University Company Accounting: AGL Energy Financial Statement Memo

VerifiedAdded on 2022/11/25

|9

|1601

|302

Report

AI Summary

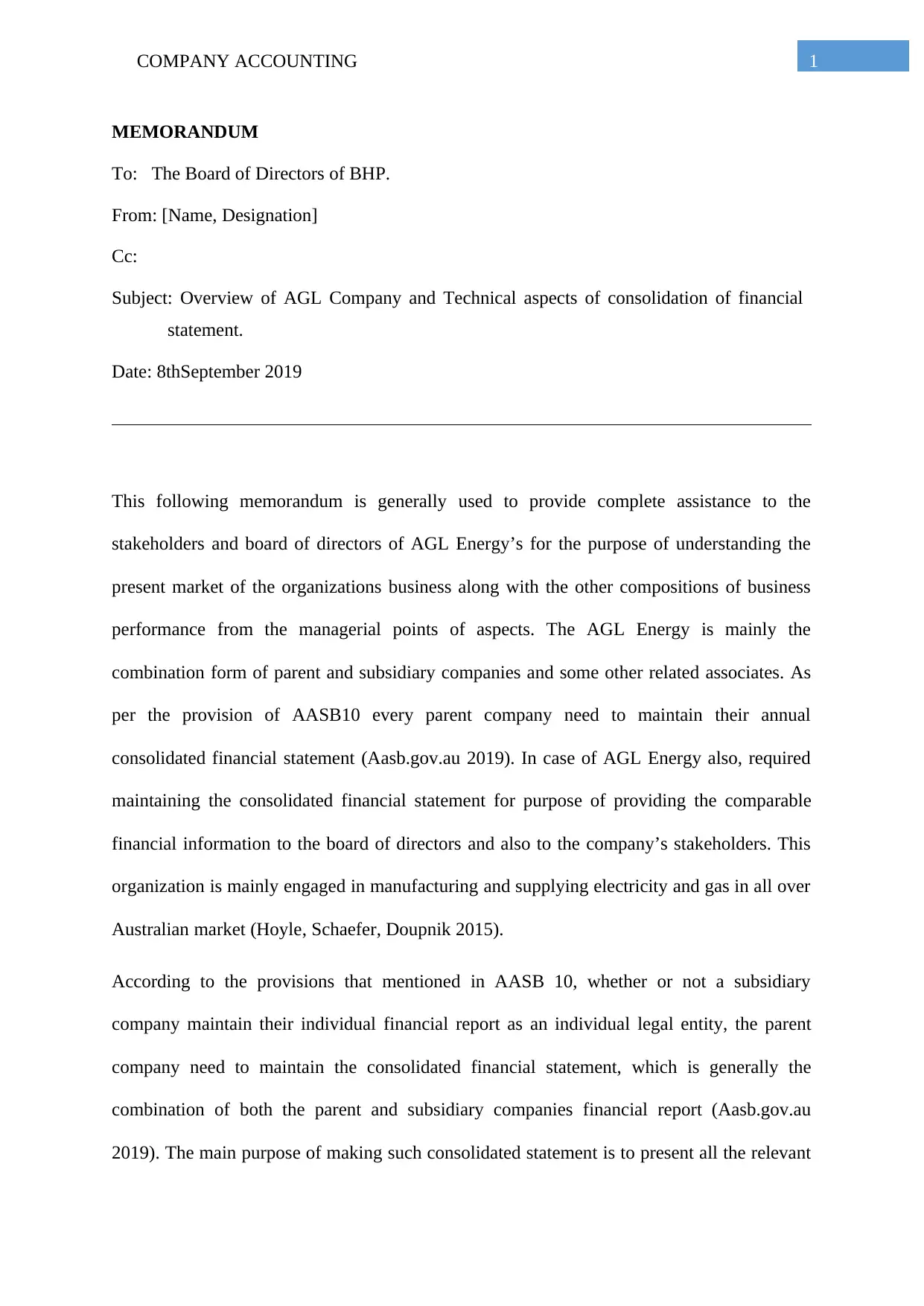

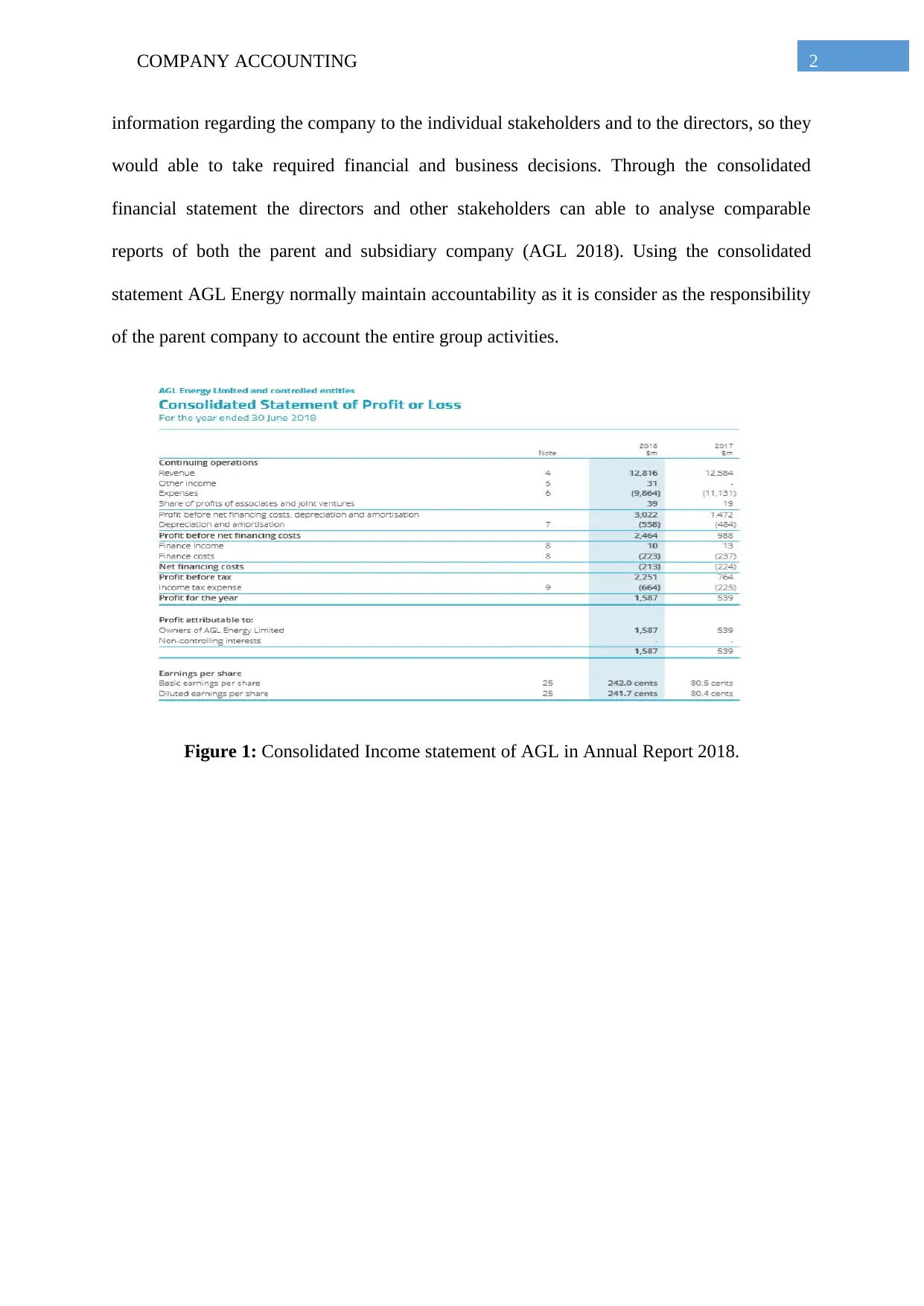

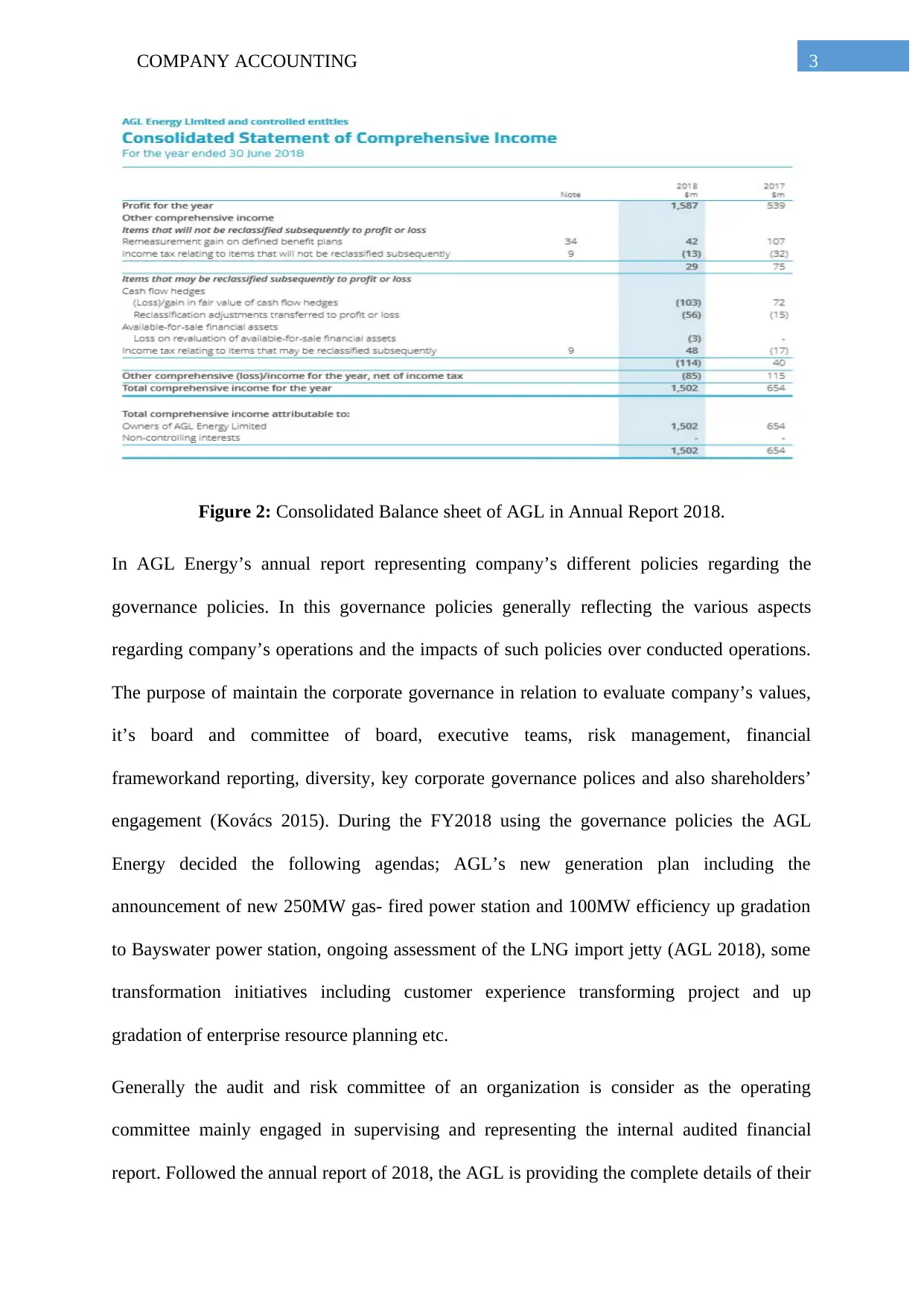

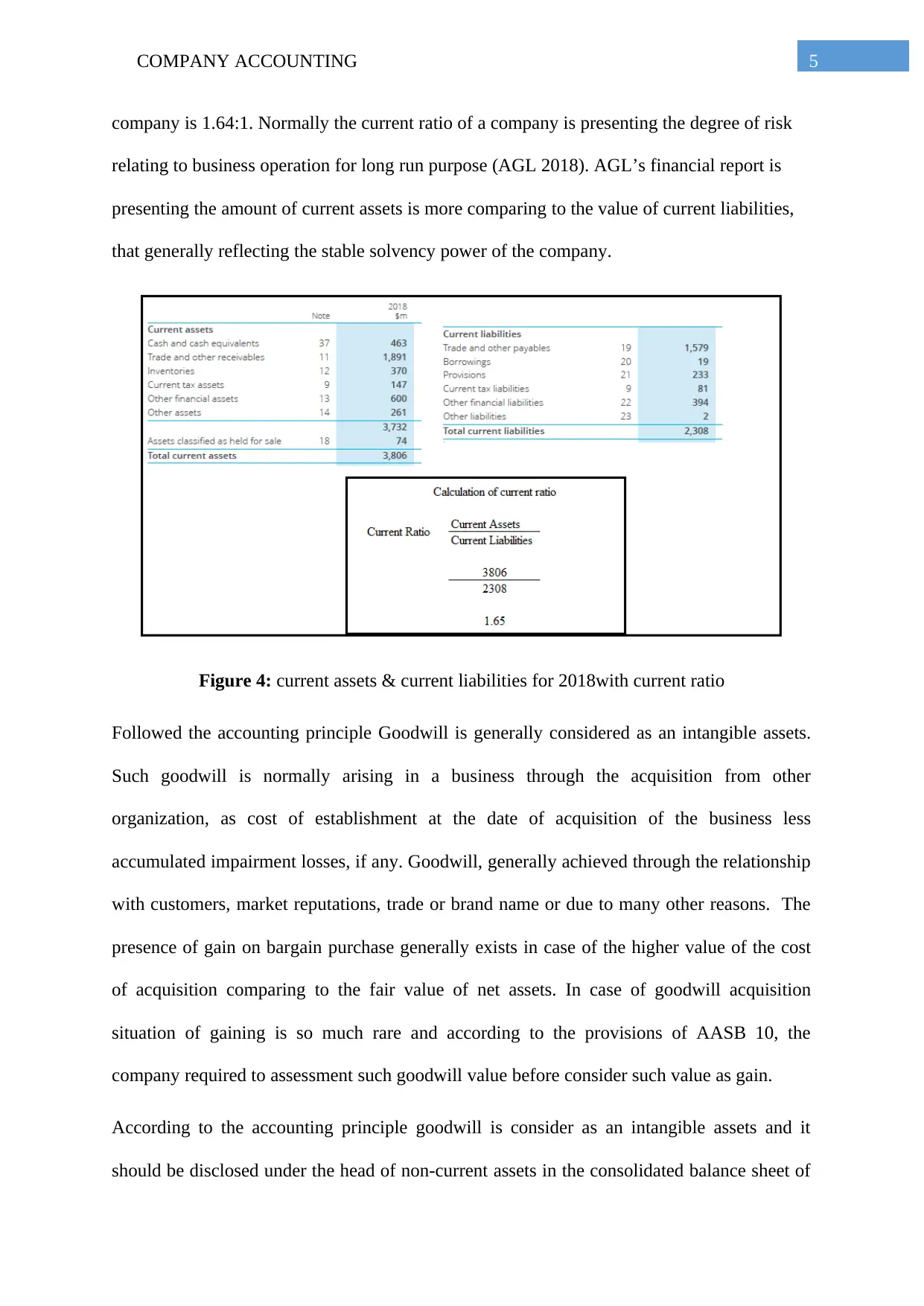

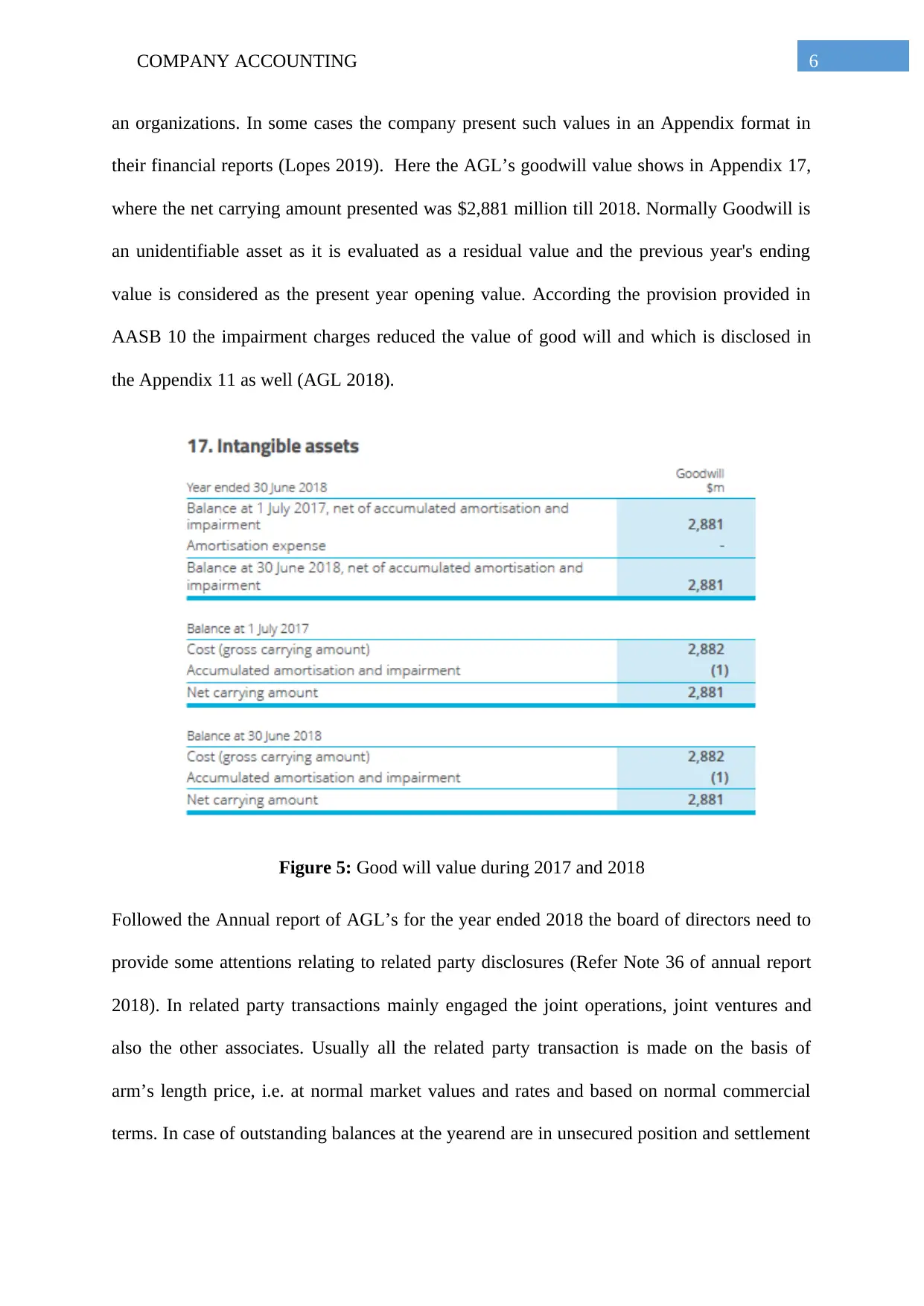

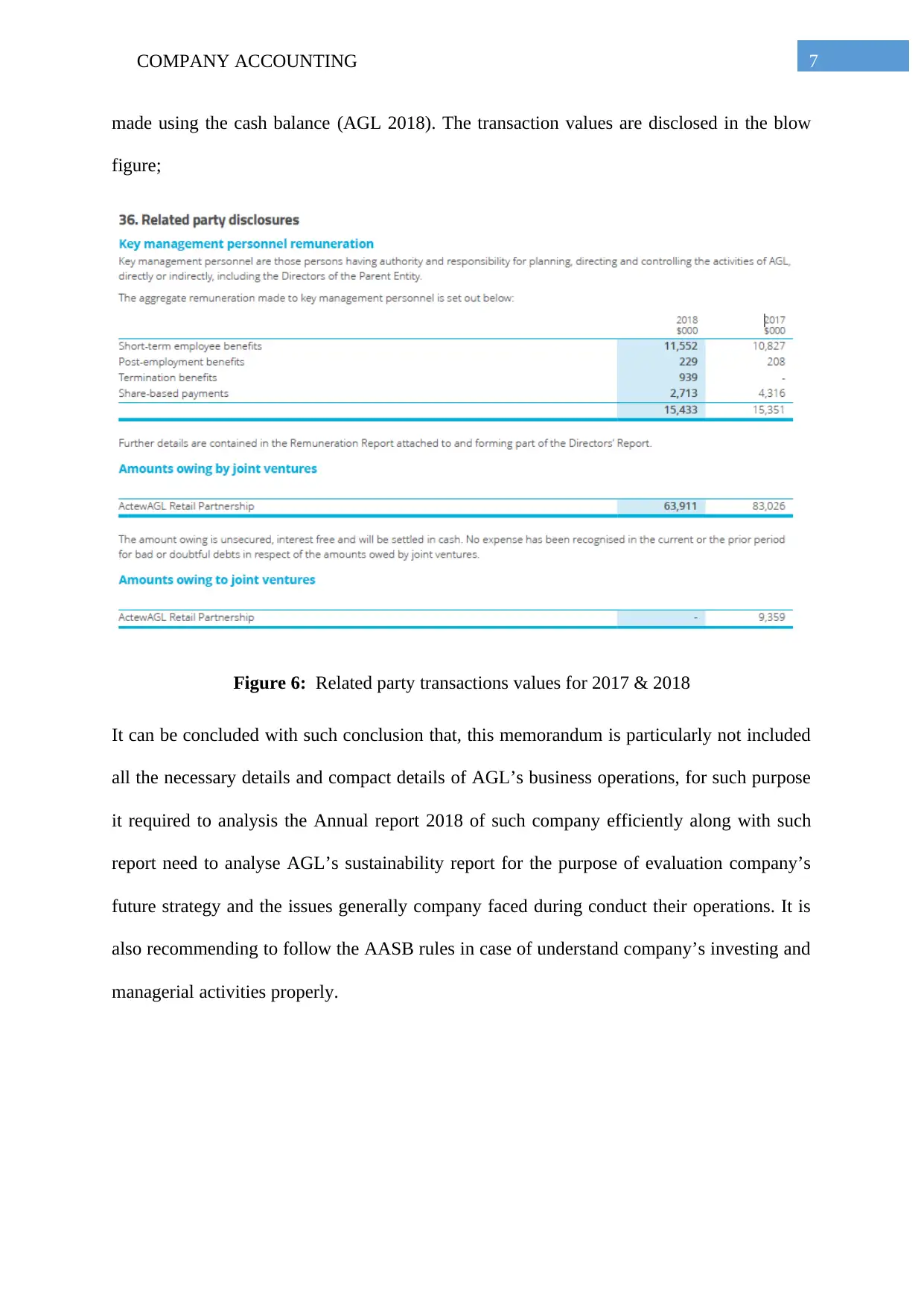

This memorandum, addressed to the Board of Directors of BHP, provides an overview of AGL Energy's business operations and technical aspects of financial statement consolidation. It analyzes AGL Energy's consolidated financial statements, prepared in accordance with AASB10, highlighting key elements such as the consolidated income statement, balance sheet, governance policies, and the role of the audit and risk committee. The memo further examines AGL's sustainability approaches, solvency through current ratio analysis, and the treatment of goodwill as an intangible asset. It also delves into related party transactions, as disclosed in the annual report, offering a comprehensive understanding of AGL's financial performance and reporting practices. The memo references AGL's 2018 annual report and relevant accounting standards, providing a solid foundation for understanding the company's financial position and operational strategies.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.