Company Accounting Assignment: ACCT20073 Term 1 2019

VerifiedAdded on 2023/03/23

|6

|741

|31

Homework Assignment

AI Summary

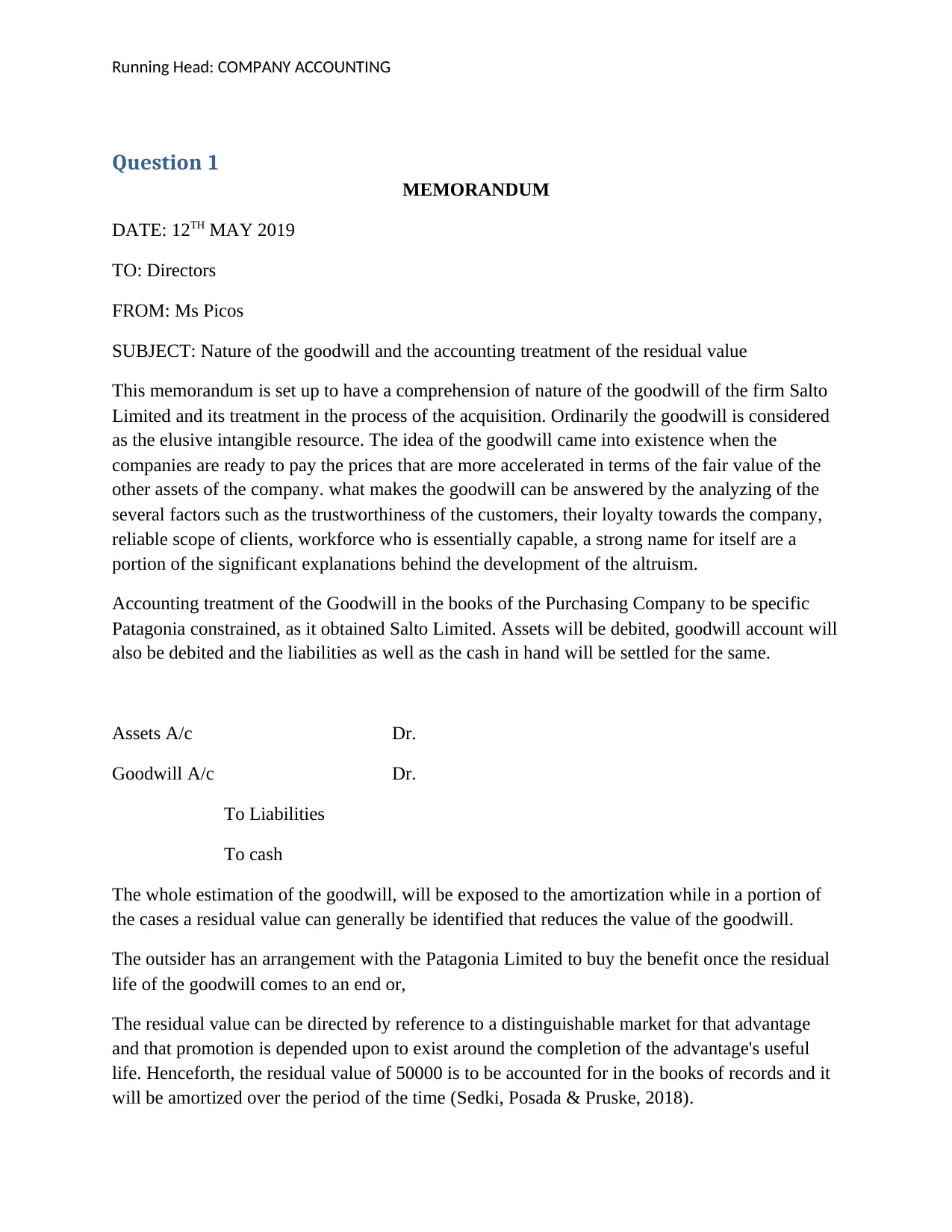

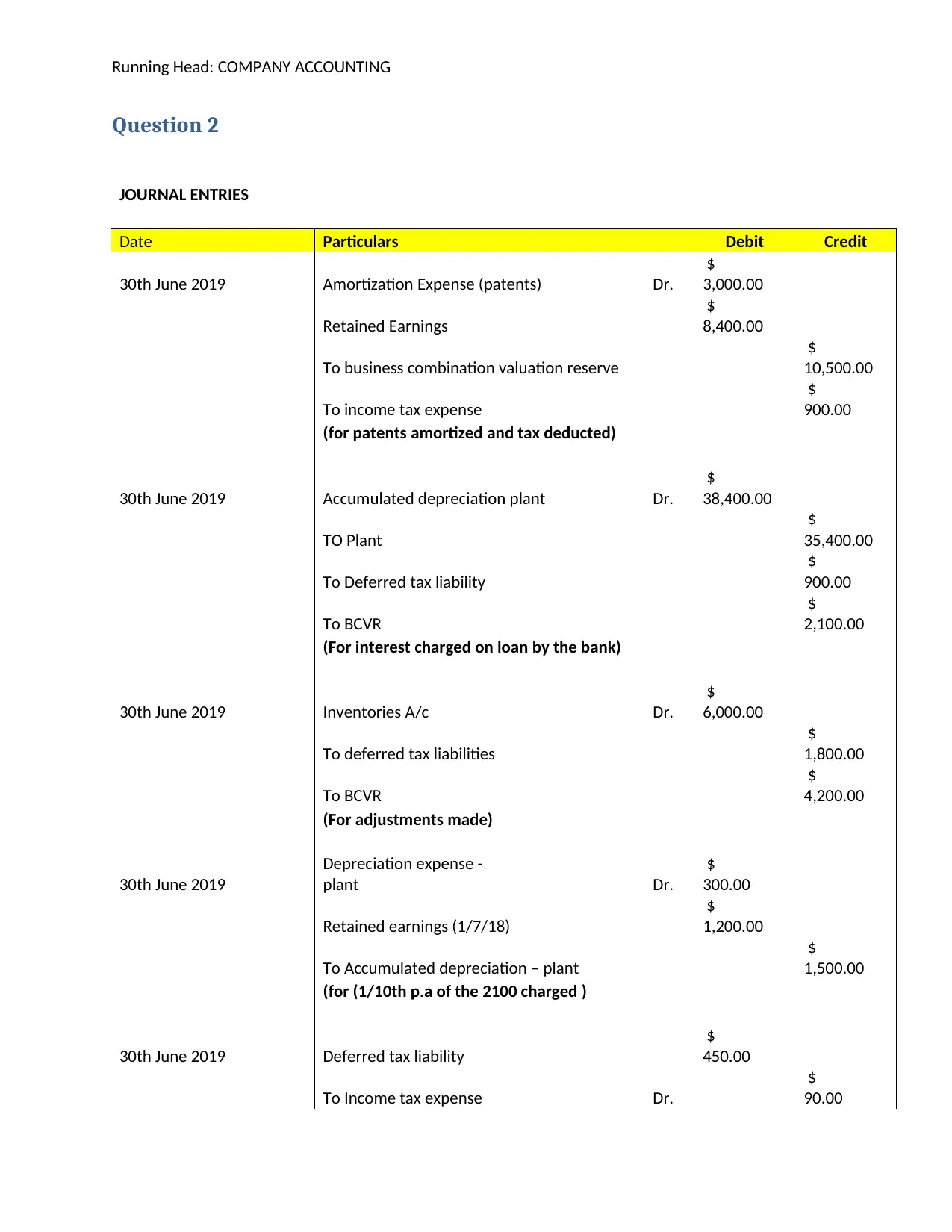

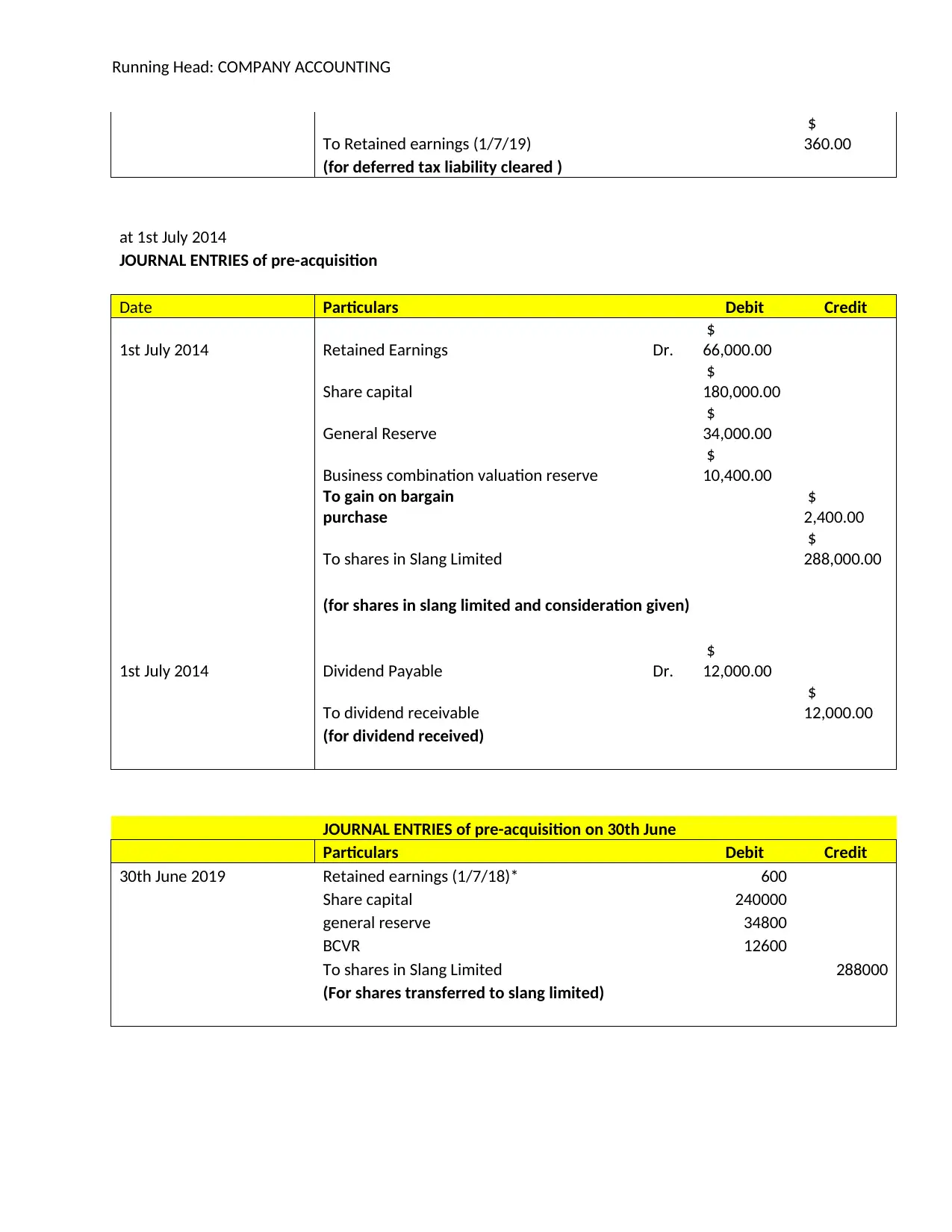

This assignment solution addresses company accounting principles, specifically focusing on the nature and accounting treatment of goodwill. The memorandum analyzes goodwill as an intangible asset, discussing factors contributing to its existence and the accounting procedures involved in acquisitions, including debiting assets and goodwill while crediting liabilities and cash. The solution includes journal entries for various accounting adjustments, such as amortization expenses, depreciation, and deferred tax liabilities, related to patents, plants, and inventories. Furthermore, it presents journal entries for pre-acquisition transactions, including share transfers and dividend payments, providing a comprehensive overview of accounting practices in business combinations and financial reporting. The assignment is a response to an assessment task for the ACCT20073 course.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.