Economics Report: Commercial Property Valuation and Lease Analysis

VerifiedAdded on 2021/01/09

|30

|5481

|33

Report

AI Summary

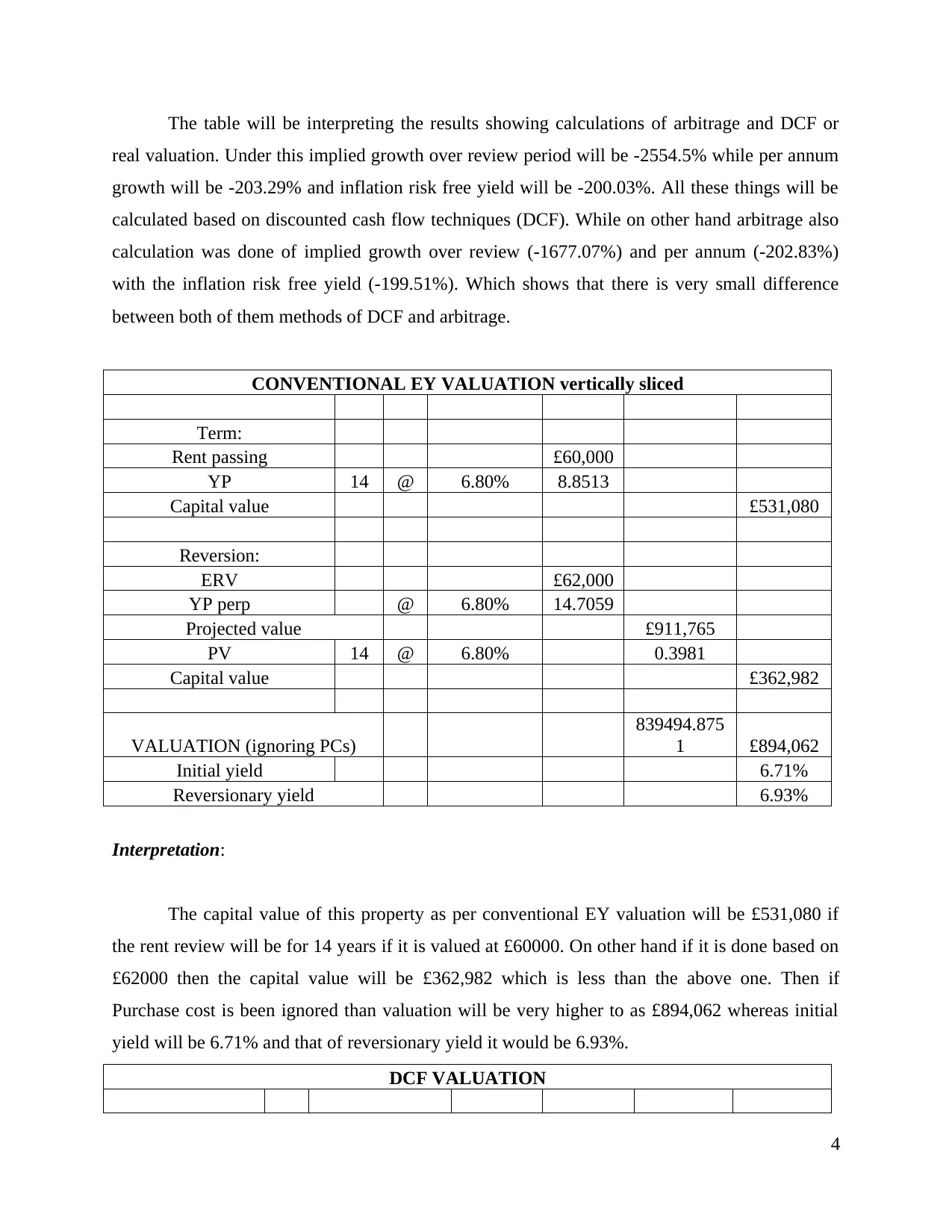

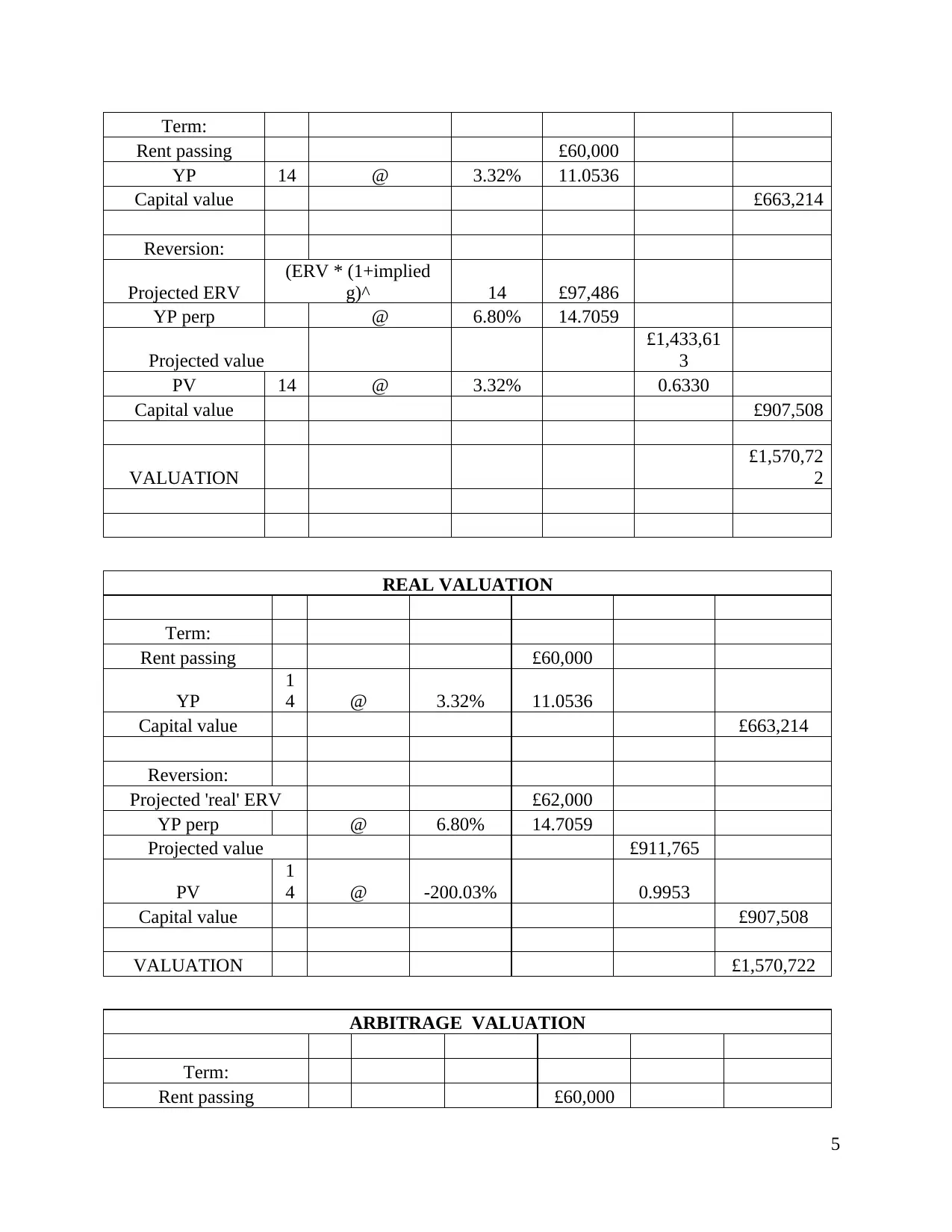

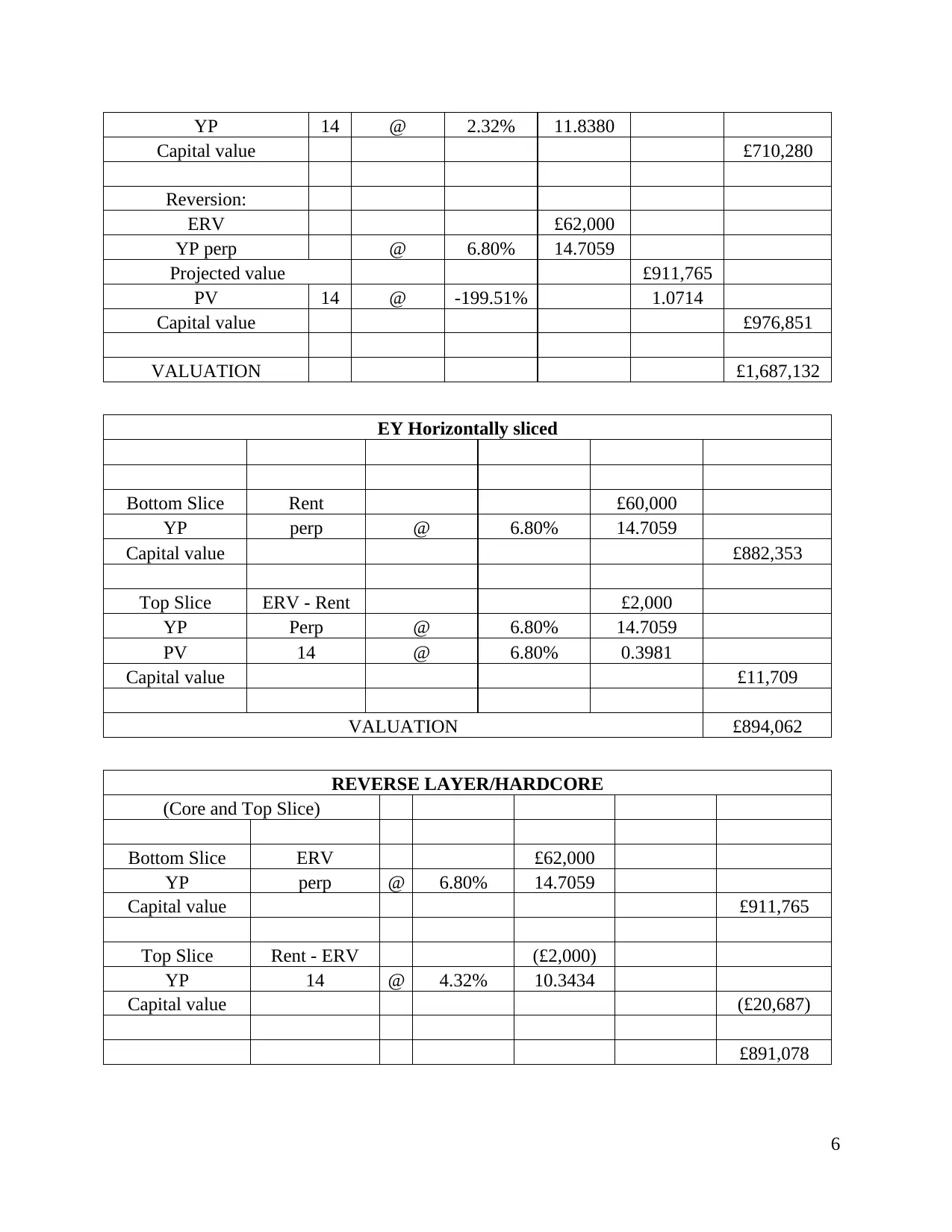

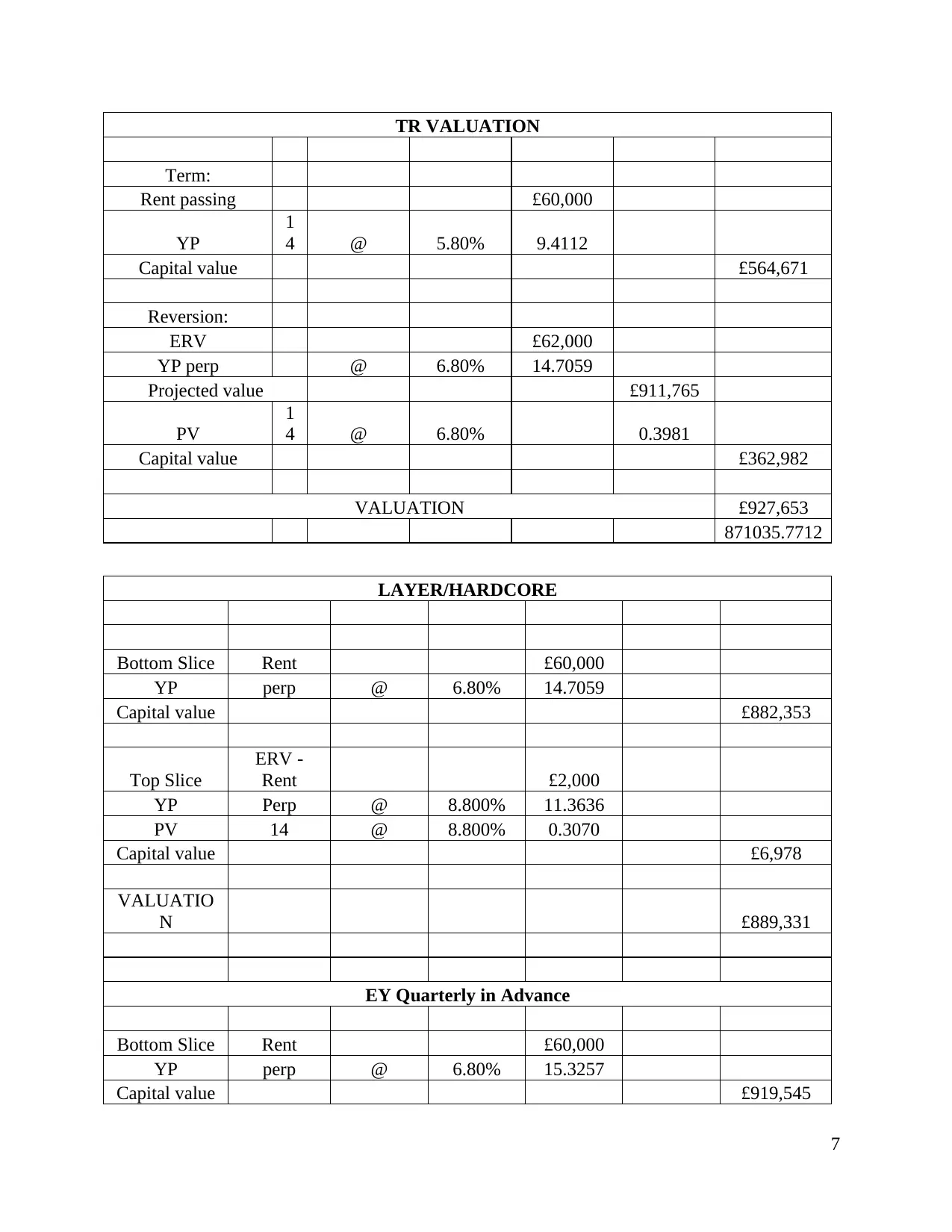

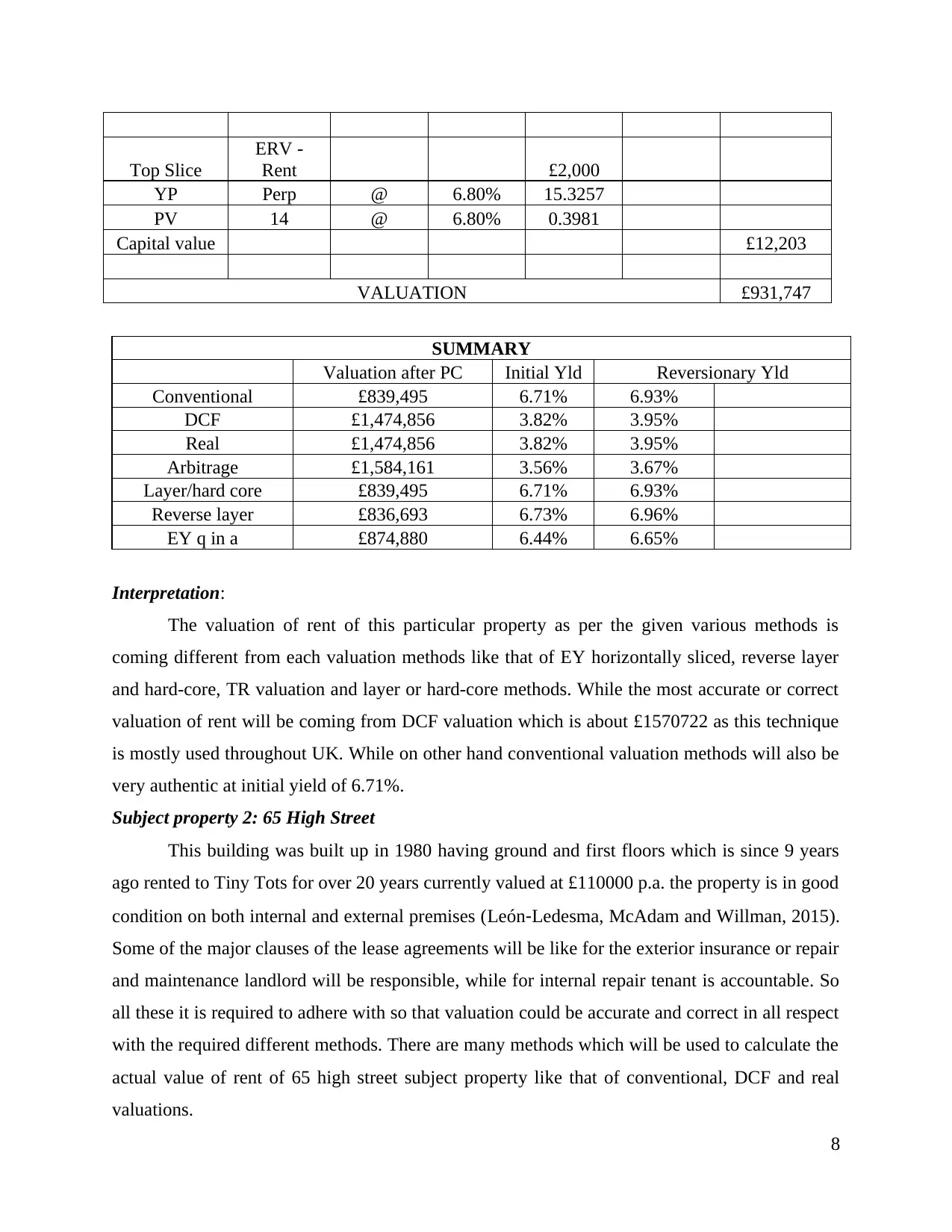

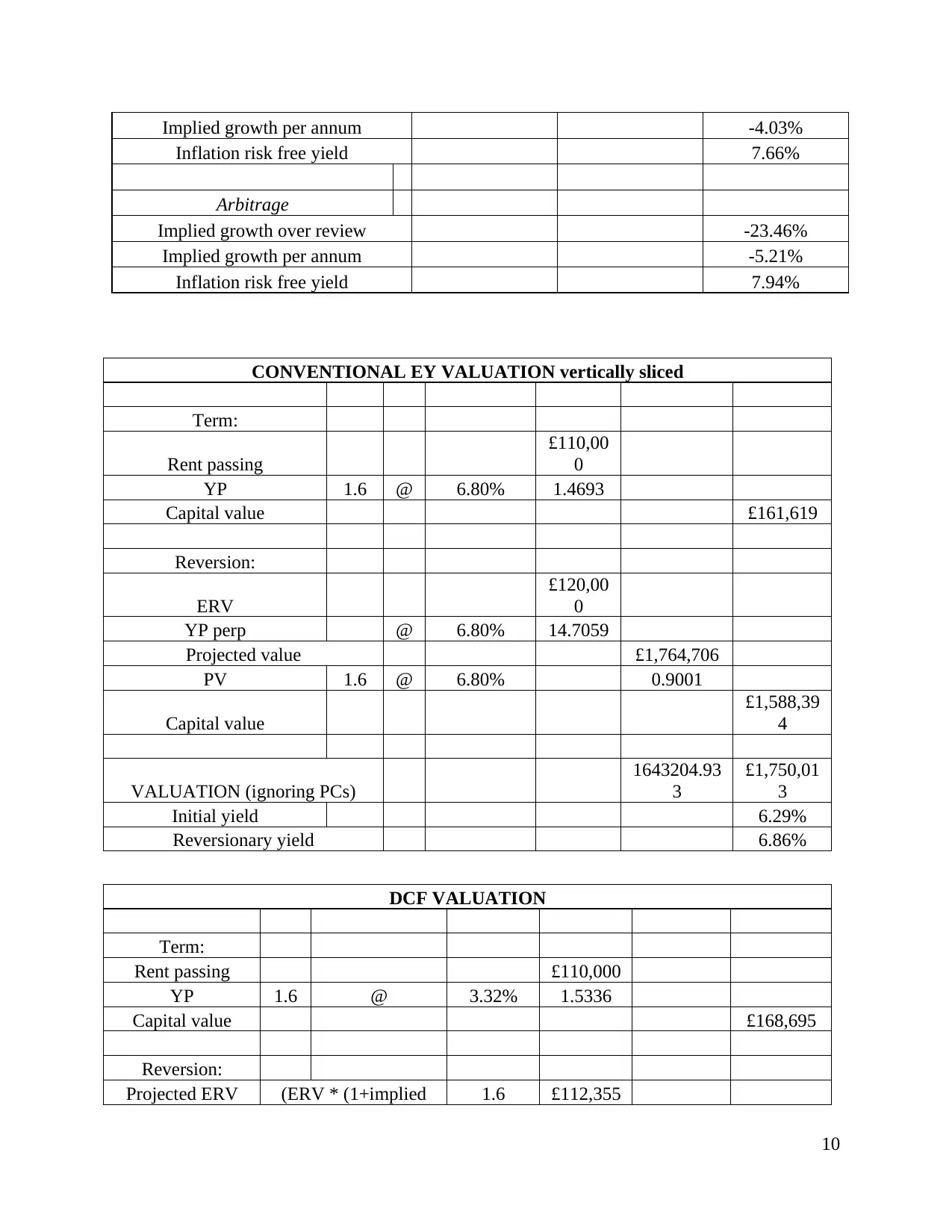

This report provides a detailed analysis of commercial property valuation and lease agreements in the UK, focusing on two subject properties: 72 and 65 High Street. It examines major lease clauses, including rent review mechanisms, tenant and landlord responsibilities, and property conditions. The report utilizes various valuation methods, such as conventional, DCF, and arbitrage, to determine the fair market rent for each property, considering factors like initial yield, risk-free rates, and purchase costs. Calculations and interpretations are presented for each method, highlighting the differences in valuation results and identifying the most accurate approaches. The report also includes details of comparable properties to support the valuation process. This report provides a comprehensive overview of commercial property valuation techniques, making it a valuable resource for students studying economics and real estate.

1 out of 30

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.