Management Accounting Report: Financial Health of Two Companies

VerifiedAdded on 2021/04/16

|18

|3787

|32

Report

AI Summary

This report provides a comprehensive financial analysis of Alpine Construction Ltd and Maple Builders Ltd, subsidiaries of BC Ltd, evaluating their financial performance, solvency, and long-term profit potential. The analysis includes a comparison of financial ratios such as gross profit margin, net profit margin, current ratio, quick ratio, debt-to-equity ratio, and EPS/DPS to assess the financial health and stability of each company. The report identifies Maple Builders Ltd as the better-performing subsidiary, recommending that BC Ltd divest from Alpine Construction Ltd to improve its return on investment. It suggests improvements for Maple Builders Ltd in asset utilization, current ratio, and return on assets. The report also explains solvency tests in accordance with the Companies Act 1993 and determines whether dividend payments are feasible. Finally, it acknowledges limitations of the financial analysis and suggests variations that might exist within the report.

Running head: MANAGEMENT ACCOUNTING

Management Accounting

Name of the Student:

Name of the University:

Authors Note:

Management Accounting

Name of the Student:

Name of the University:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

1

Executive Summary:

The overall assessment focuses in evaluating the overall financial performance of Alpine

Construction ltd and Maple Builder Ltd is mainly evaluated to identify the best performing

subsidiary. The financial ratios, solvency position and recommendation could be identified

for detecting financial performance of the company. The evaluation relevantly helps in

conducting solvency condition where relevant limitations and variations of financial analysis

could be identified. Therefore, BC Ltd should divest from Alpine construction for reducing

the looses and increase return from investment.

1

Executive Summary:

The overall assessment focuses in evaluating the overall financial performance of Alpine

Construction ltd and Maple Builder Ltd is mainly evaluated to identify the best performing

subsidiary. The financial ratios, solvency position and recommendation could be identified

for detecting financial performance of the company. The evaluation relevantly helps in

conducting solvency condition where relevant limitations and variations of financial analysis

could be identified. Therefore, BC Ltd should divest from Alpine construction for reducing

the looses and increase return from investment.

MANAGEMENT ACCOUNTING

2

Table of Contents

Introduction:...............................................................................................................................3

1. Comparing two companies in term of financial health/position:...........................................3

1.1 Depicting the best long-term profit potential of both the companies:.................................3

1.2 Depicting most financially stable position of both the companies:.....................................4

1.3 Depicting company who runs most efficiently:...................................................................6

1.4 Depicting which subsidiary is in the best market position:..................................................7

1.5 Depicting which subsidiary is the most solvent:..................................................................8

1.6 Depicting which subsidiary compares most favourably within the industry:......................9

2. Depicting the conclusion drawn from financial analysis, while depicting the company with

better financial health/position and why:.................................................................................10

3. Recommendations for BC Ltd:............................................................................................10

3.1 Recommendation for BC Ltd on which of the two companies it should divest from:.......10

3.2 Suggesting three ways in which improvements in business can be conducted in the

company that is not recommended for divesting:....................................................................11

4. Dividend payments:.............................................................................................................11

4.1 Explaining the Solvency Tests in accordance with the Companies Act 1993:..................11

4.2 Selecting and applying amounts in accordance with the solvency test and depicting

whether the dividend could be paid:........................................................................................12

5. Limitations & variations:.....................................................................................................12

5.1 Explaining the limitation of financial analysis:.................................................................12

5.2 Suggesting and explaining any variations that might exist within the report:...................13

Conclusion:..............................................................................................................................13

Reference and Bibliography:....................................................................................................14

Appendices:..............................................................................................................................16

2

Table of Contents

Introduction:...............................................................................................................................3

1. Comparing two companies in term of financial health/position:...........................................3

1.1 Depicting the best long-term profit potential of both the companies:.................................3

1.2 Depicting most financially stable position of both the companies:.....................................4

1.3 Depicting company who runs most efficiently:...................................................................6

1.4 Depicting which subsidiary is in the best market position:..................................................7

1.5 Depicting which subsidiary is the most solvent:..................................................................8

1.6 Depicting which subsidiary compares most favourably within the industry:......................9

2. Depicting the conclusion drawn from financial analysis, while depicting the company with

better financial health/position and why:.................................................................................10

3. Recommendations for BC Ltd:............................................................................................10

3.1 Recommendation for BC Ltd on which of the two companies it should divest from:.......10

3.2 Suggesting three ways in which improvements in business can be conducted in the

company that is not recommended for divesting:....................................................................11

4. Dividend payments:.............................................................................................................11

4.1 Explaining the Solvency Tests in accordance with the Companies Act 1993:..................11

4.2 Selecting and applying amounts in accordance with the solvency test and depicting

whether the dividend could be paid:........................................................................................12

5. Limitations & variations:.....................................................................................................12

5.1 Explaining the limitation of financial analysis:.................................................................12

5.2 Suggesting and explaining any variations that might exist within the report:...................13

Conclusion:..............................................................................................................................13

Reference and Bibliography:....................................................................................................14

Appendices:..............................................................................................................................16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING

3

Introduction:

The overall assessment mainly helps in identifying the overall financial viability of

Maple Builders Ltd and Alpine construction. In addition, relevant recommendation is mainly

conducted to BC Ltd for improv their financial performance and minimises the negative

impact from declining sales revenue. Relevant suggestion is mainly stated in the assessment

for improving the business conduction of BC Ltd. The solvency test is mainly conducted on

dividend payment, which helps in detecting the financial performance of the company.

Lastly, adequate recommendations are conducted for BC Ltd for improving the level of

returns from investment.

1. Comparing two companies in term of financial health/position:

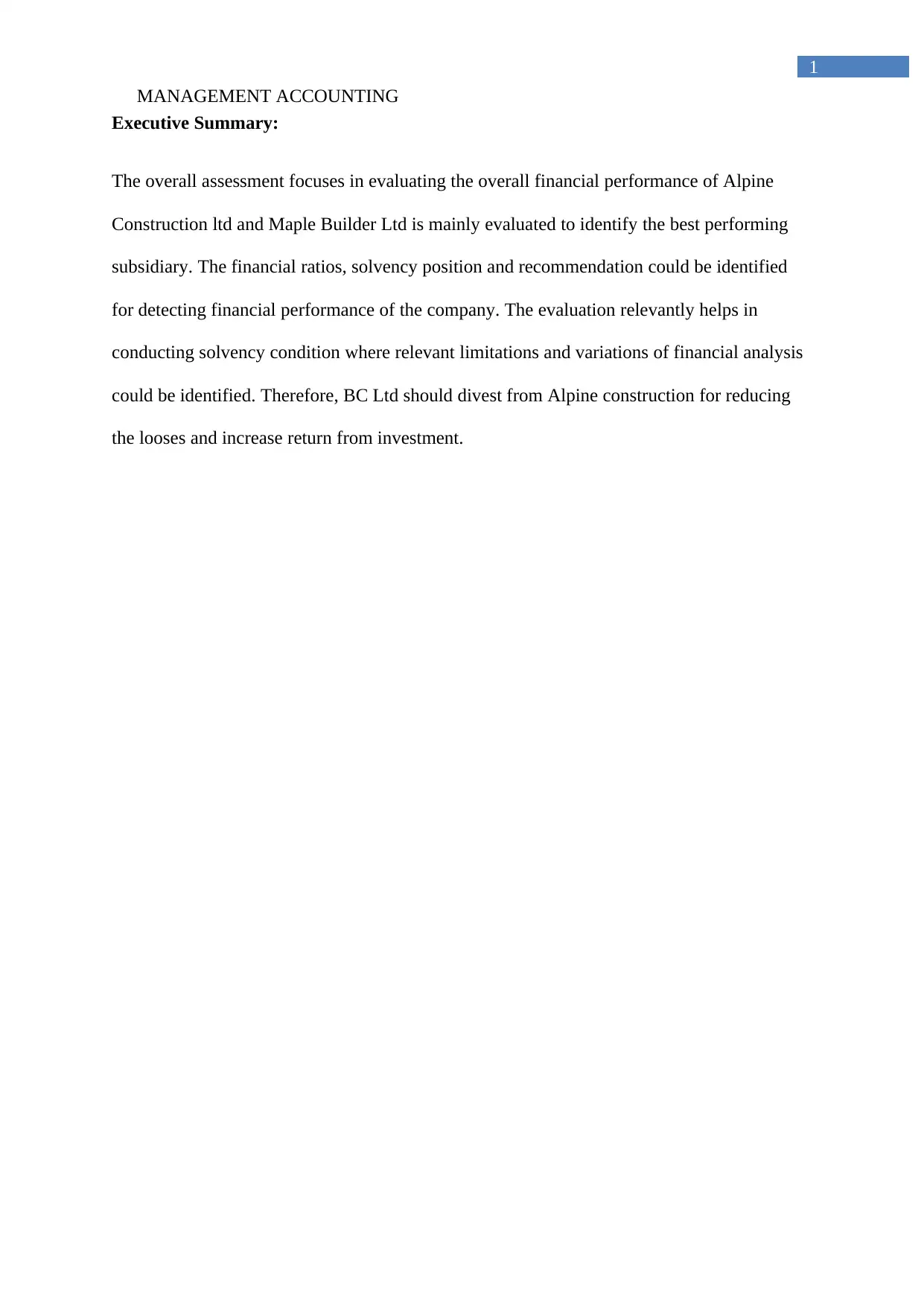

1.1 Depicting the best long-term profit potential of both the companies:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Profitability Ratios

1) Gross profit margin 2) Net Profit margin 3) Return on Asset

Name of Ratio 2015 2016 2015 2016

Profitability Ratios

1) Gross profit margin 70.10% 59.70% 67.50% 64%

2) Net Profit margin 17.38% 17.85% 21.74% 20.40%

3) Return on Asset 0.51:1 0.68:1 0.59:1 0.56:1

Alpine Construction Ltd. Maple Builders Ltd.

3

Introduction:

The overall assessment mainly helps in identifying the overall financial viability of

Maple Builders Ltd and Alpine construction. In addition, relevant recommendation is mainly

conducted to BC Ltd for improv their financial performance and minimises the negative

impact from declining sales revenue. Relevant suggestion is mainly stated in the assessment

for improving the business conduction of BC Ltd. The solvency test is mainly conducted on

dividend payment, which helps in detecting the financial performance of the company.

Lastly, adequate recommendations are conducted for BC Ltd for improving the level of

returns from investment.

1. Comparing two companies in term of financial health/position:

1.1 Depicting the best long-term profit potential of both the companies:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0.00%

10.00%

20.00%

30.00%

40.00%

50.00%

60.00%

70.00%

80.00%

Profitability Ratios

1) Gross profit margin 2) Net Profit margin 3) Return on Asset

Name of Ratio 2015 2016 2015 2016

Profitability Ratios

1) Gross profit margin 70.10% 59.70% 67.50% 64%

2) Net Profit margin 17.38% 17.85% 21.74% 20.40%

3) Return on Asset 0.51:1 0.68:1 0.59:1 0.56:1

Alpine Construction Ltd. Maple Builders Ltd.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

4

The evaluation of the ratio mainly indicates that financial performance of Maple

Builders Ltd is relatively higher than Alpine Construction Ltd, as both gross profit and net

profit margin is relatively high in 2016 of the company. The financial performance of Maple

Builders Ltd has relevantly declined over the period from 67.5% to 64%, which is relevantly

higher than the value of Alpine Construction Ltd 59.7%. The net profit margin is also higher

of Maple Builders Ltd 20.4% in comparison to Alpine Construction Ltd 17.85%. This

relevantly indicates that financial performance of Maple Builders Ltd is relatively higher than

Alpine Construction Ltd. The return on assets of Alpine Construction Ltd is higher than

Maple Builders Ltd, which does not indicate the profitability progress of the company

(Buchman, Harris & Liu, 2016). The gross profit margin of Maple Builders Ltd and Alpine

Construction Ltd relevantly declined, which is due to the high cost of sales incurred by the

company. On the other hand, Alpine Construction Ltd net profit margin inclined, due to the

occurrence of low administrative cost, which increased return on assets of the company. The

net profit margin has mainly declined for Maple Builders Ltd, due to the increment in

administrative cost, which has declined its overall return on assets.

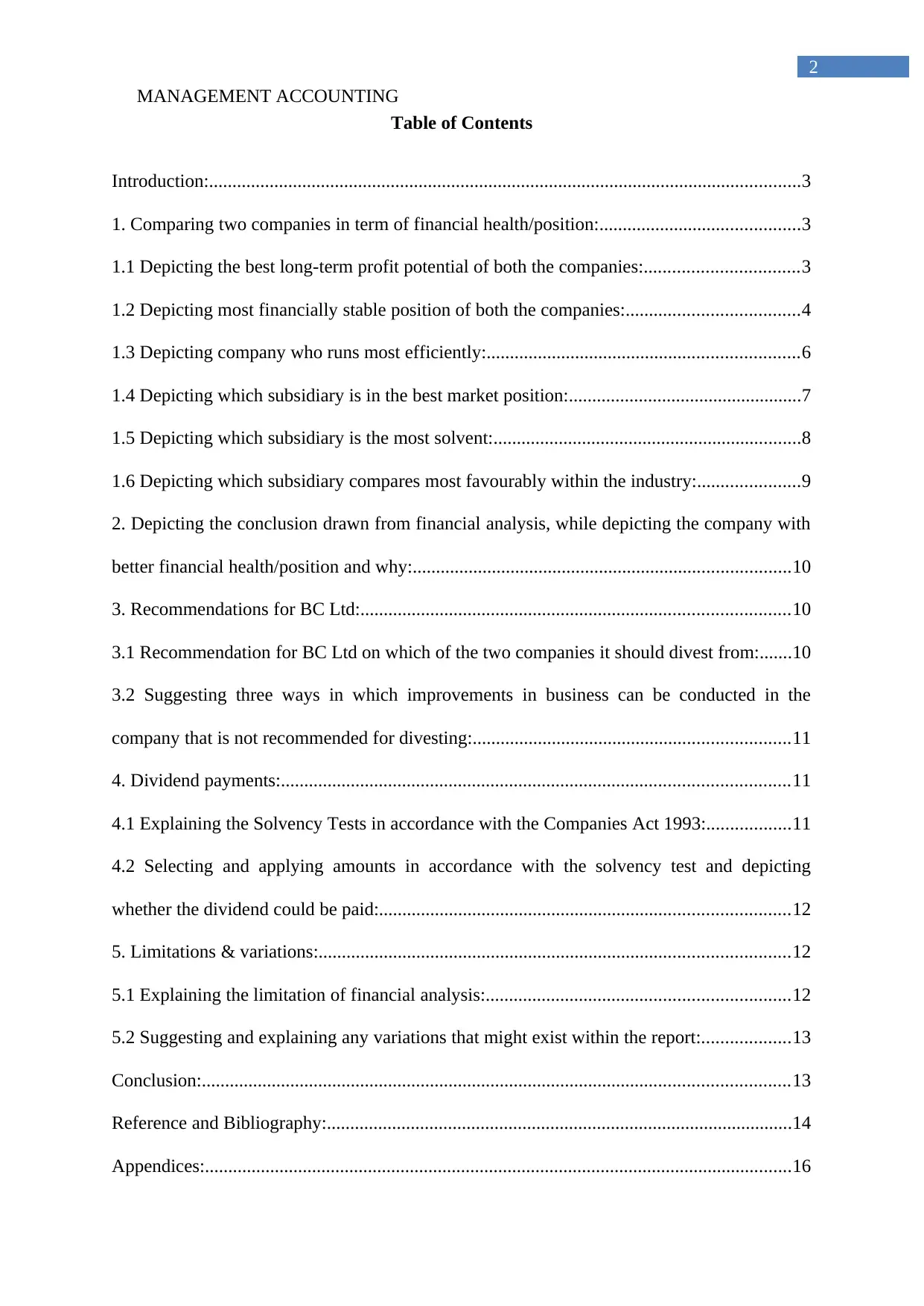

1.2 Depicting most financially stable position of both the companies:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

0.5

1

1.5

2

2.5

3

Working Capital Management Ratios

1) Current Ratio 2) Quick Ratio

4

The evaluation of the ratio mainly indicates that financial performance of Maple

Builders Ltd is relatively higher than Alpine Construction Ltd, as both gross profit and net

profit margin is relatively high in 2016 of the company. The financial performance of Maple

Builders Ltd has relevantly declined over the period from 67.5% to 64%, which is relevantly

higher than the value of Alpine Construction Ltd 59.7%. The net profit margin is also higher

of Maple Builders Ltd 20.4% in comparison to Alpine Construction Ltd 17.85%. This

relevantly indicates that financial performance of Maple Builders Ltd is relatively higher than

Alpine Construction Ltd. The return on assets of Alpine Construction Ltd is higher than

Maple Builders Ltd, which does not indicate the profitability progress of the company

(Buchman, Harris & Liu, 2016). The gross profit margin of Maple Builders Ltd and Alpine

Construction Ltd relevantly declined, which is due to the high cost of sales incurred by the

company. On the other hand, Alpine Construction Ltd net profit margin inclined, due to the

occurrence of low administrative cost, which increased return on assets of the company. The

net profit margin has mainly declined for Maple Builders Ltd, due to the increment in

administrative cost, which has declined its overall return on assets.

1.2 Depicting most financially stable position of both the companies:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

0.5

1

1.5

2

2.5

3

Working Capital Management Ratios

1) Current Ratio 2) Quick Ratio

MANAGEMENT ACCOUNTING

5

Name of Ratio 2015 2016 2015 2016

Working Capital Management Ratios

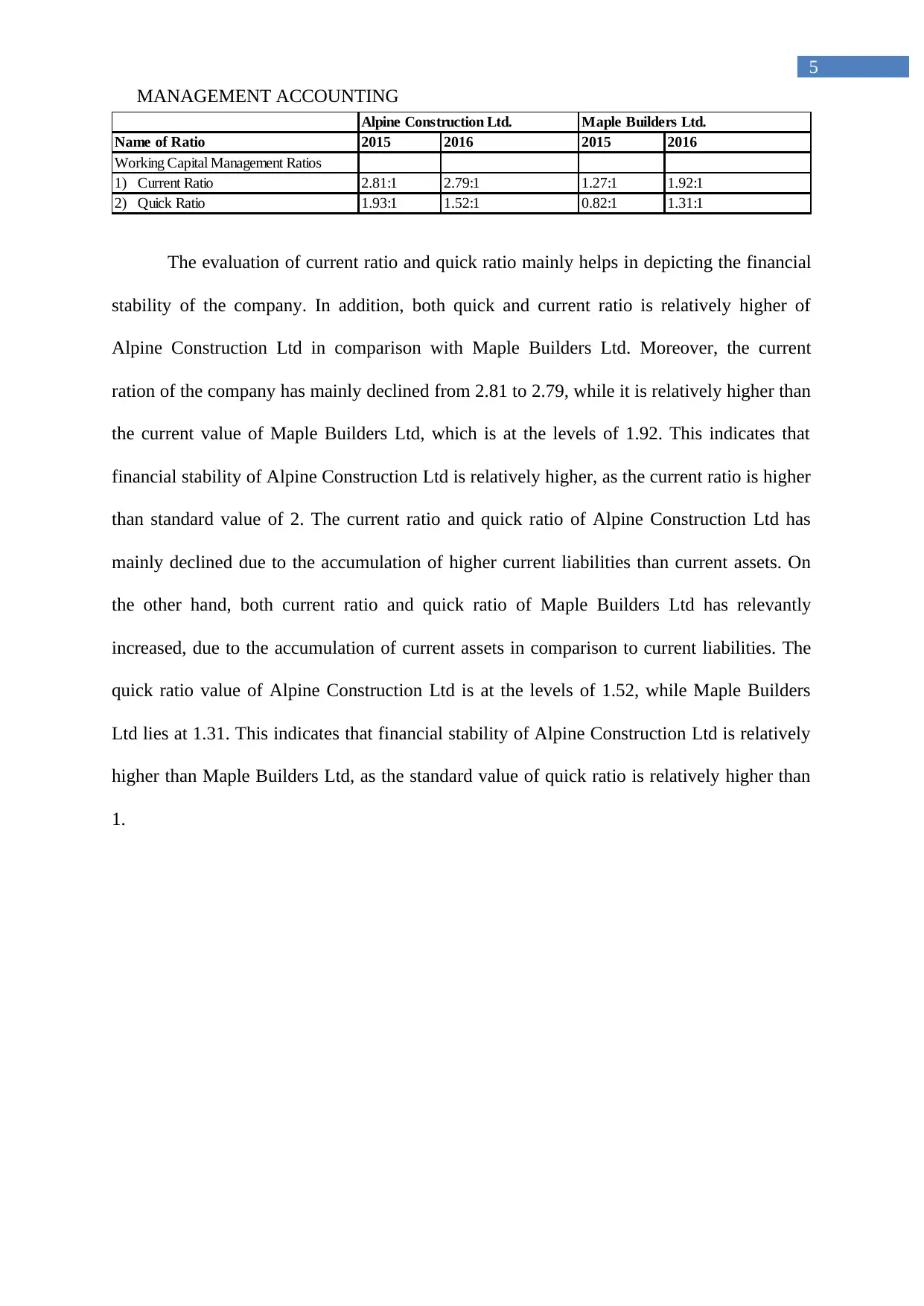

1) Current Ratio 2.81:1 2.79:1 1.27:1 1.92:1

2) Quick Ratio 1.93:1 1.52:1 0.82:1 1.31:1

Alpine Construction Ltd. Maple Builders Ltd.

The evaluation of current ratio and quick ratio mainly helps in depicting the financial

stability of the company. In addition, both quick and current ratio is relatively higher of

Alpine Construction Ltd in comparison with Maple Builders Ltd. Moreover, the current

ration of the company has mainly declined from 2.81 to 2.79, while it is relatively higher than

the current value of Maple Builders Ltd, which is at the levels of 1.92. This indicates that

financial stability of Alpine Construction Ltd is relatively higher, as the current ratio is higher

than standard value of 2. The current ratio and quick ratio of Alpine Construction Ltd has

mainly declined due to the accumulation of higher current liabilities than current assets. On

the other hand, both current ratio and quick ratio of Maple Builders Ltd has relevantly

increased, due to the accumulation of current assets in comparison to current liabilities. The

quick ratio value of Alpine Construction Ltd is at the levels of 1.52, while Maple Builders

Ltd lies at 1.31. This indicates that financial stability of Alpine Construction Ltd is relatively

higher than Maple Builders Ltd, as the standard value of quick ratio is relatively higher than

1.

5

Name of Ratio 2015 2016 2015 2016

Working Capital Management Ratios

1) Current Ratio 2.81:1 2.79:1 1.27:1 1.92:1

2) Quick Ratio 1.93:1 1.52:1 0.82:1 1.31:1

Alpine Construction Ltd. Maple Builders Ltd.

The evaluation of current ratio and quick ratio mainly helps in depicting the financial

stability of the company. In addition, both quick and current ratio is relatively higher of

Alpine Construction Ltd in comparison with Maple Builders Ltd. Moreover, the current

ration of the company has mainly declined from 2.81 to 2.79, while it is relatively higher than

the current value of Maple Builders Ltd, which is at the levels of 1.92. This indicates that

financial stability of Alpine Construction Ltd is relatively higher, as the current ratio is higher

than standard value of 2. The current ratio and quick ratio of Alpine Construction Ltd has

mainly declined due to the accumulation of higher current liabilities than current assets. On

the other hand, both current ratio and quick ratio of Maple Builders Ltd has relevantly

increased, due to the accumulation of current assets in comparison to current liabilities. The

quick ratio value of Alpine Construction Ltd is at the levels of 1.52, while Maple Builders

Ltd lies at 1.31. This indicates that financial stability of Alpine Construction Ltd is relatively

higher than Maple Builders Ltd, as the standard value of quick ratio is relatively higher than

1.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING

6

1.3 Depicting company who runs most efficiently:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

10

20

30

40

50

60

70

80

Asset Utilization Ratios

1) Inventory days 2) A/C Receivable days

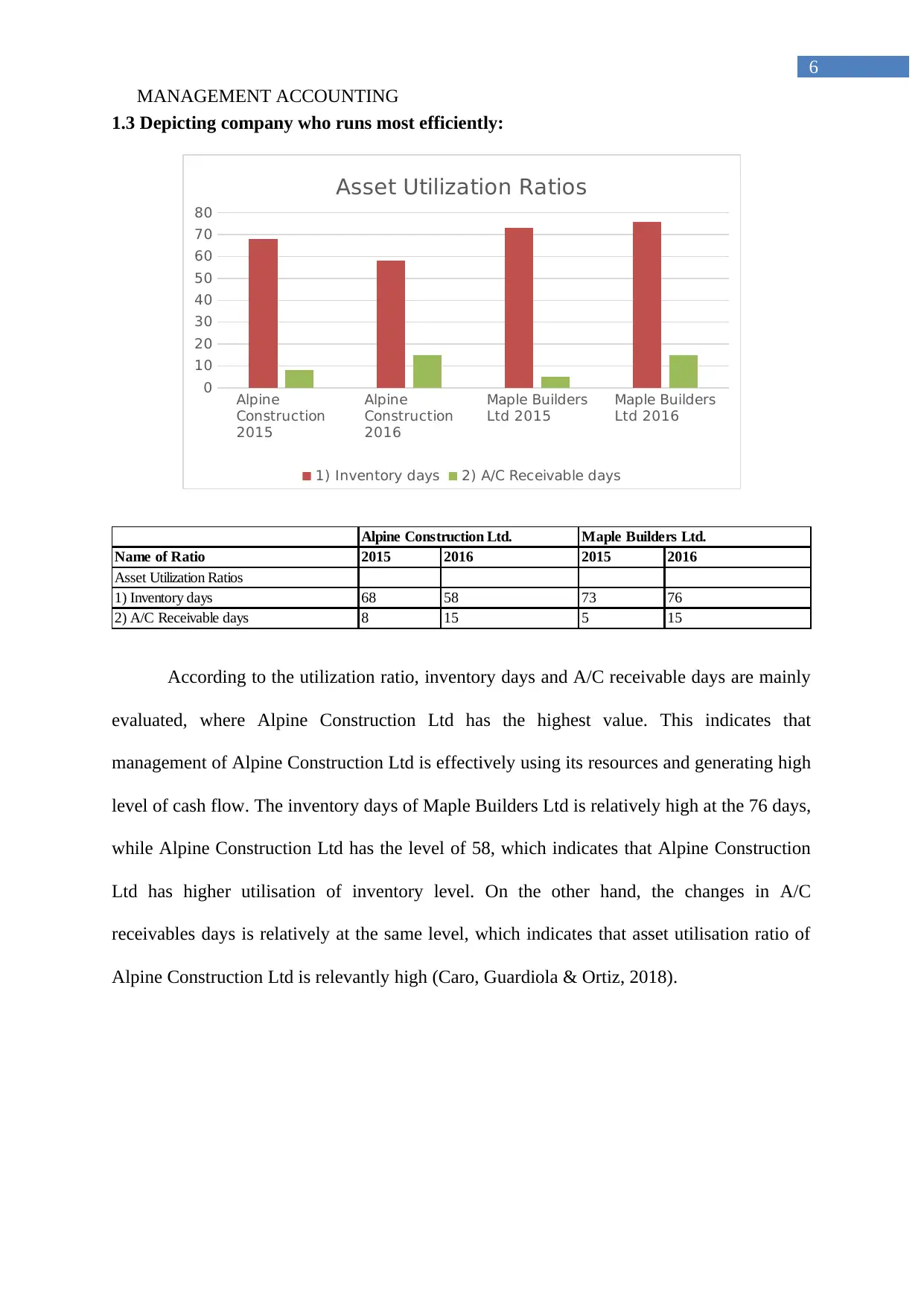

Name of Ratio 2015 2016 2015 2016

Asset Utilization Ratios

1) Inventory days 68 58 73 76

2) A/C Receivable days 8 15 5 15

Alpine Construction Ltd. Maple Builders Ltd.

According to the utilization ratio, inventory days and A/C receivable days are mainly

evaluated, where Alpine Construction Ltd has the highest value. This indicates that

management of Alpine Construction Ltd is effectively using its resources and generating high

level of cash flow. The inventory days of Maple Builders Ltd is relatively high at the 76 days,

while Alpine Construction Ltd has the level of 58, which indicates that Alpine Construction

Ltd has higher utilisation of inventory level. On the other hand, the changes in A/C

receivables days is relatively at the same level, which indicates that asset utilisation ratio of

Alpine Construction Ltd is relevantly high (Caro, Guardiola & Ortiz, 2018).

6

1.3 Depicting company who runs most efficiently:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

10

20

30

40

50

60

70

80

Asset Utilization Ratios

1) Inventory days 2) A/C Receivable days

Name of Ratio 2015 2016 2015 2016

Asset Utilization Ratios

1) Inventory days 68 58 73 76

2) A/C Receivable days 8 15 5 15

Alpine Construction Ltd. Maple Builders Ltd.

According to the utilization ratio, inventory days and A/C receivable days are mainly

evaluated, where Alpine Construction Ltd has the highest value. This indicates that

management of Alpine Construction Ltd is effectively using its resources and generating high

level of cash flow. The inventory days of Maple Builders Ltd is relatively high at the 76 days,

while Alpine Construction Ltd has the level of 58, which indicates that Alpine Construction

Ltd has higher utilisation of inventory level. On the other hand, the changes in A/C

receivables days is relatively at the same level, which indicates that asset utilisation ratio of

Alpine Construction Ltd is relevantly high (Caro, Guardiola & Ortiz, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

7

1.4 Depicting which subsidiary is in the best market position:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

0.5

1

1.5

2

2.5

3

3.5

4

Financial Market Ratios

1) EPS 2) DPS

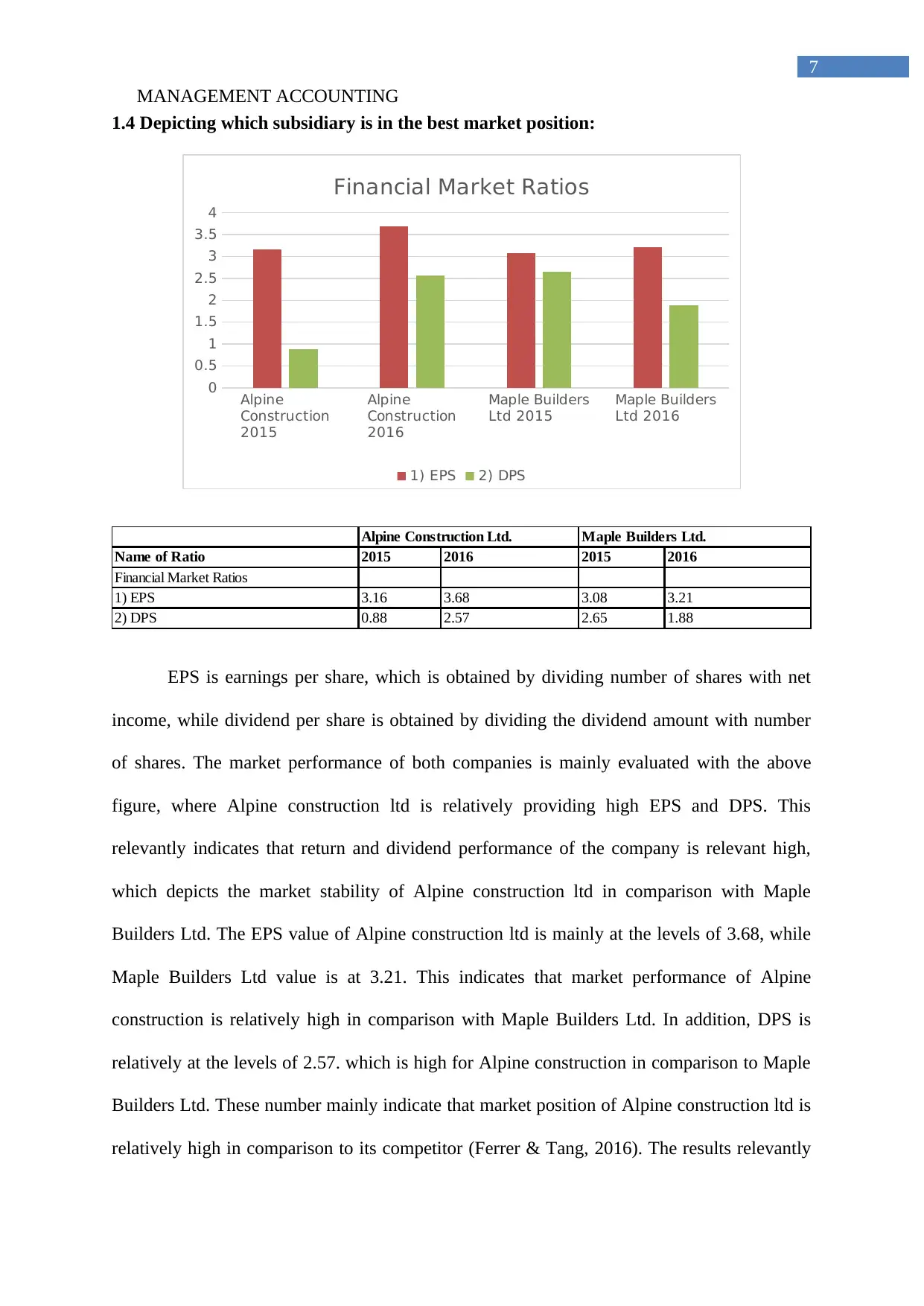

Name of Ratio 2015 2016 2015 2016

Financial Market Ratios

1) EPS 3.16 3.68 3.08 3.21

2) DPS 0.88 2.57 2.65 1.88

Alpine Construction Ltd. Maple Builders Ltd.

EPS is earnings per share, which is obtained by dividing number of shares with net

income, while dividend per share is obtained by dividing the dividend amount with number

of shares. The market performance of both companies is mainly evaluated with the above

figure, where Alpine construction ltd is relatively providing high EPS and DPS. This

relevantly indicates that return and dividend performance of the company is relevant high,

which depicts the market stability of Alpine construction ltd in comparison with Maple

Builders Ltd. The EPS value of Alpine construction ltd is mainly at the levels of 3.68, while

Maple Builders Ltd value is at 3.21. This indicates that market performance of Alpine

construction is relatively high in comparison with Maple Builders Ltd. In addition, DPS is

relatively at the levels of 2.57. which is high for Alpine construction in comparison to Maple

Builders Ltd. These number mainly indicate that market position of Alpine construction ltd is

relatively high in comparison to its competitor (Ferrer & Tang, 2016). The results relevantly

7

1.4 Depicting which subsidiary is in the best market position:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

0.5

1

1.5

2

2.5

3

3.5

4

Financial Market Ratios

1) EPS 2) DPS

Name of Ratio 2015 2016 2015 2016

Financial Market Ratios

1) EPS 3.16 3.68 3.08 3.21

2) DPS 0.88 2.57 2.65 1.88

Alpine Construction Ltd. Maple Builders Ltd.

EPS is earnings per share, which is obtained by dividing number of shares with net

income, while dividend per share is obtained by dividing the dividend amount with number

of shares. The market performance of both companies is mainly evaluated with the above

figure, where Alpine construction ltd is relatively providing high EPS and DPS. This

relevantly indicates that return and dividend performance of the company is relevant high,

which depicts the market stability of Alpine construction ltd in comparison with Maple

Builders Ltd. The EPS value of Alpine construction ltd is mainly at the levels of 3.68, while

Maple Builders Ltd value is at 3.21. This indicates that market performance of Alpine

construction is relatively high in comparison with Maple Builders Ltd. In addition, DPS is

relatively at the levels of 2.57. which is high for Alpine construction in comparison to Maple

Builders Ltd. These number mainly indicate that market position of Alpine construction ltd is

relatively high in comparison to its competitor (Ferrer & Tang, 2016). The results relevantly

MANAGEMENT ACCOUNTING

8

implies that EPS of Alpine construction ltd and Maple Builders Ltd is relevantly high due to

the net income generate by the company. However, the DPS of Alpine construction ltd has

relevantly improved due to the increment in dividends payment. On the other hand, Maple

Builders Ltd DPS mainly declined due to the low dividends paid by the company.

1.5 Depicting which subsidiary is the most solvent:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Stability/Solvency Ratios

1) Debt to assets 2) Debt to Equity

Name of Ratio 2015 2016 2015 2016

Solvency Ratios

1) Debt to assets 0.63:1 0.73:1 0.75:1 0.67:1

2) Debt to Equity 1.28 1.88 1.46 1.21

Alpine Construction Ltd. Maple Builders Ltd.

The solvency position of both the company from the evaluation could be detected,

which might help in understanding its overall financial status. The high value of debt to assets

and debt equity indicates the insolvency position that is been achieved by the company.

Hence, from the evaluation it could be detected that the solvency condition of Maple Builders

Ltd is relatively high, while the financial status of Alpine construction has deteriorated over

the fiscal year. The debt to asset of Alpine construction has increased from 0.63 to 0.73,

while debt to equity has increased from 1.28 to 1.88. this indicates that the company has been

8

implies that EPS of Alpine construction ltd and Maple Builders Ltd is relevantly high due to

the net income generate by the company. However, the DPS of Alpine construction ltd has

relevantly improved due to the increment in dividends payment. On the other hand, Maple

Builders Ltd DPS mainly declined due to the low dividends paid by the company.

1.5 Depicting which subsidiary is the most solvent:

Alpine

Construction

2015

Alpine

Construction

2016

Maple Builders

Ltd 2015

Maple Builders

Ltd 2016

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

Stability/Solvency Ratios

1) Debt to assets 2) Debt to Equity

Name of Ratio 2015 2016 2015 2016

Solvency Ratios

1) Debt to assets 0.63:1 0.73:1 0.75:1 0.67:1

2) Debt to Equity 1.28 1.88 1.46 1.21

Alpine Construction Ltd. Maple Builders Ltd.

The solvency position of both the company from the evaluation could be detected,

which might help in understanding its overall financial status. The high value of debt to assets

and debt equity indicates the insolvency position that is been achieved by the company.

Hence, from the evaluation it could be detected that the solvency condition of Maple Builders

Ltd is relatively high, while the financial status of Alpine construction has deteriorated over

the fiscal year. The debt to asset of Alpine construction has increased from 0.63 to 0.73,

while debt to equity has increased from 1.28 to 1.88. this indicates that the company has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MANAGEMENT ACCOUNTING

9

accumulating high debt for conducting its operations. However, Maple Builders Ltd has

relatively declined its overall debt accumulation, which indicate its financial strength and

positive solvency position.

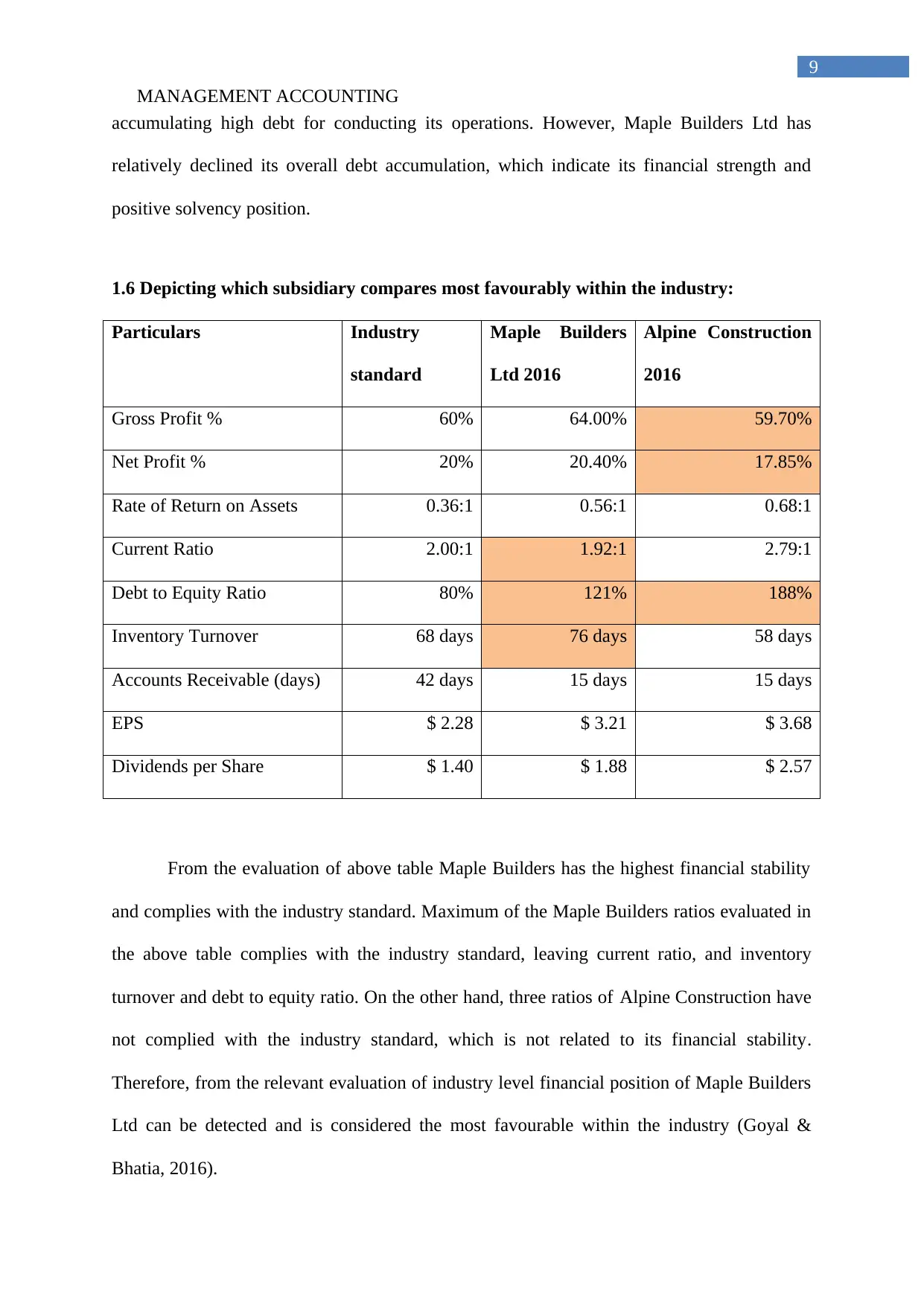

1.6 Depicting which subsidiary compares most favourably within the industry:

Particulars Industry

standard

Maple Builders

Ltd 2016

Alpine Construction

2016

Gross Profit % 60% 64.00% 59.70%

Net Profit % 20% 20.40% 17.85%

Rate of Return on Assets 0.36:1 0.56:1 0.68:1

Current Ratio 2.00:1 1.92:1 2.79:1

Debt to Equity Ratio 80% 121% 188%

Inventory Turnover 68 days 76 days 58 days

Accounts Receivable (days) 42 days 15 days 15 days

EPS $ 2.28 $ 3.21 $ 3.68

Dividends per Share $ 1.40 $ 1.88 $ 2.57

From the evaluation of above table Maple Builders has the highest financial stability

and complies with the industry standard. Maximum of the Maple Builders ratios evaluated in

the above table complies with the industry standard, leaving current ratio, and inventory

turnover and debt to equity ratio. On the other hand, three ratios of Alpine Construction have

not complied with the industry standard, which is not related to its financial stability.

Therefore, from the relevant evaluation of industry level financial position of Maple Builders

Ltd can be detected and is considered the most favourable within the industry (Goyal &

Bhatia, 2016).

9

accumulating high debt for conducting its operations. However, Maple Builders Ltd has

relatively declined its overall debt accumulation, which indicate its financial strength and

positive solvency position.

1.6 Depicting which subsidiary compares most favourably within the industry:

Particulars Industry

standard

Maple Builders

Ltd 2016

Alpine Construction

2016

Gross Profit % 60% 64.00% 59.70%

Net Profit % 20% 20.40% 17.85%

Rate of Return on Assets 0.36:1 0.56:1 0.68:1

Current Ratio 2.00:1 1.92:1 2.79:1

Debt to Equity Ratio 80% 121% 188%

Inventory Turnover 68 days 76 days 58 days

Accounts Receivable (days) 42 days 15 days 15 days

EPS $ 2.28 $ 3.21 $ 3.68

Dividends per Share $ 1.40 $ 1.88 $ 2.57

From the evaluation of above table Maple Builders has the highest financial stability

and complies with the industry standard. Maximum of the Maple Builders ratios evaluated in

the above table complies with the industry standard, leaving current ratio, and inventory

turnover and debt to equity ratio. On the other hand, three ratios of Alpine Construction have

not complied with the industry standard, which is not related to its financial stability.

Therefore, from the relevant evaluation of industry level financial position of Maple Builders

Ltd can be detected and is considered the most favourable within the industry (Goyal &

Bhatia, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

MANAGEMENT ACCOUNTING

10

2. Depicting the conclusion drawn from financial analysis, while depicting the company

with better financial health/position and why:

The evaluation of financial ratios mainly allows investors in detect financial health

and position of both the companies. In addition, the evaluation of financial position mainly

helps in detecting the relevant conditions, while making investment decisions. The financial

position of Maple Builders Ltd is relatively high in comparison with Alpine construction, as

the company is providing high end profits. Maple Builders Ltd has relatively increased the

number of profits, which could be generated from operations, which is detected from relevant

ratios. From the evaluation of ratios and comparisons from industry averages both the

companies have been providing adequate return (Johri & Maheshwari, 2015). However, the

evaluation of solvency position mainly helps in depicting the overall financial position of

Maple Builders Ltd over Alpine construction. This relevant high-end profit generated by

Maple Builders Ltd and its improving solvency position relevantly states the financial health

and position of the company in comparison with Alpine construction.

3. Recommendations for BC Ltd:

3.1 Recommendation for BC Ltd on which of the two companies it should divest from:

The evaluation of both the companies mainly helps in understanding their financial

position, which could help in detecting its ability to divest. The financial position of Maple

Builders Ltd is detected to have the most viable financial position in comparison with Alpine

construction. The financial ratios such as profitability, solvency and financial market ratios

mainly indicate the performance of Maple Builders Ltd, which might help in generating high

level of income from investment. Therefore, from the evaluation BC Ltd should divest from

with Alpine construction, as the financial position of the company is not increasing over the

period of two fiscal years.

10

2. Depicting the conclusion drawn from financial analysis, while depicting the company

with better financial health/position and why:

The evaluation of financial ratios mainly allows investors in detect financial health

and position of both the companies. In addition, the evaluation of financial position mainly

helps in detecting the relevant conditions, while making investment decisions. The financial

position of Maple Builders Ltd is relatively high in comparison with Alpine construction, as

the company is providing high end profits. Maple Builders Ltd has relatively increased the

number of profits, which could be generated from operations, which is detected from relevant

ratios. From the evaluation of ratios and comparisons from industry averages both the

companies have been providing adequate return (Johri & Maheshwari, 2015). However, the

evaluation of solvency position mainly helps in depicting the overall financial position of

Maple Builders Ltd over Alpine construction. This relevant high-end profit generated by

Maple Builders Ltd and its improving solvency position relevantly states the financial health

and position of the company in comparison with Alpine construction.

3. Recommendations for BC Ltd:

3.1 Recommendation for BC Ltd on which of the two companies it should divest from:

The evaluation of both the companies mainly helps in understanding their financial

position, which could help in detecting its ability to divest. The financial position of Maple

Builders Ltd is detected to have the most viable financial position in comparison with Alpine

construction. The financial ratios such as profitability, solvency and financial market ratios

mainly indicate the performance of Maple Builders Ltd, which might help in generating high

level of income from investment. Therefore, from the evaluation BC Ltd should divest from

with Alpine construction, as the financial position of the company is not increasing over the

period of two fiscal years.

MANAGEMENT ACCOUNTING

11

3.2 Suggesting three ways in which improvements in business can be conducted in the

company that is not recommended for divesting:

There are three ways in which relevant improvements of Maple Builders Ltd needs to

be steered, which might decline the deficiencies in its ratios.

The asset utilisation of relevant operations of the company needs to improve by

reducing the lag in inventory sales, which is derived from inventory ratios. The supply

of inventory needs to be improved by the organisation.

The increment in current ratio and quick ratio also needs to be conducted by the

company by reducing the current liability or increasing current assets.

Lastly, the increment in return on assets needs to increase, which is only possible by

effectively raising the level of revenue and net income of the organisation, which is

conducted by reducing the cost of sales and administrative expenses.

4. Dividend payments:

4.1 Explaining the Solvency Tests in accordance with the Companies Act 1993:

The relevant solvency test mainly allows directors of the company to evaluate the

financial position of the company. In addition, the Companies Act 1993 mainly focuses in

evaluating solvency test, which needs to be portrayed to its shareholder before making any

decisions. The solvency test mainly needs balance sheet limb, cash flow test to determine the

solvency position of the company. Moreover, the solvency test mainly requires section 4 of

the companies Act 1993, where both solvency limb and balance sheet limb need to be

evaluated. The liquidity limb and balance sheet limb mainly evaluate debt position of the

company, which might help in understanding its financial position. The value of company’s

11

3.2 Suggesting three ways in which improvements in business can be conducted in the

company that is not recommended for divesting:

There are three ways in which relevant improvements of Maple Builders Ltd needs to

be steered, which might decline the deficiencies in its ratios.

The asset utilisation of relevant operations of the company needs to improve by

reducing the lag in inventory sales, which is derived from inventory ratios. The supply

of inventory needs to be improved by the organisation.

The increment in current ratio and quick ratio also needs to be conducted by the

company by reducing the current liability or increasing current assets.

Lastly, the increment in return on assets needs to increase, which is only possible by

effectively raising the level of revenue and net income of the organisation, which is

conducted by reducing the cost of sales and administrative expenses.

4. Dividend payments:

4.1 Explaining the Solvency Tests in accordance with the Companies Act 1993:

The relevant solvency test mainly allows directors of the company to evaluate the

financial position of the company. In addition, the Companies Act 1993 mainly focuses in

evaluating solvency test, which needs to be portrayed to its shareholder before making any

decisions. The solvency test mainly needs balance sheet limb, cash flow test to determine the

solvency position of the company. Moreover, the solvency test mainly requires section 4 of

the companies Act 1993, where both solvency limb and balance sheet limb need to be

evaluated. The liquidity limb and balance sheet limb mainly evaluate debt position of the

company, which might help in understanding its financial position. The value of company’s

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.