Financial Analysis Report: Commonwealth Bank Performance Evaluation

VerifiedAdded on 2023/04/04

|14

|3643

|99

Report

AI Summary

This report provides a comprehensive financial analysis of the Commonwealth Bank (CBA). It begins with an overview of CBA's core activities, market position, and historical context, highlighting its competitive advantages. The report then delves into a detailed financial analysis, including the calculation and interpretation of key performance ratios such as Return on Equity (ROE), Return on Assets (ROA), Net Profit Margin, Accounts Receivable Turnover, Receivable Turnover Days, and Asset Turnover Ratio. The analysis covers the years 2016-2018, providing trend analysis of the ratios. The report further examines the company's cash management cycle, discusses systematic and unsystematic risks, and analyzes the dividend policy and payout ratio. Finally, it concludes with a recommendation regarding the company's investment potential based on the financial findings.

Running head: FINANCE

Finance

Name of the student

Name of the university

Student ID

Author note

Finance

Name of the student

Name of the university

Student ID

Author note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCE

Abstract

Purpose of the report is to outline the core activities of Commonwealth Bank, market under

which it is operating and the history that may be significant for the company in gaining

competitive advantage. The report will focus on the financial analysis of the company

covering the description of the bank, computation and the analysis of performance ratios

including profitability ratio and efficiency ratios. It will further look into the cash management

cycle of the company through focusing on marketable securities and the systematic risks and

unsystematic risks involved with the company that may impact the financial performance

adversely. In addition to that it will also concentrate on the dividend policy and dividend

payout ratio of the company and whether the company can be considered for investment.

Abstract

Purpose of the report is to outline the core activities of Commonwealth Bank, market under

which it is operating and the history that may be significant for the company in gaining

competitive advantage. The report will focus on the financial analysis of the company

covering the description of the bank, computation and the analysis of performance ratios

including profitability ratio and efficiency ratios. It will further look into the cash management

cycle of the company through focusing on marketable securities and the systematic risks and

unsystematic risks involved with the company that may impact the financial performance

adversely. In addition to that it will also concentrate on the dividend policy and dividend

payout ratio of the company and whether the company can be considered for investment.

2FINANCE

Table of Contents

I. Introduction...........................................................................................................................3

II. Financial analysis.................................................................................................................3

2.1 Description of Commonwealth Bank.................................................................................3

2.2 Computation and the analysis of performance ratios.......................................................3

2.3 Cash management cycle...................................................................................................7

2.4 Sensitivity analysis............................................................................................................7

2.5 systematic risks and unsystematic risks that may impact the financial performance.......8

2.6 Dividend policy and dividend payout ratio.........................................................................9

III. Recommendation letter...................................................................................................10

IV. Conclusion......................................................................................................................10

Reference..................................................................................................................................12

Table of Contents

I. Introduction...........................................................................................................................3

II. Financial analysis.................................................................................................................3

2.1 Description of Commonwealth Bank.................................................................................3

2.2 Computation and the analysis of performance ratios.......................................................3

2.3 Cash management cycle...................................................................................................7

2.4 Sensitivity analysis............................................................................................................7

2.5 systematic risks and unsystematic risks that may impact the financial performance.......8

2.6 Dividend policy and dividend payout ratio.........................................................................9

III. Recommendation letter...................................................................................................10

IV. Conclusion......................................................................................................................10

Reference..................................................................................................................................12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCE

I. Introduction

Main purpose of the report is to outline the core activities of Commonwealth Bank,

market under which it is operating and the history that may be significant for the company in

gaining competitive advantage. The report will further, focus on the performance of the entity

based on the outcome of its profitability ratio and efficiency ratio. It will further recognize the

marketable securities of the company and will comment upon the securities for managing the

cash. In the next step the report will perform the sensitivity analysis with the help of the data

provided. Further, the report will discuss regarding the systematic as well as unsystematic

risks those may have adverse impact on the performance of the company. Moreover, the

dividend payout ratio of the company will be highlighted and will state the dividend policy of

the entity (Vogel, 2014).

Commonwealth bank (CBA) was established in the year 1911 under Commonwealth

Bank act and it started operating in next year that is in 1912. At present the bank has more

than 52000 employees and shareholders of more than 800,000. It provides wide range of

products and services required for financial business management and for helping the

progress of the business. Further, business banking products offered by the bank includes

business loans, business credit cards, business accounts, merchant services,

superannuation, asset finance, insurances, investments and management of international

money. It is the 1st bank that implemented the fully functioned mobile banking service. Though

other banks like Westpac and ANZ implemented the mobile banking service before CBA, it

was limited to iPhone only for full functioning. Further, adoption of methodologies like project

management, outsourcing and strategic planning helps it to solve various issues

(Commbank.com.au, 2019).

II. Financial analysis

2.1 Description of Commonwealth Bank

CBA is multinational financial institution that was established in Australia in early days

of 19th century. The bank’s vision is to become the finest organization in Australia in context of

financial services through standing out in providing the customer service and the strategies of

the bank is to identify considerable opportunities within the business for developing more

value for the customers, stakeholders and people. Major competitive advantage of the bank is

that it is significantly serious regarding the customer service. Further, it is one of the examples

regarding the technology adopted by the bank that delivers excellent services to the

customers through utilizing up-to-date technologies (Robinson et al., 2015). Business loan,

bank transactions and accounts and personal lending are the major products and the services

in the market. Customers prefer these services at different dimensions through different

characteristics and at different service quality, locations, geographies and prices. Major Banks

in Australian banking industry majorly competes over the price and sizes. However, adoption

of methodologies like project management, outsourcing and strategic planning helps it to

solve various issues and gain the competitive advantages over the competitors like NAB, ANZ

and Westpac (Omar et al., 2014).

2.2 Computation and the analysis of performance ratios

Profitability ratio –

I. Introduction

Main purpose of the report is to outline the core activities of Commonwealth Bank,

market under which it is operating and the history that may be significant for the company in

gaining competitive advantage. The report will further, focus on the performance of the entity

based on the outcome of its profitability ratio and efficiency ratio. It will further recognize the

marketable securities of the company and will comment upon the securities for managing the

cash. In the next step the report will perform the sensitivity analysis with the help of the data

provided. Further, the report will discuss regarding the systematic as well as unsystematic

risks those may have adverse impact on the performance of the company. Moreover, the

dividend payout ratio of the company will be highlighted and will state the dividend policy of

the entity (Vogel, 2014).

Commonwealth bank (CBA) was established in the year 1911 under Commonwealth

Bank act and it started operating in next year that is in 1912. At present the bank has more

than 52000 employees and shareholders of more than 800,000. It provides wide range of

products and services required for financial business management and for helping the

progress of the business. Further, business banking products offered by the bank includes

business loans, business credit cards, business accounts, merchant services,

superannuation, asset finance, insurances, investments and management of international

money. It is the 1st bank that implemented the fully functioned mobile banking service. Though

other banks like Westpac and ANZ implemented the mobile banking service before CBA, it

was limited to iPhone only for full functioning. Further, adoption of methodologies like project

management, outsourcing and strategic planning helps it to solve various issues

(Commbank.com.au, 2019).

II. Financial analysis

2.1 Description of Commonwealth Bank

CBA is multinational financial institution that was established in Australia in early days

of 19th century. The bank’s vision is to become the finest organization in Australia in context of

financial services through standing out in providing the customer service and the strategies of

the bank is to identify considerable opportunities within the business for developing more

value for the customers, stakeholders and people. Major competitive advantage of the bank is

that it is significantly serious regarding the customer service. Further, it is one of the examples

regarding the technology adopted by the bank that delivers excellent services to the

customers through utilizing up-to-date technologies (Robinson et al., 2015). Business loan,

bank transactions and accounts and personal lending are the major products and the services

in the market. Customers prefer these services at different dimensions through different

characteristics and at different service quality, locations, geographies and prices. Major Banks

in Australian banking industry majorly competes over the price and sizes. However, adoption

of methodologies like project management, outsourcing and strategic planning helps it to

solve various issues and gain the competitive advantages over the competitors like NAB, ANZ

and Westpac (Omar et al., 2014).

2.2 Computation and the analysis of performance ratios

Profitability ratio –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCE

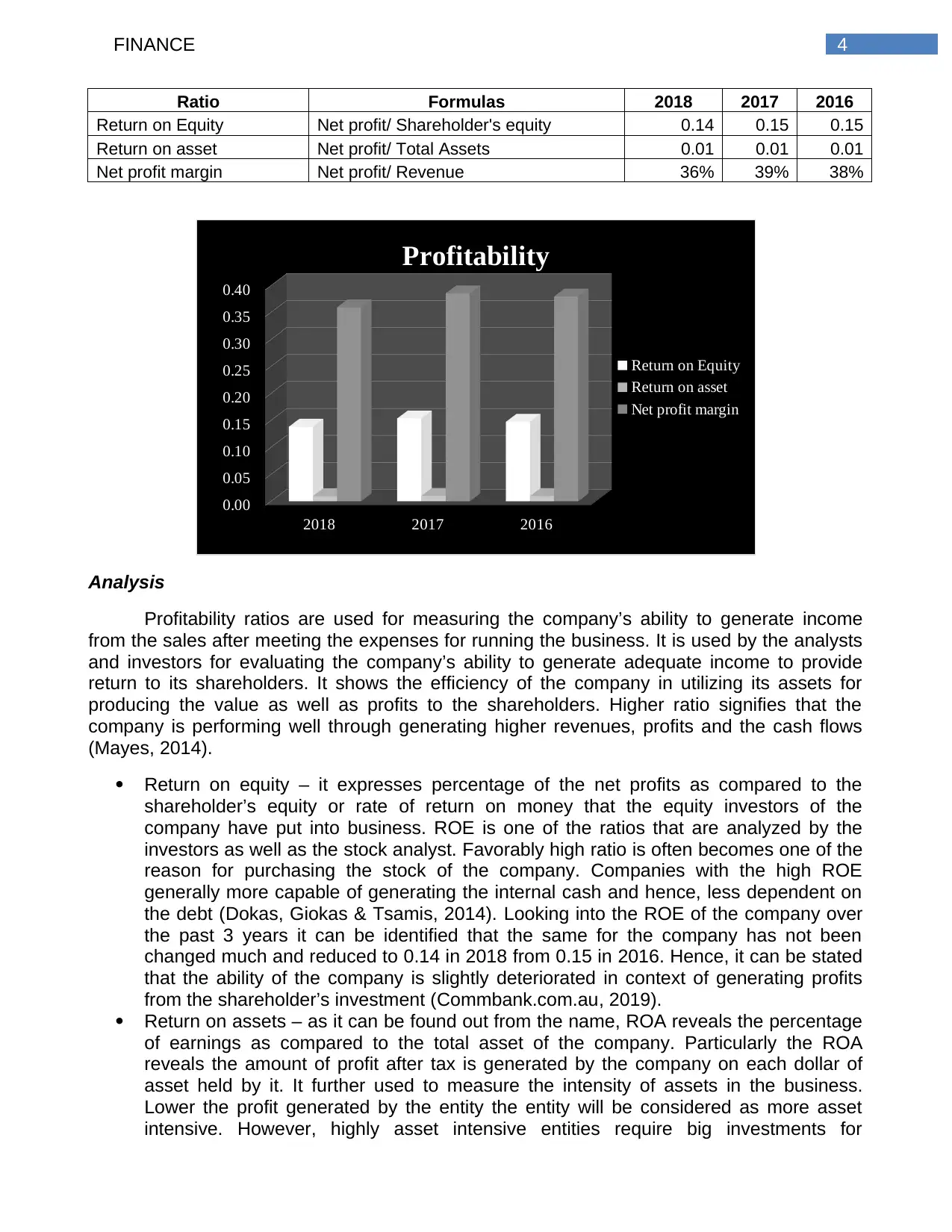

Ratio Formulas 2018 2017 2016

Return on Equity Net profit/ Shareholder's equity 0.14 0.15 0.15

Return on asset Net profit/ Total Assets 0.01 0.01 0.01

Net profit margin Net profit/ Revenue 36% 39% 38%

2018 2017 2016

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Profitability

Return on Equity

Return on asset

Net profit margin

Analysis

Profitability ratios are used for measuring the company’s ability to generate income

from the sales after meeting the expenses for running the business. It is used by the analysts

and investors for evaluating the company’s ability to generate adequate income to provide

return to its shareholders. It shows the efficiency of the company in utilizing its assets for

producing the value as well as profits to the shareholders. Higher ratio signifies that the

company is performing well through generating higher revenues, profits and the cash flows

(Mayes, 2014).

Return on equity – it expresses percentage of the net profits as compared to the

shareholder’s equity or rate of return on money that the equity investors of the

company have put into business. ROE is one of the ratios that are analyzed by the

investors as well as the stock analyst. Favorably high ratio is often becomes one of the

reason for purchasing the stock of the company. Companies with the high ROE

generally more capable of generating the internal cash and hence, less dependent on

the debt (Dokas, Giokas & Tsamis, 2014). Looking into the ROE of the company over

the past 3 years it can be identified that the same for the company has not been

changed much and reduced to 0.14 in 2018 from 0.15 in 2016. Hence, it can be stated

that the ability of the company is slightly deteriorated in context of generating profits

from the shareholder’s investment (Commbank.com.au, 2019).

Return on assets – as it can be found out from the name, ROA reveals the percentage

of earnings as compared to the total asset of the company. Particularly the ROA

reveals the amount of profit after tax is generated by the company on each dollar of

asset held by it. It further used to measure the intensity of assets in the business.

Lower the profit generated by the entity the entity will be considered as more asset

intensive. However, highly asset intensive entities require big investments for

Ratio Formulas 2018 2017 2016

Return on Equity Net profit/ Shareholder's equity 0.14 0.15 0.15

Return on asset Net profit/ Total Assets 0.01 0.01 0.01

Net profit margin Net profit/ Revenue 36% 39% 38%

2018 2017 2016

0.00

0.05

0.10

0.15

0.20

0.25

0.30

0.35

0.40

Profitability

Return on Equity

Return on asset

Net profit margin

Analysis

Profitability ratios are used for measuring the company’s ability to generate income

from the sales after meeting the expenses for running the business. It is used by the analysts

and investors for evaluating the company’s ability to generate adequate income to provide

return to its shareholders. It shows the efficiency of the company in utilizing its assets for

producing the value as well as profits to the shareholders. Higher ratio signifies that the

company is performing well through generating higher revenues, profits and the cash flows

(Mayes, 2014).

Return on equity – it expresses percentage of the net profits as compared to the

shareholder’s equity or rate of return on money that the equity investors of the

company have put into business. ROE is one of the ratios that are analyzed by the

investors as well as the stock analyst. Favorably high ratio is often becomes one of the

reason for purchasing the stock of the company. Companies with the high ROE

generally more capable of generating the internal cash and hence, less dependent on

the debt (Dokas, Giokas & Tsamis, 2014). Looking into the ROE of the company over

the past 3 years it can be identified that the same for the company has not been

changed much and reduced to 0.14 in 2018 from 0.15 in 2016. Hence, it can be stated

that the ability of the company is slightly deteriorated in context of generating profits

from the shareholder’s investment (Commbank.com.au, 2019).

Return on assets – as it can be found out from the name, ROA reveals the percentage

of earnings as compared to the total asset of the company. Particularly the ROA

reveals the amount of profit after tax is generated by the company on each dollar of

asset held by it. It further used to measure the intensity of assets in the business.

Lower the profit generated by the entity the entity will be considered as more asset

intensive. However, highly asset intensive entities require big investments for

5FINANCE

purchasing the equipments and machineries for generating income. Looking into the

ROA of the company over the past 3 years it can be identified that the same for the

company has not been changed over the past 3 years. Hence, it can be stated that the

ability of the company has not been changed in context of generating profits through

deploying its assets (Commbank.com.au, 2019).

Net profit margin – net profit is the bottom line of the business. It focuses on the net

income of the entity and it compares the net profit with the revenues earned by it. Net

profit margin provides the final picture regarding how profitable the company is after

paying all the expenses including taxes and interests. Reason behind using net profit

margin as measure of the profitability is that it takes everything into consideration.

Major drawback of net profit margin is that it includes lot of noise like gains, time

expenses that make it harder for the compatibility sake. Looking into the net profit

margin of the company over the past 3 years it can be identified that the same for the

company has been reduced over the past 3 years and reduced to 36% in 2018 from

38% in 2016. Hence, it can be stated that the ability of the company has been reduced

in context of generating profits through revenues (Commbank.com.au, 2019).

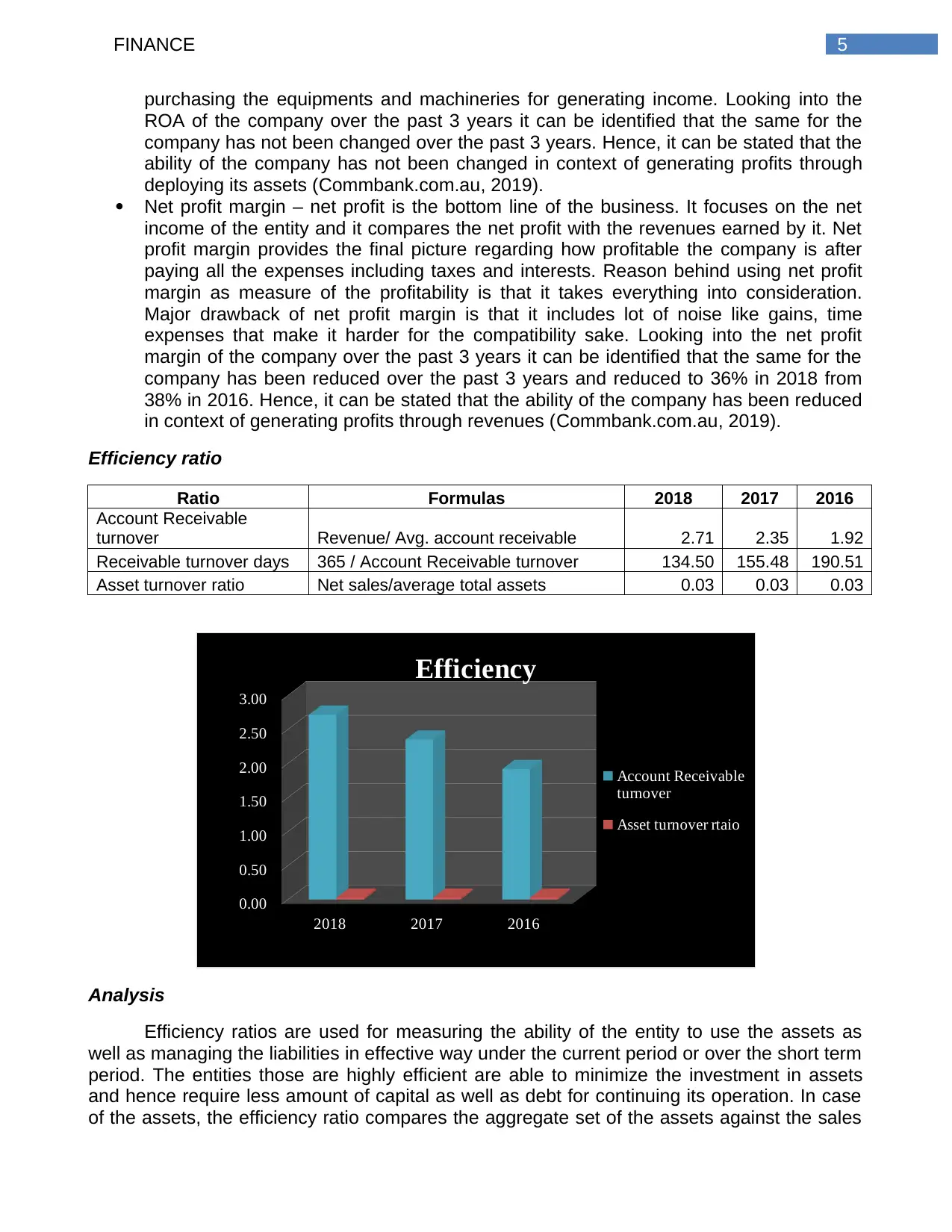

Efficiency ratio

Ratio Formulas 2018 2017 2016

Account Receivable

turnover Revenue/ Avg. account receivable 2.71 2.35 1.92

Receivable turnover days 365 / Account Receivable turnover 134.50 155.48 190.51

Asset turnover ratio Net sales/average total assets 0.03 0.03 0.03

2018 2017 2016

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Efficiency

Account Receivable

turnover

Asset turnover rtaio

Analysis

Efficiency ratios are used for measuring the ability of the entity to use the assets as

well as managing the liabilities in effective way under the current period or over the short term

period. The entities those are highly efficient are able to minimize the investment in assets

and hence require less amount of capital as well as debt for continuing its operation. In case

of the assets, the efficiency ratio compares the aggregate set of the assets against the sales

purchasing the equipments and machineries for generating income. Looking into the

ROA of the company over the past 3 years it can be identified that the same for the

company has not been changed over the past 3 years. Hence, it can be stated that the

ability of the company has not been changed in context of generating profits through

deploying its assets (Commbank.com.au, 2019).

Net profit margin – net profit is the bottom line of the business. It focuses on the net

income of the entity and it compares the net profit with the revenues earned by it. Net

profit margin provides the final picture regarding how profitable the company is after

paying all the expenses including taxes and interests. Reason behind using net profit

margin as measure of the profitability is that it takes everything into consideration.

Major drawback of net profit margin is that it includes lot of noise like gains, time

expenses that make it harder for the compatibility sake. Looking into the net profit

margin of the company over the past 3 years it can be identified that the same for the

company has been reduced over the past 3 years and reduced to 36% in 2018 from

38% in 2016. Hence, it can be stated that the ability of the company has been reduced

in context of generating profits through revenues (Commbank.com.au, 2019).

Efficiency ratio

Ratio Formulas 2018 2017 2016

Account Receivable

turnover Revenue/ Avg. account receivable 2.71 2.35 1.92

Receivable turnover days 365 / Account Receivable turnover 134.50 155.48 190.51

Asset turnover ratio Net sales/average total assets 0.03 0.03 0.03

2018 2017 2016

0.00

0.50

1.00

1.50

2.00

2.50

3.00

Efficiency

Account Receivable

turnover

Asset turnover rtaio

Analysis

Efficiency ratios are used for measuring the ability of the entity to use the assets as

well as managing the liabilities in effective way under the current period or over the short term

period. The entities those are highly efficient are able to minimize the investment in assets

and hence require less amount of capital as well as debt for continuing its operation. In case

of the assets, the efficiency ratio compares the aggregate set of the assets against the sales

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCE

or against COGS. In case of the liabilities the efficiency ratios measures the efficiency of the

company with which it can pay the dues to its suppliers from whom it has purchased the

goods.

Accounts receivable ratio and receivables turnover days – accounts receivable

turnover ratio is used for computing the efficiency of the company in terms of its ability

to collect the dues from the sales made in credit. The ratio sounds like complex

accounting concepts that involve credit sales and the average amount of receivables.

High receivables turnover ratio signifies that the entity is able to collect the debts on

time which in turn will increase the cash flows and the credit is extended to right type of

customers which in turn will result into less amount of bad debts. Looking into the

accounts receivable ratio of the company over the past 3 years it can be identified that

the same for the company are in increasing trend over the past 3 years and increased

to 2.71 times in 2018 from 1.92 times in 2016 (Brockman, Tresl & Unlu, 2014). Hence,

it can be stated that the efficiency of the company has been increased in context of

collecting debts from the debtors. On the other hand, the receivable turnover days

states the days taken by the company on an average to collect its debts within the time

frame generally the accounting period. Looking into the receivable turnover days of

the company over the past 3 years it can be identified that the same for the company

are in reducing trend over the past 3 years and reduced to 134.5 days in 2018 from

190.51 days in 2016. Hence, it can be stated that the efficiency of the company has

been increased in context of collecting debts from the debtors (Commbank.com.au,

2019).

Asset turnover ratio – ATR determines the entity’s ability in context of generating the

revenue from the assets trough comparing net sales of entity with total assets. It is

computed through dividing the net sales of the company by the average amount of

total assets. To be more specific, it determines the average assets generated by the

company through deploying each dollar of the asset. It provides an insight to creditors

as well as the investors into internal management of the entity. Low asset turnover

ratio reflects poor collection practice of the entity. Looking into the ATR of the company

over the past 3 years it can be identified that the same for the company has not been

changed over the years from 2016 to 2018 and the ATR of 0.3 is signifying that the

company shall try to improve the ATR. 2018 from 0.15 in 2016 (Commbank.com.au,

2019).

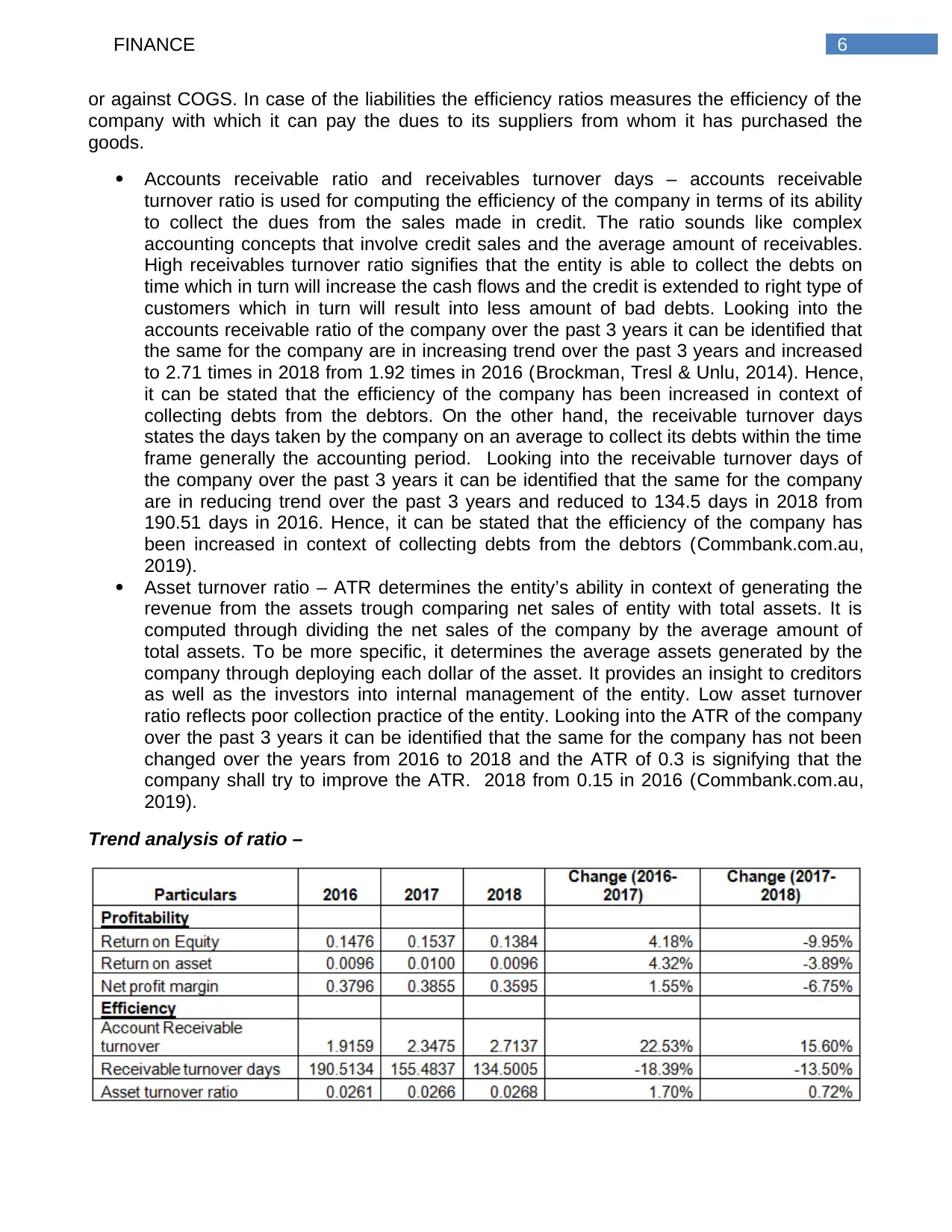

Trend analysis of ratio –

or against COGS. In case of the liabilities the efficiency ratios measures the efficiency of the

company with which it can pay the dues to its suppliers from whom it has purchased the

goods.

Accounts receivable ratio and receivables turnover days – accounts receivable

turnover ratio is used for computing the efficiency of the company in terms of its ability

to collect the dues from the sales made in credit. The ratio sounds like complex

accounting concepts that involve credit sales and the average amount of receivables.

High receivables turnover ratio signifies that the entity is able to collect the debts on

time which in turn will increase the cash flows and the credit is extended to right type of

customers which in turn will result into less amount of bad debts. Looking into the

accounts receivable ratio of the company over the past 3 years it can be identified that

the same for the company are in increasing trend over the past 3 years and increased

to 2.71 times in 2018 from 1.92 times in 2016 (Brockman, Tresl & Unlu, 2014). Hence,

it can be stated that the efficiency of the company has been increased in context of

collecting debts from the debtors. On the other hand, the receivable turnover days

states the days taken by the company on an average to collect its debts within the time

frame generally the accounting period. Looking into the receivable turnover days of

the company over the past 3 years it can be identified that the same for the company

are in reducing trend over the past 3 years and reduced to 134.5 days in 2018 from

190.51 days in 2016. Hence, it can be stated that the efficiency of the company has

been increased in context of collecting debts from the debtors (Commbank.com.au,

2019).

Asset turnover ratio – ATR determines the entity’s ability in context of generating the

revenue from the assets trough comparing net sales of entity with total assets. It is

computed through dividing the net sales of the company by the average amount of

total assets. To be more specific, it determines the average assets generated by the

company through deploying each dollar of the asset. It provides an insight to creditors

as well as the investors into internal management of the entity. Low asset turnover

ratio reflects poor collection practice of the entity. Looking into the ATR of the company

over the past 3 years it can be identified that the same for the company has not been

changed over the years from 2016 to 2018 and the ATR of 0.3 is signifying that the

company shall try to improve the ATR. 2018 from 0.15 in 2016 (Commbank.com.au,

2019).

Trend analysis of ratio –

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCE

From the above table it can be identified that all the profitability ratios over the years

from 2016 to 2017 has been in increasing trend. However, over the years from 2017 to 2018

the profitability ratios are in reducing trend. Hence, it is signifying that though the profitability

status of the company improved over 2016 – 2017, over the period of 2017-2018 it has been

deteriorated. On the other hand, if the efficiency ratios are considered it can be identified that

all the efficiency ratios over the years from 2016 to 2017 as well as from 2017 to 2018 have

been in increasing trend (Byrne & O’Connor, 2017)

2.3 Cash management cycle

Marketable securities reported by the company for the year ended 30th June 2018 are as

follows –

Trading assets - $ 32,254 million

Insurance assets - $ 372 million

Other assets - $ 258 million

Investments available for sale - $ 32,133 million (Commbank.com.au, 2019).

The entity reports marketable securities owned by it in the financial statement.

Marketable securities can be used for improving the cash management cycle of the company

as the marketable securities are readily available and are expected to get converted into cash

within period of 1 year (Ahmed, 2015).

2.4 Sensitivity analysis

Sensitivity analysis is analysis of how sensitive the result of the capital budgeting is to

the variable like discount rate, keeping other variables constant. It is useful as it reveals

model user regarding how dependent is the value of output is with the value of each input. It

provides the idea regarding how much flexibility it has for each of the variable for going

adverse. Further it helps to assess the risks. From the given data the NPV of the project and

the sensitivity analysis will be as follows –

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Sales Revenue

6,000,000.

0

6,000,000.

0

6,000,000.

0

6,000,000.

0

Total Variable

Costs

3,600,000.

0

3,600,000.

0

3,600,000.

0

3,600,000.

0

Fixed operating

costs 300,000.0 300,000.0 300,000.0 300,000.0

Depreciation

Expenses 450,000.0 450,000.0 450,000.0 450,000.0

Total Expenses @

30%

4,350,000.

0

4,350,000.

0

4,350,000.

0

4,350,000.

0

Profit before tax

1,650,000.

0

1,650,000.

0

1,650,000.

0

1,650,000.

0

Tax Expenses 495,000.0 495,000.0 495,000.0 495,000.0

Profit After Tax

1,155,000.

0

1,155,000.

0

1,155,000.

0

1,155,000.

0

Add: Depreciation 450,000.0 450,000.0 450,000.0 450,000.0

Free cash flow

1,605,000.

0

1,605,000.

0

1,605,000.

0

1,605,000.

0

From the above table it can be identified that all the profitability ratios over the years

from 2016 to 2017 has been in increasing trend. However, over the years from 2017 to 2018

the profitability ratios are in reducing trend. Hence, it is signifying that though the profitability

status of the company improved over 2016 – 2017, over the period of 2017-2018 it has been

deteriorated. On the other hand, if the efficiency ratios are considered it can be identified that

all the efficiency ratios over the years from 2016 to 2017 as well as from 2017 to 2018 have

been in increasing trend (Byrne & O’Connor, 2017)

2.3 Cash management cycle

Marketable securities reported by the company for the year ended 30th June 2018 are as

follows –

Trading assets - $ 32,254 million

Insurance assets - $ 372 million

Other assets - $ 258 million

Investments available for sale - $ 32,133 million (Commbank.com.au, 2019).

The entity reports marketable securities owned by it in the financial statement.

Marketable securities can be used for improving the cash management cycle of the company

as the marketable securities are readily available and are expected to get converted into cash

within period of 1 year (Ahmed, 2015).

2.4 Sensitivity analysis

Sensitivity analysis is analysis of how sensitive the result of the capital budgeting is to

the variable like discount rate, keeping other variables constant. It is useful as it reveals

model user regarding how dependent is the value of output is with the value of each input. It

provides the idea regarding how much flexibility it has for each of the variable for going

adverse. Further it helps to assess the risks. From the given data the NPV of the project and

the sensitivity analysis will be as follows –

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Sales Revenue

6,000,000.

0

6,000,000.

0

6,000,000.

0

6,000,000.

0

Total Variable

Costs

3,600,000.

0

3,600,000.

0

3,600,000.

0

3,600,000.

0

Fixed operating

costs 300,000.0 300,000.0 300,000.0 300,000.0

Depreciation

Expenses 450,000.0 450,000.0 450,000.0 450,000.0

Total Expenses @

30%

4,350,000.

0

4,350,000.

0

4,350,000.

0

4,350,000.

0

Profit before tax

1,650,000.

0

1,650,000.

0

1,650,000.

0

1,650,000.

0

Tax Expenses 495,000.0 495,000.0 495,000.0 495,000.0

Profit After Tax

1,155,000.

0

1,155,000.

0

1,155,000.

0

1,155,000.

0

Add: Depreciation 450,000.0 450,000.0 450,000.0 450,000.0

Free cash flow

1,605,000.

0

1,605,000.

0

1,605,000.

0

1,605,000.

0

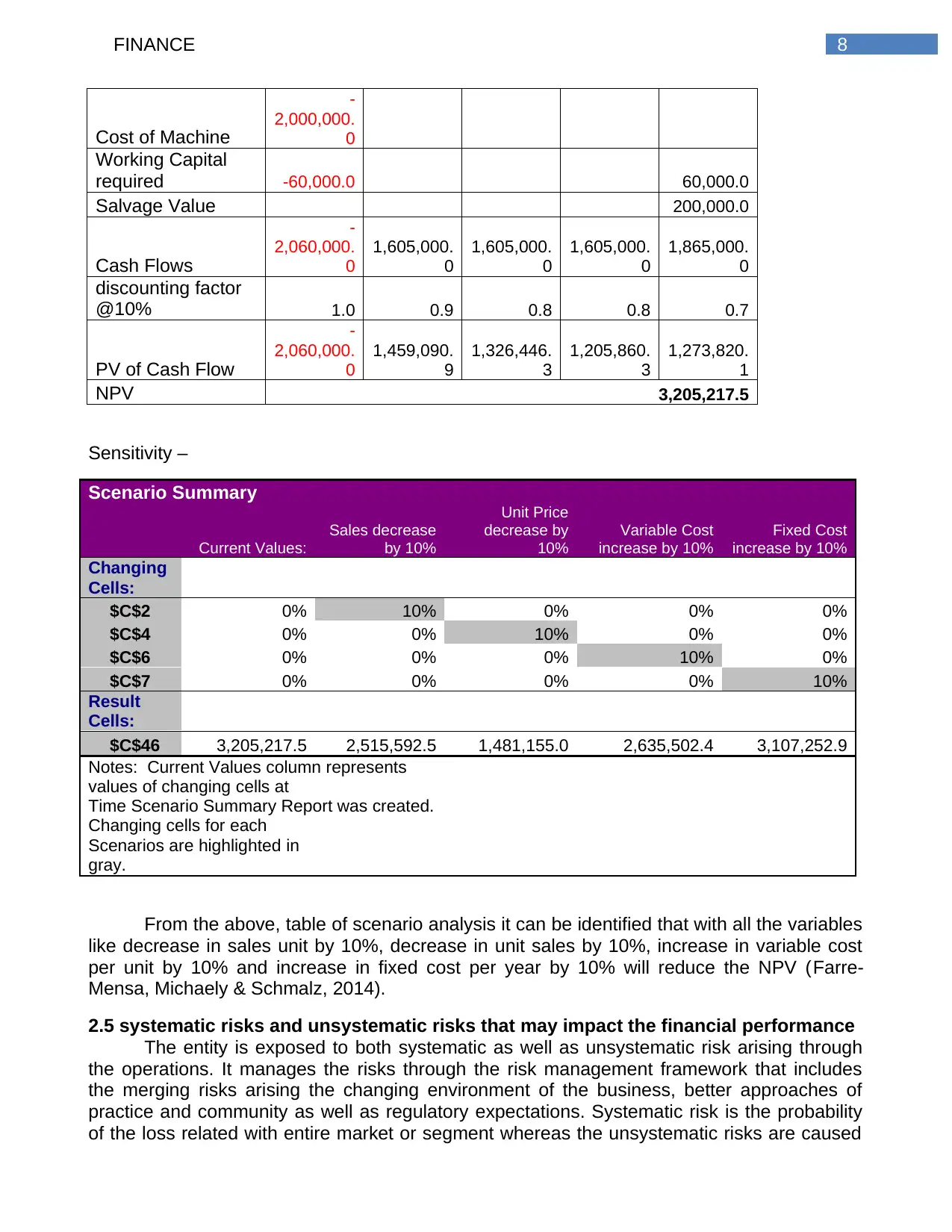

8FINANCE

Cost of Machine

-

2,000,000.

0

Working Capital

required -60,000.0 60,000.0

Salvage Value 200,000.0

Cash Flows

-

2,060,000.

0

1,605,000.

0

1,605,000.

0

1,605,000.

0

1,865,000.

0

discounting factor

@10% 1.0 0.9 0.8 0.8 0.7

PV of Cash Flow

-

2,060,000.

0

1,459,090.

9

1,326,446.

3

1,205,860.

3

1,273,820.

1

NPV 3,205,217.5

Sensitivity –

Scenario Summary

Current Values:

Sales decrease

by 10%

Unit Price

decrease by

10%

Variable Cost

increase by 10%

Fixed Cost

increase by 10%

Changing

Cells:

$C$2 0% 10% 0% 0% 0%

$C$4 0% 0% 10% 0% 0%

$C$6 0% 0% 0% 10% 0%

$C$7 0% 0% 0% 0% 10%

Result

Cells:

$C$46 3,205,217.5 2,515,592.5 1,481,155.0 2,635,502.4 3,107,252.9

Notes: Current Values column represents

values of changing cells at

Time Scenario Summary Report was created.

Changing cells for each

Scenarios are highlighted in

gray.

From the above, table of scenario analysis it can be identified that with all the variables

like decrease in sales unit by 10%, decrease in unit sales by 10%, increase in variable cost

per unit by 10% and increase in fixed cost per year by 10% will reduce the NPV (Farre-

Mensa, Michaely & Schmalz, 2014).

2.5 systematic risks and unsystematic risks that may impact the financial performance

The entity is exposed to both systematic as well as unsystematic risk arising through

the operations. It manages the risks through the risk management framework that includes

the merging risks arising the changing environment of the business, better approaches of

practice and community as well as regulatory expectations. Systematic risk is the probability

of the loss related with entire market or segment whereas the unsystematic risks are caused

Cost of Machine

-

2,000,000.

0

Working Capital

required -60,000.0 60,000.0

Salvage Value 200,000.0

Cash Flows

-

2,060,000.

0

1,605,000.

0

1,605,000.

0

1,605,000.

0

1,865,000.

0

discounting factor

@10% 1.0 0.9 0.8 0.8 0.7

PV of Cash Flow

-

2,060,000.

0

1,459,090.

9

1,326,446.

3

1,205,860.

3

1,273,820.

1

NPV 3,205,217.5

Sensitivity –

Scenario Summary

Current Values:

Sales decrease

by 10%

Unit Price

decrease by

10%

Variable Cost

increase by 10%

Fixed Cost

increase by 10%

Changing

Cells:

$C$2 0% 10% 0% 0% 0%

$C$4 0% 0% 10% 0% 0%

$C$6 0% 0% 0% 10% 0%

$C$7 0% 0% 0% 0% 10%

Result

Cells:

$C$46 3,205,217.5 2,515,592.5 1,481,155.0 2,635,502.4 3,107,252.9

Notes: Current Values column represents

values of changing cells at

Time Scenario Summary Report was created.

Changing cells for each

Scenarios are highlighted in

gray.

From the above, table of scenario analysis it can be identified that with all the variables

like decrease in sales unit by 10%, decrease in unit sales by 10%, increase in variable cost

per unit by 10% and increase in fixed cost per year by 10% will reduce the NPV (Farre-

Mensa, Michaely & Schmalz, 2014).

2.5 systematic risks and unsystematic risks that may impact the financial performance

The entity is exposed to both systematic as well as unsystematic risk arising through

the operations. It manages the risks through the risk management framework that includes

the merging risks arising the changing environment of the business, better approaches of

practice and community as well as regulatory expectations. Systematic risk is the probability

of the loss related with entire market or segment whereas the unsystematic risks are caused

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCE

owing to internal factors that can be controlled or can be reduced in relatively short span of

the time (Gamayuni, 2015).

Systematic risks involved with the company are as follows –

Credit risks – it is the potential for loss that arises from failure of counterparty to meet

the contractual obligation of the company. At the level of portfolio, credit risk involves

concentration risk that arises from independencies among customers and

concentration of exposures to the geographical regions and the industry sectors (Seay,

2014).

Market risks – it is the risk that the prices as well as market risks will change and it may

have adverse impact on the profitability or net worth of the company it includes the

changes in the interest rates, changes in the rates of foreign exchange, credit spreads,

commodity and equity prices and the resale value of the operating leased assets at the

maturity (Lakshmi, Martin & Venkatesan, 2015).

Unsystematic risks involved with the company are as follows –

Operational risk – it is the risk of the loss generated from failed or inadequate internal

processes, systems and people or from the external events.

Compliance risk – it is the risk associated with financial loss, reputational damage for

which the performance of the company may impacted adversely (Crane, Michenaud &

Weston, 2016).

2.6 Dividend policy and dividend payout ratio

The bank seeks to –

Pay the cash dividend at sustainable and strong levels

Maximize use of the franking account through paying the franked dividends fully

Target full year payout ratio of 70% - 80%

owing to internal factors that can be controlled or can be reduced in relatively short span of

the time (Gamayuni, 2015).

Systematic risks involved with the company are as follows –

Credit risks – it is the potential for loss that arises from failure of counterparty to meet

the contractual obligation of the company. At the level of portfolio, credit risk involves

concentration risk that arises from independencies among customers and

concentration of exposures to the geographical regions and the industry sectors (Seay,

2014).

Market risks – it is the risk that the prices as well as market risks will change and it may

have adverse impact on the profitability or net worth of the company it includes the

changes in the interest rates, changes in the rates of foreign exchange, credit spreads,

commodity and equity prices and the resale value of the operating leased assets at the

maturity (Lakshmi, Martin & Venkatesan, 2015).

Unsystematic risks involved with the company are as follows –

Operational risk – it is the risk of the loss generated from failed or inadequate internal

processes, systems and people or from the external events.

Compliance risk – it is the risk associated with financial loss, reputational damage for

which the performance of the company may impacted adversely (Crane, Michenaud &

Weston, 2016).

2.6 Dividend policy and dividend payout ratio

The bank seeks to –

Pay the cash dividend at sustainable and strong levels

Maximize use of the franking account through paying the franked dividends fully

Target full year payout ratio of 70% - 80%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCE

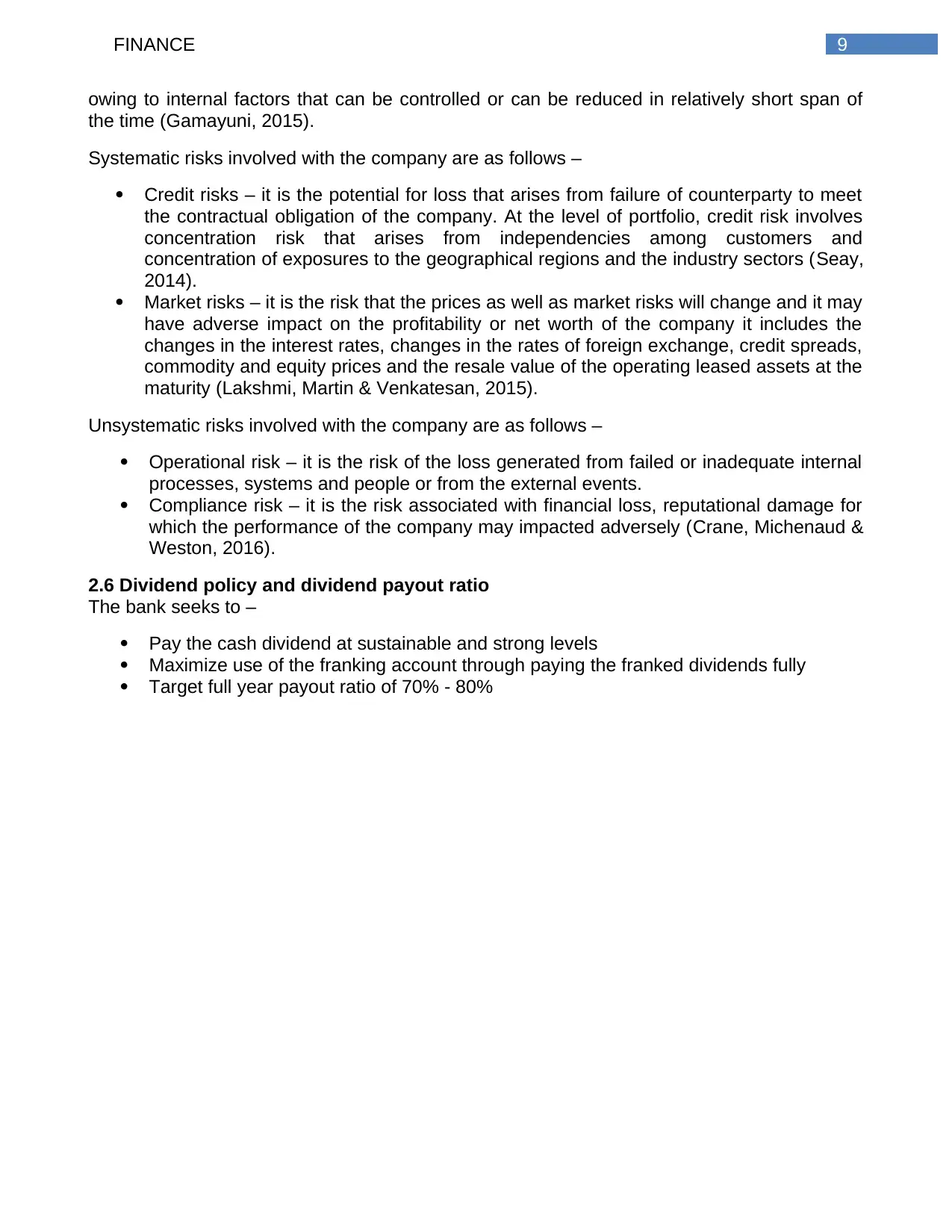

Dividend payout ratio –

Dividend payout ratio 2016 2017 2018

Dividend per share (A) 4.2 4.29 4.31

Earnings per share (B) 5.42 5.77 5.34

Dividend payout ratio (A/B) 77.49% 74.35% 80.71%

Dividend payout ratio is the dividend amount paid to the shareholders as compared to

total amount of company’s net income. It measures the net income percentage distributed to

the shareholders in form of dividends. Looking into the dividend payout ratio of the company it

can be identified that the company’s dividend payout ratio is increased from 77.49% to

80.71% over the periods from 2016 to 2018 (Floyd, Li & Skinner, 2015).

III. Recommendation letter

To: Mr John Haward

From: Emili Johnson, Investment analyst

NSW - 003

Date: 28th May 2019

Dear John,

Dividend payout ratio –

Dividend payout ratio 2016 2017 2018

Dividend per share (A) 4.2 4.29 4.31

Earnings per share (B) 5.42 5.77 5.34

Dividend payout ratio (A/B) 77.49% 74.35% 80.71%

Dividend payout ratio is the dividend amount paid to the shareholders as compared to

total amount of company’s net income. It measures the net income percentage distributed to

the shareholders in form of dividends. Looking into the dividend payout ratio of the company it

can be identified that the company’s dividend payout ratio is increased from 77.49% to

80.71% over the periods from 2016 to 2018 (Floyd, Li & Skinner, 2015).

III. Recommendation letter

To: Mr John Haward

From: Emili Johnson, Investment analyst

NSW - 003

Date: 28th May 2019

Dear John,

11FINANCE

This is to bring your kind attention that the analysis for Commonwealth Bank that was asked

by you has been completed. Looking into the performance of the bank over the last 3 years

covering the period from 2016 – 2018, it can be suggested that the bank can be considered

for investing the money. The reason behind this suggestion is that all the profitability ratios

over the years from 2016 to 2017 have been in increasing trend. However, though the same

over the years from 2017 to 2018 are in reducing trend it is still profitable and able to provide

return to the shareholders. On the other hand, if the efficiency ratios are considered it can be

identified that all the efficiency ratios over the years from 2016 to 2017 as well as from 2017

to 2018 have been in increasing trend. Hence, the performance of the company is signifying

that the shares of the entity can be purchased.

Sincerely,

Emili Johnson, Investment analyst

IV. Conclusion

It can be concluded from the above that the Commonwealth Bank provides wide range

of products and services required for financial business management and for helping the

progress of the business. Further, business banking products offered by the bank includes

business loans, business credit cards, business accounts, merchant services,

superannuation, asset finance, insurances, investments and management of international

money. Looking into the dividend payout ratio of the company it can be identified that the

company is regular in paying dividend and the company’s dividend payout ratio is increased

from 77.49% to 80.71% over the periods from 2016 to 2018. Further, the performance of the

company is signifying that the shares of the entity can be purchased.

This is to bring your kind attention that the analysis for Commonwealth Bank that was asked

by you has been completed. Looking into the performance of the bank over the last 3 years

covering the period from 2016 – 2018, it can be suggested that the bank can be considered

for investing the money. The reason behind this suggestion is that all the profitability ratios

over the years from 2016 to 2017 have been in increasing trend. However, though the same

over the years from 2017 to 2018 are in reducing trend it is still profitable and able to provide

return to the shareholders. On the other hand, if the efficiency ratios are considered it can be

identified that all the efficiency ratios over the years from 2016 to 2017 as well as from 2017

to 2018 have been in increasing trend. Hence, the performance of the company is signifying

that the shares of the entity can be purchased.

Sincerely,

Emili Johnson, Investment analyst

IV. Conclusion

It can be concluded from the above that the Commonwealth Bank provides wide range

of products and services required for financial business management and for helping the

progress of the business. Further, business banking products offered by the bank includes

business loans, business credit cards, business accounts, merchant services,

superannuation, asset finance, insurances, investments and management of international

money. Looking into the dividend payout ratio of the company it can be identified that the

company is regular in paying dividend and the company’s dividend payout ratio is increased

from 77.49% to 80.71% over the periods from 2016 to 2018. Further, the performance of the

company is signifying that the shares of the entity can be purchased.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.