Commonwealth Bank's Cash Flow Statement Analysis: Detailed Report

VerifiedAdded on 2020/11/12

|10

|2584

|260

Report

AI Summary

This report provides a comprehensive analysis of the Commonwealth Bank's cash flow statement, examining its operating, investing, and financing activities. It details the sources and uses of cash, including provisions for credit income, acquisitions, and debt financing. The report also covers other comprehensive income items, such as unrealized gains and losses, and discusses accounting for corporate income tax, including current tax assets and deferred revenues. The analysis provides insights into the bank's financial performance and its ability to generate and manage cash flows. The document also explores the income statement and balance sheet of the bank and the various financial instruments, along with relevant figures from the year 2017. The report aims to provide a detailed understanding of the bank's financial position and performance through its cash flow statement.

Commonwealth Bank and

its cash flow statement

1

its cash flow statement

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

Cash flow statements.......................................................................................................................3

(1): ..............................................................................................................................................3

(2)................................................................................................................................................4

OTHER COMPREHENSIVE INCOME.........................................................................................6

(3)...............................................................................................................................................6

(4) ...............................................................................................................................................7

(5)................................................................................................................................................7

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................8

(6): .............................................................................................................................................8

(7)................................................................................................................................................8

(8):...............................................................................................................................................8

9).................................................................................................................................................8

10)...............................................................................................................................................8

11)...............................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

2

INTRODUCTION...........................................................................................................................3

Cash flow statements.......................................................................................................................3

(1): ..............................................................................................................................................3

(2)................................................................................................................................................4

OTHER COMPREHENSIVE INCOME.........................................................................................6

(3)...............................................................................................................................................6

(4) ...............................................................................................................................................7

(5)................................................................................................................................................7

ACCOUNTING FOR CORPORATE INCOME TAX....................................................................8

(6): .............................................................................................................................................8

(7)................................................................................................................................................8

(8):...............................................................................................................................................8

9).................................................................................................................................................8

10)...............................................................................................................................................8

11)...............................................................................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

2

INTRODUCTION

The commonwealth bank is the commercial bank which have their major operations in

the Australia, New Zealand and UK. The cited bank is intending to make a certain objective in

an effective manner. Information about cash flows of an organisation is assisting in rendering

users of the financial statements along with the basis to evaluate the ability of the organisation to

produce cash and cash and cash equivalents and requirements of organisation to use those cash

flow at the time of operating, investing and financial activities (Nurnberg, 2011).

Cash flow statements

(1):

Cash flow statement is a financial report which elaborates sources of an organisation’s

cash and how that cash was spent over a particular time period. This does not covers non-cash

items like depreciation. This forms it useful for identifying short term viability of the

organisation, specifically its ability to pay bills. As management of the cash flow is so

importance for organisations and small organisations in specific, various analysts said that there

is a strong need to have cash flow statement. Cash flow statement is same to the income

statement in that it records an organisation’s performance over a particular period of time. The

main difference between tow is that the income statement likewise takes into account few non-

cash accounting items like depreciation (Brueggeman and Fisher, 2011).

Cash flow from operating activities: The cash flow amount emerge from operating

activities is the main indicator of the extent to which operations of the cited bank have produced

an adequate cash flows in order to handle the operating capabilities of the organisation, pay

dividends, repay loans and form new investments without recourse to outer sources of financing.

Information about major components of historical operating cash flows is helpful, in conjunction

with the other diverse information, in forecasting future operating cash flows.

Basically, this can be rightly said that the operating activities are the main derived from

principle revenue generating activities of the cited organisation henceforth, they normally

produce results from the transactions and other diverse events which enter into identification of

the net profit or loss. For instances: cash flow from operating activities are:

Cash flow statements is a kind of statement which considers all the expenses and

revenues which have cash entry for a certain period of time. Now, this can be said that the

3

The commonwealth bank is the commercial bank which have their major operations in

the Australia, New Zealand and UK. The cited bank is intending to make a certain objective in

an effective manner. Information about cash flows of an organisation is assisting in rendering

users of the financial statements along with the basis to evaluate the ability of the organisation to

produce cash and cash and cash equivalents and requirements of organisation to use those cash

flow at the time of operating, investing and financial activities (Nurnberg, 2011).

Cash flow statements

(1):

Cash flow statement is a financial report which elaborates sources of an organisation’s

cash and how that cash was spent over a particular time period. This does not covers non-cash

items like depreciation. This forms it useful for identifying short term viability of the

organisation, specifically its ability to pay bills. As management of the cash flow is so

importance for organisations and small organisations in specific, various analysts said that there

is a strong need to have cash flow statement. Cash flow statement is same to the income

statement in that it records an organisation’s performance over a particular period of time. The

main difference between tow is that the income statement likewise takes into account few non-

cash accounting items like depreciation (Brueggeman and Fisher, 2011).

Cash flow from operating activities: The cash flow amount emerge from operating

activities is the main indicator of the extent to which operations of the cited bank have produced

an adequate cash flows in order to handle the operating capabilities of the organisation, pay

dividends, repay loans and form new investments without recourse to outer sources of financing.

Information about major components of historical operating cash flows is helpful, in conjunction

with the other diverse information, in forecasting future operating cash flows.

Basically, this can be rightly said that the operating activities are the main derived from

principle revenue generating activities of the cited organisation henceforth, they normally

produce results from the transactions and other diverse events which enter into identification of

the net profit or loss. For instances: cash flow from operating activities are:

Cash flow statements is a kind of statement which considers all the expenses and

revenues which have cash entry for a certain period of time. Now, this can be said that the

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

management of the cited organisation is needed to consider various components in order to gain

sustainability in an effective manner.

Balance sheet – In an organisation it is important that the current state of an enterprise is

ascertain so that decision regarding future can be ascertaining. Also, it helps in identifying the

current position of business as assets are calculated against the liabilities which provide a clear

image of company. balance sheet provides idea to the enterprise that what is its financial position

and which options gave the best result to enterprise in a particular financial year. There are two

section in this financial account in which assets and liabilities are recorded which shows truth

how much liability has been raised to reach at the current state of business (Davies and

Crawford, 2011). Both the sides have to match with one another as only than the prepared

statement is considered as an authenticated one. It is an effective tool through which efficiency

of company’s finance is calculated and then used as a base to judge in future too. Investors also

use this financial tool much to determine the efficiency level of the firm.

(2)

Cash flow - Cash flow it the total amount of cash and cash-equivalents that are

transferred into a business or out of it. At the initial stage, the ability to create value for

company's shareholder is recognise by their ability to initiate positive cash flows. It is essential

for regulating the liquidity of a company, in order to perform flexibly. It is also essential for

finance performance. According to the cash flow statements which is being prepared by an

organisations. It consists of three activities which are importantly consider during formulation of

cash budget. The activities are mentioned underneath:

Operating activities: It should be basically provide majority of a company total cash

flows and widely analyse, whether a CBA is profitable for the company in coming period of

time. It generally these items that indicate that amount of money a company brings in the form

ongoing, regular business events such as production and selling products during an accounting

period of time. According to the cash flow statements of CBA, it consists of follow activities

such as:

Operating activities 2017 amount

Provision for credit income 1095

Other operating activities -1095

4

sustainability in an effective manner.

Balance sheet – In an organisation it is important that the current state of an enterprise is

ascertain so that decision regarding future can be ascertaining. Also, it helps in identifying the

current position of business as assets are calculated against the liabilities which provide a clear

image of company. balance sheet provides idea to the enterprise that what is its financial position

and which options gave the best result to enterprise in a particular financial year. There are two

section in this financial account in which assets and liabilities are recorded which shows truth

how much liability has been raised to reach at the current state of business (Davies and

Crawford, 2011). Both the sides have to match with one another as only than the prepared

statement is considered as an authenticated one. It is an effective tool through which efficiency

of company’s finance is calculated and then used as a base to judge in future too. Investors also

use this financial tool much to determine the efficiency level of the firm.

(2)

Cash flow - Cash flow it the total amount of cash and cash-equivalents that are

transferred into a business or out of it. At the initial stage, the ability to create value for

company's shareholder is recognise by their ability to initiate positive cash flows. It is essential

for regulating the liquidity of a company, in order to perform flexibly. It is also essential for

finance performance. According to the cash flow statements which is being prepared by an

organisations. It consists of three activities which are importantly consider during formulation of

cash budget. The activities are mentioned underneath:

Operating activities: It should be basically provide majority of a company total cash

flows and widely analyse, whether a CBA is profitable for the company in coming period of

time. It generally these items that indicate that amount of money a company brings in the form

ongoing, regular business events such as production and selling products during an accounting

period of time. According to the cash flow statements of CBA, it consists of follow activities

such as:

Operating activities 2017 amount

Provision for credit income 1095

Other operating activities -1095

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

All the above amounts are collected during the period of time regarding generating

overall profitability in coming period of time.

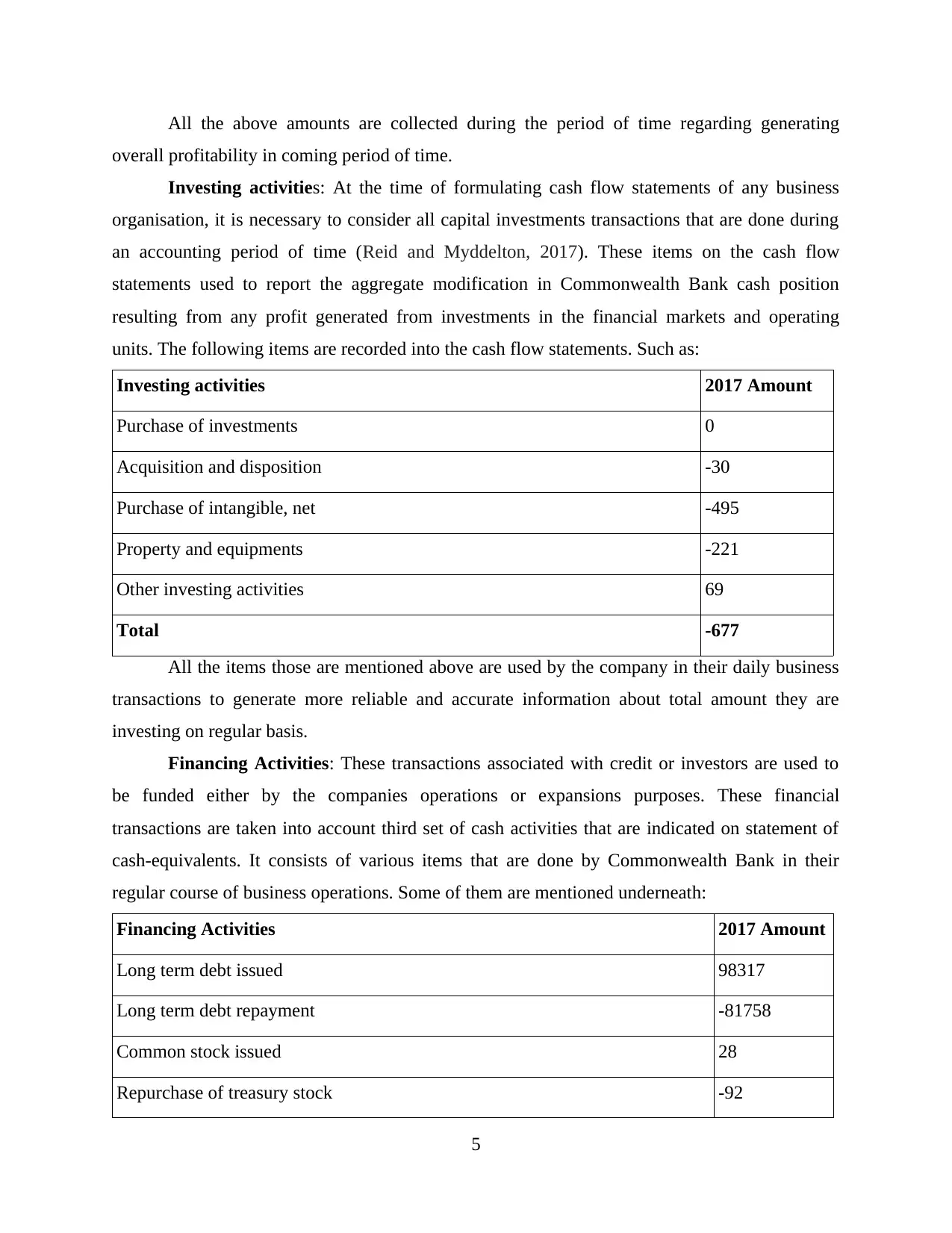

Investing activities: At the time of formulating cash flow statements of any business

organisation, it is necessary to consider all capital investments transactions that are done during

an accounting period of time (Reid and Myddelton, 2017). These items on the cash flow

statements used to report the aggregate modification in Commonwealth Bank cash position

resulting from any profit generated from investments in the financial markets and operating

units. The following items are recorded into the cash flow statements. Such as:

Investing activities 2017 Amount

Purchase of investments 0

Acquisition and disposition -30

Purchase of intangible, net -495

Property and equipments -221

Other investing activities 69

Total -677

All the items those are mentioned above are used by the company in their daily business

transactions to generate more reliable and accurate information about total amount they are

investing on regular basis.

Financing Activities: These transactions associated with credit or investors are used to

be funded either by the companies operations or expansions purposes. These financial

transactions are taken into account third set of cash activities that are indicated on statement of

cash-equivalents. It consists of various items that are done by Commonwealth Bank in their

regular course of business operations. Some of them are mentioned underneath:

Financing Activities 2017 Amount

Long term debt issued 98317

Long term debt repayment -81758

Common stock issued 28

Repurchase of treasury stock -92

5

overall profitability in coming period of time.

Investing activities: At the time of formulating cash flow statements of any business

organisation, it is necessary to consider all capital investments transactions that are done during

an accounting period of time (Reid and Myddelton, 2017). These items on the cash flow

statements used to report the aggregate modification in Commonwealth Bank cash position

resulting from any profit generated from investments in the financial markets and operating

units. The following items are recorded into the cash flow statements. Such as:

Investing activities 2017 Amount

Purchase of investments 0

Acquisition and disposition -30

Purchase of intangible, net -495

Property and equipments -221

Other investing activities 69

Total -677

All the items those are mentioned above are used by the company in their daily business

transactions to generate more reliable and accurate information about total amount they are

investing on regular basis.

Financing Activities: These transactions associated with credit or investors are used to

be funded either by the companies operations or expansions purposes. These financial

transactions are taken into account third set of cash activities that are indicated on statement of

cash-equivalents. It consists of various items that are done by Commonwealth Bank in their

regular course of business operations. Some of them are mentioned underneath:

Financing Activities 2017 Amount

Long term debt issued 98317

Long term debt repayment -81758

Common stock issued 28

Repurchase of treasury stock -92

5

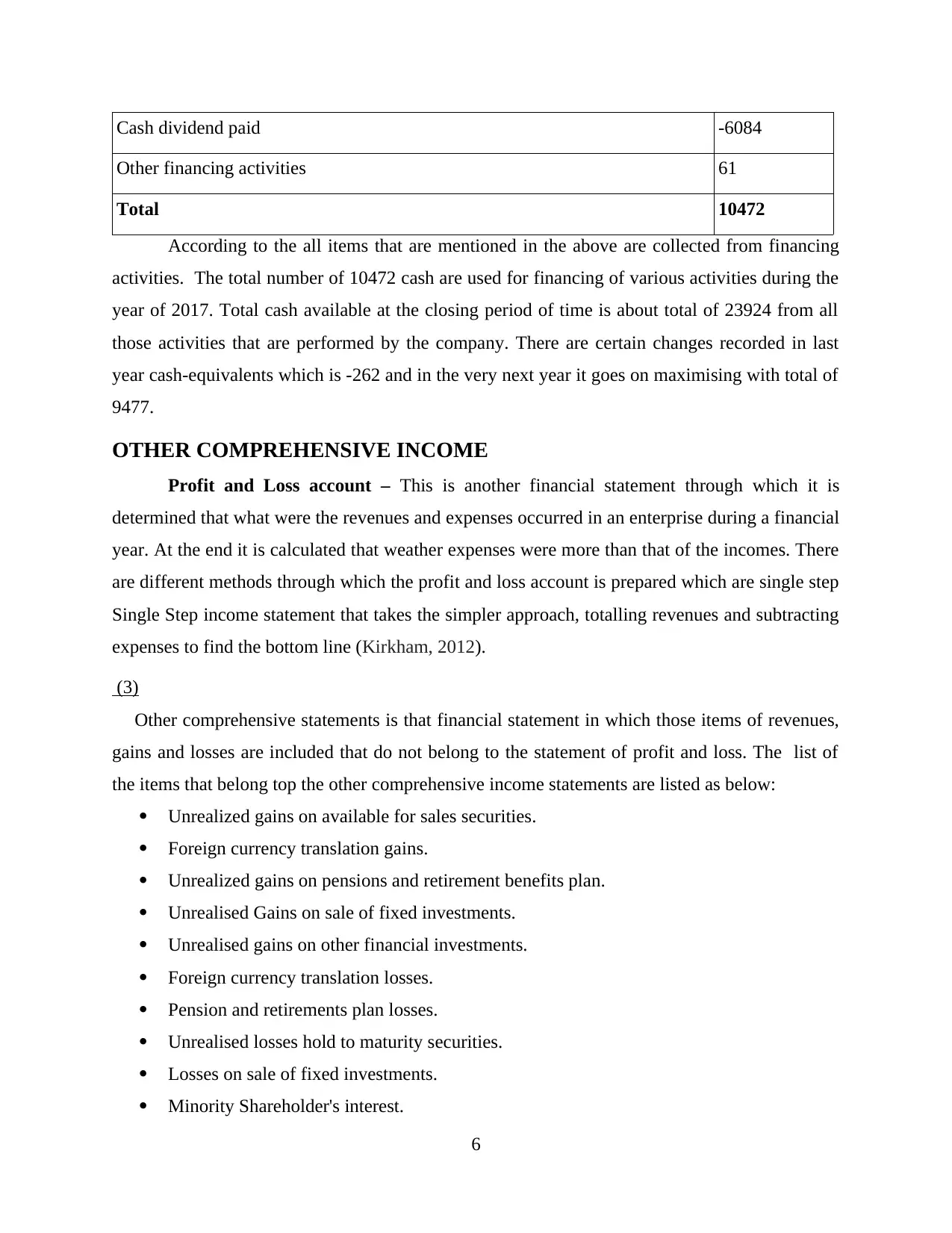

Cash dividend paid -6084

Other financing activities 61

Total 10472

According to the all items that are mentioned in the above are collected from financing

activities. The total number of 10472 cash are used for financing of various activities during the

year of 2017. Total cash available at the closing period of time is about total of 23924 from all

those activities that are performed by the company. There are certain changes recorded in last

year cash-equivalents which is -262 and in the very next year it goes on maximising with total of

9477.

OTHER COMPREHENSIVE INCOME

Profit and Loss account – This is another financial statement through which it is

determined that what were the revenues and expenses occurred in an enterprise during a financial

year. At the end it is calculated that weather expenses were more than that of the incomes. There

are different methods through which the profit and loss account is prepared which are single step

Single Step income statement that takes the simpler approach, totalling revenues and subtracting

expenses to find the bottom line (Kirkham, 2012).

(3)

Other comprehensive statements is that financial statement in which those items of revenues,

gains and losses are included that do not belong to the statement of profit and loss. The list of

the items that belong top the other comprehensive income statements are listed as below:

Unrealized gains on available for sales securities.

Foreign currency translation gains.

Unrealized gains on pensions and retirement benefits plan.

Unrealised Gains on sale of fixed investments.

Unrealised gains on other financial investments.

Foreign currency translation losses.

Pension and retirements plan losses.

Unrealised losses hold to maturity securities.

Losses on sale of fixed investments.

Minority Shareholder's interest.

6

Other financing activities 61

Total 10472

According to the all items that are mentioned in the above are collected from financing

activities. The total number of 10472 cash are used for financing of various activities during the

year of 2017. Total cash available at the closing period of time is about total of 23924 from all

those activities that are performed by the company. There are certain changes recorded in last

year cash-equivalents which is -262 and in the very next year it goes on maximising with total of

9477.

OTHER COMPREHENSIVE INCOME

Profit and Loss account – This is another financial statement through which it is

determined that what were the revenues and expenses occurred in an enterprise during a financial

year. At the end it is calculated that weather expenses were more than that of the incomes. There

are different methods through which the profit and loss account is prepared which are single step

Single Step income statement that takes the simpler approach, totalling revenues and subtracting

expenses to find the bottom line (Kirkham, 2012).

(3)

Other comprehensive statements is that financial statement in which those items of revenues,

gains and losses are included that do not belong to the statement of profit and loss. The list of

the items that belong top the other comprehensive income statements are listed as below:

Unrealized gains on available for sales securities.

Foreign currency translation gains.

Unrealized gains on pensions and retirement benefits plan.

Unrealised Gains on sale of fixed investments.

Unrealised gains on other financial investments.

Foreign currency translation losses.

Pension and retirements plan losses.

Unrealised losses hold to maturity securities.

Losses on sale of fixed investments.

Minority Shareholder's interest.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(4)

Available for sale securities: AVS is an accounting term that is used in the finance

industry for financial assets. According to the US-GAAP these are type of debt securities

or financial instruments which are neither held to maturity and neither held for trading,

these are the securities which are available readily at the current market prices.

Minority Shareholder's Interest: Minority interest is that part of the holding company

that we do not own. This minority interest is included in the company's comprehensive

statements (Collins, Hribar and Tian, 2014). This is that proportion of the holding

company net profits that belong to the minority shareholder's of the subsidiary company

whose majority holding is with the holding company.

Foreign currency gains: These are the gains of those companies which operate globally,

when the foreign currencies are translated into the domestic currency of the company it

leads to gains that occur because of the change in value of the foreign currencies. This

types of gains are reported in the OCI statement of the company.

Foreign currency Losses:This works on the same concept currency translation gains,

company incurs these losses during times of translation because of the degradation in the

value of foreign currency at the time of translation.

(5)

Comprehensive income statements items are not included in main financial statements

because these are the part of internal operations and management. These items and elements are

made in terms of owner's interest in a business. That are type of income statements are realised in

this context such as change in equity, fluctuation in capital of owners capital and equity, gains

and losses form derivative instruments, pension or other retirement plans gains and losses,

foreign currency transactions and adjustments.

7

Available for sale securities: AVS is an accounting term that is used in the finance

industry for financial assets. According to the US-GAAP these are type of debt securities

or financial instruments which are neither held to maturity and neither held for trading,

these are the securities which are available readily at the current market prices.

Minority Shareholder's Interest: Minority interest is that part of the holding company

that we do not own. This minority interest is included in the company's comprehensive

statements (Collins, Hribar and Tian, 2014). This is that proportion of the holding

company net profits that belong to the minority shareholder's of the subsidiary company

whose majority holding is with the holding company.

Foreign currency gains: These are the gains of those companies which operate globally,

when the foreign currencies are translated into the domestic currency of the company it

leads to gains that occur because of the change in value of the foreign currencies. This

types of gains are reported in the OCI statement of the company.

Foreign currency Losses:This works on the same concept currency translation gains,

company incurs these losses during times of translation because of the degradation in the

value of foreign currency at the time of translation.

(5)

Comprehensive income statements items are not included in main financial statements

because these are the part of internal operations and management. These items and elements are

made in terms of owner's interest in a business. That are type of income statements are realised in

this context such as change in equity, fluctuation in capital of owners capital and equity, gains

and losses form derivative instruments, pension or other retirement plans gains and losses,

foreign currency transactions and adjustments.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING FOR CORPORATE INCOME TAX

(6):

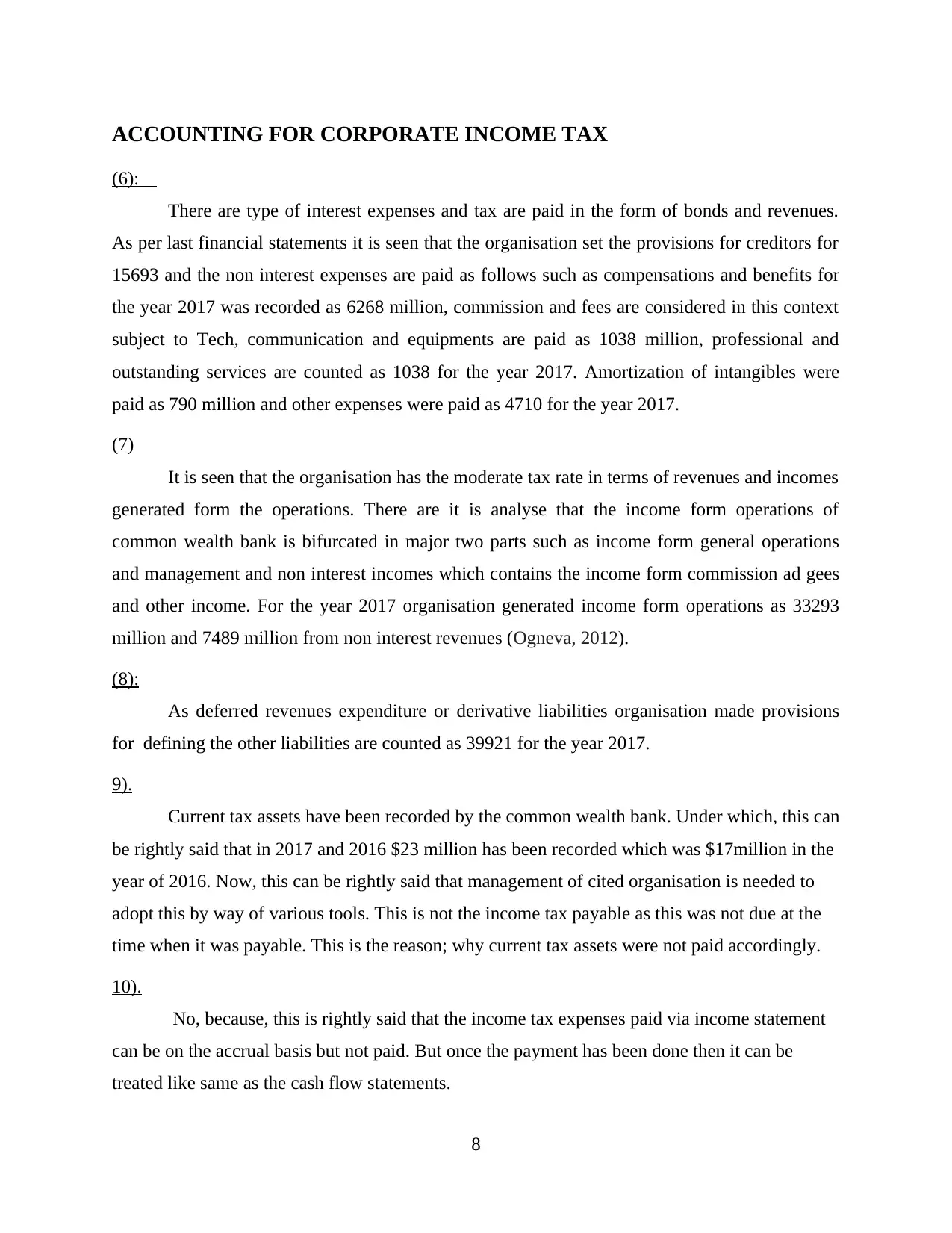

There are type of interest expenses and tax are paid in the form of bonds and revenues.

As per last financial statements it is seen that the organisation set the provisions for creditors for

15693 and the non interest expenses are paid as follows such as compensations and benefits for

the year 2017 was recorded as 6268 million, commission and fees are considered in this context

subject to Tech, communication and equipments are paid as 1038 million, professional and

outstanding services are counted as 1038 for the year 2017. Amortization of intangibles were

paid as 790 million and other expenses were paid as 4710 for the year 2017.

(7)

It is seen that the organisation has the moderate tax rate in terms of revenues and incomes

generated form the operations. There are it is analyse that the income form operations of

common wealth bank is bifurcated in major two parts such as income form general operations

and management and non interest incomes which contains the income form commission ad gees

and other income. For the year 2017 organisation generated income form operations as 33293

million and 7489 million from non interest revenues (Ogneva, 2012).

(8):

As deferred revenues expenditure or derivative liabilities organisation made provisions

for defining the other liabilities are counted as 39921 for the year 2017.

9).

Current tax assets have been recorded by the common wealth bank. Under which, this can

be rightly said that in 2017 and 2016 $23 million has been recorded which was $17million in the

year of 2016. Now, this can be rightly said that management of cited organisation is needed to

adopt this by way of various tools. This is not the income tax payable as this was not due at the

time when it was payable. This is the reason; why current tax assets were not paid accordingly.

10).

No, because, this is rightly said that the income tax expenses paid via income statement

can be on the accrual basis but not paid. But once the payment has been done then it can be

treated like same as the cash flow statements.

8

(6):

There are type of interest expenses and tax are paid in the form of bonds and revenues.

As per last financial statements it is seen that the organisation set the provisions for creditors for

15693 and the non interest expenses are paid as follows such as compensations and benefits for

the year 2017 was recorded as 6268 million, commission and fees are considered in this context

subject to Tech, communication and equipments are paid as 1038 million, professional and

outstanding services are counted as 1038 for the year 2017. Amortization of intangibles were

paid as 790 million and other expenses were paid as 4710 for the year 2017.

(7)

It is seen that the organisation has the moderate tax rate in terms of revenues and incomes

generated form the operations. There are it is analyse that the income form operations of

common wealth bank is bifurcated in major two parts such as income form general operations

and management and non interest incomes which contains the income form commission ad gees

and other income. For the year 2017 organisation generated income form operations as 33293

million and 7489 million from non interest revenues (Ogneva, 2012).

(8):

As deferred revenues expenditure or derivative liabilities organisation made provisions

for defining the other liabilities are counted as 39921 for the year 2017.

9).

Current tax assets have been recorded by the common wealth bank. Under which, this can

be rightly said that in 2017 and 2016 $23 million has been recorded which was $17million in the

year of 2016. Now, this can be rightly said that management of cited organisation is needed to

adopt this by way of various tools. This is not the income tax payable as this was not due at the

time when it was payable. This is the reason; why current tax assets were not paid accordingly.

10).

No, because, this is rightly said that the income tax expenses paid via income statement

can be on the accrual basis but not paid. But once the payment has been done then it can be

treated like same as the cash flow statements.

8

11).

` There is a difficulty in which have been shown while treating in the financial statement.

the main difficulty is that the management was totally disagreed about the introduction of the

government policies which forms uncertainty and that point out the Australia’s highest banks for

discriminatory tax treatment via bank levy.

CONCLUSION

From the above project analysis, it has been concluded that cash flow statements of

commonwealth Banks are creating wealth for the company. For this purpose all vital information

taken from cash flow statements and other financial statements are taken into consideration. This

will assist them to reach at certain level in accordance to make future decision-making. All the

analysis is done to attain future growth and sustainability in coming period of time.

9

` There is a difficulty in which have been shown while treating in the financial statement.

the main difficulty is that the management was totally disagreed about the introduction of the

government policies which forms uncertainty and that point out the Australia’s highest banks for

discriminatory tax treatment via bank levy.

CONCLUSION

From the above project analysis, it has been concluded that cash flow statements of

commonwealth Banks are creating wealth for the company. For this purpose all vital information

taken from cash flow statements and other financial statements are taken into consideration. This

will assist them to reach at certain level in accordance to make future decision-making. All the

analysis is done to attain future growth and sustainability in coming period of time.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

REFERENCES

Books and Journals:

Nurnberg, H., 2011. Cash Flow Statement. John Wiley & Sons, Ltd.

Brueggeman, W. B. and Fisher, J. D., 2011. Real estate finance and investments (pp. 5-6). New

York, NY: McGraw-Hill Irwin.

Davies, T. and Crawford, I. P., 2011. Business accounting and finance. Financial Times Prentice

Hall.

Reid, W. and Myddelton, D. R., 2017. The meaning of company accounts. Routledge.

Kirkham, R., 2012. Liquidity analysis using cash flow ratios and traditional ratios: The

telecommunications sector in Australia. The Journal of New Business Ideas & Trends.

10(1). p.1.

Collins, D. W., Hribar, P. and Tian, X. S., 2014. Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics. 58(2-3).

pp.173-200.

Ogneva, M., 2012. Accrual quality, realized returns, and expected returns: The importance of

controlling for cash flow shocks. The Accounting Review. 87(4). pp.1415-1444.

10

Books and Journals:

Nurnberg, H., 2011. Cash Flow Statement. John Wiley & Sons, Ltd.

Brueggeman, W. B. and Fisher, J. D., 2011. Real estate finance and investments (pp. 5-6). New

York, NY: McGraw-Hill Irwin.

Davies, T. and Crawford, I. P., 2011. Business accounting and finance. Financial Times Prentice

Hall.

Reid, W. and Myddelton, D. R., 2017. The meaning of company accounts. Routledge.

Kirkham, R., 2012. Liquidity analysis using cash flow ratios and traditional ratios: The

telecommunications sector in Australia. The Journal of New Business Ideas & Trends.

10(1). p.1.

Collins, D. W., Hribar, P. and Tian, X. S., 2014. Cash flow asymmetry: Causes and implications

for conditional conservatism research. Journal of Accounting and Economics. 58(2-3).

pp.173-200.

Ogneva, M., 2012. Accrual quality, realized returns, and expected returns: The importance of

controlling for cash flow shocks. The Accounting Review. 87(4). pp.1415-1444.

10

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.