Origin Energy Financial Performance Analysis - HI5002 Report

VerifiedAdded on 2023/03/17

|24

|5882

|93

Report

AI Summary

This report provides a comprehensive financial analysis of Origin Energy, an ASX-listed energy company, examining its performance over three financial years. The analysis includes an overview of Origin Energy's operations and competitive advantages, followed by an evaluation of its financial performance using profitability and operational efficiency ratios. A sensitivity analysis is conducted to assess market sensitivity, alongside the calculation of the dividend payout ratio. The report also identifies marketable securities and assesses both systematic and unsystematic risks associated with the business. The findings indicate that the company's current profitability is not strong, and the report does not recommend investment based on its dividend payout and earnings per share ratio.

Company Performance Analysis: Origin Energy

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Abstract

This report has been prepare din the context of examining the annual reports of a selected

ASX listed entity over the past three financial years. As such, it has initially discussed the

operation and comparative advantage of the selected company. It has them undertaken the

examination of its financial performance over the period by calculation and interpretation of the

profitability and operational efficiency ratios. The sensitivity analysis has also been done to

evaluate the market sensitivity of the company. This is followed by calculation of dividend

payout ratio, identification of marketable securities and examination of the systematic and

unsystematic risks related with the business operations. It has been indicated that the company is

not in a good state of profitability in the present and is not recommended to the investors to

invest within the company on the basis of its dividend payout and earnings per share ratio.

2

This report has been prepare din the context of examining the annual reports of a selected

ASX listed entity over the past three financial years. As such, it has initially discussed the

operation and comparative advantage of the selected company. It has them undertaken the

examination of its financial performance over the period by calculation and interpretation of the

profitability and operational efficiency ratios. The sensitivity analysis has also been done to

evaluate the market sensitivity of the company. This is followed by calculation of dividend

payout ratio, identification of marketable securities and examination of the systematic and

unsystematic risks related with the business operations. It has been indicated that the company is

not in a good state of profitability in the present and is not recommended to the investors to

invest within the company on the basis of its dividend payout and earnings per share ratio.

2

Contents

Part I: Introduction...........................................................................................................................4

Part II: Financial Analysis of selected company (All these parts will provide in detail in complete

file)...................................................................................................................................................4

2.1: Description of the company..................................................................................................4

2.2: Use of Ratio Analysis to evaluate the financial performance of Origin Energy..................5

Profitability Ratios of Origin Energy.......................................................................................5

Operating Efficiency Ratios.....................................................................................................8

2.3: Management of cash through of marketable securities by Origin Energy..........................10

2.4: Sensitivity Analysis of the given data.................................................................................11

2.5: Risk Analysis (Systematic and Unsystematic Risk)...........................................................16

Systematic risks......................................................................................................................17

Unsystematic risk...................................................................................................................18

2.6: Dividend Payout Ratio and dividend policy adopted by Origin Energy............................19

Part III: Recommendation Letter...................................................................................................19

Part IV: Conclusion.......................................................................................................................20

References......................................................................................................................................21

Appendix........................................................................................................................................22

3

Part I: Introduction...........................................................................................................................4

Part II: Financial Analysis of selected company (All these parts will provide in detail in complete

file)...................................................................................................................................................4

2.1: Description of the company..................................................................................................4

2.2: Use of Ratio Analysis to evaluate the financial performance of Origin Energy..................5

Profitability Ratios of Origin Energy.......................................................................................5

Operating Efficiency Ratios.....................................................................................................8

2.3: Management of cash through of marketable securities by Origin Energy..........................10

2.4: Sensitivity Analysis of the given data.................................................................................11

2.5: Risk Analysis (Systematic and Unsystematic Risk)...........................................................16

Systematic risks......................................................................................................................17

Unsystematic risk...................................................................................................................18

2.6: Dividend Payout Ratio and dividend policy adopted by Origin Energy............................19

Part III: Recommendation Letter...................................................................................................19

Part IV: Conclusion.......................................................................................................................20

References......................................................................................................................................21

Appendix........................................................................................................................................22

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part I: Introduction

Potential investor’s require detailed examination of the company financial performance

before making the valuable decision of investing the funds and becoming the shareholder. In

order to analyse the company financial performance there is need to evaluate lot of financial data

present in the annual reports of the company. It is the responsibility of company’s management

to prepare and publish their annual reports so that investors can use them for analyzing the

financial performance of the company. Investment decision requires investing of current funds

into the long term project to earn the best holding period returns and it is the reason why

evaluation of financial information becomes very important for success of such investment

opportunities. The conception of financial information implies all such information that have

been presented in the audited financial statements of an organization that can be used to ascertain

the financial performance and financial position of such company which investors seeks to make

investment. So it is highly important that appropriate financial tool must be used to evaluate the

financial performance of the company.

The purpose of this report is to analyse the financial performance of one of company

listed on ASX. The aim is to provide the investment advice to potential the investor who seeks to

make investment in the selected company. The company selected for the purpose of analysis is

Origin Energy. Origin Energy deals electricity, natural gas, solar, and LPG and this company is

listed on ASX. Comprehensive examination of the firm’s financial performance has been

performed based on the latest financial statements of Origin Energy. Annual reports of last three

years has been extracted from the investor’s relation section of the company and based on that

financial analyse has been performed. Financial tools used to evaluate the financial statements of

Origin Energy include ratio analysis, cash management analysis, risk analysis and dividend

performance.

Part II: Financial Analysis of selected company (All these parts will provide in detail in

complete file)

2.1: Description of the company

Origin Energy is a publicly listed energy company of Australia that has been

headquartered within Sydney and is traded on Australian Stock Exchange (ASX). It is an

4

Potential investor’s require detailed examination of the company financial performance

before making the valuable decision of investing the funds and becoming the shareholder. In

order to analyse the company financial performance there is need to evaluate lot of financial data

present in the annual reports of the company. It is the responsibility of company’s management

to prepare and publish their annual reports so that investors can use them for analyzing the

financial performance of the company. Investment decision requires investing of current funds

into the long term project to earn the best holding period returns and it is the reason why

evaluation of financial information becomes very important for success of such investment

opportunities. The conception of financial information implies all such information that have

been presented in the audited financial statements of an organization that can be used to ascertain

the financial performance and financial position of such company which investors seeks to make

investment. So it is highly important that appropriate financial tool must be used to evaluate the

financial performance of the company.

The purpose of this report is to analyse the financial performance of one of company

listed on ASX. The aim is to provide the investment advice to potential the investor who seeks to

make investment in the selected company. The company selected for the purpose of analysis is

Origin Energy. Origin Energy deals electricity, natural gas, solar, and LPG and this company is

listed on ASX. Comprehensive examination of the firm’s financial performance has been

performed based on the latest financial statements of Origin Energy. Annual reports of last three

years has been extracted from the investor’s relation section of the company and based on that

financial analyse has been performed. Financial tools used to evaluate the financial statements of

Origin Energy include ratio analysis, cash management analysis, risk analysis and dividend

performance.

Part II: Financial Analysis of selected company (All these parts will provide in detail in

complete file)

2.1: Description of the company

Origin Energy is a publicly listed energy company of Australia that has been

headquartered within Sydney and is traded on Australian Stock Exchange (ASX). It is an

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

integrated energy company that is involved in large-scale exploration, production, generation and

sale of energy product and services to domestic and commercial use within Australia. The core

business activities of the company include retailing of energy products and supplying the

customers electricity, natural gas, LPG and solar. It is also involved in creating renewable energy

and as such is continually seeking investment within wind, solar and storage technologies. It is

also emphasizing towards exploring the reserves of natural gas for developing it as a future

source of energy (Who we are: Origin Energy, 2017).

The company has attained a leading position within the energy sector of Australia

involved in providing electricity to about 4.2 million customers. It aspires to attain number one

position within the renewable energy sector of Australia by continuously focusing on reducing

its carbon footprint through investing in exploration and creation of renewable energy products.

It has launched its carbon reduction scheme within the year 2007 to achieve reduction in its

carbon emission and ensuring the environment protection. In this context, it has also acquired

Eraring Energy, the largest power station of Australia and its cogeneration business provides

low-carbon energy products to the customers within Victoria. The geographic foot print of the

company extends to Australia and New Zealand. The company is a recognized member of the

‘We Mean Business’ coalition that emphasizes on taking adequate action on climate change. IT

has also become the first energy company within Australia in the financial year 2015 to sign up

seven commitments in regards to climatic changes. The progress made by the company in the

key areas for monitoring the climatic changes has been provided within the public disclosures.

The progress made by the company in reducing its carbon footprint and developing energy

products through renewable sources have enabled it to gain competitiveness within the energy

sector of Australia. The natural gas portfolio of the company also enables it to achieve a core

competency within the energy sector of Australia (Who we are: Origin Energy, 2017).

2.2: Use of Ratio Analysis to evaluate the financial performance of Origin Energy

Profitability Ratios of Origin Energy

Financial Data used to calculate profitability ratio

Financial Items 2015 2016 2017 2018

Amount in $ Million

Net profit after tax $ $ $

5

sale of energy product and services to domestic and commercial use within Australia. The core

business activities of the company include retailing of energy products and supplying the

customers electricity, natural gas, LPG and solar. It is also involved in creating renewable energy

and as such is continually seeking investment within wind, solar and storage technologies. It is

also emphasizing towards exploring the reserves of natural gas for developing it as a future

source of energy (Who we are: Origin Energy, 2017).

The company has attained a leading position within the energy sector of Australia

involved in providing electricity to about 4.2 million customers. It aspires to attain number one

position within the renewable energy sector of Australia by continuously focusing on reducing

its carbon footprint through investing in exploration and creation of renewable energy products.

It has launched its carbon reduction scheme within the year 2007 to achieve reduction in its

carbon emission and ensuring the environment protection. In this context, it has also acquired

Eraring Energy, the largest power station of Australia and its cogeneration business provides

low-carbon energy products to the customers within Victoria. The geographic foot print of the

company extends to Australia and New Zealand. The company is a recognized member of the

‘We Mean Business’ coalition that emphasizes on taking adequate action on climate change. IT

has also become the first energy company within Australia in the financial year 2015 to sign up

seven commitments in regards to climatic changes. The progress made by the company in the

key areas for monitoring the climatic changes has been provided within the public disclosures.

The progress made by the company in reducing its carbon footprint and developing energy

products through renewable sources have enabled it to gain competitiveness within the energy

sector of Australia. The natural gas portfolio of the company also enables it to achieve a core

competency within the energy sector of Australia (Who we are: Origin Energy, 2017).

2.2: Use of Ratio Analysis to evaluate the financial performance of Origin Energy

Profitability Ratios of Origin Energy

Financial Data used to calculate profitability ratio

Financial Items 2015 2016 2017 2018

Amount in $ Million

Net profit after tax $ $ $

5

(576.00) (2,223.00) 221.00

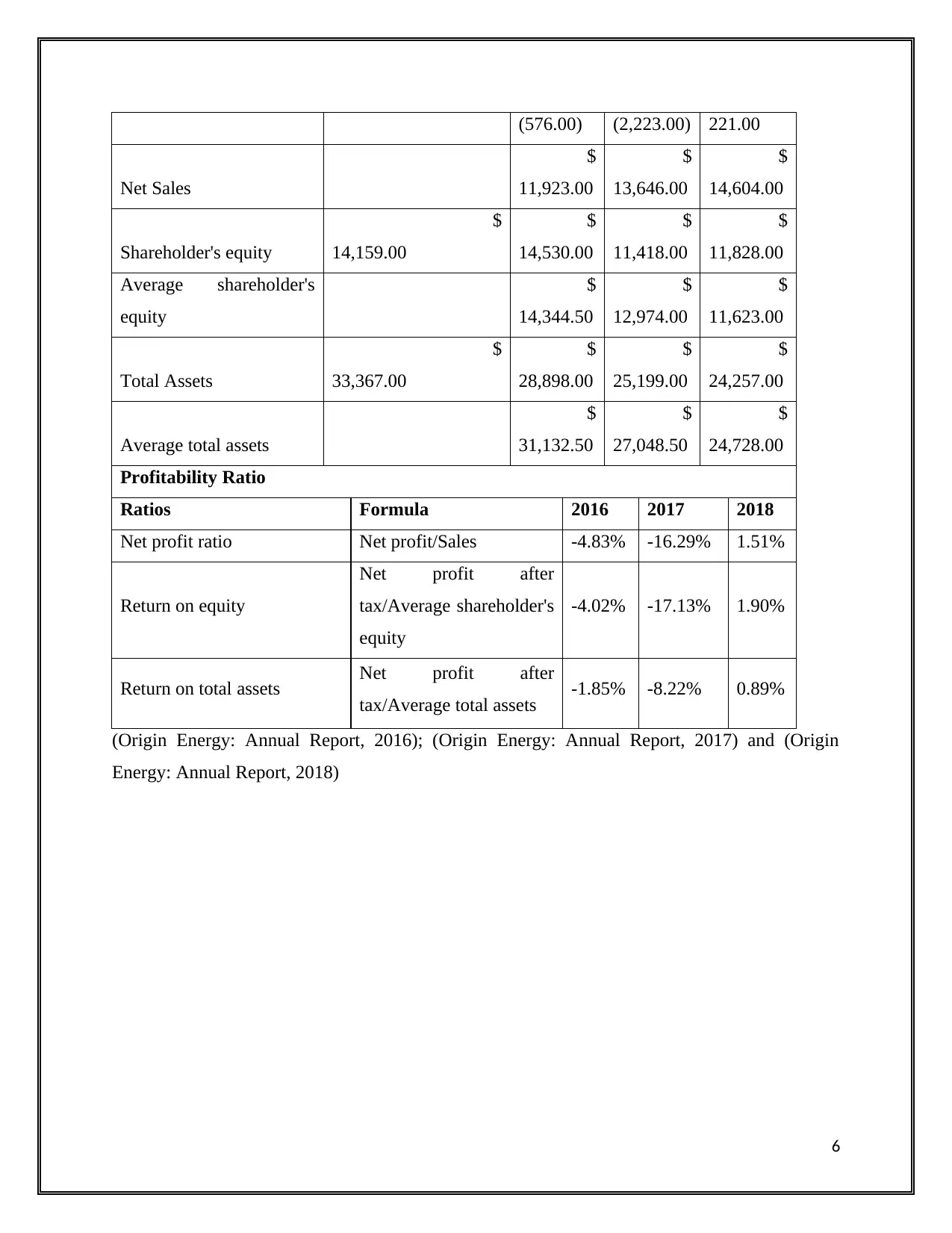

Net Sales

$

11,923.00

$

13,646.00

$

14,604.00

Shareholder's equity

$

14,159.00

$

14,530.00

$

11,418.00

$

11,828.00

Average shareholder's

equity

$

14,344.50

$

12,974.00

$

11,623.00

Total Assets

$

33,367.00

$

28,898.00

$

25,199.00

$

24,257.00

Average total assets

$

31,132.50

$

27,048.50

$

24,728.00

Profitability Ratio

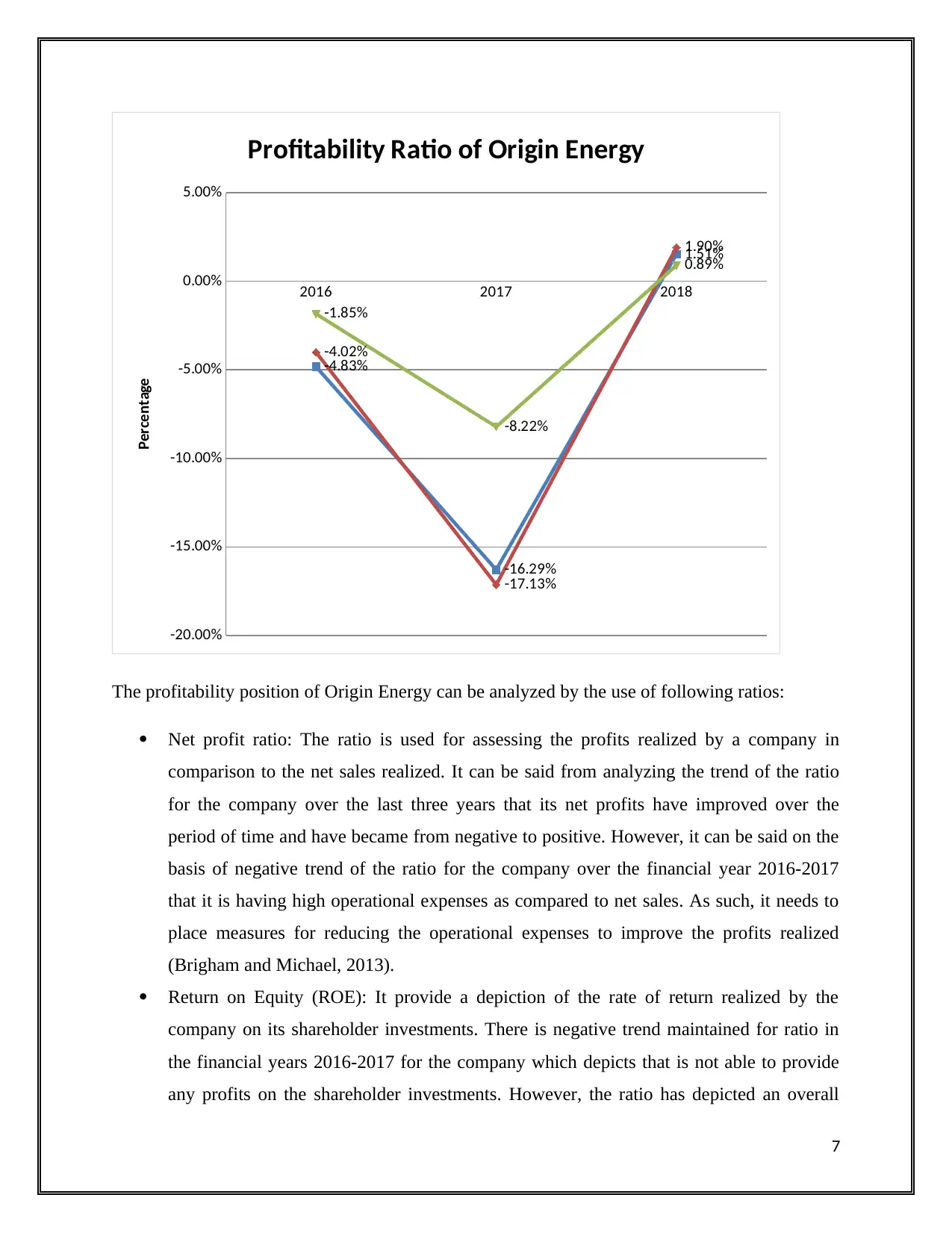

Ratios Formula 2016 2017 2018

Net profit ratio Net profit/Sales -4.83% -16.29% 1.51%

Return on equity

Net profit after

tax/Average shareholder's

equity

-4.02% -17.13% 1.90%

Return on total assets Net profit after

tax/Average total assets -1.85% -8.22% 0.89%

(Origin Energy: Annual Report, 2016); (Origin Energy: Annual Report, 2017) and (Origin

Energy: Annual Report, 2018)

6

Net Sales

$

11,923.00

$

13,646.00

$

14,604.00

Shareholder's equity

$

14,159.00

$

14,530.00

$

11,418.00

$

11,828.00

Average shareholder's

equity

$

14,344.50

$

12,974.00

$

11,623.00

Total Assets

$

33,367.00

$

28,898.00

$

25,199.00

$

24,257.00

Average total assets

$

31,132.50

$

27,048.50

$

24,728.00

Profitability Ratio

Ratios Formula 2016 2017 2018

Net profit ratio Net profit/Sales -4.83% -16.29% 1.51%

Return on equity

Net profit after

tax/Average shareholder's

equity

-4.02% -17.13% 1.90%

Return on total assets Net profit after

tax/Average total assets -1.85% -8.22% 0.89%

(Origin Energy: Annual Report, 2016); (Origin Energy: Annual Report, 2017) and (Origin

Energy: Annual Report, 2018)

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2016 2017 2018

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

-4.83%

-16.29%

1.51%

-4.02%

-17.13%

1.90%

-1.85%

-8.22%

0.89%

Profitability Ratio of Origin Energy

Percentage

The profitability position of Origin Energy can be analyzed by the use of following ratios:

Net profit ratio: The ratio is used for assessing the profits realized by a company in

comparison to the net sales realized. It can be said from analyzing the trend of the ratio

for the company over the last three years that its net profits have improved over the

period of time and have became from negative to positive. However, it can be said on the

basis of negative trend of the ratio for the company over the financial year 2016-2017

that it is having high operational expenses as compared to net sales. As such, it needs to

place measures for reducing the operational expenses to improve the profits realized

(Brigham and Michael, 2013).

Return on Equity (ROE): It provide a depiction of the rate of return realized by the

company on its shareholder investments. There is negative trend maintained for ratio in

the financial years 2016-2017 for the company which depicts that is not able to provide

any profits on the shareholder investments. However, the ratio has depicted an overall

7

-20.00%

-15.00%

-10.00%

-5.00%

0.00%

5.00%

-4.83%

-16.29%

1.51%

-4.02%

-17.13%

1.90%

-1.85%

-8.22%

0.89%

Profitability Ratio of Origin Energy

Percentage

The profitability position of Origin Energy can be analyzed by the use of following ratios:

Net profit ratio: The ratio is used for assessing the profits realized by a company in

comparison to the net sales realized. It can be said from analyzing the trend of the ratio

for the company over the last three years that its net profits have improved over the

period of time and have became from negative to positive. However, it can be said on the

basis of negative trend of the ratio for the company over the financial year 2016-2017

that it is having high operational expenses as compared to net sales. As such, it needs to

place measures for reducing the operational expenses to improve the profits realized

(Brigham and Michael, 2013).

Return on Equity (ROE): It provide a depiction of the rate of return realized by the

company on its shareholder investments. There is negative trend maintained for ratio in

the financial years 2016-2017 for the company which depicts that is not able to provide

any profits on the shareholder investments. However, the ratio has depicted an overall

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increase from -4.02 % to 1.90% for the company over the period which means that it is

able to provide positive return to the shareholders only in the year 2018. In this context,

the company is suggested to reduce the cost of debt for providing positive returns to the

shareholders (Bragg, 2010).

Return on Assets (ROA): The ratio depicts the returns realized by a company over the use

of its asset resources. The ratio has depicted a negative trend over the year 2016-2017 but

has reflected positive results for the financial year 2018. This depicts that the company is

not able to derive any returns on its assets resources over the year 2016-2017 but have

improved the capability of generate profits from its assets in the eyar2018. However, it

needs to improve its capability to derive profits from the effective use of assets to

improve its long-term profitability position (Reilly & Brown, 2011).

Operating Efficiency Ratios

Financial Data used to calculate operating efficiency ratio

Financial Items 2015 2016 2017 2018

Amount in $ Million

Net Sales

$

11,923.00

$

13,646.00 $ 14,604.00

Account Receivables

$

2,085.00

$

1,945.00

$

2,278.00 $ 2,537.00

Average account

receivable

$

2,015.00

$

2,111.50 $ 2,407.50

Total Assets

$

33,367.00

$

28,898.00

$

25,199.00 $ 24,257.00

Average total assets

$

31,132.50

$

27,048.50 $ 24,728.00

Cost of Goods Sold

$

8,964.00

$

11,099.00 $ 11,674.00

Inventory

$

239.00

$

248.00

$

138.00

$

196.00

Average Inventory

$

243.50

$

193.00

$

167.00

8

able to provide positive return to the shareholders only in the year 2018. In this context,

the company is suggested to reduce the cost of debt for providing positive returns to the

shareholders (Bragg, 2010).

Return on Assets (ROA): The ratio depicts the returns realized by a company over the use

of its asset resources. The ratio has depicted a negative trend over the year 2016-2017 but

has reflected positive results for the financial year 2018. This depicts that the company is

not able to derive any returns on its assets resources over the year 2016-2017 but have

improved the capability of generate profits from its assets in the eyar2018. However, it

needs to improve its capability to derive profits from the effective use of assets to

improve its long-term profitability position (Reilly & Brown, 2011).

Operating Efficiency Ratios

Financial Data used to calculate operating efficiency ratio

Financial Items 2015 2016 2017 2018

Amount in $ Million

Net Sales

$

11,923.00

$

13,646.00 $ 14,604.00

Account Receivables

$

2,085.00

$

1,945.00

$

2,278.00 $ 2,537.00

Average account

receivable

$

2,015.00

$

2,111.50 $ 2,407.50

Total Assets

$

33,367.00

$

28,898.00

$

25,199.00 $ 24,257.00

Average total assets

$

31,132.50

$

27,048.50 $ 24,728.00

Cost of Goods Sold

$

8,964.00

$

11,099.00 $ 11,674.00

Inventory

$

239.00

$

248.00

$

138.00

$

196.00

Average Inventory

$

243.50

$

193.00

$

167.00

8

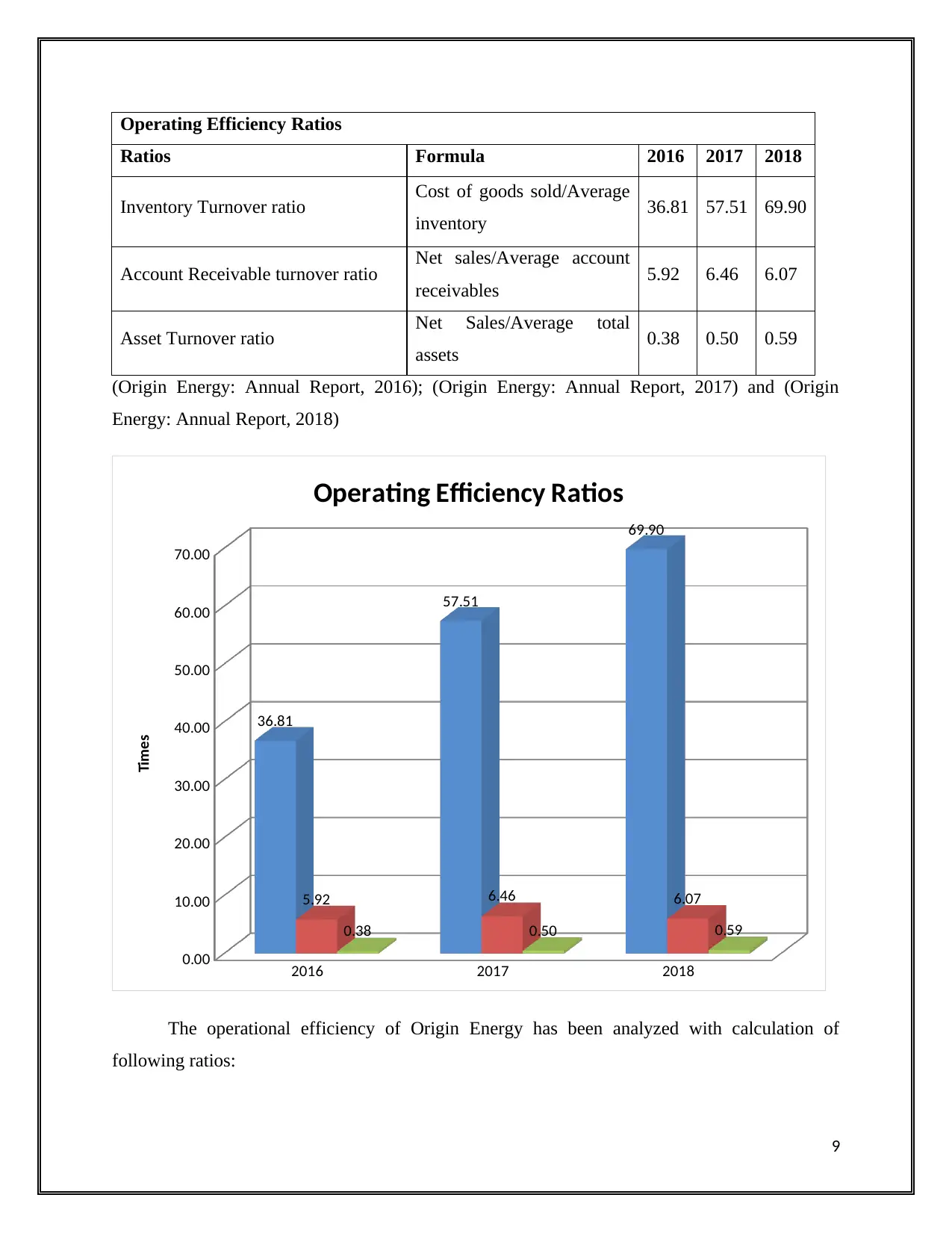

Operating Efficiency Ratios

Ratios Formula 2016 2017 2018

Inventory Turnover ratio Cost of goods sold/Average

inventory 36.81 57.51 69.90

Account Receivable turnover ratio Net sales/Average account

receivables 5.92 6.46 6.07

Asset Turnover ratio Net Sales/Average total

assets 0.38 0.50 0.59

(Origin Energy: Annual Report, 2016); (Origin Energy: Annual Report, 2017) and (Origin

Energy: Annual Report, 2018)

2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

36.81

57.51

69.90

5.92 6.46 6.07

0.38 0.50 0.59

Operating Efficiency Ratios

Times

The operational efficiency of Origin Energy has been analyzed with calculation of

following ratios:

9

Ratios Formula 2016 2017 2018

Inventory Turnover ratio Cost of goods sold/Average

inventory 36.81 57.51 69.90

Account Receivable turnover ratio Net sales/Average account

receivables 5.92 6.46 6.07

Asset Turnover ratio Net Sales/Average total

assets 0.38 0.50 0.59

(Origin Energy: Annual Report, 2016); (Origin Energy: Annual Report, 2017) and (Origin

Energy: Annual Report, 2018)

2016 2017 2018

0.00

10.00

20.00

30.00

40.00

50.00

60.00

70.00

36.81

57.51

69.90

5.92 6.46 6.07

0.38 0.50 0.59

Operating Efficiency Ratios

Times

The operational efficiency of Origin Energy has been analyzed with calculation of

following ratios:

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory turnover ratio: The ratio depicts the efficiency of a company to replace its

inventory level. It can be stated from analyzing the ratio trend for Origin Energy for the

past three years that it has depicted an increase from 36.81 to 69.90. This reflects that it is

able to continuously replace its inventory in regular period of time and thus is able to

reduce the cost of holding the inventory that would help it to improve its profitability

position (Moles & Kidwekk, 2011).

Accounts Receivable Turnover Ratio: The ratio depicts the efficiency of the company for

realizing its payments from its debtors on outstanding invoices or bills. The ratio for

Origin Energy has depicted an increase from 5.92 to 6.07 over the financial period 2016-

2018 which is good for the future growth prospects of the company as it is able to

maintaining sufficient flow of cash for meeting its financial obligations by regularly

collecting the money on its credit sales (Krantz, 2016).

Asset Turnover ratio: The ratio depicts the ability of a company to use its assets for

generating sales and revenue. The ratio has depicted an increase from 0.38 to 0.59 over

the year 2016-2018 which means that it is improving its efficiency to realize returns on

its assets. However, the ratio is less than 1 over the period which means that it need to

improve its capability to utilize asset base to produce sales and generating profits

(Schlichting, 2013).

2.3: Management of cash through of marketable securities by Origin Energy

Marketable securities can be regarded as the short-term investments that are

incurred by a company with the use of its cash resources. The securities are regarded as quick

assets of a company that can be sold quickly and transferred into cash for meeting the short-term

financial liabilities of a company as soon as they become due (Zimmerman & Yahya-Zadeh,

2011). The marketable securities as analyzed from the balance sheet of the company are

categorized as assets held for the sale and cash equivalents. The company has not incorporated

the use of any assets held for sale in the financial year 2018 but has the presence of it in the

current assets for the financial year 2016-2017. The assets that are related to the divestment of

the conventional upstream business have been falsified for sale and these are recognized at cost.

The marketable securities include cash and cash equivalents mainly as they can be used for

releasing cash on quick basis (Origin Energy: Annual Report, 2017 & Origin Energy: Annual

Report, 2018).

10

inventory level. It can be stated from analyzing the ratio trend for Origin Energy for the

past three years that it has depicted an increase from 36.81 to 69.90. This reflects that it is

able to continuously replace its inventory in regular period of time and thus is able to

reduce the cost of holding the inventory that would help it to improve its profitability

position (Moles & Kidwekk, 2011).

Accounts Receivable Turnover Ratio: The ratio depicts the efficiency of the company for

realizing its payments from its debtors on outstanding invoices or bills. The ratio for

Origin Energy has depicted an increase from 5.92 to 6.07 over the financial period 2016-

2018 which is good for the future growth prospects of the company as it is able to

maintaining sufficient flow of cash for meeting its financial obligations by regularly

collecting the money on its credit sales (Krantz, 2016).

Asset Turnover ratio: The ratio depicts the ability of a company to use its assets for

generating sales and revenue. The ratio has depicted an increase from 0.38 to 0.59 over

the year 2016-2018 which means that it is improving its efficiency to realize returns on

its assets. However, the ratio is less than 1 over the period which means that it need to

improve its capability to utilize asset base to produce sales and generating profits

(Schlichting, 2013).

2.3: Management of cash through of marketable securities by Origin Energy

Marketable securities can be regarded as the short-term investments that are

incurred by a company with the use of its cash resources. The securities are regarded as quick

assets of a company that can be sold quickly and transferred into cash for meeting the short-term

financial liabilities of a company as soon as they become due (Zimmerman & Yahya-Zadeh,

2011). The marketable securities as analyzed from the balance sheet of the company are

categorized as assets held for the sale and cash equivalents. The company has not incorporated

the use of any assets held for sale in the financial year 2018 but has the presence of it in the

current assets for the financial year 2016-2017. The assets that are related to the divestment of

the conventional upstream business have been falsified for sale and these are recognized at cost.

The marketable securities include cash and cash equivalents mainly as they can be used for

releasing cash on quick basis (Origin Energy: Annual Report, 2017 & Origin Energy: Annual

Report, 2018).

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

.

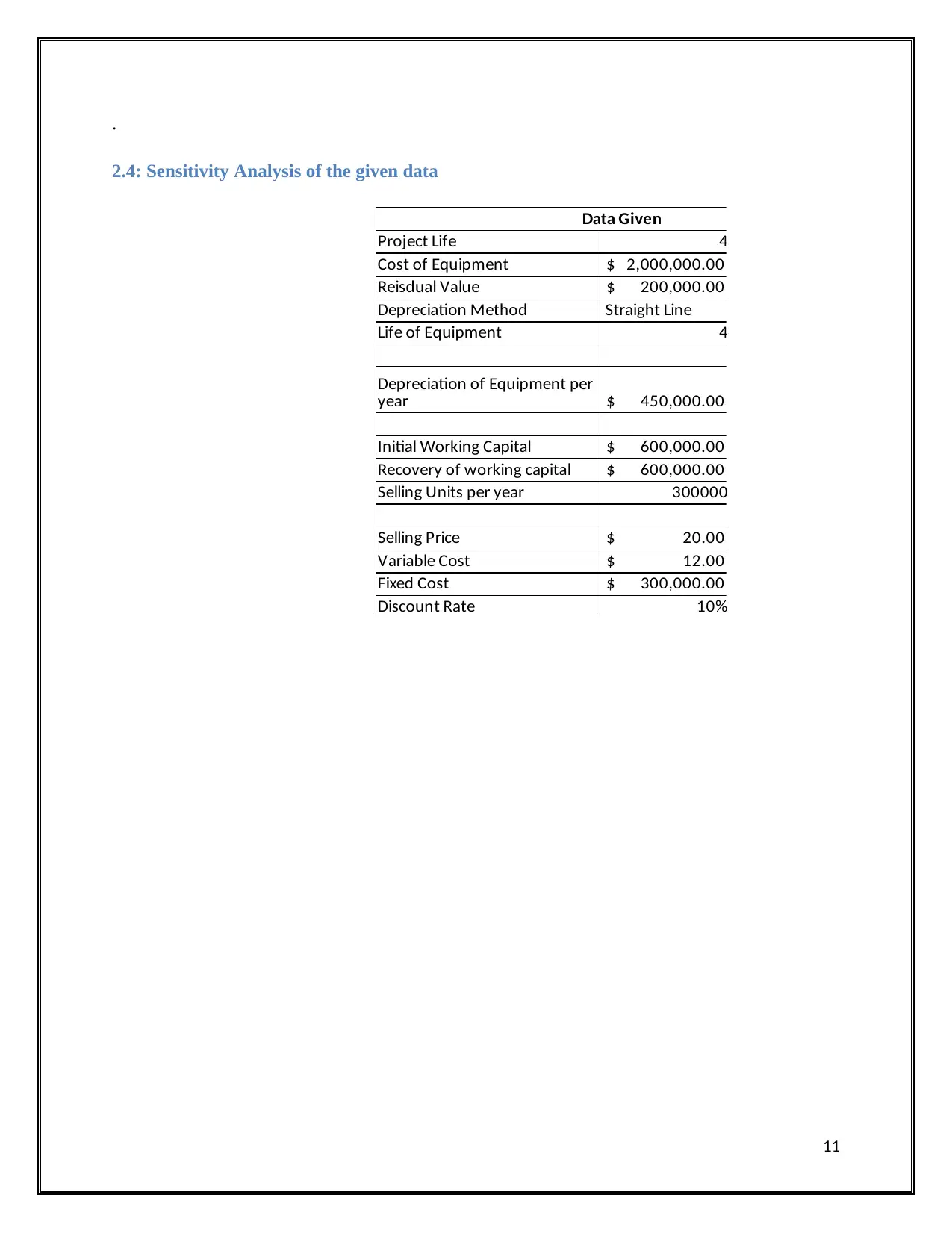

2.4: Sensitivity Analysis of the given data

Data Given

Project Life 4

Cost of Equipment $ 2,000,000.00

Reisdual Value $ 200,000.00

Depreciation Method Straight Line

Life of Equipment 4

$ 450,000.00

Initial Working Capital $ 600,000.00

Recovery of working capital $ 600,000.00

Selling Units per year 300000

Selling Price $ 20.00

Variable Cost $ 12.00

Fixed Cost $ 300,000.00

Discount Rate 10%

Depreciation of Equipment per

year

11

2.4: Sensitivity Analysis of the given data

Data Given

Project Life 4

Cost of Equipment $ 2,000,000.00

Reisdual Value $ 200,000.00

Depreciation Method Straight Line

Life of Equipment 4

$ 450,000.00

Initial Working Capital $ 600,000.00

Recovery of working capital $ 600,000.00

Selling Units per year 300000

Selling Price $ 20.00

Variable Cost $ 12.00

Fixed Cost $ 300,000.00

Discount Rate 10%

Depreciation of Equipment per

year

11

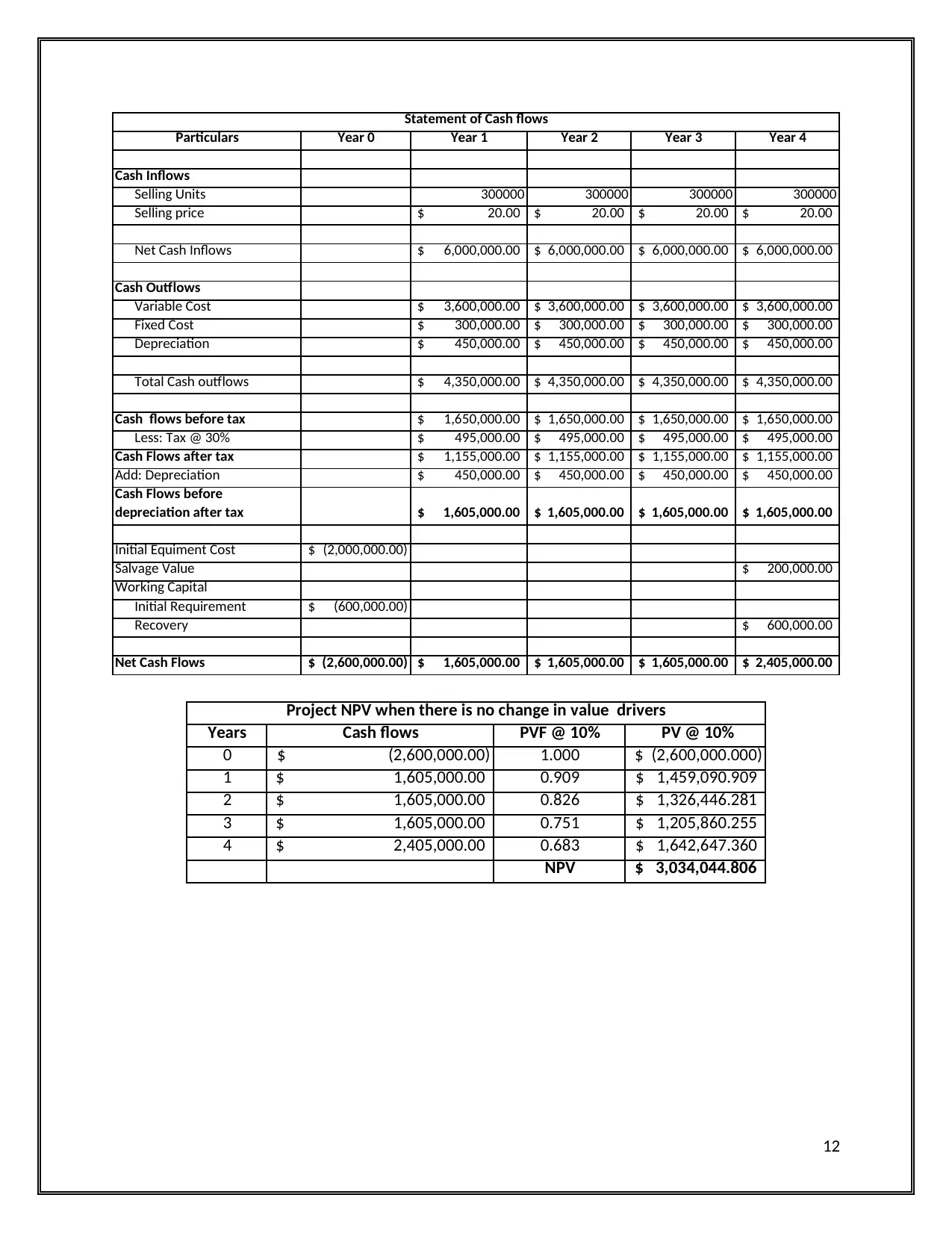

Particulars Year 0 Year 1 Year 2 Year 3 Year 4

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

Statement of Cash flows

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,605,000.00$ 0.909 1,459,090.909$

2 1,605,000.00$ 0.826 1,326,446.281$

3 1,605,000.00$ 0.751 1,205,860.255$

4 2,405,000.00$ 0.683 1,642,647.360$

NPV 3,034,044.806$

Project NPV when there is no change in value drivers

12

Cash Inflows

Selling Units 300000 300000 300000 300000

Selling price 20.00$ 20.00$ 20.00$ 20.00$

Net Cash Inflows 6,000,000.00$ 6,000,000.00$ 6,000,000.00$ 6,000,000.00$

Cash Outflows

Variable Cost 3,600,000.00$ 3,600,000.00$ 3,600,000.00$ 3,600,000.00$

Fixed Cost 300,000.00$ 300,000.00$ 300,000.00$ 300,000.00$

Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Total Cash outflows 4,350,000.00$ 4,350,000.00$ 4,350,000.00$ 4,350,000.00$

Cash flows before tax 1,650,000.00$ 1,650,000.00$ 1,650,000.00$ 1,650,000.00$

Less: Tax @ 30% 495,000.00$ 495,000.00$ 495,000.00$ 495,000.00$

Cash Flows after tax 1,155,000.00$ 1,155,000.00$ 1,155,000.00$ 1,155,000.00$

Add: Depreciation 450,000.00$ 450,000.00$ 450,000.00$ 450,000.00$

Cash Flows before

depreciation after tax 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$

Initial Equiment Cost (2,000,000.00)$

Salvage Value 200,000.00$

Working Capital

Initial Requirement (600,000.00)$

Recovery 600,000.00$

Net Cash Flows (2,600,000.00)$ 1,605,000.00$ 1,605,000.00$ 1,605,000.00$ 2,405,000.00$

Statement of Cash flows

Years Cash flows PVF @ 10% PV @ 10%

0 (2,600,000.00)$ 1.000 (2,600,000.000)$

1 1,605,000.00$ 0.909 1,459,090.909$

2 1,605,000.00$ 0.826 1,326,446.281$

3 1,605,000.00$ 0.751 1,205,860.255$

4 2,405,000.00$ 0.683 1,642,647.360$

NPV 3,034,044.806$

Project NPV when there is no change in value drivers

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.