Financial Reporting Analysis: Sakae Holdings and Soup Restaurant

VerifiedAdded on 2020/05/28

|14

|4227

|58

Report

AI Summary

This report presents a comparative financial analysis of Sakae Holdings and Soup Restaurant, both listed on the Singapore Stock Exchange. The analysis encompasses a two-year review of profitability, liquidity, asset efficiency, and gearing ratios. The report delves into key financial metrics such as gross margin, net margin, return on capital employed, return on equity, current ratio, quick ratio, asset turnover, and earnings per share. The discussion highlights the trends and implications of these ratios for each company, providing insights into their financial health and operational efficiency. The report includes a reflection on the learning journey undertaken during the analysis, offering a comprehensive overview of the financial performance and comparative strengths and weaknesses of the two companies.

Running head: FINANCIAL REPORTING

Financial Reporting of Singapore Telecommunications Limited (Sakae Holdings) and Soup

Restaurant

Name of the University:

Name of the Student:

Authors Note:

Financial Reporting of Singapore Telecommunications Limited (Sakae Holdings) and Soup

Restaurant

Name of the University:

Name of the Student:

Authors Note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1FINANCIAL REPORTING

Table of Contents

Part 1....................................................................................................................................2

Introduction......................................................................................................................2

Background of Companies..................................................................................................2

Discussion........................................................................................................................2

Profitability Ratios.......................................................................................................2

Liquidity Ratios...........................................................................................................4

Asset Efficiency Ratios................................................................................................5

Gearing Ratios.............................................................................................................7

Conclusion.......................................................................................................................9

Part 2..................................................................................................................................10

Reflection.......................................................................................................................10

References..........................................................................................................................11

Table of Contents

Part 1....................................................................................................................................2

Introduction......................................................................................................................2

Background of Companies..................................................................................................2

Discussion........................................................................................................................2

Profitability Ratios.......................................................................................................2

Liquidity Ratios...........................................................................................................4

Asset Efficiency Ratios................................................................................................5

Gearing Ratios.............................................................................................................7

Conclusion.......................................................................................................................9

Part 2..................................................................................................................................10

Reflection.......................................................................................................................10

References..........................................................................................................................11

2FINANCIAL REPORTING

Part 1

Introduction

The objective of the paper is to conduct a comparative analysis of the selected companies

Sakae Holdings and Soup Restaurant that is listed in Singapore stock exchange. Moreover, a

comparative summary for two years regarding the selected companies’ profitability, liquidity,

asset efficiency and gearing will be provided within the report. Additionally, a reflective

statement associated with the learning journey of the report will also be provided.

Background of Companies

Soup Restaurant is positioned as among the best niche restaurant in Chinatown that offers

herbal soups and home cooked food at affordable costs (Almamy, Aston & Ngwa, 2016). Sakae

Holdings is a renowned restaurant that offers quality dining Sushi, crepes and cream and catering

services. Both these companies are listed in Singapore Exchange Limited.

Discussion

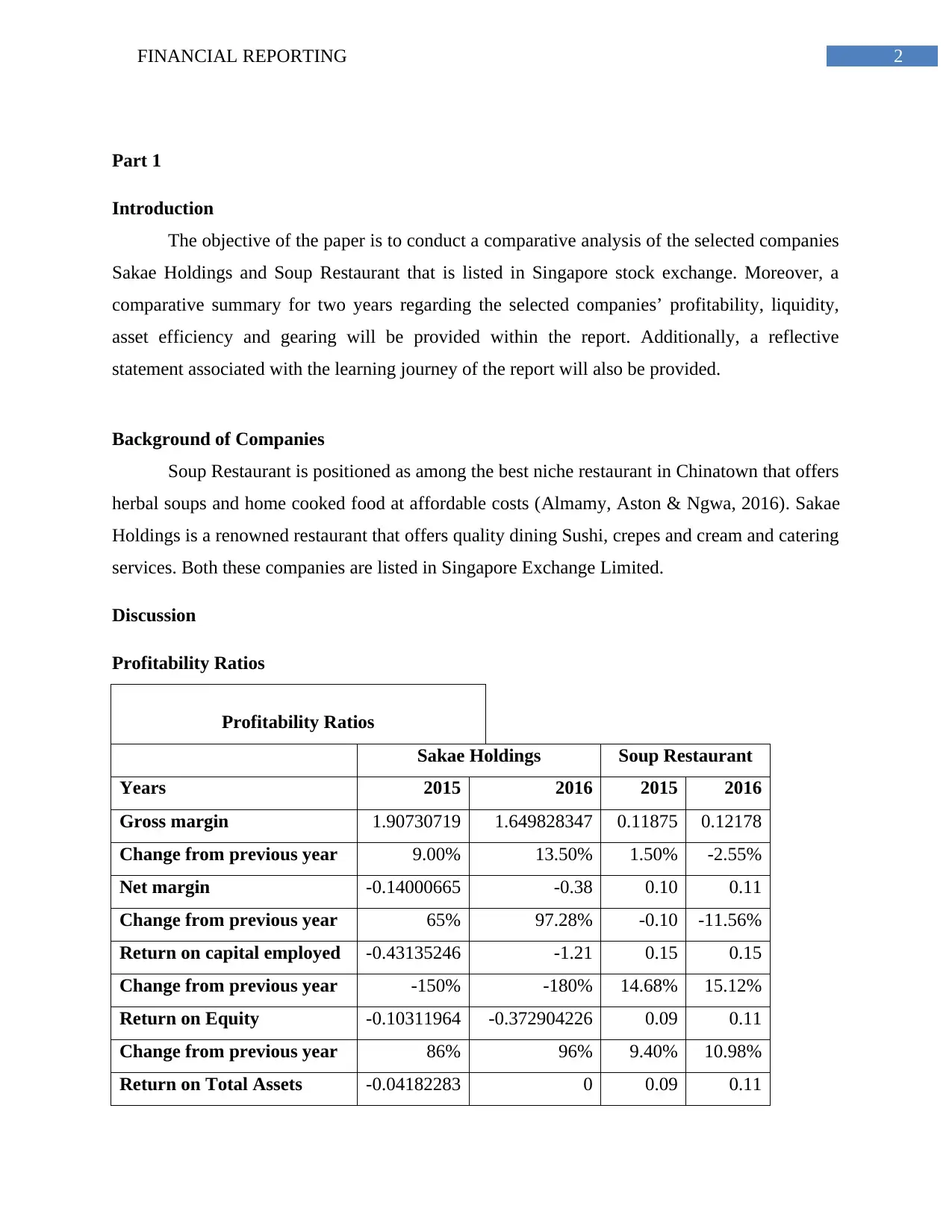

Profitability Ratios

Profitability Ratios

Sakae Holdings Soup Restaurant

Years 2015 2016 2015 2016

Gross margin 1.90730719 1.649828347 0.11875 0.12178

Change from previous year 9.00% 13.50% 1.50% -2.55%

Net margin -0.14000665 -0.38 0.10 0.11

Change from previous year 65% 97.28% -0.10 -11.56%

Return on capital employed -0.43135246 -1.21 0.15 0.15

Change from previous year -150% -180% 14.68% 15.12%

Return on Equity -0.10311964 -0.372904226 0.09 0.11

Change from previous year 86% 96% 9.40% 10.98%

Return on Total Assets -0.04182283 0 0.09 0.11

Part 1

Introduction

The objective of the paper is to conduct a comparative analysis of the selected companies

Sakae Holdings and Soup Restaurant that is listed in Singapore stock exchange. Moreover, a

comparative summary for two years regarding the selected companies’ profitability, liquidity,

asset efficiency and gearing will be provided within the report. Additionally, a reflective

statement associated with the learning journey of the report will also be provided.

Background of Companies

Soup Restaurant is positioned as among the best niche restaurant in Chinatown that offers

herbal soups and home cooked food at affordable costs (Almamy, Aston & Ngwa, 2016). Sakae

Holdings is a renowned restaurant that offers quality dining Sushi, crepes and cream and catering

services. Both these companies are listed in Singapore Exchange Limited.

Discussion

Profitability Ratios

Profitability Ratios

Sakae Holdings Soup Restaurant

Years 2015 2016 2015 2016

Gross margin 1.90730719 1.649828347 0.11875 0.12178

Change from previous year 9.00% 13.50% 1.50% -2.55%

Net margin -0.14000665 -0.38 0.10 0.11

Change from previous year 65% 97.28% -0.10 -11.56%

Return on capital employed -0.43135246 -1.21 0.15 0.15

Change from previous year -150% -180% 14.68% 15.12%

Return on Equity -0.10311964 -0.372904226 0.09 0.11

Change from previous year 86% 96% 9.40% 10.98%

Return on Total Assets -0.04182283 0 0.09 0.11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3FINANCIAL REPORTING

Change from previous year 97% 108% 9% 11%

Gross Margin

Gross margin ratio is important in measuring how much efficient will be the companies

in their business operations. Gross margin ratio of Sakae Holdings is observed to decrease by

13.50% in the year 2016 in comparison to Soup Restaurant Company that is observed to increase

from the year 2015 to year 2016 by 2.55% (Altman et al.2017). Such increasing trend of this

ratio indicates that the company retains increased amount on every dollar of its sales in order to

service its debt obligations along with other costs. Sakae Holding’s decreasing percentage

indicates a decrease in competitiveness of the company’s services and products (Sakae Holdings,

2018). It also signifies overall profitability of the company is getting poor each year with

decreased sales of its products.

Net Margin

Net margin ratio is important in indicating profitability of a company. Net margin ratio of

Sakae Holdings Company is observed to decrease by 97% from the year 2015 to year 2016 (Kou,

Peng & Wang, 2014). Such decrease is observed because of the reason that financial health of

the company is poor than Soup Restaurant Company and this signifies the company is proficient

enough in transforming its revenue into profits which is further available for all its shareholders.

It can also be gathered from the results of the company that it has less parentage of revenue left

after all expenses are decreased from the sales and it is extracting less amount of profit after its

total sales. Net margin ratio of Soup Restaurant Company is observed to increase by 11.56%

from the year 2015 to year 2016. This indicates that the company is efficient enough in

converting its revenue into profits. This also signifies the business performance of the company

is not that effective in facilitating it to attain enough net margins.

Return on Capital Employed

Return on capital employed is important in analysing the ways in which a company

employs its assets in attaining high revenues. Return on capital employed ratio of Sakae

Holdings is observed to decrease by 15% from the year 2015 to year 2016. However, and Soup

Change from previous year 97% 108% 9% 11%

Gross Margin

Gross margin ratio is important in measuring how much efficient will be the companies

in their business operations. Gross margin ratio of Sakae Holdings is observed to decrease by

13.50% in the year 2016 in comparison to Soup Restaurant Company that is observed to increase

from the year 2015 to year 2016 by 2.55% (Altman et al.2017). Such increasing trend of this

ratio indicates that the company retains increased amount on every dollar of its sales in order to

service its debt obligations along with other costs. Sakae Holding’s decreasing percentage

indicates a decrease in competitiveness of the company’s services and products (Sakae Holdings,

2018). It also signifies overall profitability of the company is getting poor each year with

decreased sales of its products.

Net Margin

Net margin ratio is important in indicating profitability of a company. Net margin ratio of

Sakae Holdings Company is observed to decrease by 97% from the year 2015 to year 2016 (Kou,

Peng & Wang, 2014). Such decrease is observed because of the reason that financial health of

the company is poor than Soup Restaurant Company and this signifies the company is proficient

enough in transforming its revenue into profits which is further available for all its shareholders.

It can also be gathered from the results of the company that it has less parentage of revenue left

after all expenses are decreased from the sales and it is extracting less amount of profit after its

total sales. Net margin ratio of Soup Restaurant Company is observed to increase by 11.56%

from the year 2015 to year 2016. This indicates that the company is efficient enough in

converting its revenue into profits. This also signifies the business performance of the company

is not that effective in facilitating it to attain enough net margins.

Return on Capital Employed

Return on capital employed is important in analysing the ways in which a company

employs its assets in attaining high revenues. Return on capital employed ratio of Sakae

Holdings is observed to decrease by 15% from the year 2015 to year 2016. However, and Soup

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4FINANCIAL REPORTING

Restaurant Company has constant ROCE in both 2015 and 2016. Such results indicate that

company’s performance within the capital intensive sectors like the restaurants. This does not

offer a good indication regarding these companies financial performance of the significant debt

(Sakae Holdings, 2018). Moreover, such decreasing and fixed trend of return of capital employed

makes it clear that these companies might occasionally have an inordinate cash amount in hand

but as the cash is not actively used within the business. There are some limitations in using this

ratio as it considers that the companies require increasing this ratio for the reason that the

investors are likely to favour the organizations with stable and increasing return on capital

employed ratio.

Return on Equity

Return in equity facilitates in analysing the company’s capability in attaining profit for

every dollar invested by shareholders. Return on equity of Sakae is observed to decrease over the

years from 2015 to 2016, while the situation is just the opposite for Soup. This is because of the

reason that Sakae Holdings is not that capable in attaining increased profit for every dollar of

common shareholders’ equity (Sakae Holdings, 2018).

Return on Total Assets

Return on total assets of both the companies is observed to decrease for Sakae and

increase for Soup Restaurant over the years from 2015 to 2016. This is because of the reason that

Sakae Company is highly capable to attain increased profit percentage in comparison to its

overall resources that is not same in case of Soup Restaurant because of which it is attaining less

profit (Sakae Holdings, 2018).

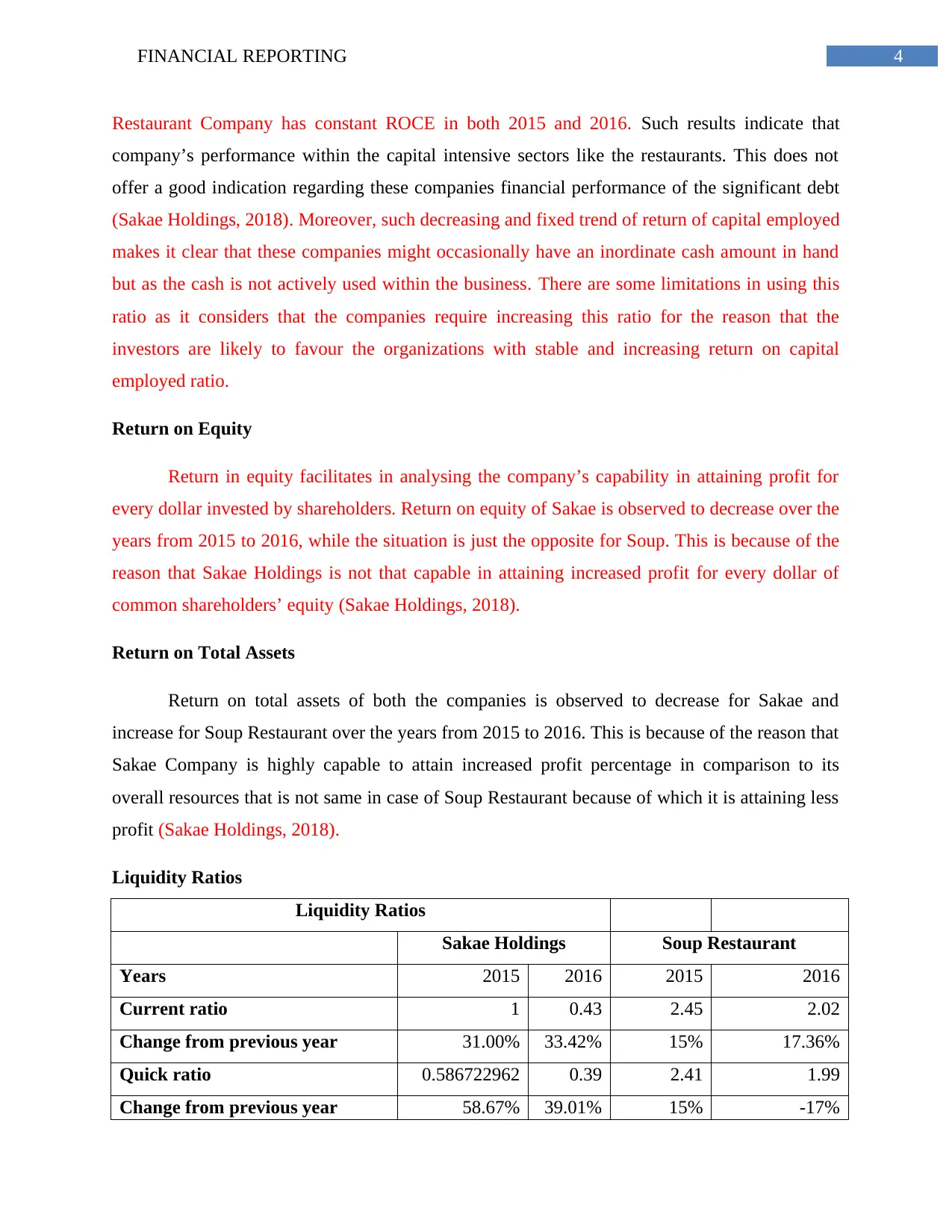

Liquidity Ratios

Liquidity Ratios

Sakae Holdings Soup Restaurant

Years 2015 2016 2015 2016

Current ratio 1 0.43 2.45 2.02

Change from previous year 31.00% 33.42% 15% 17.36%

Quick ratio 0.586722962 0.39 2.41 1.99

Change from previous year 58.67% 39.01% 15% -17%

Restaurant Company has constant ROCE in both 2015 and 2016. Such results indicate that

company’s performance within the capital intensive sectors like the restaurants. This does not

offer a good indication regarding these companies financial performance of the significant debt

(Sakae Holdings, 2018). Moreover, such decreasing and fixed trend of return of capital employed

makes it clear that these companies might occasionally have an inordinate cash amount in hand

but as the cash is not actively used within the business. There are some limitations in using this

ratio as it considers that the companies require increasing this ratio for the reason that the

investors are likely to favour the organizations with stable and increasing return on capital

employed ratio.

Return on Equity

Return in equity facilitates in analysing the company’s capability in attaining profit for

every dollar invested by shareholders. Return on equity of Sakae is observed to decrease over the

years from 2015 to 2016, while the situation is just the opposite for Soup. This is because of the

reason that Sakae Holdings is not that capable in attaining increased profit for every dollar of

common shareholders’ equity (Sakae Holdings, 2018).

Return on Total Assets

Return on total assets of both the companies is observed to decrease for Sakae and

increase for Soup Restaurant over the years from 2015 to 2016. This is because of the reason that

Sakae Company is highly capable to attain increased profit percentage in comparison to its

overall resources that is not same in case of Soup Restaurant because of which it is attaining less

profit (Sakae Holdings, 2018).

Liquidity Ratios

Liquidity Ratios

Sakae Holdings Soup Restaurant

Years 2015 2016 2015 2016

Current ratio 1 0.43 2.45 2.02

Change from previous year 31.00% 33.42% 15% 17.36%

Quick ratio 0.586722962 0.39 2.41 1.99

Change from previous year 58.67% 39.01% 15% -17%

5FINANCIAL REPORTING

Current Ratio

Current ratio is important in analysing the company’s current total assets in consideration

to its current total liabilities. Current ratio of Sakae Holdings is observed it decrease by 33.42%

from the year 2015 in the year 2016. Moreover, current ratio for Soup Restaurant is observed to

decrease by 17.36% from the year 2015 in the year 2016 (Bansal, 2014). Decreasing trend of this

ratio for Sakae Holdings Company indicates that the company is losing its capability to address

both its short and long term obligations. It can also be observed in case of the company that its

liabilities are increasing in comparison to its assets that make it incapable to address all its debt

obligations. It also signifies that Soup Restaurant Company has better liquidity position than

Sakae Holdings Company as the results indicate this organization is capable enough in settling

its current liabilities with its current assets. There is a limitation in using this ratio as it considers

analysing inventory that can lead to overestimation of liquidity position of the companies.

Quick Ratio

Quick ratio is important in evaluating the liability of companies that measures the ways in

which they address their short term financial liabilities. Quick ratio of Sakae Holdings is

observed it decrease by 39.01% from the year 2015 in the year 2016 (Buehlmaier & Whited,

2016). Such decreasing trend indicates that the company is not that efficient in maintaining its

liquidity and address all its shot tem obligations with its most liquid assets. On the other hand,

quick ratio for Soup Restaurant is observed to decrease by 17% from the year 2015 in the year

2016.This signifies that the company has increased accounts receivables that make it difficult for

the organization in collecting its receivables (Collier, 2015). There is a limitation of this ratio as

a decreasing quick ratio not always indicates that it has increased risk of bankrupts; it can signify

the company is focussing greatly on inventory or over assets for paying off its short term

liabilities.

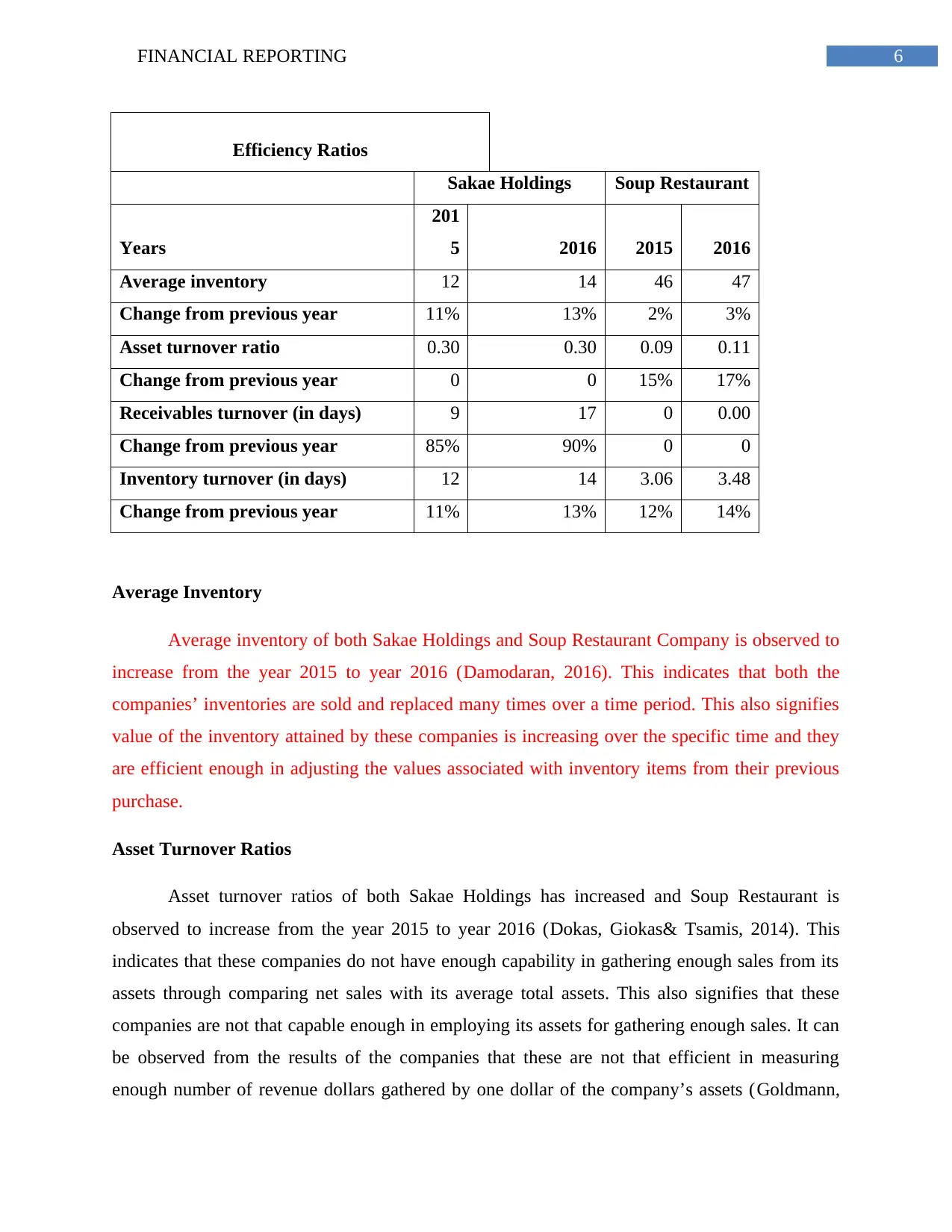

Asset Efficiency Ratios

Current Ratio

Current ratio is important in analysing the company’s current total assets in consideration

to its current total liabilities. Current ratio of Sakae Holdings is observed it decrease by 33.42%

from the year 2015 in the year 2016. Moreover, current ratio for Soup Restaurant is observed to

decrease by 17.36% from the year 2015 in the year 2016 (Bansal, 2014). Decreasing trend of this

ratio for Sakae Holdings Company indicates that the company is losing its capability to address

both its short and long term obligations. It can also be observed in case of the company that its

liabilities are increasing in comparison to its assets that make it incapable to address all its debt

obligations. It also signifies that Soup Restaurant Company has better liquidity position than

Sakae Holdings Company as the results indicate this organization is capable enough in settling

its current liabilities with its current assets. There is a limitation in using this ratio as it considers

analysing inventory that can lead to overestimation of liquidity position of the companies.

Quick Ratio

Quick ratio is important in evaluating the liability of companies that measures the ways in

which they address their short term financial liabilities. Quick ratio of Sakae Holdings is

observed it decrease by 39.01% from the year 2015 in the year 2016 (Buehlmaier & Whited,

2016). Such decreasing trend indicates that the company is not that efficient in maintaining its

liquidity and address all its shot tem obligations with its most liquid assets. On the other hand,

quick ratio for Soup Restaurant is observed to decrease by 17% from the year 2015 in the year

2016.This signifies that the company has increased accounts receivables that make it difficult for

the organization in collecting its receivables (Collier, 2015). There is a limitation of this ratio as

a decreasing quick ratio not always indicates that it has increased risk of bankrupts; it can signify

the company is focussing greatly on inventory or over assets for paying off its short term

liabilities.

Asset Efficiency Ratios

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6FINANCIAL REPORTING

Efficiency Ratios

Sakae Holdings Soup Restaurant

Years

201

5 2016 2015 2016

Average inventory 12 14 46 47

Change from previous year 11% 13% 2% 3%

Asset turnover ratio 0.30 0.30 0.09 0.11

Change from previous year 0 0 15% 17%

Receivables turnover (in days) 9 17 0 0.00

Change from previous year 85% 90% 0 0

Inventory turnover (in days) 12 14 3.06 3.48

Change from previous year 11% 13% 12% 14%

Average Inventory

Average inventory of both Sakae Holdings and Soup Restaurant Company is observed to

increase from the year 2015 to year 2016 (Damodaran, 2016). This indicates that both the

companies’ inventories are sold and replaced many times over a time period. This also signifies

value of the inventory attained by these companies is increasing over the specific time and they

are efficient enough in adjusting the values associated with inventory items from their previous

purchase.

Asset Turnover Ratios

Asset turnover ratios of both Sakae Holdings has increased and Soup Restaurant is

observed to increase from the year 2015 to year 2016 (Dokas, Giokas& Tsamis, 2014). This

indicates that these companies do not have enough capability in gathering enough sales from its

assets through comparing net sales with its average total assets. This also signifies that these

companies are not that capable enough in employing its assets for gathering enough sales. It can

be observed from the results of the companies that these are not that efficient in measuring

enough number of revenue dollars gathered by one dollar of the company’s assets (Goldmann,

Efficiency Ratios

Sakae Holdings Soup Restaurant

Years

201

5 2016 2015 2016

Average inventory 12 14 46 47

Change from previous year 11% 13% 2% 3%

Asset turnover ratio 0.30 0.30 0.09 0.11

Change from previous year 0 0 15% 17%

Receivables turnover (in days) 9 17 0 0.00

Change from previous year 85% 90% 0 0

Inventory turnover (in days) 12 14 3.06 3.48

Change from previous year 11% 13% 12% 14%

Average Inventory

Average inventory of both Sakae Holdings and Soup Restaurant Company is observed to

increase from the year 2015 to year 2016 (Damodaran, 2016). This indicates that both the

companies’ inventories are sold and replaced many times over a time period. This also signifies

value of the inventory attained by these companies is increasing over the specific time and they

are efficient enough in adjusting the values associated with inventory items from their previous

purchase.

Asset Turnover Ratios

Asset turnover ratios of both Sakae Holdings has increased and Soup Restaurant is

observed to increase from the year 2015 to year 2016 (Dokas, Giokas& Tsamis, 2014). This

indicates that these companies do not have enough capability in gathering enough sales from its

assets through comparing net sales with its average total assets. This also signifies that these

companies are not that capable enough in employing its assets for gathering enough sales. It can

be observed from the results of the companies that these are not that efficient in measuring

enough number of revenue dollars gathered by one dollar of the company’s assets (Goldmann,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7FINANCIAL REPORTING

2017). The value of these companies’ sales and revenues gathered in comparison to its assets

value is deemed to be lesser as signified by lower asset turnover ratio of these companies.

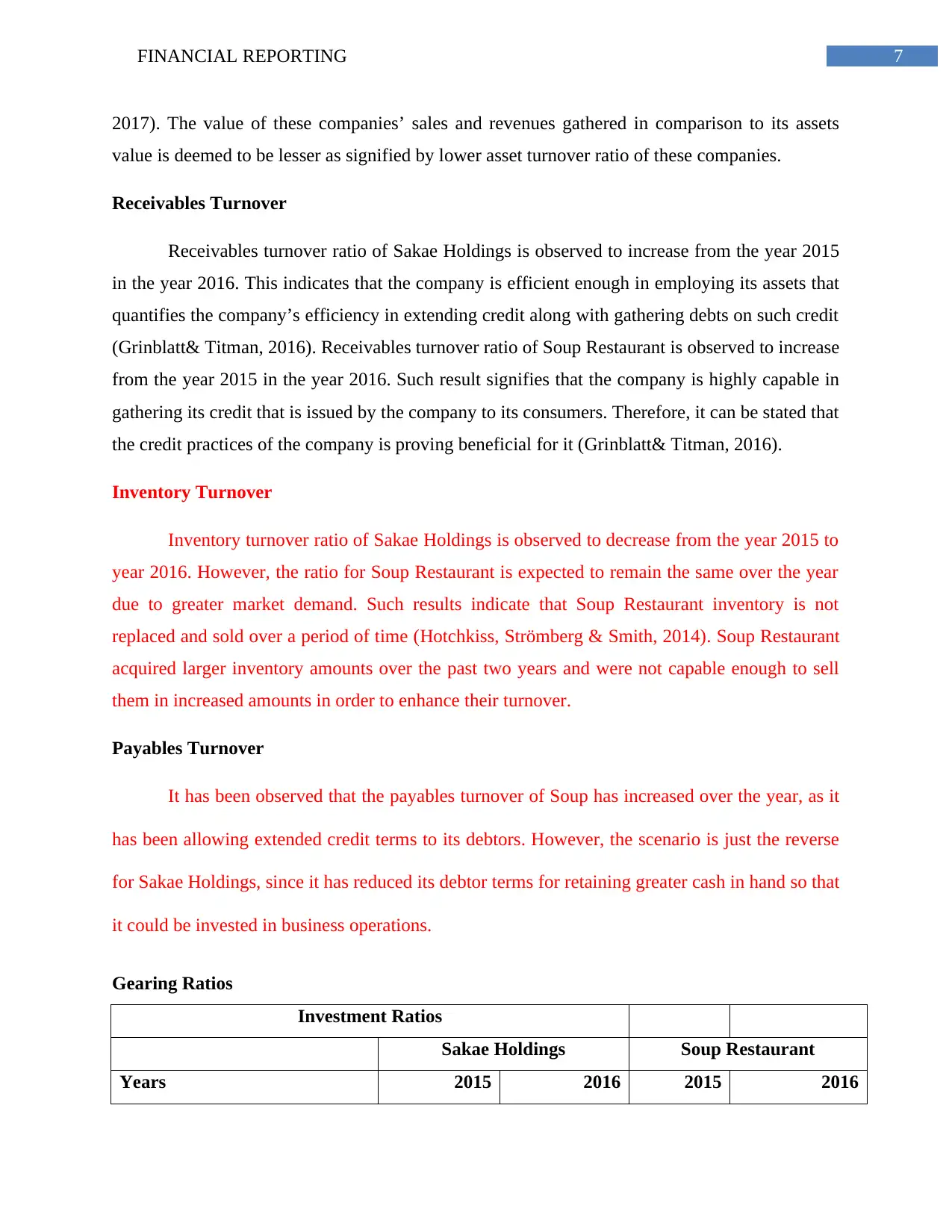

Receivables Turnover

Receivables turnover ratio of Sakae Holdings is observed to increase from the year 2015

in the year 2016. This indicates that the company is efficient enough in employing its assets that

quantifies the company’s efficiency in extending credit along with gathering debts on such credit

(Grinblatt& Titman, 2016). Receivables turnover ratio of Soup Restaurant is observed to increase

from the year 2015 in the year 2016. Such result signifies that the company is highly capable in

gathering its credit that is issued by the company to its consumers. Therefore, it can be stated that

the credit practices of the company is proving beneficial for it (Grinblatt& Titman, 2016).

Inventory Turnover

Inventory turnover ratio of Sakae Holdings is observed to decrease from the year 2015 to

year 2016. However, the ratio for Soup Restaurant is expected to remain the same over the year

due to greater market demand. Such results indicate that Soup Restaurant inventory is not

replaced and sold over a period of time (Hotchkiss, Strömberg & Smith, 2014). Soup Restaurant

acquired larger inventory amounts over the past two years and were not capable enough to sell

them in increased amounts in order to enhance their turnover.

Payables Turnover

It has been observed that the payables turnover of Soup has increased over the year, as it

has been allowing extended credit terms to its debtors. However, the scenario is just the reverse

for Sakae Holdings, since it has reduced its debtor terms for retaining greater cash in hand so that

it could be invested in business operations.

Gearing Ratios

Investment Ratios

Sakae Holdings Soup Restaurant

Years 2015 2016 2015 2016

2017). The value of these companies’ sales and revenues gathered in comparison to its assets

value is deemed to be lesser as signified by lower asset turnover ratio of these companies.

Receivables Turnover

Receivables turnover ratio of Sakae Holdings is observed to increase from the year 2015

in the year 2016. This indicates that the company is efficient enough in employing its assets that

quantifies the company’s efficiency in extending credit along with gathering debts on such credit

(Grinblatt& Titman, 2016). Receivables turnover ratio of Soup Restaurant is observed to increase

from the year 2015 in the year 2016. Such result signifies that the company is highly capable in

gathering its credit that is issued by the company to its consumers. Therefore, it can be stated that

the credit practices of the company is proving beneficial for it (Grinblatt& Titman, 2016).

Inventory Turnover

Inventory turnover ratio of Sakae Holdings is observed to decrease from the year 2015 to

year 2016. However, the ratio for Soup Restaurant is expected to remain the same over the year

due to greater market demand. Such results indicate that Soup Restaurant inventory is not

replaced and sold over a period of time (Hotchkiss, Strömberg & Smith, 2014). Soup Restaurant

acquired larger inventory amounts over the past two years and were not capable enough to sell

them in increased amounts in order to enhance their turnover.

Payables Turnover

It has been observed that the payables turnover of Soup has increased over the year, as it

has been allowing extended credit terms to its debtors. However, the scenario is just the reverse

for Sakae Holdings, since it has reduced its debtor terms for retaining greater cash in hand so that

it could be invested in business operations.

Gearing Ratios

Investment Ratios

Sakae Holdings Soup Restaurant

Years 2015 2016 2015 2016

8FINANCIAL REPORTING

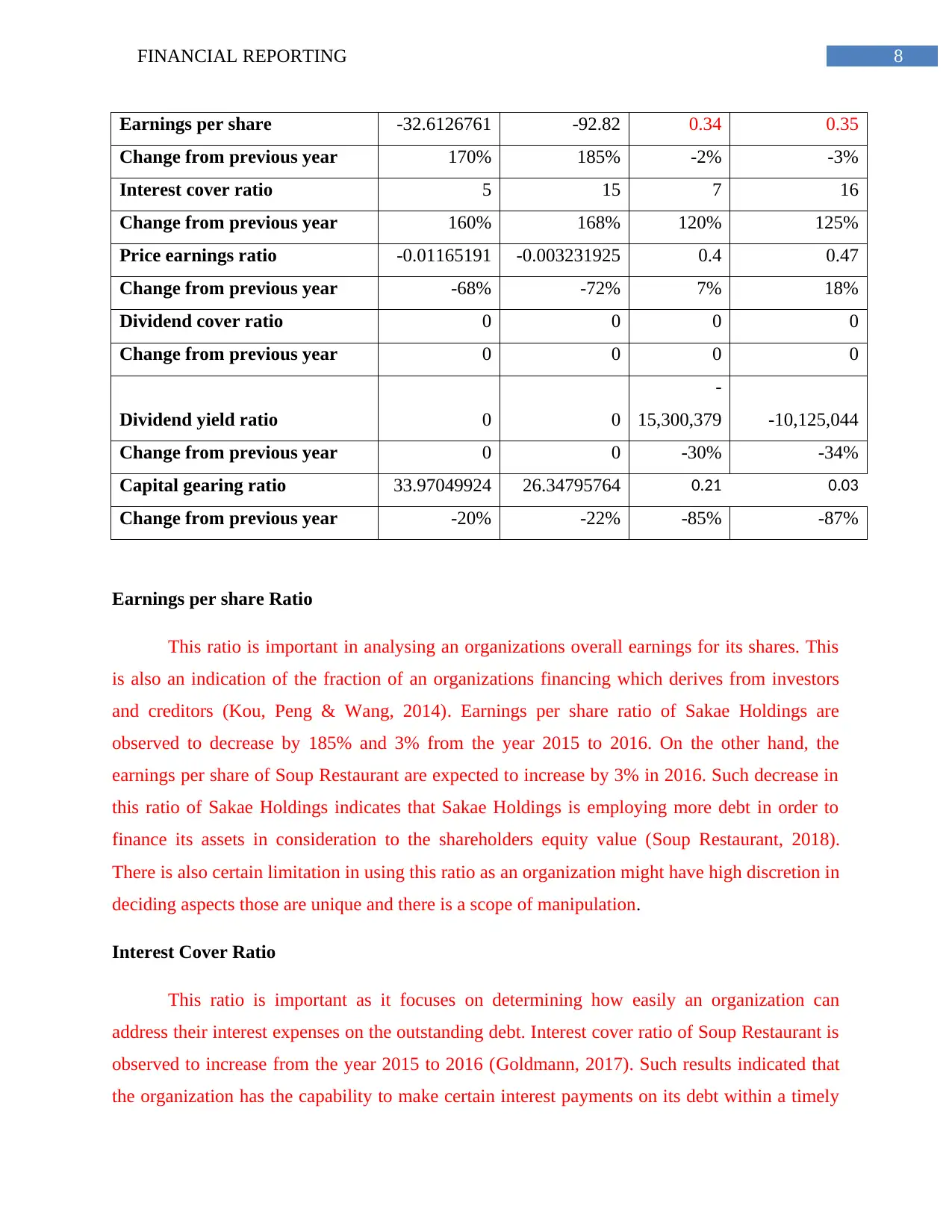

Earnings per share -32.6126761 -92.82 0.34 0.35

Change from previous year 170% 185% -2% -3%

Interest cover ratio 5 15 7 16

Change from previous year 160% 168% 120% 125%

Price earnings ratio -0.01165191 -0.003231925 0.4 0.47

Change from previous year -68% -72% 7% 18%

Dividend cover ratio 0 0 0 0

Change from previous year 0 0 0 0

Dividend yield ratio 0 0

-

15,300,379 -10,125,044

Change from previous year 0 0 -30% -34%

Capital gearing ratio 33.97049924 26.34795764 0.21 0.03

Change from previous year -20% -22% -85% -87%

Earnings per share Ratio

This ratio is important in analysing an organizations overall earnings for its shares. This

is also an indication of the fraction of an organizations financing which derives from investors

and creditors (Kou, Peng & Wang, 2014). Earnings per share ratio of Sakae Holdings are

observed to decrease by 185% and 3% from the year 2015 to 2016. On the other hand, the

earnings per share of Soup Restaurant are expected to increase by 3% in 2016. Such decrease in

this ratio of Sakae Holdings indicates that Sakae Holdings is employing more debt in order to

finance its assets in consideration to the shareholders equity value (Soup Restaurant, 2018).

There is also certain limitation in using this ratio as an organization might have high discretion in

deciding aspects those are unique and there is a scope of manipulation.

Interest Cover Ratio

This ratio is important as it focuses on determining how easily an organization can

address their interest expenses on the outstanding debt. Interest cover ratio of Soup Restaurant is

observed to increase from the year 2015 to 2016 (Goldmann, 2017). Such results indicated that

the organization has the capability to make certain interest payments on its debt within a timely

Earnings per share -32.6126761 -92.82 0.34 0.35

Change from previous year 170% 185% -2% -3%

Interest cover ratio 5 15 7 16

Change from previous year 160% 168% 120% 125%

Price earnings ratio -0.01165191 -0.003231925 0.4 0.47

Change from previous year -68% -72% 7% 18%

Dividend cover ratio 0 0 0 0

Change from previous year 0 0 0 0

Dividend yield ratio 0 0

-

15,300,379 -10,125,044

Change from previous year 0 0 -30% -34%

Capital gearing ratio 33.97049924 26.34795764 0.21 0.03

Change from previous year -20% -22% -85% -87%

Earnings per share Ratio

This ratio is important in analysing an organizations overall earnings for its shares. This

is also an indication of the fraction of an organizations financing which derives from investors

and creditors (Kou, Peng & Wang, 2014). Earnings per share ratio of Sakae Holdings are

observed to decrease by 185% and 3% from the year 2015 to 2016. On the other hand, the

earnings per share of Soup Restaurant are expected to increase by 3% in 2016. Such decrease in

this ratio of Sakae Holdings indicates that Sakae Holdings is employing more debt in order to

finance its assets in consideration to the shareholders equity value (Soup Restaurant, 2018).

There is also certain limitation in using this ratio as an organization might have high discretion in

deciding aspects those are unique and there is a scope of manipulation.

Interest Cover Ratio

This ratio is important as it focuses on determining how easily an organization can

address their interest expenses on the outstanding debt. Interest cover ratio of Soup Restaurant is

observed to increase from the year 2015 to 2016 (Goldmann, 2017). Such results indicated that

the organization has the capability to make certain interest payments on its debt within a timely

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9FINANCIAL REPORTING

manner. On the other hand, the ratio for Sakae Holdings has decreased in the same year denoting

its fall in capability to meet its interest expense with operating income. As this ratio is indicating

a increasing trend which makes sure that Soup is making enough money in addressing all its

interest payments. If this ratio keeps on increasing then it can be considered less risky that will

never attain a high bank financing (Grinblatt& Titman, 2016). However, there are certain

limitations of employing this ratio as this ratio at times fails to provide a clear picture of the

company’s stability with regards to defaults and certain interest payments. This ratio keeps on

fluctuating that questions the reliability of the results.

Price earnings ratio

Price earnings ratio has significance in evaluating the company’s increased growth in

future. Price earnings ratio of both Sakae Holdings and Soup Restaurant Company is observed to

decrease by 72% and 18% from the year 2015 to year 2016. As these companies are losing

money they are observed to have very less or no price earnings ratio. This indicates that for both

the companies the investors are not willing to pay an increased amount per dollar of its earnings

(Sakae Holdings, 2018). However, there are certain limitations of using this ratio as this employs

estimated earnings in order to attain high price earnings ratio.

Dividend cover ratio

Dividend cover ratio is vital in analysing the number of times a company is able to pay

dividends to all its shareholders that is gathered from profits earned within an accounting period.

Dividend cover ratio of both Sakae Holdings and Soup Restaurant Company is observed to be 0

from the year 2015 to year 2016. This indicates that both the companies are capable enough in

paying off all its necessary preferred dividend payments and it faces no difficulty in addressing

preferred dividend requirements (Sakae Holdings, 2018). Some limitations of using this ratio

includes proper estimation of deducting any dividends paid for the irredeemable preference

shares from the net profit gathered over the accounting period for estimating earnings to be

attained by ordinary shareholders.

Dividend yield ratio

manner. On the other hand, the ratio for Sakae Holdings has decreased in the same year denoting

its fall in capability to meet its interest expense with operating income. As this ratio is indicating

a increasing trend which makes sure that Soup is making enough money in addressing all its

interest payments. If this ratio keeps on increasing then it can be considered less risky that will

never attain a high bank financing (Grinblatt& Titman, 2016). However, there are certain

limitations of employing this ratio as this ratio at times fails to provide a clear picture of the

company’s stability with regards to defaults and certain interest payments. This ratio keeps on

fluctuating that questions the reliability of the results.

Price earnings ratio

Price earnings ratio has significance in evaluating the company’s increased growth in

future. Price earnings ratio of both Sakae Holdings and Soup Restaurant Company is observed to

decrease by 72% and 18% from the year 2015 to year 2016. As these companies are losing

money they are observed to have very less or no price earnings ratio. This indicates that for both

the companies the investors are not willing to pay an increased amount per dollar of its earnings

(Sakae Holdings, 2018). However, there are certain limitations of using this ratio as this employs

estimated earnings in order to attain high price earnings ratio.

Dividend cover ratio

Dividend cover ratio is vital in analysing the number of times a company is able to pay

dividends to all its shareholders that is gathered from profits earned within an accounting period.

Dividend cover ratio of both Sakae Holdings and Soup Restaurant Company is observed to be 0

from the year 2015 to year 2016. This indicates that both the companies are capable enough in

paying off all its necessary preferred dividend payments and it faces no difficulty in addressing

preferred dividend requirements (Sakae Holdings, 2018). Some limitations of using this ratio

includes proper estimation of deducting any dividends paid for the irredeemable preference

shares from the net profit gathered over the accounting period for estimating earnings to be

attained by ordinary shareholders.

Dividend yield ratio

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10FINANCIAL REPORTING

Dividend yield ratio is significant in analysing the basis on which the organizations pay

dividends on quarterly basis and evaluators the dividend paying capability of the organization.

Dividend yield ratio of both Sakae Holdings and is observed to be 0 and Soup Restaurant

Company is observed to decrease by 34% from the year 2015 to year 2016. This indicates that

both the companies do not pay a huge percentage of market prices of their shares to all its

shareholders in the dividend form (Soup Restaurant, 2018). However, there are certain

limitations of employing this ratio as it estimates that a company used for analysis continuously

prefer making dividend payments at the similar or increased rate like usual.

Capital gearing ratio

Capital gearing ratio is necessary in a company’s capital structure that includes the

fraction of equity and debt used by the company. Capital gearing ratio of both Sakae Holdings

and Soup Restaurant Company is observed to decrease by 22% and 87% from the year 2015 to

year 2016. This indicates that the capital structure of the company is not that low geared as a

decreased fraction of their capital is encompassed of common stockholders’ equity (Soup

Restaurant, 2018). Few drawbacks of employing thus ratio includes the complexity of this ratio

in understanding whether the organization is high or low geared along with the performance of

the organization in covering the interest payment with gathering a constant profit.

Conclusion

The objective of the paper is to conduct a comparative analysis of the selected companies

Sakae Holdings and Soup Restaurant that is listed in Singapore stock exchange. The report

revealed that profitability of Sakae Holdings Company is poor in comparison to Soup Restaurant.

Moreover, ratio analysis also explained that gearing ratios and asset efficiency ratios of Sakae

holdings is negative in comparison to Soup Restaurant that signifies the company needs

increased improvement in these ratios. For improvement of the profitability ratios, Sakae

Holdings Ltd is recommended to decrease its inventory, boost conversion rate and review its

recent pricing structure. However, the investors are recommended to invest in the shares of the

Soup Restaurant due to positive returns on investment, greater profit margin and higher dividend

payouts.

Dividend yield ratio is significant in analysing the basis on which the organizations pay

dividends on quarterly basis and evaluators the dividend paying capability of the organization.

Dividend yield ratio of both Sakae Holdings and is observed to be 0 and Soup Restaurant

Company is observed to decrease by 34% from the year 2015 to year 2016. This indicates that

both the companies do not pay a huge percentage of market prices of their shares to all its

shareholders in the dividend form (Soup Restaurant, 2018). However, there are certain

limitations of employing this ratio as it estimates that a company used for analysis continuously

prefer making dividend payments at the similar or increased rate like usual.

Capital gearing ratio

Capital gearing ratio is necessary in a company’s capital structure that includes the

fraction of equity and debt used by the company. Capital gearing ratio of both Sakae Holdings

and Soup Restaurant Company is observed to decrease by 22% and 87% from the year 2015 to

year 2016. This indicates that the capital structure of the company is not that low geared as a

decreased fraction of their capital is encompassed of common stockholders’ equity (Soup

Restaurant, 2018). Few drawbacks of employing thus ratio includes the complexity of this ratio

in understanding whether the organization is high or low geared along with the performance of

the organization in covering the interest payment with gathering a constant profit.

Conclusion

The objective of the paper is to conduct a comparative analysis of the selected companies

Sakae Holdings and Soup Restaurant that is listed in Singapore stock exchange. The report

revealed that profitability of Sakae Holdings Company is poor in comparison to Soup Restaurant.

Moreover, ratio analysis also explained that gearing ratios and asset efficiency ratios of Sakae

holdings is negative in comparison to Soup Restaurant that signifies the company needs

increased improvement in these ratios. For improvement of the profitability ratios, Sakae

Holdings Ltd is recommended to decrease its inventory, boost conversion rate and review its

recent pricing structure. However, the investors are recommended to invest in the shares of the

Soup Restaurant due to positive returns on investment, greater profit margin and higher dividend

payouts.

11FINANCIAL REPORTING

Part 2

Reflection

Through carrying out the comparative ratio analysis of the selected companies, I have

carried out comparative summary for two years regarding the selected companies profitability,

liquidity, asset efficiency and gearing will be provided within the report. Moreover, through

completing this paper I have learned that profitability ratios can be efficiently used in evaluating

the company’s performance along with operational efficiency. I have learned that these ratios

indicate the association among the profit along with resources used within the business. From

analysing the ratios of the selected companies I have learned that ratio analysis is an effective

process of determining along with analysing the numerical relationships relied on the financial

statements. I have also learned that ratio analysis serves as a statistical yardstick which offers a

measure of association among two figures and variables. After completion of the report, I have

attained a great understanding on the fact that ratio analysis provides decision makers with

increased information and facilities superior quality decision making. This also facilitates

directors, managers along with other interested members in deciding important figures such as

turnover and profit. After analysing the ratios of the selected companies, I have gathered

knowledge regarding the fact that liquidity serves as a measure of a company’s capability to

address daily expenditure. I have also gathered an understanding regarding the fact that the

companies require holding liquid assets in order to make sure that it can address their financial

commitments to an extent as liquid assets has a tendency to gather low returns. I have also

gained knowledge on the fact that financial statement analysis must centre majorly on extracting

necessary information for a specific decision. Such information needed can take several forms

that encompass comparisons like comparing variations within similar item for same organization

over several years. This can facilitate in comparing changes for the similar items for the same

organization over several years for comparing major relationships within the identical year. I

have also realised that ratio analysis of the companies facilitates comparison of financial

performance of them along with facilitating calculation of different ratios for a broad variety of

purposes.

Part 2

Reflection

Through carrying out the comparative ratio analysis of the selected companies, I have

carried out comparative summary for two years regarding the selected companies profitability,

liquidity, asset efficiency and gearing will be provided within the report. Moreover, through

completing this paper I have learned that profitability ratios can be efficiently used in evaluating

the company’s performance along with operational efficiency. I have learned that these ratios

indicate the association among the profit along with resources used within the business. From

analysing the ratios of the selected companies I have learned that ratio analysis is an effective

process of determining along with analysing the numerical relationships relied on the financial

statements. I have also learned that ratio analysis serves as a statistical yardstick which offers a

measure of association among two figures and variables. After completion of the report, I have

attained a great understanding on the fact that ratio analysis provides decision makers with

increased information and facilities superior quality decision making. This also facilitates

directors, managers along with other interested members in deciding important figures such as

turnover and profit. After analysing the ratios of the selected companies, I have gathered

knowledge regarding the fact that liquidity serves as a measure of a company’s capability to

address daily expenditure. I have also gathered an understanding regarding the fact that the

companies require holding liquid assets in order to make sure that it can address their financial

commitments to an extent as liquid assets has a tendency to gather low returns. I have also

gained knowledge on the fact that financial statement analysis must centre majorly on extracting

necessary information for a specific decision. Such information needed can take several forms

that encompass comparisons like comparing variations within similar item for same organization

over several years. This can facilitate in comparing changes for the similar items for the same

organization over several years for comparing major relationships within the identical year. I

have also realised that ratio analysis of the companies facilitates comparison of financial

performance of them along with facilitating calculation of different ratios for a broad variety of

purposes.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.