ACCT20073 Company Accounting: Palvidia Ltd's Share Purchase Analysis

VerifiedAdded on 2023/06/07

|9

|1258

|317

Homework Assignment

AI Summary

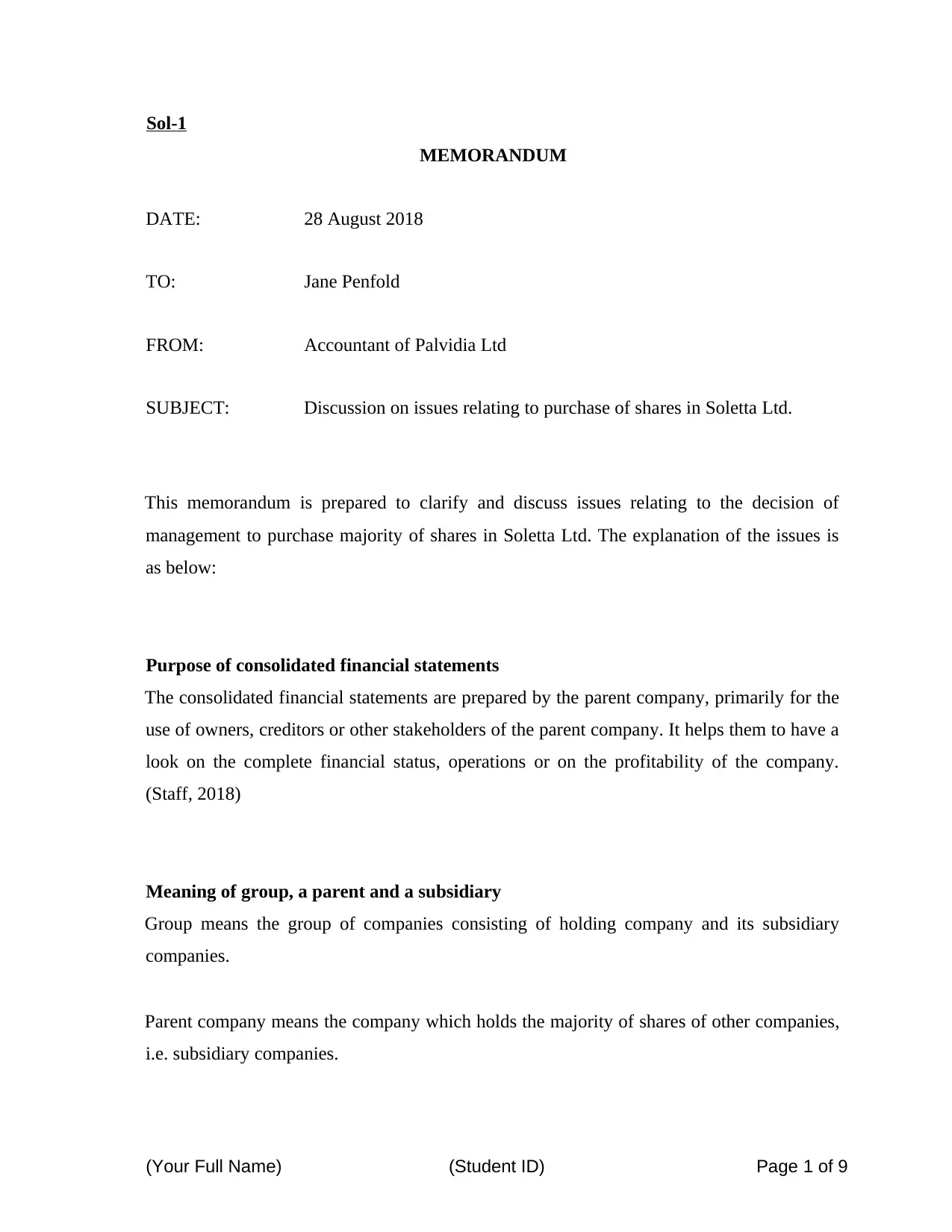

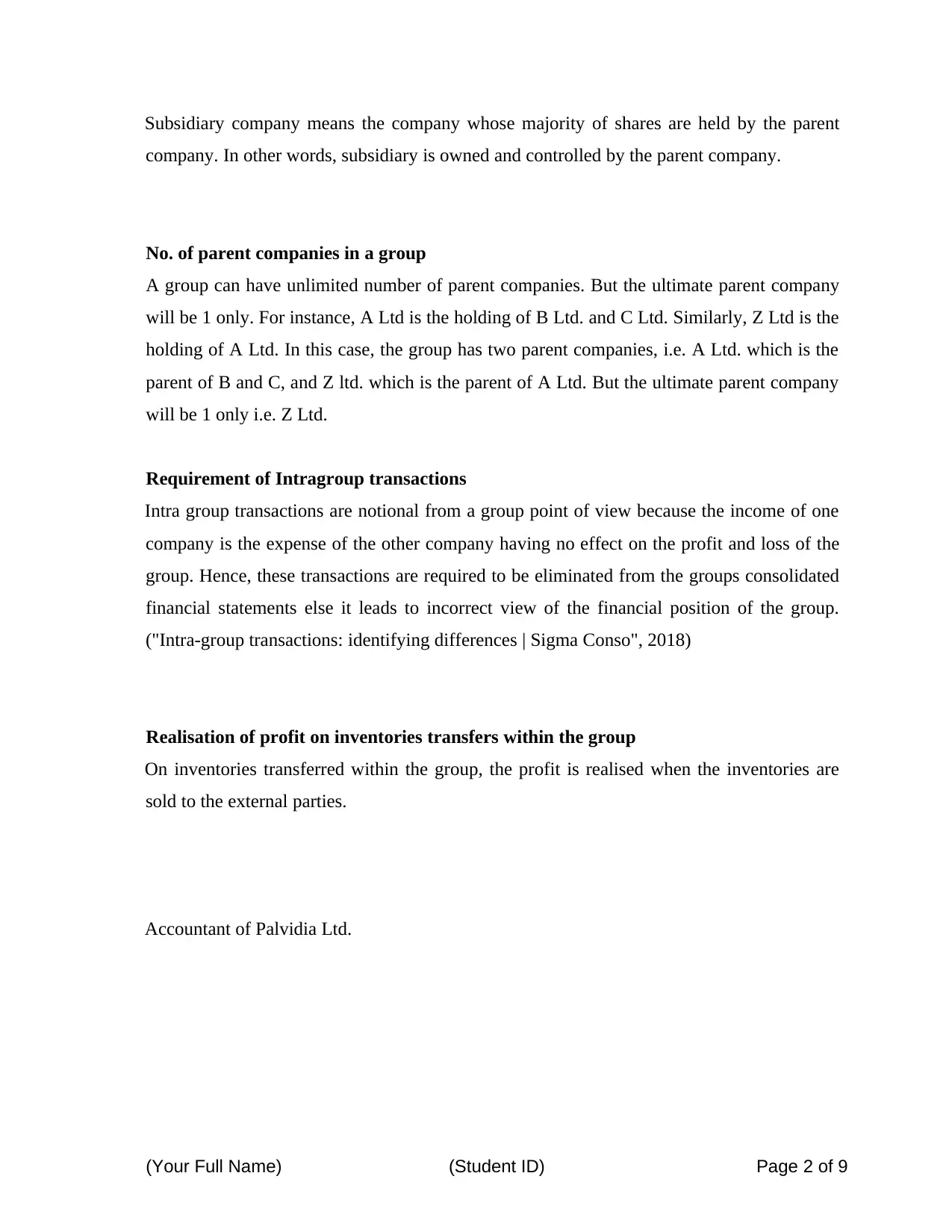

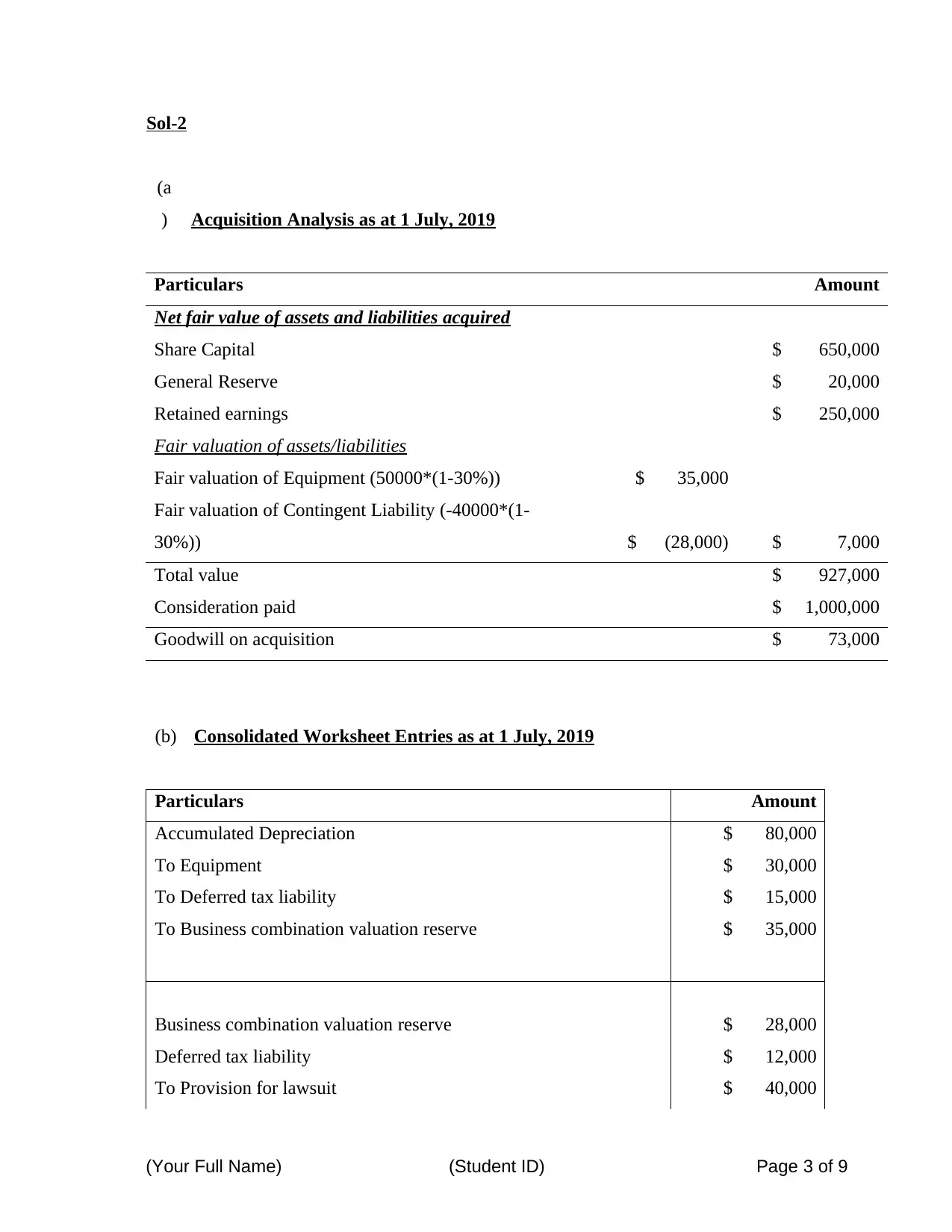

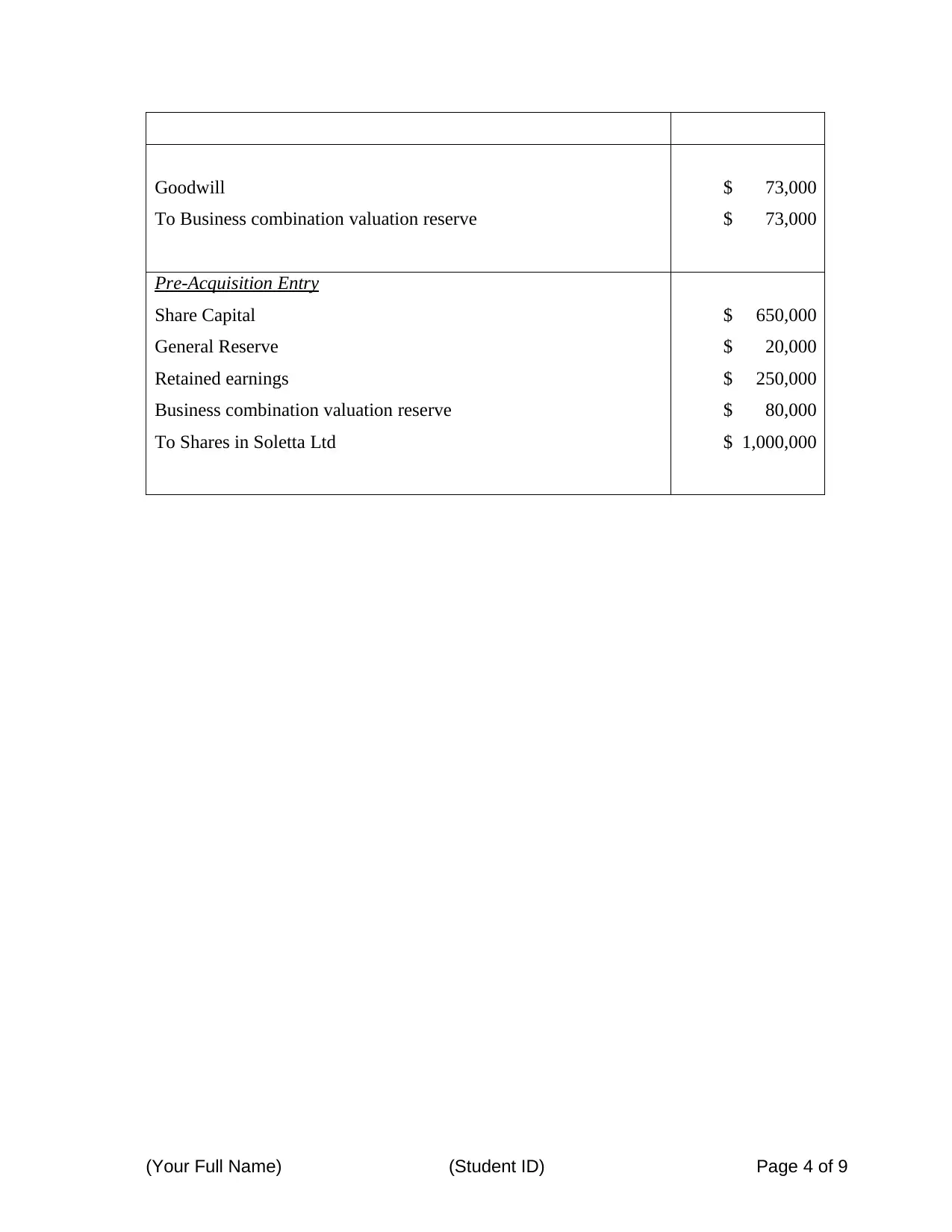

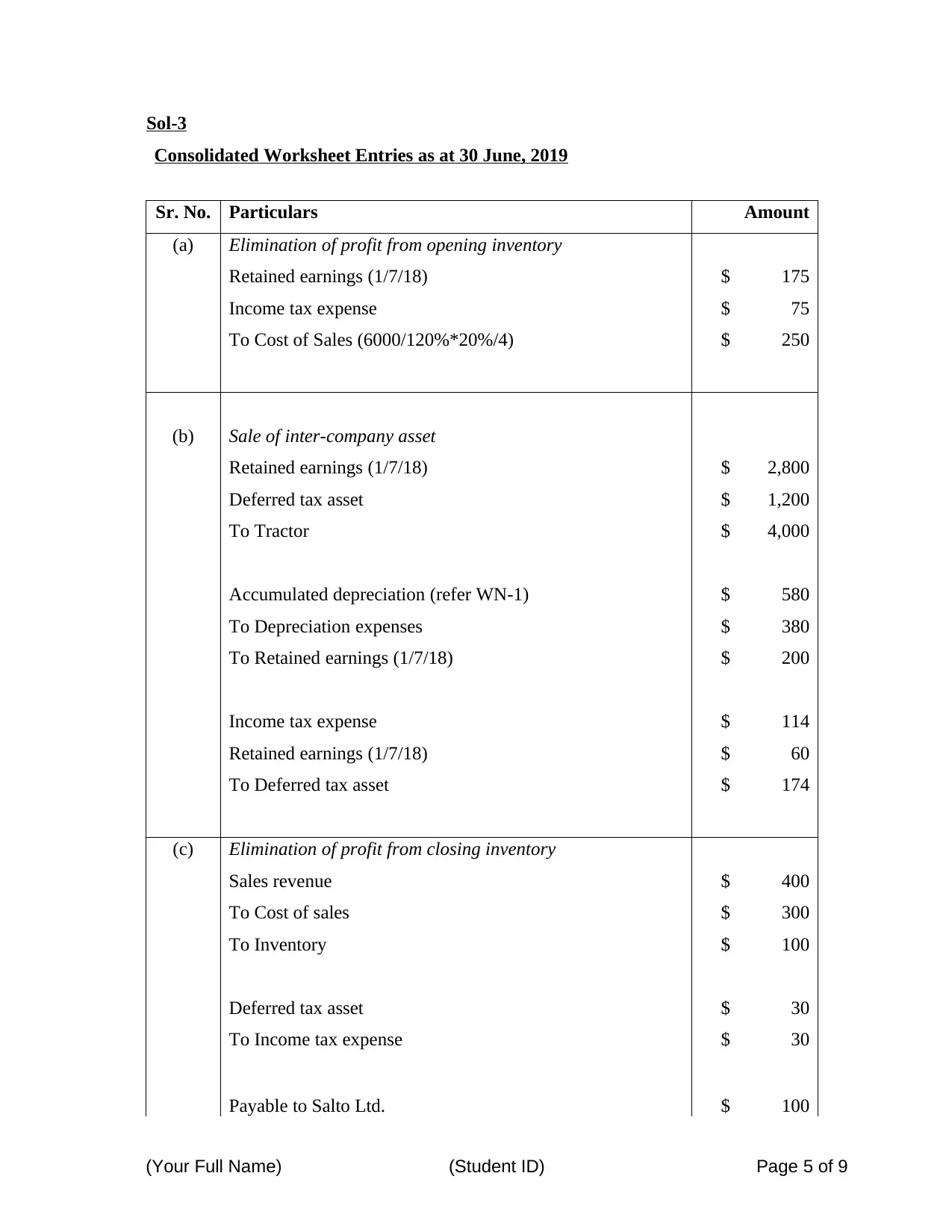

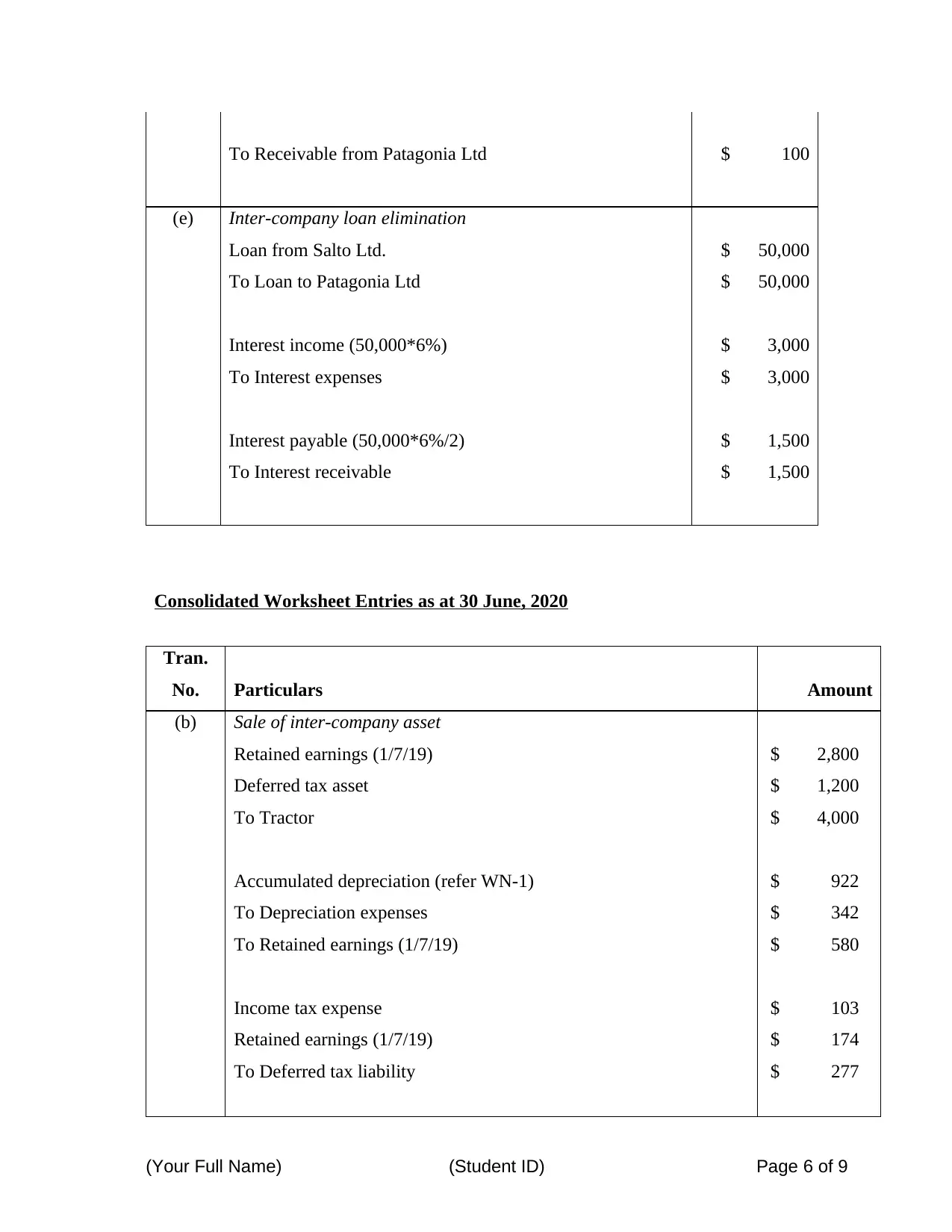

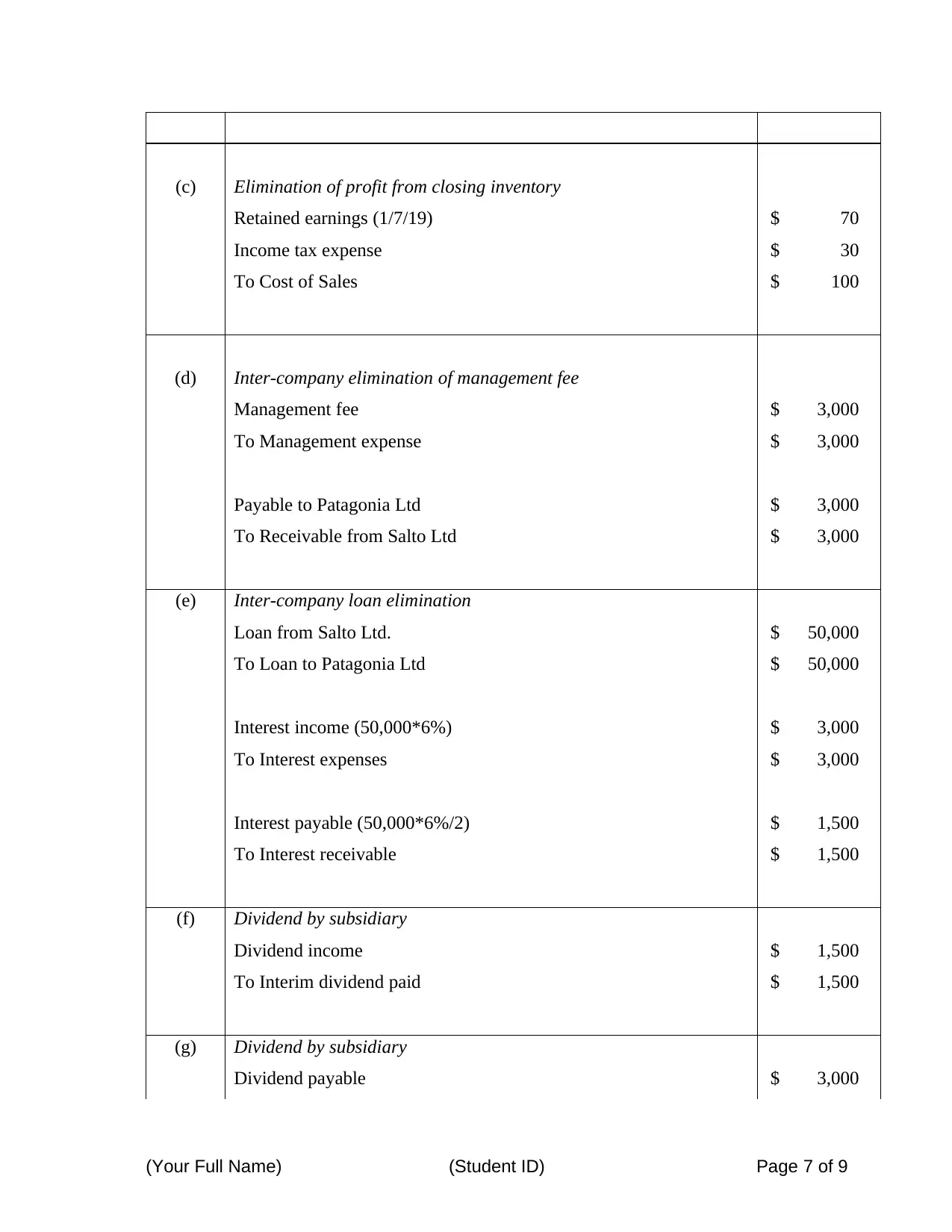

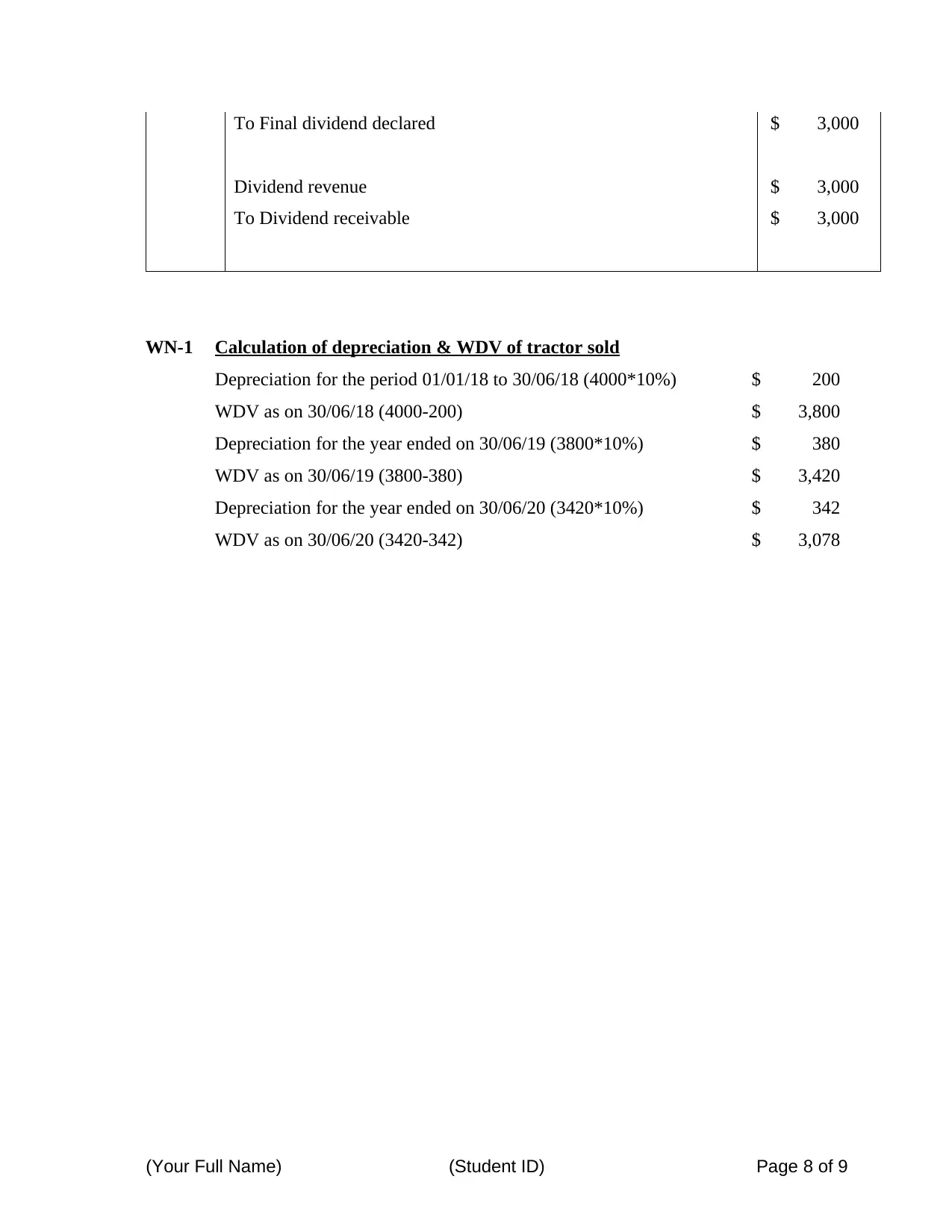

This assignment solution addresses issues related to Palvidia Ltd's decision to purchase shares in Soletta Ltd, covering the purpose of consolidated financial statements, the definition of group, parent, and subsidiary companies, and the treatment of intragroup transactions. It includes an acquisition analysis, consolidated worksheet entries for multiple periods, and detailed calculations for depreciation and the written down value of assets. The solution also eliminates profits from opening and closing inventory, addresses inter-company loan eliminations, and dividend distributions, providing a comprehensive guide to handling complex consolidation scenarios. Desklib offers a wealth of similar solved assignments and past papers to aid students in their studies.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.