Company Accounting Report: Financial Statement Analysis of CBA 2017

VerifiedAdded on 2023/06/06

|9

|1587

|349

Report

AI Summary

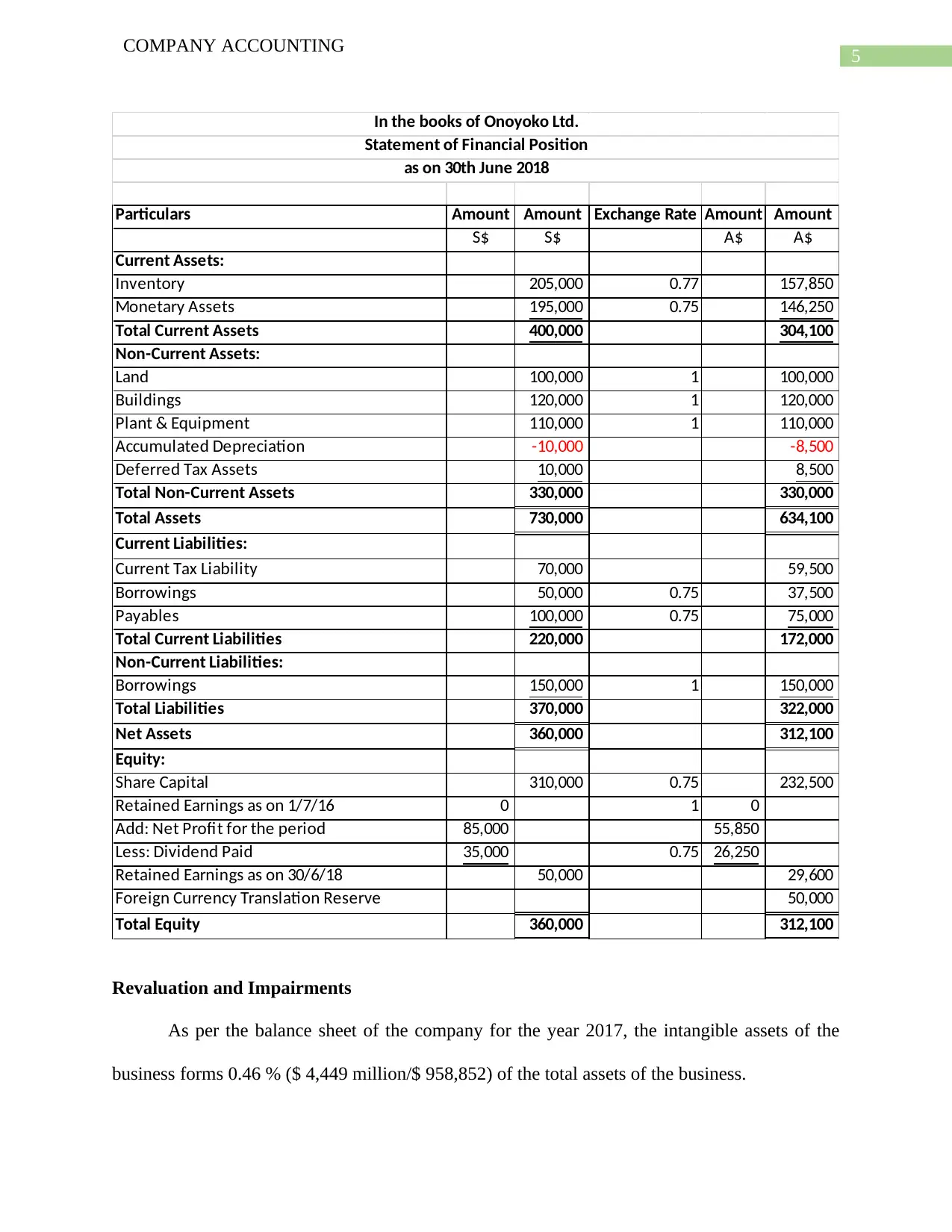

This report analyzes the financial statements of the Commonwealth Bank of Australia (CBA) for the year 2017, focusing on key accounting treatments and disclosures. It examines income tax expenses, deferred tax assets and liabilities, and the translation of foreign operations, including foreign currency risks and hedging strategies. Furthermore, the report discusses revaluation and impairment of assets, including intangible assets and properties, and analyzes the application of lease accounting standards, specifically IASB 17 and the upcoming AASB 16. The analysis includes calculations related to foreign currency trade and provides journal entries for asset revaluation. The report provides a comprehensive overview of significant financial reporting elements within CBA's 2017 annual report.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.