ACC80003 - Company Auditing: Impact of ASA on Auditor Reporting

VerifiedAdded on 2023/06/12

|14

|2792

|324

Report

AI Summary

This report examines the changes to auditor reporting introduced in Australia from December 15, 2016, by the International Auditing and Assurance Standards Board (IAASB), focusing on standards like ASA 701, ASA 705, ASA 706, and AASB 16. It discusses the impact of these changes on listed companies, emphasizing increased transparency and clarity for investors and stakeholders. The report also covers key audit matters (KAM), their identification, and areas of focus, such as going concern, impairment risks, and revenue recognition, referencing early adopters like Telstra. The analysis highlights how these standards enhance the qualitative characteristics of financial statements and improve communication between auditors and stakeholders, ensuring better-informed decision-making.

COMPANY AUDITING

ASSIGNMENT

ASSIGNMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

By student name

Professor

University

Date: 07 January 2018.

1 | P a g e

By student name

Professor

University

Date: 07 January 2018.

1 | P a g e

2

Executive Summary

In the given assignment, a report needs to be prepared on the changes that have been introduced by

the accounting boards and committees all over the world to improve the quality of reporting and

thereby auditing of the financials. The report specifically discusses on the changes in auditor reporting

brought upon by IFRS Board post 15th December 2016. These also include introduction of a couple of

accounting standards which have been discussed along with the benefits like how they contribute to the

better reporting and its transparency. Its impact on the listed companies and how the same is being

used by the different auditors has also been discussed.

2 | P a g e

Executive Summary

In the given assignment, a report needs to be prepared on the changes that have been introduced by

the accounting boards and committees all over the world to improve the quality of reporting and

thereby auditing of the financials. The report specifically discusses on the changes in auditor reporting

brought upon by IFRS Board post 15th December 2016. These also include introduction of a couple of

accounting standards which have been discussed along with the benefits like how they contribute to the

better reporting and its transparency. Its impact on the listed companies and how the same is being

used by the different auditors has also been discussed.

2 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

Contents

Introduction.................................................................................................................................................4

Analysis........................................................................................................................................................4

ASA 701: Key Audit Matters om auditors reports and its impact............................................................4

Other new audit reporting rules..............................................................................................................5

Key audit matters: Use and how to identify............................................................................................8

Areas of KAM...........................................................................................................................................8

Early adopters of auditors' reports..........................................................................................................9

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

3 | P a g e

Contents

Introduction.................................................................................................................................................4

Analysis........................................................................................................................................................4

ASA 701: Key Audit Matters om auditors reports and its impact............................................................4

Other new audit reporting rules..............................................................................................................5

Key audit matters: Use and how to identify............................................................................................8

Areas of KAM...........................................................................................................................................8

Early adopters of auditors' reports..........................................................................................................9

Conclusion.................................................................................................................................................13

References.................................................................................................................................................14

3 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

Introduction

In the recent past, various accounting standards have been introduced and many accounting reforms

have also been introduced to improve the quality of reporting by the management of the company and

also to improve the level and quality of auditing by the auditors so that the transparency of the financial

statements can be improved. These include more stress on the corporate governance so that the users

are well informed of the company practices, enhanced disclosure norms and better presentation

techniques (Alexander, 2016). The same has been discussed in the analysis section of the assignment

using the Annual report of one of the companies which was the early adopters of all these changes,

Telstra Limited.

Telstra is one of the widely known telecommunication companies in Australia and deals in setting up and

operating telecommunication networks, internets, mobile network, voice and other entertainment

products and services. It is listed on the Australian Stock Exchange and is now fully privatised employing

more than 36000 employees (Belton, 2017).

Analysis

ASA 701: Key Audit Matters om auditors reports and its impact

Among the changes that were introduced post 15th December 2016, the most eminent were ASA 701

which discusses on communicating key audit matters in the independent auditors report. This further

includes reporting of the crucial and material matters to those charged with governance and disclosing

the material misstatements and significant risks , if any in accordance with ASA 315. Also, the ASA

focuses on disclosing the significant management decisions, judgements and estiamtes, if any with

respect to the accounting treatment and policies (Bizfluent, 2017). It also focuses on mentioning the

4 | P a g e

Introduction

In the recent past, various accounting standards have been introduced and many accounting reforms

have also been introduced to improve the quality of reporting by the management of the company and

also to improve the level and quality of auditing by the auditors so that the transparency of the financial

statements can be improved. These include more stress on the corporate governance so that the users

are well informed of the company practices, enhanced disclosure norms and better presentation

techniques (Alexander, 2016). The same has been discussed in the analysis section of the assignment

using the Annual report of one of the companies which was the early adopters of all these changes,

Telstra Limited.

Telstra is one of the widely known telecommunication companies in Australia and deals in setting up and

operating telecommunication networks, internets, mobile network, voice and other entertainment

products and services. It is listed on the Australian Stock Exchange and is now fully privatised employing

more than 36000 employees (Belton, 2017).

Analysis

ASA 701: Key Audit Matters om auditors reports and its impact

Among the changes that were introduced post 15th December 2016, the most eminent were ASA 701

which discusses on communicating key audit matters in the independent auditors report. This further

includes reporting of the crucial and material matters to those charged with governance and disclosing

the material misstatements and significant risks , if any in accordance with ASA 315. Also, the ASA

focuses on disclosing the significant management decisions, judgements and estiamtes, if any with

respect to the accounting treatment and policies (Bizfluent, 2017). It also focuses on mentioning the

4 | P a g e

5

significant events and transactions that occure between the period of financial year closure and the roll

out of the annual report. This will help the investors to be informed of the latest details about the

company and thereby help them in taking informed decisions. The committee has alos clarified the

point that highlighting the key audit matters is not a substitute for expressing a modified opinion in case

the financial statements are not being able to meet the minimum standards. However, few exceptions

have been given where the auditor need not report the key audit matters in the auditor’s report, some

of them include those prohibited by law or regulation or those which can be in adverse public interest.

There is a great change in the scope of the audit which focuses on both the qualitative as well as

quantitative aspect such a relative magnitude, nature and effect of the audit report on users (Chron,

2017). The definition of the key audit matters as mentioned in the standard has been shown below:

Other new audit reporting rules

ASA 705 requires the auditor to mention the reason for giving out an adverse or qualified opinion on the

financial statements and its brief description which will help the user to understand the intended users

to understand and identify such circumstances when it may occur. Separating this communication in th

auditors report from the key audit matter gives more prominence and importance to the audot report,

thereby clarifying that both of these are separate issues and the auditor will be required to report key

audit matters even if the auditor gives the adverse or qualified opinion (DeZoort & Harrison, 2016).

ASA 706 which has also been introduced during this period establishes additional mechanisms for the

auditors to include in the audit report “emphasis on matter paragraph and Other relevant matters

paragraph” whevever it considers the same necessary. The standard mentions this to be different from

5 | P a g e

significant events and transactions that occure between the period of financial year closure and the roll

out of the annual report. This will help the investors to be informed of the latest details about the

company and thereby help them in taking informed decisions. The committee has alos clarified the

point that highlighting the key audit matters is not a substitute for expressing a modified opinion in case

the financial statements are not being able to meet the minimum standards. However, few exceptions

have been given where the auditor need not report the key audit matters in the auditor’s report, some

of them include those prohibited by law or regulation or those which can be in adverse public interest.

There is a great change in the scope of the audit which focuses on both the qualitative as well as

quantitative aspect such a relative magnitude, nature and effect of the audit report on users (Chron,

2017). The definition of the key audit matters as mentioned in the standard has been shown below:

Other new audit reporting rules

ASA 705 requires the auditor to mention the reason for giving out an adverse or qualified opinion on the

financial statements and its brief description which will help the user to understand the intended users

to understand and identify such circumstances when it may occur. Separating this communication in th

auditors report from the key audit matter gives more prominence and importance to the audot report,

thereby clarifying that both of these are separate issues and the auditor will be required to report key

audit matters even if the auditor gives the adverse or qualified opinion (DeZoort & Harrison, 2016).

ASA 706 which has also been introduced during this period establishes additional mechanisms for the

auditors to include in the audit report “emphasis on matter paragraph and Other relevant matters

paragraph” whevever it considers the same necessary. The standard mentions this to be different from

5 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

the key audit matters. The standard also gives a note and mentions the areas which require the specific

attention of the auditors like the risk based areas and identifying the chances of the material

misstatements in the financial reports. The planning and performance of the audit procedures should be

done based on the assessed risk of material misstatement in a particular class of accounts or

transactions and the same needs to be defined at the assesrtion level only (Dichev, 2017). The standard

also requires the auditors to focus on the complex and areas where the management has applied some

judgements and estimations.

The AASB has also brought about changes in the leasing standard AASB 16. Effective in the coming

period, most of the companies would have to report the operating leases on the Balance Sheet. This has

brought about a major change as earlier a lot of companies which were having all its working capital and

assets/ property in the form of the operating leases did not show the liability in the balance sheet but

ideally it is a part of the loan. Now the standard has done away with all the differences uin between the

operating leases and the financial leases and now the company will have to report the opeartibg leases

as well in the financial statements. This will bring a major change in the reporting for the different

companies as now the companies which were being casted as debt free in the balance shetet will now

be heavily loaded with the debt (Félix, 2017). This will not only ensure better transparency of the

accounts but also will let the users of financial statements know about the company’s lease

commitments, the true gearing ratio and the debt liability. The lessor accounting as per AASB 117 will

largely be unchanged. Due to the above changes, a great deal of financial and operational challenges are

expected to come in way besides the financial reporting and therefore auditors need to have a check on

the internal controls of the companies, their leasing judgements, the basis, debt covenants, credit

ratings, impairment testing, etc. The auditors will also get an opportunity to check the IT systems and

whether or not they are efficient enough for the companies to capture the above changes.

6 | P a g e

the key audit matters. The standard also gives a note and mentions the areas which require the specific

attention of the auditors like the risk based areas and identifying the chances of the material

misstatements in the financial reports. The planning and performance of the audit procedures should be

done based on the assessed risk of material misstatement in a particular class of accounts or

transactions and the same needs to be defined at the assesrtion level only (Dichev, 2017). The standard

also requires the auditors to focus on the complex and areas where the management has applied some

judgements and estimations.

The AASB has also brought about changes in the leasing standard AASB 16. Effective in the coming

period, most of the companies would have to report the operating leases on the Balance Sheet. This has

brought about a major change as earlier a lot of companies which were having all its working capital and

assets/ property in the form of the operating leases did not show the liability in the balance sheet but

ideally it is a part of the loan. Now the standard has done away with all the differences uin between the

operating leases and the financial leases and now the company will have to report the opeartibg leases

as well in the financial statements. This will bring a major change in the reporting for the different

companies as now the companies which were being casted as debt free in the balance shetet will now

be heavily loaded with the debt (Félix, 2017). This will not only ensure better transparency of the

accounts but also will let the users of financial statements know about the company’s lease

commitments, the true gearing ratio and the debt liability. The lessor accounting as per AASB 117 will

largely be unchanged. Due to the above changes, a great deal of financial and operational challenges are

expected to come in way besides the financial reporting and therefore auditors need to have a check on

the internal controls of the companies, their leasing judgements, the basis, debt covenants, credit

ratings, impairment testing, etc. The auditors will also get an opportunity to check the IT systems and

whether or not they are efficient enough for the companies to capture the above changes.

6 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

Besides introduction of the new standard ASA 701, necessary amendments were also carried out in

many accounting standards to ensure that all that is necessary are reported to those charged with

governance like the directors, the key managements personnels and so on (Heminway, 2017). All this

was aimed at increasing the communicating power of the auditor’s report and hence the changes were

introduced to make the users well informed of most of the aspects and share as much infimration as it is

possible and viable. This approach of AUASB is more in line with the approach of International Standards

of Auditing Board which most of the companies are following. These changes have been termed as

revolutionary as it will bring about a massive change in the investors point of view as well as other

stakeholders (Jones, 2017).

Some of the other changes to the existing accounting standards include ASA 700 as per which the

format of the audit report has been changed bringing the audit opinion to the front page to make it

more concise and understandable and thereby enhancing the qualitative characteristics of the financial

statements. ASA 570 which deals with the Going concern concept has now to be reported in the audit

report wherever there is uncertainity over going concern of the company. It also states whaat are the

changes in the work effort required to check on the going concern assumption of the client. Auditors can

also now include in the audit report any work conducted on any other information of the company in

one of the separate sections (Visinescu, et al., 2017). The Auditors responsibilities have also undergone

some change mentioning which specific standards needs to be compulsorily followed and enhanced

description of the responsibilities.

7 | P a g e

Besides introduction of the new standard ASA 701, necessary amendments were also carried out in

many accounting standards to ensure that all that is necessary are reported to those charged with

governance like the directors, the key managements personnels and so on (Heminway, 2017). All this

was aimed at increasing the communicating power of the auditor’s report and hence the changes were

introduced to make the users well informed of most of the aspects and share as much infimration as it is

possible and viable. This approach of AUASB is more in line with the approach of International Standards

of Auditing Board which most of the companies are following. These changes have been termed as

revolutionary as it will bring about a massive change in the investors point of view as well as other

stakeholders (Jones, 2017).

Some of the other changes to the existing accounting standards include ASA 700 as per which the

format of the audit report has been changed bringing the audit opinion to the front page to make it

more concise and understandable and thereby enhancing the qualitative characteristics of the financial

statements. ASA 570 which deals with the Going concern concept has now to be reported in the audit

report wherever there is uncertainity over going concern of the company. It also states whaat are the

changes in the work effort required to check on the going concern assumption of the client. Auditors can

also now include in the audit report any work conducted on any other information of the company in

one of the separate sections (Visinescu, et al., 2017). The Auditors responsibilities have also undergone

some change mentioning which specific standards needs to be compulsorily followed and enhanced

description of the responsibilities.

7 | P a g e

8

Key audit matters: Use and how to identify

Discussing on the key audit matters, the objective of the same is to ensure greater transparency of the

audit performed and accounting standards which were being used in checking and mitigating the risks. It

also aims to provide that information of the users of financial statements where the auditors

independent professional judgement has been involved in the current period. The next question is how

to identify the key audit issues? The same has also been mentioned as auditor will identify the key audit

findungs and discuss the same with the Audit committee and those charged with governance out of

which few topics or areas will be selected as those which require “significant auditor attention” (Kuhn &

Morris, 2016). This are areas which pose a risk or for which the auditor has not been able to find the

sufficient audit evidences or where the auditor is finding it difficult to form an opinion in absence of

conlusive evidences. All these matters are generally rare situations where there is huge complexity

involved and thereby complex auditor and management judgements. These are then to be reported in

the auditors report.

Areas of KAM

Some of common areas of KAM and auditors focus include:

1. Going concern

2. Risks of Impairment

3. Revenue Recognition

4. Legal, regulatory and taxation affairs

5. Weaknesses in the internal control having impact on the other areas

6. Acquisition and disposal of investments

8 | P a g e

Key audit matters: Use and how to identify

Discussing on the key audit matters, the objective of the same is to ensure greater transparency of the

audit performed and accounting standards which were being used in checking and mitigating the risks. It

also aims to provide that information of the users of financial statements where the auditors

independent professional judgement has been involved in the current period. The next question is how

to identify the key audit issues? The same has also been mentioned as auditor will identify the key audit

findungs and discuss the same with the Audit committee and those charged with governance out of

which few topics or areas will be selected as those which require “significant auditor attention” (Kuhn &

Morris, 2016). This are areas which pose a risk or for which the auditor has not been able to find the

sufficient audit evidences or where the auditor is finding it difficult to form an opinion in absence of

conlusive evidences. All these matters are generally rare situations where there is huge complexity

involved and thereby complex auditor and management judgements. These are then to be reported in

the auditors report.

Areas of KAM

Some of common areas of KAM and auditors focus include:

1. Going concern

2. Risks of Impairment

3. Revenue Recognition

4. Legal, regulatory and taxation affairs

5. Weaknesses in the internal control having impact on the other areas

6. Acquisition and disposal of investments

8 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

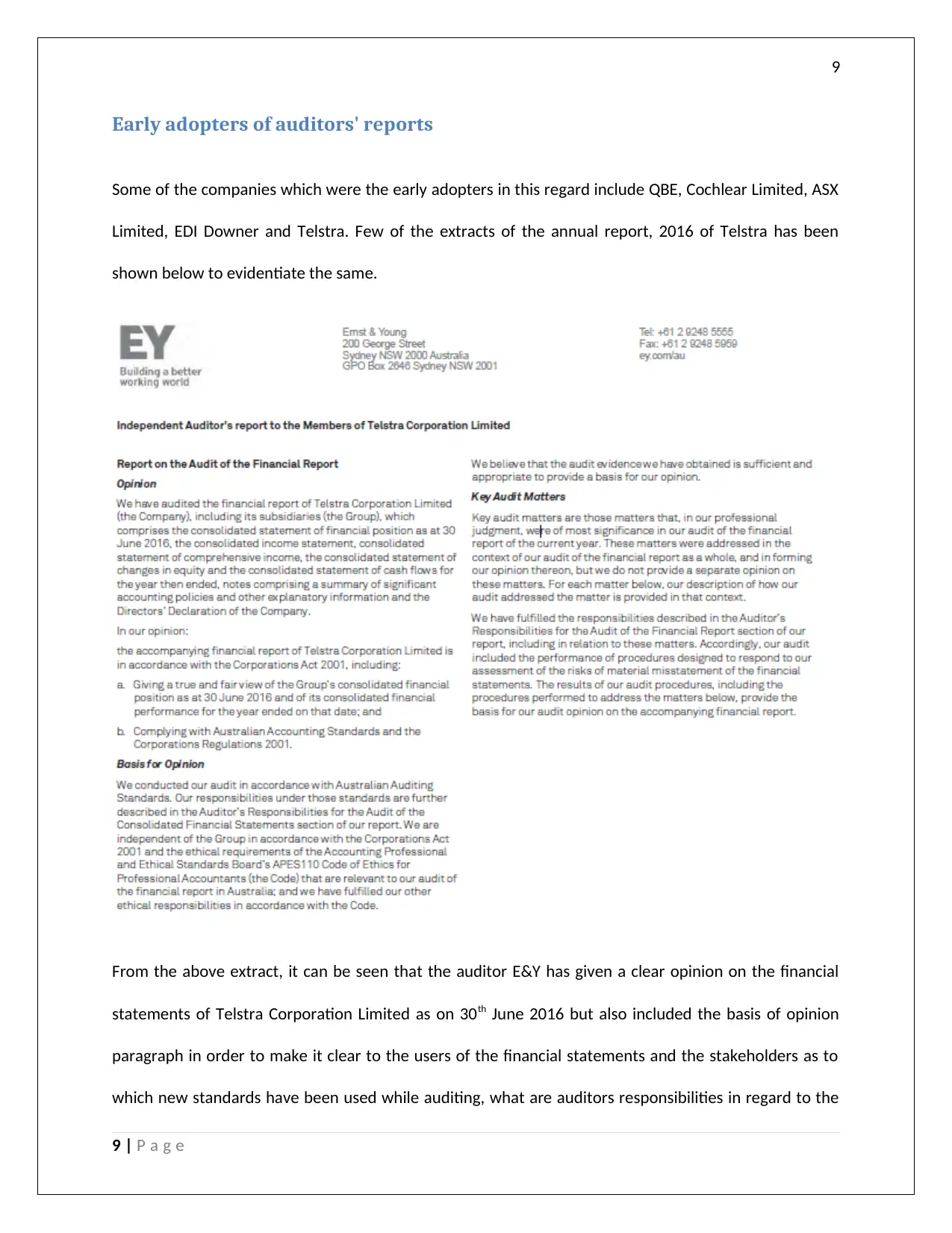

Early adopters of auditors' reports

Some of the companies which were the early adopters in this regard include QBE, Cochlear Limited, ASX

Limited, EDI Downer and Telstra. Few of the extracts of the annual report, 2016 of Telstra has been

shown below to evidentiate the same.

From the above extract, it can be seen that the auditor E&Y has given a clear opinion on the financial

statements of Telstra Corporation Limited as on 30th June 2016 but also included the basis of opinion

paragraph in order to make it clear to the users of the financial statements and the stakeholders as to

which new standards have been used while auditing, what are auditors responsibilities in regard to the

9 | P a g e

Early adopters of auditors' reports

Some of the companies which were the early adopters in this regard include QBE, Cochlear Limited, ASX

Limited, EDI Downer and Telstra. Few of the extracts of the annual report, 2016 of Telstra has been

shown below to evidentiate the same.

From the above extract, it can be seen that the auditor E&Y has given a clear opinion on the financial

statements of Telstra Corporation Limited as on 30th June 2016 but also included the basis of opinion

paragraph in order to make it clear to the users of the financial statements and the stakeholders as to

which new standards have been used while auditing, what are auditors responsibilities in regard to the

9 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

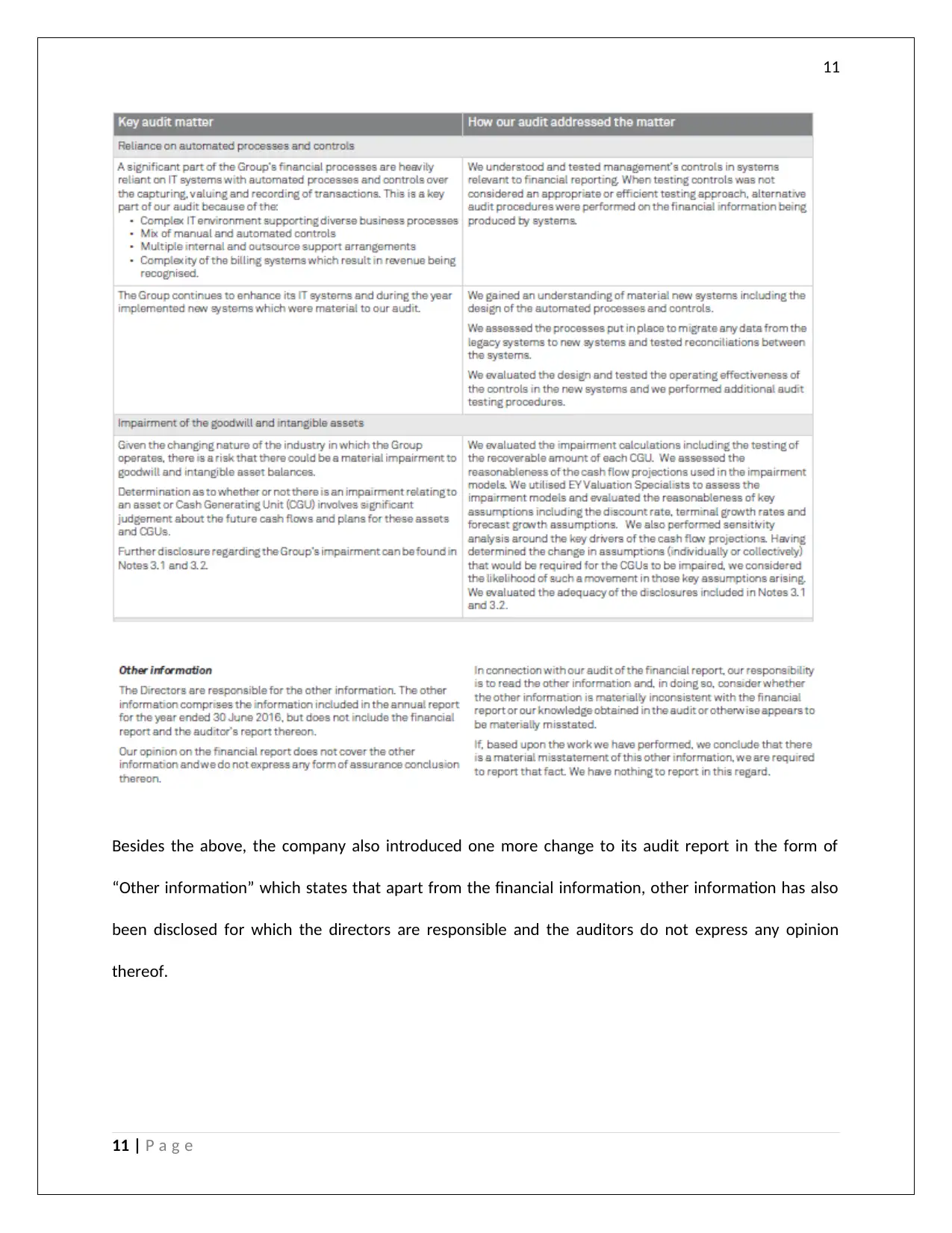

financials, and they are independent and have followed the ethical code of conduct while auditing. They

has also include a separate paragraph for key audit matters which was was the change introduced post

15th December 2016 (Knechel & Salterio, 2016). It says what were the key matters involved, how they

were being identified and how they were being addressed in forming the audit opinion and giving a

reasonable assurance to the users that the accounts are free fro material misstatements. Some

examples of key audit matters include revenue recognition, reliance being placed by the management

on the automated controls and processes, impairment of the goodwill and the intangibles, employee

retirements and employee benefits, etc like shown below.

The auditor mentions that in order to overcome thses risks, test of control and test of designs of the

internal control were being checked and operating effectiveness of the IT system was also being tested.

Furthermore, to ensure that the calculations of the impairment was satisfactory, teh auditors also

employed the use of EY valuation experts to check the reasonableness of the key assumptions. The team

also made use of the actuarial experts to check where the external valuation of retirement benefits of

the employees is satisfactory and good to go ahead (Sithole, et al., 2017).

10 | P a g e

financials, and they are independent and have followed the ethical code of conduct while auditing. They

has also include a separate paragraph for key audit matters which was was the change introduced post

15th December 2016 (Knechel & Salterio, 2016). It says what were the key matters involved, how they

were being identified and how they were being addressed in forming the audit opinion and giving a

reasonable assurance to the users that the accounts are free fro material misstatements. Some

examples of key audit matters include revenue recognition, reliance being placed by the management

on the automated controls and processes, impairment of the goodwill and the intangibles, employee

retirements and employee benefits, etc like shown below.

The auditor mentions that in order to overcome thses risks, test of control and test of designs of the

internal control were being checked and operating effectiveness of the IT system was also being tested.

Furthermore, to ensure that the calculations of the impairment was satisfactory, teh auditors also

employed the use of EY valuation experts to check the reasonableness of the key assumptions. The team

also made use of the actuarial experts to check where the external valuation of retirement benefits of

the employees is satisfactory and good to go ahead (Sithole, et al., 2017).

10 | P a g e

11

Besides the above, the company also introduced one more change to its audit report in the form of

“Other information” which states that apart from the financial information, other information has also

been disclosed for which the directors are responsible and the auditors do not express any opinion

thereof.

11 | P a g e

Besides the above, the company also introduced one more change to its audit report in the form of

“Other information” which states that apart from the financial information, other information has also

been disclosed for which the directors are responsible and the auditors do not express any opinion

thereof.

11 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.