Comparative Financial Performance Analysis: JB Hi-Fi vs. Harvey Norman

VerifiedAdded on 2021/05/30

|20

|4411

|73

Report

AI Summary

This report presents a comprehensive financial performance analysis of JB Hi-Fi Limited and Harvey Norman Limited, two prominent companies in the Australian retail industry. The analysis employs ratio analysis techniques to evaluate the companies' financial health for the years 2016 and 2017. The report is divided into key categories including short-term liquidity, long-term solvency, asset utilization, profitability, and market value ratios. A comparative analysis is conducted to highlight the strengths and weaknesses of each company, including the impact of debt-to-equity ratios, interest coverage, and profit margins. The findings provide valuable insights into the operational efficiency, financial leverage, and overall profitability of the two companies, culminating in recommendations for strategic improvements.

ANALYSIS OF FINANCIAL PERFORMANCE

JB Fi-Fi Limited and Harvey Norman Limited

1

JB Fi-Fi Limited and Harvey Norman Limited

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Introduction................................................................................................................................3

Ratio analysis of JB Hi-fi Limited.............................................................................................4

Short term financial ratios/ Liquidity ratios...........................................................................4

Long term solvency/ Financial leverage ratio........................................................................4

Asset utilization (efficiency or turnover ratios).....................................................................5

Profitability ratio....................................................................................................................6

Market value ratios.................................................................................................................7

Ratio analysis of Harvey Normal Limited.................................................................................8

Short term solvency (Liquidity ratios)...................................................................................8

Long term solvency (Financial Leverage ratios)...................................................................8

Profitability ratios...................................................................................................................9

Asset unitization Ratios........................................................................................................10

Market valuation......................................................................................................................10

Comparative analysis...............................................................................................................12

Recommendation......................................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

2

Introduction................................................................................................................................3

Ratio analysis of JB Hi-fi Limited.............................................................................................4

Short term financial ratios/ Liquidity ratios...........................................................................4

Long term solvency/ Financial leverage ratio........................................................................4

Asset utilization (efficiency or turnover ratios).....................................................................5

Profitability ratio....................................................................................................................6

Market value ratios.................................................................................................................7

Ratio analysis of Harvey Normal Limited.................................................................................8

Short term solvency (Liquidity ratios)...................................................................................8

Long term solvency (Financial Leverage ratios)...................................................................8

Profitability ratios...................................................................................................................9

Asset unitization Ratios........................................................................................................10

Market valuation......................................................................................................................10

Comparative analysis...............................................................................................................12

Recommendation......................................................................................................................14

Conclusion................................................................................................................................15

References................................................................................................................................16

2

Introduction

Performance valuation has become an important management technique used to evaluate past

performances and make strategies for growth and development. There are various techniques

that are used by management of a company for performance evaluation and one of the most

popular techniques is ratio analysis. Ratio analysis helps in establishing a meaningful

relationship between two or more financial figures which can be used to evaluate different

aspects of the business (Baños-Caballero et.al, 2014). Here ratio analysis of two companies

has been conducted to evaluate their preferences. In addition to individual performance

evaluation, the comparison is also made between ratios of these two companies. Companies

taken into consideration for such evaluation are Harvey Norman Limited and JB Hi-fi

Limited. Both of these companies are working in Australian retail industry. Australian retail

market is highly competitive that makes performance evaluation more vital for growth and

development. From a general overview, it can be said that Harvey Norman is a larger

company as compared to JB Hi-fi limited if the size of market capital and yearly revenue

generated is considered.

3

Performance valuation has become an important management technique used to evaluate past

performances and make strategies for growth and development. There are various techniques

that are used by management of a company for performance evaluation and one of the most

popular techniques is ratio analysis. Ratio analysis helps in establishing a meaningful

relationship between two or more financial figures which can be used to evaluate different

aspects of the business (Baños-Caballero et.al, 2014). Here ratio analysis of two companies

has been conducted to evaluate their preferences. In addition to individual performance

evaluation, the comparison is also made between ratios of these two companies. Companies

taken into consideration for such evaluation are Harvey Norman Limited and JB Hi-fi

Limited. Both of these companies are working in Australian retail industry. Australian retail

market is highly competitive that makes performance evaluation more vital for growth and

development. From a general overview, it can be said that Harvey Norman is a larger

company as compared to JB Hi-fi limited if the size of market capital and yearly revenue

generated is considered.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

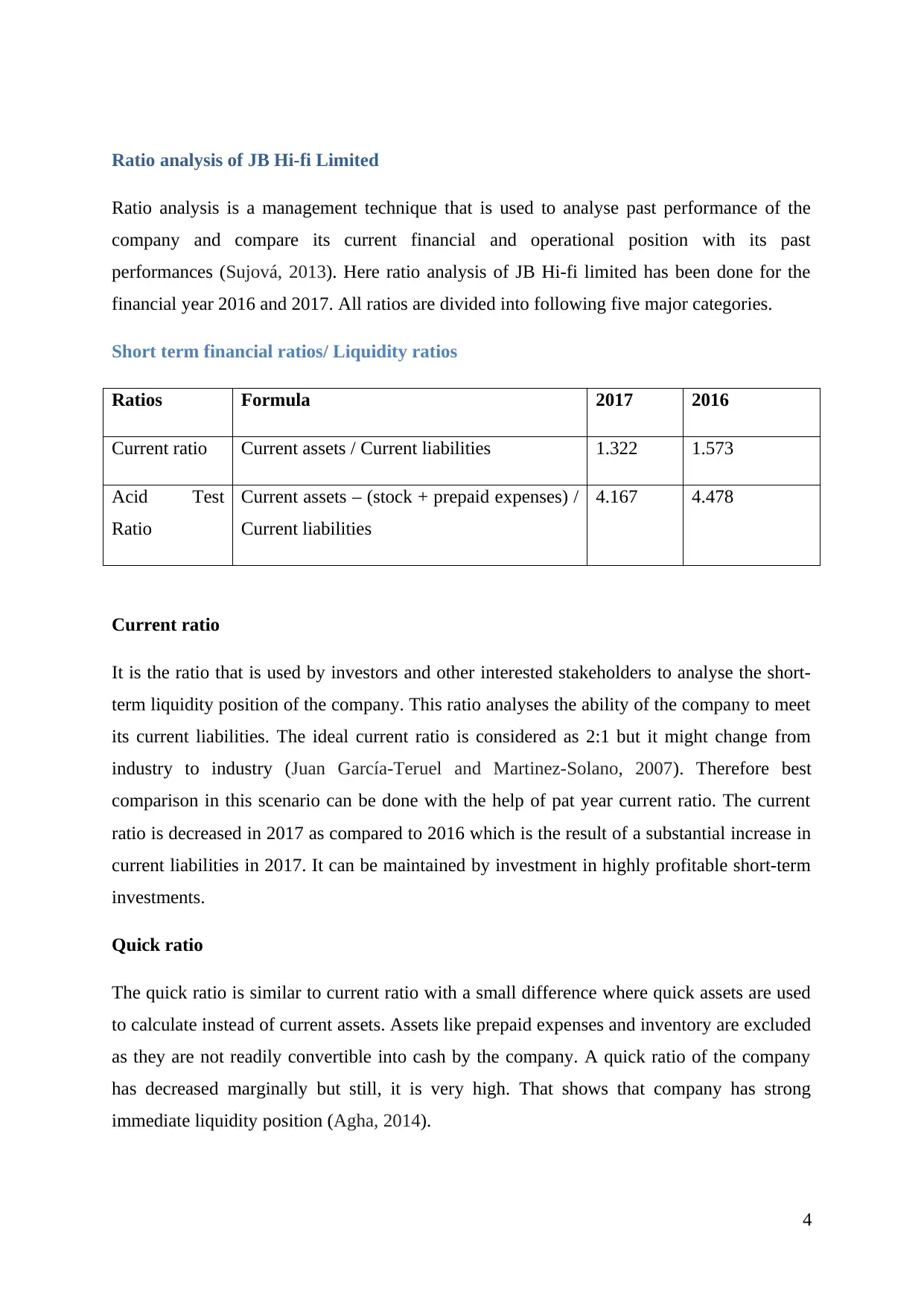

Ratio analysis of JB Hi-fi Limited

Ratio analysis is a management technique that is used to analyse past performance of the

company and compare its current financial and operational position with its past

performances (Sujová, 2013). Here ratio analysis of JB Hi-fi limited has been done for the

financial year 2016 and 2017. All ratios are divided into following five major categories.

Short term financial ratios/ Liquidity ratios

Ratios Formula 2017 2016

Current ratio Current assets / Current liabilities 1.322 1.573

Acid Test

Ratio

Current assets – (stock + prepaid expenses) /

Current liabilities

4.167 4.478

Current ratio

It is the ratio that is used by investors and other interested stakeholders to analyse the short-

term liquidity position of the company. This ratio analyses the ability of the company to meet

its current liabilities. The ideal current ratio is considered as 2:1 but it might change from

industry to industry (Juan García-Teruel and Martinez-Solano, 2007). Therefore best

comparison in this scenario can be done with the help of pat year current ratio. The current

ratio is decreased in 2017 as compared to 2016 which is the result of a substantial increase in

current liabilities in 2017. It can be maintained by investment in highly profitable short-term

investments.

Quick ratio

The quick ratio is similar to current ratio with a small difference where quick assets are used

to calculate instead of current assets. Assets like prepaid expenses and inventory are excluded

as they are not readily convertible into cash by the company. A quick ratio of the company

has decreased marginally but still, it is very high. That shows that company has strong

immediate liquidity position (Agha, 2014).

4

Ratio analysis is a management technique that is used to analyse past performance of the

company and compare its current financial and operational position with its past

performances (Sujová, 2013). Here ratio analysis of JB Hi-fi limited has been done for the

financial year 2016 and 2017. All ratios are divided into following five major categories.

Short term financial ratios/ Liquidity ratios

Ratios Formula 2017 2016

Current ratio Current assets / Current liabilities 1.322 1.573

Acid Test

Ratio

Current assets – (stock + prepaid expenses) /

Current liabilities

4.167 4.478

Current ratio

It is the ratio that is used by investors and other interested stakeholders to analyse the short-

term liquidity position of the company. This ratio analyses the ability of the company to meet

its current liabilities. The ideal current ratio is considered as 2:1 but it might change from

industry to industry (Juan García-Teruel and Martinez-Solano, 2007). Therefore best

comparison in this scenario can be done with the help of pat year current ratio. The current

ratio is decreased in 2017 as compared to 2016 which is the result of a substantial increase in

current liabilities in 2017. It can be maintained by investment in highly profitable short-term

investments.

Quick ratio

The quick ratio is similar to current ratio with a small difference where quick assets are used

to calculate instead of current assets. Assets like prepaid expenses and inventory are excluded

as they are not readily convertible into cash by the company. A quick ratio of the company

has decreased marginally but still, it is very high. That shows that company has strong

immediate liquidity position (Agha, 2014).

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

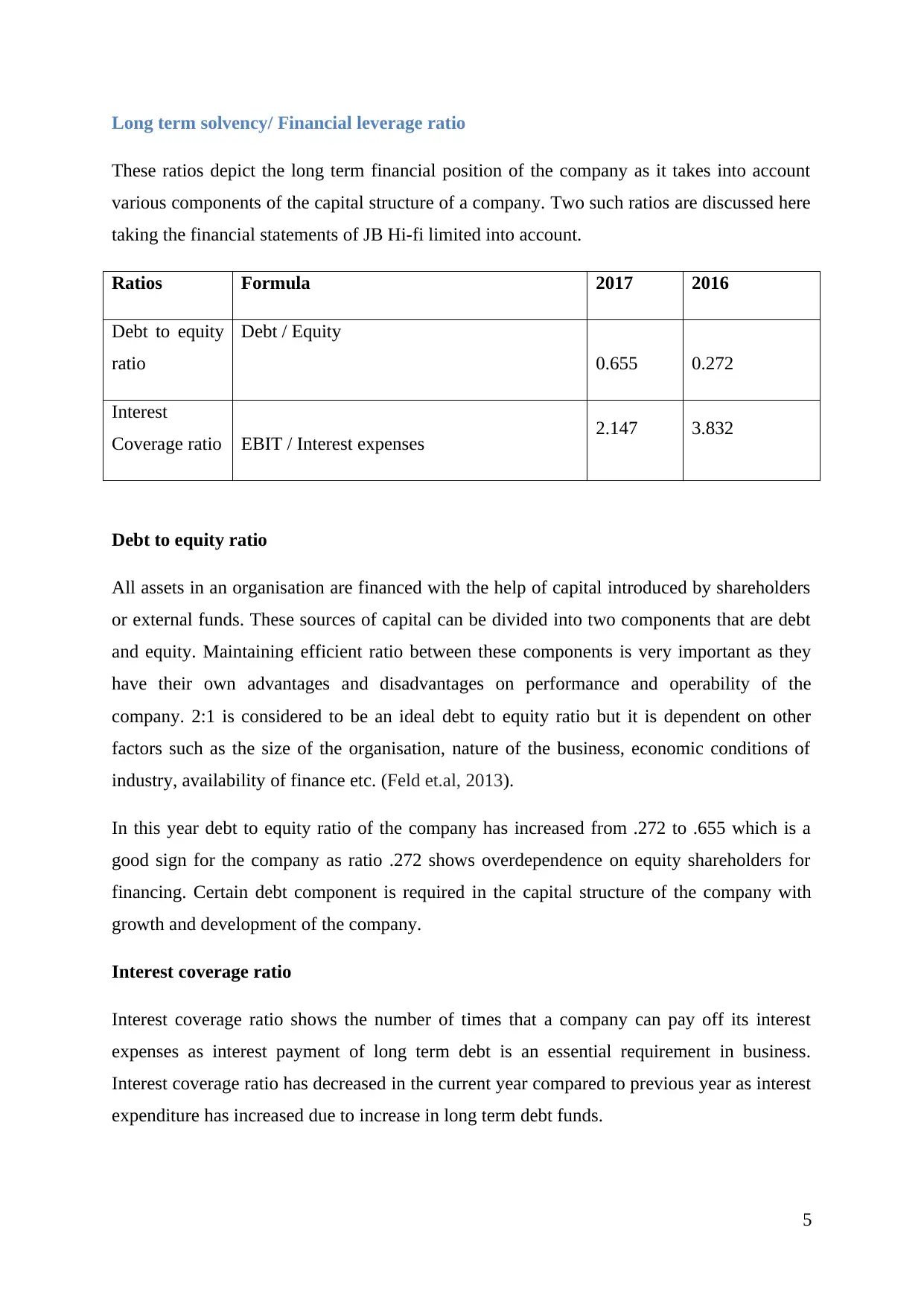

Long term solvency/ Financial leverage ratio

These ratios depict the long term financial position of the company as it takes into account

various components of the capital structure of a company. Two such ratios are discussed here

taking the financial statements of JB Hi-fi limited into account.

Ratios Formula 2017 2016

Debt to equity

ratio

Debt / Equity

0.655 0.272

Interest

Coverage ratio EBIT / Interest expenses 2.147 3.832

Debt to equity ratio

All assets in an organisation are financed with the help of capital introduced by shareholders

or external funds. These sources of capital can be divided into two components that are debt

and equity. Maintaining efficient ratio between these components is very important as they

have their own advantages and disadvantages on performance and operability of the

company. 2:1 is considered to be an ideal debt to equity ratio but it is dependent on other

factors such as the size of the organisation, nature of the business, economic conditions of

industry, availability of finance etc. (Feld et.al, 2013).

In this year debt to equity ratio of the company has increased from .272 to .655 which is a

good sign for the company as ratio .272 shows overdependence on equity shareholders for

financing. Certain debt component is required in the capital structure of the company with

growth and development of the company.

Interest coverage ratio

Interest coverage ratio shows the number of times that a company can pay off its interest

expenses as interest payment of long term debt is an essential requirement in business.

Interest coverage ratio has decreased in the current year compared to previous year as interest

expenditure has increased due to increase in long term debt funds.

5

These ratios depict the long term financial position of the company as it takes into account

various components of the capital structure of a company. Two such ratios are discussed here

taking the financial statements of JB Hi-fi limited into account.

Ratios Formula 2017 2016

Debt to equity

ratio

Debt / Equity

0.655 0.272

Interest

Coverage ratio EBIT / Interest expenses 2.147 3.832

Debt to equity ratio

All assets in an organisation are financed with the help of capital introduced by shareholders

or external funds. These sources of capital can be divided into two components that are debt

and equity. Maintaining efficient ratio between these components is very important as they

have their own advantages and disadvantages on performance and operability of the

company. 2:1 is considered to be an ideal debt to equity ratio but it is dependent on other

factors such as the size of the organisation, nature of the business, economic conditions of

industry, availability of finance etc. (Feld et.al, 2013).

In this year debt to equity ratio of the company has increased from .272 to .655 which is a

good sign for the company as ratio .272 shows overdependence on equity shareholders for

financing. Certain debt component is required in the capital structure of the company with

growth and development of the company.

Interest coverage ratio

Interest coverage ratio shows the number of times that a company can pay off its interest

expenses as interest payment of long term debt is an essential requirement in business.

Interest coverage ratio has decreased in the current year compared to previous year as interest

expenditure has increased due to increase in long term debt funds.

5

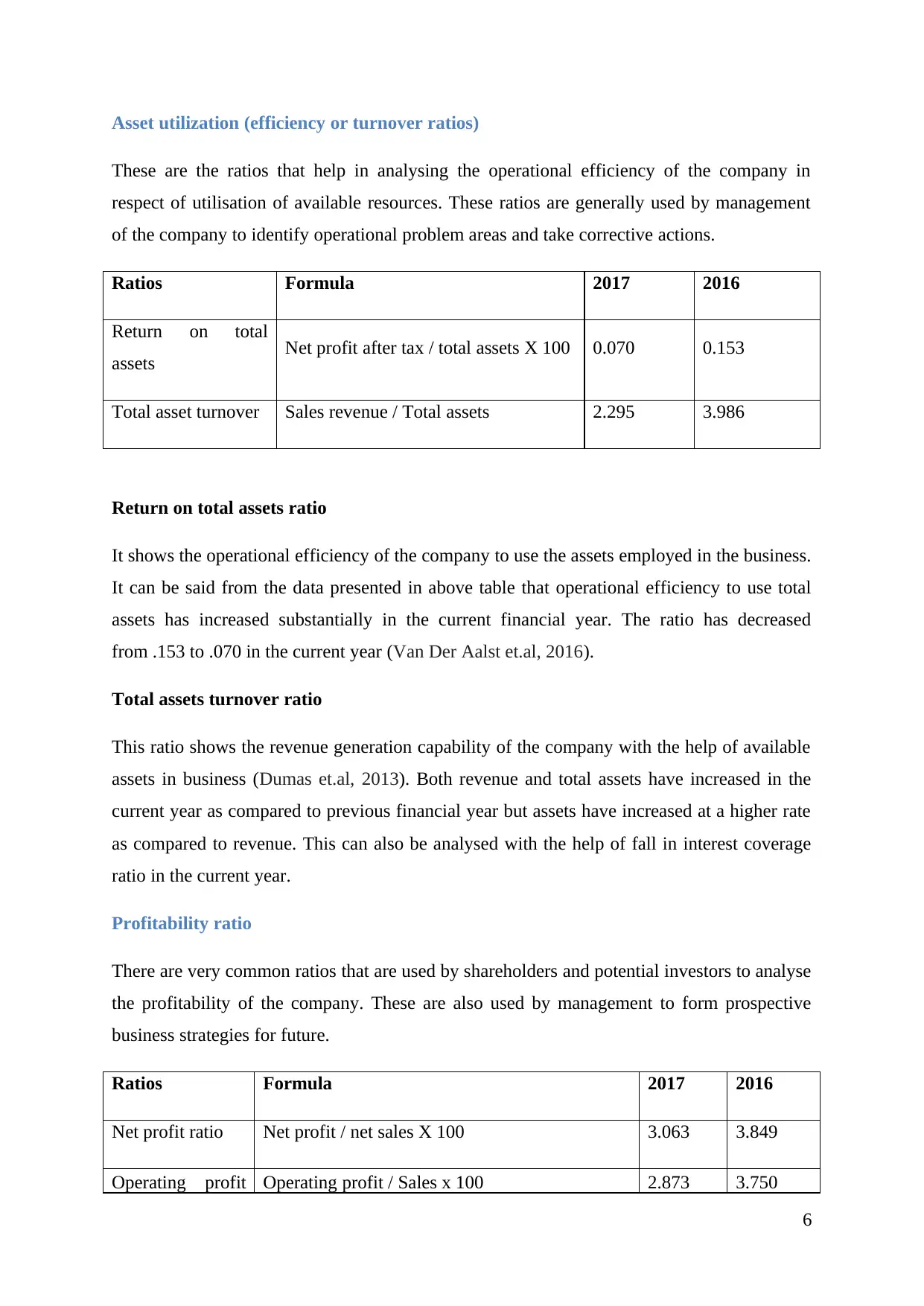

Asset utilization (efficiency or turnover ratios)

These are the ratios that help in analysing the operational efficiency of the company in

respect of utilisation of available resources. These ratios are generally used by management

of the company to identify operational problem areas and take corrective actions.

Ratios Formula 2017 2016

Return on total

assets Net profit after tax / total assets X 100 0.070 0.153

Total asset turnover Sales revenue / Total assets 2.295 3.986

Return on total assets ratio

It shows the operational efficiency of the company to use the assets employed in the business.

It can be said from the data presented in above table that operational efficiency to use total

assets has increased substantially in the current financial year. The ratio has decreased

from .153 to .070 in the current year (Van Der Aalst et.al, 2016).

Total assets turnover ratio

This ratio shows the revenue generation capability of the company with the help of available

assets in business (Dumas et.al, 2013). Both revenue and total assets have increased in the

current year as compared to previous financial year but assets have increased at a higher rate

as compared to revenue. This can also be analysed with the help of fall in interest coverage

ratio in the current year.

Profitability ratio

There are very common ratios that are used by shareholders and potential investors to analyse

the profitability of the company. These are also used by management to form prospective

business strategies for future.

Ratios Formula 2017 2016

Net profit ratio Net profit / net sales X 100 3.063 3.849

Operating profit Operating profit / Sales x 100 2.873 3.750

6

These are the ratios that help in analysing the operational efficiency of the company in

respect of utilisation of available resources. These ratios are generally used by management

of the company to identify operational problem areas and take corrective actions.

Ratios Formula 2017 2016

Return on total

assets Net profit after tax / total assets X 100 0.070 0.153

Total asset turnover Sales revenue / Total assets 2.295 3.986

Return on total assets ratio

It shows the operational efficiency of the company to use the assets employed in the business.

It can be said from the data presented in above table that operational efficiency to use total

assets has increased substantially in the current financial year. The ratio has decreased

from .153 to .070 in the current year (Van Der Aalst et.al, 2016).

Total assets turnover ratio

This ratio shows the revenue generation capability of the company with the help of available

assets in business (Dumas et.al, 2013). Both revenue and total assets have increased in the

current year as compared to previous financial year but assets have increased at a higher rate

as compared to revenue. This can also be analysed with the help of fall in interest coverage

ratio in the current year.

Profitability ratio

There are very common ratios that are used by shareholders and potential investors to analyse

the profitability of the company. These are also used by management to form prospective

business strategies for future.

Ratios Formula 2017 2016

Net profit ratio Net profit / net sales X 100 3.063 3.849

Operating profit Operating profit / Sales x 100 2.873 3.750

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

ratio

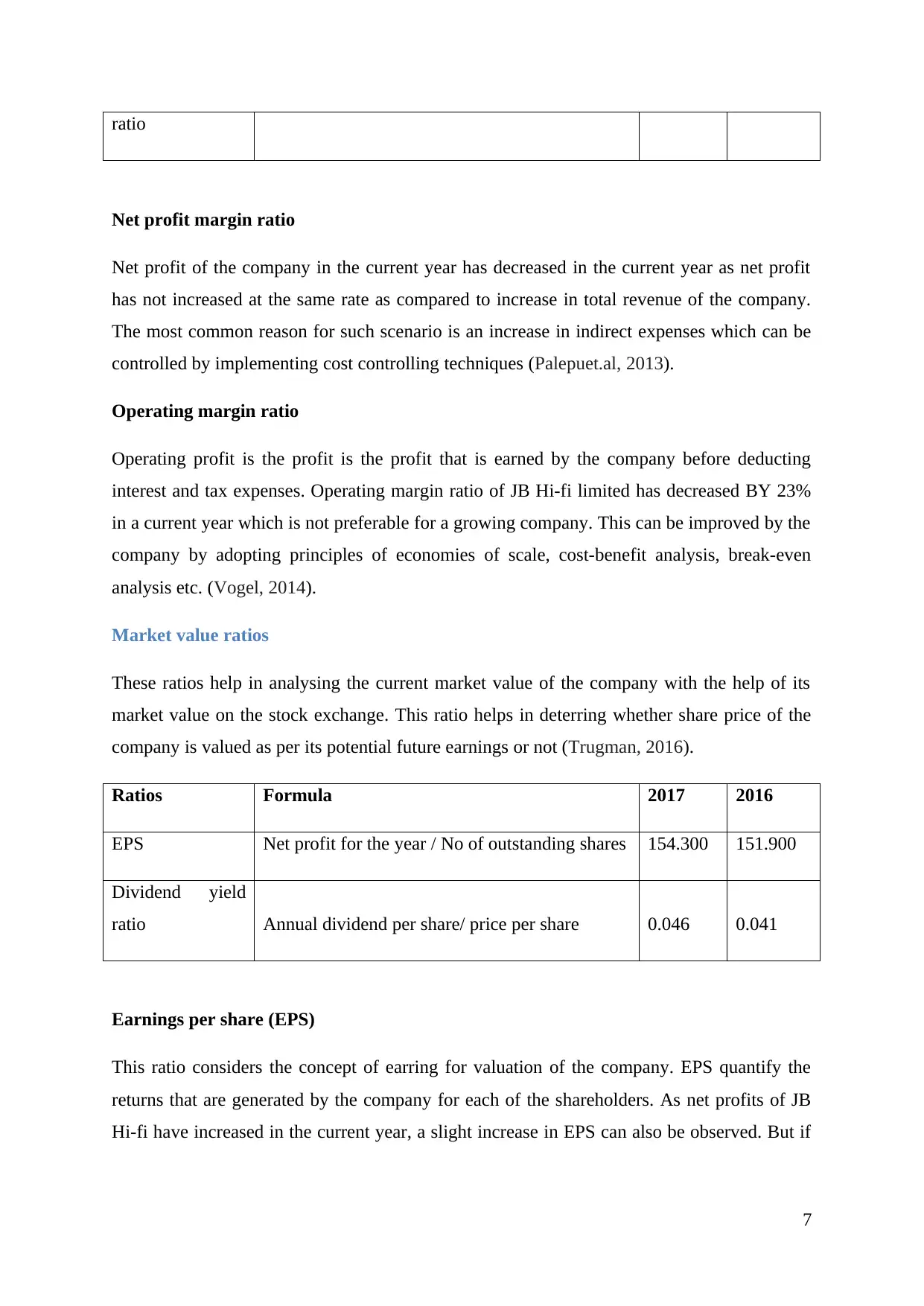

Net profit margin ratio

Net profit of the company in the current year has decreased in the current year as net profit

has not increased at the same rate as compared to increase in total revenue of the company.

The most common reason for such scenario is an increase in indirect expenses which can be

controlled by implementing cost controlling techniques (Palepuet.al, 2013).

Operating margin ratio

Operating profit is the profit is the profit that is earned by the company before deducting

interest and tax expenses. Operating margin ratio of JB Hi-fi limited has decreased BY 23%

in a current year which is not preferable for a growing company. This can be improved by the

company by adopting principles of economies of scale, cost-benefit analysis, break-even

analysis etc. (Vogel, 2014).

Market value ratios

These ratios help in analysing the current market value of the company with the help of its

market value on the stock exchange. This ratio helps in deterring whether share price of the

company is valued as per its potential future earnings or not (Trugman, 2016).

Ratios Formula 2017 2016

EPS Net profit for the year / No of outstanding shares 154.300 151.900

Dividend yield

ratio Annual dividend per share/ price per share 0.046 0.041

Earnings per share (EPS)

This ratio considers the concept of earring for valuation of the company. EPS quantify the

returns that are generated by the company for each of the shareholders. As net profits of JB

Hi-fi have increased in the current year, a slight increase in EPS can also be observed. But if

7

Net profit margin ratio

Net profit of the company in the current year has decreased in the current year as net profit

has not increased at the same rate as compared to increase in total revenue of the company.

The most common reason for such scenario is an increase in indirect expenses which can be

controlled by implementing cost controlling techniques (Palepuet.al, 2013).

Operating margin ratio

Operating profit is the profit is the profit that is earned by the company before deducting

interest and tax expenses. Operating margin ratio of JB Hi-fi limited has decreased BY 23%

in a current year which is not preferable for a growing company. This can be improved by the

company by adopting principles of economies of scale, cost-benefit analysis, break-even

analysis etc. (Vogel, 2014).

Market value ratios

These ratios help in analysing the current market value of the company with the help of its

market value on the stock exchange. This ratio helps in deterring whether share price of the

company is valued as per its potential future earnings or not (Trugman, 2016).

Ratios Formula 2017 2016

EPS Net profit for the year / No of outstanding shares 154.300 151.900

Dividend yield

ratio Annual dividend per share/ price per share 0.046 0.041

Earnings per share (EPS)

This ratio considers the concept of earring for valuation of the company. EPS quantify the

returns that are generated by the company for each of the shareholders. As net profits of JB

Hi-fi have increased in the current year, a slight increase in EPS can also be observed. But if

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

the increase in total assets and revenue is considered then it can be said that present increase

in EPS is not ideal.

Dividend yield ratio

It helps in depicting a relationship between dividend distributed by the company and its

market value. In simple words, dividend yield ratio shows the portion of the market value of

the company that is distributed in for of dividend (Bandurov, 2015). The dividend yield of the

company has increased in the current year as both dividend per share of the company and

market value of the company at the end of the financial year has increased.

8

in EPS is not ideal.

Dividend yield ratio

It helps in depicting a relationship between dividend distributed by the company and its

market value. In simple words, dividend yield ratio shows the portion of the market value of

the company that is distributed in for of dividend (Bandurov, 2015). The dividend yield of the

company has increased in the current year as both dividend per share of the company and

market value of the company at the end of the financial year has increased.

8

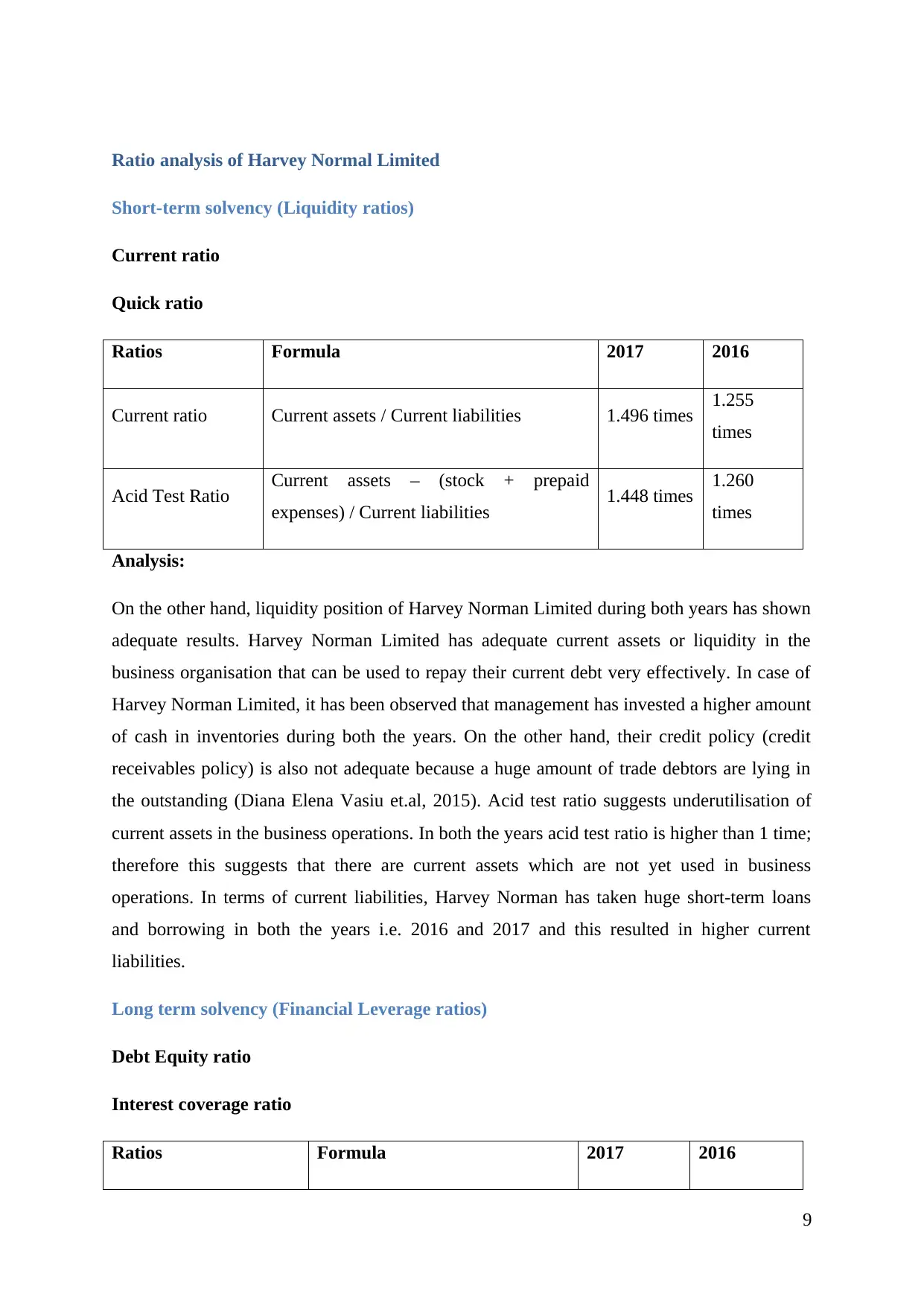

Ratio analysis of Harvey Normal Limited

Short-term solvency (Liquidity ratios)

Current ratio

Quick ratio

Ratios Formula 2017 2016

Current ratio Current assets / Current liabilities 1.496 times 1.255

times

Acid Test Ratio Current assets – (stock + prepaid

expenses) / Current liabilities 1.448 times 1.260

times

Analysis:

On the other hand, liquidity position of Harvey Norman Limited during both years has shown

adequate results. Harvey Norman Limited has adequate current assets or liquidity in the

business organisation that can be used to repay their current debt very effectively. In case of

Harvey Norman Limited, it has been observed that management has invested a higher amount

of cash in inventories during both the years. On the other hand, their credit policy (credit

receivables policy) is also not adequate because a huge amount of trade debtors are lying in

the outstanding (Diana Elena Vasiu et.al, 2015). Acid test ratio suggests underutilisation of

current assets in the business operations. In both the years acid test ratio is higher than 1 time;

therefore this suggests that there are current assets which are not yet used in business

operations. In terms of current liabilities, Harvey Norman has taken huge short-term loans

and borrowing in both the years i.e. 2016 and 2017 and this resulted in higher current

liabilities.

Long term solvency (Financial Leverage ratios)

Debt Equity ratio

Interest coverage ratio

Ratios Formula 2017 2016

9

Short-term solvency (Liquidity ratios)

Current ratio

Quick ratio

Ratios Formula 2017 2016

Current ratio Current assets / Current liabilities 1.496 times 1.255

times

Acid Test Ratio Current assets – (stock + prepaid

expenses) / Current liabilities 1.448 times 1.260

times

Analysis:

On the other hand, liquidity position of Harvey Norman Limited during both years has shown

adequate results. Harvey Norman Limited has adequate current assets or liquidity in the

business organisation that can be used to repay their current debt very effectively. In case of

Harvey Norman Limited, it has been observed that management has invested a higher amount

of cash in inventories during both the years. On the other hand, their credit policy (credit

receivables policy) is also not adequate because a huge amount of trade debtors are lying in

the outstanding (Diana Elena Vasiu et.al, 2015). Acid test ratio suggests underutilisation of

current assets in the business operations. In both the years acid test ratio is higher than 1 time;

therefore this suggests that there are current assets which are not yet used in business

operations. In terms of current liabilities, Harvey Norman has taken huge short-term loans

and borrowing in both the years i.e. 2016 and 2017 and this resulted in higher current

liabilities.

Long term solvency (Financial Leverage ratios)

Debt Equity ratio

Interest coverage ratio

Ratios Formula 2017 2016

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

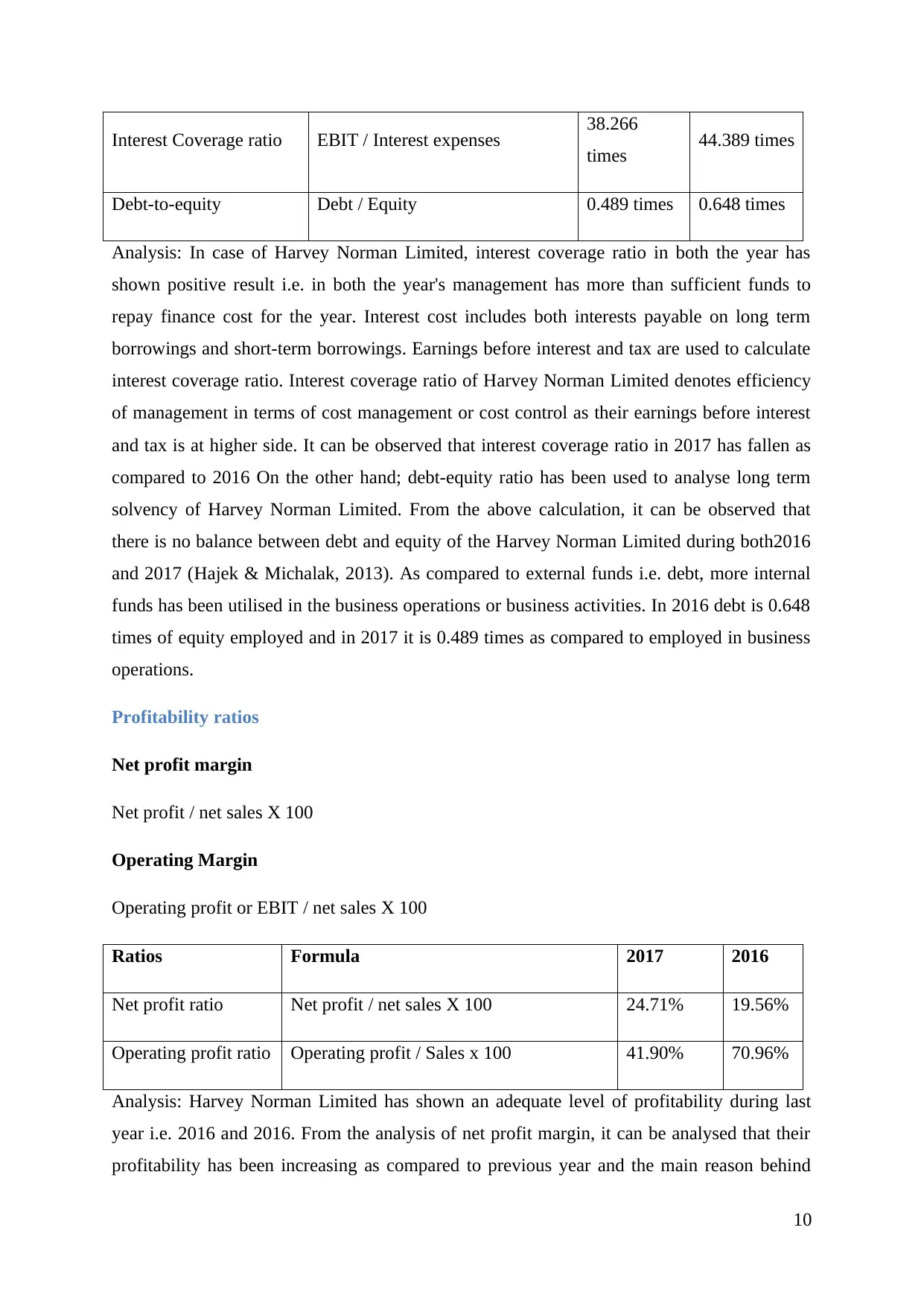

Interest Coverage ratio EBIT / Interest expenses 38.266

times 44.389 times

Debt-to-equity Debt / Equity 0.489 times 0.648 times

Analysis: In case of Harvey Norman Limited, interest coverage ratio in both the year has

shown positive result i.e. in both the year's management has more than sufficient funds to

repay finance cost for the year. Interest cost includes both interests payable on long term

borrowings and short-term borrowings. Earnings before interest and tax are used to calculate

interest coverage ratio. Interest coverage ratio of Harvey Norman Limited denotes efficiency

of management in terms of cost management or cost control as their earnings before interest

and tax is at higher side. It can be observed that interest coverage ratio in 2017 has fallen as

compared to 2016 On the other hand; debt-equity ratio has been used to analyse long term

solvency of Harvey Norman Limited. From the above calculation, it can be observed that

there is no balance between debt and equity of the Harvey Norman Limited during both2016

and 2017 (Hajek & Michalak, 2013). As compared to external funds i.e. debt, more internal

funds has been utilised in the business operations or business activities. In 2016 debt is 0.648

times of equity employed and in 2017 it is 0.489 times as compared to employed in business

operations.

Profitability ratios

Net profit margin

Net profit / net sales X 100

Operating Margin

Operating profit or EBIT / net sales X 100

Ratios Formula 2017 2016

Net profit ratio Net profit / net sales X 100 24.71% 19.56%

Operating profit ratio Operating profit / Sales x 100 41.90% 70.96%

Analysis: Harvey Norman Limited has shown an adequate level of profitability during last

year i.e. 2016 and 2016. From the analysis of net profit margin, it can be analysed that their

profitability has been increasing as compared to previous year and the main reason behind

10

times 44.389 times

Debt-to-equity Debt / Equity 0.489 times 0.648 times

Analysis: In case of Harvey Norman Limited, interest coverage ratio in both the year has

shown positive result i.e. in both the year's management has more than sufficient funds to

repay finance cost for the year. Interest cost includes both interests payable on long term

borrowings and short-term borrowings. Earnings before interest and tax are used to calculate

interest coverage ratio. Interest coverage ratio of Harvey Norman Limited denotes efficiency

of management in terms of cost management or cost control as their earnings before interest

and tax is at higher side. It can be observed that interest coverage ratio in 2017 has fallen as

compared to 2016 On the other hand; debt-equity ratio has been used to analyse long term

solvency of Harvey Norman Limited. From the above calculation, it can be observed that

there is no balance between debt and equity of the Harvey Norman Limited during both2016

and 2017 (Hajek & Michalak, 2013). As compared to external funds i.e. debt, more internal

funds has been utilised in the business operations or business activities. In 2016 debt is 0.648

times of equity employed and in 2017 it is 0.489 times as compared to employed in business

operations.

Profitability ratios

Net profit margin

Net profit / net sales X 100

Operating Margin

Operating profit or EBIT / net sales X 100

Ratios Formula 2017 2016

Net profit ratio Net profit / net sales X 100 24.71% 19.56%

Operating profit ratio Operating profit / Sales x 100 41.90% 70.96%

Analysis: Harvey Norman Limited has shown an adequate level of profitability during last

year i.e. 2016 and 2016. From the analysis of net profit margin, it can be analysed that their

profitability has been increasing as compared to previous year and the main reason behind

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

this are increases swales level and moderate cost of sales level. As compared to industry

standards, Harvey Norman Limited has generated a moderate level of net profit during both

the years. On the other hand, operating profit of Harvey Norman Limited has shown most

favourable results in both the years (Merwe Oberholzer, 2012). In 2016 operating profit

margin of Harvey Norman Limited is 70.96 % which is very attractive for any investor or any

stakeholder. It has been observed that operating profit margin has been declined in 2017 and

the main reason behind this is an increase in expenses as compared to increase sales revenue.

That means sales revenue is increased with less, no and operating expenses has been

increased with higher margins (Hofmann & Lampe, 2013).

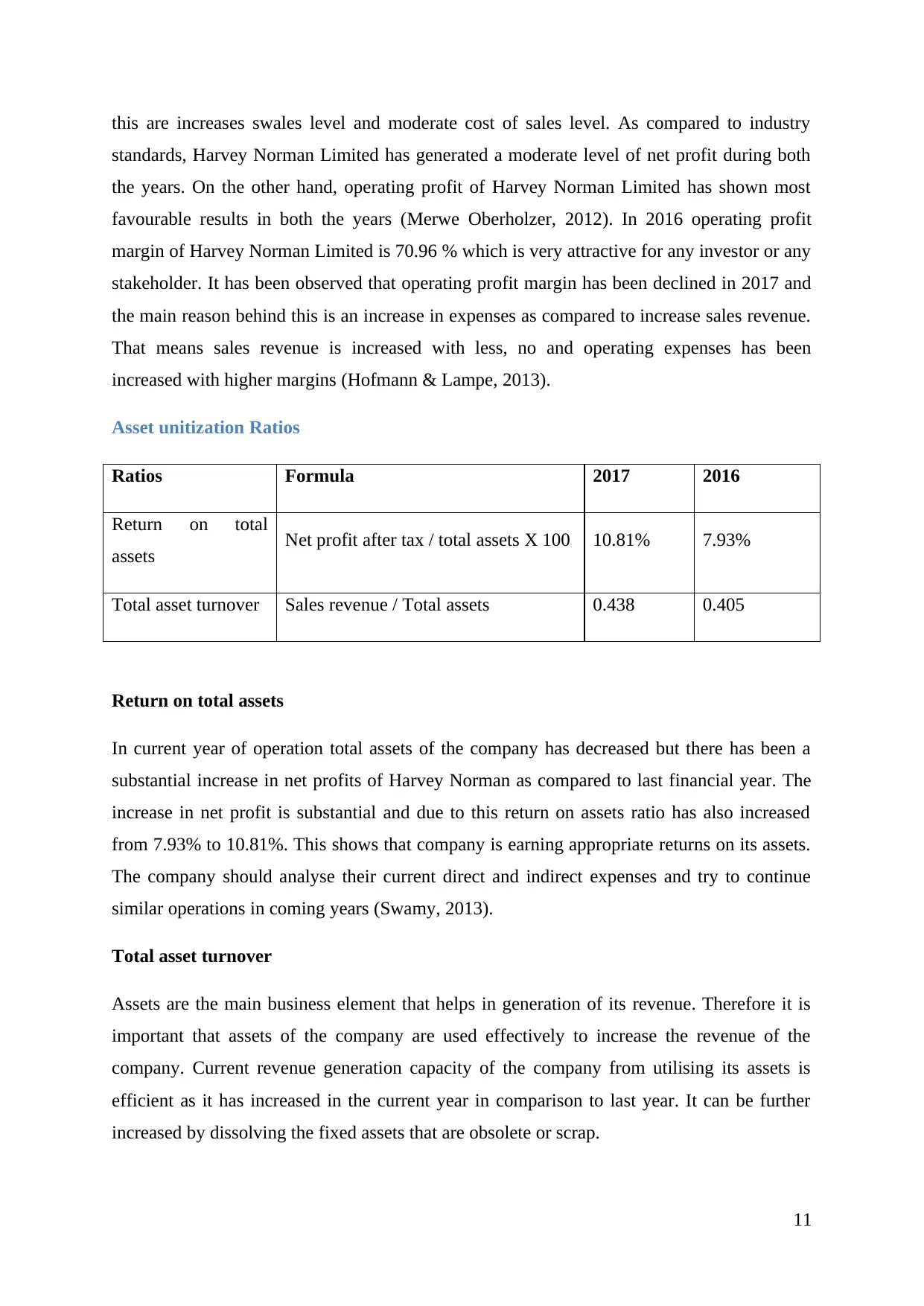

Asset unitization Ratios

Ratios Formula 2017 2016

Return on total

assets Net profit after tax / total assets X 100 10.81% 7.93%

Total asset turnover Sales revenue / Total assets 0.438 0.405

Return on total assets

In current year of operation total assets of the company has decreased but there has been a

substantial increase in net profits of Harvey Norman as compared to last financial year. The

increase in net profit is substantial and due to this return on assets ratio has also increased

from 7.93% to 10.81%. This shows that company is earning appropriate returns on its assets.

The company should analyse their current direct and indirect expenses and try to continue

similar operations in coming years (Swamy, 2013).

Total asset turnover

Assets are the main business element that helps in generation of its revenue. Therefore it is

important that assets of the company are used effectively to increase the revenue of the

company. Current revenue generation capacity of the company from utilising its assets is

efficient as it has increased in the current year in comparison to last year. It can be further

increased by dissolving the fixed assets that are obsolete or scrap.

11

standards, Harvey Norman Limited has generated a moderate level of net profit during both

the years. On the other hand, operating profit of Harvey Norman Limited has shown most

favourable results in both the years (Merwe Oberholzer, 2012). In 2016 operating profit

margin of Harvey Norman Limited is 70.96 % which is very attractive for any investor or any

stakeholder. It has been observed that operating profit margin has been declined in 2017 and

the main reason behind this is an increase in expenses as compared to increase sales revenue.

That means sales revenue is increased with less, no and operating expenses has been

increased with higher margins (Hofmann & Lampe, 2013).

Asset unitization Ratios

Ratios Formula 2017 2016

Return on total

assets Net profit after tax / total assets X 100 10.81% 7.93%

Total asset turnover Sales revenue / Total assets 0.438 0.405

Return on total assets

In current year of operation total assets of the company has decreased but there has been a

substantial increase in net profits of Harvey Norman as compared to last financial year. The

increase in net profit is substantial and due to this return on assets ratio has also increased

from 7.93% to 10.81%. This shows that company is earning appropriate returns on its assets.

The company should analyse their current direct and indirect expenses and try to continue

similar operations in coming years (Swamy, 2013).

Total asset turnover

Assets are the main business element that helps in generation of its revenue. Therefore it is

important that assets of the company are used effectively to increase the revenue of the

company. Current revenue generation capacity of the company from utilising its assets is

efficient as it has increased in the current year in comparison to last year. It can be further

increased by dissolving the fixed assets that are obsolete or scrap.

11

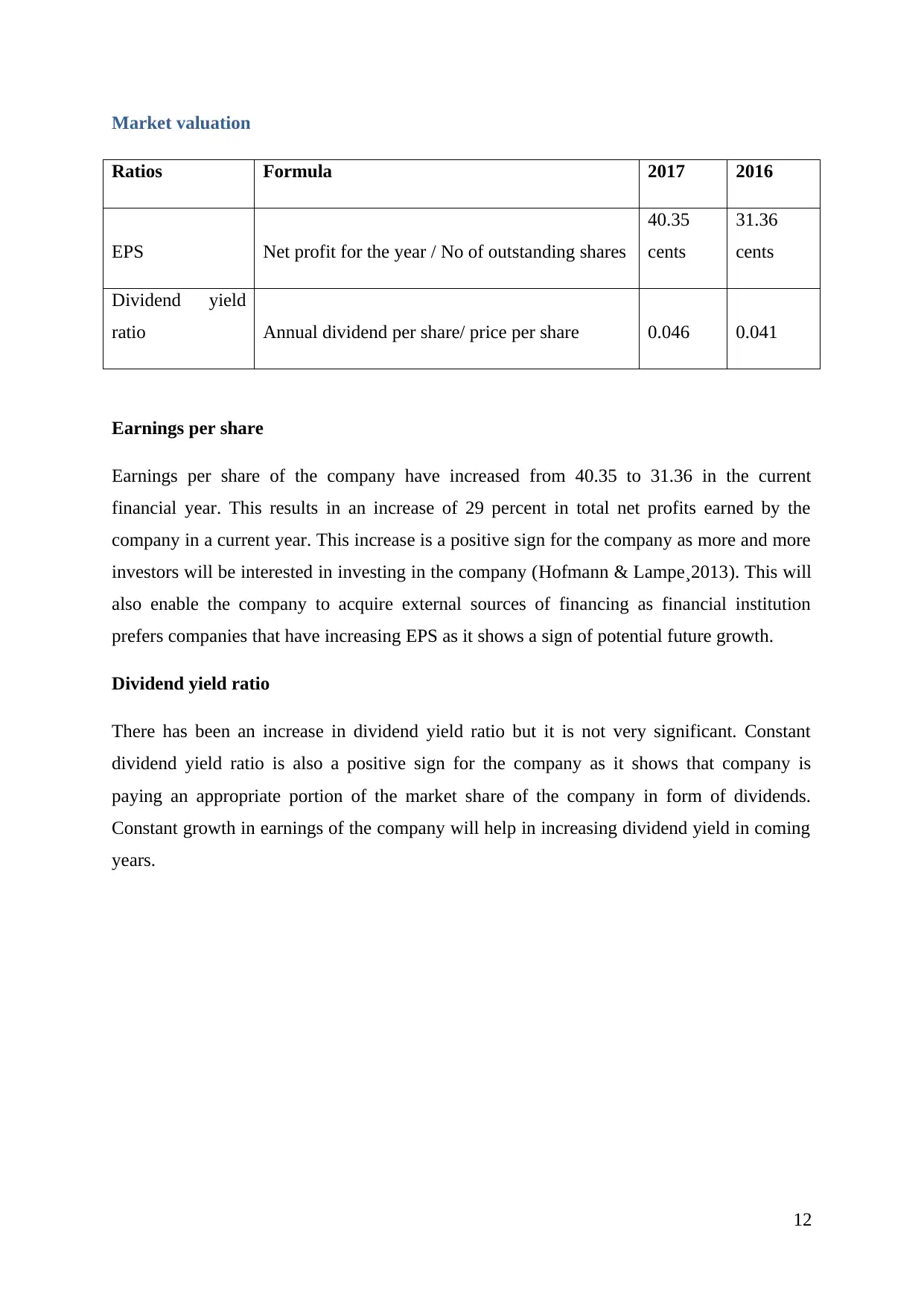

Market valuation

Ratios Formula 2017 2016

EPS Net profit for the year / No of outstanding shares

40.35

cents

31.36

cents

Dividend yield

ratio Annual dividend per share/ price per share 0.046 0.041

Earnings per share

Earnings per share of the company have increased from 40.35 to 31.36 in the current

financial year. This results in an increase of 29 percent in total net profits earned by the

company in a current year. This increase is a positive sign for the company as more and more

investors will be interested in investing in the company (Hofmann & Lampe¸2013). This will

also enable the company to acquire external sources of financing as financial institution

prefers companies that have increasing EPS as it shows a sign of potential future growth.

Dividend yield ratio

There has been an increase in dividend yield ratio but it is not very significant. Constant

dividend yield ratio is also a positive sign for the company as it shows that company is

paying an appropriate portion of the market share of the company in form of dividends.

Constant growth in earnings of the company will help in increasing dividend yield in coming

years.

12

Ratios Formula 2017 2016

EPS Net profit for the year / No of outstanding shares

40.35

cents

31.36

cents

Dividend yield

ratio Annual dividend per share/ price per share 0.046 0.041

Earnings per share

Earnings per share of the company have increased from 40.35 to 31.36 in the current

financial year. This results in an increase of 29 percent in total net profits earned by the

company in a current year. This increase is a positive sign for the company as more and more

investors will be interested in investing in the company (Hofmann & Lampe¸2013). This will

also enable the company to acquire external sources of financing as financial institution

prefers companies that have increasing EPS as it shows a sign of potential future growth.

Dividend yield ratio

There has been an increase in dividend yield ratio but it is not very significant. Constant

dividend yield ratio is also a positive sign for the company as it shows that company is

paying an appropriate portion of the market share of the company in form of dividends.

Constant growth in earnings of the company will help in increasing dividend yield in coming

years.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.