Detailed Solutions for Company Accounting 2019 Assignment Questions

VerifiedAdded on 2023/03/21

|24

|4199

|32

Homework Assignment

AI Summary

This document presents a comprehensive solution to a company accounting assignment. It addresses multiple questions, including detailed journal entries, computations for deferred tax assets and liabilities, and the application of accounting principles to business combinations. The solution includes calculations for taxable income, deferred tax, and the impact of various transactions on financial statements. Furthermore, it provides an in-depth analysis of business combinations, outlining the necessary steps for recording assets, liabilities, and goodwill. Additional questions delve into consolidated financial statements, requiring journal entries to eliminate intercompany transactions and unrealized profits. The assignment also considers the impact of depreciation, impairment, and dividends on the financial statements. The document includes thorough explanations, making it a valuable resource for students studying company accounting.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company Accounting 2019

Table of Contents

Answer to Question No.1............................................................................................................................3

Answer to Question 1 (1).........................................................................................................................3

Answer to Question 1 (2).........................................................................................................................3

Answer to Question 1 (3).........................................................................................................................4

Answer to Question 1 (4).........................................................................................................................4

Answer to Question No.2 (Part A) (1)..........................................................................................................5

Answer to Question No.2 (Part A) (2)..........................................................................................................6

Answer to Question No.2 (Part B)...............................................................................................................7

Business Combination.............................................................................................................................7

Answer to Question No.3 (1).......................................................................................................................8

Answer to Question No.3 (2) & (3)..............................................................................................................9

Answer to Question No.3 (4).....................................................................................................................13

Answer to Question No.3 (5) (a)................................................................................................................14

Answer to Question No.3 (5) (b)................................................................................................................15

Answer to Question No.3 (5) (c)................................................................................................................16

Answer to Question No.4 (1).....................................................................................................................17

Answer to Question No.4 (2).....................................................................................................................18

Answer to Question No.4 (3).....................................................................................................................18

Answer to Question No.4 (4).....................................................................................................................19

Answer to Question No.4 (5).....................................................................................................................20

Bibliography...............................................................................................................................................23

Name of the Student Page 2

Table of Contents

Answer to Question No.1............................................................................................................................3

Answer to Question 1 (1).........................................................................................................................3

Answer to Question 1 (2).........................................................................................................................3

Answer to Question 1 (3).........................................................................................................................4

Answer to Question 1 (4).........................................................................................................................4

Answer to Question No.2 (Part A) (1)..........................................................................................................5

Answer to Question No.2 (Part A) (2)..........................................................................................................6

Answer to Question No.2 (Part B)...............................................................................................................7

Business Combination.............................................................................................................................7

Answer to Question No.3 (1).......................................................................................................................8

Answer to Question No.3 (2) & (3)..............................................................................................................9

Answer to Question No.3 (4).....................................................................................................................13

Answer to Question No.3 (5) (a)................................................................................................................14

Answer to Question No.3 (5) (b)................................................................................................................15

Answer to Question No.3 (5) (c)................................................................................................................16

Answer to Question No.4 (1).....................................................................................................................17

Answer to Question No.4 (2).....................................................................................................................18

Answer to Question No.4 (3).....................................................................................................................18

Answer to Question No.4 (4).....................................................................................................................19

Answer to Question No.4 (5).....................................................................................................................20

Bibliography...............................................................................................................................................23

Name of the Student Page 2

Company Accounting 2019

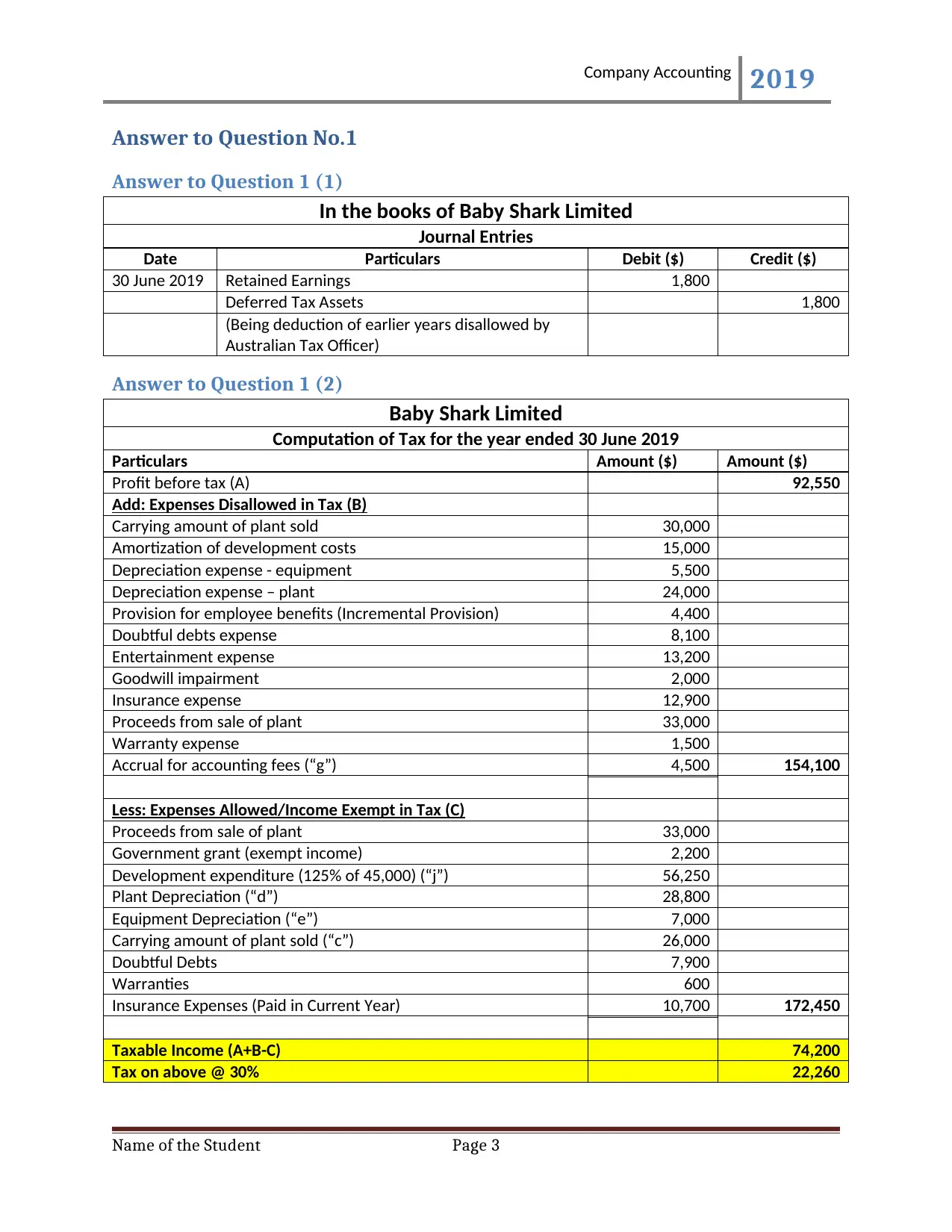

Answer to Question No.1

Answer to Question 1 (1)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Retained Earnings 1,800

Deferred Tax Assets 1,800

(Being deduction of earlier years disallowed by

Australian Tax Officer)

Answer to Question 1 (2)

Baby Shark Limited

Computation of Tax for the year ended 30 June 2019

Particulars Amount ($) Amount ($)

Profit before tax (A) 92,550

Add: Expenses Disallowed in Tax (B)

Carrying amount of plant sold 30,000

Amortization of development costs 15,000

Depreciation expense - equipment 5,500

Depreciation expense – plant 24,000

Provision for employee benefits (Incremental Provision) 4,400

Doubtful debts expense 8,100

Entertainment expense 13,200

Goodwill impairment 2,000

Insurance expense 12,900

Proceeds from sale of plant 33,000

Warranty expense 1,500

Accrual for accounting fees (“g”) 4,500 154,100

Less: Expenses Allowed/Income Exempt in Tax (C)

Proceeds from sale of plant 33,000

Government grant (exempt income) 2,200

Development expenditure (125% of 45,000) (“j”) 56,250

Plant Depreciation (“d”) 28,800

Equipment Depreciation (“e”) 7,000

Carrying amount of plant sold (“c”) 26,000

Doubtful Debts 7,900

Warranties 600

Insurance Expenses (Paid in Current Year) 10,700 172,450

Taxable Income (A+B-C) 74,200

Tax on above @ 30% 22,260

Name of the Student Page 3

Answer to Question No.1

Answer to Question 1 (1)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Retained Earnings 1,800

Deferred Tax Assets 1,800

(Being deduction of earlier years disallowed by

Australian Tax Officer)

Answer to Question 1 (2)

Baby Shark Limited

Computation of Tax for the year ended 30 June 2019

Particulars Amount ($) Amount ($)

Profit before tax (A) 92,550

Add: Expenses Disallowed in Tax (B)

Carrying amount of plant sold 30,000

Amortization of development costs 15,000

Depreciation expense - equipment 5,500

Depreciation expense – plant 24,000

Provision for employee benefits (Incremental Provision) 4,400

Doubtful debts expense 8,100

Entertainment expense 13,200

Goodwill impairment 2,000

Insurance expense 12,900

Proceeds from sale of plant 33,000

Warranty expense 1,500

Accrual for accounting fees (“g”) 4,500 154,100

Less: Expenses Allowed/Income Exempt in Tax (C)

Proceeds from sale of plant 33,000

Government grant (exempt income) 2,200

Development expenditure (125% of 45,000) (“j”) 56,250

Plant Depreciation (“d”) 28,800

Equipment Depreciation (“e”) 7,000

Carrying amount of plant sold (“c”) 26,000

Doubtful Debts 7,900

Warranties 600

Insurance Expenses (Paid in Current Year) 10,700 172,450

Taxable Income (A+B-C) 74,200

Tax on above @ 30% 22,260

Name of the Student Page 3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Company Accounting 2019

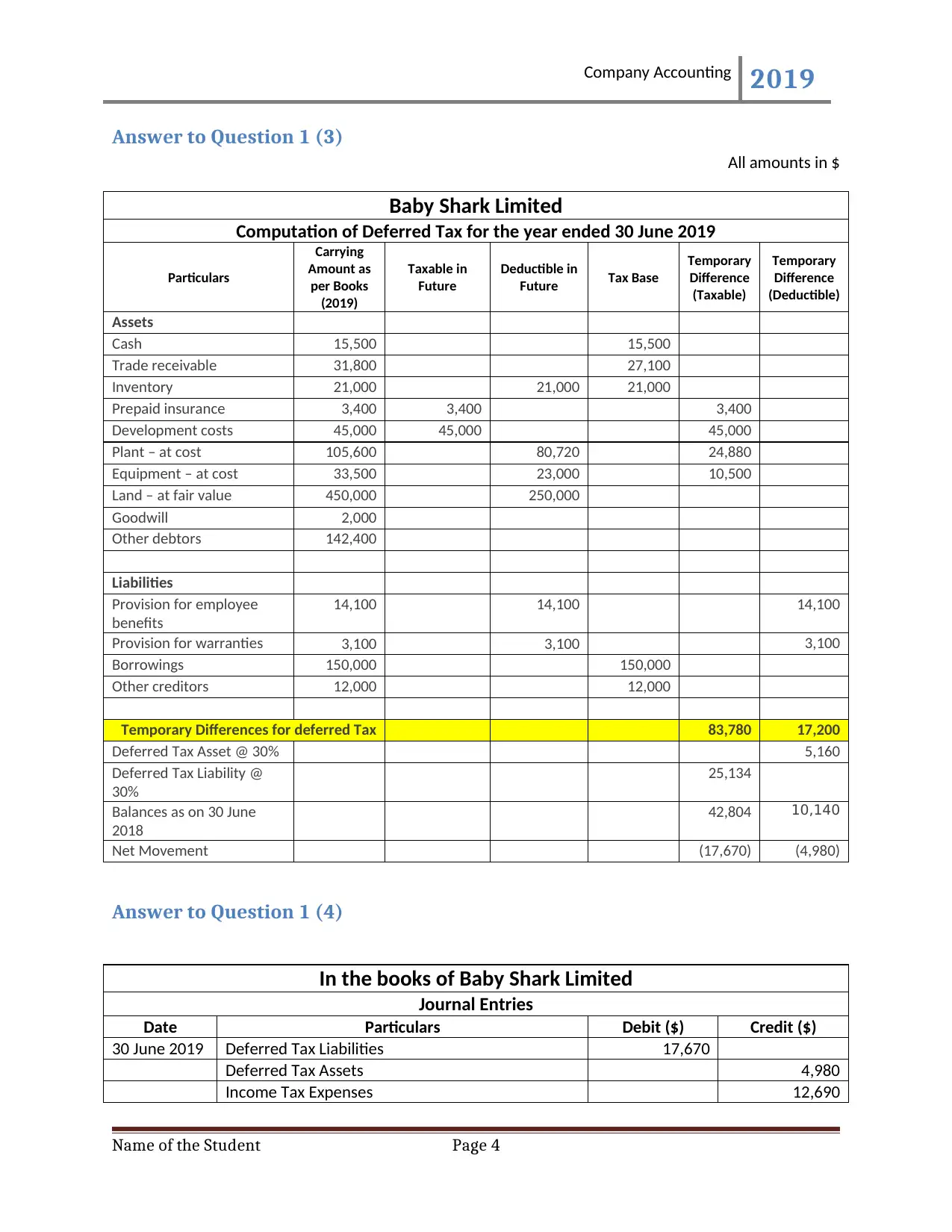

Answer to Question 1 (3)

All amounts in $

Baby Shark Limited

Computation of Deferred Tax for the year ended 30 June 2019

Particulars

Carrying

Amount as

per Books

(2019)

Taxable in

Future

Deductible in

Future Tax Base

Temporary

Difference

(Taxable)

Temporary

Difference

(Deductible)

Assets

Cash 15,500 15,500

Trade receivable 31,800 27,100

Inventory 21,000 21,000 21,000

Prepaid insurance 3,400 3,400 3,400

Development costs 45,000 45,000 45,000

Plant – at cost 105,600 80,720 24,880

Equipment – at cost 33,500 23,000 10,500

Land – at fair value 450,000 250,000

Goodwill 2,000

Other debtors 142,400

Liabilities

Provision for employee

benefits

14,100 14,100 14,100

Provision for warranties 3,100 3,100 3,100

Borrowings 150,000 150,000

Other creditors 12,000 12,000

Temporary Differences for deferred Tax 83,780 17,200

Deferred Tax Asset @ 30% 5,160

Deferred Tax Liability @

30%

25,134

Balances as on 30 June

2018

42,804 10,140

Net Movement (17,670) (4,980)

Answer to Question 1 (4)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Deferred Tax Liabilities 17,670

Deferred Tax Assets 4,980

Income Tax Expenses 12,690

Name of the Student Page 4

Answer to Question 1 (3)

All amounts in $

Baby Shark Limited

Computation of Deferred Tax for the year ended 30 June 2019

Particulars

Carrying

Amount as

per Books

(2019)

Taxable in

Future

Deductible in

Future Tax Base

Temporary

Difference

(Taxable)

Temporary

Difference

(Deductible)

Assets

Cash 15,500 15,500

Trade receivable 31,800 27,100

Inventory 21,000 21,000 21,000

Prepaid insurance 3,400 3,400 3,400

Development costs 45,000 45,000 45,000

Plant – at cost 105,600 80,720 24,880

Equipment – at cost 33,500 23,000 10,500

Land – at fair value 450,000 250,000

Goodwill 2,000

Other debtors 142,400

Liabilities

Provision for employee

benefits

14,100 14,100 14,100

Provision for warranties 3,100 3,100 3,100

Borrowings 150,000 150,000

Other creditors 12,000 12,000

Temporary Differences for deferred Tax 83,780 17,200

Deferred Tax Asset @ 30% 5,160

Deferred Tax Liability @

30%

25,134

Balances as on 30 June

2018

42,804 10,140

Net Movement (17,670) (4,980)

Answer to Question 1 (4)

In the books of Baby Shark Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

30 June 2019 Deferred Tax Liabilities 17,670

Deferred Tax Assets 4,980

Income Tax Expenses 12,690

Name of the Student Page 4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company Accounting 2019

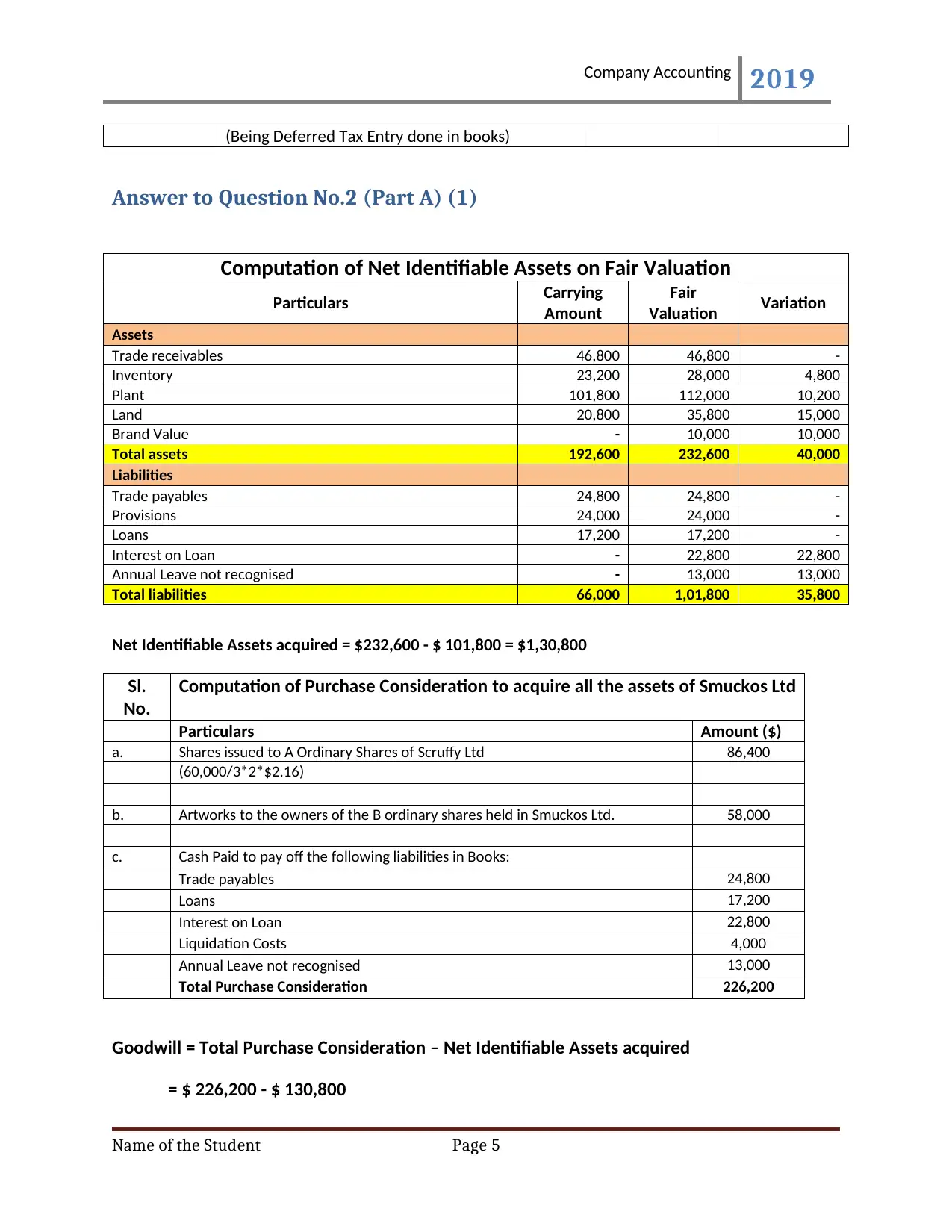

(Being Deferred Tax Entry done in books)

Answer to Question No.2 (Part A) (1)

Computation of Net Identifiable Assets on Fair Valuation

Particulars Carrying

Amount

Fair

Valuation Variation

Assets

Trade receivables 46,800 46,800 -

Inventory 23,200 28,000 4,800

Plant 101,800 112,000 10,200

Land 20,800 35,800 15,000

Brand Value - 10,000 10,000

Total assets 192,600 232,600 40,000

Liabilities

Trade payables 24,800 24,800 -

Provisions 24,000 24,000 -

Loans 17,200 17,200 -

Interest on Loan - 22,800 22,800

Annual Leave not recognised - 13,000 13,000

Total liabilities 66,000 1,01,800 35,800

Net Identifiable Assets acquired = $232,600 - $ 101,800 = $1,30,800

Sl.

No.

Computation of Purchase Consideration to acquire all the assets of Smuckos Ltd

Particulars Amount ($)

a. Shares issued to A Ordinary Shares of Scruffy Ltd 86,400

(60,000/3*2*$2.16)

b. Artworks to the owners of the B ordinary shares held in Smuckos Ltd. 58,000

c. Cash Paid to pay off the following liabilities in Books:

Trade payables 24,800

Loans 17,200

Interest on Loan 22,800

Liquidation Costs 4,000

Annual Leave not recognised 13,000

Total Purchase Consideration 226,200

Goodwill = Total Purchase Consideration – Net Identifiable Assets acquired

= $ 226,200 - $ 130,800

Name of the Student Page 5

(Being Deferred Tax Entry done in books)

Answer to Question No.2 (Part A) (1)

Computation of Net Identifiable Assets on Fair Valuation

Particulars Carrying

Amount

Fair

Valuation Variation

Assets

Trade receivables 46,800 46,800 -

Inventory 23,200 28,000 4,800

Plant 101,800 112,000 10,200

Land 20,800 35,800 15,000

Brand Value - 10,000 10,000

Total assets 192,600 232,600 40,000

Liabilities

Trade payables 24,800 24,800 -

Provisions 24,000 24,000 -

Loans 17,200 17,200 -

Interest on Loan - 22,800 22,800

Annual Leave not recognised - 13,000 13,000

Total liabilities 66,000 1,01,800 35,800

Net Identifiable Assets acquired = $232,600 - $ 101,800 = $1,30,800

Sl.

No.

Computation of Purchase Consideration to acquire all the assets of Smuckos Ltd

Particulars Amount ($)

a. Shares issued to A Ordinary Shares of Scruffy Ltd 86,400

(60,000/3*2*$2.16)

b. Artworks to the owners of the B ordinary shares held in Smuckos Ltd. 58,000

c. Cash Paid to pay off the following liabilities in Books:

Trade payables 24,800

Loans 17,200

Interest on Loan 22,800

Liquidation Costs 4,000

Annual Leave not recognised 13,000

Total Purchase Consideration 226,200

Goodwill = Total Purchase Consideration – Net Identifiable Assets acquired

= $ 226,200 - $ 130,800

Name of the Student Page 5

Company Accounting 2019

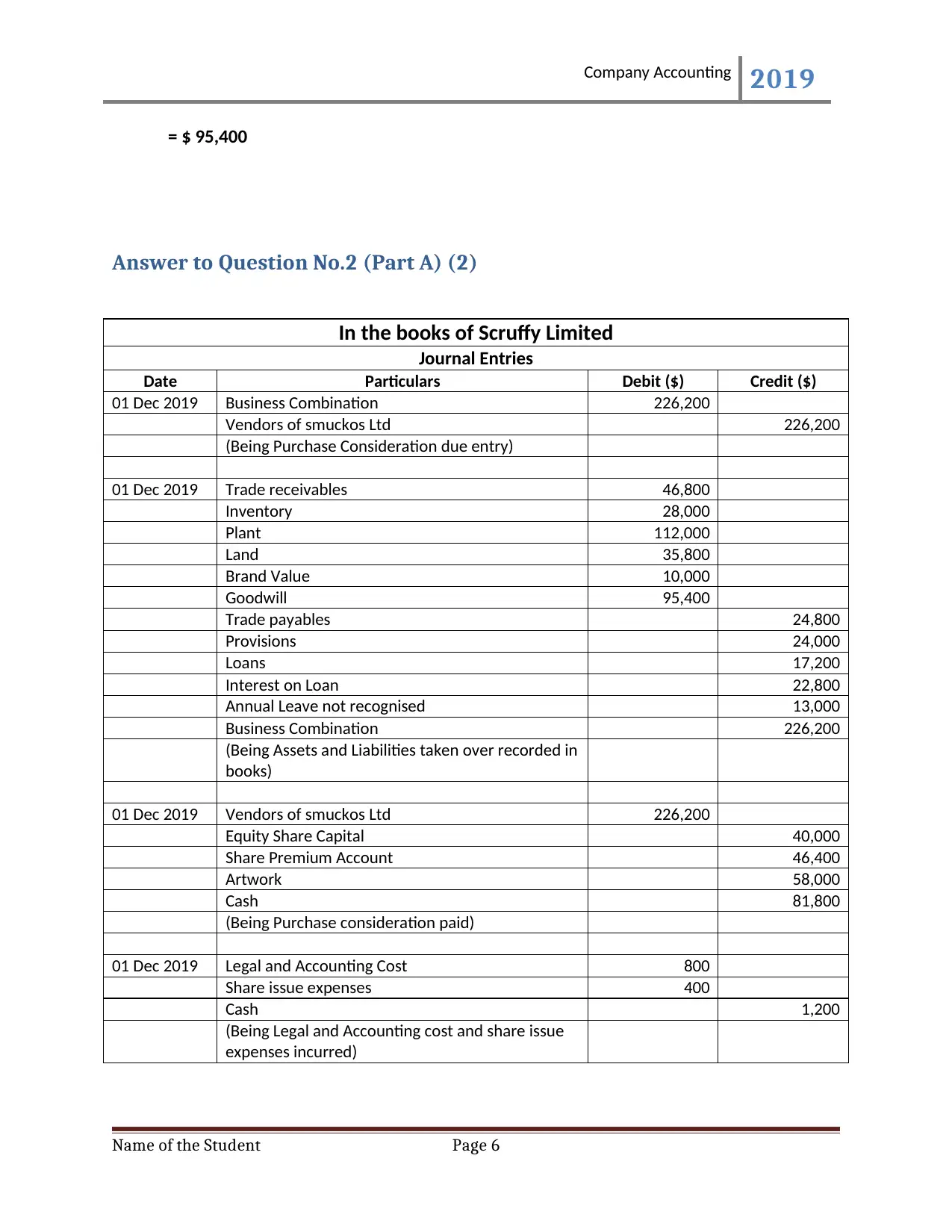

= $ 95,400

Answer to Question No.2 (Part A) (2)

In the books of Scruffy Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

01 Dec 2019 Business Combination 226,200

Vendors of smuckos Ltd 226,200

(Being Purchase Consideration due entry)

01 Dec 2019 Trade receivables 46,800

Inventory 28,000

Plant 112,000

Land 35,800

Brand Value 10,000

Goodwill 95,400

Trade payables 24,800

Provisions 24,000

Loans 17,200

Interest on Loan 22,800

Annual Leave not recognised 13,000

Business Combination 226,200

(Being Assets and Liabilities taken over recorded in

books)

01 Dec 2019 Vendors of smuckos Ltd 226,200

Equity Share Capital 40,000

Share Premium Account 46,400

Artwork 58,000

Cash 81,800

(Being Purchase consideration paid)

01 Dec 2019 Legal and Accounting Cost 800

Share issue expenses 400

Cash 1,200

(Being Legal and Accounting cost and share issue

expenses incurred)

Name of the Student Page 6

= $ 95,400

Answer to Question No.2 (Part A) (2)

In the books of Scruffy Limited

Journal Entries

Date Particulars Debit ($) Credit ($)

01 Dec 2019 Business Combination 226,200

Vendors of smuckos Ltd 226,200

(Being Purchase Consideration due entry)

01 Dec 2019 Trade receivables 46,800

Inventory 28,000

Plant 112,000

Land 35,800

Brand Value 10,000

Goodwill 95,400

Trade payables 24,800

Provisions 24,000

Loans 17,200

Interest on Loan 22,800

Annual Leave not recognised 13,000

Business Combination 226,200

(Being Assets and Liabilities taken over recorded in

books)

01 Dec 2019 Vendors of smuckos Ltd 226,200

Equity Share Capital 40,000

Share Premium Account 46,400

Artwork 58,000

Cash 81,800

(Being Purchase consideration paid)

01 Dec 2019 Legal and Accounting Cost 800

Share issue expenses 400

Cash 1,200

(Being Legal and Accounting cost and share issue

expenses incurred)

Name of the Student Page 6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Company Accounting 2019

Answer to Question No.2 (Part B)

Business Combination

A business combination is essentially an event or transaction where an

acquirer acquires control of either one or over one business. Further, a

business can be defined as a set of integrated assets and activities, which

are capable of being managed and conducted with an intention of offering a

return to the investing members or other participants, owners and members.

Generally, business combinations refer to transactions in which one company

gains control, or at least controlling interest, in another company. A business

combination can be aptly defined as amalgamation of the assets of two or

more business entities for their consolidation as a single entity under single

ownership. A business combination can be managed easily through the way

of a voluntary acquisition, a merger, or a hostile takeover. A business

combination is not a part or creation of new joint venture neither it involves

acquiring an asset which do not form part of business. (AccountingTools.com,

2019)

Three important aspects of business definition are that a business consists of

inputs and processes applied to those inputs that have the ability to create

outputs. Only Purchasing of some asset or liabilities does not amount to

business combination.

Different forms of business combination that might take are

(I) Vertical combination

(II) Horizontal combination

(III) Circular combination

(IV) Diagonal combination

A combination of different business who is involved in the manufacturing and

distribution of different product. (Merriam-Webster, 2019)

A combination of business who are engaged in the manufacturing of same

type of products. For example, Holcim group and Lafarge Cement.

When the firm is involved in manufacturing different types of product

together it is known to be mixed or circular combination. (Sai, 2019)

Name of the Student Page 7

Answer to Question No.2 (Part B)

Business Combination

A business combination is essentially an event or transaction where an

acquirer acquires control of either one or over one business. Further, a

business can be defined as a set of integrated assets and activities, which

are capable of being managed and conducted with an intention of offering a

return to the investing members or other participants, owners and members.

Generally, business combinations refer to transactions in which one company

gains control, or at least controlling interest, in another company. A business

combination can be aptly defined as amalgamation of the assets of two or

more business entities for their consolidation as a single entity under single

ownership. A business combination can be managed easily through the way

of a voluntary acquisition, a merger, or a hostile takeover. A business

combination is not a part or creation of new joint venture neither it involves

acquiring an asset which do not form part of business. (AccountingTools.com,

2019)

Three important aspects of business definition are that a business consists of

inputs and processes applied to those inputs that have the ability to create

outputs. Only Purchasing of some asset or liabilities does not amount to

business combination.

Different forms of business combination that might take are

(I) Vertical combination

(II) Horizontal combination

(III) Circular combination

(IV) Diagonal combination

A combination of different business who is involved in the manufacturing and

distribution of different product. (Merriam-Webster, 2019)

A combination of business who are engaged in the manufacturing of same

type of products. For example, Holcim group and Lafarge Cement.

When the firm is involved in manufacturing different types of product

together it is known to be mixed or circular combination. (Sai, 2019)

Name of the Student Page 7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company Accounting 2019

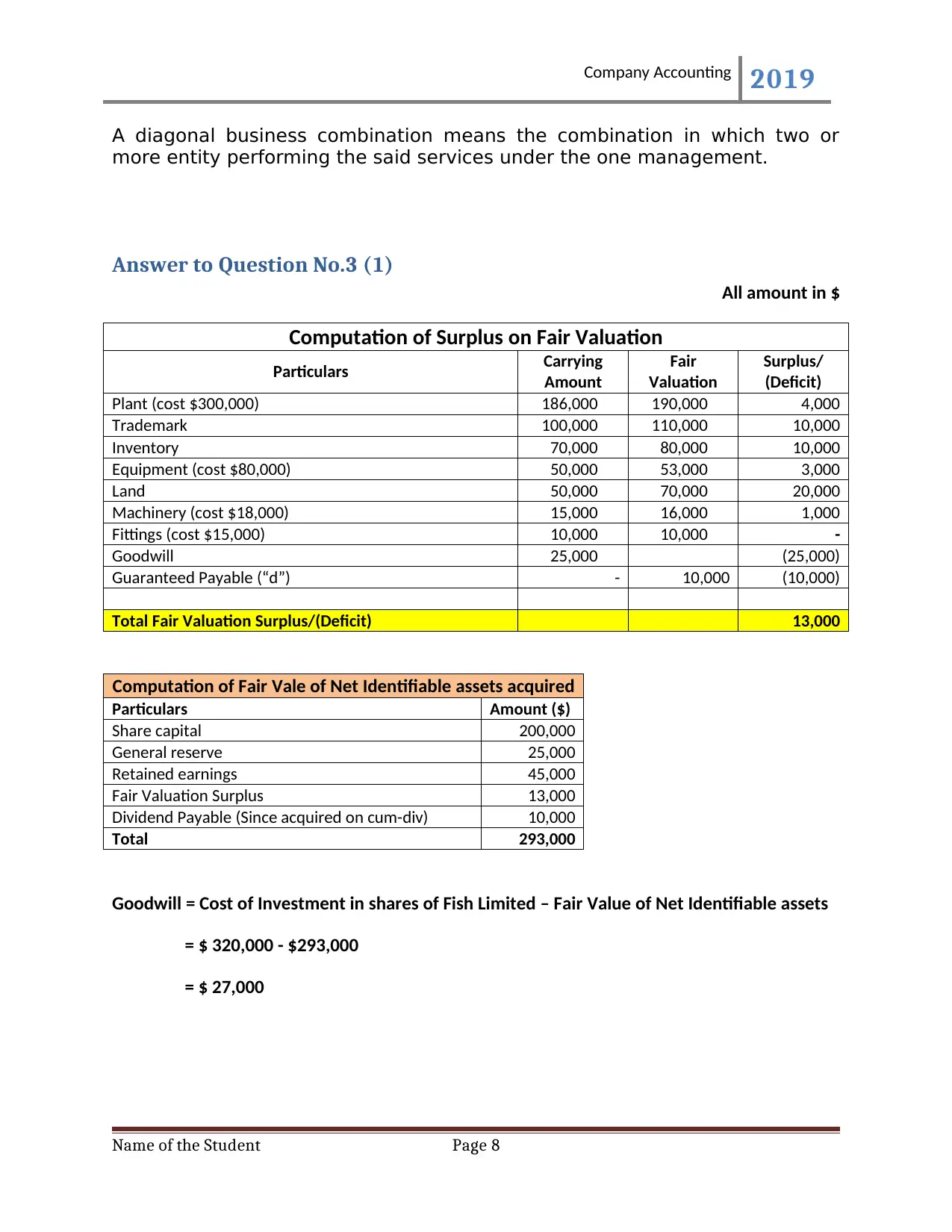

A diagonal business combination means the combination in which two or

more entity performing the said services under the one management.

Answer to Question No.3 (1)

All amount in $

Computation of Surplus on Fair Valuation

Particulars Carrying

Amount

Fair

Valuation

Surplus/

(Deficit)

Plant (cost $300,000) 186,000 190,000 4,000

Trademark 100,000 110,000 10,000

Inventory 70,000 80,000 10,000

Equipment (cost $80,000) 50,000 53,000 3,000

Land 50,000 70,000 20,000

Machinery (cost $18,000) 15,000 16,000 1,000

Fittings (cost $15,000) 10,000 10,000 -

Goodwill 25,000 (25,000)

Guaranteed Payable (“d”) - 10,000 (10,000)

Total Fair Valuation Surplus/(Deficit) 13,000

Computation of Fair Vale of Net Identifiable assets acquired

Particulars Amount ($)

Share capital 200,000

General reserve 25,000

Retained earnings 45,000

Fair Valuation Surplus 13,000

Dividend Payable (Since acquired on cum-div) 10,000

Total 293,000

Goodwill = Cost of Investment in shares of Fish Limited – Fair Value of Net Identifiable assets

= $ 320,000 - $293,000

= $ 27,000

Name of the Student Page 8

A diagonal business combination means the combination in which two or

more entity performing the said services under the one management.

Answer to Question No.3 (1)

All amount in $

Computation of Surplus on Fair Valuation

Particulars Carrying

Amount

Fair

Valuation

Surplus/

(Deficit)

Plant (cost $300,000) 186,000 190,000 4,000

Trademark 100,000 110,000 10,000

Inventory 70,000 80,000 10,000

Equipment (cost $80,000) 50,000 53,000 3,000

Land 50,000 70,000 20,000

Machinery (cost $18,000) 15,000 16,000 1,000

Fittings (cost $15,000) 10,000 10,000 -

Goodwill 25,000 (25,000)

Guaranteed Payable (“d”) - 10,000 (10,000)

Total Fair Valuation Surplus/(Deficit) 13,000

Computation of Fair Vale of Net Identifiable assets acquired

Particulars Amount ($)

Share capital 200,000

General reserve 25,000

Retained earnings 45,000

Fair Valuation Surplus 13,000

Dividend Payable (Since acquired on cum-div) 10,000

Total 293,000

Goodwill = Cost of Investment in shares of Fish Limited – Fair Value of Net Identifiable assets

= $ 320,000 - $293,000

= $ 27,000

Name of the Student Page 8

Company Accounting 2019

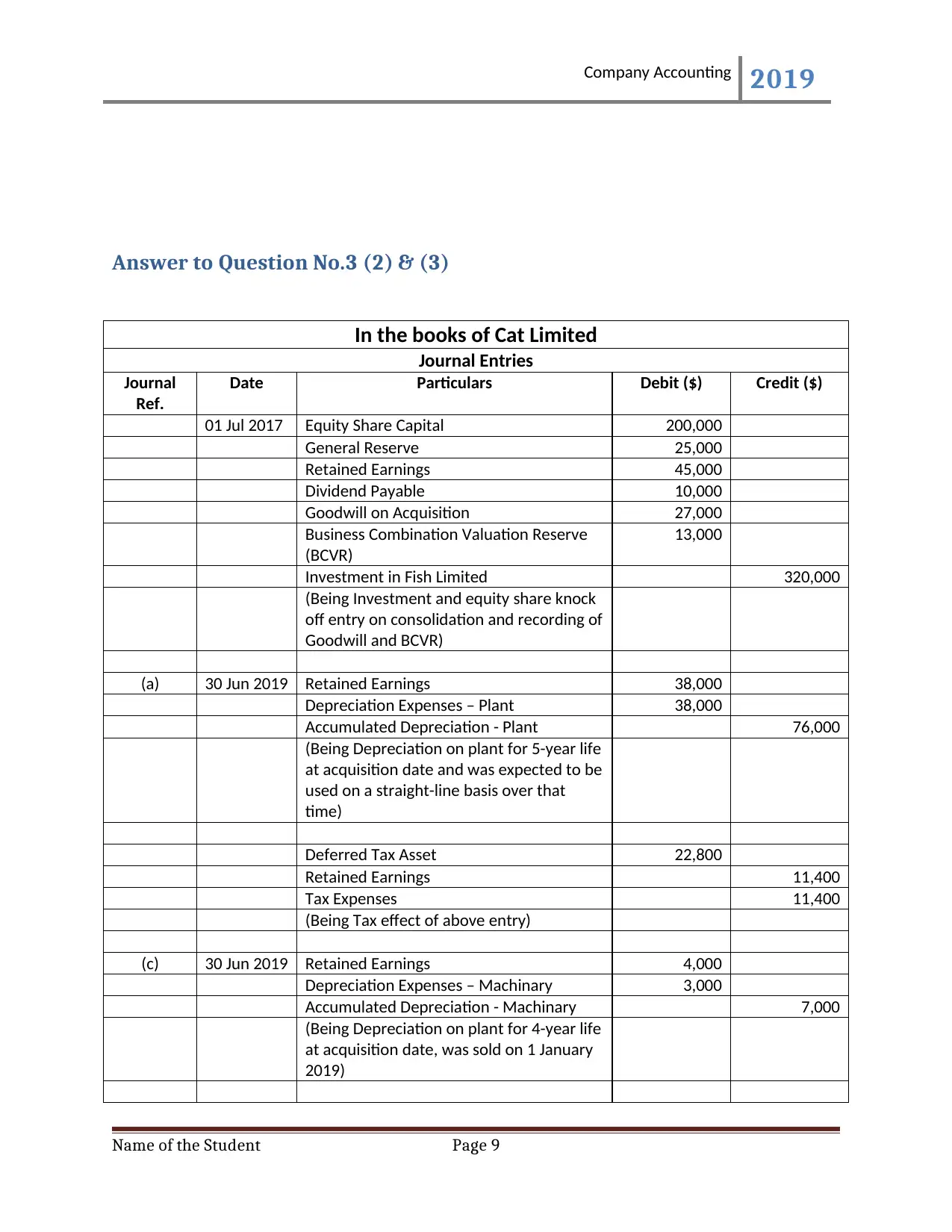

Answer to Question No.3 (2) & (3)

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

01 Jul 2017 Equity Share Capital 200,000

General Reserve 25,000

Retained Earnings 45,000

Dividend Payable 10,000

Goodwill on Acquisition 27,000

Business Combination Valuation Reserve

(BCVR)

13,000

Investment in Fish Limited 320,000

(Being Investment and equity share knock

off entry on consolidation and recording of

Goodwill and BCVR)

(a) 30 Jun 2019 Retained Earnings 38,000

Depreciation Expenses – Plant 38,000

Accumulated Depreciation - Plant 76,000

(Being Depreciation on plant for 5-year life

at acquisition date and was expected to be

used on a straight-line basis over that

time)

Deferred Tax Asset 22,800

Retained Earnings 11,400

Tax Expenses 11,400

(Being Tax effect of above entry)

(c) 30 Jun 2019 Retained Earnings 4,000

Depreciation Expenses – Machinary 3,000

Accumulated Depreciation - Machinary 7,000

(Being Depreciation on plant for 4-year life

at acquisition date, was sold on 1 January

2019)

Name of the Student Page 9

Answer to Question No.3 (2) & (3)

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

01 Jul 2017 Equity Share Capital 200,000

General Reserve 25,000

Retained Earnings 45,000

Dividend Payable 10,000

Goodwill on Acquisition 27,000

Business Combination Valuation Reserve

(BCVR)

13,000

Investment in Fish Limited 320,000

(Being Investment and equity share knock

off entry on consolidation and recording of

Goodwill and BCVR)

(a) 30 Jun 2019 Retained Earnings 38,000

Depreciation Expenses – Plant 38,000

Accumulated Depreciation - Plant 76,000

(Being Depreciation on plant for 5-year life

at acquisition date and was expected to be

used on a straight-line basis over that

time)

Deferred Tax Asset 22,800

Retained Earnings 11,400

Tax Expenses 11,400

(Being Tax effect of above entry)

(c) 30 Jun 2019 Retained Earnings 4,000

Depreciation Expenses – Machinary 3,000

Accumulated Depreciation - Machinary 7,000

(Being Depreciation on plant for 4-year life

at acquisition date, was sold on 1 January

2019)

Name of the Student Page 9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

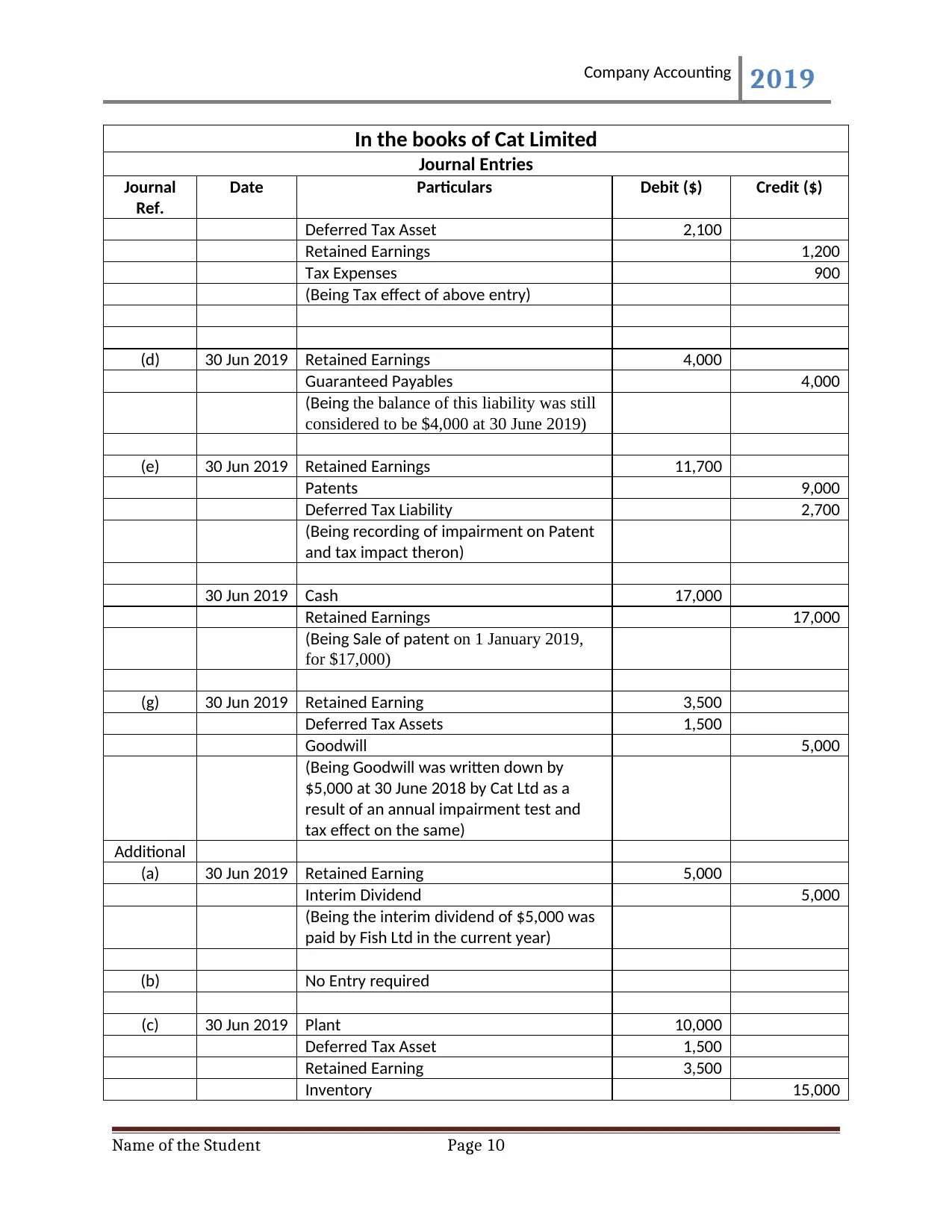

Company Accounting 2019

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

Deferred Tax Asset 2,100

Retained Earnings 1,200

Tax Expenses 900

(Being Tax effect of above entry)

(d) 30 Jun 2019 Retained Earnings 4,000

Guaranteed Payables 4,000

(Being the balance of this liability was still

considered to be $4,000 at 30 June 2019)

(e) 30 Jun 2019 Retained Earnings 11,700

Patents 9,000

Deferred Tax Liability 2,700

(Being recording of impairment on Patent

and tax impact theron)

30 Jun 2019 Cash 17,000

Retained Earnings 17,000

(Being Sale of patent on 1 January 2019,

for $17,000)

(g) 30 Jun 2019 Retained Earning 3,500

Deferred Tax Assets 1,500

Goodwill 5,000

(Being Goodwill was written down by

$5,000 at 30 June 2018 by Cat Ltd as a

result of an annual impairment test and

tax effect on the same)

Additional

(a) 30 Jun 2019 Retained Earning 5,000

Interim Dividend 5,000

(Being the interim dividend of $5,000 was

paid by Fish Ltd in the current year)

(b) No Entry required

(c) 30 Jun 2019 Plant 10,000

Deferred Tax Asset 1,500

Retained Earning 3,500

Inventory 15,000

Name of the Student Page 10

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

Deferred Tax Asset 2,100

Retained Earnings 1,200

Tax Expenses 900

(Being Tax effect of above entry)

(d) 30 Jun 2019 Retained Earnings 4,000

Guaranteed Payables 4,000

(Being the balance of this liability was still

considered to be $4,000 at 30 June 2019)

(e) 30 Jun 2019 Retained Earnings 11,700

Patents 9,000

Deferred Tax Liability 2,700

(Being recording of impairment on Patent

and tax impact theron)

30 Jun 2019 Cash 17,000

Retained Earnings 17,000

(Being Sale of patent on 1 January 2019,

for $17,000)

(g) 30 Jun 2019 Retained Earning 3,500

Deferred Tax Assets 1,500

Goodwill 5,000

(Being Goodwill was written down by

$5,000 at 30 June 2018 by Cat Ltd as a

result of an annual impairment test and

tax effect on the same)

Additional

(a) 30 Jun 2019 Retained Earning 5,000

Interim Dividend 5,000

(Being the interim dividend of $5,000 was

paid by Fish Ltd in the current year)

(b) No Entry required

(c) 30 Jun 2019 Plant 10,000

Deferred Tax Asset 1,500

Retained Earning 3,500

Inventory 15,000

Name of the Student Page 10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Company Accounting 2019

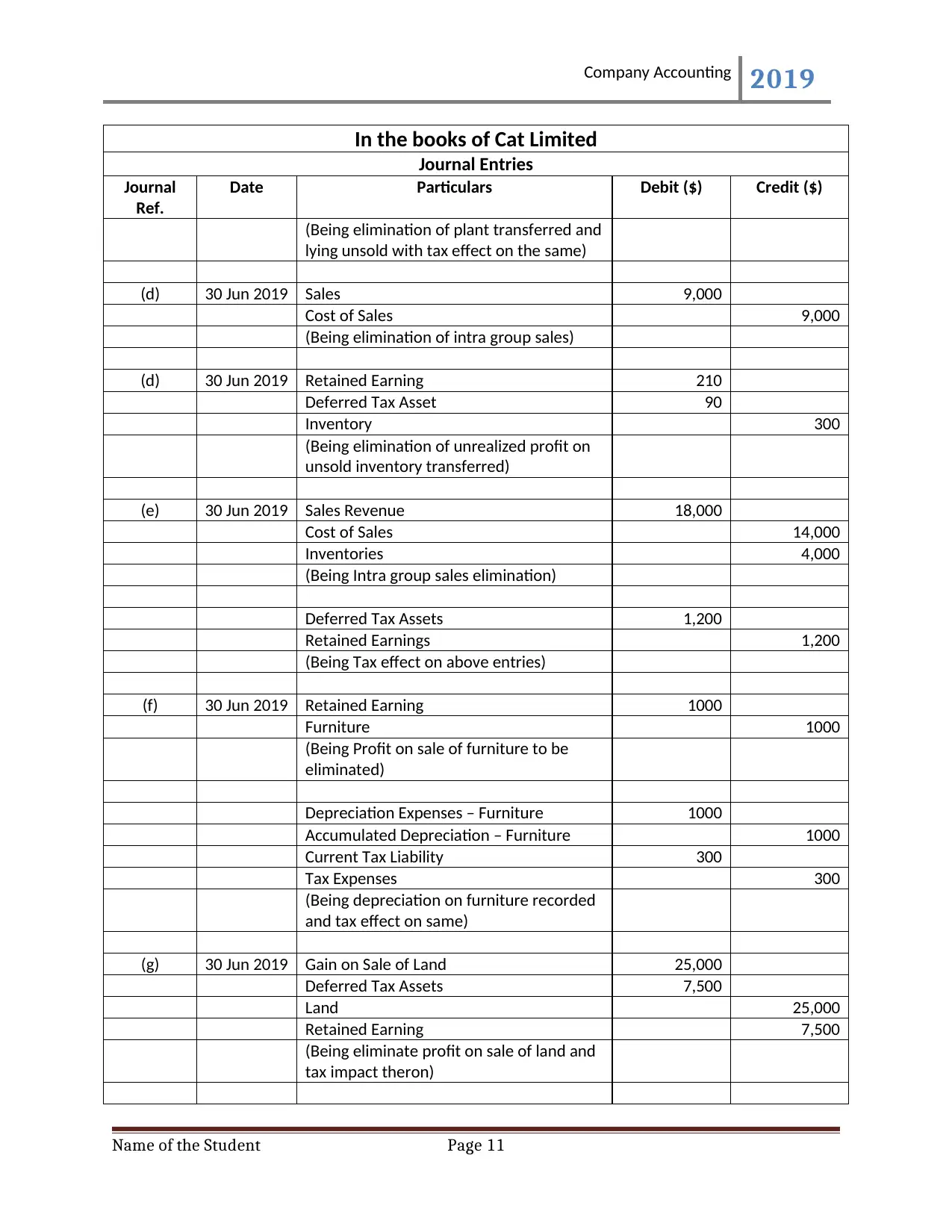

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

(Being elimination of plant transferred and

lying unsold with tax effect on the same)

(d) 30 Jun 2019 Sales 9,000

Cost of Sales 9,000

(Being elimination of intra group sales)

(d) 30 Jun 2019 Retained Earning 210

Deferred Tax Asset 90

Inventory 300

(Being elimination of unrealized profit on

unsold inventory transferred)

(e) 30 Jun 2019 Sales Revenue 18,000

Cost of Sales 14,000

Inventories 4,000

(Being Intra group sales elimination)

Deferred Tax Assets 1,200

Retained Earnings 1,200

(Being Tax effect on above entries)

(f) 30 Jun 2019 Retained Earning 1000

Furniture 1000

(Being Profit on sale of furniture to be

eliminated)

Depreciation Expenses – Furniture 1000

Accumulated Depreciation – Furniture 1000

Current Tax Liability 300

Tax Expenses 300

(Being depreciation on furniture recorded

and tax effect on same)

(g) 30 Jun 2019 Gain on Sale of Land 25,000

Deferred Tax Assets 7,500

Land 25,000

Retained Earning 7,500

(Being eliminate profit on sale of land and

tax impact theron)

Name of the Student Page 11

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

(Being elimination of plant transferred and

lying unsold with tax effect on the same)

(d) 30 Jun 2019 Sales 9,000

Cost of Sales 9,000

(Being elimination of intra group sales)

(d) 30 Jun 2019 Retained Earning 210

Deferred Tax Asset 90

Inventory 300

(Being elimination of unrealized profit on

unsold inventory transferred)

(e) 30 Jun 2019 Sales Revenue 18,000

Cost of Sales 14,000

Inventories 4,000

(Being Intra group sales elimination)

Deferred Tax Assets 1,200

Retained Earnings 1,200

(Being Tax effect on above entries)

(f) 30 Jun 2019 Retained Earning 1000

Furniture 1000

(Being Profit on sale of furniture to be

eliminated)

Depreciation Expenses – Furniture 1000

Accumulated Depreciation – Furniture 1000

Current Tax Liability 300

Tax Expenses 300

(Being depreciation on furniture recorded

and tax effect on same)

(g) 30 Jun 2019 Gain on Sale of Land 25,000

Deferred Tax Assets 7,500

Land 25,000

Retained Earning 7,500

(Being eliminate profit on sale of land and

tax impact theron)

Name of the Student Page 11

Company Accounting 2019

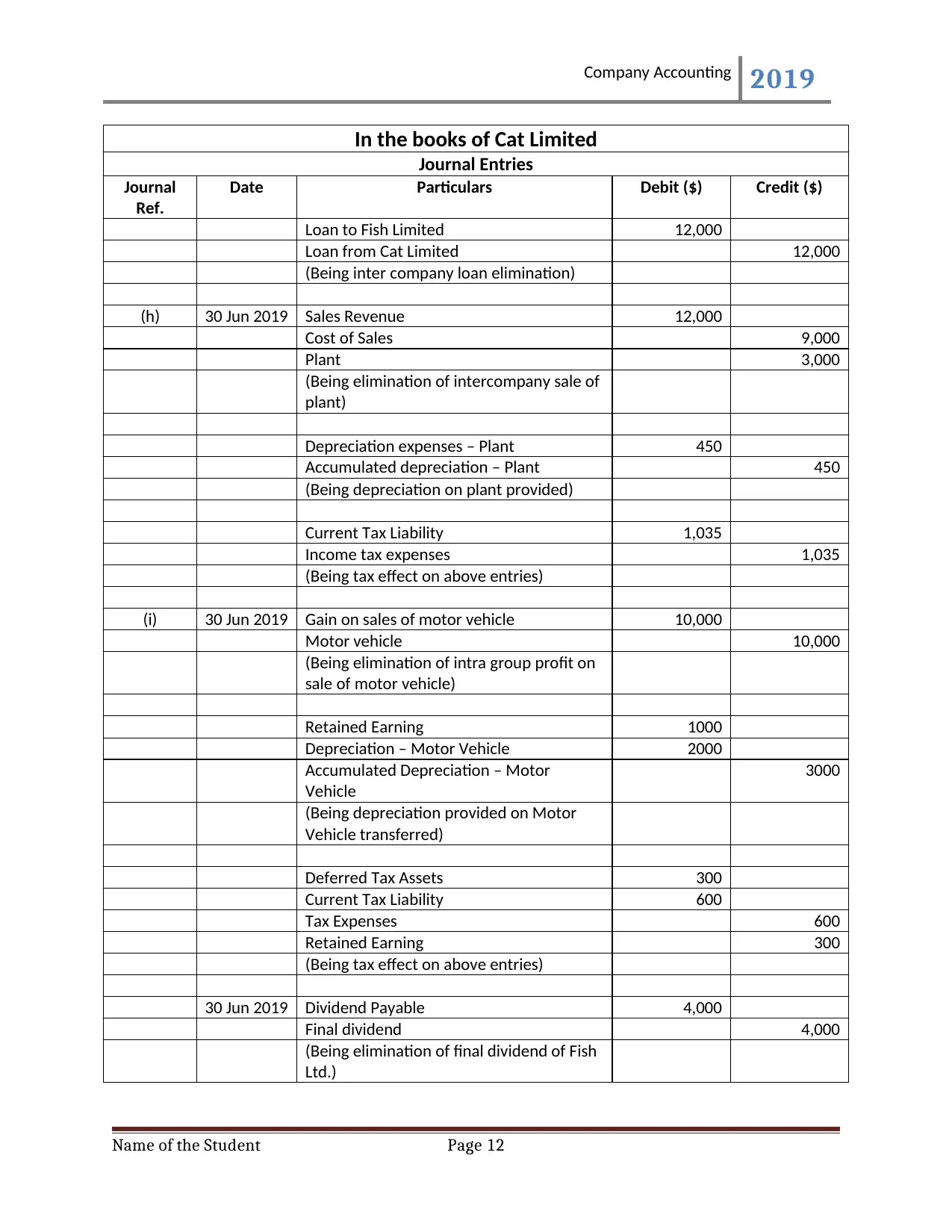

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

Loan to Fish Limited 12,000

Loan from Cat Limited 12,000

(Being inter company loan elimination)

(h) 30 Jun 2019 Sales Revenue 12,000

Cost of Sales 9,000

Plant 3,000

(Being elimination of intercompany sale of

plant)

Depreciation expenses – Plant 450

Accumulated depreciation – Plant 450

(Being depreciation on plant provided)

Current Tax Liability 1,035

Income tax expenses 1,035

(Being tax effect on above entries)

(i) 30 Jun 2019 Gain on sales of motor vehicle 10,000

Motor vehicle 10,000

(Being elimination of intra group profit on

sale of motor vehicle)

Retained Earning 1000

Depreciation – Motor Vehicle 2000

Accumulated Depreciation – Motor

Vehicle

3000

(Being depreciation provided on Motor

Vehicle transferred)

Deferred Tax Assets 300

Current Tax Liability 600

Tax Expenses 600

Retained Earning 300

(Being tax effect on above entries)

30 Jun 2019 Dividend Payable 4,000

Final dividend 4,000

(Being elimination of final dividend of Fish

Ltd.)

Name of the Student Page 12

In the books of Cat Limited

Journal Entries

Journal

Ref.

Date Particulars Debit ($) Credit ($)

Loan to Fish Limited 12,000

Loan from Cat Limited 12,000

(Being inter company loan elimination)

(h) 30 Jun 2019 Sales Revenue 12,000

Cost of Sales 9,000

Plant 3,000

(Being elimination of intercompany sale of

plant)

Depreciation expenses – Plant 450

Accumulated depreciation – Plant 450

(Being depreciation on plant provided)

Current Tax Liability 1,035

Income tax expenses 1,035

(Being tax effect on above entries)

(i) 30 Jun 2019 Gain on sales of motor vehicle 10,000

Motor vehicle 10,000

(Being elimination of intra group profit on

sale of motor vehicle)

Retained Earning 1000

Depreciation – Motor Vehicle 2000

Accumulated Depreciation – Motor

Vehicle

3000

(Being depreciation provided on Motor

Vehicle transferred)

Deferred Tax Assets 300

Current Tax Liability 600

Tax Expenses 600

Retained Earning 300

(Being tax effect on above entries)

30 Jun 2019 Dividend Payable 4,000

Final dividend 4,000

(Being elimination of final dividend of Fish

Ltd.)

Name of the Student Page 12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.