Marketing Management: Analyzing Consumer Behavior at Commonwealth Bank

VerifiedAdded on 2023/04/25

|17

|4610

|497

Report

AI Summary

This report provides an analysis of customer buying behavior in the context of the Commonwealth Bank of Australia (CBA). It examines the influence of social factors on consumer decision-making and brand switching, referencing the Royal Banking Commission's findings on unethical practices and their impact on CBA's brand image. The report identifies CBA's target customer base as working-class individuals aged 30-54 and discusses the bank's segmentation strategies, including usage-based segmentation. It also assesses external factors in the Australian business market, marketing strategies such as digital marketing and cost leadership and product diversification and their impact on CBA's success. Ultimately, the report offers recommendations for enhancing customer engagement and mitigating the adverse effects of brand switching.

Running head: MARKETING MANAGEMENT

Marketing Management

Name of the Student:

Name of the University:

Author’s Note:

Marketing Management

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MARKETING MANAGEMENT

Table of Contents

Introduction................................................................................................................................2

Social factors and their influence on consumer decision-making and brand switching............2

Results from Situational Analysis..............................................................................................5

Individual difference influence factors and their influence on consumer decision-making......9

Recommendations....................................................................................................................12

Conclusion................................................................................................................................13

References................................................................................................................................14

Table of Contents

Introduction................................................................................................................................2

Social factors and their influence on consumer decision-making and brand switching............2

Results from Situational Analysis..............................................................................................5

Individual difference influence factors and their influence on consumer decision-making......9

Recommendations....................................................................................................................12

Conclusion................................................................................................................................13

References................................................................................................................................14

2MARKETING MANAGEMENT

Introduction

Ozuem, Howell & Lancaster (2016) are of the viewpoint that dynamicity of the

contemporary business world had caused a significant amount of change within the buying

behavior of the customers and also the kind of products or services that they opt for. Different

organizations are resorting to the usage of different kinds of strategies so as to influence the

buying behavior of the customers in the best possible manner and thereby to earn a higher

amount of revenue (McIlroy, 2018). This report will analyze the concept of customer buying

behavior and the impact of this concept in the particular context of the organization

Commonwealth Bank of Australia.

Social factors and their influence on consumer decision-making and brand switching

Commonwealth Bank of Australia also known by the name of CBA, founded in 1911

is not only the largest bank of Australia but also the largest bank of the entire Southern

Hemisphere (Commbank.com.au, 2019). More importantly, the bank is known for the

plethora of financial services that it offers to the customers starting from personal loans,

saving accounts to retail or commercial loans, insurance, pension plans and others

(Commbank.com.au, 2019). Furthermore, the bank under discussion here currently offers

employment services to more than 52,000 people from different parts of the nation and the

gross revenue generated by the organization for the year 2017 was more than A$26.005

billion (Commbank.com.au, 2019). In addition to these, the bank in conjunction with

Westpac, First National Bank and ANZ is called by the name of “Big Four” because of the

economic contribution that they make towards the national economy of Australia (McIlroy,

2018). However, the results of the Royal Banking Commission of 2017 revealed that the bank

along with the other ones of Australia were taking the help of unethical as well as unfair

business practices to enhance the amount of revenue gained by them and were at the same

Introduction

Ozuem, Howell & Lancaster (2016) are of the viewpoint that dynamicity of the

contemporary business world had caused a significant amount of change within the buying

behavior of the customers and also the kind of products or services that they opt for. Different

organizations are resorting to the usage of different kinds of strategies so as to influence the

buying behavior of the customers in the best possible manner and thereby to earn a higher

amount of revenue (McIlroy, 2018). This report will analyze the concept of customer buying

behavior and the impact of this concept in the particular context of the organization

Commonwealth Bank of Australia.

Social factors and their influence on consumer decision-making and brand switching

Commonwealth Bank of Australia also known by the name of CBA, founded in 1911

is not only the largest bank of Australia but also the largest bank of the entire Southern

Hemisphere (Commbank.com.au, 2019). More importantly, the bank is known for the

plethora of financial services that it offers to the customers starting from personal loans,

saving accounts to retail or commercial loans, insurance, pension plans and others

(Commbank.com.au, 2019). Furthermore, the bank under discussion here currently offers

employment services to more than 52,000 people from different parts of the nation and the

gross revenue generated by the organization for the year 2017 was more than A$26.005

billion (Commbank.com.au, 2019). In addition to these, the bank in conjunction with

Westpac, First National Bank and ANZ is called by the name of “Big Four” because of the

economic contribution that they make towards the national economy of Australia (McIlroy,

2018). However, the results of the Royal Banking Commission of 2017 revealed that the bank

along with the other ones of Australia were taking the help of unethical as well as unfair

business practices to enhance the amount of revenue gained by them and were at the same

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MARKETING MANAGEMENT

time misleading the customers as well (O'Connor, 2018). This had adversely affected the

business prospects of the under discussion here and the net result of this is that the bank had

lost a substantial amount of the monopoly that it used to hold in the financial business market

of Australia.

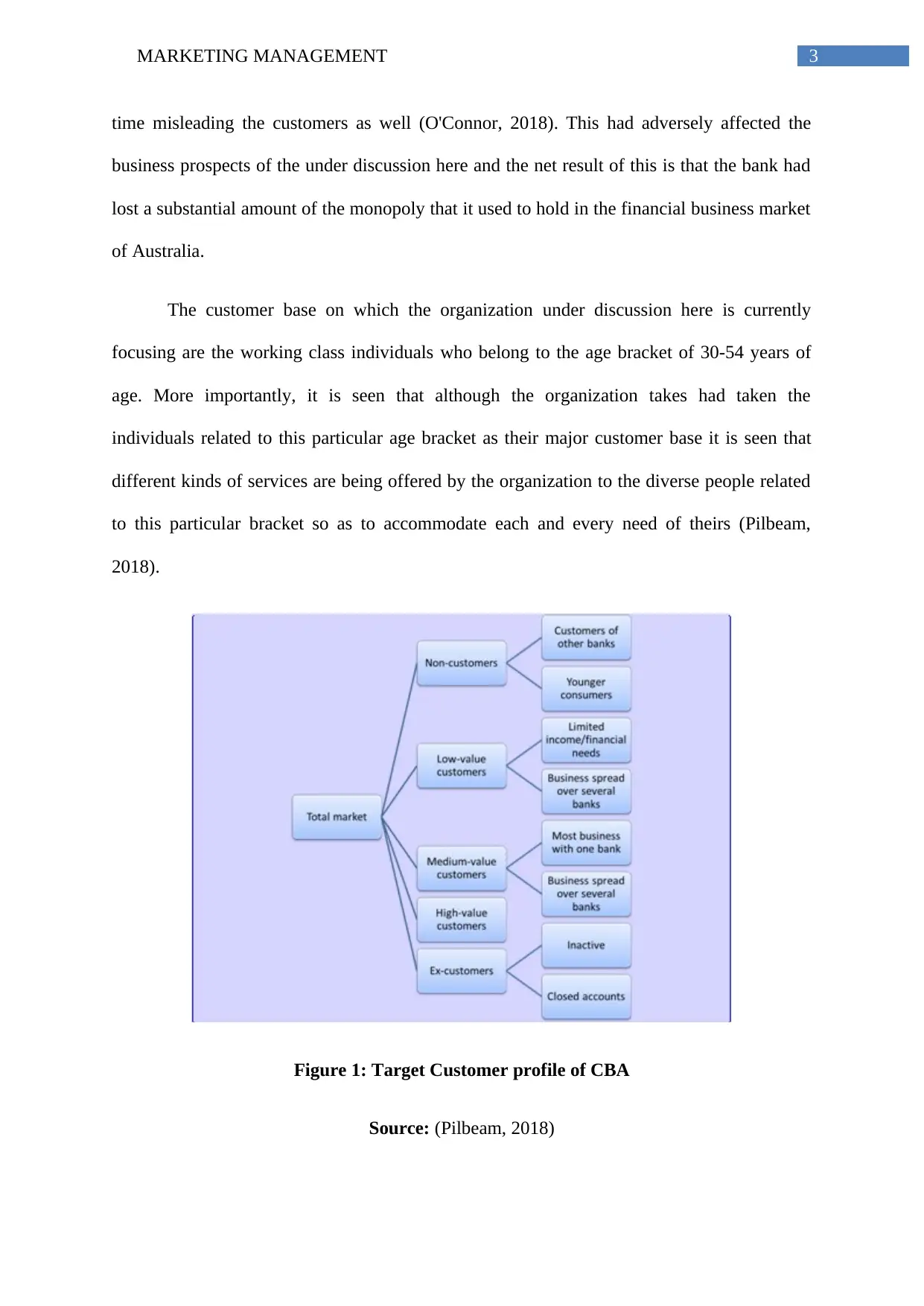

The customer base on which the organization under discussion here is currently

focusing are the working class individuals who belong to the age bracket of 30-54 years of

age. More importantly, it is seen that although the organization takes had taken the

individuals related to this particular age bracket as their major customer base it is seen that

different kinds of services are being offered by the organization to the diverse people related

to this particular bracket so as to accommodate each and every need of theirs (Pilbeam,

2018).

Figure 1: Target Customer profile of CBA

Source: (Pilbeam, 2018)

time misleading the customers as well (O'Connor, 2018). This had adversely affected the

business prospects of the under discussion here and the net result of this is that the bank had

lost a substantial amount of the monopoly that it used to hold in the financial business market

of Australia.

The customer base on which the organization under discussion here is currently

focusing are the working class individuals who belong to the age bracket of 30-54 years of

age. More importantly, it is seen that although the organization takes had taken the

individuals related to this particular age bracket as their major customer base it is seen that

different kinds of services are being offered by the organization to the diverse people related

to this particular bracket so as to accommodate each and every need of theirs (Pilbeam,

2018).

Figure 1: Target Customer profile of CBA

Source: (Pilbeam, 2018)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MARKETING MANAGEMENT

Abdeen, Rajah and Gaur (2016) are of the viewpoint that one of the most important

aspects of the segmentation process used by the organization is its extensive usage of the

innovative strategy of usage-based segmentation. As opined by Pearson (2016), this kind of

segmentation focuses on the behavior of the customers and thereby helps the organizations to

design their services or products in likewise manner. More importantly, it is seen that the

organization focuses mainly on the customers related to the city areas like Melbourne, Perth,

Adelaide and others so as to derive the maximum amount of financial rewards. In addition to

these, it is seen that the organization in the recent times is trying to enhance their existing

customer base and thereby is trying to offer the kind of financial services which would be in

synchronicity with the demands of the younger people as well as their financial needs (Yusof

et al., 2015). More importantly, it is seen that the bank utilizes the social factors like family

status, role of the family members and other factors for targeting the right kind of customers.

In addition to these, the individual factors like age, education and profession also play a key

role in the process of targeting and thus it is seen that the white-collar employees in the age

bracket of 30-59 years of age are being targeted by the bank. According to Fatma, Rahman

and Khan (2015), one of the major reasons for the extensive success gained by the financial

organization under discussion here can be attributed to the effective usage of the

segmentation, targeting and positioning strategies and also to the fact that the organization

takes into effective consideration the needs or the demands of the customers.

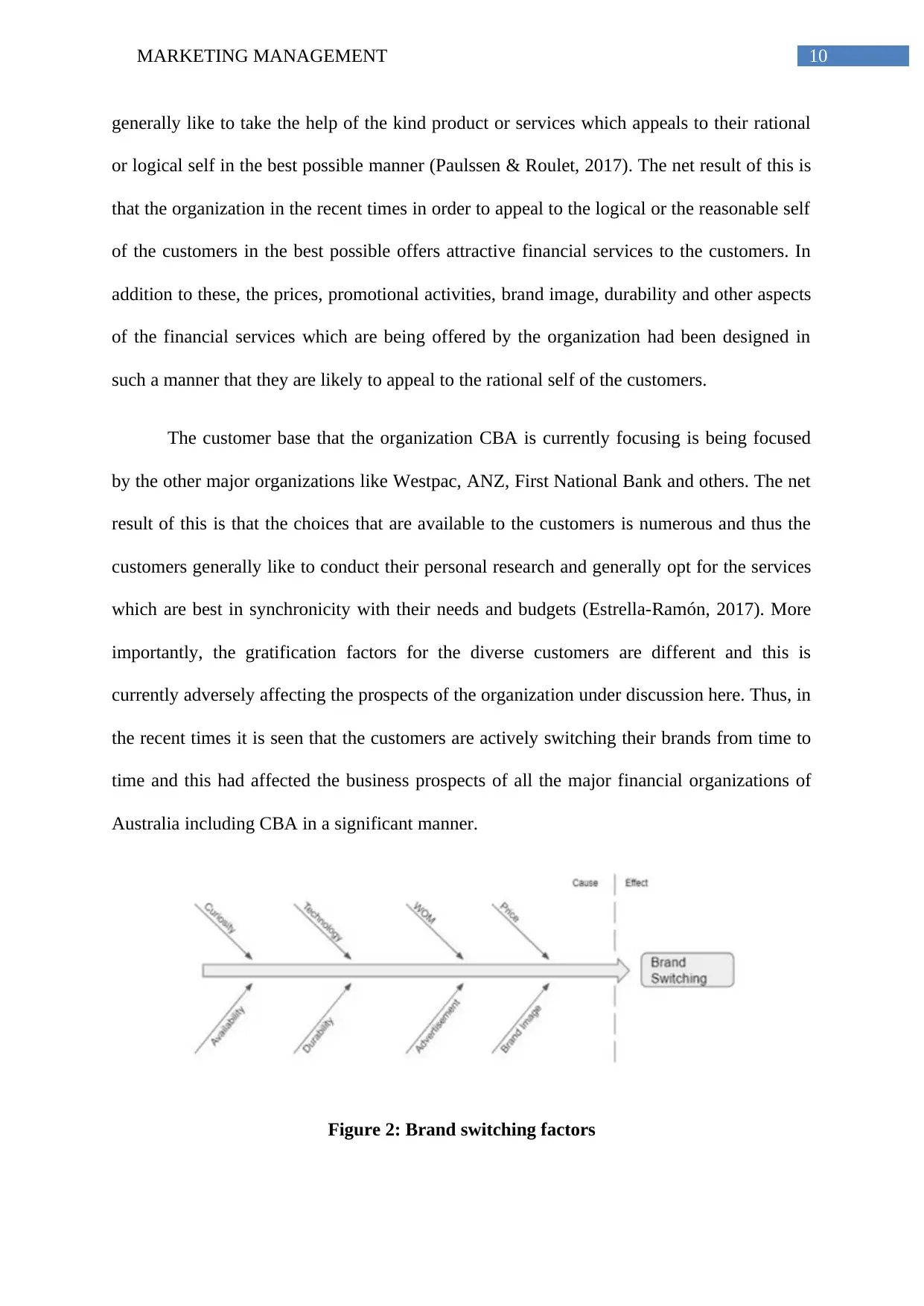

The external factors of the Australian business market act as an opportunity for the

organization, which it can utilize to attain a higher level of financial growth. However, the

fierce competition within the Australian financial sector means that the customers switch

their brands or services on a regular basis and this had considerably reduced the loyalty of the

customers towards the organization in the present times. This in turn is adversely affecting

the financial prospects of the organization under discussion here and the net result of this

Abdeen, Rajah and Gaur (2016) are of the viewpoint that one of the most important

aspects of the segmentation process used by the organization is its extensive usage of the

innovative strategy of usage-based segmentation. As opined by Pearson (2016), this kind of

segmentation focuses on the behavior of the customers and thereby helps the organizations to

design their services or products in likewise manner. More importantly, it is seen that the

organization focuses mainly on the customers related to the city areas like Melbourne, Perth,

Adelaide and others so as to derive the maximum amount of financial rewards. In addition to

these, it is seen that the organization in the recent times is trying to enhance their existing

customer base and thereby is trying to offer the kind of financial services which would be in

synchronicity with the demands of the younger people as well as their financial needs (Yusof

et al., 2015). More importantly, it is seen that the bank utilizes the social factors like family

status, role of the family members and other factors for targeting the right kind of customers.

In addition to these, the individual factors like age, education and profession also play a key

role in the process of targeting and thus it is seen that the white-collar employees in the age

bracket of 30-59 years of age are being targeted by the bank. According to Fatma, Rahman

and Khan (2015), one of the major reasons for the extensive success gained by the financial

organization under discussion here can be attributed to the effective usage of the

segmentation, targeting and positioning strategies and also to the fact that the organization

takes into effective consideration the needs or the demands of the customers.

The external factors of the Australian business market act as an opportunity for the

organization, which it can utilize to attain a higher level of financial growth. However, the

fierce competition within the Australian financial sector means that the customers switch

their brands or services on a regular basis and this had considerably reduced the loyalty of the

customers towards the organization in the present times. This in turn is adversely affecting

the financial prospects of the organization under discussion here and the net result of this

5MARKETING MANAGEMENT

frequent switch in brands by the customers is the fact that none of the organizations are being

able to profit in a significant manner from this (Amin et al., 2017). More importantly, in order

to mitigate the adverse effect of these aspects the organization in the recent times is taking the

help of aggressive marketing strategies and also using various kinds of advertisements to

enhance its customer base. In addition to these, various kinds of discounted services are being

offered by the bank in the present times to attract new customers so as to enhance the amount

of profit or revenue earned by the organization.

Results from Situational Analysis

The situational analysis of the organization CBA which was conducted in the earlier

clearly reveals that most of the external as well as the internal factors of the external business

environment of Australia are congenial for the business operations of the organization under

discussion here. For example, the stable political environment of the nation acts as an

opportunity for the organization which it can utilize to attain a higher level of financial

growth (Küster, Vila & Canales, 2016). Furthermore, booming economy of the nation ensures

the fact that the people of the nation had to right amount of capital to opt for the financial

services offered by the organization (Berbegal-Mirabent, Mas-Machuca & Marimon, 2016).

In addition to these, the people of the nation like to insure things and also like to take capital

on interest or use credit cards and similar services offered by the banks and this turn ensures

the fact that the fact that the financial services offered by the bank are in demand with the

people (Armour et al., 2016).

The technological advancements of the nation also ensures the fact that the

organization is being to use these advancements to offer online payment options to the people

and also to manage the data or the information of these transactions or the financial details of

the customers in an adequate manner (Noori, 2015). Moreover, the lenient corporate laws of

frequent switch in brands by the customers is the fact that none of the organizations are being

able to profit in a significant manner from this (Amin et al., 2017). More importantly, in order

to mitigate the adverse effect of these aspects the organization in the recent times is taking the

help of aggressive marketing strategies and also using various kinds of advertisements to

enhance its customer base. In addition to these, various kinds of discounted services are being

offered by the bank in the present times to attract new customers so as to enhance the amount

of profit or revenue earned by the organization.

Results from Situational Analysis

The situational analysis of the organization CBA which was conducted in the earlier

clearly reveals that most of the external as well as the internal factors of the external business

environment of Australia are congenial for the business operations of the organization under

discussion here. For example, the stable political environment of the nation acts as an

opportunity for the organization which it can utilize to attain a higher level of financial

growth (Küster, Vila & Canales, 2016). Furthermore, booming economy of the nation ensures

the fact that the people of the nation had to right amount of capital to opt for the financial

services offered by the organization (Berbegal-Mirabent, Mas-Machuca & Marimon, 2016).

In addition to these, the people of the nation like to insure things and also like to take capital

on interest or use credit cards and similar services offered by the banks and this turn ensures

the fact that the fact that the financial services offered by the bank are in demand with the

people (Armour et al., 2016).

The technological advancements of the nation also ensures the fact that the

organization is being to use these advancements to offer online payment options to the people

and also to manage the data or the information of these transactions or the financial details of

the customers in an adequate manner (Noori, 2015). Moreover, the lenient corporate laws of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MARKETING MANAGEMENT

the nation also ensure the fact that the bank is being able to conduct its business activities in

an effective manner and also in compliance with the stipulations or the legislations of the

national government (Alshurideh, 2016). Lastly, the organization ardently follows the

different environment legislations or the stipulations given by the national government so as

to contribute in a significant manner towards the cause of the environment.

Yusof et al. (2015) have articulated the viewpoint that the primary purpose of the

different marketing strategies which the organizations use is to effective market as well as

promote the products or services offered by them in an effective manner. As opined by Wali,

Wright and Uduma (2015), effective marketing strategies not only helps the organizations to

convey adequate information regarding the products or services offered by them to the

customers but at the same time help them to grab new customers as well. In this regard, it

needs to be said that the organization CBA takes the help of digital marketing strategies like

SEO, content marketing, e-newsletters and others for the purpose of marketing (Amin et al.,

2017). Furthermore, taking the help of these strategies the organization sends regular

promotional email, e-newsletters and others to the customers to keep them updated regarding

the financial services offered by them (Tung & Carlson, 2015). More importantly, through

the effective usage of the processes of SEO and content marketing the organization had been

able to create an effective online presence of the services offered by them to the customers.

CBA in addition to the digital marketing strategies also takes the help of the strategy

of cost leadership so as to offer the best quality financial services to the customers and that

too at a cost which is comparatively lower than the ones offered by the other financial

organizations of Australia like Westpac, ANZ, First National Bank and others (Amin et al.,

2017). In this regard, it needs to be said that the interest rate which is being charged by the

organization for the various private or personal loans that they offer to the customers is only

3% which is way lower than the ones charged by the other financial organizations of

the nation also ensure the fact that the bank is being able to conduct its business activities in

an effective manner and also in compliance with the stipulations or the legislations of the

national government (Alshurideh, 2016). Lastly, the organization ardently follows the

different environment legislations or the stipulations given by the national government so as

to contribute in a significant manner towards the cause of the environment.

Yusof et al. (2015) have articulated the viewpoint that the primary purpose of the

different marketing strategies which the organizations use is to effective market as well as

promote the products or services offered by them in an effective manner. As opined by Wali,

Wright and Uduma (2015), effective marketing strategies not only helps the organizations to

convey adequate information regarding the products or services offered by them to the

customers but at the same time help them to grab new customers as well. In this regard, it

needs to be said that the organization CBA takes the help of digital marketing strategies like

SEO, content marketing, e-newsletters and others for the purpose of marketing (Amin et al.,

2017). Furthermore, taking the help of these strategies the organization sends regular

promotional email, e-newsletters and others to the customers to keep them updated regarding

the financial services offered by them (Tung & Carlson, 2015). More importantly, through

the effective usage of the processes of SEO and content marketing the organization had been

able to create an effective online presence of the services offered by them to the customers.

CBA in addition to the digital marketing strategies also takes the help of the strategy

of cost leadership so as to offer the best quality financial services to the customers and that

too at a cost which is comparatively lower than the ones offered by the other financial

organizations of Australia like Westpac, ANZ, First National Bank and others (Amin et al.,

2017). In this regard, it needs to be said that the interest rate which is being charged by the

organization for the various private or personal loans that they offer to the customers is only

3% which is way lower than the ones charged by the other financial organizations of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MARKETING MANAGEMENT

Australia (Commbank.com.au, 2019). More importantly, the organization also actively takes

the help of the marketing strategy of product diversification so as to offer a wide range of

financial services to the customers. The net result of this is that the organization under

discussion here in the present times had broadened the genre of services offered by it to the

customers and offers not only personal loans, insurances, pension plans and others but at the

same time different kinds of retail or corporate loans as well (Ramanathan, Subramanian &

Parrott, 2017). Thus, it can be said that the extensive success gained by the organization

under discussion here can be attributed to the effective usage of the mentioned marketing as

well as promotional strategies.

Product Personal loans, insurances, pension plans and others

Corporate or retail loans

Credit cards, debit or ATM cards and others

Price Uses cost leadership strategy

Charges only 3% interest from the customers on personal or private

loans which is way lower than the ones charged by the other financial

organizations (Commbank.com.au, 2019)

Place The organization is headquartered in Sydney and offers financial

services to the customers from all over the nation

In the recent times the organization is following the path of

internationalization and had expanded in different nations like China,

USA, UK and others (Commbank.com.au, 2019)

Australia (Commbank.com.au, 2019). More importantly, the organization also actively takes

the help of the marketing strategy of product diversification so as to offer a wide range of

financial services to the customers. The net result of this is that the organization under

discussion here in the present times had broadened the genre of services offered by it to the

customers and offers not only personal loans, insurances, pension plans and others but at the

same time different kinds of retail or corporate loans as well (Ramanathan, Subramanian &

Parrott, 2017). Thus, it can be said that the extensive success gained by the organization

under discussion here can be attributed to the effective usage of the mentioned marketing as

well as promotional strategies.

Product Personal loans, insurances, pension plans and others

Corporate or retail loans

Credit cards, debit or ATM cards and others

Price Uses cost leadership strategy

Charges only 3% interest from the customers on personal or private

loans which is way lower than the ones charged by the other financial

organizations (Commbank.com.au, 2019)

Place The organization is headquartered in Sydney and offers financial

services to the customers from all over the nation

In the recent times the organization is following the path of

internationalization and had expanded in different nations like China,

USA, UK and others (Commbank.com.au, 2019)

8MARKETING MANAGEMENT

Takes the help of the strategy of time-based competition to offer fast

services to the customers and also to enhance the efficiency of its supply

chain and thereby to improve the quality of services (Pappas, 2016)

Promotio

n

Active usage of digital and traditional forms of promotional methods

Traditional promotional methods used by the organization includes

advertizing in newspapers, television, radios and others

Digital promotional methods used by the organization includes

advertising over social media platforms, content marketing, SEO and

others

The findings of the Royal Banking Commission (2017) by revealing the unethical as

well as misguiding practices used by the organization had adversely affected the brand image

as well as the profitability of the organization under discussion here (McIlroy, 2018). For

example, the commission clearly revealed the fact that the organization in order to earn more

profit was not only misleading the customers but at the same time extracting more money

from them than the amount they needed to pay (O'Connor, 2018). The net result of this is that

in the recent times many of the loyal customers have stopped opting for the services offered

by the bank and have switched over to its competitors. In addition to this, post the

Commission the organization had failed to attract new customers within the fold of the

organization and this is adversely affecting its profitability (Amin et al., 2017). In this regard,

it needs to be said that the organization was asked to pay more than $1.6 billion to the

national government as well as the customers as compensation for the fraudulent practices

used by it (Pilbeam, 2018). More importantly, the analysis of the results of the survey (given

Takes the help of the strategy of time-based competition to offer fast

services to the customers and also to enhance the efficiency of its supply

chain and thereby to improve the quality of services (Pappas, 2016)

Promotio

n

Active usage of digital and traditional forms of promotional methods

Traditional promotional methods used by the organization includes

advertizing in newspapers, television, radios and others

Digital promotional methods used by the organization includes

advertising over social media platforms, content marketing, SEO and

others

The findings of the Royal Banking Commission (2017) by revealing the unethical as

well as misguiding practices used by the organization had adversely affected the brand image

as well as the profitability of the organization under discussion here (McIlroy, 2018). For

example, the commission clearly revealed the fact that the organization in order to earn more

profit was not only misleading the customers but at the same time extracting more money

from them than the amount they needed to pay (O'Connor, 2018). The net result of this is that

in the recent times many of the loyal customers have stopped opting for the services offered

by the bank and have switched over to its competitors. In addition to this, post the

Commission the organization had failed to attract new customers within the fold of the

organization and this is adversely affecting its profitability (Amin et al., 2017). In this regard,

it needs to be said that the organization was asked to pay more than $1.6 billion to the

national government as well as the customers as compensation for the fraudulent practices

used by it (Pilbeam, 2018). More importantly, the analysis of the results of the survey (given

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MARKETING MANAGEMENT

in the excel file) clearly reveals that the majority of the customers of CBA post the

revelations of this commission are opting for the services offered by the other banks and thus

the loyalty of the customers towards the bank is at an all time low. In addition to this, the

results of the survey clearly that a significant number of customers had switched over to the

other banks because of the fraudulent practices used by it. This had led many customers to

switch brands and move over to the other brands in the financial sector of Australia. The

organization in order to overcome the adverse effects of these issues is currently taking the

help of various kinds of corporate social responsibility (CSR) so as to improve its brand

image within the financial business market. In addition to this, the organization is also using

different kinds of digital marketing strategies like SEO, content marketing and others to

advertise in an effective manner the positive aspects of the services offered by it.

Furthermore, the organization at the same time is trying to bring in new customers and

thereby increase the sale of the services offered by it to the customers.

Individual factors and their influence on consumer decision-making

Hjort et al. (2016) have articulated the viewpoint that because of the fierce

competition which exists within the framework of the contemporary business world the

behavior of the customers had changed in a significant manner. More importantly, in the

present times it is seen that there are various factors which affect the buying behavior of the

customers like price, product attributes, brand image of the concerned organization and others

(Kaihatu & Spence, 2016). Furthermore, the prominence that the concept of customer buying

behavior holds within the framework of the contemporary business world becomes evident in

the emergence of the different kinds of theories or frameworks that are being used by the

organizations. In this regard, it needs to be said that taking the help of the “theory of reasoned

action” the organization CBA believes the fact that the customers are rational creatures and

in the excel file) clearly reveals that the majority of the customers of CBA post the

revelations of this commission are opting for the services offered by the other banks and thus

the loyalty of the customers towards the bank is at an all time low. In addition to this, the

results of the survey clearly that a significant number of customers had switched over to the

other banks because of the fraudulent practices used by it. This had led many customers to

switch brands and move over to the other brands in the financial sector of Australia. The

organization in order to overcome the adverse effects of these issues is currently taking the

help of various kinds of corporate social responsibility (CSR) so as to improve its brand

image within the financial business market. In addition to this, the organization is also using

different kinds of digital marketing strategies like SEO, content marketing and others to

advertise in an effective manner the positive aspects of the services offered by it.

Furthermore, the organization at the same time is trying to bring in new customers and

thereby increase the sale of the services offered by it to the customers.

Individual factors and their influence on consumer decision-making

Hjort et al. (2016) have articulated the viewpoint that because of the fierce

competition which exists within the framework of the contemporary business world the

behavior of the customers had changed in a significant manner. More importantly, in the

present times it is seen that there are various factors which affect the buying behavior of the

customers like price, product attributes, brand image of the concerned organization and others

(Kaihatu & Spence, 2016). Furthermore, the prominence that the concept of customer buying

behavior holds within the framework of the contemporary business world becomes evident in

the emergence of the different kinds of theories or frameworks that are being used by the

organizations. In this regard, it needs to be said that taking the help of the “theory of reasoned

action” the organization CBA believes the fact that the customers are rational creatures and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MARKETING MANAGEMENT

generally like to take the help of the kind product or services which appeals to their rational

or logical self in the best possible manner (Paulssen & Roulet, 2017). The net result of this is

that the organization in the recent times in order to appeal to the logical or the reasonable self

of the customers in the best possible offers attractive financial services to the customers. In

addition to these, the prices, promotional activities, brand image, durability and other aspects

of the financial services which are being offered by the organization had been designed in

such a manner that they are likely to appeal to the rational self of the customers.

The customer base that the organization CBA is currently focusing is being focused

by the other major organizations like Westpac, ANZ, First National Bank and others. The net

result of this is that the choices that are available to the customers is numerous and thus the

customers generally like to conduct their personal research and generally opt for the services

which are best in synchronicity with their needs and budgets (Estrella-Ramón, 2017). More

importantly, the gratification factors for the diverse customers are different and this is

currently adversely affecting the prospects of the organization under discussion here. Thus, in

the recent times it is seen that the customers are actively switching their brands from time to

time and this had affected the business prospects of all the major financial organizations of

Australia including CBA in a significant manner.

Figure 2: Brand switching factors

generally like to take the help of the kind product or services which appeals to their rational

or logical self in the best possible manner (Paulssen & Roulet, 2017). The net result of this is

that the organization in the recent times in order to appeal to the logical or the reasonable self

of the customers in the best possible offers attractive financial services to the customers. In

addition to these, the prices, promotional activities, brand image, durability and other aspects

of the financial services which are being offered by the organization had been designed in

such a manner that they are likely to appeal to the rational self of the customers.

The customer base that the organization CBA is currently focusing is being focused

by the other major organizations like Westpac, ANZ, First National Bank and others. The net

result of this is that the choices that are available to the customers is numerous and thus the

customers generally like to conduct their personal research and generally opt for the services

which are best in synchronicity with their needs and budgets (Estrella-Ramón, 2017). More

importantly, the gratification factors for the diverse customers are different and this is

currently adversely affecting the prospects of the organization under discussion here. Thus, in

the recent times it is seen that the customers are actively switching their brands from time to

time and this had affected the business prospects of all the major financial organizations of

Australia including CBA in a significant manner.

Figure 2: Brand switching factors

11MARKETING MANAGEMENT

Source: (Schaper, 2016)

An competitor analysis of CBA with the other organizations of Australia in terms of

the services offered by it and also the buying behavior of the customers is being represented

by the below given table-

CBA Westpac ANZ First National

Bank

Value

Proposition

High quality

financial

services, low

interest rates,

diversity of

financial

services and

others

Quality services,

plethora of

services,

reliability

Reliability, low

cost services,

high quality

services

Diversity of

services,

reliability

Brand Switch

by the

customers

High High High High

Interests Rate 3% 4.1% 3.5% 4.9%

Revenue (2017) A$26.005

billion

A$ 21.642

billion

A$ 21.071

billion

A$ 21.001

billion

Online

Presence

Yes Yes Yes Yes

Brand Image

pre-Royal

Positive Positive Positive Positive

Source: (Schaper, 2016)

An competitor analysis of CBA with the other organizations of Australia in terms of

the services offered by it and also the buying behavior of the customers is being represented

by the below given table-

CBA Westpac ANZ First National

Bank

Value

Proposition

High quality

financial

services, low

interest rates,

diversity of

financial

services and

others

Quality services,

plethora of

services,

reliability

Reliability, low

cost services,

high quality

services

Diversity of

services,

reliability

Brand Switch

by the

customers

High High High High

Interests Rate 3% 4.1% 3.5% 4.9%

Revenue (2017) A$26.005

billion

A$ 21.642

billion

A$ 21.071

billion

A$ 21.001

billion

Online

Presence

Yes Yes Yes Yes

Brand Image

pre-Royal

Positive Positive Positive Positive

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.