University Accounting Assignment: Goodwill and Accounting Practices

VerifiedAdded on 2023/01/03

|7

|537

|84

Homework Assignment

AI Summary

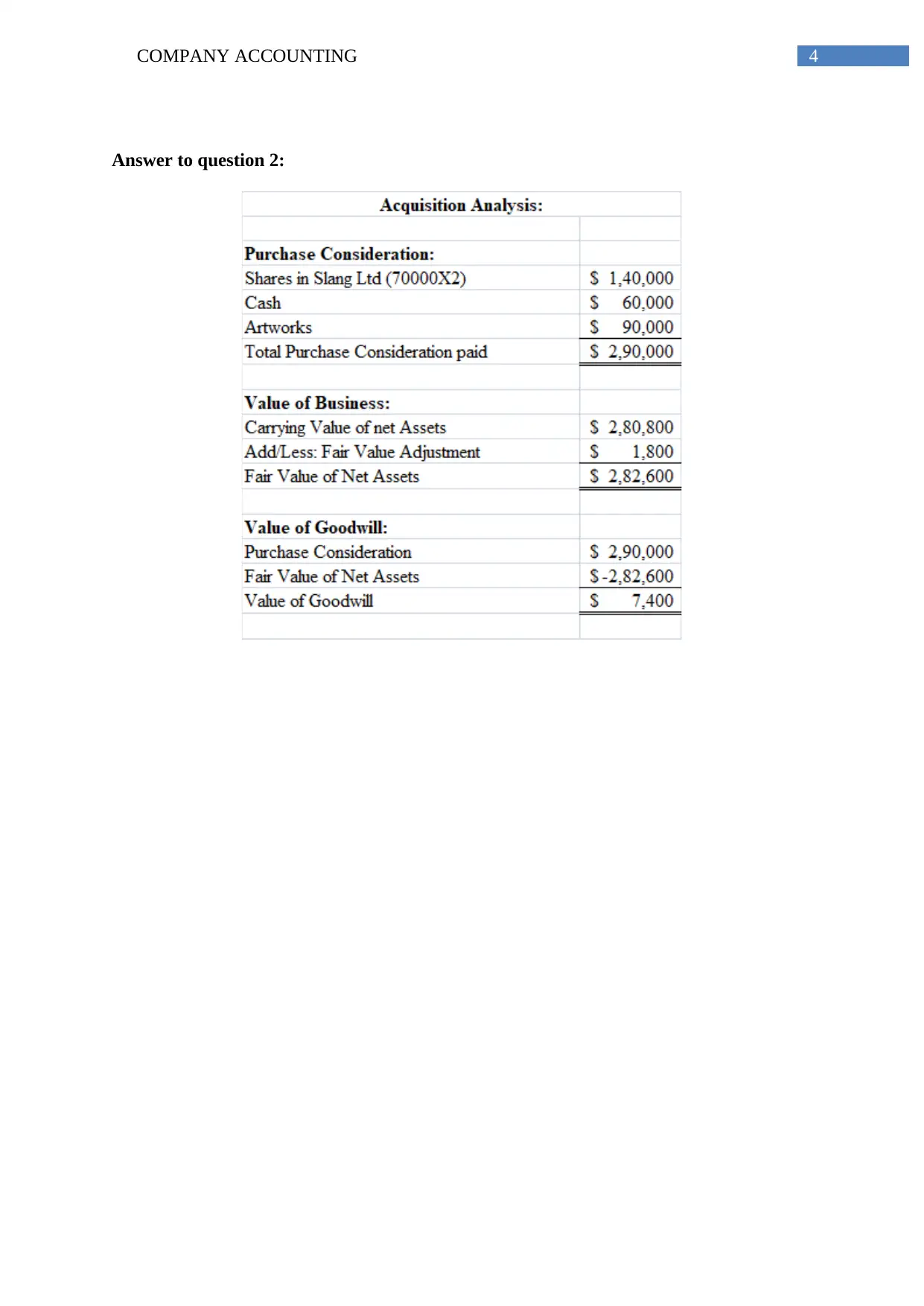

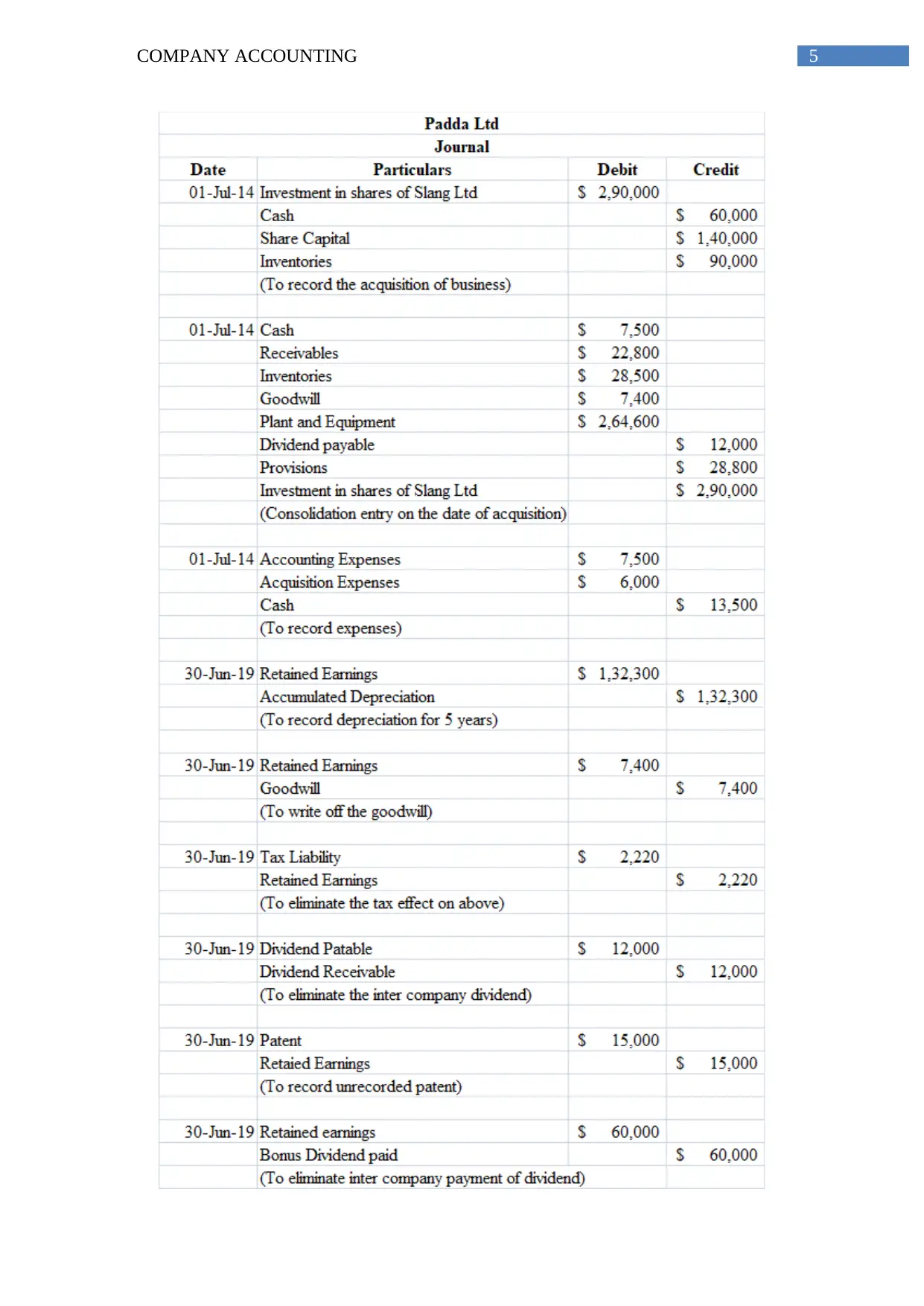

This assignment solution addresses the nature of goodwill and its accounting treatment, specifically focusing on purchased and inherent goodwill. The document begins with a memorandum from a Chief Financial Officer to the Directors of Patagonia Ltd, explaining the concept of goodwill as the ability of a business to earn supernormal profits. It distinguishes between inherent goodwill, arising from brand loyalty and image, and purchased goodwill, which is the excess paid during acquisition. The solution details the accounting treatment, suggesting that inherent goodwill should not be recognized in the balance sheet, while purchased goodwill can be recognized and is subject to impairment testing. The assignment includes a bibliography citing relevant academic sources, providing a comprehensive overview of the topic. This assignment is a valuable resource for students studying company accounting, offering clear explanations and practical applications of key accounting principles related to goodwill.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.