ACCT20073 Company Accounting: Financial Statement Analysis Term 2 2018

VerifiedAdded on 2023/06/11

|11

|2366

|392

Homework Assignment

AI Summary

This assignment delves into various aspects of company accounting, focusing on the application of IAS 16 in determining the carrying amount of Property, Plant, and Equipment, emphasizing the separate depreciation of significant components and the inclusion of replacement costs and major inspection costs. It also explains Fair Value as the price in an orderly transaction between knowledgeable and willing participants, highlighting its importance in consolidation and compliance with IFRS 13. The assignment includes calculations and corrections of accounting treatments related to equipment depreciation and impairment, demonstrating the inaccuracies in the initial journal entries and providing the correct computations and journal entries for asset revaluation, depreciation, and impairment losses. It rectifies errors in impairment loss calculations and journal entries related to plant assets, providing corrected entries and calculations for accumulated depreciation, impairment loss, and subsequent depreciation charges, ensuring compliance with accounting standards. The document is a student contribution available on Desklib, a platform offering AI-powered study tools and a wide range of academic resources.

Running head: COMPANY ACCOUNTING

Company Accounting

Name of the Student:

Name of the University:

Author’s Note:

Company Accounting

Name of the Student:

Name of the University:

Author’s Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1COMPANY ACCOUNTING

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................2

Answer to Question 3:.....................................................................................................................2

Calculations:................................................................................................................................2

Answer to Question 4:.....................................................................................................................4

Requirement a:.............................................................................................................................4

Journal Entries:........................................................................................................................4

Calculation:..............................................................................................................................4

Requirement b:.............................................................................................................................5

Journal Entries:........................................................................................................................5

Calculation:..............................................................................................................................6

Answer to Question 5:.....................................................................................................................6

Requirement a:.............................................................................................................................6

Calculations:................................................................................................................................6

Requirement b:.............................................................................................................................7

Journal Entries:........................................................................................................................7

Calculation:..............................................................................................................................7

Requirement c:.............................................................................................................................7

Journal Entries:........................................................................................................................7

Calculation:..............................................................................................................................8

Answer to Question 6:.....................................................................................................................8

Journal Entries:........................................................................................................................8

Calculation:..............................................................................................................................9

Reference.......................................................................................................................................10

Table of Contents

Answer to Question 1:.....................................................................................................................2

Answer to Question 2:.....................................................................................................................2

Answer to Question 3:.....................................................................................................................2

Calculations:................................................................................................................................2

Answer to Question 4:.....................................................................................................................4

Requirement a:.............................................................................................................................4

Journal Entries:........................................................................................................................4

Calculation:..............................................................................................................................4

Requirement b:.............................................................................................................................5

Journal Entries:........................................................................................................................5

Calculation:..............................................................................................................................6

Answer to Question 5:.....................................................................................................................6

Requirement a:.............................................................................................................................6

Calculations:................................................................................................................................6

Requirement b:.............................................................................................................................7

Journal Entries:........................................................................................................................7

Calculation:..............................................................................................................................7

Requirement c:.............................................................................................................................7

Journal Entries:........................................................................................................................7

Calculation:..............................................................................................................................8

Answer to Question 6:.....................................................................................................................8

Journal Entries:........................................................................................................................8

Calculation:..............................................................................................................................9

Reference.......................................................................................................................................10

2COMPANY ACCOUNTING

Answer to Question 1:

The determination of carrying amount of Property, Plant and Equipment needs to be in

compliance with IAS 16 which deals with Property, Plants and Equipment. As per the provisions

which are stated in IAS 16.43, in case the business uses cost model, each part of the property,

plant and equipment with a cost which is considered to be significant in relation to the total cost

of the asset must be depreciated in a separate manner (André, Filip and Paugam 2015). The

carrying amount of an item of property, plant and equipment will be including the cost of

replacement for parts of the item depending on the recognition criteria. In addition to this, the

standard also provides cost of major inspections should also be recognised in the carrying

amount of the item of property, plant and equipment (Trifan and Anton 2014).

Answer to Question 2:

Fair Value can be described as the sale price at the buyers are willing to purchase the

asset and the sellers are also willing to sell the assets and it is assumed that the buyers and sellers

for the asset have adequate knowledge of the market conditions of the business (Blankespoor et

al. 2013). Fair value also represents the value of the assets and liabilities of a business in case of

consolidation of financial statements of the company. In accounting practice and principle, fair

value accounting is considered to be a valuation concept and the same is implemented by FASB

(Magnan, Menini and Parbonetti 2015). In accounting terms, fair value is used as a certainty of

the market value of an asset. As per US GAAP, fair value is the price at which the assets are

purchased or sold in an orderly fashion between participants of the transaction. When a business

is measuring fair value of an asset, assumption is made that the pricing of the asset and liabilities

are under current market conditions and also considers the risks which is associated with the

asset. As per the provision which is provided by IFRS 13, an entity is required to consider the

effects of credit risk while determining fair value measurement. The concept of fair value

measurement is very important in accounting process and measuring the value of the assets and

liabilities of the business.

Answer to Question 3:

Calculations:

a) Depreciation p.a. on Equipment:

Answer to Question 1:

The determination of carrying amount of Property, Plant and Equipment needs to be in

compliance with IAS 16 which deals with Property, Plants and Equipment. As per the provisions

which are stated in IAS 16.43, in case the business uses cost model, each part of the property,

plant and equipment with a cost which is considered to be significant in relation to the total cost

of the asset must be depreciated in a separate manner (André, Filip and Paugam 2015). The

carrying amount of an item of property, plant and equipment will be including the cost of

replacement for parts of the item depending on the recognition criteria. In addition to this, the

standard also provides cost of major inspections should also be recognised in the carrying

amount of the item of property, plant and equipment (Trifan and Anton 2014).

Answer to Question 2:

Fair Value can be described as the sale price at the buyers are willing to purchase the

asset and the sellers are also willing to sell the assets and it is assumed that the buyers and sellers

for the asset have adequate knowledge of the market conditions of the business (Blankespoor et

al. 2013). Fair value also represents the value of the assets and liabilities of a business in case of

consolidation of financial statements of the company. In accounting practice and principle, fair

value accounting is considered to be a valuation concept and the same is implemented by FASB

(Magnan, Menini and Parbonetti 2015). In accounting terms, fair value is used as a certainty of

the market value of an asset. As per US GAAP, fair value is the price at which the assets are

purchased or sold in an orderly fashion between participants of the transaction. When a business

is measuring fair value of an asset, assumption is made that the pricing of the asset and liabilities

are under current market conditions and also considers the risks which is associated with the

asset. As per the provision which is provided by IFRS 13, an entity is required to consider the

effects of credit risk while determining fair value measurement. The concept of fair value

measurement is very important in accounting process and measuring the value of the assets and

liabilities of the business.

Answer to Question 3:

Calculations:

a) Depreciation p.a. on Equipment:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3COMPANY ACCOUNTING

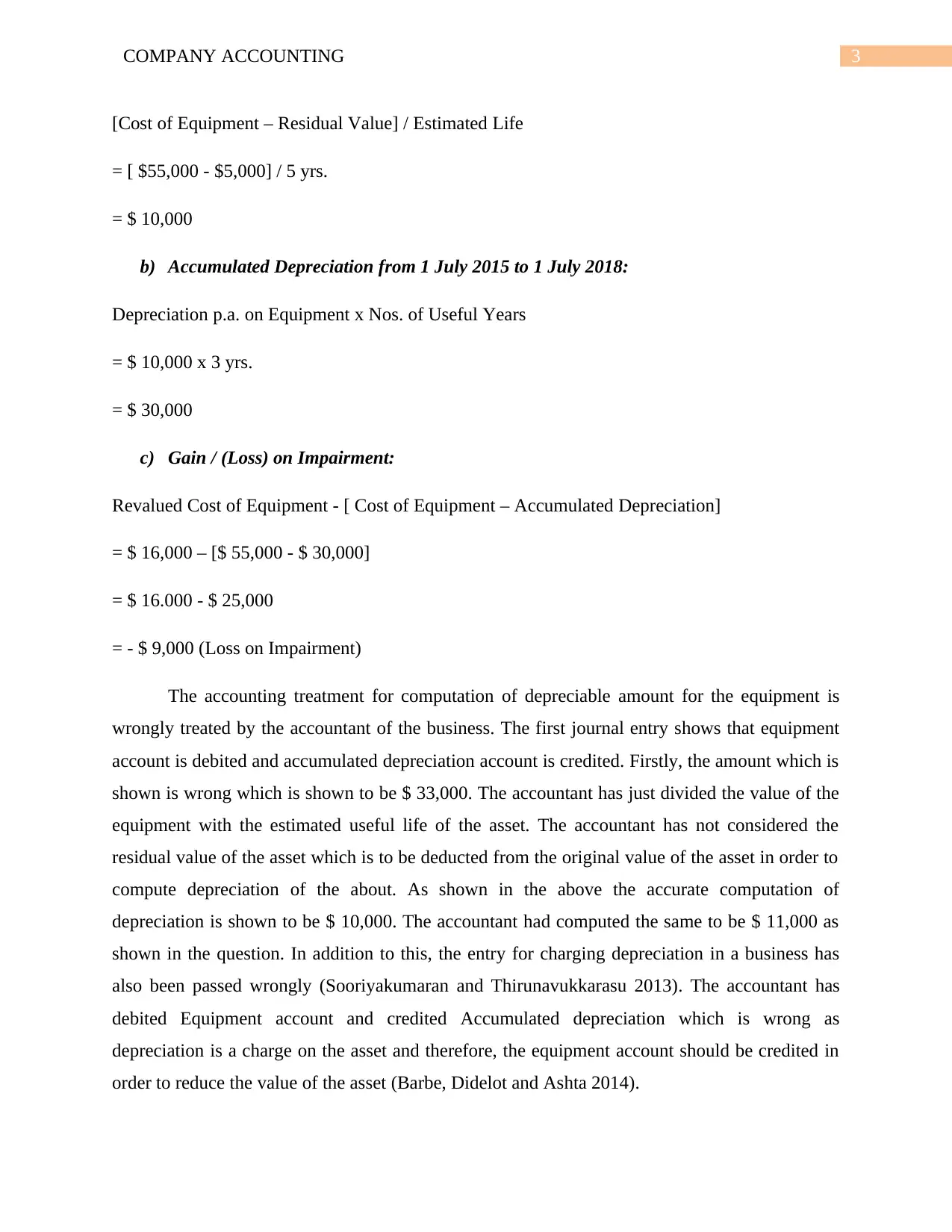

[Cost of Equipment – Residual Value] / Estimated Life

= [ $55,000 - $5,000] / 5 yrs.

= $ 10,000

b) Accumulated Depreciation from 1 July 2015 to 1 July 2018:

Depreciation p.a. on Equipment x Nos. of Useful Years

= $ 10,000 x 3 yrs.

= $ 30,000

c) Gain / (Loss) on Impairment:

Revalued Cost of Equipment - [ Cost of Equipment – Accumulated Depreciation]

= $ 16,000 – [$ 55,000 - $ 30,000]

= $ 16.000 - $ 25,000

= - $ 9,000 (Loss on Impairment)

The accounting treatment for computation of depreciable amount for the equipment is

wrongly treated by the accountant of the business. The first journal entry shows that equipment

account is debited and accumulated depreciation account is credited. Firstly, the amount which is

shown is wrong which is shown to be $ 33,000. The accountant has just divided the value of the

equipment with the estimated useful life of the asset. The accountant has not considered the

residual value of the asset which is to be deducted from the original value of the asset in order to

compute depreciation of the about. As shown in the above the accurate computation of

depreciation is shown to be $ 10,000. The accountant had computed the same to be $ 11,000 as

shown in the question. In addition to this, the entry for charging depreciation in a business has

also been passed wrongly (Sooriyakumaran and Thirunavukkarasu 2013). The accountant has

debited Equipment account and credited Accumulated depreciation which is wrong as

depreciation is a charge on the asset and therefore, the equipment account should be credited in

order to reduce the value of the asset (Barbe, Didelot and Ashta 2014).

[Cost of Equipment – Residual Value] / Estimated Life

= [ $55,000 - $5,000] / 5 yrs.

= $ 10,000

b) Accumulated Depreciation from 1 July 2015 to 1 July 2018:

Depreciation p.a. on Equipment x Nos. of Useful Years

= $ 10,000 x 3 yrs.

= $ 30,000

c) Gain / (Loss) on Impairment:

Revalued Cost of Equipment - [ Cost of Equipment – Accumulated Depreciation]

= $ 16,000 – [$ 55,000 - $ 30,000]

= $ 16.000 - $ 25,000

= - $ 9,000 (Loss on Impairment)

The accounting treatment for computation of depreciable amount for the equipment is

wrongly treated by the accountant of the business. The first journal entry shows that equipment

account is debited and accumulated depreciation account is credited. Firstly, the amount which is

shown is wrong which is shown to be $ 33,000. The accountant has just divided the value of the

equipment with the estimated useful life of the asset. The accountant has not considered the

residual value of the asset which is to be deducted from the original value of the asset in order to

compute depreciation of the about. As shown in the above the accurate computation of

depreciation is shown to be $ 10,000. The accountant had computed the same to be $ 11,000 as

shown in the question. In addition to this, the entry for charging depreciation in a business has

also been passed wrongly (Sooriyakumaran and Thirunavukkarasu 2013). The accountant has

debited Equipment account and credited Accumulated depreciation which is wrong as

depreciation is a charge on the asset and therefore, the equipment account should be credited in

order to reduce the value of the asset (Barbe, Didelot and Ashta 2014).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4COMPANY ACCOUNTING

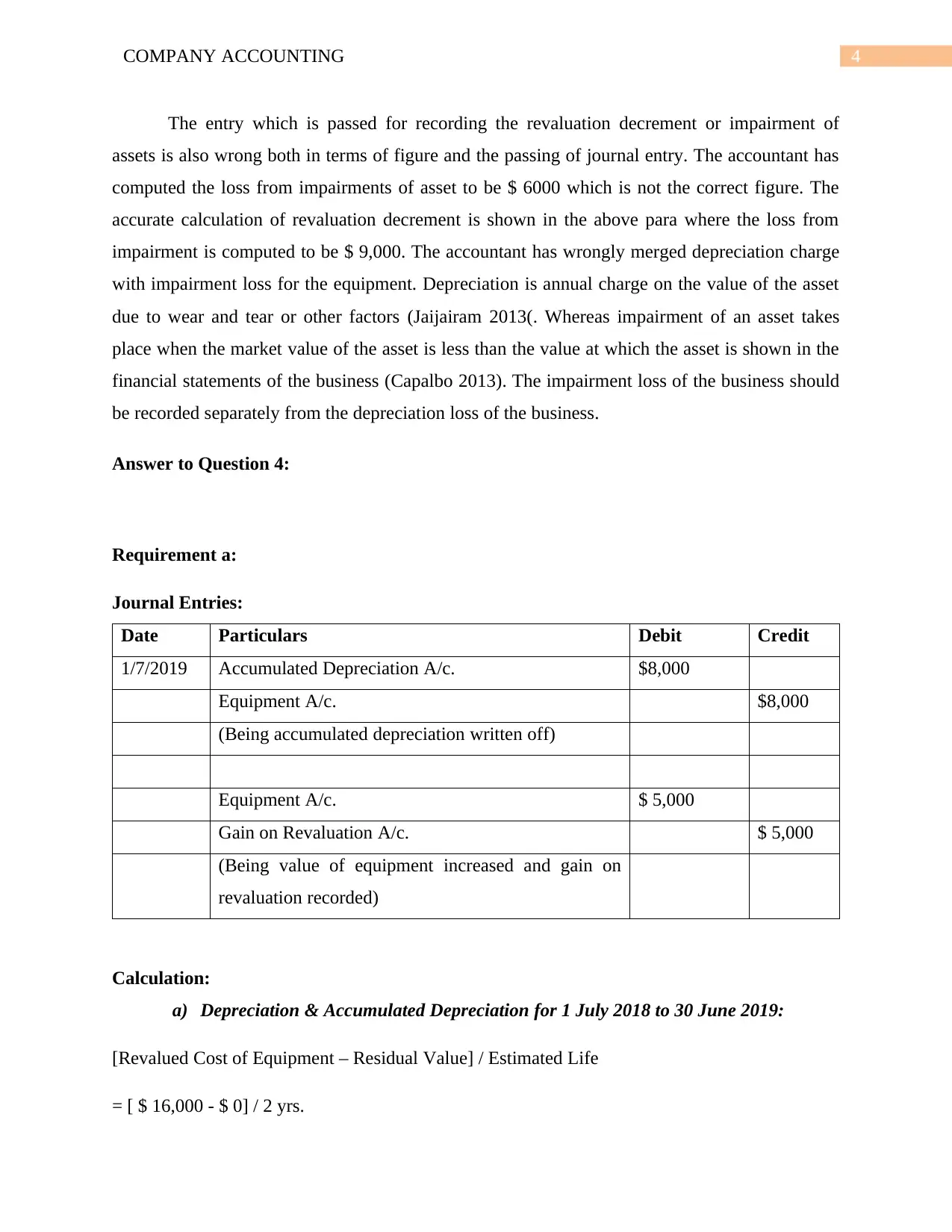

The entry which is passed for recording the revaluation decrement or impairment of

assets is also wrong both in terms of figure and the passing of journal entry. The accountant has

computed the loss from impairments of asset to be $ 6000 which is not the correct figure. The

accurate calculation of revaluation decrement is shown in the above para where the loss from

impairment is computed to be $ 9,000. The accountant has wrongly merged depreciation charge

with impairment loss for the equipment. Depreciation is annual charge on the value of the asset

due to wear and tear or other factors (Jaijairam 2013(. Whereas impairment of an asset takes

place when the market value of the asset is less than the value at which the asset is shown in the

financial statements of the business (Capalbo 2013). The impairment loss of the business should

be recorded separately from the depreciation loss of the business.

Answer to Question 4:

Requirement a:

Journal Entries:

Date Particulars Debit Credit

1/7/2019 Accumulated Depreciation A/c. $8,000

Equipment A/c. $8,000

(Being accumulated depreciation written off)

Equipment A/c. $ 5,000

Gain on Revaluation A/c. $ 5,000

(Being value of equipment increased and gain on

revaluation recorded)

Calculation:

a) Depreciation & Accumulated Depreciation for 1 July 2018 to 30 June 2019:

[Revalued Cost of Equipment – Residual Value] / Estimated Life

= [ $ 16,000 - $ 0] / 2 yrs.

The entry which is passed for recording the revaluation decrement or impairment of

assets is also wrong both in terms of figure and the passing of journal entry. The accountant has

computed the loss from impairments of asset to be $ 6000 which is not the correct figure. The

accurate calculation of revaluation decrement is shown in the above para where the loss from

impairment is computed to be $ 9,000. The accountant has wrongly merged depreciation charge

with impairment loss for the equipment. Depreciation is annual charge on the value of the asset

due to wear and tear or other factors (Jaijairam 2013(. Whereas impairment of an asset takes

place when the market value of the asset is less than the value at which the asset is shown in the

financial statements of the business (Capalbo 2013). The impairment loss of the business should

be recorded separately from the depreciation loss of the business.

Answer to Question 4:

Requirement a:

Journal Entries:

Date Particulars Debit Credit

1/7/2019 Accumulated Depreciation A/c. $8,000

Equipment A/c. $8,000

(Being accumulated depreciation written off)

Equipment A/c. $ 5,000

Gain on Revaluation A/c. $ 5,000

(Being value of equipment increased and gain on

revaluation recorded)

Calculation:

a) Depreciation & Accumulated Depreciation for 1 July 2018 to 30 June 2019:

[Revalued Cost of Equipment – Residual Value] / Estimated Life

= [ $ 16,000 - $ 0] / 2 yrs.

5COMPANY ACCOUNTING

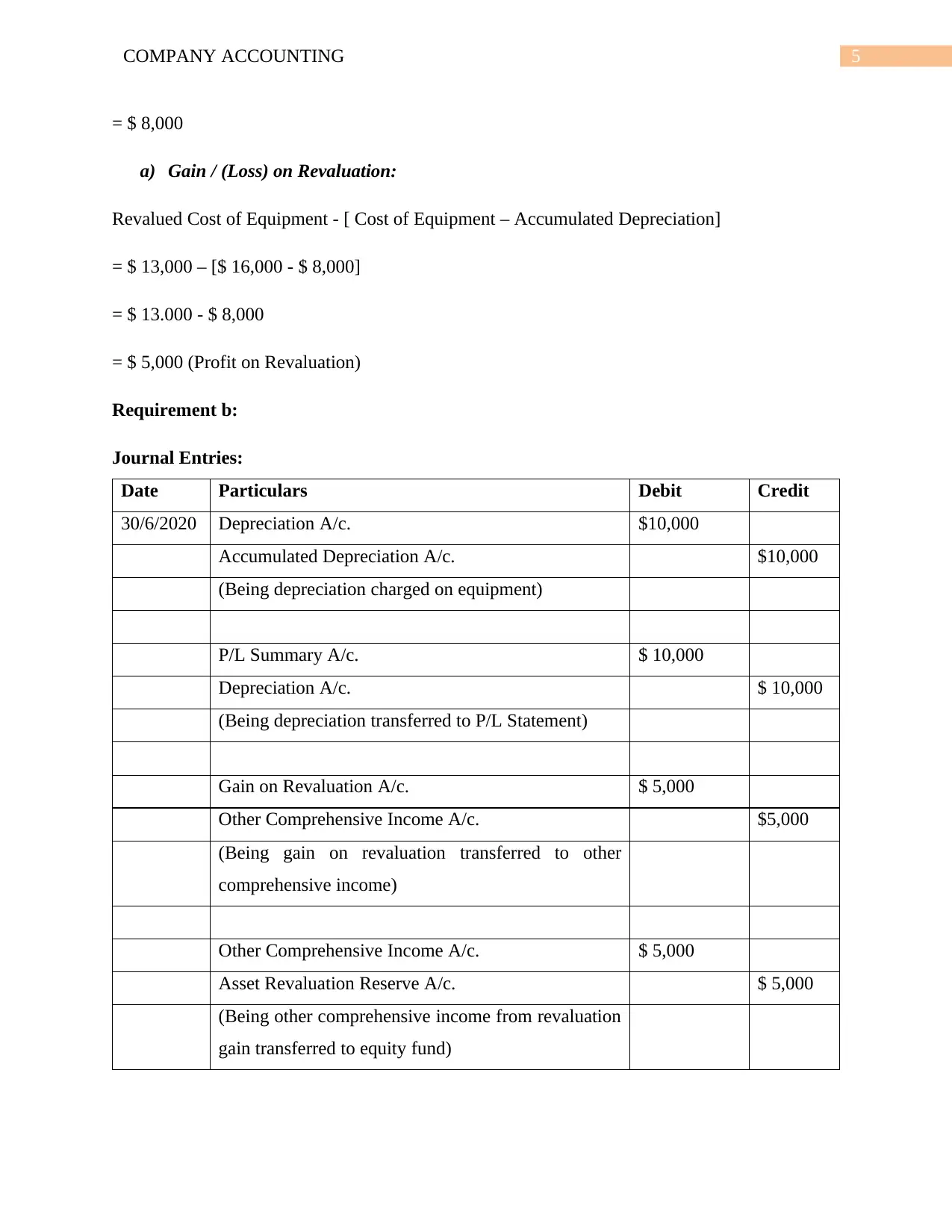

= $ 8,000

a) Gain / (Loss) on Revaluation:

Revalued Cost of Equipment - [ Cost of Equipment – Accumulated Depreciation]

= $ 13,000 – [$ 16,000 - $ 8,000]

= $ 13.000 - $ 8,000

= $ 5,000 (Profit on Revaluation)

Requirement b:

Journal Entries:

Date Particulars Debit Credit

30/6/2020 Depreciation A/c. $10,000

Accumulated Depreciation A/c. $10,000

(Being depreciation charged on equipment)

P/L Summary A/c. $ 10,000

Depreciation A/c. $ 10,000

(Being depreciation transferred to P/L Statement)

Gain on Revaluation A/c. $ 5,000

Other Comprehensive Income A/c. $5,000

(Being gain on revaluation transferred to other

comprehensive income)

Other Comprehensive Income A/c. $ 5,000

Asset Revaluation Reserve A/c. $ 5,000

(Being other comprehensive income from revaluation

gain transferred to equity fund)

= $ 8,000

a) Gain / (Loss) on Revaluation:

Revalued Cost of Equipment - [ Cost of Equipment – Accumulated Depreciation]

= $ 13,000 – [$ 16,000 - $ 8,000]

= $ 13.000 - $ 8,000

= $ 5,000 (Profit on Revaluation)

Requirement b:

Journal Entries:

Date Particulars Debit Credit

30/6/2020 Depreciation A/c. $10,000

Accumulated Depreciation A/c. $10,000

(Being depreciation charged on equipment)

P/L Summary A/c. $ 10,000

Depreciation A/c. $ 10,000

(Being depreciation transferred to P/L Statement)

Gain on Revaluation A/c. $ 5,000

Other Comprehensive Income A/c. $5,000

(Being gain on revaluation transferred to other

comprehensive income)

Other Comprehensive Income A/c. $ 5,000

Asset Revaluation Reserve A/c. $ 5,000

(Being other comprehensive income from revaluation

gain transferred to equity fund)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6COMPANY ACCOUNTING

Calculation:

a) Depreciation & Accumulated Depreciation for 1 July 2018 to 30 June 2019:

[Revalued Cost of Equipment – Residual Value] / Estimated Life

= [ $ 13,000 - $ 3,000] / 1 yrs.

= $ 10,000

Answer to Question 5:

Requirement a:

The accountant has wrongly passed the journal entry regarding impairment of assets of

the business. The accountant has debited impairment loss and credited accumulated depreciation.

The accountant has wrongly mixed up the impairment loss on the equipment with the charges of

depreciation which is clearly shown in the journal entry which is passed by the accountant. The

amount for the impairment loss which is computed by the accountant is shown to be $ 30,000

which is incorrect as well (Kulikova, Gubaidullina and Elsukova 2016). The accurate

calculations for the impairment loss which the business incurs on the equipment is shown below

and the same is shown by deducting the carrying cost of the plant from the revalued cost of the

plan and the same is shown to be $ 15,000. Therefore, the management needs to pass adjustment

entries for improving both the journal entry and also the amount which is shown as impairment

loss of the business (Amiraslani, Iatridis and Pope 2013). The revalued cost of the plant is shown

to be $ 225,000 and the carrying cost of the plant is shown to be $ 2,40,000. Therefore, the

provisions for impairments needs to be applied for which necessary adjustment entries regarding

impairments needs to be passed by the management.

Calculations:

a) Gain /(Loss) on Impairment:

Revalued Cost of Plant (Higher of Value in use & Fair Value, less, disposal) – Carrying Cost

of Plant

= $ 225,000 - $240, 000

Calculation:

a) Depreciation & Accumulated Depreciation for 1 July 2018 to 30 June 2019:

[Revalued Cost of Equipment – Residual Value] / Estimated Life

= [ $ 13,000 - $ 3,000] / 1 yrs.

= $ 10,000

Answer to Question 5:

Requirement a:

The accountant has wrongly passed the journal entry regarding impairment of assets of

the business. The accountant has debited impairment loss and credited accumulated depreciation.

The accountant has wrongly mixed up the impairment loss on the equipment with the charges of

depreciation which is clearly shown in the journal entry which is passed by the accountant. The

amount for the impairment loss which is computed by the accountant is shown to be $ 30,000

which is incorrect as well (Kulikova, Gubaidullina and Elsukova 2016). The accurate

calculations for the impairment loss which the business incurs on the equipment is shown below

and the same is shown by deducting the carrying cost of the plant from the revalued cost of the

plan and the same is shown to be $ 15,000. Therefore, the management needs to pass adjustment

entries for improving both the journal entry and also the amount which is shown as impairment

loss of the business (Amiraslani, Iatridis and Pope 2013). The revalued cost of the plant is shown

to be $ 225,000 and the carrying cost of the plant is shown to be $ 2,40,000. Therefore, the

provisions for impairments needs to be applied for which necessary adjustment entries regarding

impairments needs to be passed by the management.

Calculations:

a) Gain /(Loss) on Impairment:

Revalued Cost of Plant (Higher of Value in use & Fair Value, less, disposal) – Carrying Cost

of Plant

= $ 225,000 - $240, 000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7COMPANY ACCOUNTING

= - $15,000 (Loss on Impairment)

Requirement b:

Journal Entries:

Date Particulars Debit Credit

1/7/2017 Accumulated Depreciation A/c. $60,000

Plant A/c. $60,000

(Being accumulated depreciation written off)

Impairment Loss A/c. $ 15,000

Plant A/c. $ 15,000

(Being value of equipment decreased and loss on

impairment recorded)

Calculation:

a) Accumulated Depreciation of Plant:

Actual Cost of Plant – Carrying Cost of Plant

= $300,000 - $240,000

= $ 60,000

Requirement c:

Journal Entries:

Date Particulars Debit Credit

30/6/2018 Depreciation A/c. $22,500

Accumulated Depreciation A/c. $ 22,500

(Being depreciation charged on plant)

= - $15,000 (Loss on Impairment)

Requirement b:

Journal Entries:

Date Particulars Debit Credit

1/7/2017 Accumulated Depreciation A/c. $60,000

Plant A/c. $60,000

(Being accumulated depreciation written off)

Impairment Loss A/c. $ 15,000

Plant A/c. $ 15,000

(Being value of equipment decreased and loss on

impairment recorded)

Calculation:

a) Accumulated Depreciation of Plant:

Actual Cost of Plant – Carrying Cost of Plant

= $300,000 - $240,000

= $ 60,000

Requirement c:

Journal Entries:

Date Particulars Debit Credit

30/6/2018 Depreciation A/c. $22,500

Accumulated Depreciation A/c. $ 22,500

(Being depreciation charged on plant)

8COMPANY ACCOUNTING

P/L Summary A/c. $ 22,500

Depreciation A/c. $ 22,500

(Being depreciation and impairment loss transferred

to P/L Statement)

Other Comprehensive Income A/c. $ 15,000

Impairment Loss A/c. $ 15,000

(Being impairment loss transferred to other

comprehensive income)

Asset Revaluation Reserve A/c. $ 15,000

Other Comprehensive Income A/c. $ 15,000

(Being other comprehensive loss due to impairment

transferred to equity fund)

Calculation:

a) Depreciation from 1 July 2017 to 30 June 2018:

Revalued Cost of Equipment x Rate of Depreciation p.a.

= $ 225,000 x 10%

= $ 22,500

Answer to Question 6:

Journal Entries:

Date Particulars Debit Credit

1/7/2018 Accumulated Depreciation A/c. $ 22,500

Plant A/c. $ 22,500

(Being accumulated depreciation written off)

P/L Summary A/c. $ 22,500

Depreciation A/c. $ 22,500

(Being depreciation and impairment loss transferred

to P/L Statement)

Other Comprehensive Income A/c. $ 15,000

Impairment Loss A/c. $ 15,000

(Being impairment loss transferred to other

comprehensive income)

Asset Revaluation Reserve A/c. $ 15,000

Other Comprehensive Income A/c. $ 15,000

(Being other comprehensive loss due to impairment

transferred to equity fund)

Calculation:

a) Depreciation from 1 July 2017 to 30 June 2018:

Revalued Cost of Equipment x Rate of Depreciation p.a.

= $ 225,000 x 10%

= $ 22,500

Answer to Question 6:

Journal Entries:

Date Particulars Debit Credit

1/7/2018 Accumulated Depreciation A/c. $ 22,500

Plant A/c. $ 22,500

(Being accumulated depreciation written off)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9COMPANY ACCOUNTING

Plant A/c. $ 37,500

Gain on Revaluation A/c. $ 37,500

(Being value of equipment increased and gain on

revaluation recorded)

Calculation:

a) Gain/(Loss) on Revaluation of Plant:

Revalued Cost of Plant – [Cost of Plant – Accumulated Depreciation]

= $ 240,000 – [$ 225,000 - $ 22,500]

= $ 240,000 - $ 202,500

= $ 37,500

Plant A/c. $ 37,500

Gain on Revaluation A/c. $ 37,500

(Being value of equipment increased and gain on

revaluation recorded)

Calculation:

a) Gain/(Loss) on Revaluation of Plant:

Revalued Cost of Plant – [Cost of Plant – Accumulated Depreciation]

= $ 240,000 – [$ 225,000 - $ 22,500]

= $ 240,000 - $ 202,500

= $ 37,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10COMPANY ACCOUNTING

Reference

Amiraslani, H., Iatridis, G.E. and Pope, P.F., 2013. Accounting for asset impairment: a test for

IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

André, P., Filip, A. and Paugam, L., 2015. The effect of mandatory IFRS adoption on conditional

conservatism in Europe. Journal of Business Finance & Accounting, 42(3-4), pp.482-514.

Barbe, O., Didelot, L. and Ashta, A., 2014. From Disconnected to Integrated tax and financial

systems A post-IFRS evaluation of evolution of Tax and Financial Reporting relationships based

on the French case. Research in Accounting Regulation, 26(2), pp.242-256.

Blankespoor, E., Linsmeier, T.J., Petroni, K.R. and Shakespeare, C., 2013. Fair value accounting

for financial instruments: Does it improve the association between bank leverage and credit

risk?. The Accounting Review, 88(4), pp.1143-1177.

Capalbo, F., 2013. Impairment of Assets.

Jaijairam, P., 2013. Fair value accounting vs. historical cost accounting. The Review of Business

Information Systems (Online), 17(1), p.1.

Kulikova, L.I., Gubaidullina, A.R. and Elsukova, T.V., 2016. Disclosure of the risks of the

organization influencing decision making by users of financial reporting. International Business

Management, 10(22), pp.5280-5285.

Magnan, M., Menini, A. and Parbonetti, A., 2015. Fair value accounting: information or

confusion for financial markets?. Review of Accounting Studies, 20(1), pp.559-591.

Sooriyakumaran, L. and Thirunavukkarasu, V., 2013. Disclosures and impacts of impairment of

non-current assets in the financial statements: A study on listed manufacturing companies in

Colombo Stock Exchange (CSE) in Sri Lanka.

Trifan, A. and Anton, C., 2014. ACCOUNTING TREATMENT FOR PROPERTY, PLANT

AND EQUIPMENT REVALUATIONS. Management & Marketing, 9(2).

Reference

Amiraslani, H., Iatridis, G.E. and Pope, P.F., 2013. Accounting for asset impairment: a test for

IFRS compliance across Europe. Centre for Financial Analysis and Reporting Research

(CeFARR).

André, P., Filip, A. and Paugam, L., 2015. The effect of mandatory IFRS adoption on conditional

conservatism in Europe. Journal of Business Finance & Accounting, 42(3-4), pp.482-514.

Barbe, O., Didelot, L. and Ashta, A., 2014. From Disconnected to Integrated tax and financial

systems A post-IFRS evaluation of evolution of Tax and Financial Reporting relationships based

on the French case. Research in Accounting Regulation, 26(2), pp.242-256.

Blankespoor, E., Linsmeier, T.J., Petroni, K.R. and Shakespeare, C., 2013. Fair value accounting

for financial instruments: Does it improve the association between bank leverage and credit

risk?. The Accounting Review, 88(4), pp.1143-1177.

Capalbo, F., 2013. Impairment of Assets.

Jaijairam, P., 2013. Fair value accounting vs. historical cost accounting. The Review of Business

Information Systems (Online), 17(1), p.1.

Kulikova, L.I., Gubaidullina, A.R. and Elsukova, T.V., 2016. Disclosure of the risks of the

organization influencing decision making by users of financial reporting. International Business

Management, 10(22), pp.5280-5285.

Magnan, M., Menini, A. and Parbonetti, A., 2015. Fair value accounting: information or

confusion for financial markets?. Review of Accounting Studies, 20(1), pp.559-591.

Sooriyakumaran, L. and Thirunavukkarasu, V., 2013. Disclosures and impacts of impairment of

non-current assets in the financial statements: A study on listed manufacturing companies in

Colombo Stock Exchange (CSE) in Sri Lanka.

Trifan, A. and Anton, C., 2014. ACCOUNTING TREATMENT FOR PROPERTY, PLANT

AND EQUIPMENT REVALUATIONS. Management & Marketing, 9(2).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.