ECON6001 Economic Principles: Analyzing Fiscal Policy During Crisis

VerifiedAdded on 2023/05/29

|14

|3319

|474

Case Study

AI Summary

This case study provides a comparative analysis of economic policies in Sweden and the United Kingdom, focusing on monetary policy effectiveness in controlling inflation and fiscal policy utilization during the 2008-09 financial crisis. It evaluates Sweden's inflation targeting approach, highlighting its benefits in reducing inflation volatility and fostering employment, and compares it to the Bank of England's strategies, including the role of the Monetary Policy Committee (MPC). The study also assesses the fiscal policy responses of both countries, examining Sweden's budget surplus target and the UK's nationalization efforts and interest rate adjustments. Ultimately, the analysis evaluates which country was more successful in minimizing the negative effects of the recession, considering factors such as net lending, government debt, and GDP growth.

ECON6001 Economic

Principles

1

Principles

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents........................................................................................................................................2

Introduction................................................................................................................................................3

(a) The comparative statement of two countries in context of effective monetary policy to control

inflation..................................................................................................................................................3

(b) Explanation about the factors that impeded the policy implementation in case of UK.....................5

(c) Evaluation of utilization of Fiscal policy during Financial crisis (of 2008-09) by Sweden and

United Kingdom....................................................................................................................................6

(d)Evaluation which of two countries was more successful in minimizing the potential negative

effects of recession.................................................................................................................................8

Conclusion..................................................................................................................................................8

References..................................................................................................................................................9

2

Table of Contents........................................................................................................................................2

Introduction................................................................................................................................................3

(a) The comparative statement of two countries in context of effective monetary policy to control

inflation..................................................................................................................................................3

(b) Explanation about the factors that impeded the policy implementation in case of UK.....................5

(c) Evaluation of utilization of Fiscal policy during Financial crisis (of 2008-09) by Sweden and

United Kingdom....................................................................................................................................6

(d)Evaluation which of two countries was more successful in minimizing the potential negative

effects of recession.................................................................................................................................8

Conclusion..................................................................................................................................................8

References..................................................................................................................................................9

2

Introduction

Inflation Targeting as the monetary policy tool with the involvement of central bank of

country, where the central bank set some rules and regulations regarding the inflation rate as its

objectives (Caputo, Leyva and Pedersen, 2014). It is used to create the right economic situation

to create rising prices. For this the inflation targeting uses to solve it. The central government

spurs economic growth by providing liquidity, credit and jobs opportunities in the economy.

(a) The comparative statement of two countries in context of effective monetary policy to

control inflation

In case of Sweden

Inflation targeting used as monetary policy in Sweden to control the problem of inflation.

The effect of adopting the inflation targeting the Sweden enjoys three benefits after

implementation that are first, the inflation targeting reduces the inflation and makes inflation less

volatile. Second, the inflation targeting reduces the real cost of disinflation and the third is

creation of new employment opportunities. It helps in context of stabilize both inflation around

low rate and resources utilization around the highest sustainable level. For this, the federal bank

and Riksbank are both involved in it. Both these banks played dominant role in controlling the

inflation by adopting the inflation targeting as monetary policy tool. The Federal Reserve has

dual objective of creation of employment opportunities and stable prices implemented for

stabilized inflation. Along with the stable inflation rate and stabilize employment around highest

sustainability among employment rate (Bernanke, B.S, et. al, 2018). Maximum employment

opportunity leads to highest sustainability in employment rate. The Riksbank’s main target is to

stabilize inflation by implementing inflation targeting and utilization for great sustainability

level (Davis, 2014). The Riksbank forecasts the inflation. The Riksbank stabilizes the inflation

around inflation target and stabilize the production and employment in long term sustainability

paths and Riksbank mandate the constant the issues of European system of central banks, that is

useful in price stability which is the primary objective of the Riksbank. However, no deviation

between the Riksbank hierarchical and the Federal Reserve bank’s dual objectives, the explicit

inflation target, inflation rate at that time was 2% per year and is enforced by Riksbank of

3

Inflation Targeting as the monetary policy tool with the involvement of central bank of

country, where the central bank set some rules and regulations regarding the inflation rate as its

objectives (Caputo, Leyva and Pedersen, 2014). It is used to create the right economic situation

to create rising prices. For this the inflation targeting uses to solve it. The central government

spurs economic growth by providing liquidity, credit and jobs opportunities in the economy.

(a) The comparative statement of two countries in context of effective monetary policy to

control inflation

In case of Sweden

Inflation targeting used as monetary policy in Sweden to control the problem of inflation.

The effect of adopting the inflation targeting the Sweden enjoys three benefits after

implementation that are first, the inflation targeting reduces the inflation and makes inflation less

volatile. Second, the inflation targeting reduces the real cost of disinflation and the third is

creation of new employment opportunities. It helps in context of stabilize both inflation around

low rate and resources utilization around the highest sustainable level. For this, the federal bank

and Riksbank are both involved in it. Both these banks played dominant role in controlling the

inflation by adopting the inflation targeting as monetary policy tool. The Federal Reserve has

dual objective of creation of employment opportunities and stable prices implemented for

stabilized inflation. Along with the stable inflation rate and stabilize employment around highest

sustainability among employment rate (Bernanke, B.S, et. al, 2018). Maximum employment

opportunity leads to highest sustainability in employment rate. The Riksbank’s main target is to

stabilize inflation by implementing inflation targeting and utilization for great sustainability

level (Davis, 2014). The Riksbank forecasts the inflation. The Riksbank stabilizes the inflation

around inflation target and stabilize the production and employment in long term sustainability

paths and Riksbank mandate the constant the issues of European system of central banks, that is

useful in price stability which is the primary objective of the Riksbank. However, no deviation

between the Riksbank hierarchical and the Federal Reserve bank’s dual objectives, the explicit

inflation target, inflation rate at that time was 2% per year and is enforced by Riksbank of

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

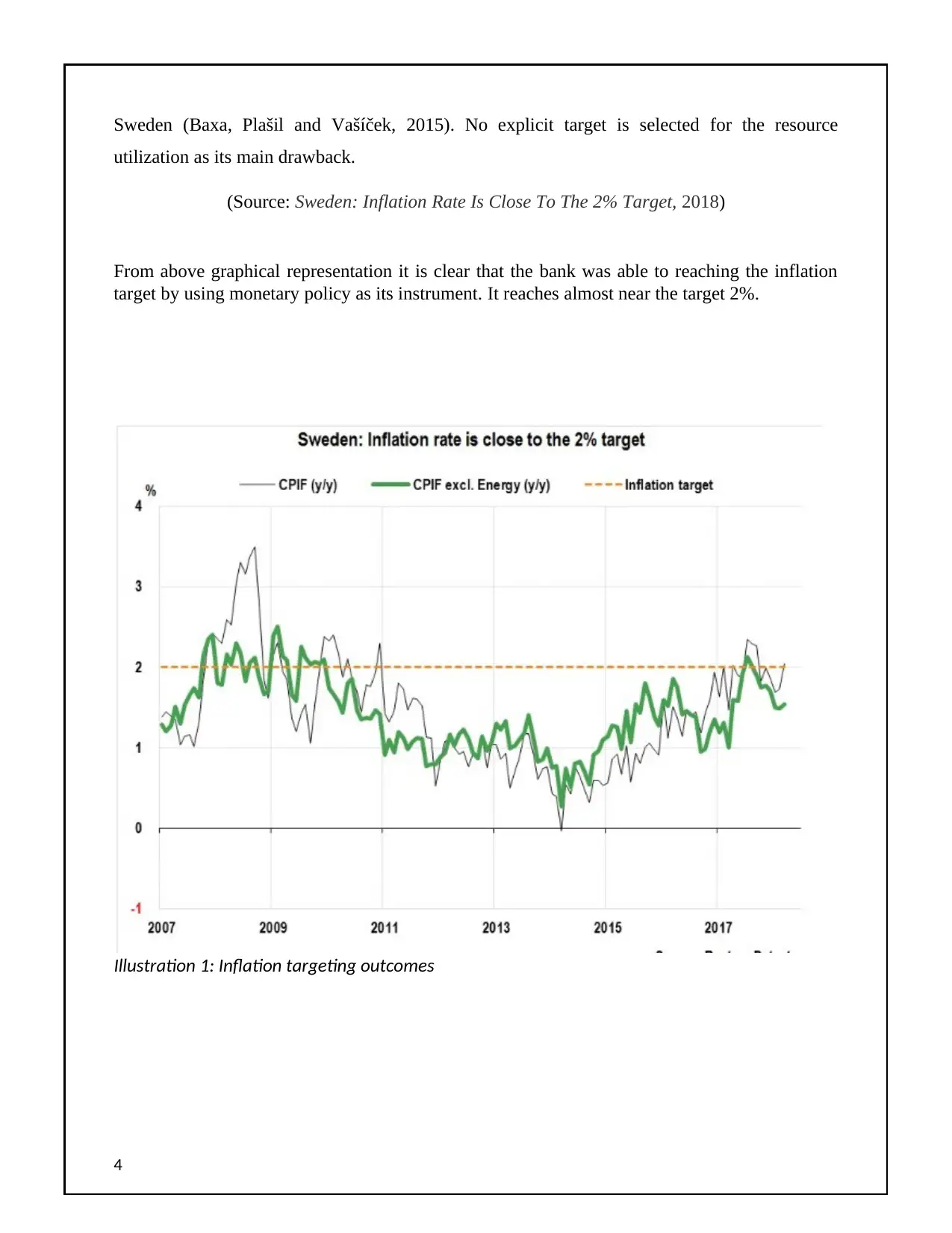

Sweden (Baxa, Plašil and Vašíček, 2015). No explicit target is selected for the resource

utilization as its main drawback.

(Source: Sweden: Inflation Rate Is Close To The 2% Target, 2018)

From above graphical representation it is clear that the bank was able to reaching the inflation

target by using monetary policy as its instrument. It reaches almost near the target 2%.

4

Illustration 1: Inflation targeting outcomes

utilization as its main drawback.

(Source: Sweden: Inflation Rate Is Close To The 2% Target, 2018)

From above graphical representation it is clear that the bank was able to reaching the inflation

target by using monetary policy as its instrument. It reaches almost near the target 2%.

4

Illustration 1: Inflation targeting outcomes

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

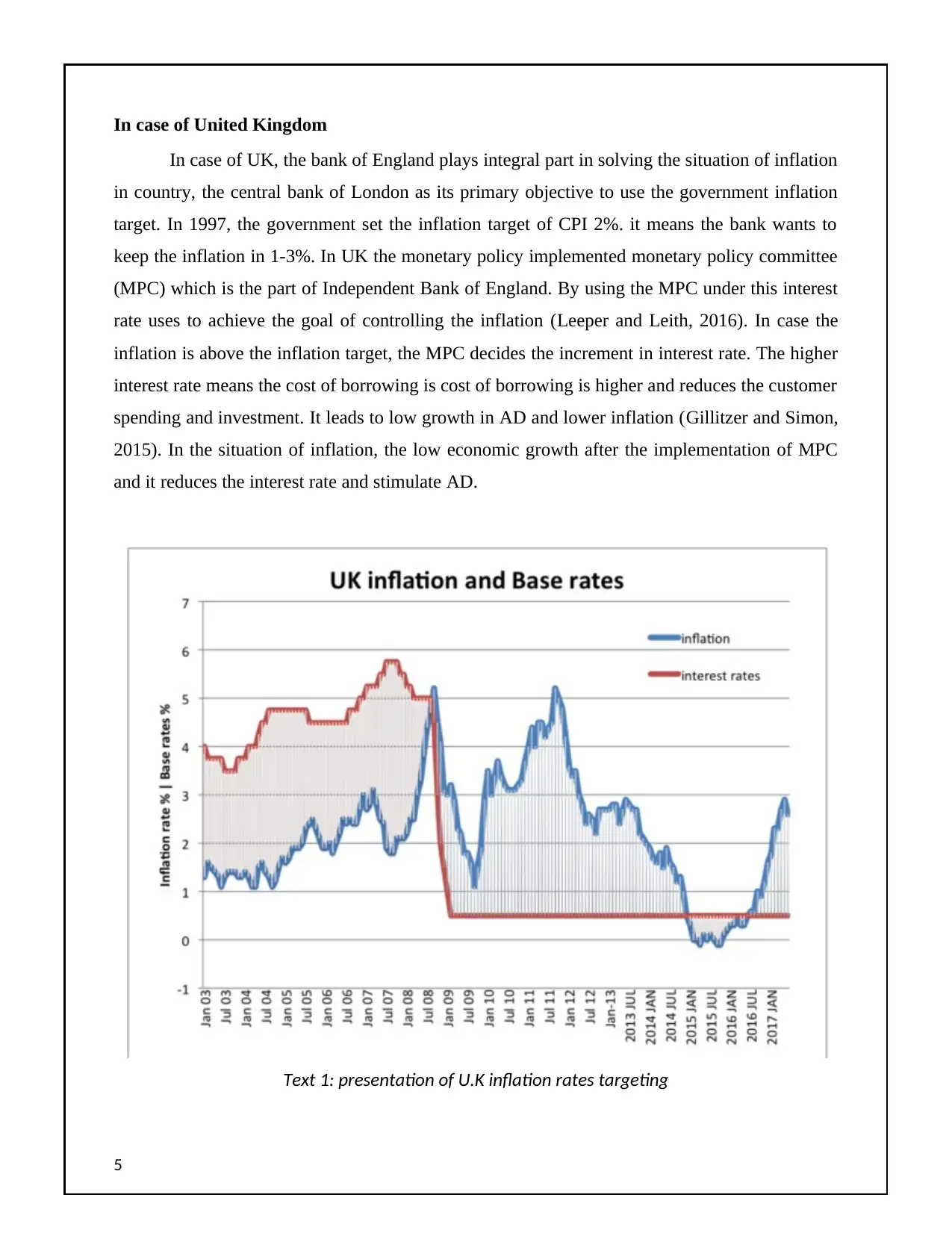

In case of United Kingdom

In case of UK, the bank of England plays integral part in solving the situation of inflation

in country, the central bank of London as its primary objective to use the government inflation

target. In 1997, the government set the inflation target of CPI 2%. it means the bank wants to

keep the inflation in 1-3%. In UK the monetary policy implemented monetary policy committee

(MPC) which is the part of Independent Bank of England. By using the MPC under this interest

rate uses to achieve the goal of controlling the inflation (Leeper and Leith, 2016). In case the

inflation is above the inflation target, the MPC decides the increment in interest rate. The higher

interest rate means the cost of borrowing is cost of borrowing is higher and reduces the customer

spending and investment. It leads to low growth in AD and lower inflation (Gillitzer and Simon,

2015). In the situation of inflation, the low economic growth after the implementation of MPC

and it reduces the interest rate and stimulate AD.

5

Text 1: presentation of U.K inflation rates targeting

In case of UK, the bank of England plays integral part in solving the situation of inflation

in country, the central bank of London as its primary objective to use the government inflation

target. In 1997, the government set the inflation target of CPI 2%. it means the bank wants to

keep the inflation in 1-3%. In UK the monetary policy implemented monetary policy committee

(MPC) which is the part of Independent Bank of England. By using the MPC under this interest

rate uses to achieve the goal of controlling the inflation (Leeper and Leith, 2016). In case the

inflation is above the inflation target, the MPC decides the increment in interest rate. The higher

interest rate means the cost of borrowing is cost of borrowing is higher and reduces the customer

spending and investment. It leads to low growth in AD and lower inflation (Gillitzer and Simon,

2015). In the situation of inflation, the low economic growth after the implementation of MPC

and it reduces the interest rate and stimulate AD.

5

Text 1: presentation of U.K inflation rates targeting

From above graphical representation it is clearly understandable that how rates increased year by

year and after using monetary policy as a tool these are decreased and reached to the target.

Moreover, the ECB has target to maintain the inflation rate below the 2%. The UK

economy suffers from the “Boom and Bust” economic cycles. Moreover, the UK experienced

the cost push inflation of 5% due to increase in prices of oil (Nguyen, 2017). In order to

maintain the inflation rate at 2% and increase the growth rate the bank of England allowed the

interest rate to increase above the target because the inflation was temporary and recession was

stable. Not only this, the ECB increases the interest rate, despite low growth rate and consists

with deflationary pressure. The ECB sets the monetary policy to maintain the inflation in

Eurozone, as by targeting the inflation leads to costs of rising unemployment. The ECB is

unconcerned about the Eurozone’s slide as in case of double dip recession instead of preventing

prolonged slump they fixated the low inflation impotencies (El-Shagi and Giesen, 2013). The

inflation, if above can impose the costs on economy such as uncertainty, but these costs are less

than social and economic costs of mass employment. Unemployment in UK reached by 25%,

but there was little monetary stimulates in Eurozone because the ECB leads inflation at 2.6%

this reduces the inflation in minor context of recession (Andersson and Jonung, 2017).

The above explanation depicts that the Sweden had achieved better results in controlling

the inflation by using the Inflation targeting as monetary policy tool.

(b) Explanation about the factors that impeded the policy implementation in case of UK

In case of UK, Inflation targeting used as monetary policy to reduces or remove the

inflation rate and its affects. MPC uses the interest rate used to solve the problem. In prior era of

implementation, the MPC predicts the future inflation and used various statistical tools to control

the inflation. If the prediction declares rise in inflation rate (more than 2%), then MPC increases

the interest rates. The increment in interest rates leads to reduction in demand of the economy

and also leads to very slower growth (fluctuations in very slow growing rate) of economy

instead of steady economy growth (growth with same growing rate) (Neuenkirch and Tillmann,

2014). Impacts of increment in interest rates are as follows.

Increased rates lead to increment in borrowing costs, discouraging consumer borrowing

and their spending.

6

year and after using monetary policy as a tool these are decreased and reached to the target.

Moreover, the ECB has target to maintain the inflation rate below the 2%. The UK

economy suffers from the “Boom and Bust” economic cycles. Moreover, the UK experienced

the cost push inflation of 5% due to increase in prices of oil (Nguyen, 2017). In order to

maintain the inflation rate at 2% and increase the growth rate the bank of England allowed the

interest rate to increase above the target because the inflation was temporary and recession was

stable. Not only this, the ECB increases the interest rate, despite low growth rate and consists

with deflationary pressure. The ECB sets the monetary policy to maintain the inflation in

Eurozone, as by targeting the inflation leads to costs of rising unemployment. The ECB is

unconcerned about the Eurozone’s slide as in case of double dip recession instead of preventing

prolonged slump they fixated the low inflation impotencies (El-Shagi and Giesen, 2013). The

inflation, if above can impose the costs on economy such as uncertainty, but these costs are less

than social and economic costs of mass employment. Unemployment in UK reached by 25%,

but there was little monetary stimulates in Eurozone because the ECB leads inflation at 2.6%

this reduces the inflation in minor context of recession (Andersson and Jonung, 2017).

The above explanation depicts that the Sweden had achieved better results in controlling

the inflation by using the Inflation targeting as monetary policy tool.

(b) Explanation about the factors that impeded the policy implementation in case of UK

In case of UK, Inflation targeting used as monetary policy to reduces or remove the

inflation rate and its affects. MPC uses the interest rate used to solve the problem. In prior era of

implementation, the MPC predicts the future inflation and used various statistical tools to control

the inflation. If the prediction declares rise in inflation rate (more than 2%), then MPC increases

the interest rates. The increment in interest rates leads to reduction in demand of the economy

and also leads to very slower growth (fluctuations in very slow growing rate) of economy

instead of steady economy growth (growth with same growing rate) (Neuenkirch and Tillmann,

2014). Impacts of increment in interest rates are as follows.

Increased rates lead to increment in borrowing costs, discouraging consumer borrowing

and their spending.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Increased rates ensure increment in savings of money.

It leads to reduction in disposable income with mortgages.

There are some reasons that impeded the implementation of the policy which are as follows.

MPC becomes ineffective in maintaining steady rate of growth: Increment in interest

rates and results in cost of borrowings and reduces spending this was beneficial in

creating lower inflation but it drastically affects the economic growth and leads to heavy

downfall.

MPC fails in reduction of unemployment rate: Increment in interest rates affects the business

expansions as due increased cost of borrowings, this all were not helpful in creation of

employment opportunities or reduction in unemployment rate of UK (Creel and Hubert, 2015).

(c) Evaluation of utilization of Fiscal policy during Financial crisis (of 2008-09) by Sweden

and United Kingdom

Fiscal policy used by Sweden

During the financial crisis of 2008-09, Swedish government targeted the budget surplus

of one percent of GDP over the business cycle, as the main fiscal target (Cloyne, J., & Hürtgen,

2016). This target is examined by three intentions which are as follows.

Ascertainment of assumable development of expenditures and taxes.

Sustainability of public finance in long run.

Equal distribution of fiscal resources across generations.

For analyzing the performance of economy against surplus target three indicators were used,

which are as follows.

Average net lending from year 2005 concerted with information regarding the estimated

output gap over the same period.

Average net lending of seven years, including three net years, three premature years and

one current year.

7

It leads to reduction in disposable income with mortgages.

There are some reasons that impeded the implementation of the policy which are as follows.

MPC becomes ineffective in maintaining steady rate of growth: Increment in interest

rates and results in cost of borrowings and reduces spending this was beneficial in

creating lower inflation but it drastically affects the economic growth and leads to heavy

downfall.

MPC fails in reduction of unemployment rate: Increment in interest rates affects the business

expansions as due increased cost of borrowings, this all were not helpful in creation of

employment opportunities or reduction in unemployment rate of UK (Creel and Hubert, 2015).

(c) Evaluation of utilization of Fiscal policy during Financial crisis (of 2008-09) by Sweden

and United Kingdom

Fiscal policy used by Sweden

During the financial crisis of 2008-09, Swedish government targeted the budget surplus

of one percent of GDP over the business cycle, as the main fiscal target (Cloyne, J., & Hürtgen,

2016). This target is examined by three intentions which are as follows.

Ascertainment of assumable development of expenditures and taxes.

Sustainability of public finance in long run.

Equal distribution of fiscal resources across generations.

For analyzing the performance of economy against surplus target three indicators were used,

which are as follows.

Average net lending from year 2005 concerted with information regarding the estimated

output gap over the same period.

Average net lending of seven years, including three net years, three premature years and

one current year.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

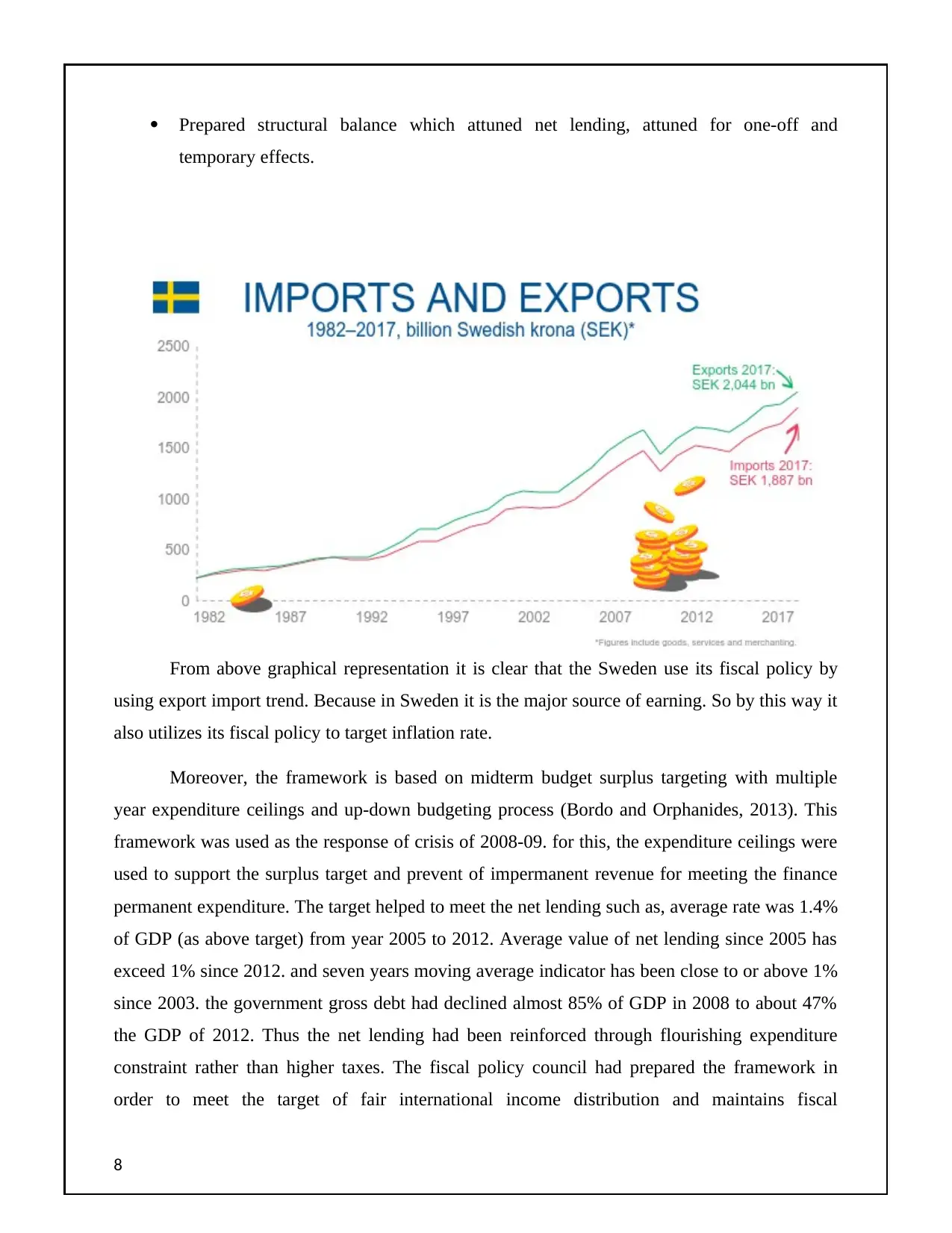

Prepared structural balance which attuned net lending, attuned for one-off and

temporary effects.

From above graphical representation it is clear that the Sweden use its fiscal policy by

using export import trend. Because in Sweden it is the major source of earning. So by this way it

also utilizes its fiscal policy to target inflation rate.

Moreover, the framework is based on midterm budget surplus targeting with multiple

year expenditure ceilings and up-down budgeting process (Bordo and Orphanides, 2013). This

framework was used as the response of crisis of 2008-09. for this, the expenditure ceilings were

used to support the surplus target and prevent of impermanent revenue for meeting the finance

permanent expenditure. The target helped to meet the net lending such as, average rate was 1.4%

of GDP (as above target) from year 2005 to 2012. Average value of net lending since 2005 has

exceed 1% since 2012. and seven years moving average indicator has been close to or above 1%

since 2003. the government gross debt had declined almost 85% of GDP in 2008 to about 47%

the GDP of 2012. Thus the net lending had been reinforced through flourishing expenditure

constraint rather than higher taxes. The fiscal policy council had prepared the framework in

order to meet the target of fair international income distribution and maintains fiscal

8

temporary effects.

From above graphical representation it is clear that the Sweden use its fiscal policy by

using export import trend. Because in Sweden it is the major source of earning. So by this way it

also utilizes its fiscal policy to target inflation rate.

Moreover, the framework is based on midterm budget surplus targeting with multiple

year expenditure ceilings and up-down budgeting process (Bordo and Orphanides, 2013). This

framework was used as the response of crisis of 2008-09. for this, the expenditure ceilings were

used to support the surplus target and prevent of impermanent revenue for meeting the finance

permanent expenditure. The target helped to meet the net lending such as, average rate was 1.4%

of GDP (as above target) from year 2005 to 2012. Average value of net lending since 2005 has

exceed 1% since 2012. and seven years moving average indicator has been close to or above 1%

since 2003. the government gross debt had declined almost 85% of GDP in 2008 to about 47%

the GDP of 2012. Thus the net lending had been reinforced through flourishing expenditure

constraint rather than higher taxes. The fiscal policy council had prepared the framework in

order to meet the target of fair international income distribution and maintains fiscal

8

sustainability for long term. Fiscal sustainability express that “current tax and spending policy

settings can rest unaltered in the future without making increment in government debt”. It

depicts that the government debt remained stable as proportion of GDP in long run (Yoshino and

Taghizadeh Hesary, 2014). As a result, this framework has restricted the automatic and

discretionary fiscal response during the crisis of 2008-09.

Fiscal policy used by United Kingdom

In UK, during the financial crisis the Bradford and Bingley building society was

effectively nationalized in late 2008 and after that partly sold to Spanish Group Santander Bank.

The UK government efficaciously forced the UK's largest mortgage lender, Halifax Bank of

Scotland(HBOS) etc. were in deep trouble and other UK banks like Barclays and HSBC, were

forced to raise capital by new issue of shares as due to Rise interest rates the cost of borrowings

increases it affects the profitability (Mahadeva and Sterne, 2012). Along with this, in UK retail

sales, furnishing and DIY sectors suffered from large falls. The businesses were suffered from

great fall in sales and profitability and due to lack of bank support for running the trade. Various

well-known brands were going out of their businesses. In fourth quarter of 2008, UK Gross

Domestic Product(GDP) fell by 1.5% and recession continued through 2009. it affects the GDP

growth in 0.3%, of UK in the beginning of crisis era. Not only this, the unemployment rate was

tending to increase by 7% and increase with last more than four years. The fiscal policy

framework was designed by the government council and give great respond to the financial

crisis by reducing the interest rates and cost of borrowing this reduces the industrial falls and

promote businesses again (Gerlach and Tillmann, 2012).

9

settings can rest unaltered in the future without making increment in government debt”. It

depicts that the government debt remained stable as proportion of GDP in long run (Yoshino and

Taghizadeh Hesary, 2014). As a result, this framework has restricted the automatic and

discretionary fiscal response during the crisis of 2008-09.

Fiscal policy used by United Kingdom

In UK, during the financial crisis the Bradford and Bingley building society was

effectively nationalized in late 2008 and after that partly sold to Spanish Group Santander Bank.

The UK government efficaciously forced the UK's largest mortgage lender, Halifax Bank of

Scotland(HBOS) etc. were in deep trouble and other UK banks like Barclays and HSBC, were

forced to raise capital by new issue of shares as due to Rise interest rates the cost of borrowings

increases it affects the profitability (Mahadeva and Sterne, 2012). Along with this, in UK retail

sales, furnishing and DIY sectors suffered from large falls. The businesses were suffered from

great fall in sales and profitability and due to lack of bank support for running the trade. Various

well-known brands were going out of their businesses. In fourth quarter of 2008, UK Gross

Domestic Product(GDP) fell by 1.5% and recession continued through 2009. it affects the GDP

growth in 0.3%, of UK in the beginning of crisis era. Not only this, the unemployment rate was

tending to increase by 7% and increase with last more than four years. The fiscal policy

framework was designed by the government council and give great respond to the financial

crisis by reducing the interest rates and cost of borrowing this reduces the industrial falls and

promote businesses again (Gerlach and Tillmann, 2012).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

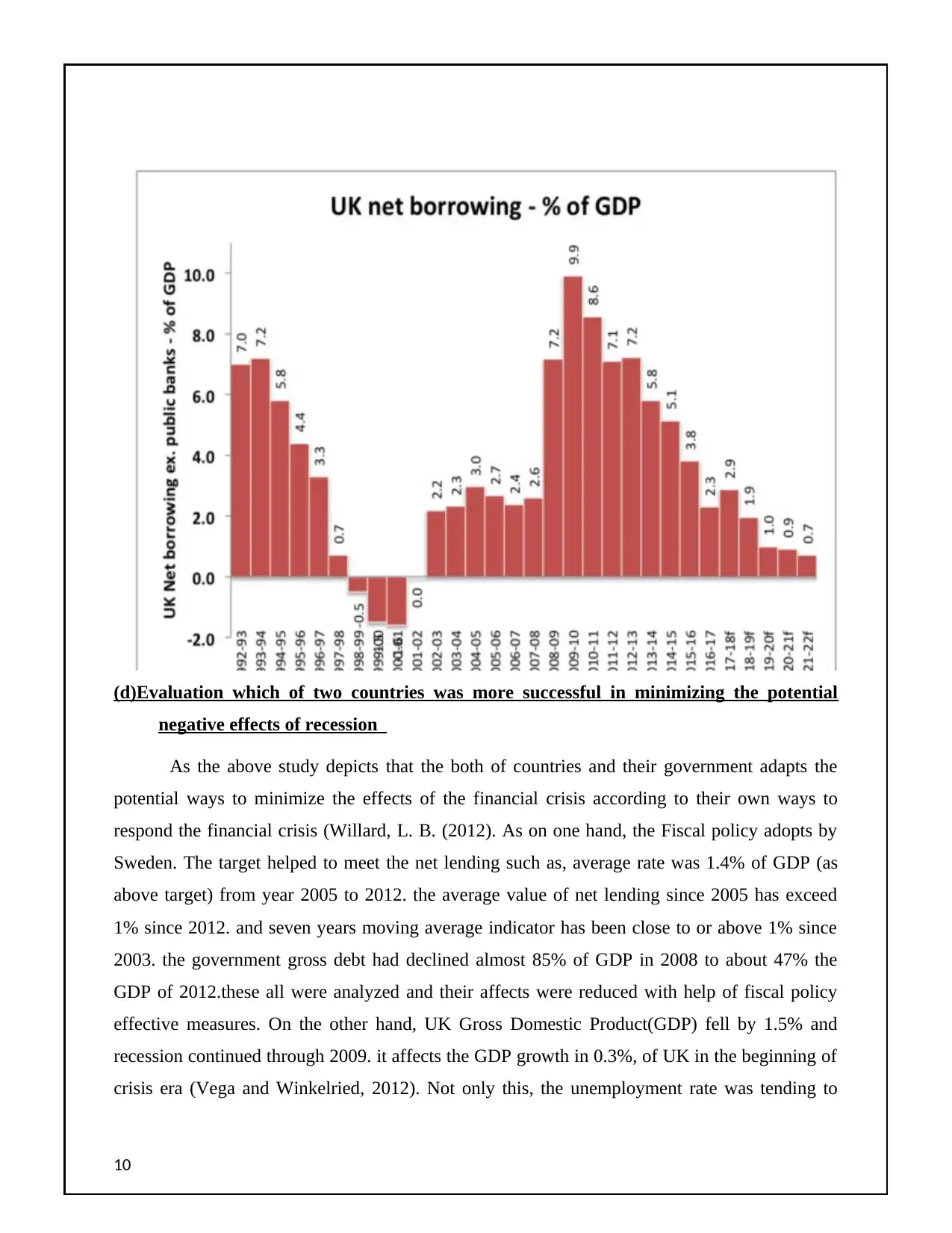

(d)Evaluation which of two countries was more successful in minimizing the potential

negative effects of recession

As the above study depicts that the both of countries and their government adapts the

potential ways to minimize the effects of the financial crisis according to their own ways to

respond the financial crisis (Willard, L. B. (2012). As on one hand, the Fiscal policy adopts by

Sweden. The target helped to meet the net lending such as, average rate was 1.4% of GDP (as

above target) from year 2005 to 2012. the average value of net lending since 2005 has exceed

1% since 2012. and seven years moving average indicator has been close to or above 1% since

2003. the government gross debt had declined almost 85% of GDP in 2008 to about 47% the

GDP of 2012.these all were analyzed and their affects were reduced with help of fiscal policy

effective measures. On the other hand, UK Gross Domestic Product(GDP) fell by 1.5% and

recession continued through 2009. it affects the GDP growth in 0.3%, of UK in the beginning of

crisis era (Vega and Winkelried, 2012). Not only this, the unemployment rate was tending to

10

negative effects of recession

As the above study depicts that the both of countries and their government adapts the

potential ways to minimize the effects of the financial crisis according to their own ways to

respond the financial crisis (Willard, L. B. (2012). As on one hand, the Fiscal policy adopts by

Sweden. The target helped to meet the net lending such as, average rate was 1.4% of GDP (as

above target) from year 2005 to 2012. the average value of net lending since 2005 has exceed

1% since 2012. and seven years moving average indicator has been close to or above 1% since

2003. the government gross debt had declined almost 85% of GDP in 2008 to about 47% the

GDP of 2012.these all were analyzed and their affects were reduced with help of fiscal policy

effective measures. On the other hand, UK Gross Domestic Product(GDP) fell by 1.5% and

recession continued through 2009. it affects the GDP growth in 0.3%, of UK in the beginning of

crisis era (Vega and Winkelried, 2012). Not only this, the unemployment rate was tending to

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increase by 7% and increase with last more than four years. The Central Bank of England

removes the MPC, which results in reduction of interest rates and exchange rates, it leads to

reduction in costs of borrowings and promoting the import and export of the country.

Conclusion

From the above study it has been concluded that the inflation is not good for the

development of the economy of country and it is inevitable to control and reduce its affects. as in

case of Sweden and United Kingdom, the inflation rises above inflation target and for solving

this problem both the countries uses inflation targeting as the monetary policy tool to control

inflation. In Sweden, the Riksbank performs major function in order to minimize the effects of

inflation and in UK the Central bank of England performs major functions for overcoming from

the inflation but, the central bank of England focuses only on adjustment of interest, while the

Riksbank focuses minimising the interest rates as well as promotes employment and Ensures

stable exchange rates with international trading partner countries. it helps the Sweden

government to response the inflation in more appropriate manner quickly.

11

removes the MPC, which results in reduction of interest rates and exchange rates, it leads to

reduction in costs of borrowings and promoting the import and export of the country.

Conclusion

From the above study it has been concluded that the inflation is not good for the

development of the economy of country and it is inevitable to control and reduce its affects. as in

case of Sweden and United Kingdom, the inflation rises above inflation target and for solving

this problem both the countries uses inflation targeting as the monetary policy tool to control

inflation. In Sweden, the Riksbank performs major function in order to minimize the effects of

inflation and in UK the Central bank of England performs major functions for overcoming from

the inflation but, the central bank of England focuses only on adjustment of interest, while the

Riksbank focuses minimising the interest rates as well as promotes employment and Ensures

stable exchange rates with international trading partner countries. it helps the Sweden

government to response the inflation in more appropriate manner quickly.

11

References

Andersson, F. N., & Jonung, L. (2017). How Tolerant Should Inflation-Targeting Central Banks

Be? Selecting the Proper Tolerance Band–Lessons from Sweden. Lund University

Department of Economics Working Papers, 2017(2).

Baxa, J., Plašil, M., & Vašíček, B. (2015). Changes in inflation dynamics under inflation

targeting? Evidence from Central European countries. Economic Modelling, 44, 116-130.

Bernanke, B. S., Laubach, T., Mishkin, F. S., & Posen, A. S. (2018). Inflation targeting: lessons

from the international experience. Princeton University Press.

Caputo, R., Leyva, G., & Pedersen, M. (2014). The Changing Nature of Real Exchange Rate

Fluctuations. New Evidence for Inflation-Targeting Countries (No. 730). Central Bank

of Chile.

Gillitzer, C., & Simon, J. (2015). Inflation Targeting: A Victim of Its Own

Success?. International Journal of Central Banking, 11(4), 259-287.

Nguyen, A. D. M. (2017). UK Monetary Policy under Inflation Targeting (No. 41). Bank of

Lithuania.

Vega, M., & Winkelried, D. (2012). Inflation targeting and inflation behaviour: a successful

story?.

Hüfner, F. (2012). Foreign exchange intervention as a monetary policy instrument: Evidence for

inflation targeting countries (Vol. 23). Springer Science & Business Media.

Willard, L. B. (2012). Does inflation targeting matter? A reassessment. Applied Economics,

44(17), 2231-2244.

Gerlach, S., & Tillmann, P. (2012). Inflation targeting and inflation persistence in Asia–Pacific.

Journal of Asian Economics, 23(4), 360-373.

Mahadeva, L., & Sterne, G. (2012). Monetary policy frameworks in a global context. Routledge.

12

Andersson, F. N., & Jonung, L. (2017). How Tolerant Should Inflation-Targeting Central Banks

Be? Selecting the Proper Tolerance Band–Lessons from Sweden. Lund University

Department of Economics Working Papers, 2017(2).

Baxa, J., Plašil, M., & Vašíček, B. (2015). Changes in inflation dynamics under inflation

targeting? Evidence from Central European countries. Economic Modelling, 44, 116-130.

Bernanke, B. S., Laubach, T., Mishkin, F. S., & Posen, A. S. (2018). Inflation targeting: lessons

from the international experience. Princeton University Press.

Caputo, R., Leyva, G., & Pedersen, M. (2014). The Changing Nature of Real Exchange Rate

Fluctuations. New Evidence for Inflation-Targeting Countries (No. 730). Central Bank

of Chile.

Gillitzer, C., & Simon, J. (2015). Inflation Targeting: A Victim of Its Own

Success?. International Journal of Central Banking, 11(4), 259-287.

Nguyen, A. D. M. (2017). UK Monetary Policy under Inflation Targeting (No. 41). Bank of

Lithuania.

Vega, M., & Winkelried, D. (2012). Inflation targeting and inflation behaviour: a successful

story?.

Hüfner, F. (2012). Foreign exchange intervention as a monetary policy instrument: Evidence for

inflation targeting countries (Vol. 23). Springer Science & Business Media.

Willard, L. B. (2012). Does inflation targeting matter? A reassessment. Applied Economics,

44(17), 2231-2244.

Gerlach, S., & Tillmann, P. (2012). Inflation targeting and inflation persistence in Asia–Pacific.

Journal of Asian Economics, 23(4), 360-373.

Mahadeva, L., & Sterne, G. (2012). Monetary policy frameworks in a global context. Routledge.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.