HI5002 Finance for Business: CBA Financial Performance Analysis Report

VerifiedAdded on 2022/11/24

|12

|3160

|312

Report

AI Summary

This report presents a comprehensive financial analysis of the Commonwealth Bank of Australia (CBA), examining its performance over a three-year period. The analysis includes an overview of the company, followed by a detailed examination of its financial ratios, including profitability and operating efficiency ratios. The report delves into CBA's dividend policy, analyzing dividend payouts and trends. It also covers the concepts of systematic and unsystematic risk, providing insights into the risks faced by the bank. Based on the financial analysis, the report offers a recommendation to an institutional investor regarding investment in CBA. The analysis utilizes financial data to assess the bank's performance, providing a thorough understanding of its financial health and investment potential.

Running Head: FINANCE FOR BUSINESS 1

FINANCE FOR BUSINESS

[Name of Writer]

[Name of Institution]

FINANCE FOR BUSINESS

[Name of Writer]

[Name of Institution]

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR BUSINESS 2

I. Introduction:

This paper is aimed to observe and analyze financial status of any selected

organization and will be communicated to an institutional investor. Organization must be

listed at Australian Stock Exchange and industry with lucrative expected return. After

industry analysis, Commonwealth Bank of Australia is finalized and will analyzed for

financial performance over three years. Commonwealth Bank of Australia operates in

banking sector and register under ticker name of CBA. Commonwealth Bank of

Australia provide a range of financial services to Australia and abroad. Historical data of

Commonwealth Bank of Australia shows a stable growth and share price. There is no

any abnormal growth or deterioration of share price and net income. This report is

divided into three parts overview of selected company, financial analysis and

recommendation. Profitability ratios of Commonwealth Bank of Australia will be

analyzed to determine ability of organization to generate profit. Apart from profitability

ratios, operating efficiency ratios for last three years will also be discussed. Every

investor is interested to know about dividend trend and dividend policy of organization

therefore, dividend payout and current dividend policy will be discussed in detail. This

report also contain literature about Systematic risk and un-systemic risk. Based on the

financial analysis of the selected organization, a recommendation will be handed over to

investor. Recommendation letter will contain suggestion to invest or not to invest in

Commonwealth Bank of Australia.

II. Financial Analysis

II.1. Description of Company

Commonwealth Bank of Australia is listed on Australian Stock Exchange under

code CBA. Commonwealth Bank of Australia was established under banking act of

commonwealth in 1911 and just after one year it started its operation. Commonwealth

Bank of Australia started both general and saving services for Australia. With a

continuous and stable growth strategy, Commonwealth Bank is considered among

largest banks of world. Currently, there are almost 0.8 Million shareholders and about

52 thousand employees work in Commonwealth Bank of Australia. A large range of

financial services are provided to individual and institutional investors over the globe.

Commonwealth Bank provides saving and transaction accounts, term deposits,

personal and business loans, credit cards, insurance products, international payment,

and private banking services along with home loans (Yahoo Finance, 2019).

Commonwealth Bank of Australia also provide assets management services, debt

raising services and financial assistance. Commonwealth Bank facilitate customers with

more than 1000 branches and more than 4000 Automated Teller Machines alone in

Australia.

I. Introduction:

This paper is aimed to observe and analyze financial status of any selected

organization and will be communicated to an institutional investor. Organization must be

listed at Australian Stock Exchange and industry with lucrative expected return. After

industry analysis, Commonwealth Bank of Australia is finalized and will analyzed for

financial performance over three years. Commonwealth Bank of Australia operates in

banking sector and register under ticker name of CBA. Commonwealth Bank of

Australia provide a range of financial services to Australia and abroad. Historical data of

Commonwealth Bank of Australia shows a stable growth and share price. There is no

any abnormal growth or deterioration of share price and net income. This report is

divided into three parts overview of selected company, financial analysis and

recommendation. Profitability ratios of Commonwealth Bank of Australia will be

analyzed to determine ability of organization to generate profit. Apart from profitability

ratios, operating efficiency ratios for last three years will also be discussed. Every

investor is interested to know about dividend trend and dividend policy of organization

therefore, dividend payout and current dividend policy will be discussed in detail. This

report also contain literature about Systematic risk and un-systemic risk. Based on the

financial analysis of the selected organization, a recommendation will be handed over to

investor. Recommendation letter will contain suggestion to invest or not to invest in

Commonwealth Bank of Australia.

II. Financial Analysis

II.1. Description of Company

Commonwealth Bank of Australia is listed on Australian Stock Exchange under

code CBA. Commonwealth Bank of Australia was established under banking act of

commonwealth in 1911 and just after one year it started its operation. Commonwealth

Bank of Australia started both general and saving services for Australia. With a

continuous and stable growth strategy, Commonwealth Bank is considered among

largest banks of world. Currently, there are almost 0.8 Million shareholders and about

52 thousand employees work in Commonwealth Bank of Australia. A large range of

financial services are provided to individual and institutional investors over the globe.

Commonwealth Bank provides saving and transaction accounts, term deposits,

personal and business loans, credit cards, insurance products, international payment,

and private banking services along with home loans (Yahoo Finance, 2019).

Commonwealth Bank of Australia also provide assets management services, debt

raising services and financial assistance. Commonwealth Bank facilitate customers with

more than 1000 branches and more than 4000 Automated Teller Machines alone in

Australia.

FINANCE FOR BUSINESS 3

There are many events in the history of Commonwealth Bank of Australia that

contributed to success such as mergers, acquisitions, international expansion and

innovative financial services. Among all, merger with State Bank of Victoria is

considered as reason of success and competitive advantage. In august 1990,

Commonwealth Bank of Australia initiated an agreement to merge with State Bank of

Victoria. This event helped organization to develop its leadership and paved into retail

branch banking services. Over a period of more than one century, Commonwealth Bank

of Australia faced many radical changes and risks but not only managed to survive but

pursued stable growth.

II.2. Ratio Analysis

Financial ratio analysis is a tool to analyze financial status of firms with simple

calculation (Babalola & Abiola, 2013). Financial experts have categorized financial

ratios to serve investors different purposes (Brown, 2012). Profitability ratios will help

investors to understand the ability of organization to generate profit for each dollar

invested (Petria, Capraru & Ihnatov, 2015). Operating efficiency ratios are used to

determine efficiency of firm in operations.

Operating efficiency ratios also known as activity ratios are used by management

and investors to measure ability of organization to utilize assets to generate sales

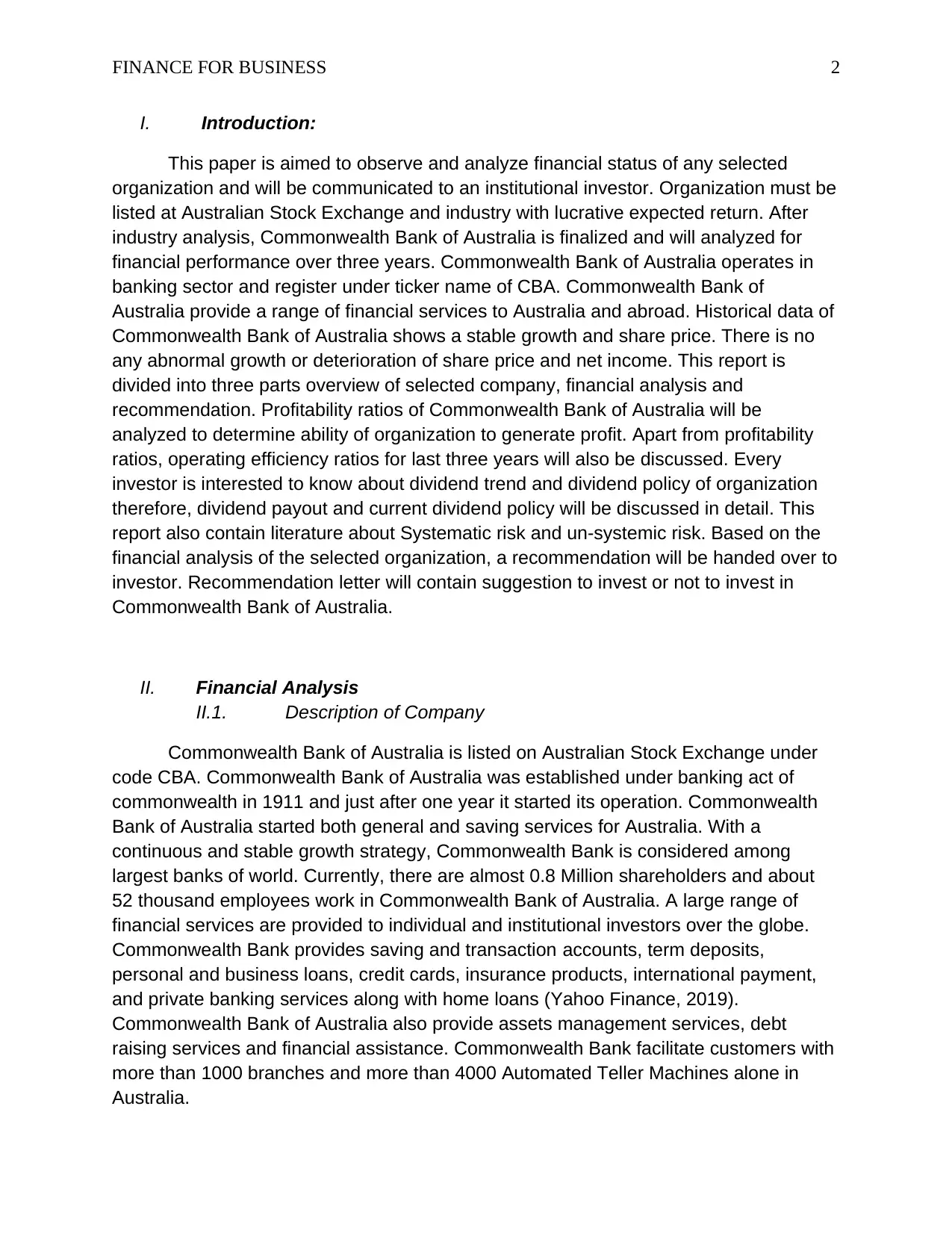

(Odunga, Nyangweso, Carter & Mwarumba, 2013). Net asset turnover shows that how

effectively resources are utilized by management to generate revenue (Lin, Liang &

Chen, 2011). Higher ratio shows that company is effectively utilizing resources to

generate revenue while lower ratio shows efficiency. Net asset turnover ratio of

Commonwealth Bank of Australia was 38.25%, 40.65% and 44.64% in year 2018, 2017

and 2016 respectively (Morningstar, 2019). Every year net asset turnover ratio is

decreasing which means that organization possess many idle resources. Other possible

reason for decline in net asset turnover ratio is highly expensive assets which are either

not used in sales generation or ineffectively used. Given below is graph of net asset

turnover ratio.

2016 2017 2018

0.34

0.36

0.38

0.4

0.42

0.44

0.46

0.4464290

4290429

0.4065277

91345121 0.3825444

63886243

Net Assets Turnover Ratio

There are many events in the history of Commonwealth Bank of Australia that

contributed to success such as mergers, acquisitions, international expansion and

innovative financial services. Among all, merger with State Bank of Victoria is

considered as reason of success and competitive advantage. In august 1990,

Commonwealth Bank of Australia initiated an agreement to merge with State Bank of

Victoria. This event helped organization to develop its leadership and paved into retail

branch banking services. Over a period of more than one century, Commonwealth Bank

of Australia faced many radical changes and risks but not only managed to survive but

pursued stable growth.

II.2. Ratio Analysis

Financial ratio analysis is a tool to analyze financial status of firms with simple

calculation (Babalola & Abiola, 2013). Financial experts have categorized financial

ratios to serve investors different purposes (Brown, 2012). Profitability ratios will help

investors to understand the ability of organization to generate profit for each dollar

invested (Petria, Capraru & Ihnatov, 2015). Operating efficiency ratios are used to

determine efficiency of firm in operations.

Operating efficiency ratios also known as activity ratios are used by management

and investors to measure ability of organization to utilize assets to generate sales

(Odunga, Nyangweso, Carter & Mwarumba, 2013). Net asset turnover shows that how

effectively resources are utilized by management to generate revenue (Lin, Liang &

Chen, 2011). Higher ratio shows that company is effectively utilizing resources to

generate revenue while lower ratio shows efficiency. Net asset turnover ratio of

Commonwealth Bank of Australia was 38.25%, 40.65% and 44.64% in year 2018, 2017

and 2016 respectively (Morningstar, 2019). Every year net asset turnover ratio is

decreasing which means that organization possess many idle resources. Other possible

reason for decline in net asset turnover ratio is highly expensive assets which are either

not used in sales generation or ineffectively used. Given below is graph of net asset

turnover ratio.

2016 2017 2018

0.34

0.36

0.38

0.4

0.42

0.44

0.46

0.4464290

4290429

0.4065277

91345121 0.3825444

63886243

Net Assets Turnover Ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS 4

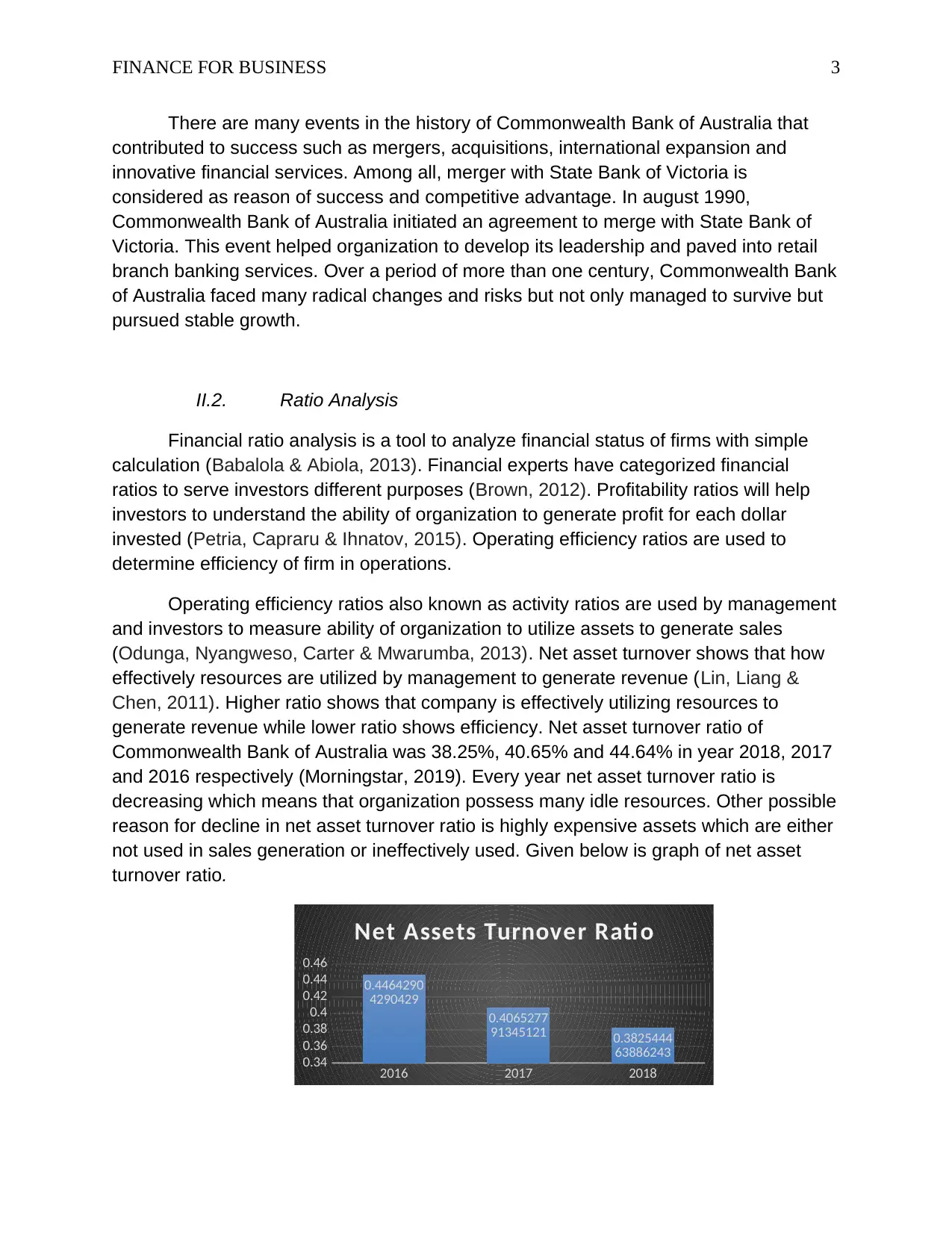

Efficiency ratio is widely used by banks because it tells ability of organization to

transform resources into revenue (Trujillo, 2013). Lower efficiency ratio is better

because lower ratio shows that company is effectively handling costs. A higher

efficiency ratio is associated with more inefficiency because more portion of revenue

goes to costs. Efficiency ratios of Commonwealth Bank of Australia were 46.9%, 47.1%

and 49.9% in 2018, 2017 and 2016 respectively. Efficiency ratio of Commonwealth

Bank of Australia is decreasing every year. Decreasing efficiency ratio means that

organizational performance and efficiency is improving. Given below is graph of

efficiency ratios for last three years that shows decreasing trend.

2016 2017 2018

0.45

0.46

0.47

0.48

0.49

0.5

0.51

0.4992163

70464559

0.4713603

46018683 0.4690385

89583997

Effi ciency Rati o

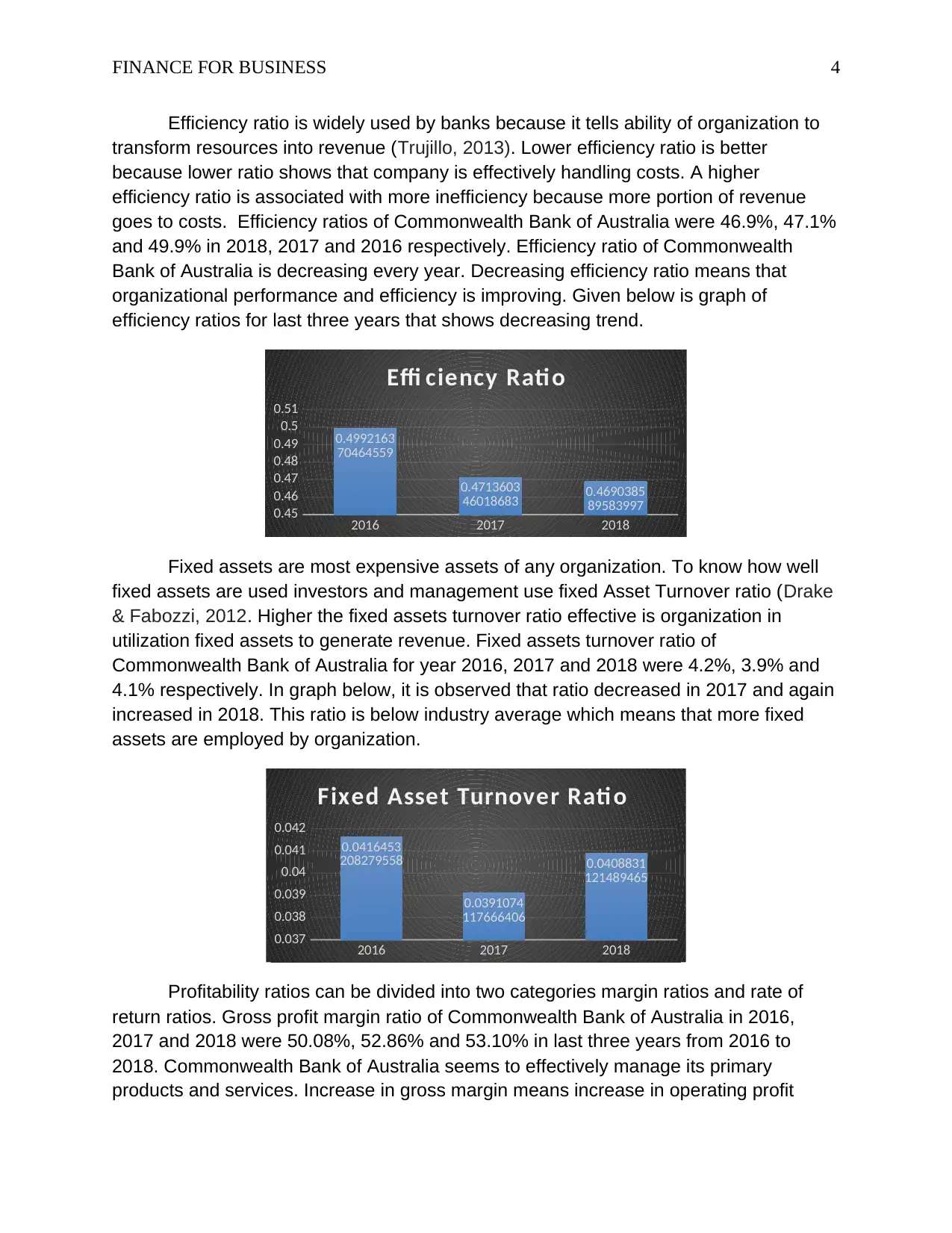

Fixed assets are most expensive assets of any organization. To know how well

fixed assets are used investors and management use fixed Asset Turnover ratio (Drake

& Fabozzi, 2012. Higher the fixed assets turnover ratio effective is organization in

utilization fixed assets to generate revenue. Fixed assets turnover ratio of

Commonwealth Bank of Australia for year 2016, 2017 and 2018 were 4.2%, 3.9% and

4.1% respectively. In graph below, it is observed that ratio decreased in 2017 and again

increased in 2018. This ratio is below industry average which means that more fixed

assets are employed by organization.

2016 2017 2018

0.037

0.038

0.039

0.04

0.041

0.042

0.0416453

208279558

0.0391074

117666406

0.0408831

121489465

Fixed Asset Turnover Rati o

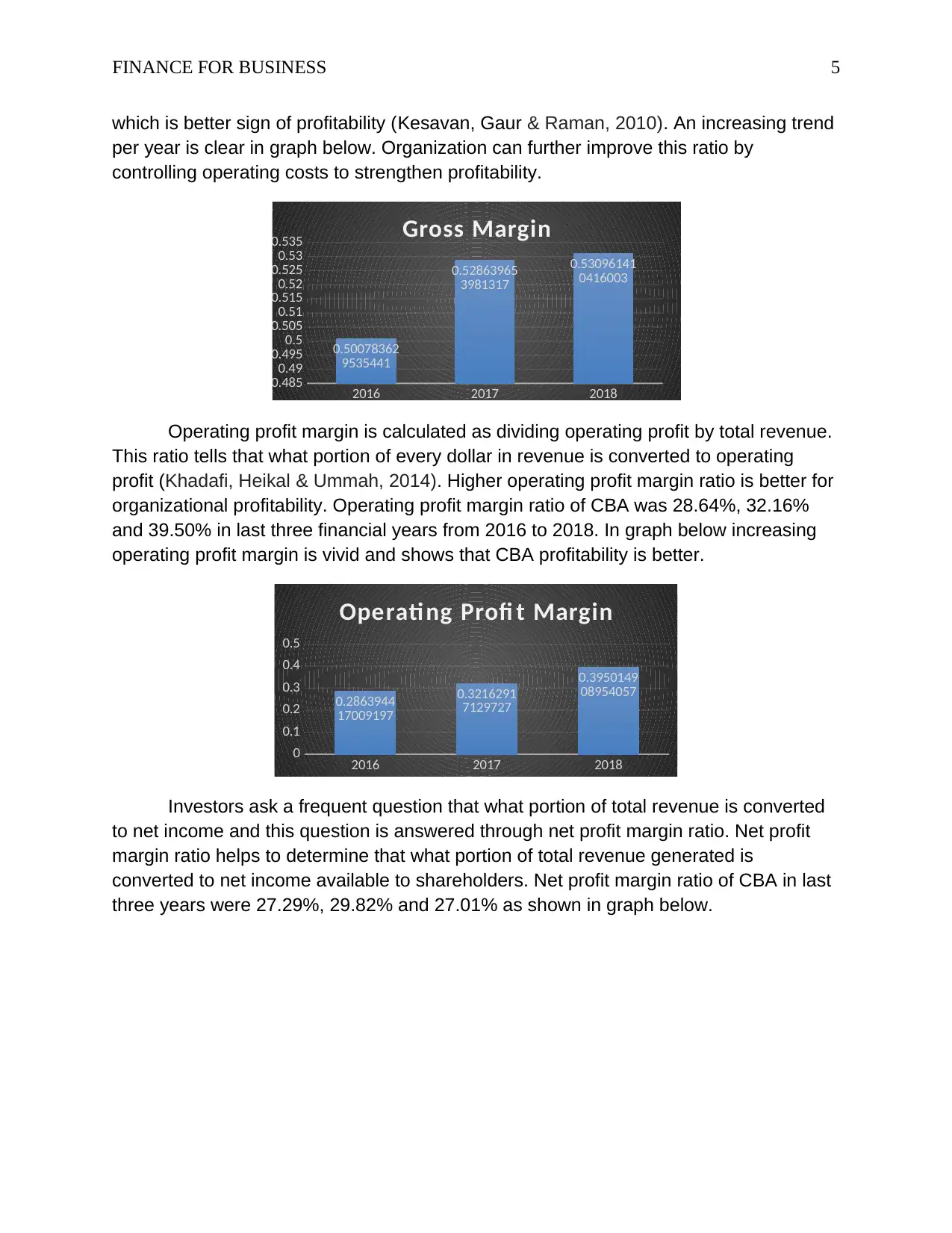

Profitability ratios can be divided into two categories margin ratios and rate of

return ratios. Gross profit margin ratio of Commonwealth Bank of Australia in 2016,

2017 and 2018 were 50.08%, 52.86% and 53.10% in last three years from 2016 to

2018. Commonwealth Bank of Australia seems to effectively manage its primary

products and services. Increase in gross margin means increase in operating profit

Efficiency ratio is widely used by banks because it tells ability of organization to

transform resources into revenue (Trujillo, 2013). Lower efficiency ratio is better

because lower ratio shows that company is effectively handling costs. A higher

efficiency ratio is associated with more inefficiency because more portion of revenue

goes to costs. Efficiency ratios of Commonwealth Bank of Australia were 46.9%, 47.1%

and 49.9% in 2018, 2017 and 2016 respectively. Efficiency ratio of Commonwealth

Bank of Australia is decreasing every year. Decreasing efficiency ratio means that

organizational performance and efficiency is improving. Given below is graph of

efficiency ratios for last three years that shows decreasing trend.

2016 2017 2018

0.45

0.46

0.47

0.48

0.49

0.5

0.51

0.4992163

70464559

0.4713603

46018683 0.4690385

89583997

Effi ciency Rati o

Fixed assets are most expensive assets of any organization. To know how well

fixed assets are used investors and management use fixed Asset Turnover ratio (Drake

& Fabozzi, 2012. Higher the fixed assets turnover ratio effective is organization in

utilization fixed assets to generate revenue. Fixed assets turnover ratio of

Commonwealth Bank of Australia for year 2016, 2017 and 2018 were 4.2%, 3.9% and

4.1% respectively. In graph below, it is observed that ratio decreased in 2017 and again

increased in 2018. This ratio is below industry average which means that more fixed

assets are employed by organization.

2016 2017 2018

0.037

0.038

0.039

0.04

0.041

0.042

0.0416453

208279558

0.0391074

117666406

0.0408831

121489465

Fixed Asset Turnover Rati o

Profitability ratios can be divided into two categories margin ratios and rate of

return ratios. Gross profit margin ratio of Commonwealth Bank of Australia in 2016,

2017 and 2018 were 50.08%, 52.86% and 53.10% in last three years from 2016 to

2018. Commonwealth Bank of Australia seems to effectively manage its primary

products and services. Increase in gross margin means increase in operating profit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR BUSINESS 5

which is better sign of profitability (Kesavan, Gaur & Raman, 2010). An increasing trend

per year is clear in graph below. Organization can further improve this ratio by

controlling operating costs to strengthen profitability.

2016 2017 2018

0.485

0.49

0.495

0.5

0.505

0.51

0.515

0.52

0.525

0.53

0.535

0.50078362

9535441

0.52863965

3981317

0.53096141

0416003

Gross Margin

Operating profit margin is calculated as dividing operating profit by total revenue.

This ratio tells that what portion of every dollar in revenue is converted to operating

profit (Khadafi, Heikal & Ummah, 2014). Higher operating profit margin ratio is better for

organizational profitability. Operating profit margin ratio of CBA was 28.64%, 32.16%

and 39.50% in last three financial years from 2016 to 2018. In graph below increasing

operating profit margin is vivid and shows that CBA profitability is better.

2016 2017 2018

0

0.1

0.2

0.3

0.4

0.5

0.2863944

17009197

0.3216291

7129727

0.3950149

08954057

Operati ng Profi t Margin

Investors ask a frequent question that what portion of total revenue is converted

to net income and this question is answered through net profit margin ratio. Net profit

margin ratio helps to determine that what portion of total revenue generated is

converted to net income available to shareholders. Net profit margin ratio of CBA in last

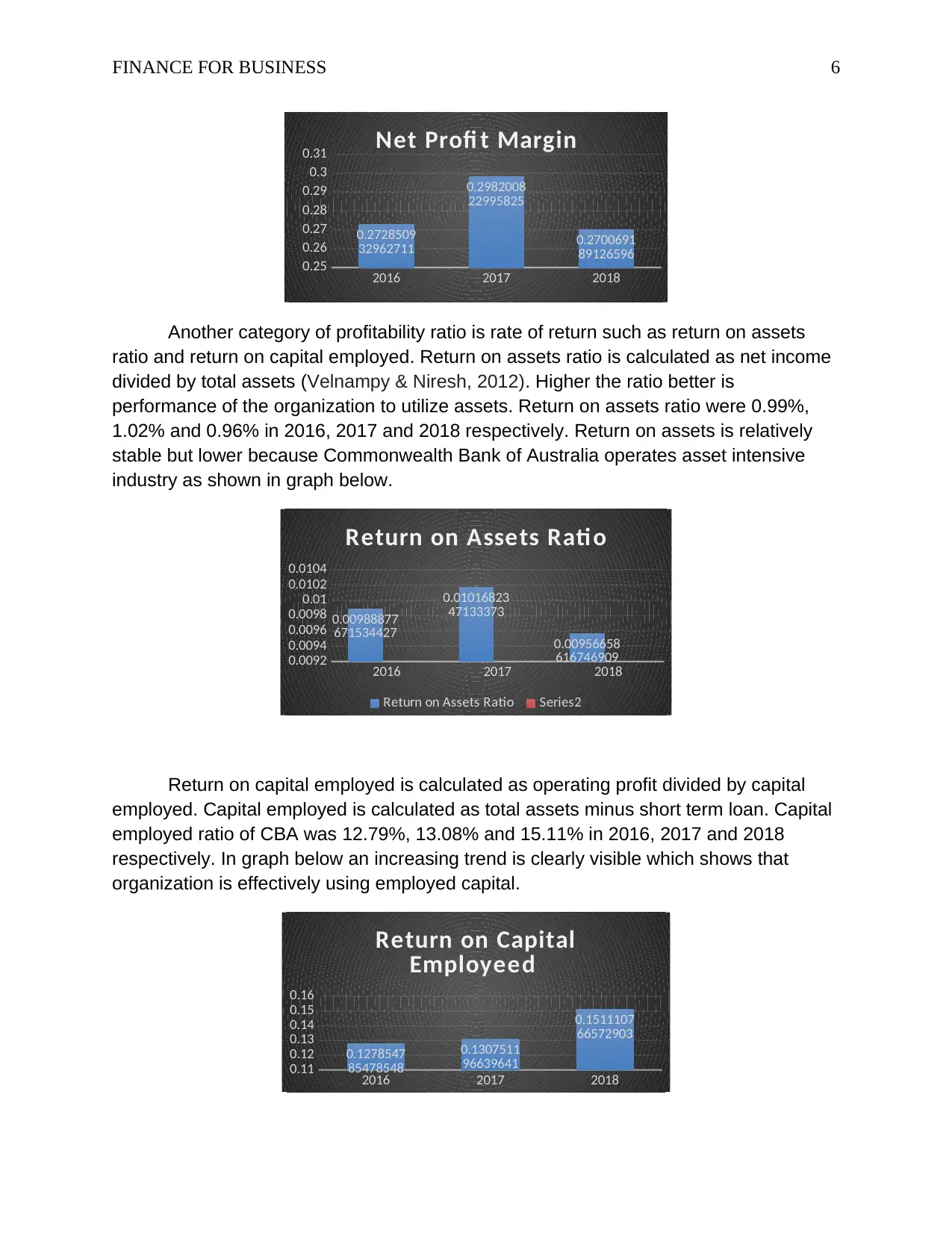

three years were 27.29%, 29.82% and 27.01% as shown in graph below.

which is better sign of profitability (Kesavan, Gaur & Raman, 2010). An increasing trend

per year is clear in graph below. Organization can further improve this ratio by

controlling operating costs to strengthen profitability.

2016 2017 2018

0.485

0.49

0.495

0.5

0.505

0.51

0.515

0.52

0.525

0.53

0.535

0.50078362

9535441

0.52863965

3981317

0.53096141

0416003

Gross Margin

Operating profit margin is calculated as dividing operating profit by total revenue.

This ratio tells that what portion of every dollar in revenue is converted to operating

profit (Khadafi, Heikal & Ummah, 2014). Higher operating profit margin ratio is better for

organizational profitability. Operating profit margin ratio of CBA was 28.64%, 32.16%

and 39.50% in last three financial years from 2016 to 2018. In graph below increasing

operating profit margin is vivid and shows that CBA profitability is better.

2016 2017 2018

0

0.1

0.2

0.3

0.4

0.5

0.2863944

17009197

0.3216291

7129727

0.3950149

08954057

Operati ng Profi t Margin

Investors ask a frequent question that what portion of total revenue is converted

to net income and this question is answered through net profit margin ratio. Net profit

margin ratio helps to determine that what portion of total revenue generated is

converted to net income available to shareholders. Net profit margin ratio of CBA in last

three years were 27.29%, 29.82% and 27.01% as shown in graph below.

FINANCE FOR BUSINESS 6

2016 2017 2018

0.25

0.26

0.27

0.28

0.29

0.3

0.31

0.2728509

32962711

0.2982008

22995825

0.2700691

89126596

Net Profi t Margin

Another category of profitability ratio is rate of return such as return on assets

ratio and return on capital employed. Return on assets ratio is calculated as net income

divided by total assets (Velnampy & Niresh, 2012). Higher the ratio better is

performance of the organization to utilize assets. Return on assets ratio were 0.99%,

1.02% and 0.96% in 2016, 2017 and 2018 respectively. Return on assets is relatively

stable but lower because Commonwealth Bank of Australia operates asset intensive

industry as shown in graph below.

2016 2017 2018

0.0092

0.0094

0.0096

0.0098

0.01

0.0102

0.0104

0.00988877

671534427

0.01016823

47133373

0.00956658

616746909

Return on Assets Rati o

Return on Assets Ratio Series2

Return on capital employed is calculated as operating profit divided by capital

employed. Capital employed is calculated as total assets minus short term loan. Capital

employed ratio of CBA was 12.79%, 13.08% and 15.11% in 2016, 2017 and 2018

respectively. In graph below an increasing trend is clearly visible which shows that

organization is effectively using employed capital.

2016 2017 2018

0.11

0.12

0.13

0.14

0.15

0.16

0.1278547

85478548

0.1307511

96639641

0.1511107

66572903

Return on Capital

Employeed

2016 2017 2018

0.25

0.26

0.27

0.28

0.29

0.3

0.31

0.2728509

32962711

0.2982008

22995825

0.2700691

89126596

Net Profi t Margin

Another category of profitability ratio is rate of return such as return on assets

ratio and return on capital employed. Return on assets ratio is calculated as net income

divided by total assets (Velnampy & Niresh, 2012). Higher the ratio better is

performance of the organization to utilize assets. Return on assets ratio were 0.99%,

1.02% and 0.96% in 2016, 2017 and 2018 respectively. Return on assets is relatively

stable but lower because Commonwealth Bank of Australia operates asset intensive

industry as shown in graph below.

2016 2017 2018

0.0092

0.0094

0.0096

0.0098

0.01

0.0102

0.0104

0.00988877

671534427

0.01016823

47133373

0.00956658

616746909

Return on Assets Rati o

Return on Assets Ratio Series2

Return on capital employed is calculated as operating profit divided by capital

employed. Capital employed is calculated as total assets minus short term loan. Capital

employed ratio of CBA was 12.79%, 13.08% and 15.11% in 2016, 2017 and 2018

respectively. In graph below an increasing trend is clearly visible which shows that

organization is effectively using employed capital.

2016 2017 2018

0.11

0.12

0.13

0.14

0.15

0.16

0.1278547

85478548

0.1307511

96639641

0.1511107

66572903

Return on Capital

Employeed

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS 7

II.3. Cash Management Analysis

Cash management is vital for competitive advantage and survival in competitive

environment (Kusnadi & Wei, 2011). Marketable securities are used as alternative to

cash because it can be easily converted to cash by selling in public exchange (Brown,

2014). Significant amount of Commonwealth bank’s assets comprises of marketable

securities. There are different types of marketable securities but serve same purpose.

Derivative assets and debt security are two important marketable securities which are

used in Commonwealth Bank of Australia for cash management purpose. Cash in bank

or cash in hand does not earn profit and termed as idle cash therefore, organizations

invest in marketable securities (Subramaniam, Tang, Yue & Zhou, 2011). Debt

securities are short term debt instruments that are issued by other firms and purchased

by Commonwealth Bank of Australia.

Marketable securities are listed in current asset section of balance sheet

because these can be easily converted to cash. Marketable debt securities earn interest

and can be sold at any time to other institute. Banks generally provide overnight loan

which is also a short term investment. At time of acquisition or any even that requires

cash, company will sell marketable debt securities. Commonwealth Bank of Australia on

average hold 15% of current assets as cash. Holding large amount of cash at branches

also reduces performance of organization.

II.4. Sensitivity Analysis with provided data

This section is available in excel file.

II.5. Systematic and Unsystematic risk

Risk is inherent part of every business whether it is local or international (Reuvid,

2010). According to definition, risk can be systematic or market risk and un-systematic

risk or company risk. Systematic risk is same for every organization and industry that

operates in market and no organization can control it (Savor & Wilson, 2016).

Systematic risk cannot be diversified through diversification because it affects every

participant of market. Systematic risk arises form macroeconomic factors such as

change in government policies, natural disaster, factors of international trade and shift in

economic indicators (Chen, Xu & Yang, 2012). According to financial report of

Commonwealth Bank of Australia, CBA faces interest rate risk and inflation risk. Market

risk that CBA faces are changes in interest rates, foreign exchange rates, equity and

commodity prices, credit spreads, and the resale value of operating leased assets at

maturity (CBA,2018). Systematic risk strongly affects overall profitability of the

organization and net profit.

II.3. Cash Management Analysis

Cash management is vital for competitive advantage and survival in competitive

environment (Kusnadi & Wei, 2011). Marketable securities are used as alternative to

cash because it can be easily converted to cash by selling in public exchange (Brown,

2014). Significant amount of Commonwealth bank’s assets comprises of marketable

securities. There are different types of marketable securities but serve same purpose.

Derivative assets and debt security are two important marketable securities which are

used in Commonwealth Bank of Australia for cash management purpose. Cash in bank

or cash in hand does not earn profit and termed as idle cash therefore, organizations

invest in marketable securities (Subramaniam, Tang, Yue & Zhou, 2011). Debt

securities are short term debt instruments that are issued by other firms and purchased

by Commonwealth Bank of Australia.

Marketable securities are listed in current asset section of balance sheet

because these can be easily converted to cash. Marketable debt securities earn interest

and can be sold at any time to other institute. Banks generally provide overnight loan

which is also a short term investment. At time of acquisition or any even that requires

cash, company will sell marketable debt securities. Commonwealth Bank of Australia on

average hold 15% of current assets as cash. Holding large amount of cash at branches

also reduces performance of organization.

II.4. Sensitivity Analysis with provided data

This section is available in excel file.

II.5. Systematic and Unsystematic risk

Risk is inherent part of every business whether it is local or international (Reuvid,

2010). According to definition, risk can be systematic or market risk and un-systematic

risk or company risk. Systematic risk is same for every organization and industry that

operates in market and no organization can control it (Savor & Wilson, 2016).

Systematic risk cannot be diversified through diversification because it affects every

participant of market. Systematic risk arises form macroeconomic factors such as

change in government policies, natural disaster, factors of international trade and shift in

economic indicators (Chen, Xu & Yang, 2012). According to financial report of

Commonwealth Bank of Australia, CBA faces interest rate risk and inflation risk. Market

risk that CBA faces are changes in interest rates, foreign exchange rates, equity and

commodity prices, credit spreads, and the resale value of operating leased assets at

maturity (CBA,2018). Systematic risk strongly affects overall profitability of the

organization and net profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR BUSINESS 8

Unsystematic risk on other hand is company alone risk or industry alone risk

which can be controlled through strong risk management initiatives. Unsystematic risk

can be diversified and diminished through management actions. Unsystematic risk that

CBA faces are compliance risk, insurance risk, credit risk, operational risk and strategic

risk (CBA, 2017).

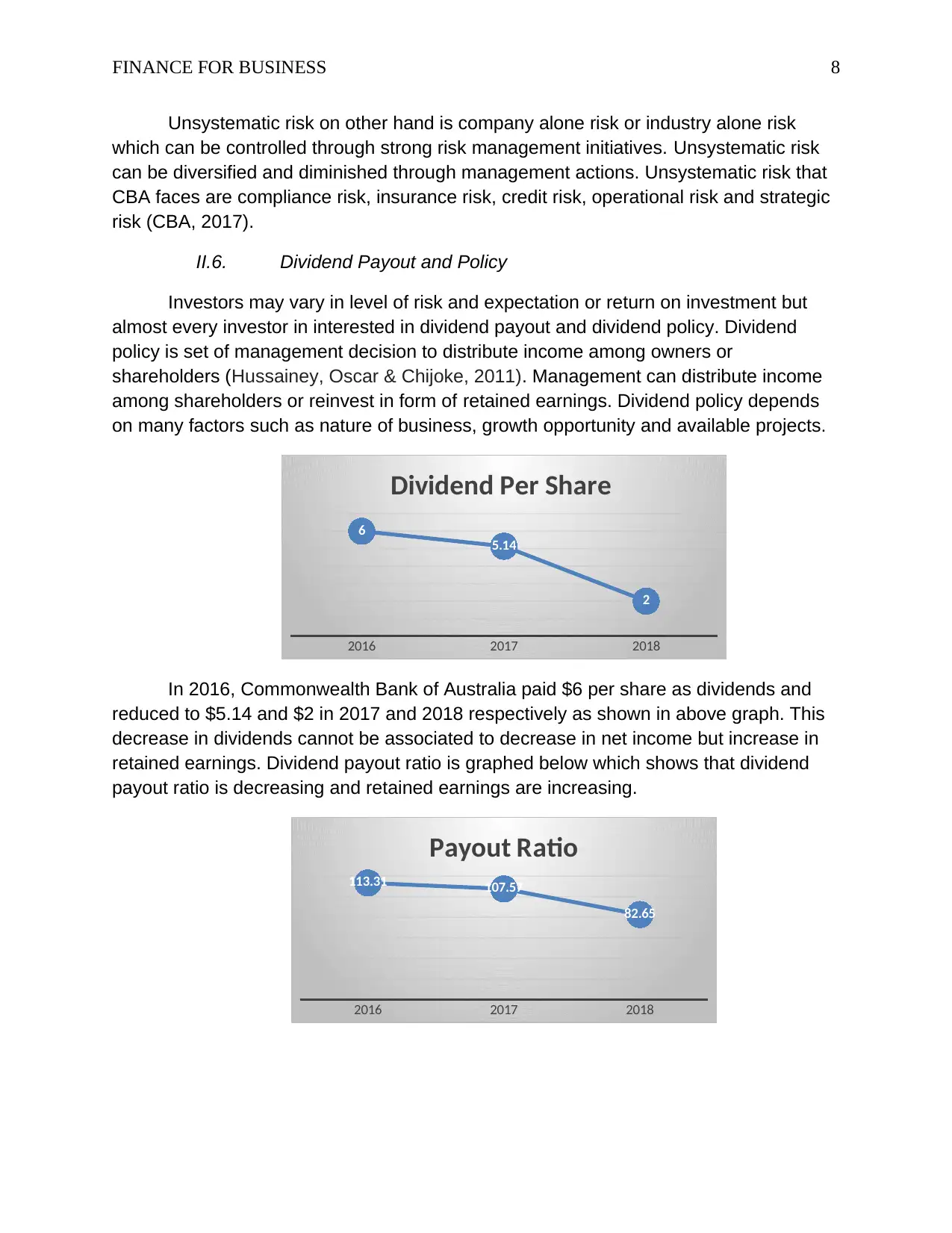

II.6. Dividend Payout and Policy

Investors may vary in level of risk and expectation or return on investment but

almost every investor in interested in dividend payout and dividend policy. Dividend

policy is set of management decision to distribute income among owners or

shareholders (Hussainey, Oscar & Chijoke, 2011). Management can distribute income

among shareholders or reinvest in form of retained earnings. Dividend policy depends

on many factors such as nature of business, growth opportunity and available projects.

2016 2017 2018

6

5.14

2

Dividend Per Share

In 2016, Commonwealth Bank of Australia paid $6 per share as dividends and

reduced to $5.14 and $2 in 2017 and 2018 respectively as shown in above graph. This

decrease in dividends cannot be associated to decrease in net income but increase in

retained earnings. Dividend payout ratio is graphed below which shows that dividend

payout ratio is decreasing and retained earnings are increasing.

2016 2017 2018

113.31 107.57

82.65

Payout Ratio

Unsystematic risk on other hand is company alone risk or industry alone risk

which can be controlled through strong risk management initiatives. Unsystematic risk

can be diversified and diminished through management actions. Unsystematic risk that

CBA faces are compliance risk, insurance risk, credit risk, operational risk and strategic

risk (CBA, 2017).

II.6. Dividend Payout and Policy

Investors may vary in level of risk and expectation or return on investment but

almost every investor in interested in dividend payout and dividend policy. Dividend

policy is set of management decision to distribute income among owners or

shareholders (Hussainey, Oscar & Chijoke, 2011). Management can distribute income

among shareholders or reinvest in form of retained earnings. Dividend policy depends

on many factors such as nature of business, growth opportunity and available projects.

2016 2017 2018

6

5.14

2

Dividend Per Share

In 2016, Commonwealth Bank of Australia paid $6 per share as dividends and

reduced to $5.14 and $2 in 2017 and 2018 respectively as shown in above graph. This

decrease in dividends cannot be associated to decrease in net income but increase in

retained earnings. Dividend payout ratio is graphed below which shows that dividend

payout ratio is decreasing and retained earnings are increasing.

2016 2017 2018

113.31 107.57

82.65

Payout Ratio

FINANCE FOR BUSINESS 9

2016 2017 2018

23,627 26,330 28,360

Retained Earnings

In 2018, net income of CBA faced noteworthy decrease which affected dividend per

share and dividend payout ratio. In 2016, company paid 100% of net income as

dividend and plus 13% from retained earnings. While in 2017, 107% of net income was

paid as dividend. Commonwealth Bank of Australia has a continuous history of dividend

payment. Because management believes that there is relationship between dividend

payment and share price increase.

III. Recommendation

Financial information users study financial information of firms to make effective

decision. Financial information of the multinational business is prepared in complex

method and it is difficult to understand without some financial techniques. In order to

clearly communicate the financial health and history of Commonwealth Bank of

Australia, we have conducted ratio analysis and dividend policy analysis. Each ratio is

discussed with graph for CBA data which shows that firm is both profitable and growing.

Dividend policy of CBA is very attractive because they pay good portion of income as

dividend and invest some portion in projects.

Based on financial analysis and historical performance of Commonwealth Bank

of Australia, it is recommended that it is profitable to invest in Commonwealth Bank of

Australia.

2016 2017 2018

23,627 26,330 28,360

Retained Earnings

In 2018, net income of CBA faced noteworthy decrease which affected dividend per

share and dividend payout ratio. In 2016, company paid 100% of net income as

dividend and plus 13% from retained earnings. While in 2017, 107% of net income was

paid as dividend. Commonwealth Bank of Australia has a continuous history of dividend

payment. Because management believes that there is relationship between dividend

payment and share price increase.

III. Recommendation

Financial information users study financial information of firms to make effective

decision. Financial information of the multinational business is prepared in complex

method and it is difficult to understand without some financial techniques. In order to

clearly communicate the financial health and history of Commonwealth Bank of

Australia, we have conducted ratio analysis and dividend policy analysis. Each ratio is

discussed with graph for CBA data which shows that firm is both profitable and growing.

Dividend policy of CBA is very attractive because they pay good portion of income as

dividend and invest some portion in projects.

Based on financial analysis and historical performance of Commonwealth Bank

of Australia, it is recommended that it is profitable to invest in Commonwealth Bank of

Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FINANCE FOR BUSINESS 10

References

Babalola, Y.A. and Abiola, F.R., 2013. Financial ratio analysis of firms: A tool for

decision making. International journal of management sciences, 1(4), pp.132-137.

http://www.academia.edu/download/32371001/Paper_4.pdf

Brown, C., 2014. Marketable securities: Storage or investment?. Available at SSRN

1446683. http://citeseerx.ist.psu.edu/viewdoc/download?

doi=10.1.1.710.116&rep=rep1&type=pdf

Brown, R., 2012. Analysis of investments & management of portfolios.

http://dspace.lzuu.lt/bitstream/1/1911/1/Analysis%20of%20investments

%20%26%20management%20of%20portfolios.pdf

CBA., 2017. Annual Report 2017. From the Official website of Commonwealth Bank of

Australia.

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/

annual-reports/annual_report_2017_14_aug_2017.pdf

CBA., 2018. Annual Report 2018. From the Official website of Commonwealth Bank of

Australia.

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/

results/fy18/cba-annual-report-2018.pdf

Chen, H., Xu, Y. and Yang, J., 2012. Systematic risk, debt maturity, and the term

structure of credit spreads (No. w18367). National Bureau of Economic Research.

https://www.nber.org/papers/w18367.pdf

Drake, P.P. and Fabozzi, F.J., 2012. Financial ratio analysis. Encyclopedia of Financial

Models. https://onlinelibrary.wiley.com/doi/abs/10.1002/9781118182635.efm0074

Hussainey, K., Oscar Mgbame, C. and Chijoke-Mgbame, A.M., 2011. Dividend policy

and share price volatility: UK evidence. The Journal of risk finance, 12(1), pp.57-68.

http://alqashi.com/wp/wp-content/uploads/2012/02/Dividend-policy-and-share-price-

volatility.pdf

Kesavan, S., Gaur, V. and Raman, A., 2010. Do inventory and gross margin data

improve sales forecasts for US public retailers?. Management Science, 56(9), pp.1519-

1533.

https://www.researchgate.net/profile/Vishal_Gaur/publication/220534775_Do_Inventory

_and_Gross_Margin_Data_Improve_Sales_Forecasts_for_US_Public_Retailers/links/

02e7e5319cace87fa1000000.pdf

References

Babalola, Y.A. and Abiola, F.R., 2013. Financial ratio analysis of firms: A tool for

decision making. International journal of management sciences, 1(4), pp.132-137.

http://www.academia.edu/download/32371001/Paper_4.pdf

Brown, C., 2014. Marketable securities: Storage or investment?. Available at SSRN

1446683. http://citeseerx.ist.psu.edu/viewdoc/download?

doi=10.1.1.710.116&rep=rep1&type=pdf

Brown, R., 2012. Analysis of investments & management of portfolios.

http://dspace.lzuu.lt/bitstream/1/1911/1/Analysis%20of%20investments

%20%26%20management%20of%20portfolios.pdf

CBA., 2017. Annual Report 2017. From the Official website of Commonwealth Bank of

Australia.

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/

annual-reports/annual_report_2017_14_aug_2017.pdf

CBA., 2018. Annual Report 2018. From the Official website of Commonwealth Bank of

Australia.

https://www.commbank.com.au/content/dam/commbank/about-us/shareholders/pdfs/

results/fy18/cba-annual-report-2018.pdf

Chen, H., Xu, Y. and Yang, J., 2012. Systematic risk, debt maturity, and the term

structure of credit spreads (No. w18367). National Bureau of Economic Research.

https://www.nber.org/papers/w18367.pdf

Drake, P.P. and Fabozzi, F.J., 2012. Financial ratio analysis. Encyclopedia of Financial

Models. https://onlinelibrary.wiley.com/doi/abs/10.1002/9781118182635.efm0074

Hussainey, K., Oscar Mgbame, C. and Chijoke-Mgbame, A.M., 2011. Dividend policy

and share price volatility: UK evidence. The Journal of risk finance, 12(1), pp.57-68.

http://alqashi.com/wp/wp-content/uploads/2012/02/Dividend-policy-and-share-price-

volatility.pdf

Kesavan, S., Gaur, V. and Raman, A., 2010. Do inventory and gross margin data

improve sales forecasts for US public retailers?. Management Science, 56(9), pp.1519-

1533.

https://www.researchgate.net/profile/Vishal_Gaur/publication/220534775_Do_Inventory

_and_Gross_Margin_Data_Improve_Sales_Forecasts_for_US_Public_Retailers/links/

02e7e5319cace87fa1000000.pdf

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCE FOR BUSINESS 11

Khadafi, M., Heikal, M. and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and

current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12). http://repository.unimal.ac.id/1351/1/Financial%20Performance.pdf

Kusnadi, Y. and Wei, K.J., 2011. The determinants of corporate cash management

policies: Evidence from around the world. Journal of Corporate Finance, 17(3), pp.725-

740.

https://pdfs.semanticscholar.org/49c4/15b9f64f718c30d00a77e2bacada5457a907.pdf

Lin, F., Liang, D. and Chen, E., 2011. Financial ratio selection for business crisis

prediction. Expert Systems with Applications, 38(12), pp.15094-15102.

https://isslab.csie.ncu.edu.tw/download/publications/10.pdf

Morningstar., 2019. CBA. Official website of Morning star.

https://www.morningstar.com/stocks/pinx/cbauf/quote.html

Odunga, R.M., Nyangweso, P.M., Carter, D.A. and Mwarumba, M., 2013. Credit

Risk,“Capital Adequacy and Operating Efficiency Of Commercial Banks in

Kenya”. International Journal of Business and Management Invention, 2(9), pp.6-12.

http://www.academia.edu/download/32103916/B029206012.pdf

Petria, N., Capraru, B. and Ihnatov, I., 2015. Determinants of banks’ profitability:

Evidence from EU 27 banking systems. Procedia Economics and Finance, 20, pp.518-

524. https://www.sciencedirect.com/science/article/pii/S2212567115001045/pdf?

md5=ad2a66b817cabd599251ca3369aa53ca&pid=1-s2.0-S2212567115001045-

main.pdf&_valck=1

Reuvid, J., 2010. Managing business risk: a practical guide to protecting your business.

Kogan Page Publishers. https://books.google.com./books?

hl=en&lr=&id=4aNO5PmbEtEC&oi=fnd&pg=PR16&dq=business+risk+&ots=sRsc3RxH

Lx&sig=N8gAN4yHV55GWPvfDQeIiqCFNYI#v=onepage&q=business%20risk&f=false

Savor, P. and Wilson, M., 2016. Earnings announcements and systematic risk. The

Journal of Finance, 71(1), pp.83-138.

https://pdfs.semanticscholar.org/4b37/e1bedd4b6d06b00c3cd28b9c00ce29a86bff.pdf

Subramaniam, V., Tang, T.T., Yue, H. and Zhou, X., 2011. Firm structure and corporate

cash holdings. Journal of Corporate Finance, 17(3), pp.759-773.

https://ink.library.smu.edu.sg/cgi/viewcontent.cgi?referer=https://scholar.google.com/

&httpsredir=1&article=2611&context=soa_research

Khadafi, M., Heikal, M. and Ummah, A., 2014. Influence analysis of return on assets

(ROA), return on equity (ROE), net profit margin (NPM), debt to equity ratio (DER), and

current ratio (CR), against corporate profit growth in automotive in Indonesia Stock

Exchange. International Journal of Academic Research in Business and Social

Sciences, 4(12). http://repository.unimal.ac.id/1351/1/Financial%20Performance.pdf

Kusnadi, Y. and Wei, K.J., 2011. The determinants of corporate cash management

policies: Evidence from around the world. Journal of Corporate Finance, 17(3), pp.725-

740.

https://pdfs.semanticscholar.org/49c4/15b9f64f718c30d00a77e2bacada5457a907.pdf

Lin, F., Liang, D. and Chen, E., 2011. Financial ratio selection for business crisis

prediction. Expert Systems with Applications, 38(12), pp.15094-15102.

https://isslab.csie.ncu.edu.tw/download/publications/10.pdf

Morningstar., 2019. CBA. Official website of Morning star.

https://www.morningstar.com/stocks/pinx/cbauf/quote.html

Odunga, R.M., Nyangweso, P.M., Carter, D.A. and Mwarumba, M., 2013. Credit

Risk,“Capital Adequacy and Operating Efficiency Of Commercial Banks in

Kenya”. International Journal of Business and Management Invention, 2(9), pp.6-12.

http://www.academia.edu/download/32103916/B029206012.pdf

Petria, N., Capraru, B. and Ihnatov, I., 2015. Determinants of banks’ profitability:

Evidence from EU 27 banking systems. Procedia Economics and Finance, 20, pp.518-

524. https://www.sciencedirect.com/science/article/pii/S2212567115001045/pdf?

md5=ad2a66b817cabd599251ca3369aa53ca&pid=1-s2.0-S2212567115001045-

main.pdf&_valck=1

Reuvid, J., 2010. Managing business risk: a practical guide to protecting your business.

Kogan Page Publishers. https://books.google.com./books?

hl=en&lr=&id=4aNO5PmbEtEC&oi=fnd&pg=PR16&dq=business+risk+&ots=sRsc3RxH

Lx&sig=N8gAN4yHV55GWPvfDQeIiqCFNYI#v=onepage&q=business%20risk&f=false

Savor, P. and Wilson, M., 2016. Earnings announcements and systematic risk. The

Journal of Finance, 71(1), pp.83-138.

https://pdfs.semanticscholar.org/4b37/e1bedd4b6d06b00c3cd28b9c00ce29a86bff.pdf

Subramaniam, V., Tang, T.T., Yue, H. and Zhou, X., 2011. Firm structure and corporate

cash holdings. Journal of Corporate Finance, 17(3), pp.759-773.

https://ink.library.smu.edu.sg/cgi/viewcontent.cgi?referer=https://scholar.google.com/

&httpsredir=1&article=2611&context=soa_research

FINANCE FOR BUSINESS 12

Trujillo‐Ponce, A., 2013. What determines the profitability of banks? Evidence from

Spain. Accounting & Finance, 53(2), pp.561-586.

https://pdfs.semanticscholar.org/2023/cecbaac61b6edff5c905dc85531f0995ff47.pdf

Velnampy, T. and Niresh, J.A., 2012. The relationship between capital structure and

profitability. Global Journal of Management and Business Research, 12(13).

https://journalofbusiness.org/index.php/GJMBR/article/view/766

Yahoo Finance., 2019. CBA Company Profile. Official website of Commonwealth Bank

of Australia. https://finance.yahoo.com/quote/CBA.AX/profile?p=CBA.AX

Trujillo‐Ponce, A., 2013. What determines the profitability of banks? Evidence from

Spain. Accounting & Finance, 53(2), pp.561-586.

https://pdfs.semanticscholar.org/2023/cecbaac61b6edff5c905dc85531f0995ff47.pdf

Velnampy, T. and Niresh, J.A., 2012. The relationship between capital structure and

profitability. Global Journal of Management and Business Research, 12(13).

https://journalofbusiness.org/index.php/GJMBR/article/view/766

Yahoo Finance., 2019. CBA Company Profile. Official website of Commonwealth Bank

of Australia. https://finance.yahoo.com/quote/CBA.AX/profile?p=CBA.AX

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.