Report: Analysis of Costing Methods in Management Accounting

VerifiedAdded on 2022/08/21

|9

|2224

|28

Report

AI Summary

This report provides a comprehensive analysis of costing methods in management accounting, comparing traditional and activity-based costing approaches within a coffee business context. It begins by calculating the predetermined overhead rate using traditional costing, then determines product costs and selling prices for Kona and Malaysian coffee. The report then delves into activity-based costing, calculating cost driver rates and allocating overheads based on various activities such as purchasing, material handling, and packaging. A detailed comparison of product costs derived from both methods reveals significant differences, with the report explaining the reasons for these variations. Finally, the report determines the selling prices for both coffee types using activity-based costing, taking into account a 30% profit margin. The conclusion summarizes the key findings, highlighting the strengths and weaknesses of each costing method and their impact on pricing and profitability.

1

Introduction to management

accounting

Introduction to management

accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2

Table of Contents

Introduction...............................................................................................................................3

1.................................................................................................................................................3

a) Calculation of predetermined overhead rate..............................................................3

b) Calculation of selling price and product cost..............................................................4

2.................................................................................................................................................4

3.................................................................................................................................................6

a) Product cost comparison...............................................................................................6

b) Selling price determination............................................................................................7

Conclusion................................................................................................................................7

References...............................................................................................................................9

Table of Contents

Introduction...............................................................................................................................3

1.................................................................................................................................................3

a) Calculation of predetermined overhead rate..............................................................3

b) Calculation of selling price and product cost..............................................................4

2.................................................................................................................................................4

3.................................................................................................................................................6

a) Product cost comparison...............................................................................................6

b) Selling price determination............................................................................................7

Conclusion................................................................................................................................7

References...............................................................................................................................9

3

Introduction

The company is involved in the coffee business and in that it is highly required that

there shall be ascertainment of the proper cost which can be used for various

purposes. The cost can be determined with the help of several approaches which

include traditional costing and activity-based costing. The report will be prepared and

in that there will be calculations which will be made for the calculation of cost by

using both the approaches.

1.

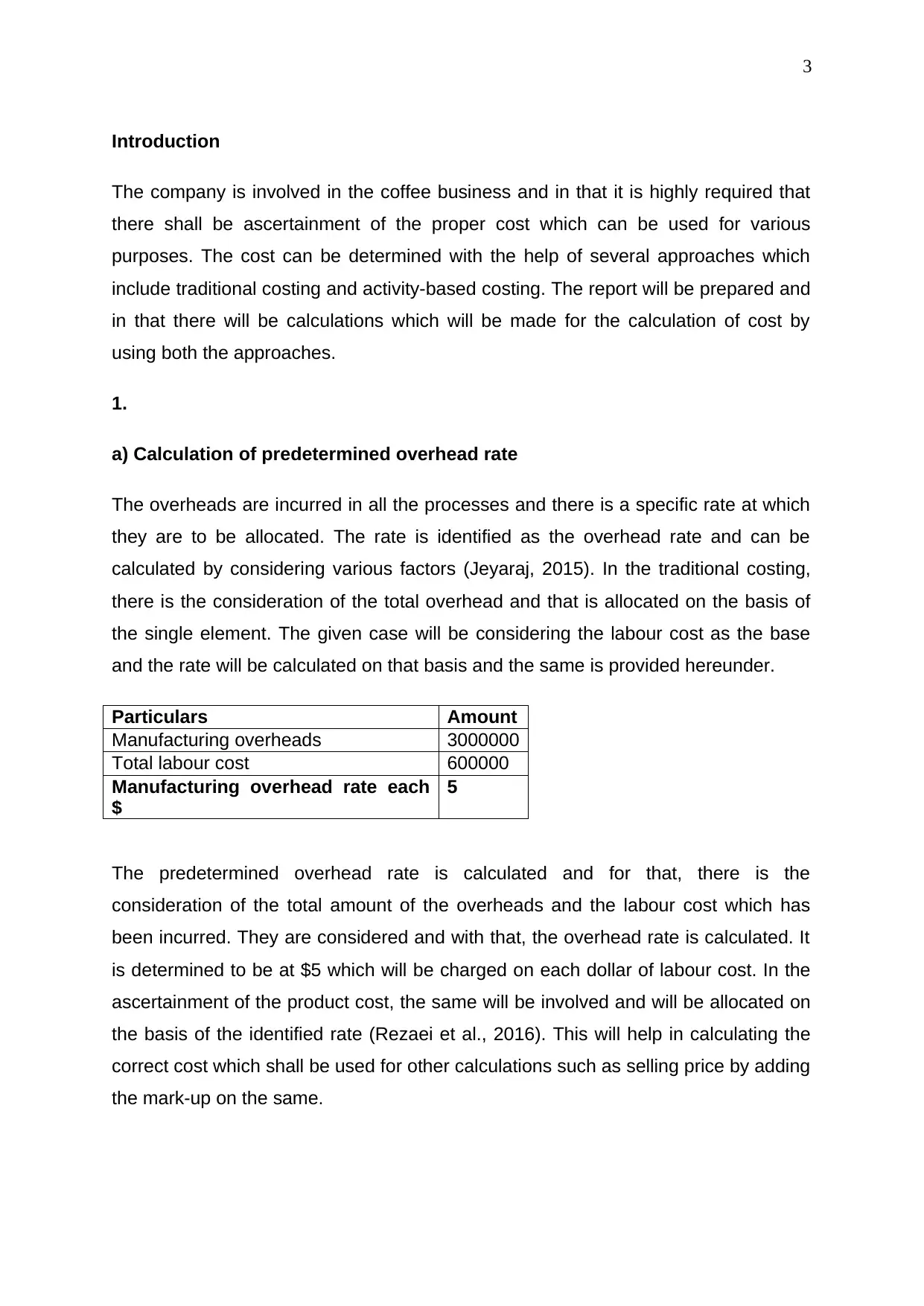

a) Calculation of predetermined overhead rate

The overheads are incurred in all the processes and there is a specific rate at which

they are to be allocated. The rate is identified as the overhead rate and can be

calculated by considering various factors (Jeyaraj, 2015). In the traditional costing,

there is the consideration of the total overhead and that is allocated on the basis of

the single element. The given case will be considering the labour cost as the base

and the rate will be calculated on that basis and the same is provided hereunder.

Particulars Amount

Manufacturing overheads 3000000

Total labour cost 600000

Manufacturing overhead rate each

$

5

The predetermined overhead rate is calculated and for that, there is the

consideration of the total amount of the overheads and the labour cost which has

been incurred. They are considered and with that, the overhead rate is calculated. It

is determined to be at $5 which will be charged on each dollar of labour cost. In the

ascertainment of the product cost, the same will be involved and will be allocated on

the basis of the identified rate (Rezaei et al., 2016). This will help in calculating the

correct cost which shall be used for other calculations such as selling price by adding

the mark-up on the same.

Introduction

The company is involved in the coffee business and in that it is highly required that

there shall be ascertainment of the proper cost which can be used for various

purposes. The cost can be determined with the help of several approaches which

include traditional costing and activity-based costing. The report will be prepared and

in that there will be calculations which will be made for the calculation of cost by

using both the approaches.

1.

a) Calculation of predetermined overhead rate

The overheads are incurred in all the processes and there is a specific rate at which

they are to be allocated. The rate is identified as the overhead rate and can be

calculated by considering various factors (Jeyaraj, 2015). In the traditional costing,

there is the consideration of the total overhead and that is allocated on the basis of

the single element. The given case will be considering the labour cost as the base

and the rate will be calculated on that basis and the same is provided hereunder.

Particulars Amount

Manufacturing overheads 3000000

Total labour cost 600000

Manufacturing overhead rate each

$

5

The predetermined overhead rate is calculated and for that, there is the

consideration of the total amount of the overheads and the labour cost which has

been incurred. They are considered and with that, the overhead rate is calculated. It

is determined to be at $5 which will be charged on each dollar of labour cost. In the

ascertainment of the product cost, the same will be involved and will be allocated on

the basis of the identified rate (Rezaei et al., 2016). This will help in calculating the

correct cost which shall be used for other calculations such as selling price by adding

the mark-up on the same.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4

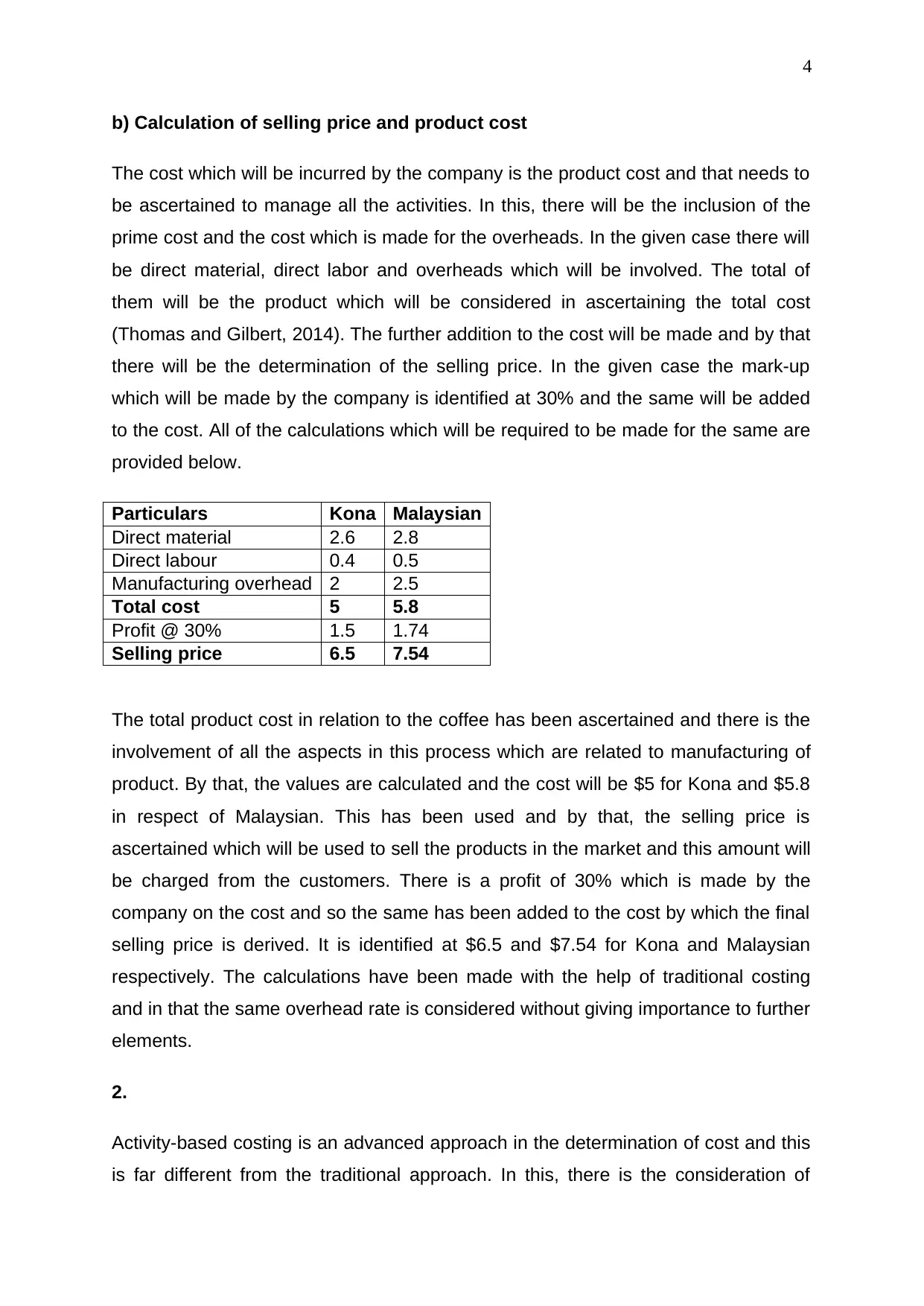

b) Calculation of selling price and product cost

The cost which will be incurred by the company is the product cost and that needs to

be ascertained to manage all the activities. In this, there will be the inclusion of the

prime cost and the cost which is made for the overheads. In the given case there will

be direct material, direct labor and overheads which will be involved. The total of

them will be the product which will be considered in ascertaining the total cost

(Thomas and Gilbert, 2014). The further addition to the cost will be made and by that

there will be the determination of the selling price. In the given case the mark-up

which will be made by the company is identified at 30% and the same will be added

to the cost. All of the calculations which will be required to be made for the same are

provided below.

Particulars Kona Malaysian

Direct material 2.6 2.8

Direct labour 0.4 0.5

Manufacturing overhead 2 2.5

Total cost 5 5.8

Profit @ 30% 1.5 1.74

Selling price 6.5 7.54

The total product cost in relation to the coffee has been ascertained and there is the

involvement of all the aspects in this process which are related to manufacturing of

product. By that, the values are calculated and the cost will be $5 for Kona and $5.8

in respect of Malaysian. This has been used and by that, the selling price is

ascertained which will be used to sell the products in the market and this amount will

be charged from the customers. There is a profit of 30% which is made by the

company on the cost and so the same has been added to the cost by which the final

selling price is derived. It is identified at $6.5 and $7.54 for Kona and Malaysian

respectively. The calculations have been made with the help of traditional costing

and in that the same overhead rate is considered without giving importance to further

elements.

2.

Activity-based costing is an advanced approach in the determination of cost and this

is far different from the traditional approach. In this, there is the consideration of

b) Calculation of selling price and product cost

The cost which will be incurred by the company is the product cost and that needs to

be ascertained to manage all the activities. In this, there will be the inclusion of the

prime cost and the cost which is made for the overheads. In the given case there will

be direct material, direct labor and overheads which will be involved. The total of

them will be the product which will be considered in ascertaining the total cost

(Thomas and Gilbert, 2014). The further addition to the cost will be made and by that

there will be the determination of the selling price. In the given case the mark-up

which will be made by the company is identified at 30% and the same will be added

to the cost. All of the calculations which will be required to be made for the same are

provided below.

Particulars Kona Malaysian

Direct material 2.6 2.8

Direct labour 0.4 0.5

Manufacturing overhead 2 2.5

Total cost 5 5.8

Profit @ 30% 1.5 1.74

Selling price 6.5 7.54

The total product cost in relation to the coffee has been ascertained and there is the

involvement of all the aspects in this process which are related to manufacturing of

product. By that, the values are calculated and the cost will be $5 for Kona and $5.8

in respect of Malaysian. This has been used and by that, the selling price is

ascertained which will be used to sell the products in the market and this amount will

be charged from the customers. There is a profit of 30% which is made by the

company on the cost and so the same has been added to the cost by which the final

selling price is derived. It is identified at $6.5 and $7.54 for Kona and Malaysian

respectively. The calculations have been made with the help of traditional costing

and in that the same overhead rate is considered without giving importance to further

elements.

2.

Activity-based costing is an advanced approach in the determination of cost and this

is far different from the traditional approach. In this, there is the consideration of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5

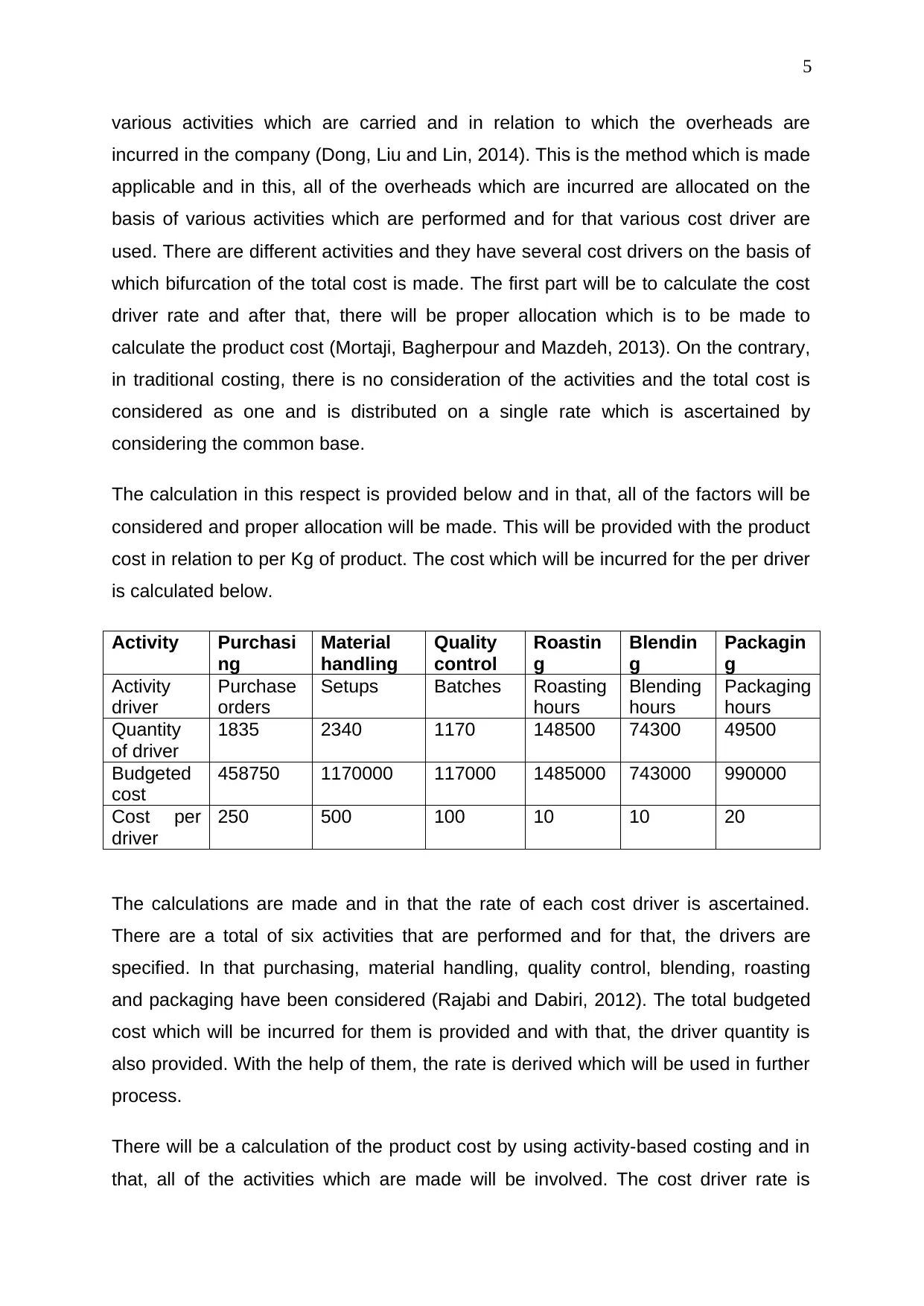

various activities which are carried and in relation to which the overheads are

incurred in the company (Dong, Liu and Lin, 2014). This is the method which is made

applicable and in this, all of the overheads which are incurred are allocated on the

basis of various activities which are performed and for that various cost driver are

used. There are different activities and they have several cost drivers on the basis of

which bifurcation of the total cost is made. The first part will be to calculate the cost

driver rate and after that, there will be proper allocation which is to be made to

calculate the product cost (Mortaji, Bagherpour and Mazdeh, 2013). On the contrary,

in traditional costing, there is no consideration of the activities and the total cost is

considered as one and is distributed on a single rate which is ascertained by

considering the common base.

The calculation in this respect is provided below and in that, all of the factors will be

considered and proper allocation will be made. This will be provided with the product

cost in relation to per Kg of product. The cost which will be incurred for the per driver

is calculated below.

Activity Purchasi

ng

Material

handling

Quality

control

Roastin

g

Blendin

g

Packagin

g

Activity

driver

Purchase

orders

Setups Batches Roasting

hours

Blending

hours

Packaging

hours

Quantity

of driver

1835 2340 1170 148500 74300 49500

Budgeted

cost

458750 1170000 117000 1485000 743000 990000

Cost per

driver

250 500 100 10 10 20

The calculations are made and in that the rate of each cost driver is ascertained.

There are a total of six activities that are performed and for that, the drivers are

specified. In that purchasing, material handling, quality control, blending, roasting

and packaging have been considered (Rajabi and Dabiri, 2012). The total budgeted

cost which will be incurred for them is provided and with that, the driver quantity is

also provided. With the help of them, the rate is derived which will be used in further

process.

There will be a calculation of the product cost by using activity-based costing and in

that, all of the activities which are made will be involved. The cost driver rate is

various activities which are carried and in relation to which the overheads are

incurred in the company (Dong, Liu and Lin, 2014). This is the method which is made

applicable and in this, all of the overheads which are incurred are allocated on the

basis of various activities which are performed and for that various cost driver are

used. There are different activities and they have several cost drivers on the basis of

which bifurcation of the total cost is made. The first part will be to calculate the cost

driver rate and after that, there will be proper allocation which is to be made to

calculate the product cost (Mortaji, Bagherpour and Mazdeh, 2013). On the contrary,

in traditional costing, there is no consideration of the activities and the total cost is

considered as one and is distributed on a single rate which is ascertained by

considering the common base.

The calculation in this respect is provided below and in that, all of the factors will be

considered and proper allocation will be made. This will be provided with the product

cost in relation to per Kg of product. The cost which will be incurred for the per driver

is calculated below.

Activity Purchasi

ng

Material

handling

Quality

control

Roastin

g

Blendin

g

Packagin

g

Activity

driver

Purchase

orders

Setups Batches Roasting

hours

Blending

hours

Packaging

hours

Quantity

of driver

1835 2340 1170 148500 74300 49500

Budgeted

cost

458750 1170000 117000 1485000 743000 990000

Cost per

driver

250 500 100 10 10 20

The calculations are made and in that the rate of each cost driver is ascertained.

There are a total of six activities that are performed and for that, the drivers are

specified. In that purchasing, material handling, quality control, blending, roasting

and packaging have been considered (Rajabi and Dabiri, 2012). The total budgeted

cost which will be incurred for them is provided and with that, the driver quantity is

also provided. With the help of them, the rate is derived which will be used in further

process.

There will be a calculation of the product cost by using activity-based costing and in

that, all of the activities which are made will be involved. The cost driver rate is

6

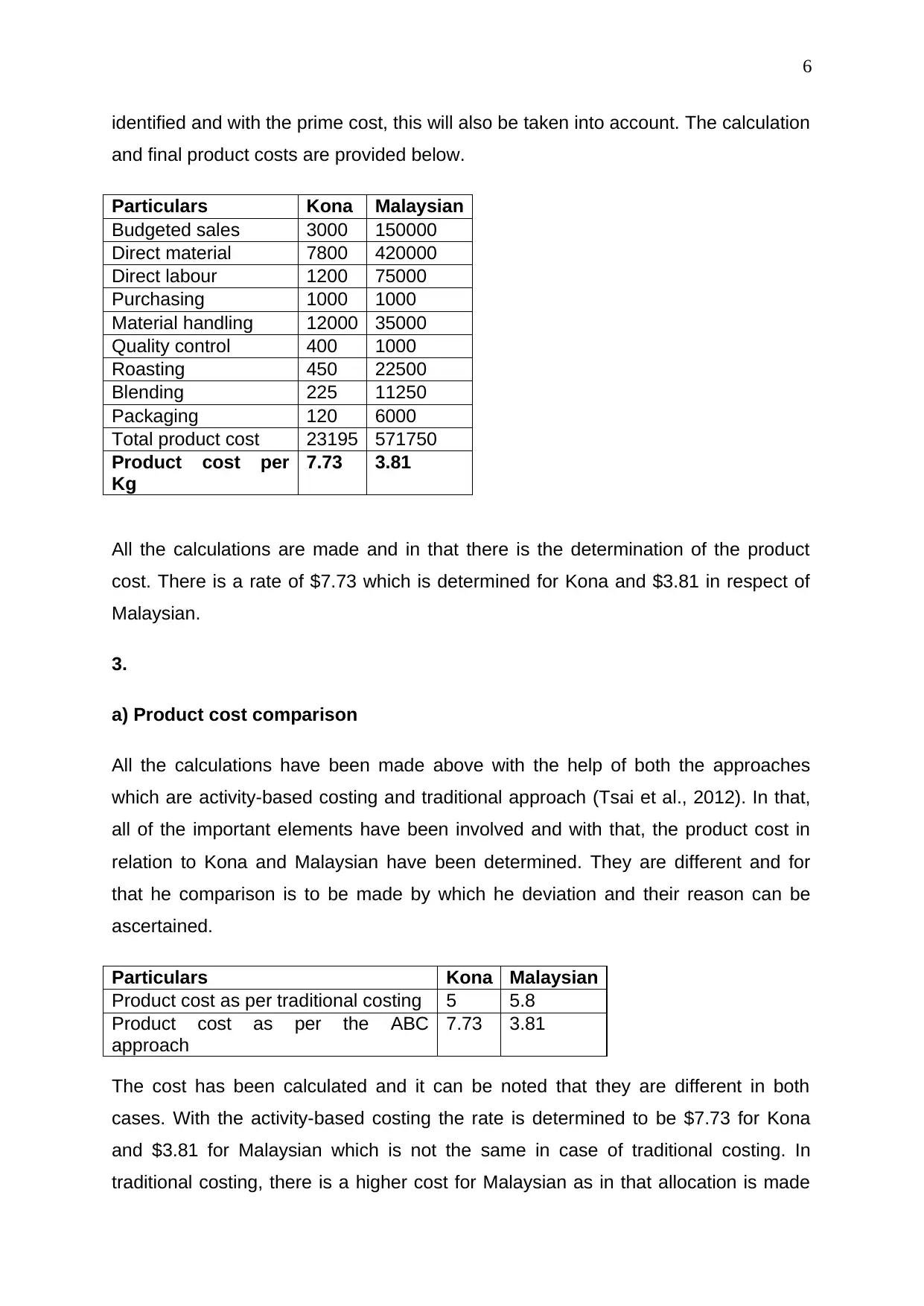

identified and with the prime cost, this will also be taken into account. The calculation

and final product costs are provided below.

Particulars Kona Malaysian

Budgeted sales 3000 150000

Direct material 7800 420000

Direct labour 1200 75000

Purchasing 1000 1000

Material handling 12000 35000

Quality control 400 1000

Roasting 450 22500

Blending 225 11250

Packaging 120 6000

Total product cost 23195 571750

Product cost per

Kg

7.73 3.81

All the calculations are made and in that there is the determination of the product

cost. There is a rate of $7.73 which is determined for Kona and $3.81 in respect of

Malaysian.

3.

a) Product cost comparison

All the calculations have been made above with the help of both the approaches

which are activity-based costing and traditional approach (Tsai et al., 2012). In that,

all of the important elements have been involved and with that, the product cost in

relation to Kona and Malaysian have been determined. They are different and for

that he comparison is to be made by which he deviation and their reason can be

ascertained.

Particulars Kona Malaysian

Product cost as per traditional costing 5 5.8

Product cost as per the ABC

approach

7.73 3.81

The cost has been calculated and it can be noted that they are different in both

cases. With the activity-based costing the rate is determined to be $7.73 for Kona

and $3.81 for Malaysian which is not the same in case of traditional costing. In

traditional costing, there is a higher cost for Malaysian as in that allocation is made

identified and with the prime cost, this will also be taken into account. The calculation

and final product costs are provided below.

Particulars Kona Malaysian

Budgeted sales 3000 150000

Direct material 7800 420000

Direct labour 1200 75000

Purchasing 1000 1000

Material handling 12000 35000

Quality control 400 1000

Roasting 450 22500

Blending 225 11250

Packaging 120 6000

Total product cost 23195 571750

Product cost per

Kg

7.73 3.81

All the calculations are made and in that there is the determination of the product

cost. There is a rate of $7.73 which is determined for Kona and $3.81 in respect of

Malaysian.

3.

a) Product cost comparison

All the calculations have been made above with the help of both the approaches

which are activity-based costing and traditional approach (Tsai et al., 2012). In that,

all of the important elements have been involved and with that, the product cost in

relation to Kona and Malaysian have been determined. They are different and for

that he comparison is to be made by which he deviation and their reason can be

ascertained.

Particulars Kona Malaysian

Product cost as per traditional costing 5 5.8

Product cost as per the ABC

approach

7.73 3.81

The cost has been calculated and it can be noted that they are different in both

cases. With the activity-based costing the rate is determined to be $7.73 for Kona

and $3.81 for Malaysian which is not the same in case of traditional costing. In

traditional costing, there is a higher cost for Malaysian as in that allocation is made

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

7

by labor cost and the same is higher for it. This is not the case with other approach

and in that, all the areas are considered and by that cost declined in the Malaysian.

This single factor is not considered and there is the involvement of all the activities

which lead to the proper and reasonable allocation of total overheads (Elhamma and

Zhang, 2013). There are more quantities that are involved in Malaysian and so the

number of batches and set-ups are affected by the same. There is the saving of cost

in this respect and by that the overall cost which is incurred is declined.

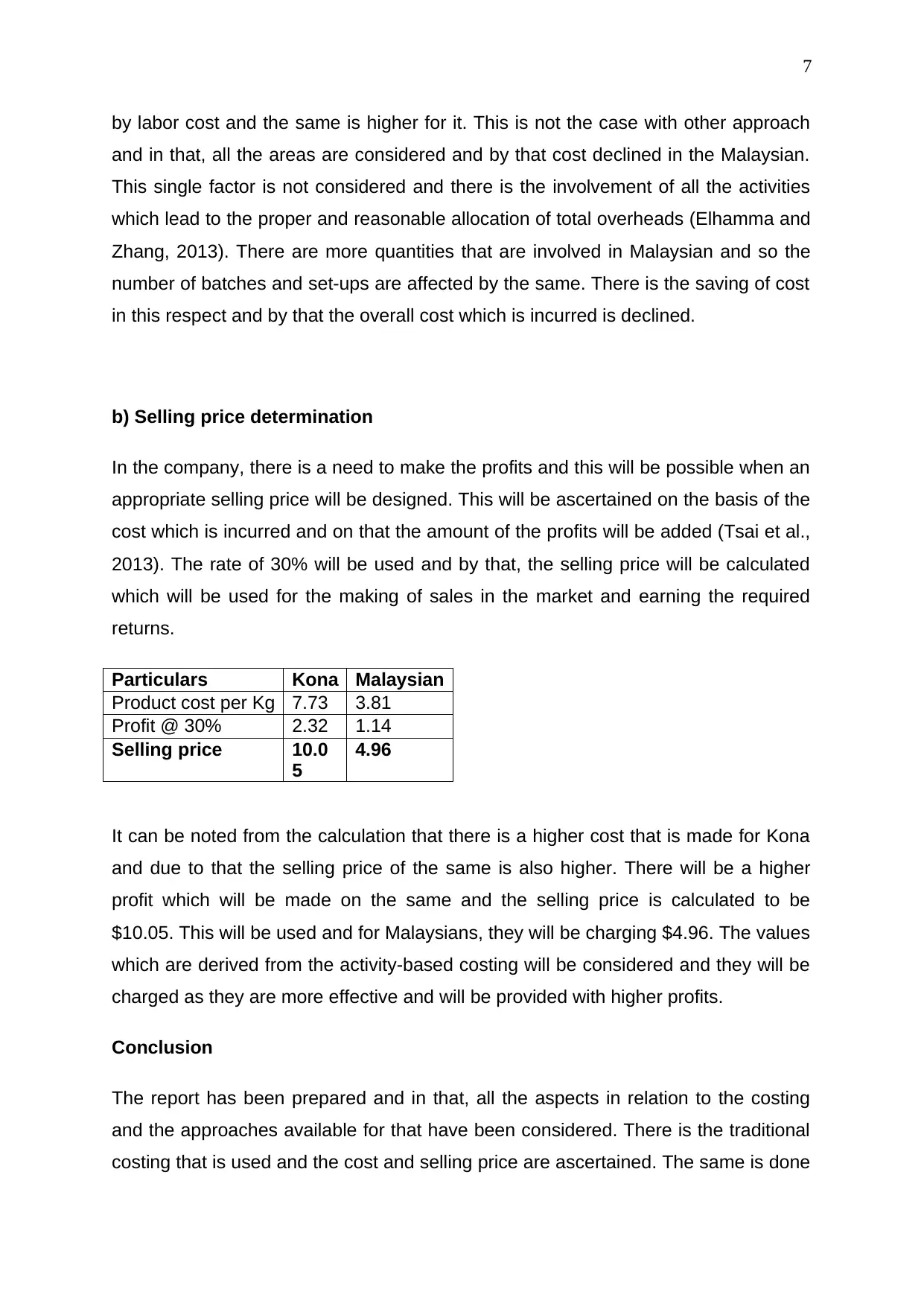

b) Selling price determination

In the company, there is a need to make the profits and this will be possible when an

appropriate selling price will be designed. This will be ascertained on the basis of the

cost which is incurred and on that the amount of the profits will be added (Tsai et al.,

2013). The rate of 30% will be used and by that, the selling price will be calculated

which will be used for the making of sales in the market and earning the required

returns.

Particulars Kona Malaysian

Product cost per Kg 7.73 3.81

Profit @ 30% 2.32 1.14

Selling price 10.0

5

4.96

It can be noted from the calculation that there is a higher cost that is made for Kona

and due to that the selling price of the same is also higher. There will be a higher

profit which will be made on the same and the selling price is calculated to be

$10.05. This will be used and for Malaysians, they will be charging $4.96. The values

which are derived from the activity-based costing will be considered and they will be

charged as they are more effective and will be provided with higher profits.

Conclusion

The report has been prepared and in that, all the aspects in relation to the costing

and the approaches available for that have been considered. There is the traditional

costing that is used and the cost and selling price are ascertained. The same is done

by labor cost and the same is higher for it. This is not the case with other approach

and in that, all the areas are considered and by that cost declined in the Malaysian.

This single factor is not considered and there is the involvement of all the activities

which lead to the proper and reasonable allocation of total overheads (Elhamma and

Zhang, 2013). There are more quantities that are involved in Malaysian and so the

number of batches and set-ups are affected by the same. There is the saving of cost

in this respect and by that the overall cost which is incurred is declined.

b) Selling price determination

In the company, there is a need to make the profits and this will be possible when an

appropriate selling price will be designed. This will be ascertained on the basis of the

cost which is incurred and on that the amount of the profits will be added (Tsai et al.,

2013). The rate of 30% will be used and by that, the selling price will be calculated

which will be used for the making of sales in the market and earning the required

returns.

Particulars Kona Malaysian

Product cost per Kg 7.73 3.81

Profit @ 30% 2.32 1.14

Selling price 10.0

5

4.96

It can be noted from the calculation that there is a higher cost that is made for Kona

and due to that the selling price of the same is also higher. There will be a higher

profit which will be made on the same and the selling price is calculated to be

$10.05. This will be used and for Malaysians, they will be charging $4.96. The values

which are derived from the activity-based costing will be considered and they will be

charged as they are more effective and will be provided with higher profits.

Conclusion

The report has been prepared and in that, all the aspects in relation to the costing

and the approaches available for that have been considered. There is the traditional

costing that is used and the cost and selling price are ascertained. The same is done

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

8

in case of activity-based costing and then the results of both have been compared

with one other. The causes because of which they are different are also identified

and also the profits which will be made have been accounted for.

in case of activity-based costing and then the results of both have been compared

with one other. The causes because of which they are different are also identified

and also the profits which will be made have been accounted for.

9

References

Dong, J., Liu, C. and Lin, Z. (2014) Charging infrastructure planning for promoting

battery electric vehicles: An activity-based approach using multiday travel

data. Transportation Research Part C: Emerging Technologies, 38, pp.44-55.

Elhamma, A. and Zhang, Y.I. (2013) The relationship between activity-based costing,

business strategy and performance in Moroccan enterprises. Accounting and

Management Information Systems, 12(1), p.22.

Jeyaraj, S.S. (2015) Activity Based Costing vs Volume Based Costing: Relevance

and Applicability. The international journal of management, 4, pp.39-46.

Mortaji, S.T.H., Bagherpour, M. and Mazdeh, M.M. (2013) Fuzzy time-driven activity-

based costing. Engineering Management Journal, 25(3), pp.63-73.

Rajabi, A. and Dabiri, A. (2012) Applying activity-based costing (ABC) method to

calculate cost price in hospital and remedy services. Iranian journal of public

health, 41(4), p.100.

Rezaei, J., Nispeling, T., Sarkis, J. and Tavasszy, L. (2016) A supplier selection life

cycle approach integrating traditional and environmental criteria using the best worst

method. Journal of Cleaner Production, 135, pp.577-588.

Thomas, D.S. and Gilbert, S.W. (2014) Costs and cost-effectiveness of additive

manufacturing. NIST special publication, 1176, p.12.

Tsai, W.H., Chen, H.C., Leu, J.D., Chang, Y.C. and Lin, T.W. (2013) A product-mix

decision model using green manufacturing technologies under activity-based

costing. Journal of cleaner production, 57, pp.178-187.

Tsai, W.H., Shen, Y.S., Lee, P.L., Chen, H.C., Kuo, L. and Huang, C.C. (2012)

Integrating information about the cost of carbon through activity-based

costing. Journal of Cleaner Production, 36, pp.102-111.

References

Dong, J., Liu, C. and Lin, Z. (2014) Charging infrastructure planning for promoting

battery electric vehicles: An activity-based approach using multiday travel

data. Transportation Research Part C: Emerging Technologies, 38, pp.44-55.

Elhamma, A. and Zhang, Y.I. (2013) The relationship between activity-based costing,

business strategy and performance in Moroccan enterprises. Accounting and

Management Information Systems, 12(1), p.22.

Jeyaraj, S.S. (2015) Activity Based Costing vs Volume Based Costing: Relevance

and Applicability. The international journal of management, 4, pp.39-46.

Mortaji, S.T.H., Bagherpour, M. and Mazdeh, M.M. (2013) Fuzzy time-driven activity-

based costing. Engineering Management Journal, 25(3), pp.63-73.

Rajabi, A. and Dabiri, A. (2012) Applying activity-based costing (ABC) method to

calculate cost price in hospital and remedy services. Iranian journal of public

health, 41(4), p.100.

Rezaei, J., Nispeling, T., Sarkis, J. and Tavasszy, L. (2016) A supplier selection life

cycle approach integrating traditional and environmental criteria using the best worst

method. Journal of Cleaner Production, 135, pp.577-588.

Thomas, D.S. and Gilbert, S.W. (2014) Costs and cost-effectiveness of additive

manufacturing. NIST special publication, 1176, p.12.

Tsai, W.H., Chen, H.C., Leu, J.D., Chang, Y.C. and Lin, T.W. (2013) A product-mix

decision model using green manufacturing technologies under activity-based

costing. Journal of cleaner production, 57, pp.178-187.

Tsai, W.H., Shen, Y.S., Lee, P.L., Chen, H.C., Kuo, L. and Huang, C.C. (2012)

Integrating information about the cost of carbon through activity-based

costing. Journal of Cleaner Production, 36, pp.102-111.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.