Company Accounting Case Study Assessment 2 - ACCT6005 Analysis

VerifiedAdded on 2022/12/14

|10

|1843

|451

Case Study

AI Summary

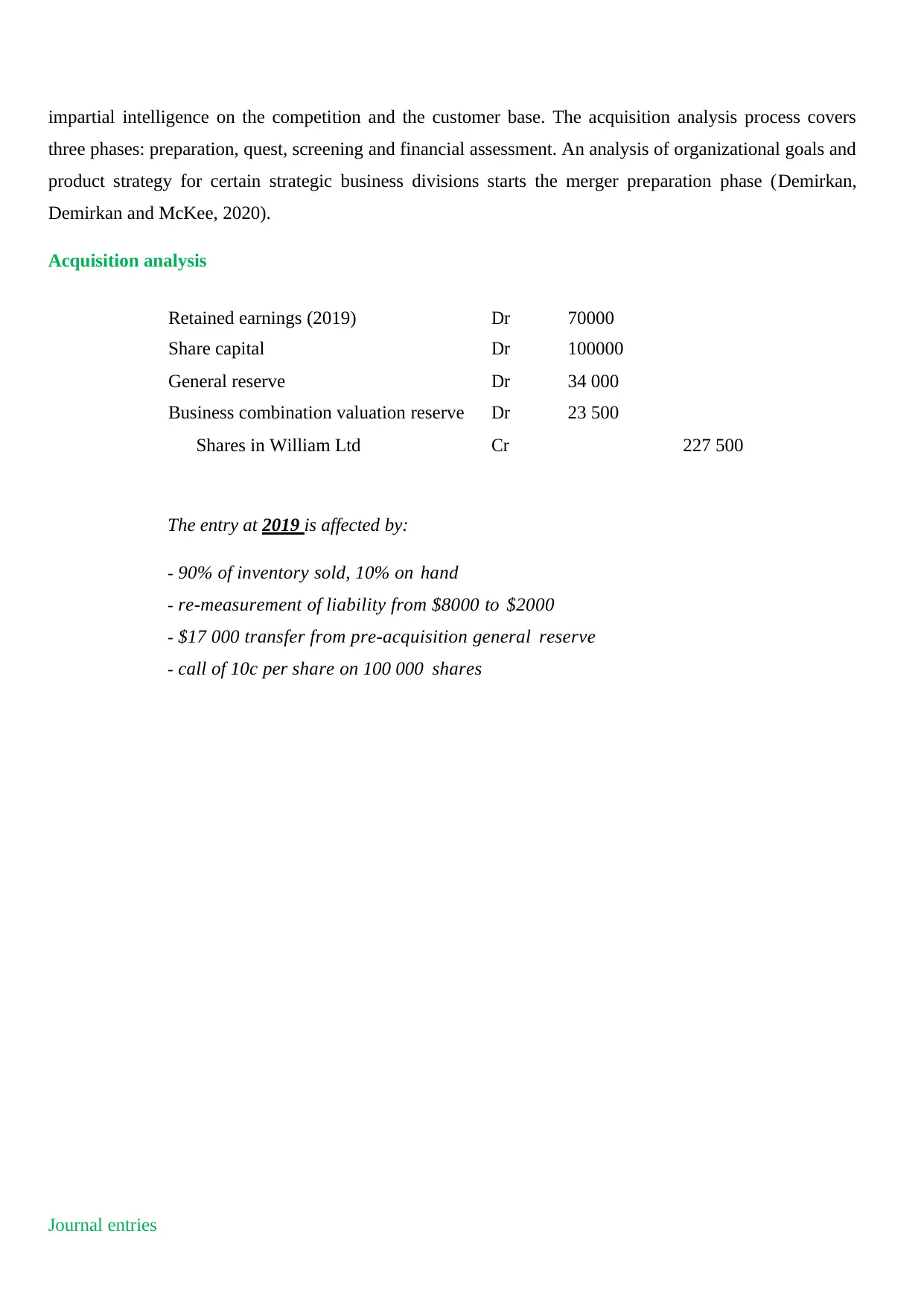

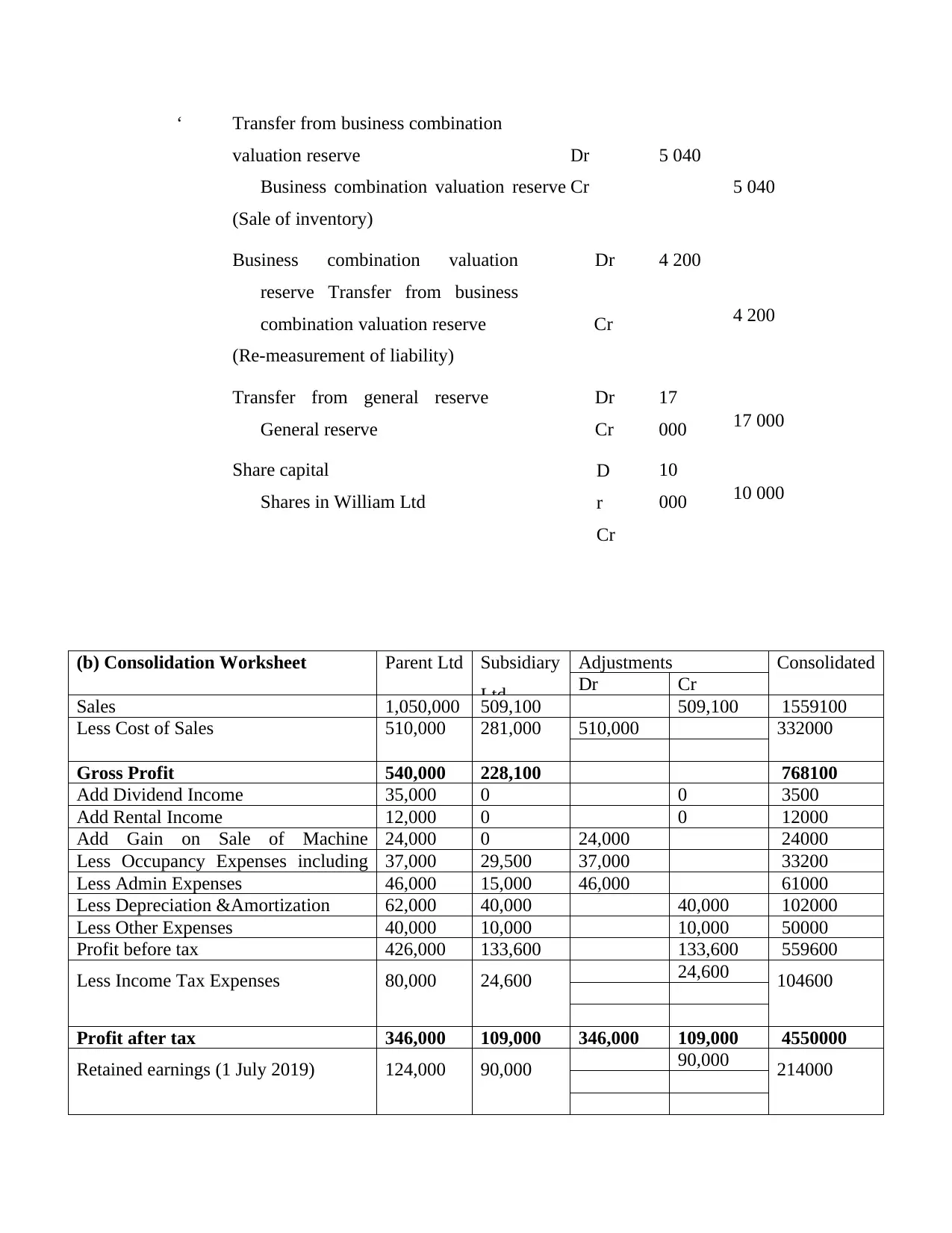

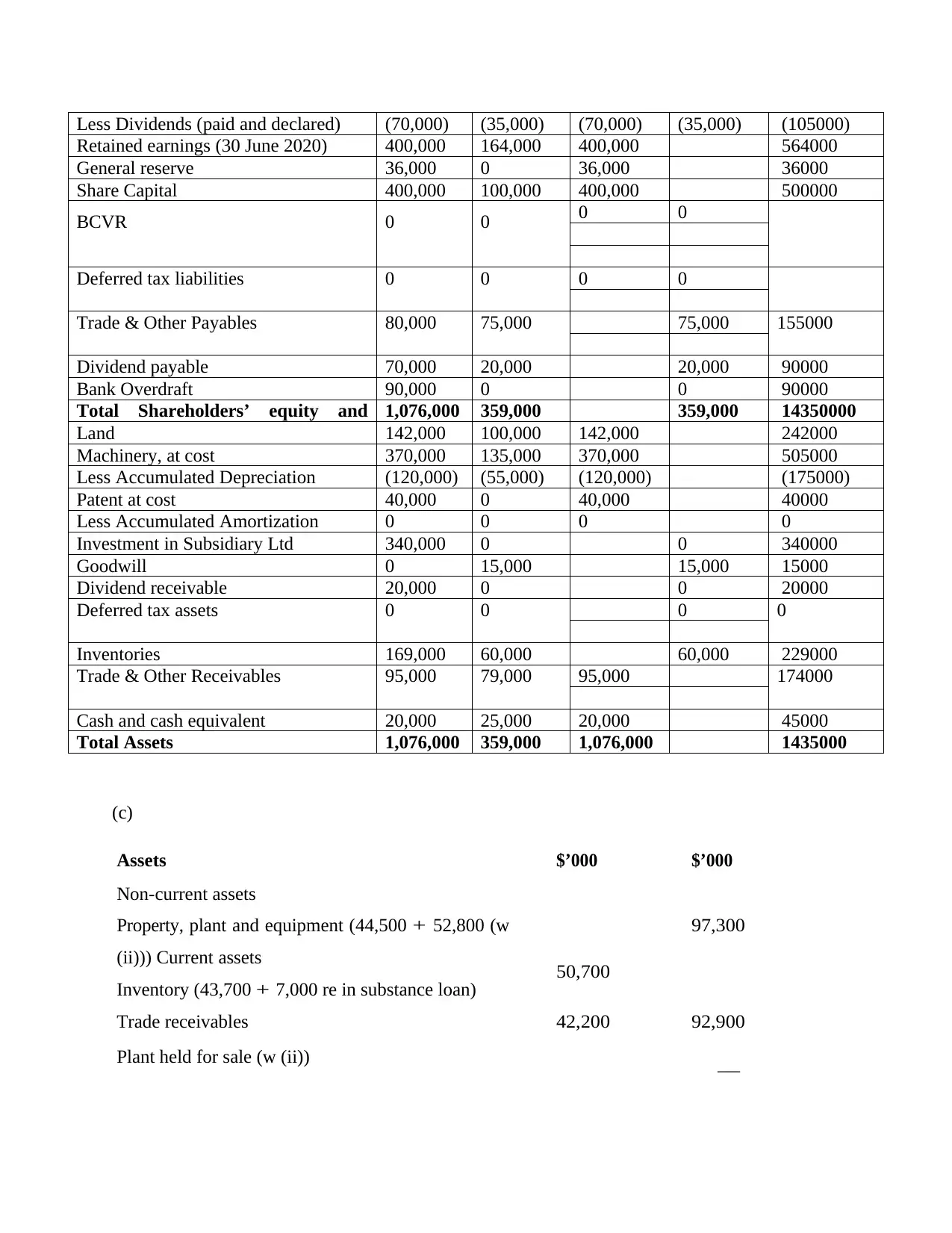

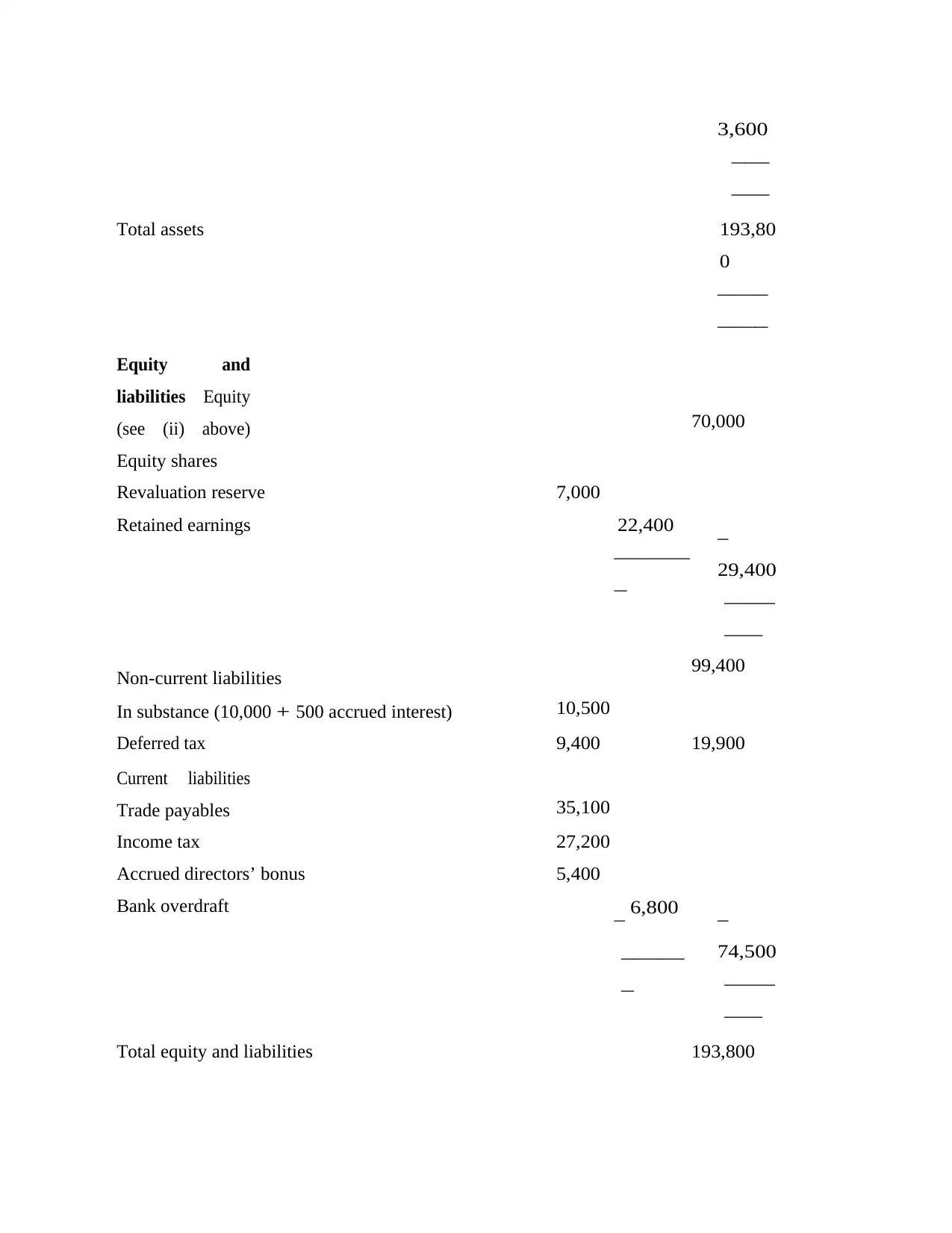

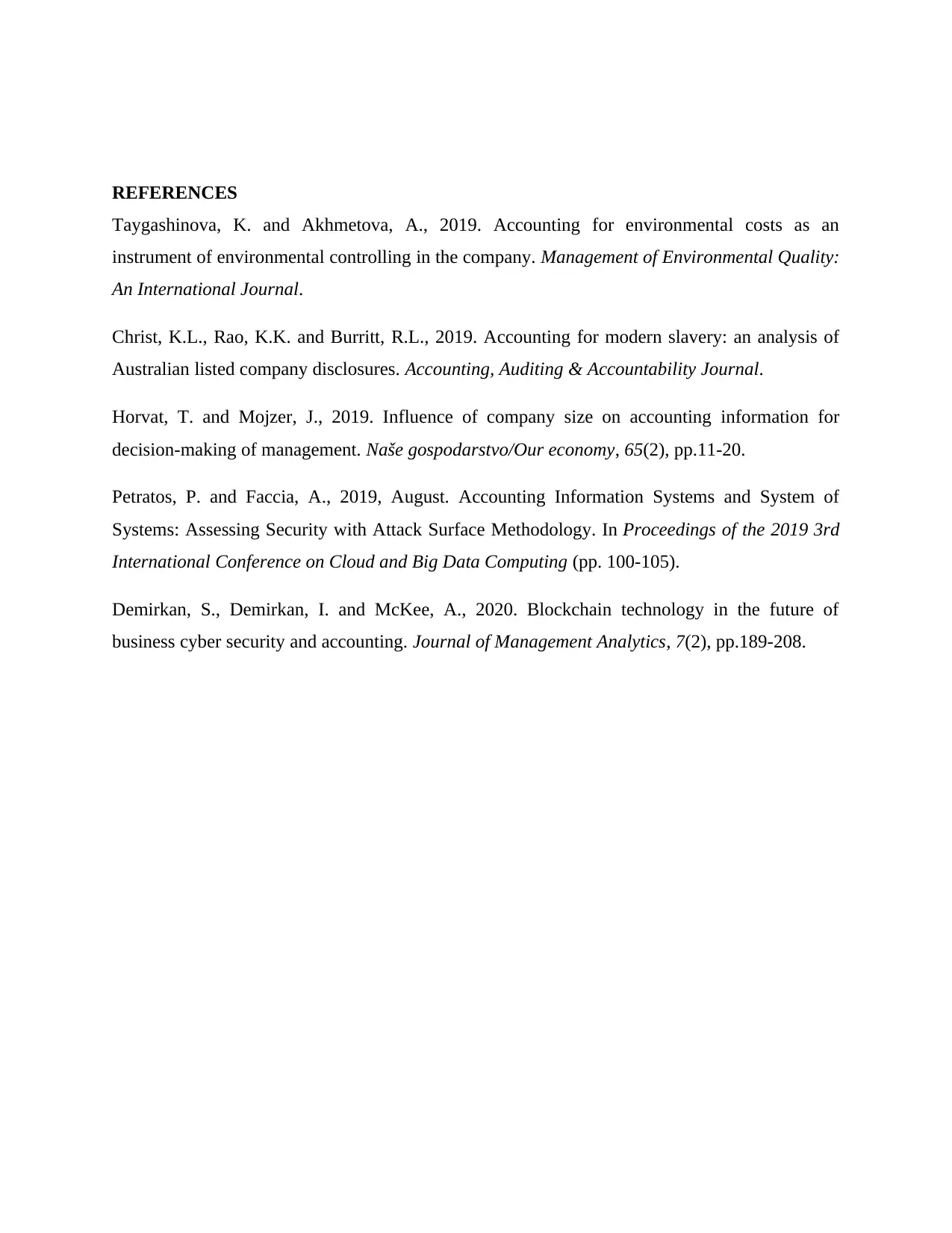

This document presents a complete solution to the ACCT6005 Company Accounting case study, addressing both the theoretical and practical aspects of the assessment. Part A analyzes the theoretical framework of company accounting, specifically focusing on shareholder rights, the power to dismiss managers, and the requirements for various corporate actions like constitutional changes and election of directors. It also discusses the implications of shareholder consent in different scenarios and the rights of shareholders to take decisions against board desires. Part B provides a practical application through acquisition analysis, journal entries, and a consolidation worksheet. The worksheet includes consolidated financial statements, incorporating adjustments for intercompany transactions and fair value adjustments. The document also presents consolidated financial statements and discusses the assets, equity, and liabilities. It provides a detailed breakdown of the financial data, including sales, cost of sales, profit, and various balance sheet items, offering a comprehensive understanding of the consolidation process and the resulting financial statements.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.