans provided by bank

workers who were seeking commission on their ability to secure borrowers. Cost of

regulation has since become an issue to the consumer because of government auditing and

investigation on poorly advised loans, and in turn increased the cost of securing a loan for

consumers as these costs were passed on by the banks through consumer fees for loan

application. This limited consumers’ ability to purchase property, resulting in the value of

property assets not growing as rapidly (Karas, Pyle and Schoors 2013, p.187).

With the value of housing and property falling after a significant increase in long term

loans to consumers who were unable to repay their debts, the economy began to suffer as a

result of these major issues. As a result, banks were involuntary required to reclaim

ownership of borrower’s homes in order to cover the cost of unpaid loans by selling

properties below market value in order to cut the total amount of loss.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Title 7

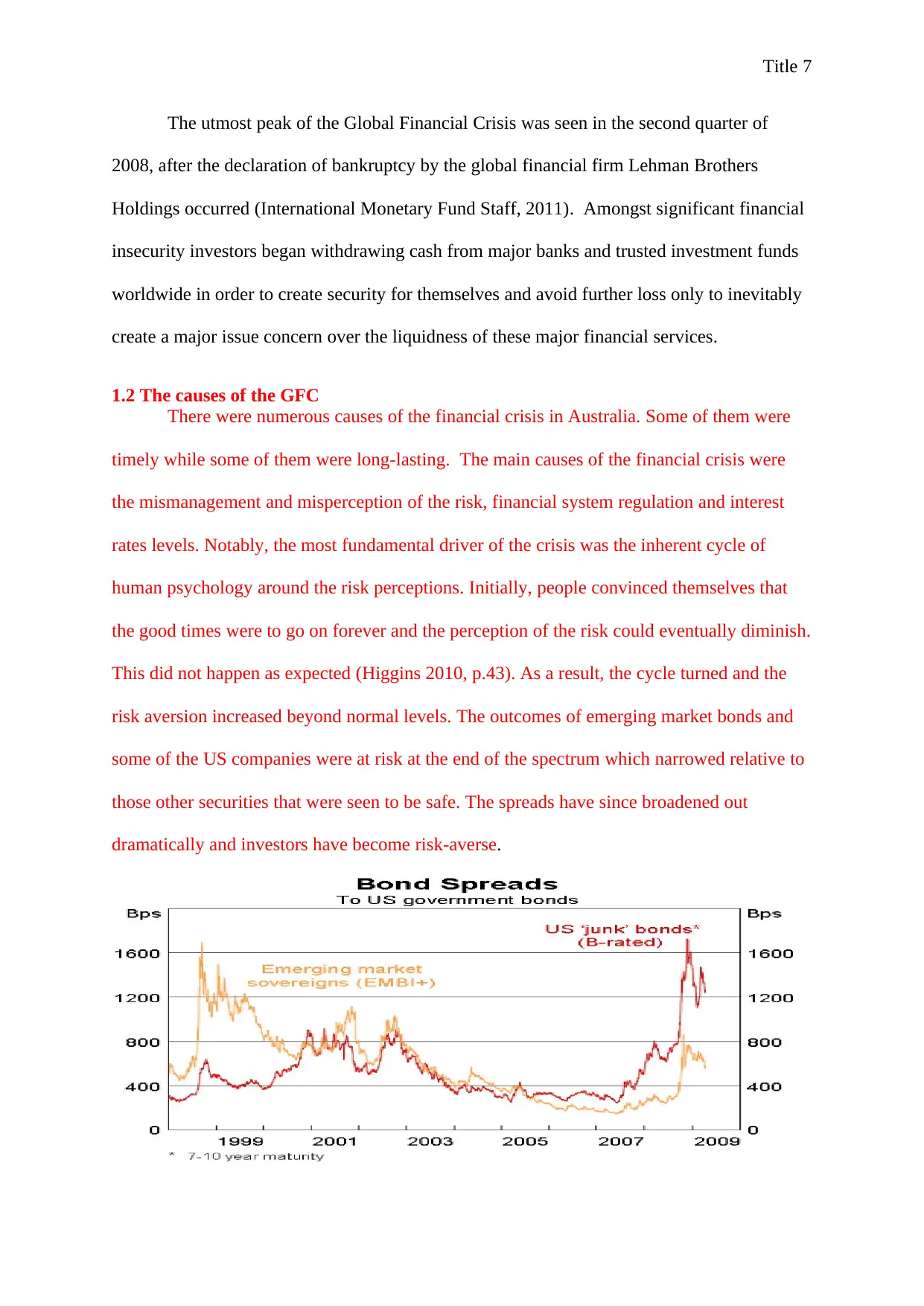

The utmost peak of the Global Financial Crisis was seen in the second quarter of

2008, after the declaration of bankruptcy by the global financial firm Lehman Brothers

Holdings occurred (International Monetary Fund Staff, 2011). Amongst significant financial

insecurity investors began withdrawing cash from major banks and trusted investment funds

worldwide in order to create security for themselves and avoid further loss only to inevitably

create a major issue concern over the liquidness of these major financial services.

1.2 The causes of the GFC

There were numerous causes of the financial crisis in Australia. Some of them were

timely while some of them were long-lasting. The main causes of the financial crisis were

the mismanagement and misperception of the risk, financial system regulation and interest

rates levels. Notably, the most fundamental driver of the crisis was the inherent cycle of

human psychology around the risk perceptions. Initially, people convinced themselves that

the good times were to go on forever and the perception of the risk could eventually diminish.

This did not happen as expected (Higgins 2010, p.43). As a result, the cycle turned and the

risk aversion increased beyond normal levels. The outcomes of emerging market bonds and

some of the US companies were at risk at the end of the spectrum which narrowed relative to

those other securities that were seen to be safe. The spreads have since broadened out

dramatically and investors have become risk-averse.

The utmost peak of the Global Financial Crisis was seen in the second quarter of

2008, after the declaration of bankruptcy by the global financial firm Lehman Brothers

Holdings occurred (International Monetary Fund Staff, 2011). Amongst significant financial

insecurity investors began withdrawing cash from major banks and trusted investment funds

worldwide in order to create security for themselves and avoid further loss only to inevitably

create a major issue concern over the liquidness of these major financial services.

1.2 The causes of the GFC

There were numerous causes of the financial crisis in Australia. Some of them were

timely while some of them were long-lasting. The main causes of the financial crisis were

the mismanagement and misperception of the risk, financial system regulation and interest

rates levels. Notably, the most fundamental driver of the crisis was the inherent cycle of

human psychology around the risk perceptions. Initially, people convinced themselves that

the good times were to go on forever and the perception of the risk could eventually diminish.

This did not happen as expected (Higgins 2010, p.43). As a result, the cycle turned and the

risk aversion increased beyond normal levels. The outcomes of emerging market bonds and

some of the US companies were at risk at the end of the spectrum which narrowed relative to

those other securities that were seen to be safe. The spreads have since broadened out

dramatically and investors have become risk-averse.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Title 8

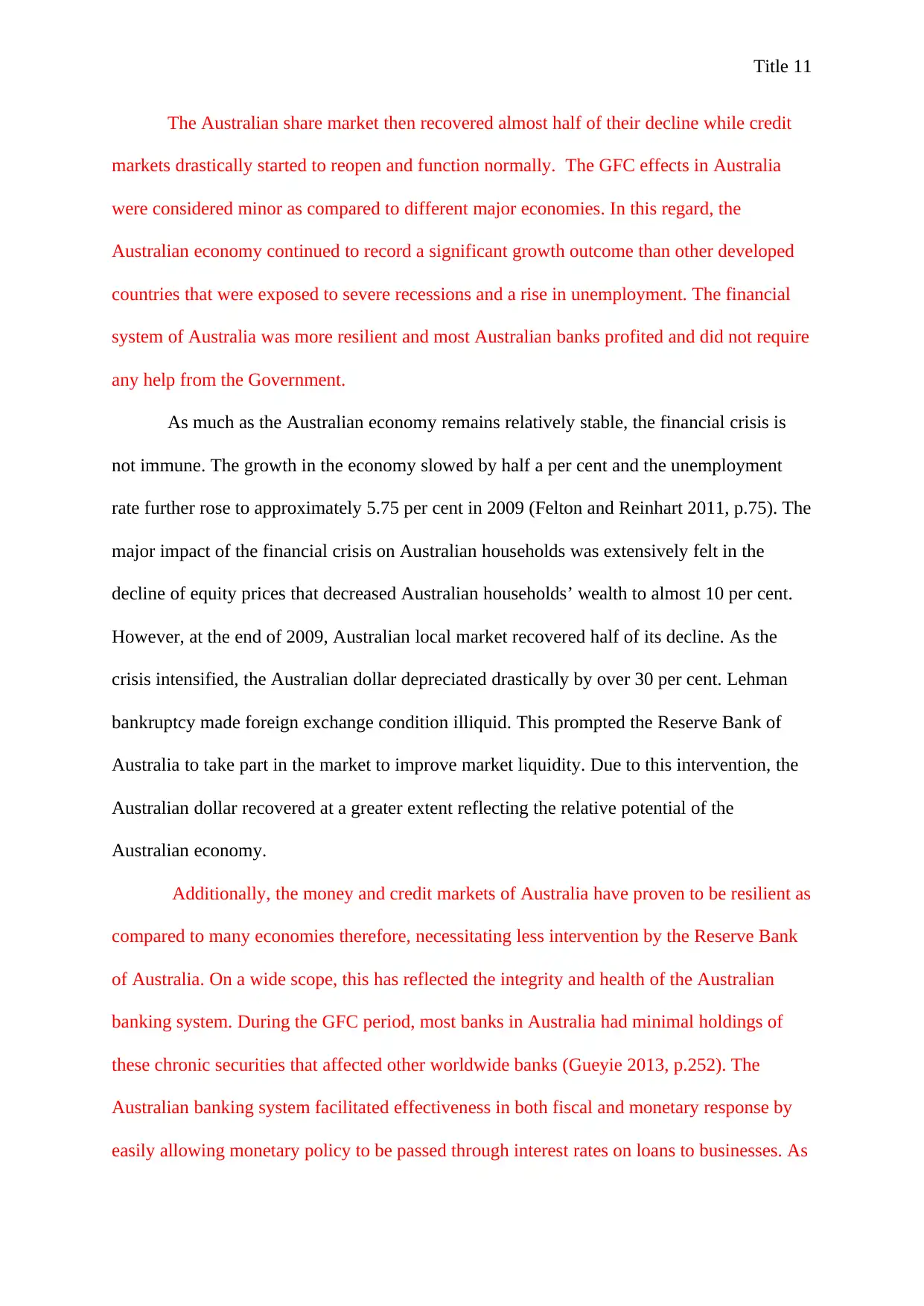

Figure 1showing the spread of US government bonds that resulted to emergence of GFC

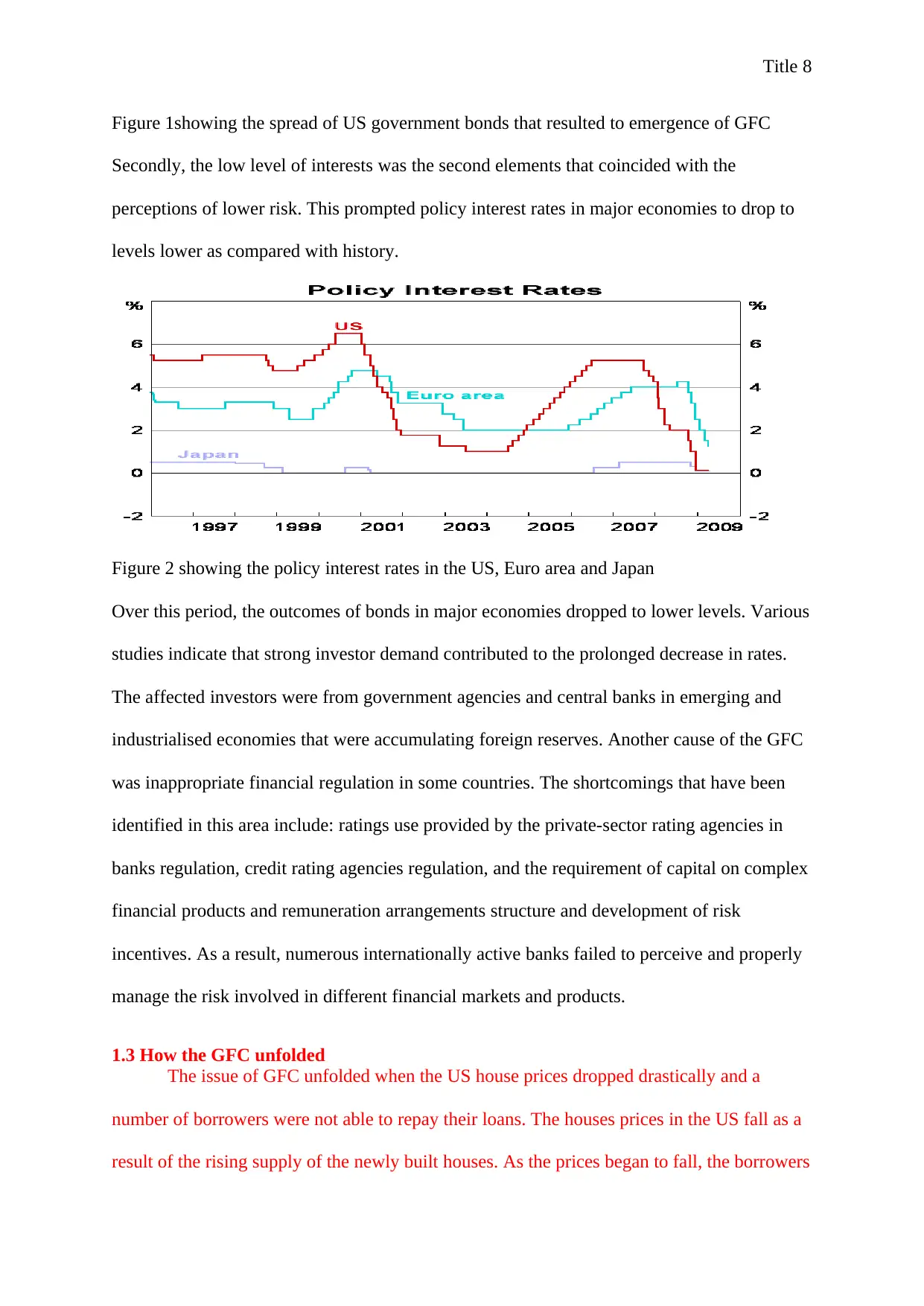

Secondly, the low level of interests was the second elements that coincided with the

perceptions of lower risk. This prompted policy interest rates in major economies to drop to

levels lower as compared with history.

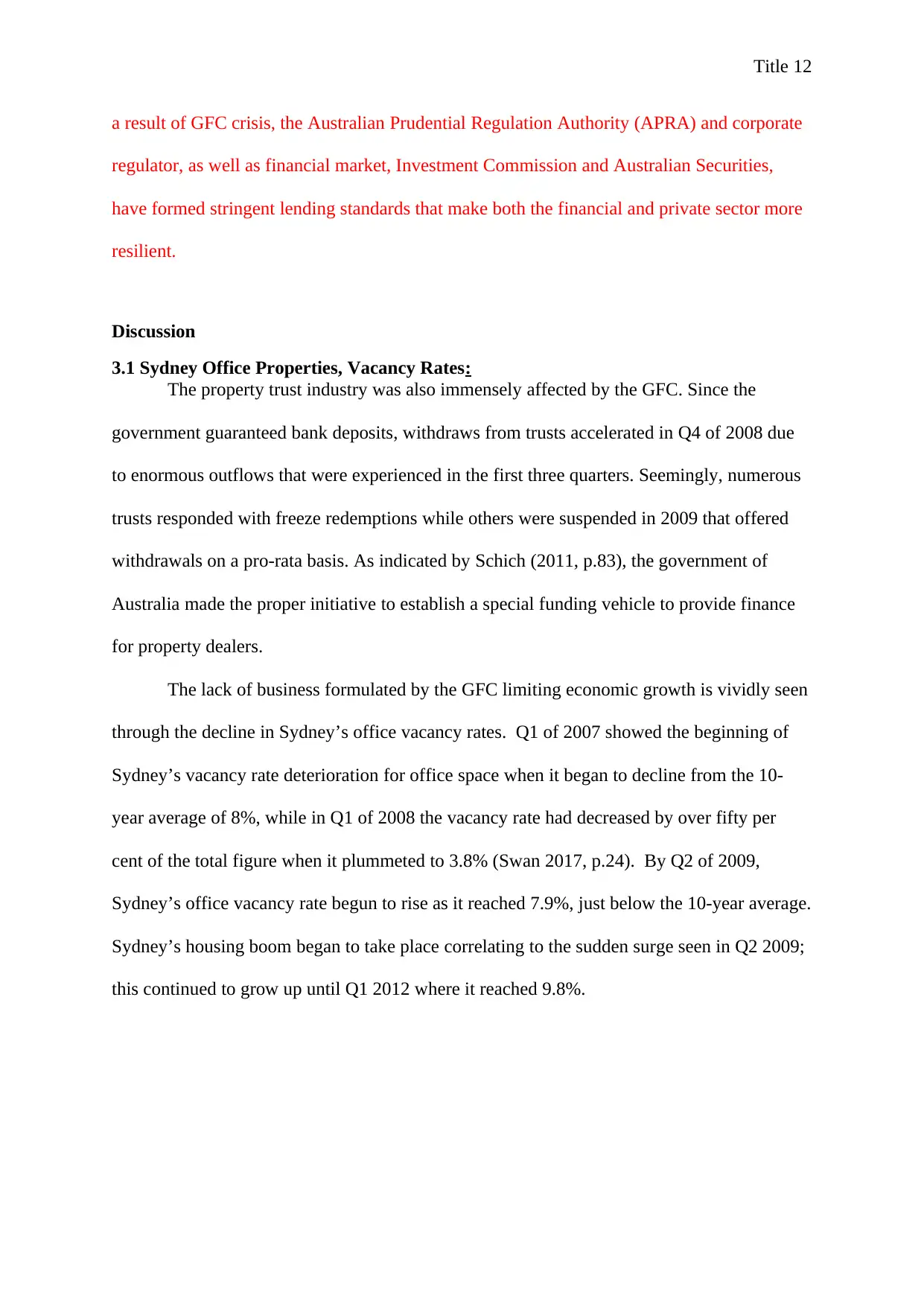

Figure 2 showing the policy interest rates in the US, Euro area and Japan

Over this period, the outcomes of bonds in major economies dropped to lower levels. Various

studies indicate that strong investor demand contributed to the prolonged decrease in rates.

The affected investors were from government agencies and central banks in emerging and

industrialised economies that were accumulating foreign reserves. Another cause of the GFC

was inappropriate financial regulation in some countries. The shortcomings that have been

identified in this area include: ratings use provided by the private-sector rating agencies in

banks regulation, credit rating agencies regulation, and the requirement of capital on complex

financial products and remuneration arrangements structure and development of risk

incentives. As a result, numerous internationally active banks failed to perceive and properly

manage the risk involved in different financial markets and products.

1.3 How the GFC unfolded

The issue of GFC unfolded when the US house prices dropped drastically and a

number of borrowers were not able to repay their loans. The houses prices in the US fall as a

result of the rising supply of the newly built houses. As the prices began to fall, the borrowers

Figure 1showing the spread of US government bonds that resulted to emergence of GFC

Secondly, the low level of interests was the second elements that coincided with the

perceptions of lower risk. This prompted policy interest rates in major economies to drop to

levels lower as compared with history.

Figure 2 showing the policy interest rates in the US, Euro area and Japan

Over this period, the outcomes of bonds in major economies dropped to lower levels. Various

studies indicate that strong investor demand contributed to the prolonged decrease in rates.

The affected investors were from government agencies and central banks in emerging and

industrialised economies that were accumulating foreign reserves. Another cause of the GFC

was inappropriate financial regulation in some countries. The shortcomings that have been

identified in this area include: ratings use provided by the private-sector rating agencies in

banks regulation, credit rating agencies regulation, and the requirement of capital on complex

financial products and remuneration arrangements structure and development of risk

incentives. As a result, numerous internationally active banks failed to perceive and properly

manage the risk involved in different financial markets and products.

1.3 How the GFC unfolded

The issue of GFC unfolded when the US house prices dropped drastically and a

number of borrowers were not able to repay their loans. The houses prices in the US fall as a

result of the rising supply of the newly built houses. As the prices began to fall, the borrowers

Title 9

failed to pay for their loans and their number increased. In the US, the loan repayment was

sensitive to house prices making the proportion of US households with large debts to

increase. Due to GFC, the financial system also experienced stress. Many investors and

lenders started to experience major losses because their houses had been repossessed after

failing to pay the loan balance. Investors were not willing to buy MBS products and working

tirelessly to sell their holdings. Failure to buy MBS by investors reduced the prices of MBS

which eventually declined the value of MBS.

Literature review

2.1The GFC’s impact on Australia:

The impact the Global Financial Crisis held on Australia when shown in comparison

to the greater worldwide developed countries affected by the GFC, provides the image that

Australia was able to brush majority of the negative factors that were associated with the

GFC. Despite the effects of the GFC in 2009, Australia would perform to see a high in GDP

at 1.6% that would then plateau and again begin to rise in the fourth quarter of 2009,

prompting the idea that Australia was working its way out of the GFC with positive results

(Santos 2016, p. 461).

2.2 The GFC and impact on Australian Bank Risk

Reviewing Australia’s structured financial system, it is astonishing that Australia was

to an extent, largely unaffected by the impacts that were emplaced after the Global Financial

Crisis. Australia and its bank appeared immune to the credit crunch. As most countries were

cutting local interest rates, the Reserve Bank of Australia increased the rates. When the global

share markets experienced a huge fall in 2008, Australia share market became unstable and

most of its banks suffered accordingly. Behind America the largest economy in the world,

Australia was ranked as the second largest distributor of asset-backed securities with the

fourth biggest fund managerial sector in the world at 1.2 trillion dollars (AUD) (RBA, 2017,

failed to pay for their loans and their number increased. In the US, the loan repayment was

sensitive to house prices making the proportion of US households with large debts to

increase. Due to GFC, the financial system also experienced stress. Many investors and

lenders started to experience major losses because their houses had been repossessed after

failing to pay the loan balance. Investors were not willing to buy MBS products and working

tirelessly to sell their holdings. Failure to buy MBS by investors reduced the prices of MBS

which eventually declined the value of MBS.

Literature review

2.1The GFC’s impact on Australia:

The impact the Global Financial Crisis held on Australia when shown in comparison

to the greater worldwide developed countries affected by the GFC, provides the image that

Australia was able to brush majority of the negative factors that were associated with the

GFC. Despite the effects of the GFC in 2009, Australia would perform to see a high in GDP

at 1.6% that would then plateau and again begin to rise in the fourth quarter of 2009,

prompting the idea that Australia was working its way out of the GFC with positive results

(Santos 2016, p. 461).

2.2 The GFC and impact on Australian Bank Risk

Reviewing Australia’s structured financial system, it is astonishing that Australia was

to an extent, largely unaffected by the impacts that were emplaced after the Global Financial

Crisis. Australia and its bank appeared immune to the credit crunch. As most countries were

cutting local interest rates, the Reserve Bank of Australia increased the rates. When the global

share markets experienced a huge fall in 2008, Australia share market became unstable and

most of its banks suffered accordingly. Behind America the largest economy in the world,

Australia was ranked as the second largest distributor of asset-backed securities with the

fourth biggest fund managerial sector in the world at 1.2 trillion dollars (AUD) (RBA, 2017,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Title 10

p.99). Australian Banks were also seen after the GFC to have less than 18% of assets held in

offshore funding, while still being active in the international bond market with the biggest

hedge fund sector in Asia (Schwartz 2015, p. 19). Due to these figures, the average for an

Australian home price was seen to be at its most affordable point in history, as the average

house price slowly rose again.

Although Australia was viewed through performance indicators as the economies top

contender throughout and post the GFC, it did not, however, escape from the GFC unscarred.

Australian banks were seen to hold steady after the collapse of Americas fourth largest

financial firm Lehman Brothers Holdings, showing Australia’s integrity when they were

ranked in the top 40 banks worldwide after the Reserve Bank of Australia and the Federal

Government provided guaranteed bank deposits through the introduction of the Guarantee

Scheme to further encourage investors into long term bank debt and prompt continual growth

in the economy (RBA 2017, p.104). Post GFC, The RBA and the Australian Federal

Government continued to work simultaneously to ensure positive changes were made via

updated regulations in order to adapt to the conditions faced, while also controlling further

destruction to the already struggling economy.

After the introduction of the Guarantee Scheme that was run for a period of three

years, the RBA with revised securities allowed for guaranteed debt and deposits under $1m

(AUD) and fee-based options for debt and deposits over $1m (AUD), in an effort to re-

liquidise Australian financial markets (Schich 2008, p.76). According to Rudd (2009, p.20),

the scheme was to operate as a segment of the new retail deposit which guaranteed wholesale

term funding of Australian incorporated banks and other deposit-taking institutions that had

to pay a specified fee in return. As a result of these policy responses, financial market

conditions improved in the course of 2009. This was achieved through the abating of the

averted risk.

p.99). Australian Banks were also seen after the GFC to have less than 18% of assets held in

offshore funding, while still being active in the international bond market with the biggest

hedge fund sector in Asia (Schwartz 2015, p. 19). Due to these figures, the average for an

Australian home price was seen to be at its most affordable point in history, as the average

house price slowly rose again.

Although Australia was viewed through performance indicators as the economies top

contender throughout and post the GFC, it did not, however, escape from the GFC unscarred.

Australian banks were seen to hold steady after the collapse of Americas fourth largest

financial firm Lehman Brothers Holdings, showing Australia’s integrity when they were

ranked in the top 40 banks worldwide after the Reserve Bank of Australia and the Federal

Government provided guaranteed bank deposits through the introduction of the Guarantee

Scheme to further encourage investors into long term bank debt and prompt continual growth

in the economy (RBA 2017, p.104). Post GFC, The RBA and the Australian Federal

Government continued to work simultaneously to ensure positive changes were made via

updated regulations in order to adapt to the conditions faced, while also controlling further

destruction to the already struggling economy.

After the introduction of the Guarantee Scheme that was run for a period of three

years, the RBA with revised securities allowed for guaranteed debt and deposits under $1m

(AUD) and fee-based options for debt and deposits over $1m (AUD), in an effort to re-

liquidise Australian financial markets (Schich 2008, p.76). According to Rudd (2009, p.20),

the scheme was to operate as a segment of the new retail deposit which guaranteed wholesale

term funding of Australian incorporated banks and other deposit-taking institutions that had

to pay a specified fee in return. As a result of these policy responses, financial market

conditions improved in the course of 2009. This was achieved through the abating of the

averted risk.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Title 11

The Australian share market then recovered almost half of their decline while credit

markets drastically started to reopen and function normally. The GFC effects in Australia

were considered minor as compared to different major economies. In this regard, the

Australian economy continued to record a significant growth outcome than other developed

countries that were exposed to severe recessions and a rise in unemployment. The financial

system of Australia was more resilient and most Australian banks profited and did not require

any help from the Government.

As much as the Australian economy remains relatively stable, the financial crisis is

not immune. The growth in the economy slowed by half a per cent and the unemployment

rate further rose to approximately 5.75 per cent in 2009 (Felton and Reinhart 2011, p.75). The

major impact of the financial crisis on Australian households was extensively felt in the

decline of equity prices that decreased Australian households’ wealth to almost 10 per cent.

However, at the end of 2009, Australian local market recovered half of its decline. As the

crisis intensified, the Australian dollar depreciated drastically by over 30 per cent. Lehman

bankruptcy made foreign exchange condition illiquid. This prompted the Reserve Bank of

Australia to take part in the market to improve market liquidity. Due to this intervention, the

Australian dollar recovered at a greater extent reflecting the relative potential of the

Australian economy.

Additionally, the money and credit markets of Australia have proven to be resilient as

compared to many economies therefore, necessitating less intervention by the Reserve Bank

of Australia. On a wide scope, this has reflected the integrity and health of the Australian

banking system. During the GFC period, most banks in Australia had minimal holdings of

these chronic securities that affected other worldwide banks (Gueyie 2013, p.252). The

Australian banking system facilitated effectiveness in both fiscal and monetary response by

easily allowing monetary policy to be passed through interest rates on loans to businesses. As

The Australian share market then recovered almost half of their decline while credit

markets drastically started to reopen and function normally. The GFC effects in Australia

were considered minor as compared to different major economies. In this regard, the

Australian economy continued to record a significant growth outcome than other developed

countries that were exposed to severe recessions and a rise in unemployment. The financial

system of Australia was more resilient and most Australian banks profited and did not require

any help from the Government.

As much as the Australian economy remains relatively stable, the financial crisis is

not immune. The growth in the economy slowed by half a per cent and the unemployment

rate further rose to approximately 5.75 per cent in 2009 (Felton and Reinhart 2011, p.75). The

major impact of the financial crisis on Australian households was extensively felt in the

decline of equity prices that decreased Australian households’ wealth to almost 10 per cent.

However, at the end of 2009, Australian local market recovered half of its decline. As the

crisis intensified, the Australian dollar depreciated drastically by over 30 per cent. Lehman

bankruptcy made foreign exchange condition illiquid. This prompted the Reserve Bank of

Australia to take part in the market to improve market liquidity. Due to this intervention, the

Australian dollar recovered at a greater extent reflecting the relative potential of the

Australian economy.

Additionally, the money and credit markets of Australia have proven to be resilient as

compared to many economies therefore, necessitating less intervention by the Reserve Bank

of Australia. On a wide scope, this has reflected the integrity and health of the Australian

banking system. During the GFC period, most banks in Australia had minimal holdings of

these chronic securities that affected other worldwide banks (Gueyie 2013, p.252). The

Australian banking system facilitated effectiveness in both fiscal and monetary response by

easily allowing monetary policy to be passed through interest rates on loans to businesses. As

Title 12

a result of GFC crisis, the Australian Prudential Regulation Authority (APRA) and corporate

regulator, as well as financial market, Investment Commission and Australian Securities,

have formed stringent lending standards that make both the financial and private sector more

resilient.

Discussion

3.1 Sydney Office Properties, Vacancy Rates:

The property trust industry was also immensely affected by the GFC. Since the

government guaranteed bank deposits, withdraws from trusts accelerated in Q4 of 2008 due

to enormous outflows that were experienced in the first three quarters. Seemingly, numerous

trusts responded with freeze redemptions while others were suspended in 2009 that offered

withdrawals on a pro-rata basis. As indicated by Schich (2011, p.83), the government of

Australia made the proper initiative to establish a special funding vehicle to provide finance

for property dealers.

The lack of business formulated by the GFC limiting economic growth is vividly seen

through the decline in Sydney’s office vacancy rates. Q1 of 2007 showed the beginning of

Sydney’s vacancy rate deterioration for office space when it began to decline from the 10-

year average of 8%, while in Q1 of 2008 the vacancy rate had decreased by over fifty per

cent of the total figure when it plummeted to 3.8% (Swan 2017, p.24). By Q2 of 2009,

Sydney’s office vacancy rate begun to rise as it reached 7.9%, just below the 10-year average.

Sydney’s housing boom began to take place correlating to the sudden surge seen in Q2 2009;

this continued to grow up until Q1 2012 where it reached 9.8%.

a result of GFC crisis, the Australian Prudential Regulation Authority (APRA) and corporate

regulator, as well as financial market, Investment Commission and Australian Securities,

have formed stringent lending standards that make both the financial and private sector more

resilient.

Discussion

3.1 Sydney Office Properties, Vacancy Rates:

The property trust industry was also immensely affected by the GFC. Since the

government guaranteed bank deposits, withdraws from trusts accelerated in Q4 of 2008 due

to enormous outflows that were experienced in the first three quarters. Seemingly, numerous

trusts responded with freeze redemptions while others were suspended in 2009 that offered

withdrawals on a pro-rata basis. As indicated by Schich (2011, p.83), the government of

Australia made the proper initiative to establish a special funding vehicle to provide finance

for property dealers.

The lack of business formulated by the GFC limiting economic growth is vividly seen

through the decline in Sydney’s office vacancy rates. Q1 of 2007 showed the beginning of

Sydney’s vacancy rate deterioration for office space when it began to decline from the 10-

year average of 8%, while in Q1 of 2008 the vacancy rate had decreased by over fifty per

cent of the total figure when it plummeted to 3.8% (Swan 2017, p.24). By Q2 of 2009,

Sydney’s office vacancy rate begun to rise as it reached 7.9%, just below the 10-year average.

Sydney’s housing boom began to take place correlating to the sudden surge seen in Q2 2009;

this continued to grow up until Q1 2012 where it reached 9.8%.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 28

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.