A Comparative Analysis of Credit Institutions in Provision of Credit

VerifiedAdded on 2021/04/16

|19

|4443

|125

Report

AI Summary

This report offers a comparative analysis of credit institutions in the provision of credit. It begins with an introduction outlining the importance of credit institutions in financing businesses and projects, followed by a background study highlighting the role of credit in economic development and the challenges faced by small lenders. The literature review explores theoretical frameworks, the provision of financial services, and debates within the literature, including the linkages between formal and informal financial institutions. The report examines the characteristics of both formal and informal credit institutions, including microfinance institutions, and analyzes their varying approaches to providing credit, transaction costs, and the challenges they face. The study emphasizes the importance of understanding the regulations and policies of credit institutions to make informed decisions, especially for individuals seeking loans. The report concludes with a critical analysis and references, offering a comprehensive overview of credit institutions and their role in financial services.

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 1

Comparative Analysis of Credit Institutions in Provision of Credit.

By [Name]

Course

Professor’s Name

Institution

Location of Institution

Date

Comparative Analysis of Credit Institutions in Provision of Credit.

By [Name]

Course

Professor’s Name

Institution

Location of Institution

Date

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 2

Table of Contents

Comparative Analysis of Credit Institutions in Provision of Credit..............................3

1.0 Brief introduction............................................................................................... 3

1.1 Background of the study...................................................................................3

1.2 Justification........................................................................................................ 5

1.3 Business discipline and academic areas related to the research......................5

LITERATURE REVIEW.................................................................................................. 6

2.1 Introduction....................................................................................................... 6

2.2 Theoretical framework...................................................................................... 6

2.3 Provision of financial services...........................................................................7

2.4 Debates within the literature.............................................................................8

2.5 Linkages between formal and informal financial institutions............................9

2.6 Conceptual framework....................................................................................10

2.7 Summary of literature review..........................................................................11

3.0 Critical Analysis of a Text................................................................................... 11

4.0 References........................................................................................................ 16

Table of Contents

Comparative Analysis of Credit Institutions in Provision of Credit..............................3

1.0 Brief introduction............................................................................................... 3

1.1 Background of the study...................................................................................3

1.2 Justification........................................................................................................ 5

1.3 Business discipline and academic areas related to the research......................5

LITERATURE REVIEW.................................................................................................. 6

2.1 Introduction....................................................................................................... 6

2.2 Theoretical framework...................................................................................... 6

2.3 Provision of financial services...........................................................................7

2.4 Debates within the literature.............................................................................8

2.5 Linkages between formal and informal financial institutions............................9

2.6 Conceptual framework....................................................................................10

2.7 Summary of literature review..........................................................................11

3.0 Critical Analysis of a Text................................................................................... 11

4.0 References........................................................................................................ 16

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 3

Comparative Analysis of Credit Institutions in Provision of Credit.

1.0 Brief introduction

A credit institution is an official chartered institution that receives deposits, provide

savings and checking accounts, and provide loans among other services. This paper will research

credit institutions in providing credit. Many people or firms take loans to finance their businesses

to do major projects, credit institution has been to their rescue in providing them with this funds

and paying later at a profit (Crouhy et al, 200). Before getting credit from the credit institutions,

some documents must be filled, and collateral is taken to the bank. The amount of money, which

can be loaned to the individual, depends on the value of the collateral

When there is breach in contract by the borrower, the credit institution with the help of

law has the right to take the collateral that is of the same value as the credit given and trade it to

compensate for the loss. Credit institutions have been of great benefit to small businesses and the

government since it contributes to the development of economy by funding entrepreneurs to start

their own business (Mosley & Hulme, 2006). Therefore, this paper will analyze credit

institutions in the provision of credit.

1.1 Background of the study

Provision of credit has widely been considered as one of the most important sources of

finance for most people in the world at large. Greater populations in the country both in the rural

and urban areas acquire credit from various credit institutions to facilitate their developmental

activities (Muldrew, 2016). Loans help increase family income and therefore help the less

Comparative Analysis of Credit Institutions in Provision of Credit.

1.0 Brief introduction

A credit institution is an official chartered institution that receives deposits, provide

savings and checking accounts, and provide loans among other services. This paper will research

credit institutions in providing credit. Many people or firms take loans to finance their businesses

to do major projects, credit institution has been to their rescue in providing them with this funds

and paying later at a profit (Crouhy et al, 200). Before getting credit from the credit institutions,

some documents must be filled, and collateral is taken to the bank. The amount of money, which

can be loaned to the individual, depends on the value of the collateral

When there is breach in contract by the borrower, the credit institution with the help of

law has the right to take the collateral that is of the same value as the credit given and trade it to

compensate for the loss. Credit institutions have been of great benefit to small businesses and the

government since it contributes to the development of economy by funding entrepreneurs to start

their own business (Mosley & Hulme, 2006). Therefore, this paper will analyze credit

institutions in the provision of credit.

1.1 Background of the study

Provision of credit has widely been considered as one of the most important sources of

finance for most people in the world at large. Greater populations in the country both in the rural

and urban areas acquire credit from various credit institutions to facilitate their developmental

activities (Muldrew, 2016). Loans help increase family income and therefore help the less

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 4

fortune collect their capital funds and therefore enable them to invest in activities that generate

employment

With the growing population and an increasing lack of employment, more people acquire

loans to fund their entrepreneurial projects. However, financial institutions such as commercial

banks are reluctant when it comes to catering to the needs of small lenders as per their lending

terms and conditions (Chaibi and Ftiti, 2015). There is a myth in financial institutions that it is

almost impossible to loan the poor as they cannot present the required security or collateral and

therefore considered as un-creditworthy

In accordance with some survey (Leone and Porretta, 2014), most people are

withdrawing from SACCOS, and this begs for the question, what is happening with the provision

of credit in SACCOS now that was not earlier before. This is in line with the fact that in the

recent past years, SACCOS were considered the best in the provision of credit

Alongside formal financial institutions, Informal financial institutions have also

embraced financial transactions relating to the provision of credit in many countries Knowledge

acquired after informal finance indicates that most of the rural poor, a good example being

women, in most get better access to the informal credit facilities as compared to the formal

sources. This has also been proven as per the reports obtained from the surveys of credit the

markets. This, in turn, leads to the question: Why have informal financial institutions succeeded

even in circumstances where formal institutions have failed?

Another credit institution that has grown over time is the category of microfinance

institutions. One of their main features is that they do have a large number of clients regardless

of the fact that their total asset base is so small as compared to the traditional financial

institutions. They provide credit to the less fortunate who do not have or have little collateral and

fortune collect their capital funds and therefore enable them to invest in activities that generate

employment

With the growing population and an increasing lack of employment, more people acquire

loans to fund their entrepreneurial projects. However, financial institutions such as commercial

banks are reluctant when it comes to catering to the needs of small lenders as per their lending

terms and conditions (Chaibi and Ftiti, 2015). There is a myth in financial institutions that it is

almost impossible to loan the poor as they cannot present the required security or collateral and

therefore considered as un-creditworthy

In accordance with some survey (Leone and Porretta, 2014), most people are

withdrawing from SACCOS, and this begs for the question, what is happening with the provision

of credit in SACCOS now that was not earlier before. This is in line with the fact that in the

recent past years, SACCOS were considered the best in the provision of credit

Alongside formal financial institutions, Informal financial institutions have also

embraced financial transactions relating to the provision of credit in many countries Knowledge

acquired after informal finance indicates that most of the rural poor, a good example being

women, in most get better access to the informal credit facilities as compared to the formal

sources. This has also been proven as per the reports obtained from the surveys of credit the

markets. This, in turn, leads to the question: Why have informal financial institutions succeeded

even in circumstances where formal institutions have failed?

Another credit institution that has grown over time is the category of microfinance

institutions. One of their main features is that they do have a large number of clients regardless

of the fact that their total asset base is so small as compared to the traditional financial

institutions. They provide credit to the less fortunate who do not have or have little collateral and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 5

in most cases possess minimal business experience (Tang & Guo, 2017). Another feature is that

they hold loan portfolios that are poorly diversified since their target households tend to come

from the same region and furthermore often practice similar activities. This situation makes the

MFIs operate under information asymmetry among there borrowers and as subjects of high

default risk.

It is therefore evident that there is a huge disparity in the provision of credit between both

the formal and informal institutions in general. This study will be aimed at analyzing these

variations and their roles in access s and provision of credit to individuals.

1.2 Justification

The findings of this study will reveal the shortcomings of the policy used by credit

institutions thus important in policymaking. It will determine places that should be emphasized

and corrected

The study is also of significant value especially at the time when most people were

considering taking loans from credit institutions but failed to understand the regulations. This

mainly focused on the ordinary human beings who are speculating enjoying credit facilities.

The study is also of assistance to the existing credit institutions. Since most of the

institutions are competitors for the same market, they were able to gauge what competitive edge

one institution had from the other.

1.3 Business discipline and academic areas related to the research

The research report is related to many disciplines like finance, business management,

accounting, human resource, marketing among others. It is related to finance, accounting,

in most cases possess minimal business experience (Tang & Guo, 2017). Another feature is that

they hold loan portfolios that are poorly diversified since their target households tend to come

from the same region and furthermore often practice similar activities. This situation makes the

MFIs operate under information asymmetry among there borrowers and as subjects of high

default risk.

It is therefore evident that there is a huge disparity in the provision of credit between both

the formal and informal institutions in general. This study will be aimed at analyzing these

variations and their roles in access s and provision of credit to individuals.

1.2 Justification

The findings of this study will reveal the shortcomings of the policy used by credit

institutions thus important in policymaking. It will determine places that should be emphasized

and corrected

The study is also of significant value especially at the time when most people were

considering taking loans from credit institutions but failed to understand the regulations. This

mainly focused on the ordinary human beings who are speculating enjoying credit facilities.

The study is also of assistance to the existing credit institutions. Since most of the

institutions are competitors for the same market, they were able to gauge what competitive edge

one institution had from the other.

1.3 Business discipline and academic areas related to the research

The research report is related to many disciplines like finance, business management,

accounting, human resource, marketing among others. It is related to finance, accounting,

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 6

actuarial, statistic and economics such that bank rates are used by the financial manager to

calculate the probability of the company getting loss or gain if they borrow given amount

(Siqueira et al, 2016). Sales and marketing people use the research topic to see the area of

influence and to advise their clients.

LITERATURE REVIEW

2.1 Introduction

This chapter will help to review the existing literature based on credit institutions and

provision of credit. It mainly focuses on the features of these institutions and how the differences

affect the mentality of lenders, which in turn generates to how they are viewed regarding the

provision of credit. This chapter also forms the basis for which a conceptual framework will be

done later on.

2.2 Theoretical framework

A lot of research work has tried to outline the various functions of credit institutions.

Theoretical analysis majorly bases their arguments on the informal sector. According to Amaral

and Quintin (2006), there are four major approaches used by informal institutions for providing

credit. These approaches include lending to individuals, incorporated credit models, lending to

community-based businesses and group-based minimalists’ credit systems.

As per the minimalist approach, there is the provision of credit even without any form of

support. The group-based approach tends to use already formed groups that are in existence or

newly formed ones. The functionality of this approach is based on the principle that

entrepreneurs view credit as one of the important things in putting a business. According to this

actuarial, statistic and economics such that bank rates are used by the financial manager to

calculate the probability of the company getting loss or gain if they borrow given amount

(Siqueira et al, 2016). Sales and marketing people use the research topic to see the area of

influence and to advise their clients.

LITERATURE REVIEW

2.1 Introduction

This chapter will help to review the existing literature based on credit institutions and

provision of credit. It mainly focuses on the features of these institutions and how the differences

affect the mentality of lenders, which in turn generates to how they are viewed regarding the

provision of credit. This chapter also forms the basis for which a conceptual framework will be

done later on.

2.2 Theoretical framework

A lot of research work has tried to outline the various functions of credit institutions.

Theoretical analysis majorly bases their arguments on the informal sector. According to Amaral

and Quintin (2006), there are four major approaches used by informal institutions for providing

credit. These approaches include lending to individuals, incorporated credit models, lending to

community-based businesses and group-based minimalists’ credit systems.

As per the minimalist approach, there is the provision of credit even without any form of

support. The group-based approach tends to use already formed groups that are in existence or

newly formed ones. The functionality of this approach is based on the principle that

entrepreneurs view credit as one of the important things in putting a business. According to this

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 7

approach, credit is offered to small groups that guarantee the loans provided to their members

(Amaral and Quintin, 2006). The members need to make a weekly contribution to a joined

account baring the name of the group. This account acts as a loan guarantee fund and as a saving

account for every member. The members are allowed to receive another loan only after they have

paid the first loan. This, therefore, ensures responsibility of the members.

In the integrated model, there is a combination of credit with technical assistance and

training (Amaral and Quintin, 2006). Individuals who require loans interact directly with the loan

officers. Before any loan is granted, there have to be either one or two guarantors who will

guarantee the loan. The funds used in training and offering technical assistance makes this

approach expensive.

2.3 Provision of financial services

Provision of credit by financial institutions is normally viewed as one of the restrictions

limiting their gain from borrowers. Most credit institutions, especially the formal financial

institutions prohibit the problem of accessibility, which is displayed in the form of complicated

application procedures, prearranged minimum loan amounts and restrictions put on credits

obtained for specific purposes (Demirgüç-Kunt & Singer, 2017).

More problems occur on the side of borrowers who are smallholders and poor. The

requirements such as collateral tend to stand in their way, which should be the case. As long as

there are proper procedures for disbursement, proper supervision and repayment dates have been

established; the poor will be able to obtain loans and repay them. Moreover putting high-interest

rates on credits, helps discourage the influential non-targeted credit program. This clearly

approach, credit is offered to small groups that guarantee the loans provided to their members

(Amaral and Quintin, 2006). The members need to make a weekly contribution to a joined

account baring the name of the group. This account acts as a loan guarantee fund and as a saving

account for every member. The members are allowed to receive another loan only after they have

paid the first loan. This, therefore, ensures responsibility of the members.

In the integrated model, there is a combination of credit with technical assistance and

training (Amaral and Quintin, 2006). Individuals who require loans interact directly with the loan

officers. Before any loan is granted, there have to be either one or two guarantors who will

guarantee the loan. The funds used in training and offering technical assistance makes this

approach expensive.

2.3 Provision of financial services

Provision of credit by financial institutions is normally viewed as one of the restrictions

limiting their gain from borrowers. Most credit institutions, especially the formal financial

institutions prohibit the problem of accessibility, which is displayed in the form of complicated

application procedures, prearranged minimum loan amounts and restrictions put on credits

obtained for specific purposes (Demirgüç-Kunt & Singer, 2017).

More problems occur on the side of borrowers who are smallholders and poor. The

requirements such as collateral tend to stand in their way, which should be the case. As long as

there are proper procedures for disbursement, proper supervision and repayment dates have been

established; the poor will be able to obtain loans and repay them. Moreover putting high-interest

rates on credits, helps discourage the influential non-targeted credit program. This clearly

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 8

indicates the necessity to build up appropriate institutions that will conveniently provide the

small-scale borrowers with loans (Coleman, 2016).

Microfinance institutions, on the other hand, put in place more lenient policies on the

provision of credit, which have been an added advantage to them. Microfinance institutions

attempt to overcome problems of contract enforcement and imperfect information (Martinez-

Sola et al., 2014). This is through the development of non-traditional mechanisms that are

necessary for screening applicants, monitoring borrowers’ actions and the creation of incentives

to repay. Traditionally, microfinance institutions have depended on donor funds, and subsidies as

raising funds on the commercial basis have rendered difficult. Because of these irregularities,

one wonders whether these institutions should be regulated (Demirgüç-Kunt & Singer, 2017).

2.4 Debates within the literature

Credit institutions have been characterized by their varying ways of providing credit to

borrowers. The informal institutions mainly show the inability to satisfy the existing demand

especially in the rural areas that is their main target. According to Straub (2005), the small size

of resource controlled by the informal sector has been the main reason for its inability while the

difficulty in administration of loan like risk of default, monitoring and screening and high cost of

transaction has affected formal sector.

Both formal and informal institutions exhibit certain similarities. These similarities relate

to their mode of penalties. When the formal contract enforcement mechanism is missing, the

informal and formal institution resort to borrowing practices that uses loan screening instead of

monitoring that appears to propose more concern with contrary selection than moral hazard. The

differences only appear in method employed by these institutions (Coleman, 2016). Formal

indicates the necessity to build up appropriate institutions that will conveniently provide the

small-scale borrowers with loans (Coleman, 2016).

Microfinance institutions, on the other hand, put in place more lenient policies on the

provision of credit, which have been an added advantage to them. Microfinance institutions

attempt to overcome problems of contract enforcement and imperfect information (Martinez-

Sola et al., 2014). This is through the development of non-traditional mechanisms that are

necessary for screening applicants, monitoring borrowers’ actions and the creation of incentives

to repay. Traditionally, microfinance institutions have depended on donor funds, and subsidies as

raising funds on the commercial basis have rendered difficult. Because of these irregularities,

one wonders whether these institutions should be regulated (Demirgüç-Kunt & Singer, 2017).

2.4 Debates within the literature

Credit institutions have been characterized by their varying ways of providing credit to

borrowers. The informal institutions mainly show the inability to satisfy the existing demand

especially in the rural areas that is their main target. According to Straub (2005), the small size

of resource controlled by the informal sector has been the main reason for its inability while the

difficulty in administration of loan like risk of default, monitoring and screening and high cost of

transaction has affected formal sector.

Both formal and informal institutions exhibit certain similarities. These similarities relate

to their mode of penalties. When the formal contract enforcement mechanism is missing, the

informal and formal institution resort to borrowing practices that uses loan screening instead of

monitoring that appears to propose more concern with contrary selection than moral hazard. The

differences only appear in method employed by these institutions (Coleman, 2016). Formal

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 9

institution uses project screening while the informal institution checks on the reputation of the

borrower. They rely on history and character of the borrower. Informal institutions rarely

undertake loan monitoring since they know borrowers as opposed to formal institutions, which

are because of lack of facilities (Martinez-sola et al., 2014). Another difference that emerges in

characteristics of credit institutions is that transaction costs are lower in informal institutions as

compared to formal institutions.

Most financial institutions serve as financial intermediaries. These financial institutions

based on their primary sources of funds and how they use these funds. The institutions are

depository institutions known as banks, investment intermediaries, and contractual savings

institutions. The following explanation of the characteristics of each of these institutions has

followed from the work.

2.5 Linkages between formal and informal financial institutions

Past literature has revealed that there are some linkages in credit institutions. These

linkages mainly exist between the formal institutions and the informal institutions.

The structure of formal credit institutions does not allow them to respond efficiently to

the small farmers and individual’s needs. This may be because of information asymmetry

between the borrowers and the banks therefore hard for the bank to guarantee repayment.

Furthermore, loans require security before it approved and granted (Islam, 2016). This, therefore,

acts, as a limiting factor since small farmers and individuals may not be in a position to provide

the required security, and in any case, they do it might not be in an acceptable form as required

by formal financial institutions (Deville, 2015).

institution uses project screening while the informal institution checks on the reputation of the

borrower. They rely on history and character of the borrower. Informal institutions rarely

undertake loan monitoring since they know borrowers as opposed to formal institutions, which

are because of lack of facilities (Martinez-sola et al., 2014). Another difference that emerges in

characteristics of credit institutions is that transaction costs are lower in informal institutions as

compared to formal institutions.

Most financial institutions serve as financial intermediaries. These financial institutions

based on their primary sources of funds and how they use these funds. The institutions are

depository institutions known as banks, investment intermediaries, and contractual savings

institutions. The following explanation of the characteristics of each of these institutions has

followed from the work.

2.5 Linkages between formal and informal financial institutions

Past literature has revealed that there are some linkages in credit institutions. These

linkages mainly exist between the formal institutions and the informal institutions.

The structure of formal credit institutions does not allow them to respond efficiently to

the small farmers and individual’s needs. This may be because of information asymmetry

between the borrowers and the banks therefore hard for the bank to guarantee repayment.

Furthermore, loans require security before it approved and granted (Islam, 2016). This, therefore,

acts, as a limiting factor since small farmers and individuals may not be in a position to provide

the required security, and in any case, they do it might not be in an acceptable form as required

by formal financial institutions (Deville, 2015).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 10

Informal financial institutions are more open to short-term credit requirements as

compared to the formal sector (Lane and McQuade, 2014). This, therefore, gives low-income

individuals access to loans, which might be easily accessible in other institutions and sometimes

at a lower cost. The linkages between these financial institutions in two ways; that is horizontal

and vertical. Under horizontal view, the formal sector banks are allowed to be in direct

competition with small-scale moneylenders in the provision of credit (Gough, 2017). On the

other hand, vertical view allows formal lenders access the formal lending sources and be able to

re-lend the borrowed funds.

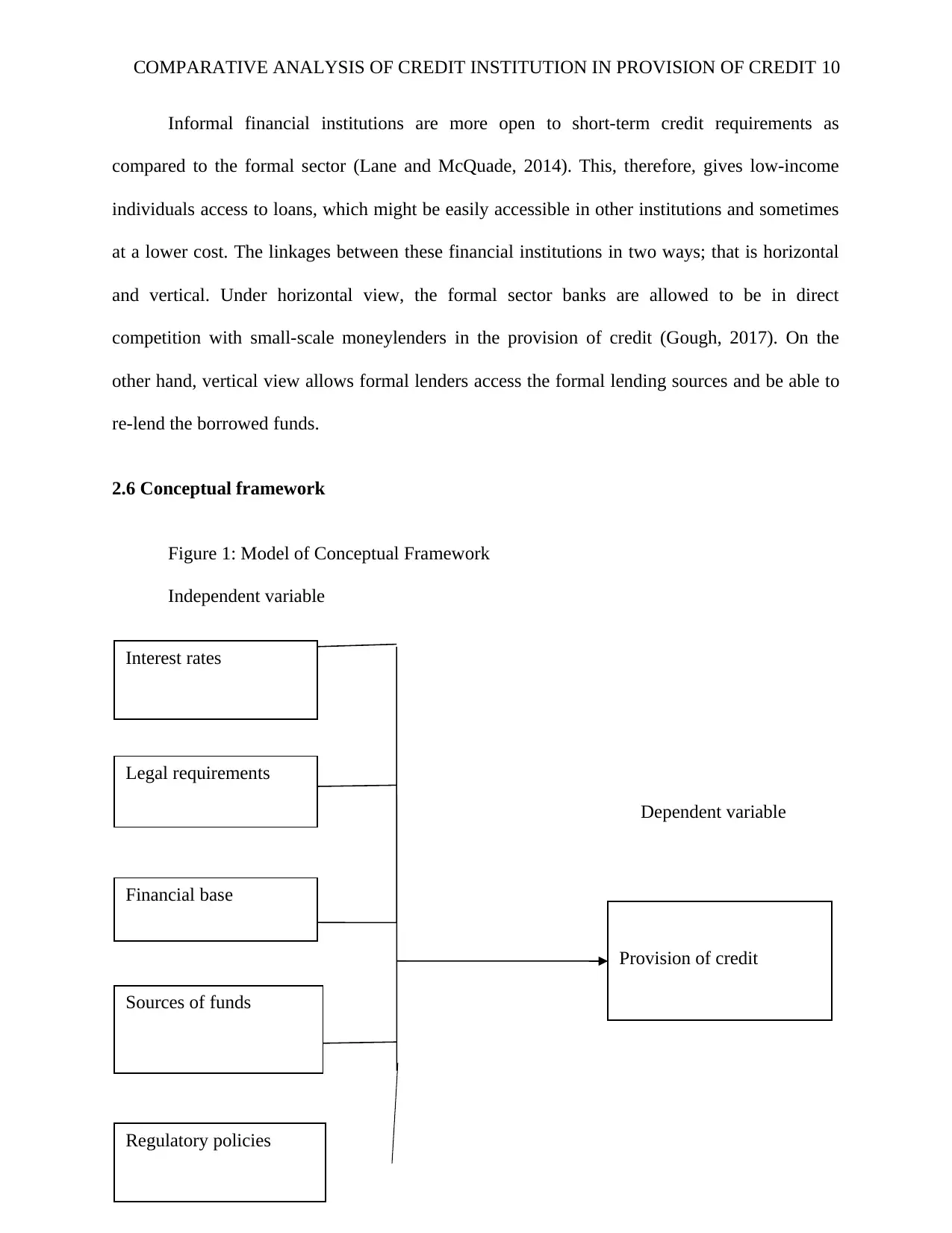

2.6 Conceptual framework

Figure 1: Model of Conceptual Framework

Independent variable

Dependent variable

Interest rates

Legal requirements

Provision of credit

Financial base

Sources of funds

Regulatory policies

Informal financial institutions are more open to short-term credit requirements as

compared to the formal sector (Lane and McQuade, 2014). This, therefore, gives low-income

individuals access to loans, which might be easily accessible in other institutions and sometimes

at a lower cost. The linkages between these financial institutions in two ways; that is horizontal

and vertical. Under horizontal view, the formal sector banks are allowed to be in direct

competition with small-scale moneylenders in the provision of credit (Gough, 2017). On the

other hand, vertical view allows formal lenders access the formal lending sources and be able to

re-lend the borrowed funds.

2.6 Conceptual framework

Figure 1: Model of Conceptual Framework

Independent variable

Dependent variable

Interest rates

Legal requirements

Provision of credit

Financial base

Sources of funds

Regulatory policies

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 11

Figure 2.1: Factors that influence provision of credit among credit institutions

Source: (Author, 2018).

2.7 Summary of literature review

The literature review about past research has mainly focused on the differences portrayed

by various credit institutions concerning their features and characteristics. This literature has also

shown that credit institutions vary in their policies, for example, formal credit institutions mainly

focus on loan screening and monitoring and place collateral as security while on the other hand

informal credit institutions base their security on personal information about the loaner. Despite

these variations, individuals still prefer certain institutions than others when securing loans and

over the recent years, SACCOs have shown greater performance in the provision of credit. This

study seeks to establish the added advantage some institutions have over others.

3.0 Critical Analysis of a Text

Full Reference of Peer Reviewed Text:

Mosley, P. and Hulme, D., 2006. Finance against Poverty: Volume 2: Country Case Studies.

Routledge.

Figure 2.1: Factors that influence provision of credit among credit institutions

Source: (Author, 2018).

2.7 Summary of literature review

The literature review about past research has mainly focused on the differences portrayed

by various credit institutions concerning their features and characteristics. This literature has also

shown that credit institutions vary in their policies, for example, formal credit institutions mainly

focus on loan screening and monitoring and place collateral as security while on the other hand

informal credit institutions base their security on personal information about the loaner. Despite

these variations, individuals still prefer certain institutions than others when securing loans and

over the recent years, SACCOs have shown greater performance in the provision of credit. This

study seeks to establish the added advantage some institutions have over others.

3.0 Critical Analysis of a Text

Full Reference of Peer Reviewed Text:

Mosley, P. and Hulme, D., 2006. Finance against Poverty: Volume 2: Country Case Studies.

Routledge.

COMPARATIVE ANALYSIS OF CREDIT INSTITUTION IN PROVISION OF CREDIT 12

1. What review question am I asking of this text?

(e.g. what is my research question? why select this text? does the Critical Analysis of this

text fit into my investigation with a wider focus? what is my constructive purpose in

undertaking a Critical Analysis of this text?)

My topic ‘comparative analysis of credit institution in provision of credit’ and the research

article has been able to answer the research questions like

1. What variations were observed in provision of credit among credit institutions?

2. How did those variations impact the performance of credit institutions and loaners at large?

3. What criteria did credit institutions use while issuing credit to its customers.

2. What type of literature is this?

(e.g. theoretical, research, practice, policy? are there links with other types of literature?)

This is a research paper because it reports on steps and factors credit institutions consider before

they issue out loans. It also tries to identify the linkage between formal and informal sectors in

allocation of credit and finally the literature review shows the dependent and independent

variables necessary for this research paper

3. What sort of intellectual project for study is being undertaken?

a) How clear is it which project the authors are undertaking? (e.g. knowledge-for-

understanding, knowledge-for-critical evaluation, knowledge-for-action, instrumentalism,

reflexive action?)

1. What review question am I asking of this text?

(e.g. what is my research question? why select this text? does the Critical Analysis of this

text fit into my investigation with a wider focus? what is my constructive purpose in

undertaking a Critical Analysis of this text?)

My topic ‘comparative analysis of credit institution in provision of credit’ and the research

article has been able to answer the research questions like

1. What variations were observed in provision of credit among credit institutions?

2. How did those variations impact the performance of credit institutions and loaners at large?

3. What criteria did credit institutions use while issuing credit to its customers.

2. What type of literature is this?

(e.g. theoretical, research, practice, policy? are there links with other types of literature?)

This is a research paper because it reports on steps and factors credit institutions consider before

they issue out loans. It also tries to identify the linkage between formal and informal sectors in

allocation of credit and finally the literature review shows the dependent and independent

variables necessary for this research paper

3. What sort of intellectual project for study is being undertaken?

a) How clear is it which project the authors are undertaking? (e.g. knowledge-for-

understanding, knowledge-for-critical evaluation, knowledge-for-action, instrumentalism,

reflexive action?)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.