HI5002 Finance for Business - CBA Company Performance Analysis Report

VerifiedAdded on 2022/12/30

|14

|4134

|64

Report

AI Summary

This assignment analyzes the financial performance of the Commonwealth Bank (CBA), focusing on its key products and services, with an emphasis on mobile banking as a primary service. The report delves into the bank's liquidity and capital structure, examining financial ratios such as the loan-to-deposit ratio, debt-to-equity ratio, and debt ratio over a three-year period. It assesses the bank's non-current assets, including property, plant, and equipment, and the depreciation method used. Furthermore, the report conducts a scenario analysis, evaluating the net present value (NPV) under normal, worst-case, and best-case scenarios to understand the sensitivity of the investment. Finally, the assignment analyzes the bank's share price performance using the price-to-earnings (PE) ratio and stock movement, culminating in a recommendation letter to a client, justifying the inclusion of CBA in their investment portfolio. The analysis highlights both the strengths and weaknesses of CBA's financial position and provides insights into its future sustainability and potential for growth.

Running head: FINANCE FOR BUSINESS - MASTERS

Finance for business – masters

Name of the student

Name of the university

Student ID

Author note

Finance for business – masters

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE FOR BUSINESS - MASTERS

Table of Contents

Abstract.......................................................................................................................................2

I. Introduction...........................................................................................................................3

II. Financial analysis of Commonwealth Bank.........................................................................3

2.1 Description of key product or service................................................................................3

2.2 Calculation and analysis of the selected performance ratios...........................................3

2.3 Analysis of non-current asset............................................................................................5

2.4 Scenario analysis..............................................................................................................6

2.5 Issuance of bonds or shares.............................................................................................8

2.6 PE ratio and share price movement..................................................................................9

III. Recommendation letter...................................................................................................10

IV. Conclusion......................................................................................................................11

Reference..................................................................................................................................12

Table of Contents

Abstract.......................................................................................................................................2

I. Introduction...........................................................................................................................3

II. Financial analysis of Commonwealth Bank.........................................................................3

2.1 Description of key product or service................................................................................3

2.2 Calculation and analysis of the selected performance ratios...........................................3

2.3 Analysis of non-current asset............................................................................................5

2.4 Scenario analysis..............................................................................................................6

2.5 Issuance of bonds or shares.............................................................................................8

2.6 PE ratio and share price movement..................................................................................9

III. Recommendation letter...................................................................................................10

IV. Conclusion......................................................................................................................11

Reference..................................................................................................................................12

2FINANCE FOR BUSINESS - MASTERS

Abstract

The task portrays the main issues associated with Commonwealth Bank, its financial

performance from different aspects, acceptability of new project under different scenarios and

its share price movements. Among others, the key service provided by the bank is the mobile

banking as it is the 1st one that became successful in implementing the fully functional mobile

banking services. Regarding liquidity position it is found that the loan deposit ratio has been

reduced from 126.67% to 119.61% over the 3 years period. The capital structure of the bank

shows that significantly high level of debt that may raise question on its future sustainability.

During the last year the bank did not issue any shares, however covered bond issued by it

amounting to $555 million. Further, though the net profit of the bank is in reducing trend over

the past 3 years, the PE ratio and share price have been improved during the same period.

Abstract

The task portrays the main issues associated with Commonwealth Bank, its financial

performance from different aspects, acceptability of new project under different scenarios and

its share price movements. Among others, the key service provided by the bank is the mobile

banking as it is the 1st one that became successful in implementing the fully functional mobile

banking services. Regarding liquidity position it is found that the loan deposit ratio has been

reduced from 126.67% to 119.61% over the 3 years period. The capital structure of the bank

shows that significantly high level of debt that may raise question on its future sustainability.

During the last year the bank did not issue any shares, however covered bond issued by it

amounting to $555 million. Further, though the net profit of the bank is in reducing trend over

the past 3 years, the PE ratio and share price have been improved during the same period.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE FOR BUSINESS - MASTERS

I. Introduction

Purpose of the assignment is to analyse the financial performance of any ASX listed

company that will be Commonwealth Bank Australia (CBA) for this assignment.

Commonwealth Bank was established under Commonwealth Bank Act during the year 1911

and it started operating during the year 1912. It was empowered to conduct the savings as

well as general business related to banking. At present the bank has 52,000 employees and

800,000 shareholders. It offers wide range of services for assisting the Australians to build as

well as manage the finances. Objective of the bank is becoming the finest organization in

Australia providing financial services through excelling the customer’s services as well as

strategies of the bank for recognising significant opportunities within business. It will further

help in developing more value for the people, stakeholders and people (Commbank.com.au

2019). The task will depict the key product or services offered by the entity and importance of

those products or services. In the next section the report will comment upon its capital

structure as well as liquidity position taking into account the financial data provided through its

annual report for last 3 years. Next, the report will conduct the analysis of non-current assets

along with the method of depreciation used by the bank. In the next section it will conduct

scenario analysis for the situation provided and will comment upon the normal case, worst

case and best case analysis that will help in understanding the sensitivity of NPV. The report

will also highlight and comment upon the performance of its share price through its PE ratio

and stock movement. Based on all these facts the report will provide the recommendation

letter to the client that will provide the explanation regarding why the entity shall be included in

his / her portfolio.

II. Financial analysis of Commonwealth Bank

2.1 Description of key product or service

Different products and services related to business banking are offered by CBA those

include business accounts, merchant services, business loans, superannuation, asset

finance, investment, insurance and investments. However, the key service provided by the

bank among others is the mobile banking. Though implantation of the mobile technology was

not the new approach for the Australian customers, CBA is 1st one that became successful in

implementing the fully functional mobile banking services through offering free application for

different mobiles along with iPhone (Revelli and Viviani 2015). Its competitors like Westpac

and ANZ also implemented the mobile banking even before CBA, however, it was only limited

to iPhone to be functioned it fully. Since, its 1st implementation of the services related to

mobile banking, CBA is managing as well as maintaining the same on continuous basis

through making the service more convenient as well as efficient for any of the mobile where

internet can be used. Further, it simplified the lives of number of customers and offers them

the eservices related to transfer of money, paying bills, checking the account balances

through using the mobile phones (Commbank.com.au 2019).

2.2 Calculation and analysis of the selected performance ratios

Liquidity ratio – liquidity ratios helps to determine the ability of the company whether it is

able to meet its short term debt obligation with available short term assets. Analysis of

liquidity position plays important role to the potential investors as it says lot about the

company’s existing obligation and future prospects. Deposit funding ratio or loans to deposit

ratio is used in case of banks for measuring through comparing total loans of a bank with its

I. Introduction

Purpose of the assignment is to analyse the financial performance of any ASX listed

company that will be Commonwealth Bank Australia (CBA) for this assignment.

Commonwealth Bank was established under Commonwealth Bank Act during the year 1911

and it started operating during the year 1912. It was empowered to conduct the savings as

well as general business related to banking. At present the bank has 52,000 employees and

800,000 shareholders. It offers wide range of services for assisting the Australians to build as

well as manage the finances. Objective of the bank is becoming the finest organization in

Australia providing financial services through excelling the customer’s services as well as

strategies of the bank for recognising significant opportunities within business. It will further

help in developing more value for the people, stakeholders and people (Commbank.com.au

2019). The task will depict the key product or services offered by the entity and importance of

those products or services. In the next section the report will comment upon its capital

structure as well as liquidity position taking into account the financial data provided through its

annual report for last 3 years. Next, the report will conduct the analysis of non-current assets

along with the method of depreciation used by the bank. In the next section it will conduct

scenario analysis for the situation provided and will comment upon the normal case, worst

case and best case analysis that will help in understanding the sensitivity of NPV. The report

will also highlight and comment upon the performance of its share price through its PE ratio

and stock movement. Based on all these facts the report will provide the recommendation

letter to the client that will provide the explanation regarding why the entity shall be included in

his / her portfolio.

II. Financial analysis of Commonwealth Bank

2.1 Description of key product or service

Different products and services related to business banking are offered by CBA those

include business accounts, merchant services, business loans, superannuation, asset

finance, investment, insurance and investments. However, the key service provided by the

bank among others is the mobile banking. Though implantation of the mobile technology was

not the new approach for the Australian customers, CBA is 1st one that became successful in

implementing the fully functional mobile banking services through offering free application for

different mobiles along with iPhone (Revelli and Viviani 2015). Its competitors like Westpac

and ANZ also implemented the mobile banking even before CBA, however, it was only limited

to iPhone to be functioned it fully. Since, its 1st implementation of the services related to

mobile banking, CBA is managing as well as maintaining the same on continuous basis

through making the service more convenient as well as efficient for any of the mobile where

internet can be used. Further, it simplified the lives of number of customers and offers them

the eservices related to transfer of money, paying bills, checking the account balances

through using the mobile phones (Commbank.com.au 2019).

2.2 Calculation and analysis of the selected performance ratios

Liquidity ratio – liquidity ratios helps to determine the ability of the company whether it is

able to meet its short term debt obligation with available short term assets. Analysis of

liquidity position plays important role to the potential investors as it says lot about the

company’s existing obligation and future prospects. Deposit funding ratio or loans to deposit

ratio is used in case of banks for measuring through comparing total loans of a bank with its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE FOR BUSINESS - MASTERS

total deposits over the same period of time. It is computed through dividing the total loan

amount by total deposit amounts and is expressed in percentage form and the percentage of

more than 100% signifies that the bank is earning sufficient amount to cover up its liabilities

(Ahmed 2015).

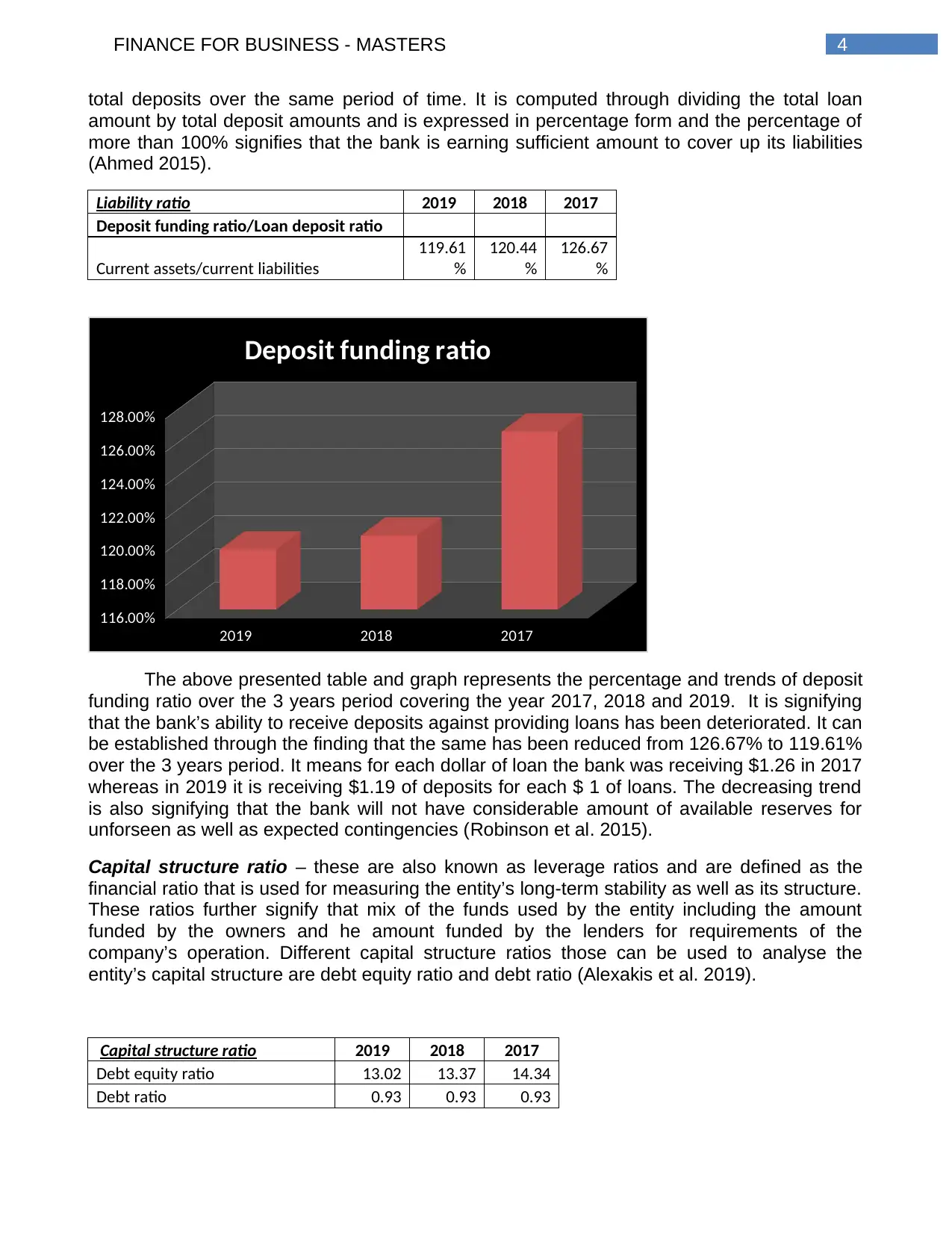

Liability ratio 2019 2018 2017

Deposit funding ratio/Loan deposit ratio

Current assets/current liabilities

119.61

%

120.44

%

126.67

%

2019 2018 2017

116.00%

118.00%

120.00%

122.00%

124.00%

126.00%

128.00%

Deposit funding ratio

The above presented table and graph represents the percentage and trends of deposit

funding ratio over the 3 years period covering the year 2017, 2018 and 2019. It is signifying

that the bank’s ability to receive deposits against providing loans has been deteriorated. It can

be established through the finding that the same has been reduced from 126.67% to 119.61%

over the 3 years period. It means for each dollar of loan the bank was receiving $1.26 in 2017

whereas in 2019 it is receiving $1.19 of deposits for each $ 1 of loans. The decreasing trend

is also signifying that the bank will not have considerable amount of available reserves for

unforseen as well as expected contingencies (Robinson et al. 2015).

Capital structure ratio – these are also known as leverage ratios and are defined as the

financial ratio that is used for measuring the entity’s long-term stability as well as its structure.

These ratios further signify that mix of the funds used by the entity including the amount

funded by the owners and he amount funded by the lenders for requirements of the

company’s operation. Different capital structure ratios those can be used to analyse the

entity’s capital structure are debt equity ratio and debt ratio (Alexakis et al. 2019).

Capital structure ratio 2019 2018 2017

Debt equity ratio 13.02 13.37 14.34

Debt ratio 0.93 0.93 0.93

total deposits over the same period of time. It is computed through dividing the total loan

amount by total deposit amounts and is expressed in percentage form and the percentage of

more than 100% signifies that the bank is earning sufficient amount to cover up its liabilities

(Ahmed 2015).

Liability ratio 2019 2018 2017

Deposit funding ratio/Loan deposit ratio

Current assets/current liabilities

119.61

%

120.44

%

126.67

%

2019 2018 2017

116.00%

118.00%

120.00%

122.00%

124.00%

126.00%

128.00%

Deposit funding ratio

The above presented table and graph represents the percentage and trends of deposit

funding ratio over the 3 years period covering the year 2017, 2018 and 2019. It is signifying

that the bank’s ability to receive deposits against providing loans has been deteriorated. It can

be established through the finding that the same has been reduced from 126.67% to 119.61%

over the 3 years period. It means for each dollar of loan the bank was receiving $1.26 in 2017

whereas in 2019 it is receiving $1.19 of deposits for each $ 1 of loans. The decreasing trend

is also signifying that the bank will not have considerable amount of available reserves for

unforseen as well as expected contingencies (Robinson et al. 2015).

Capital structure ratio – these are also known as leverage ratios and are defined as the

financial ratio that is used for measuring the entity’s long-term stability as well as its structure.

These ratios further signify that mix of the funds used by the entity including the amount

funded by the owners and he amount funded by the lenders for requirements of the

company’s operation. Different capital structure ratios those can be used to analyse the

entity’s capital structure are debt equity ratio and debt ratio (Alexakis et al. 2019).

Capital structure ratio 2019 2018 2017

Debt equity ratio 13.02 13.37 14.34

Debt ratio 0.93 0.93 0.93

5FINANCE FOR BUSINESS - MASTERS

2019 2018 2017

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Capital structure ratio

Debt equity

ratio

Debt ratio

Debt equity ratio – this ratio is also known as the gearing ratio or risk ratio and is a capital

structure or leverage ratio. It is used for computing the weights of financial obligations

including total debt as compared to total equity. It further highlights the way in which the entity

structures its capital that is whether it is tilted towards equity or debt (Omar et al. 2014).

Though the debt to equity ratio varies from industry to industry, generally the same of 1 to 1.5

is considered as ideal. From the above it can be identified that though the bank was able to

reduce its debt equity ratio from 14.34 times to 13.02 times over the period of past 3 years,

the debt portion is significantly high as against equity. High level of debt equity ratio signifies

that the bank is overburdened with the debt and significant amount is spent towards payment

of interest and any further loss will lead to insolvency (Commbank.com.au 2019).

Debt ratio – it is used to measure the portion of assets paid with the debt. This ratio helps in

measuring the solvency of the bank. Though the debt ratio varies from industry to industry,

generally lower level of debt ratio that is 0.4 or lower is preferred if the cash flows of the bank

are subject to unpredictable variation as the same will lead to unserviceable debt. From the

above it can be identified that the bank’s debt ratio has not been changed much and

remained at 0.93 over the period of past 3 years, the debt used for acquiring assets is

significantly high (Wagner et al. 2015).

Hence, if the overall liquidity and capital structure of the bank is considered it can be

determined that liquidity position of the company over the past 3 years has been deteriorated.

Further, the capital structure of the bank includes significantly high level of debt that may raise

question on its future sustainability.

2.3 Analysis of non-current asset

2019 2018 2017

Amount in million

Property, plant and equipment $ 2,383.00 $ 2,576.00 $ 3,873.00

Investment in associates and joint ventures $ 3,001.00 $ 1,842.00 $ 2,778.00

Intangibles $ 7,965.00 $ 9,090.00 $ 10,024.00

Total $ 13,349.00 $ 13,508.00 $ 16,675.00

2019 2018 2017

0.00

2.00

4.00

6.00

8.00

10.00

12.00

14.00

16.00

Capital structure ratio

Debt equity

ratio

Debt ratio

Debt equity ratio – this ratio is also known as the gearing ratio or risk ratio and is a capital

structure or leverage ratio. It is used for computing the weights of financial obligations

including total debt as compared to total equity. It further highlights the way in which the entity

structures its capital that is whether it is tilted towards equity or debt (Omar et al. 2014).

Though the debt to equity ratio varies from industry to industry, generally the same of 1 to 1.5

is considered as ideal. From the above it can be identified that though the bank was able to

reduce its debt equity ratio from 14.34 times to 13.02 times over the period of past 3 years,

the debt portion is significantly high as against equity. High level of debt equity ratio signifies

that the bank is overburdened with the debt and significant amount is spent towards payment

of interest and any further loss will lead to insolvency (Commbank.com.au 2019).

Debt ratio – it is used to measure the portion of assets paid with the debt. This ratio helps in

measuring the solvency of the bank. Though the debt ratio varies from industry to industry,

generally lower level of debt ratio that is 0.4 or lower is preferred if the cash flows of the bank

are subject to unpredictable variation as the same will lead to unserviceable debt. From the

above it can be identified that the bank’s debt ratio has not been changed much and

remained at 0.93 over the period of past 3 years, the debt used for acquiring assets is

significantly high (Wagner et al. 2015).

Hence, if the overall liquidity and capital structure of the bank is considered it can be

determined that liquidity position of the company over the past 3 years has been deteriorated.

Further, the capital structure of the bank includes significantly high level of debt that may raise

question on its future sustainability.

2.3 Analysis of non-current asset

2019 2018 2017

Amount in million

Property, plant and equipment $ 2,383.00 $ 2,576.00 $ 3,873.00

Investment in associates and joint ventures $ 3,001.00 $ 1,842.00 $ 2,778.00

Intangibles $ 7,965.00 $ 9,090.00 $ 10,024.00

Total $ 13,349.00 $ 13,508.00 $ 16,675.00

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE FOR BUSINESS - MASTERS

Above table presents the schedule of the bank’s non-current assets that portrays that

the amount invested in non-current assets have been reduced over the past period of 3 years.

However, amount of total assets have been increased over the same period that is indicating

that the bank is shifting towards investment in current assets rather than non-current assets.

Though the company purchased some property, plant and equipment (PPE) during the

concerned period amount of PPE sold is more as compared to amount of PPE purchased by

it. Hence, the amount of PPE reduced from $3873 million to $2383 million over the concerned

period. The company used straight line method for depreciating PPE. Hence, the value of

PPE is uniformly reduced over their useful life till it reaches the salvage value (Gamayuni

2015).

Operating cash flow is the section represented under the cash flow statement that

delivers information of the entity’s ability to generate cash from the core activities of the entity.

Generally the operating cash flow is computed as per the below mentioned formula –

Operating cash flow = Net income + non-cash expenses + changes in the working capital.

Non-cash expenses include the expenses like depreciation or amortization expenses

represented under the income statement of the organization. While computing the cash flow

of a long term project depreciation is deducted while computing the project’s income.

However, at the time of computing the cash flow the depreciation expenses is added back as

the same is non-cash expenses. Further, while computing the capex the depreciation

expenses is added to the difference of current PPE and previous PPE. This is analysed while

purchasing long term asset as the same are not shown under income statement but have

significant impact on the cash flows (Huang and Kou 2014).

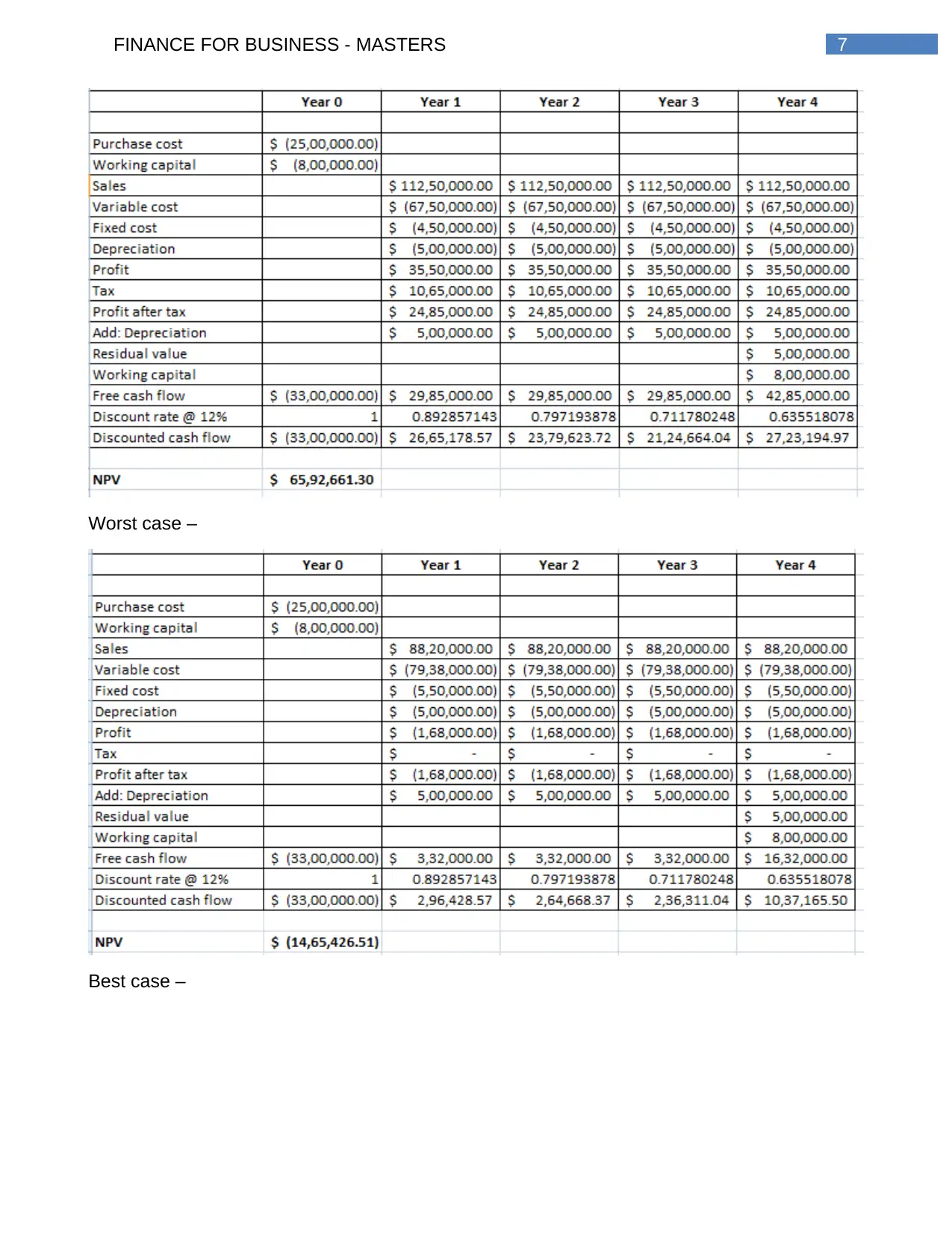

2.4 Scenario analysis

Net present value (NPV) is fundamental profitability measure for profitability of the

investments project. It is equal to sum of the present values of entire cash flows including

inflows as well as outflows of any project. The project is acceptable if the NPV of the project is

positive as positive NPV determines that the project will create shareholder’s wealth. On the

contrary, project is not accepted if the NPV is negative. Scenario analysis is the process of

project management that analyses various scenarios for predicting their impacts including

both positive as well as negative (Gallo 2014). In the given case, the computation of NPV

under different scenarios have been computed as below –

Normal case –

Above table presents the schedule of the bank’s non-current assets that portrays that

the amount invested in non-current assets have been reduced over the past period of 3 years.

However, amount of total assets have been increased over the same period that is indicating

that the bank is shifting towards investment in current assets rather than non-current assets.

Though the company purchased some property, plant and equipment (PPE) during the

concerned period amount of PPE sold is more as compared to amount of PPE purchased by

it. Hence, the amount of PPE reduced from $3873 million to $2383 million over the concerned

period. The company used straight line method for depreciating PPE. Hence, the value of

PPE is uniformly reduced over their useful life till it reaches the salvage value (Gamayuni

2015).

Operating cash flow is the section represented under the cash flow statement that

delivers information of the entity’s ability to generate cash from the core activities of the entity.

Generally the operating cash flow is computed as per the below mentioned formula –

Operating cash flow = Net income + non-cash expenses + changes in the working capital.

Non-cash expenses include the expenses like depreciation or amortization expenses

represented under the income statement of the organization. While computing the cash flow

of a long term project depreciation is deducted while computing the project’s income.

However, at the time of computing the cash flow the depreciation expenses is added back as

the same is non-cash expenses. Further, while computing the capex the depreciation

expenses is added to the difference of current PPE and previous PPE. This is analysed while

purchasing long term asset as the same are not shown under income statement but have

significant impact on the cash flows (Huang and Kou 2014).

2.4 Scenario analysis

Net present value (NPV) is fundamental profitability measure for profitability of the

investments project. It is equal to sum of the present values of entire cash flows including

inflows as well as outflows of any project. The project is acceptable if the NPV of the project is

positive as positive NPV determines that the project will create shareholder’s wealth. On the

contrary, project is not accepted if the NPV is negative. Scenario analysis is the process of

project management that analyses various scenarios for predicting their impacts including

both positive as well as negative (Gallo 2014). In the given case, the computation of NPV

under different scenarios have been computed as below –

Normal case –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE FOR BUSINESS - MASTERS

Worst case –

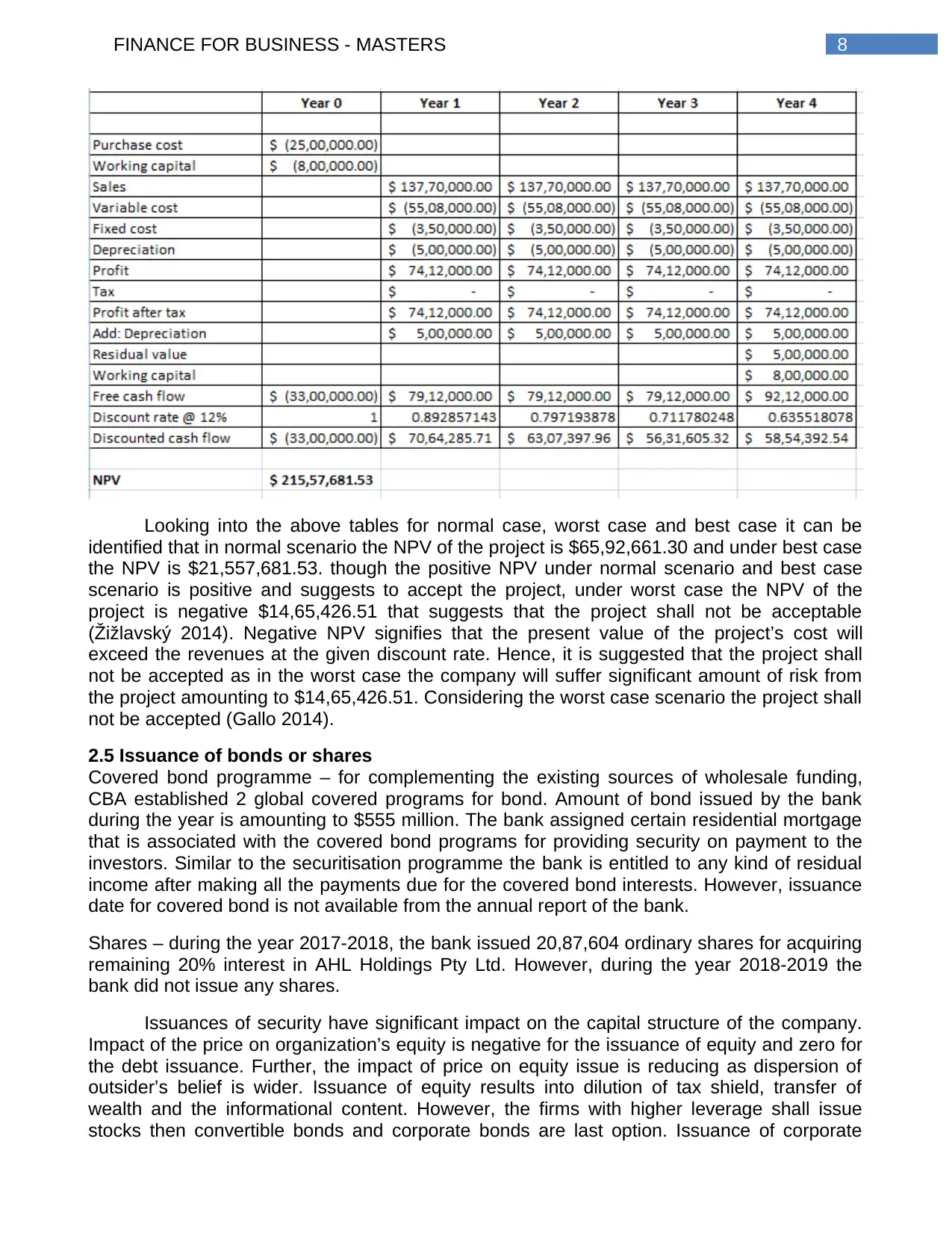

Best case –

Worst case –

Best case –

8FINANCE FOR BUSINESS - MASTERS

Looking into the above tables for normal case, worst case and best case it can be

identified that in normal scenario the NPV of the project is $65,92,661.30 and under best case

the NPV is $21,557,681.53. though the positive NPV under normal scenario and best case

scenario is positive and suggests to accept the project, under worst case the NPV of the

project is negative $14,65,426.51 that suggests that the project shall not be acceptable

(Žižlavský 2014). Negative NPV signifies that the present value of the project’s cost will

exceed the revenues at the given discount rate. Hence, it is suggested that the project shall

not be accepted as in the worst case the company will suffer significant amount of risk from

the project amounting to $14,65,426.51. Considering the worst case scenario the project shall

not be accepted (Gallo 2014).

2.5 Issuance of bonds or shares

Covered bond programme – for complementing the existing sources of wholesale funding,

CBA established 2 global covered programs for bond. Amount of bond issued by the bank

during the year is amounting to $555 million. The bank assigned certain residential mortgage

that is associated with the covered bond programs for providing security on payment to the

investors. Similar to the securitisation programme the bank is entitled to any kind of residual

income after making all the payments due for the covered bond interests. However, issuance

date for covered bond is not available from the annual report of the bank.

Shares – during the year 2017-2018, the bank issued 20,87,604 ordinary shares for acquiring

remaining 20% interest in AHL Holdings Pty Ltd. However, during the year 2018-2019 the

bank did not issue any shares.

Issuances of security have significant impact on the capital structure of the company.

Impact of the price on organization’s equity is negative for the issuance of equity and zero for

the debt issuance. Further, the impact of price on equity issue is reducing as dispersion of

outsider’s belief is wider. Issuance of equity results into dilution of tax shield, transfer of

wealth and the informational content. However, the firms with higher leverage shall issue

stocks then convertible bonds and corporate bonds are last option. Issuance of corporate

Looking into the above tables for normal case, worst case and best case it can be

identified that in normal scenario the NPV of the project is $65,92,661.30 and under best case

the NPV is $21,557,681.53. though the positive NPV under normal scenario and best case

scenario is positive and suggests to accept the project, under worst case the NPV of the

project is negative $14,65,426.51 that suggests that the project shall not be acceptable

(Žižlavský 2014). Negative NPV signifies that the present value of the project’s cost will

exceed the revenues at the given discount rate. Hence, it is suggested that the project shall

not be accepted as in the worst case the company will suffer significant amount of risk from

the project amounting to $14,65,426.51. Considering the worst case scenario the project shall

not be accepted (Gallo 2014).

2.5 Issuance of bonds or shares

Covered bond programme – for complementing the existing sources of wholesale funding,

CBA established 2 global covered programs for bond. Amount of bond issued by the bank

during the year is amounting to $555 million. The bank assigned certain residential mortgage

that is associated with the covered bond programs for providing security on payment to the

investors. Similar to the securitisation programme the bank is entitled to any kind of residual

income after making all the payments due for the covered bond interests. However, issuance

date for covered bond is not available from the annual report of the bank.

Shares – during the year 2017-2018, the bank issued 20,87,604 ordinary shares for acquiring

remaining 20% interest in AHL Holdings Pty Ltd. However, during the year 2018-2019 the

bank did not issue any shares.

Issuances of security have significant impact on the capital structure of the company.

Impact of the price on organization’s equity is negative for the issuance of equity and zero for

the debt issuance. Further, the impact of price on equity issue is reducing as dispersion of

outsider’s belief is wider. Issuance of equity results into dilution of tax shield, transfer of

wealth and the informational content. However, the firms with higher leverage shall issue

stocks then convertible bonds and corporate bonds are last option. Issuance of corporate

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE FOR BUSINESS - MASTERS

bonds have negative impact on the price earnings, however, the impact reduces over the long

term period. However, on short term period no significant impact is there on yield if corporate

bonds are issued (Karna, Richter and Riesenkampff 2016).

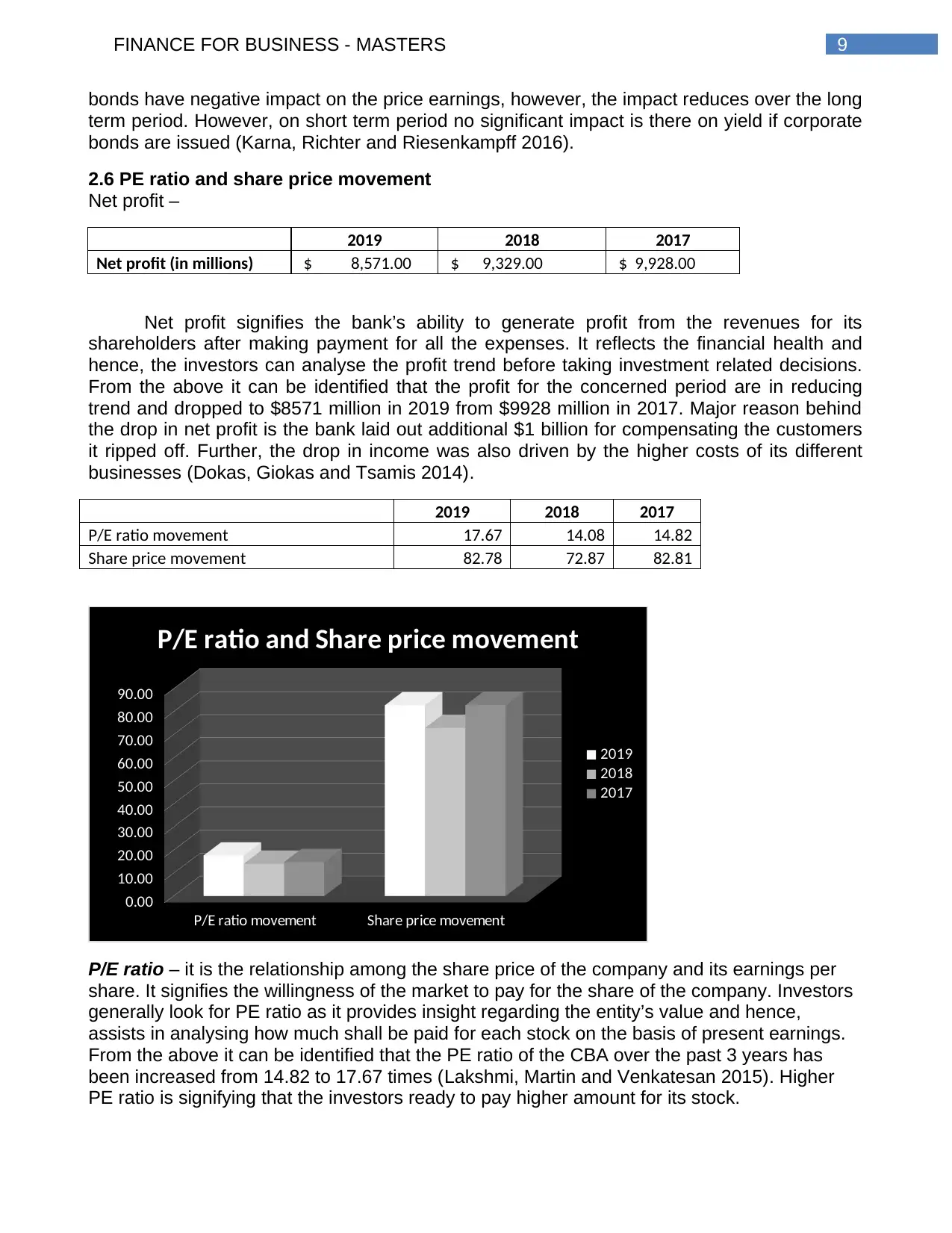

2.6 PE ratio and share price movement

Net profit –

2019 2018 2017

Net profit (in millions) $ 8,571.00 $ 9,329.00 $ 9,928.00

Net profit signifies the bank’s ability to generate profit from the revenues for its

shareholders after making payment for all the expenses. It reflects the financial health and

hence, the investors can analyse the profit trend before taking investment related decisions.

From the above it can be identified that the profit for the concerned period are in reducing

trend and dropped to $8571 million in 2019 from $9928 million in 2017. Major reason behind

the drop in net profit is the bank laid out additional $1 billion for compensating the customers

it ripped off. Further, the drop in income was also driven by the higher costs of its different

businesses (Dokas, Giokas and Tsamis 2014).

2019 2018 2017

P/E ratio movement 17.67 14.08 14.82

Share price movement 82.78 72.87 82.81

P/E ratio movement Share price movement

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

P/E ratio and Share price movement

2019

2018

2017

P/E ratio – it is the relationship among the share price of the company and its earnings per

share. It signifies the willingness of the market to pay for the share of the company. Investors

generally look for PE ratio as it provides insight regarding the entity’s value and hence,

assists in analysing how much shall be paid for each stock on the basis of present earnings.

From the above it can be identified that the PE ratio of the CBA over the past 3 years has

been increased from 14.82 to 17.67 times (Lakshmi, Martin and Venkatesan 2015). Higher

PE ratio is signifying that the investors ready to pay higher amount for its stock.

bonds have negative impact on the price earnings, however, the impact reduces over the long

term period. However, on short term period no significant impact is there on yield if corporate

bonds are issued (Karna, Richter and Riesenkampff 2016).

2.6 PE ratio and share price movement

Net profit –

2019 2018 2017

Net profit (in millions) $ 8,571.00 $ 9,329.00 $ 9,928.00

Net profit signifies the bank’s ability to generate profit from the revenues for its

shareholders after making payment for all the expenses. It reflects the financial health and

hence, the investors can analyse the profit trend before taking investment related decisions.

From the above it can be identified that the profit for the concerned period are in reducing

trend and dropped to $8571 million in 2019 from $9928 million in 2017. Major reason behind

the drop in net profit is the bank laid out additional $1 billion for compensating the customers

it ripped off. Further, the drop in income was also driven by the higher costs of its different

businesses (Dokas, Giokas and Tsamis 2014).

2019 2018 2017

P/E ratio movement 17.67 14.08 14.82

Share price movement 82.78 72.87 82.81

P/E ratio movement Share price movement

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

80.00

90.00

P/E ratio and Share price movement

2019

2018

2017

P/E ratio – it is the relationship among the share price of the company and its earnings per

share. It signifies the willingness of the market to pay for the share of the company. Investors

generally look for PE ratio as it provides insight regarding the entity’s value and hence,

assists in analysing how much shall be paid for each stock on the basis of present earnings.

From the above it can be identified that the PE ratio of the CBA over the past 3 years has

been increased from 14.82 to 17.67 times (Lakshmi, Martin and Venkatesan 2015). Higher

PE ratio is signifying that the investors ready to pay higher amount for its stock.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE FOR BUSINESS - MASTERS

Share price movement – looking into the trend of share price movement over the last 3

years it is identified that though the net profit are in reducing trend, the share price went up to

$ 82.78 per share in 2019 from $ 72.87 per share in 2018 (Asx.com.au 2019). There are

differences between the trend of profit and share price as net profit drop as the bank laid out

additional $1 billion for compensating the customers it ripped off and excess expenses for

various businesses (Mayes 2014). However, the share price is increasing for last 6 months as

it followed the resolution of Hayne Royal Commission earlier 2019. The bank that was the

centre of different scandals start following the resolution of Hayne Royal Commission and

also pledged for shutting down one of its division that was most troubled that led to increase

of confidence among investors and hence, the share price went up (Asx.com.au 2019).

III. Recommendation letter

Andrew Johnson

Investment Solution Pty Ltd

231, Madison Avenue

Brisbane – 200 310

Date: 30th Aug 2019

Mr. John Taylor

299 Park Road,

Brisbane

Subject: Recommendation for investment portfolio

Dear Mr Taylor

This is to inform you I have completed the financial analysis of Commonwealth Bank taking

into consideration its performance over the past 3 years. Based on the analysis, I would like

to inform you that the net profit of the bank is in reducing trend however, the PE ratio and

share price have been improved. This denotes that even if the profit reduced, it is just the

temporary phase and the investors are ready to pay higher amount for each stock of the

bank. If the liquidity position is considered, it can be stated that the same is indicating that the

company is able to meet its liability efficiently. Though the bank has higher level of debt, it has

improved its leverage position over the last 3 years.

Hence, considering the overall performance it is recommended that the stock of CBA shall be

included in your portfolio.

Sincerely,

Andrew Johnson,

Investment analyst, Investment Solution Pty Ltd

Share price movement – looking into the trend of share price movement over the last 3

years it is identified that though the net profit are in reducing trend, the share price went up to

$ 82.78 per share in 2019 from $ 72.87 per share in 2018 (Asx.com.au 2019). There are

differences between the trend of profit and share price as net profit drop as the bank laid out

additional $1 billion for compensating the customers it ripped off and excess expenses for

various businesses (Mayes 2014). However, the share price is increasing for last 6 months as

it followed the resolution of Hayne Royal Commission earlier 2019. The bank that was the

centre of different scandals start following the resolution of Hayne Royal Commission and

also pledged for shutting down one of its division that was most troubled that led to increase

of confidence among investors and hence, the share price went up (Asx.com.au 2019).

III. Recommendation letter

Andrew Johnson

Investment Solution Pty Ltd

231, Madison Avenue

Brisbane – 200 310

Date: 30th Aug 2019

Mr. John Taylor

299 Park Road,

Brisbane

Subject: Recommendation for investment portfolio

Dear Mr Taylor

This is to inform you I have completed the financial analysis of Commonwealth Bank taking

into consideration its performance over the past 3 years. Based on the analysis, I would like

to inform you that the net profit of the bank is in reducing trend however, the PE ratio and

share price have been improved. This denotes that even if the profit reduced, it is just the

temporary phase and the investors are ready to pay higher amount for each stock of the

bank. If the liquidity position is considered, it can be stated that the same is indicating that the

company is able to meet its liability efficiently. Though the bank has higher level of debt, it has

improved its leverage position over the last 3 years.

Hence, considering the overall performance it is recommended that the stock of CBA shall be

included in your portfolio.

Sincerely,

Andrew Johnson,

Investment analyst, Investment Solution Pty Ltd

11FINANCE FOR BUSINESS - MASTERS

IV. Conclusion

As the evidences presented it can be concluded that CBA offers wide range of services

for assisting the Australians to build as well as manage the finances. Considering the financial

performances of the bank in terms of its liquidity position and capital structure that portrays its

solvency position it can be determined that the bank’s ability to receive deposits against

providing loans has been deteriorated over the period of last 3 years. It indicates that the

bank will not have considerable amount of available reserves for unforseen as well as

expected contingencies. However, as the same is more than 100%, the bank is still in good

position to maintain its liquidity position. Further, the capital structure of the bank includes

significantly high level of debt that may raise question on its future sustainability. However, it

has improved its debt position over the years. Net profit and PE ratio further indicates that

even if the profit over the years have been reduced, it is just the temporary phase and the

investors are ready to pay higher amount for each stock of the bank. Hence, the stock of CBA

can be considered for investment.

IV. Conclusion

As the evidences presented it can be concluded that CBA offers wide range of services

for assisting the Australians to build as well as manage the finances. Considering the financial

performances of the bank in terms of its liquidity position and capital structure that portrays its

solvency position it can be determined that the bank’s ability to receive deposits against

providing loans has been deteriorated over the period of last 3 years. It indicates that the

bank will not have considerable amount of available reserves for unforseen as well as

expected contingencies. However, as the same is more than 100%, the bank is still in good

position to maintain its liquidity position. Further, the capital structure of the bank includes

significantly high level of debt that may raise question on its future sustainability. However, it

has improved its debt position over the years. Net profit and PE ratio further indicates that

even if the profit over the years have been reduced, it is just the temporary phase and the

investors are ready to pay higher amount for each stock of the bank. Hence, the stock of CBA

can be considered for investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.